Sample Category Title

Summary 3/17 – 3/21

Monday, Mar 17, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Feb | 50.4 | |

| 00:01 | GBP | Rightmove House Price Index M/M Mar | 0.50% | |

| 02:00 | CNY | Industrial Production Y/Y Feb | 5.30% | 6.20% |

| 02:00 | CNY | Retail Sales Y/Y Feb | 3.80% | 3.70% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Feb | 3.20% | 3.20% |

| 12:15 | CAD | Housing Starts Y/Y Feb | 249K | 240K |

| 12:30 | USD | Empire State Manufacturing Index Mar | -1.9 | 5.7 |

| 12:30 | USD | Retail Sales M/M Feb | 0.70% | -0.90% |

| 12:30 | USD | Retail Sales ex Autos M/M Feb | 0.50% | -0.40% |

| 14:00 | USD | NAHB Housing Market Index Mar | 43 | 42 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Feb | |

| Forecast: | Previous: 50.4 | ||

| 00:01 | GBP | Rightmove House Price Index M/M Mar | |

| Forecast: | Previous: 0.50% | ||

| 02:00 | CNY | Industrial Production Y/Y Feb | |

| Forecast: 5.30% | Previous: 6.20% | ||

| 02:00 | CNY | Retail Sales Y/Y Feb | |

| Forecast: 3.80% | Previous: 3.70% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Feb | |

| Forecast: 3.20% | Previous: 3.20% | ||

| 12:15 | CAD | Housing Starts Y/Y Feb | |

| Forecast: 249K | Previous: 240K | ||

| 12:30 | USD | Empire State Manufacturing Index Mar | |

| Forecast: -1.9 | Previous: 5.7 | ||

| 12:30 | USD | Retail Sales M/M Feb | |

| Forecast: 0.70% | Previous: -0.90% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Feb | |

| Forecast: 0.50% | Previous: -0.40% | ||

| 14:00 | USD | NAHB Housing Market Index Mar | |

| Forecast: 43 | Previous: 42 | ||

Tuesday, Mar 18, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jan | -0.10% | 0.10% |

| 08:00 | CHF | SECO Economic Forecasts | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 14.1B | 14.6B |

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 35 | 26 |

| 10:00 | EUR | Germany ZEW Current Situation Mar | -88.5 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 39.6 | 24.2 |

| 12:30 | CAD | CPI M/M Feb | 0.60% | 0.10% |

| 12:30 | CAD | CPI Y/Y Feb | 2.10% | 1.90% |

| 12:30 | CAD | CPI Median Y/Y Feb | 2.70% | |

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 2.70% | |

| 12:30 | CAD | CPI Common Y/Y Feb | 2.20% | |

| 12:30 | USD | Building Permits Feb | 1.45M | 1.47M |

| 12:30 | USD | Housing Starts Feb | 1.38M | 1.37M |

| 12:30 | USD | Import Price Index M/M Feb | -0.10% | 0.30% |

| 13:15 | USD | Industrial Production M/M Feb | 0.20% | 0.50% |

| 13:15 | USD | Capacity Utilization Feb | 77.80% | 77.80% |

| 20:00 | NZD | Westpac Consumer Survey Q1 | 97.5 | |

| 21:45 | NZD | Current Account (NZD) Q4 | -6.64B | -10.58B |

| 23:50 | JPY | Trade Balance (JPY) Feb | 0.51T | -0.86T |

| 23:30 | AUD | Westpac Leading Index M/M Feb | 0.13% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jan | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 08:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | |

| Forecast: 14.1B | Previous: 14.6B | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | |

| Forecast: 35 | Previous: 26 | ||

| 10:00 | EUR | Germany ZEW Current Situation Mar | |

| Forecast: | Previous: -88.5 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | |

| Forecast: 39.6 | Previous: 24.2 | ||

| 12:30 | CAD | CPI M/M Feb | |

| Forecast: 0.60% | Previous: 0.10% | ||

| 12:30 | CAD | CPI Y/Y Feb | |

| Forecast: 2.10% | Previous: 1.90% | ||

| 12:30 | CAD | CPI Median Y/Y Feb | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Feb | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | CAD | CPI Common Y/Y Feb | |

| Forecast: | Previous: 2.20% | ||

| 12:30 | USD | Building Permits Feb | |

| Forecast: 1.45M | Previous: 1.47M | ||

| 12:30 | USD | Housing Starts Feb | |

| Forecast: 1.38M | Previous: 1.37M | ||

| 12:30 | USD | Import Price Index M/M Feb | |

| Forecast: -0.10% | Previous: 0.30% | ||

| 13:15 | USD | Industrial Production M/M Feb | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 13:15 | USD | Capacity Utilization Feb | |

| Forecast: 77.80% | Previous: 77.80% | ||

| 20:00 | NZD | Westpac Consumer Survey Q1 | |

| Forecast: | Previous: 97.5 | ||

| 21:45 | NZD | Current Account (NZD) Q4 | |

| Forecast: -6.64B | Previous: -10.58B | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | |

| Forecast: 0.51T | Previous: -0.86T | ||

| 23:30 | AUD | Westpac Leading Index M/M Feb | |

| Forecast: | Previous: 0.13% | ||

Wednesday, Mar 19, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.50% | 0.50% | |

| 04:30 | JPY | Industrial Production M/M Jan F | -1.10% | -1.10% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 2.60% | 2.60% |

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 2.40% | 2.40% |

| 14:30 | USD | Crude Oil Inventories | 1.4M | |

| 18:00 | USD | Fed Interest Rate Decision | 4.50% | 4.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | GDP Q/Q Q4 | 0.40% | -1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.50% | Previous: 0.50% | ||

| 04:30 | JPY | Industrial Production M/M Jan F | |

| Forecast: -1.10% | Previous: -1.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.4M | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | GDP Q/Q Q4 | |

| Forecast: 0.40% | Previous: -1.00% | ||

Thursday, Mar 20, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Employment Change Feb | 30K | 44K |

| 00:30 | AUD | Unemployment Rate Feb | 4.10% | 4.10% |

| 01:00 | CNY | 1-Y Loan Prime Rate | 3.10% | 3.10% |

| 01:00 | CNY | 5-Y Loan Prime Rate | 3.60% | 3.60% |

| 07:00 | CHF | Trade Balance (CHF) Feb | 5.01B | 6.12B |

| 07:00 | EUR | GermanyPPI M/M Feb | 0.20% | -0.10% |

| 07:00 | EUR | GermanyPPI Y/Y Feb | 0.50% | |

| 07:00 | GBP | Claimant Count Change Feb | 7.9K | 22K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 4.50% | 4.40% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 5.90% | 6.00% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 5.90% | |

| 08:30 | CHF | SNB Interest Rate Decision | 0.25% | 0.50% |

| 09:00 | CHF | SNB Press Conference | ||

| 09:00 | EUR | ECB Economic Bulletin | ||

| 11:00 | GBP | BoE Interest Rate Decision | 4.50% | 4.50% |

| 12:30 | CAD | Industrial Product Price M/M Feb | 1.60% | |

| 12:30 | CAD | Raw Material Price Index M/M Feb | 3.70% | |

| 12:30 | USD | Current Account (USD) Q4 | -337B | -311B |

| 12:30 | USD | Initial Jobless Claims (Mar 14) | 222K | 220K |

| 12:30 | USD | Philadelphia Fed Survey Mar | 12.1 | 18.1 |

| 14:00 | USD | Existing Home Sales Feb | 3.92M | 4.08M |

| 14:30 | USD | Natural Gas Storage | -62B | |

| 21:45 | NZD | Trade Balance NZD M/M Feb | -235M | -486M |

| 23:50 | JPY | National CPI Y/Y Feb | 4% | |

| 23:50 | JPY | National CPI CoreY/Y Feb | 2.90% | 3.20% |

| 23:50 | JPY | National CPI Core-Core Y/Y Feb | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Employment Change Feb | |

| Forecast: 30K | Previous: 44K | ||

| 00:30 | AUD | Unemployment Rate Feb | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 01:00 | CNY | 1-Y Loan Prime Rate | |

| Forecast: 3.10% | Previous: 3.10% | ||

| 01:00 | CNY | 5-Y Loan Prime Rate | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 07:00 | CHF | Trade Balance (CHF) Feb | |

| Forecast: 5.01B | Previous: 6.12B | ||

| 07:00 | EUR | GermanyPPI M/M Feb | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 07:00 | EUR | GermanyPPI Y/Y Feb | |

| Forecast: | Previous: 0.50% | ||

| 07:00 | GBP | Claimant Count Change Feb | |

| Forecast: 7.9K | Previous: 22K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | |

| Forecast: 4.50% | Previous: 4.40% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | |

| Forecast: 5.90% | Previous: 6.00% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | |

| Forecast: | Previous: 5.90% | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 0.25% | Previous: 0.50% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | |

| Forecast: | Previous: 1.60% | ||

| 12:30 | CAD | Raw Material Price Index M/M Feb | |

| Forecast: | Previous: 3.70% | ||

| 12:30 | USD | Current Account (USD) Q4 | |

| Forecast: -337B | Previous: -311B | ||

| 12:30 | USD | Initial Jobless Claims (Mar 14) | |

| Forecast: 222K | Previous: 220K | ||

| 12:30 | USD | Philadelphia Fed Survey Mar | |

| Forecast: 12.1 | Previous: 18.1 | ||

| 14:00 | USD | Existing Home Sales Feb | |

| Forecast: 3.92M | Previous: 4.08M | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -62B | ||

| 21:45 | NZD | Trade Balance NZD M/M Feb | |

| Forecast: -235M | Previous: -486M | ||

| 23:50 | JPY | National CPI Y/Y Feb | |

| Forecast: | Previous: 4% | ||

| 23:50 | JPY | National CPI CoreY/Y Feb | |

| Forecast: 2.90% | Previous: 3.20% | ||

| 23:50 | JPY | National CPI Core-Core Y/Y Feb | |

| Forecast: | Previous: 2.50% | ||

Friday, Mar 21, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Mar | -21 | -20 |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | -10.9B | -15.4B |

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 38.4B | |

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.00% | -0.10% |

| 12:30 | CAD | Retail Sales M/M Jan | -0.40% | 2.50% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | 0.00% | 2.70% |

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | -12.8 | -13.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Mar | |

| Forecast: -21 | Previous: -20 | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | |

| Forecast: -10.9B | Previous: -15.4B | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | |

| Forecast: | Previous: 38.4B | ||

| 12:30 | CAD | New Housing Price Index M/M Feb | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 12:30 | CAD | Retail Sales M/M Jan | |

| Forecast: -0.40% | Previous: 2.50% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | |

| Forecast: 0.00% | Previous: 2.70% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | |

| Forecast: -12.8 | Previous: -13.6 | ||

The Weekly Bottom Line: Markets Tumble as Continued Trade Fights Reignite Recession Concerns

Canadian Highlights

- Markets were on edge this week as the U.S. followed through on its 25% tariffs on steel and aluminum imports.

- Trade tensions haven’t fully translated into economic data yet. Canadian household wealth rose for the fifth consecutive quarter while debt servicing costs fell to the lowest level since 2022.

- The Bank of Canada cut its policy rate by 25 basis points to 2.75% this week, but Governor Tiff Macklem warned that monetary policy can’t fully offset a trade war.

U.S. Highlights

- All three major indexes briefly entered correction territory this week as the trade fight continued to escalate. The sentiment has partially recovered by Friday boosted by the news that the government shutdown was averted.

- Consumer and business confidence continued to slide amid high trade uncertainty, while inflation expectations continued to spike.

- Continued policy and inflation uncertainty will keep the Federal Reserve on the sideline at its meeting next week until some time this summer.

Canada – Bank of Canada Cuts But Can’t Fight a Trade War

Markets were on edge this week. The S&P/TSX fell about 1.5% for the week and is now down 5% from its January peak. Long-term bond yields initially dipped as recession fears grew amid escalating trade tensions, but rebounded later in the week, closing a few basis points higher. The Canadian dollar remained under pressure, ending the week unchanged at 69 cents U.S.

The so-called “golden era” promised by President Trump is giving way to a “period of transition”, marked by heightened market volatility as trade policies shift. On Wednesday, the U.S. administration imposed 25% tariffs on Canadian steel and aluminum imports.

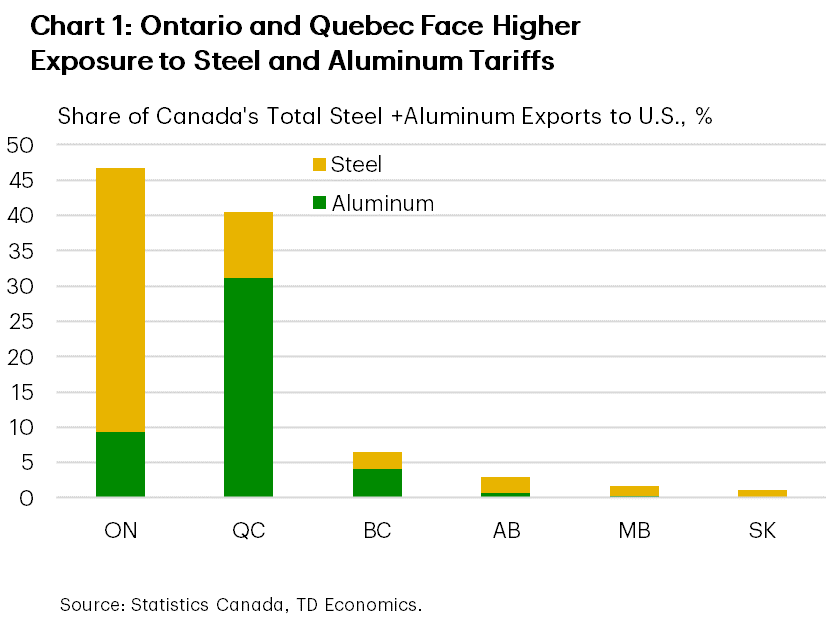

While steel and aluminum exports make up only about 6% of Canada’s total merchandise exports, the regional impact is more significant. Quebec produces most of Canada’s aluminum exports, while Ontario supplies the bulk of its steel exports to the U.S. (Chart 1). In response, Canada implemented new counter-tariffs on Thursday, adding to the $30 billion in U.S. imports already subject to duties as of last week.

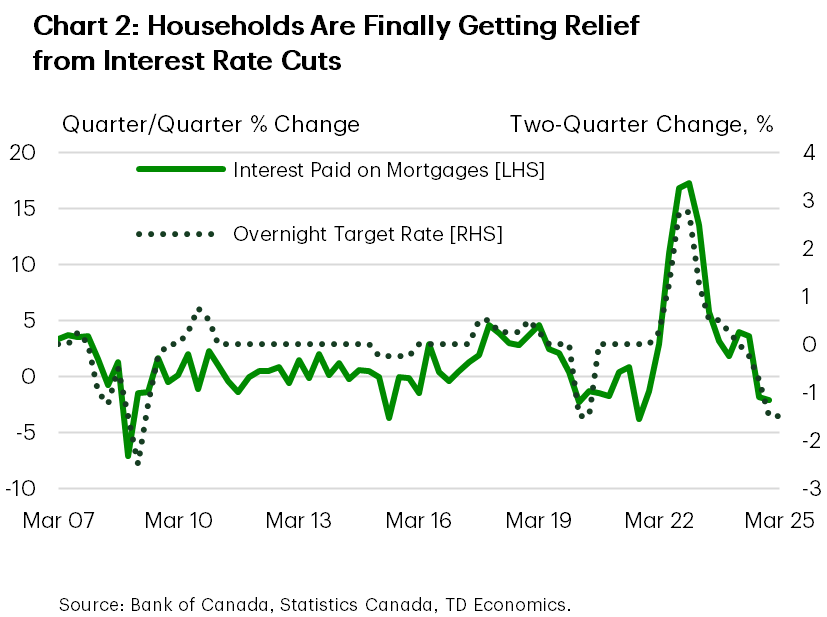

So far, tough trade rhetoric hasn’t fully translated into economic data. This week’s report on Canadian household balance sheet showed that wealth increased for the fifth consecutive quarter, supported by gains in financial and real estate assets. Importantly, households’ debt service ratio fell to its lowest level since 2022, reflecting the cumulative impact Bank of Canada rate cuts, which are now translating into lower aggregate interest payments (Chart 2). In turn, this should provide households with some financial relief, potentially supporting consumer spending.

However, uncertainty is weighing on sentiment. Preliminary results from the Bank of Canada’s business and consumer surveys suggest households are becoming more cautious with spending, while businesses – particularly in the manufacturing sector – are revising down their sales outlooks. Our latest TD debit and credit card spending data, set for release on March 17th, indicate that consumers are shifting toward precautionary savings and are cutting back on discretionary purchases. Still, given a solid hand-off into 2025, we anticipate one more quarter of above-trend growth in Q1 2025.

Beyond that, the outlook becomes murkier. The Bank of Canada cut its policy rate by 25 basis points to 2.75% this week, but Governor Tiff Macklem warned of “a new crisis” where “monetary policy cannot offset the impacts of a trade war”. This is because sustained tariffs risk lifting inflation, threatening the BoC’s hard-won 2% target. This limits how far the BoC can cut rates to support demand. As long as the pressure on tariffs remains in place, the BoC should keep its dovish bias, and we expect two more quarter-point cuts to take the overnight rate to 2.25% by June. Although markets are currently pricing in only a 50% chance of a cut next month.

U.S. – Markets Tumble as Continued Trade Fights Reignite Recession Concerns

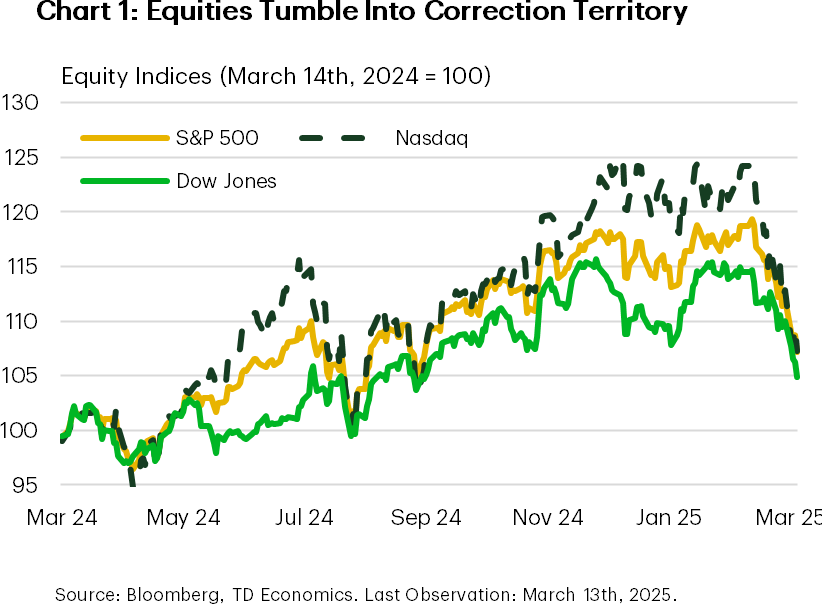

This has been another one of those “everything, everywhere, all at once” weeks. Investors were caught between a rock and a hard place, forced to navigate both a trade dispute and the threat of a potential government shutdown. Trade risks remain a major concern, reigniting fears of a recession and intensifying the selloff in financial markets. All three major indexes briefly entered correction territory, before retracting a bit on Friday as Senate Democrats appear to back the Republican’s stopgap spending bill that will keep the government funded through September 30th (Chart 1).

Tariff threats continued to dominate headlines this week, with the administration’s 25% steel and aluminum tariffs coming into effect on Wednesday, prompting retaliation from Canada, the E.U. and China. The E.U. imposed tariffs on $26 million of U.S. imports, while Canada imposed a 25% tariff on $30 billion worth of U.S. goods. In addition, China announced a 15% tariff on some key American farm products, such as pork, chicken, and soybeans, following the U.S.’s decision to raise the tariff rate on all Chinese imports by an additional 10% on March 4th – bringing the effective tariff rate on China to around 30%.

The recent ratcheting up of trade tensions has fueled concerns that tariffs could weight more meaningfully on growth this year and put further upward pressure on inflation. This week’s CPI report showed that inflationary pressures eased in February, with headline inflation slowing to 2.8% year-over-year down from 3% in January. While welcome, this reprieve may be short-lived as the latest numbers would have only captured the initial 10% tariff on China that came into effect on February 4th.

Business surveys indicate that inflation expectations and pricing intentions have risen, suggesting that price pressures are building in the supply chain. If tariffs remain in place, companies will eventually need to raise prices or absorb higher costs themselves. Some smaller businesses have already started raising prices. This week’s NFIB Small Business Confidence Survey showed a 10-point jump in the share of businesses increasing average selling prices.

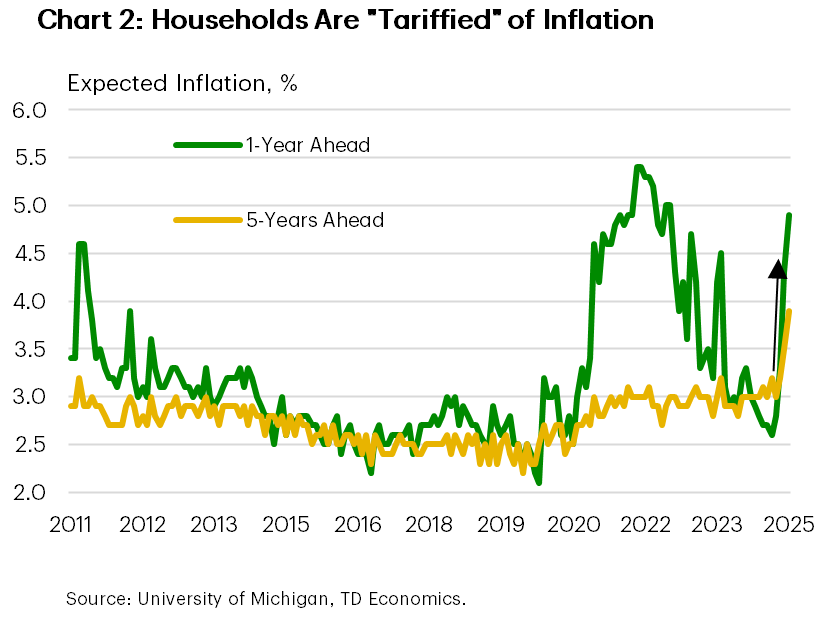

Household confidence has also been weakening rapidly, driven not only by the recent stock market selloff but also by expectations of higher inflation in the months ahead. Indeed, the March reading of University of Michigan’s survey of consumer confidence shows that after declines in the prior two months, consumer confidence continued to nosedive this March – falling to the lowest level since November 2022. Year-ahead inflation expectations surged from 4.3% last month to 4.9% in March, marking the highest reading since November 2022 (Chart 2).

Given the current storm of uncertainty, the Federal Reserve is likely to remain on hold at its next meeting next week. With inflation expectations becoming more unhinged, we expect the Fed to remain on the sidelines until some time this summer, at which point slowing economic growth will likely prompt the need for additional support in the form of lower interest rates.

Weekly Economic & Financial Commentary: Steel Yourself for a Section 232 Revival

Summary

United States: Hard to Get a Clear View on Restless Waters

- Amid rising uncertainty, lagging indicators show activity was stable before the tariff storm. The number of job openings was slightly higher than anticipated at the end of January, and both the CPI and PPI came in softer than expected in February. Yet, we expect a mixture of weaker hiring and stronger inflation by midyear, which would present a challenge to the FOMC. We now look for the Committee to cut 75 bps, bringing the fed funds rate target range to 3.50%-3.75% by year-end.

- Next week: Retail Sales (Mon.), Industrial Production (Tue.), FOMC (Wed.)

International: Mix of Economic News and Data from Global Economies

- This week saw a variety of economic developments and data releases from G10 and emerging economies. The Bank of Canada lowered its policy rate by 25 bps this week to 2.75% and provided accompanying commentary that was somewhat mixed, but overall somewhat dovish-leaning, in our view. The U.K. economy unexpectedly shrank in January, early results from the spring wage negotiations in Japan look encouraging and Norway saw an upside inflation surprise. Brazil's monthly inflation data, while not coming in as a surprise, continued to point to elevated price pressures.

- Next week: China Industrial Production and Retail Sales (Mon.), Bank of Japan Policy Rate (Wed.), Brazilian Central Bank Selic Rate (Wed.)

Credit Market Insights: Why Have Mortgage Rates Remained Elevated?

- Amid high mortgage rates, purchasing and refinancing applications remain suppressed from their earlier peaks. Even with the Federal Reserve's easing cycle being under way, mortgage rates remain high with upward pressure from the 10-year Treasury and mortgage spread.

Topic of the Week: Steel Yourself for a Section 232 Revival

- This week, the 25% tariffs on steel and aluminum imports announced by the Trump administration last month went into effect. All imports of certain steel articles and derivative steel articles are subject to the 25% tariffs under Section 232, essentially eliminating the carve-outs to the original Section 232 tariffs enacted during President Trump's first term (with a few changes).

Fed Expected to Keep Interest Rates on Hold, Canadian Price Growth to Move Higher

The balance of risk around the U.S.’s growth may be shifting, but government data still shows a strong economy and that will likely lead the U.S. Federal Reserve to stand pat on interest rates on Wednesday.

At the recent U.S. Monetary Policy Conference in Chicago, Chair Jerome Powell said that “despite elevated levels of uncertainty, the U.S. economy continues to be in a good place.”

Our own forecasts for U.S. GDP growth for 2025 have been marked lower on signs that an 11-quarter run of steady growth may have paused in Q1. The U.S. economy is less sensitive to international trade risks than many of its close trading partners (like Canada), but some sectors, particularly manufacturing, will be negatively impacted by tariff increases.

Still, labour markets look firm. The Trump administration’s DOGE cuts will likely nudge the unemployment rate higher in coming months but we expect it to remain historically low. A slower month-over- month increase in the consumer price index (CPI) in February confirmed that a spike in prices in January was more a reflection of technical seasonal adjustment issues than a change in trend, but inflation is still running above the Fed’s 2% objective.

Our base case assumption is that an outperforming U.S. economy and above-target inflation will keep the Fed from cutting the fed funds target range this year. But, the balance of risks around that call have been shifting with market expectations for additional cuts already showing up significantly in lower term bond yields.

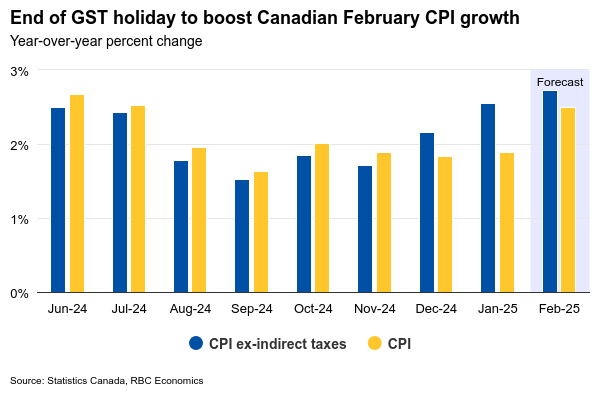

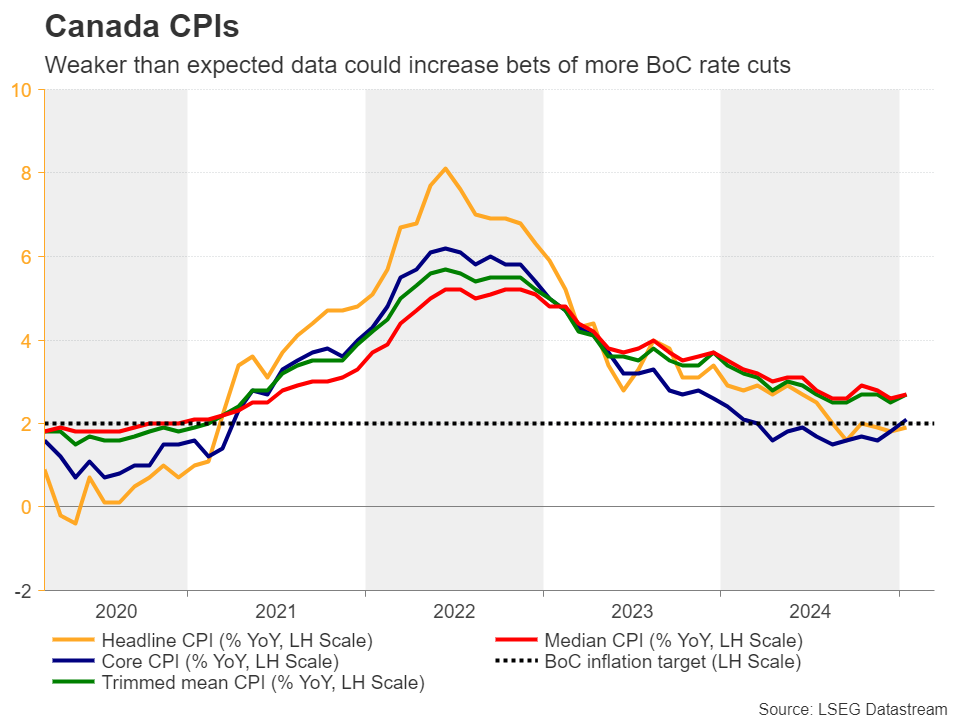

In Canada, the focus will be on February CPI data—in addition to international trade headlines. We expect to see a rise in year-over-year price growth to 2.5% with the GST tax holiday that mechanically depressed prices in December and January, ending in mid-February. That would end a string of six straight readings at or below the Bank of Canada’s 2% inflation target.

Indeed, evidence was building that a faster-than-expected re-acceleration in Canadian growth late last year and into early 2025 was also putting a floor under inflation. The BoC’s preferred “median” and “trim” core measures (which exclude the impact of changes in indirect taxes) picked up 2.7% year-over-year on average in January, and we expect it likely edged higher again in February. But, concerns that intensifying international trade risks will weigh on the economy are overshadowing stronger recent growth data. We continue to expect further BoC interest rate cuts down to 2.25% this summer.

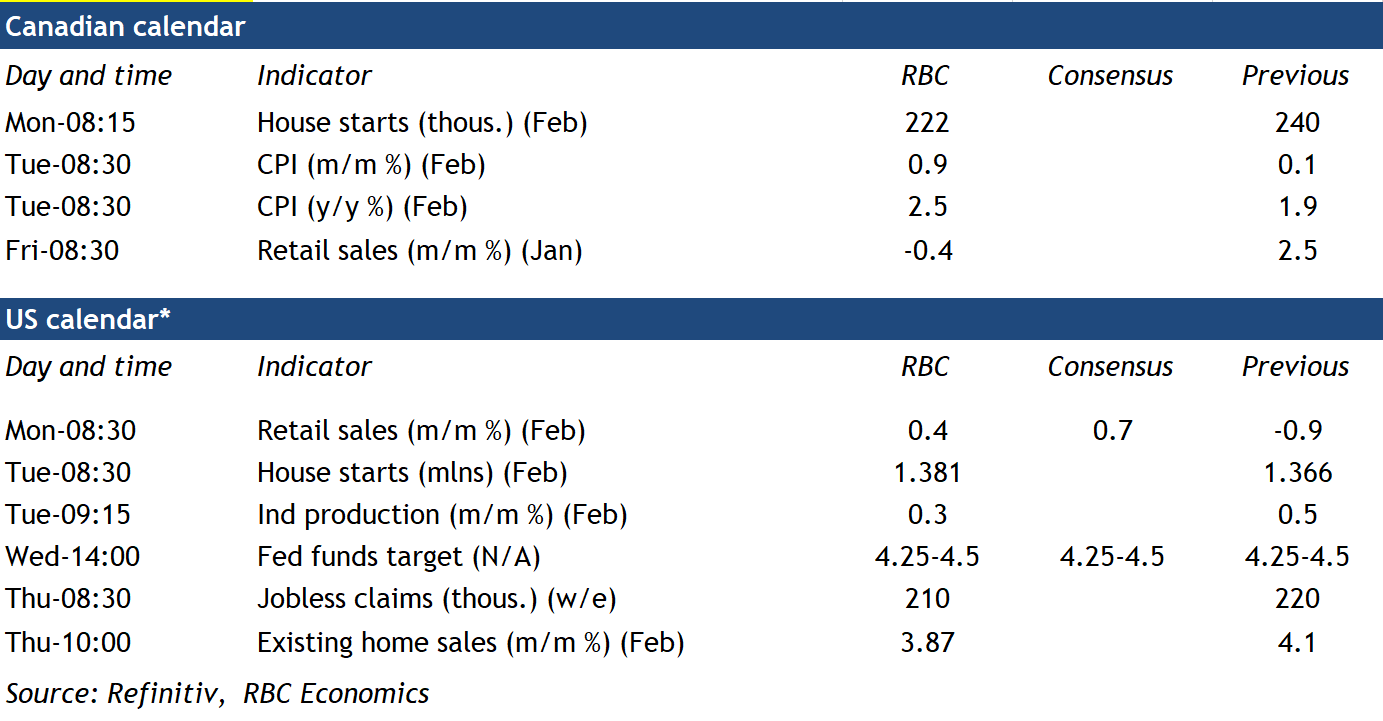

Week ahead data watch

Canadian retail sales are expected to contract by 0.4% in January, following robust growth in the previous month. This decline is primarily attributed to a significant 9% reduction in unit auto sales, partially offset by higher sales at gas stations due to price increases.

Canadian housing starts are forecasted to decrease to 222,000 units in February from 240,000 in January. February's construction activity was notably hampered by severe winter storms.

U.S. retail sales are expected to rise 0.4% in February, partially recovering from January's contraction. This growth is largely fueled by stronger auto sales and increased gas station sales.

U.S. industrial production is anticipated to expand by 0.3%, mainly driven by extended manufacturing hours that have boosted output across the sector.

Fed Preview: Aiming for Stability

- We expect the Fed to maintain its monetary policy unchanged in March, in line with wide consensus and market pricing.

- We do not expect Powell to guide explicitly towards a cut in May, but we do still anticipate three 25bp reductions later in the year starting from June.

- The Fed could signal either tapering or completely ending QT in the coming meetings. We do not anticipate strong immediate market reactions.

The Fed is inarguably navigating uncertain waters, but with hard data signalling little reason for concern, we doubt Powell will sound the alarm next week. While anything other than an unchanged rate decision would be a major surprise, markets are pricing in 35-40% probability of the Fed restarting cuts already in May.

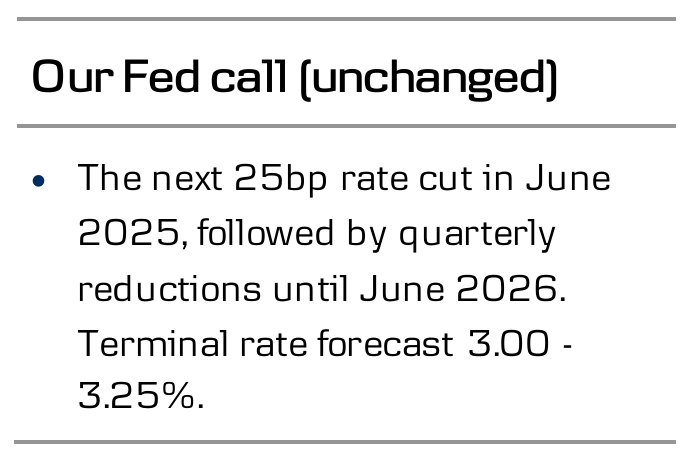

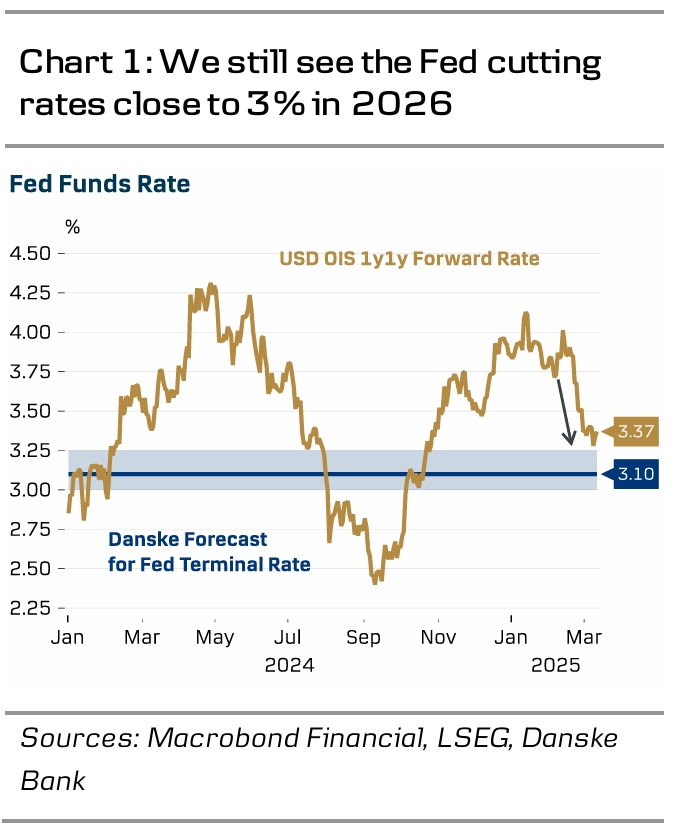

And while Powell has no incentive to close any doors, we do not expect explicit guidance towards a cut in May. We continue to forecast three rate cuts for 2025 followed by two more in 2026, which would take the terminal rate down to 3.00-3.25% - a level below current market pricing. But with employment growth remaining solid and the number of layoffs still low, we think the Fed has room to opt for a more gradual approach.

The updated rate projections could be revised slightly lower to indicate a faster return to neutral (currently only by 2027). The GDP forecast could also be revised slightly lower, while inflation forecasts will likely see only marginal changes. Forecast for unemployment rate could be revised lower as slower immigration tightens labour supply growth.

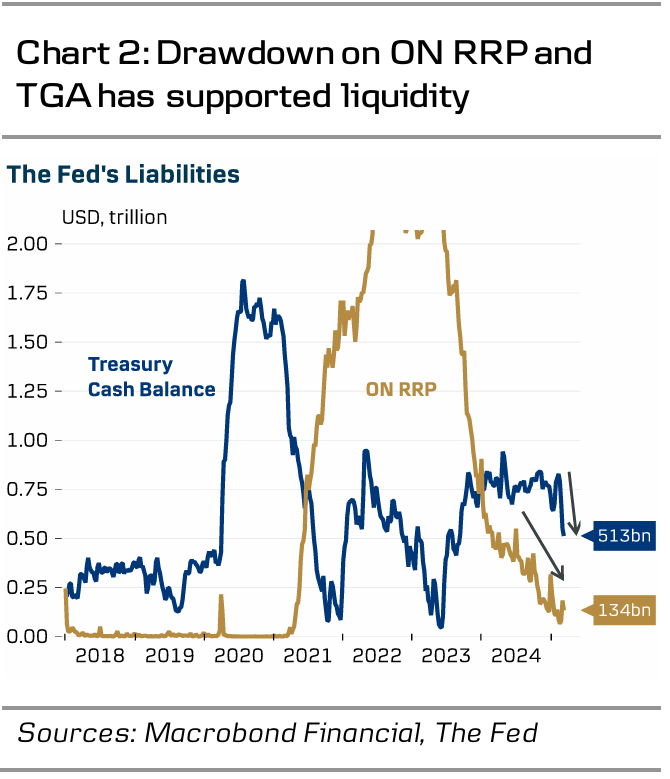

The latest minutes revealed that the policymakers had discussed the endgame for QT in detail already in January, and while we expect no changes next week, the decision to taper or even completely end the balance sheet run-off could be announced already now. While we think that the current level of bank reserves is still generally ample, the policymakers have previously communicated a preference for a cautious approach. The spread between SOFR and Fed Funds Rate has seen occasional upticks especially around month-ends and the liquidity buffer from the ON RRP facility is now mostly depleted. The April tax date and the ongoing process for lifting the debt ceiling create further near-term uncertainty around the liquidity outlook. While passing the debt ceiling raise as part of the Republicans' budget reconciliation package could still be weeks or even months away, it could theoretically be approved already in April or May. Together with larger-than-usual tax payments, rebuilding the Treasury cash balance could lead to an unexpected tightening of liquidity before the June meeting, which could justify ending the runoff already in May.

With 70bp worth of cuts priced in total for 2025 and 10y UST yield not far from our 12M target (4.20%), we do not anticipate strong market reactions to Wednesday's announcements. Even if the Fed likely does not see May as the base scenario for restarting the cutting cycle, Powell will have to choose his words cautiously, as sounding too hawkish might drive unwanted tightening of financial conditions. At times of extraordinary uncertainty, a 'boring' reaction in the markets is likely high up on Powell's wish list.

Week Ahead – Central Banks in Focus Amid Trade War Turmoil

- Fed decides on policy amid recession fears.

- Yen traders lock gaze on BoJ for hike signals.

- SNB seen cutting interest rates by another 25bps.

- BoE to stand pat after February’s dovish cut.

Tariffs remain at the top of investors’ agenda

The US dollar exhibited a mixed performance this week against its major counterparts as US President Donald Trump’s erratic tariff strategy left investors in a state of uncertainty. On Tuesday, Trump announced a 50% tariff on steel and aluminum imported into the US from Canada, only to backtrack after the Canadian province of Ontario suspended its 25% surcharges on electricity that it sends to some northern states in the US.

Nonetheless, the 25% tariffs on steel and aluminum went into effect on Wednesday, with both Canada and the EU retaliating on Thursday. Further escalation remains a possibility, as the introduction of reciprocal tariffs and a potential increase of the steel and aluminum duty to 50% loom on the horizon, with April 2 being the critical date for imposition.

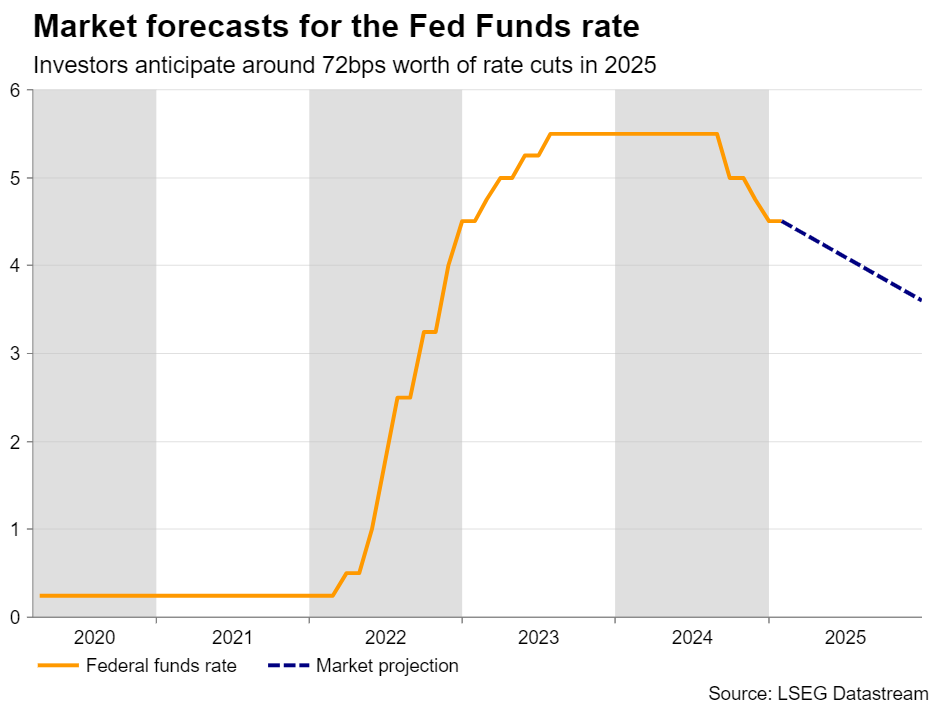

All this uncertainty has led to a marked deterioration in risk appetite, with Wall Street indices tumbling. The US dollar, too, has been caught in the crossfire of Trump’s tariff threats and attacks, as investors shifted their focus from inflation concerns to the broader implication on economic growth. They are currently penciling in around 72bps worth of rate cuts by the Fed this year, which is nearly one additional quarter-point rate cut compared to the 50bps indicated in the December dot plot.

Fed decision: Mind the dots

With all that in mind, next week’s FOMC decision, scheduled for Wednesday, may attract amplified attention. This will be one of the bigger meetings where, besides the decision, the statement and the press conference, the Committee will release updated economic projections, including a new “dot plot”; and with no action expected until June, the spotlight is likely to be firmly on the dots.

If Powell and Co. appear genuinely concerned about the impact of tariffs on the US economy and the dots are revised lower to point to more basis points worth of rate reductions this year, the US dollar is likely to extend its slide. Equities, which in the recent past were celebrating the prospect of lower borrowing costs, are more likely to continue their downturn as expectations grow that the US economy may tip into recession.

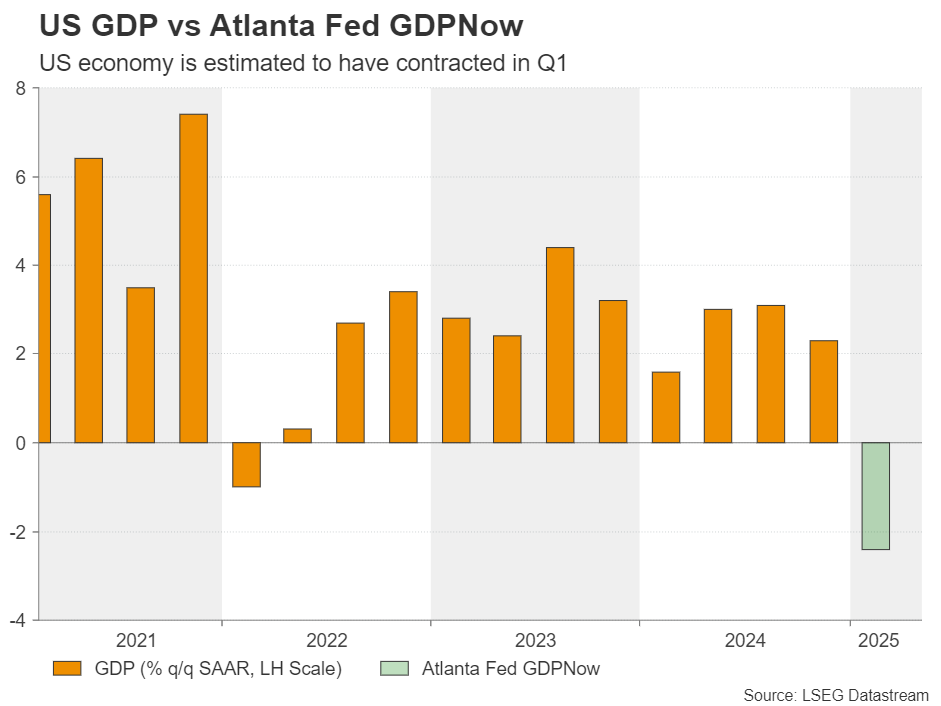

Speaking of recession, the day before the decision, the Atlanta Fed will release its updated estimate of GDP for Q1. The GDPNow model is already projecting a 2.4% qoq SAAR contraction, and a worse print may intensify speculation about the need for further rate cuts. Weaker-than-expected retail sales on Monday could indeed trigger such a downside revision.

Yen bulls await BoJ hike signals

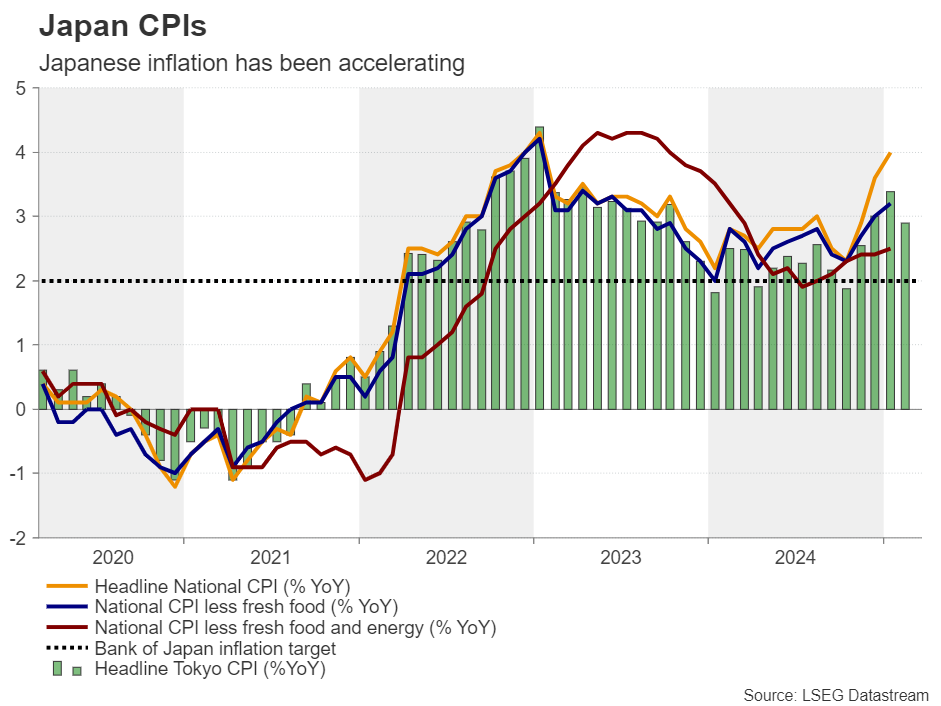

The Fed is not the only central bank to decide on interest rates next week. During Wednesday’s Asian session, the Bank of Japan (BoJ) will announce its own decision. At its first gathering of 2025, this Bank raised its key interest rate by 25bps to 0.5%, with Governor Ueda reaffirming his stance that additional hikes will probably be needed if economic conditions unfold as anticipated.

Since then, data has continued to suggest that underlying trends of wage growth remain solid, with consumer prices accelerating to 4.0% y/y from 3.6% in December and the BoJ’s own core CPI metric rising to 2.2% y/y from 1.9%. Although the Tokyo prints for February pointed to a mild slowdown, they were far from indicating that price pressures are well anchored around the Bank’s 2% objective. The Nationwide prints for February will be released during Friday’s Asian session, after the rate decision.

Taking all of this into account, along with the recent hawkish remarks by BoJ policymakers and the acceleration in economic activity during the last quarter of 2024, investors are fully pricing in the next 25bps rate increase to be delivered in September, assigning a strong 80% probability for it to occur in July. What further bolsters investors’ expectations is the fact that many of Japan’s biggest companies have met union demands for substantial wage hikes for a third straight year, helping employees cope with rising cost of living.

Thus, although the Bank is not expected to alter its monetary policy decision at this gathering, any hawkish commentary may allow the yen, which has been the top-performing currency this year, to extend its prevailing uptrend.

Will the SNB press the cut button again?

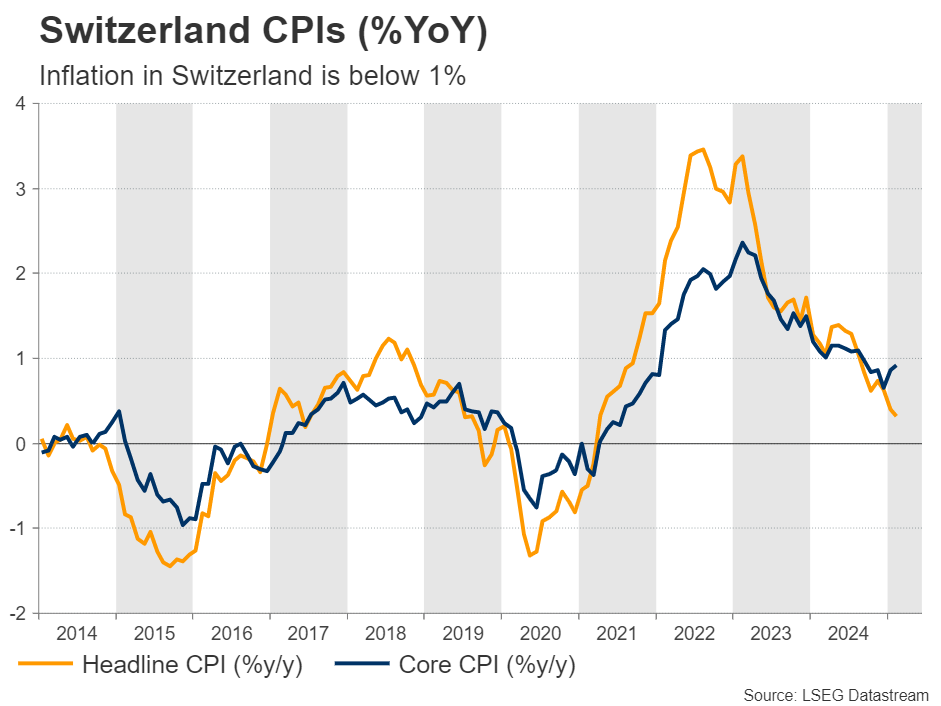

On Thursday, the central bank torch will be passed to the SNB and the BoE. Getting the ball rolling with the SNB, this will be the Bank’s first policy meeting since the turn of the year. Back in December, policymakers delivered a bigger-than-expected 50bps rate cut in an effort to curb gains in the Swiss franc.

However, the uncertainty surrounding Trump’s tariff policies has further fuelled the currency, while Swiss inflation fell to its lowest level in nearly four years in February, increasing the likelihood for another rate cut this year. The probability for another 25bps reduction next week rests at 75%, with the remaining 25% pointing to no action.

Thus, the rate cut alone is unlikely to spark significant volatility in the Swiss franc. For the currency to surrender a notable portion of its recent gains, the Bank may appear willing to proceed with more reductions if necessary.

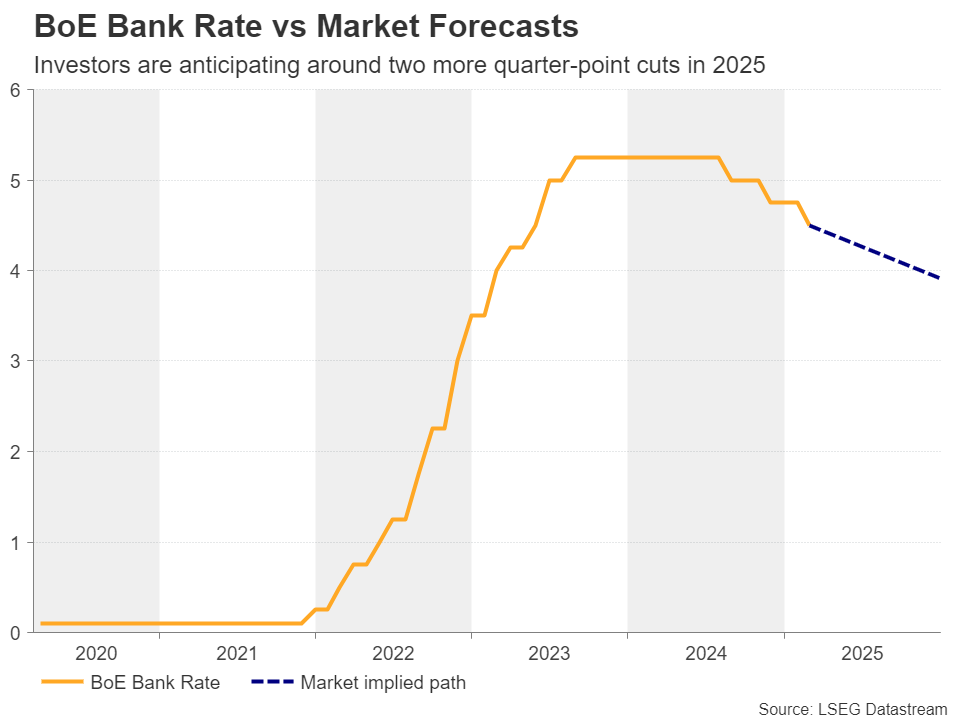

Will the BoE sound hawkish or dovish?

Passing the ball to the BoE, UK policymakers are widely anticipated to remain on hold after cutting interest rates by 25bps in February. At that meeting, the Bank downgraded its growth projections and raised its inflation forecasts. That said, the direction of the revisions was largely anticipated. What caught markets off guard was the fact that two members voted for a 50bps cut, with notorious hawk Catherine Mann – who was the sole advocate for keeping rates steady in November – this time voting for a double reduction.

Since then, economic data has mostly surprised to the upside, leading market participants to price in only two additional quarter-point reductions for this year, with the next one expected in June. However, a week ago, Catherine Mann said that Trump’s tariffs and volatility in financial markets mean policymakers need to act more decisively.

Thus, although no action is expected next week, a dovish stance, suggesting that more policymakers are holding the same view, could hurt the pound as investors may revive bets on deeper rate cuts. For the pound to extend its gains, the Committee may need to sound more concerned about inflation spiralling out of control.

Canada’s CPI, NZ GDP and AU jobs report also on tap

Elsewhere, Canada’s CPI numbers for February and the nation’s retail sales for January are set for release on Tuesday and Friday, respectively. This week, the BoC cut rates by another 25bps, warning that the nation is now facing a “new crisis” due to Trump’s tariffs. Market participants swiftly pencilled in another reduction for the April decision and weaker-than-expected data could further solidify that view.

New Zealand’s Q4 GDP report and Australia’s February employment data are also on the radar, which are both set to be released during Thursday’s Asian session.

Weekly Focus – Trade War Escalation Weighs on Markets

An intensifying trade war weighed on risk appetite in a week when particularly US equities traded lower still. The dollar stabilised at the new much weaker levels and global yields largely traded sideways. US steel and aluminium tariffs took effect, and the EU Commission responded with a range of countermeasures, including jeans and bourbon tariffs, but also highlights that they would prefer to remove them and find a solution with the US. The measures cover around 5% of total EU exports to the US and thus should have limited direct macro impact. In an uncertain world, gold prices tested new highs this week.

After a possible US recession has been gradually priced back into markets, some largely uplifting data was welcome, with inflation pressures moderating in February as core CPI declined to 0.2% mom, a relief for the Fed and markets not least with the recent surge in consumers' inflation expectations in mind. The number of job openings ticked a bit higher again in January, and jobless claims declined slightly despite the concerns related to federal layoffs, both confirming the solid picture of the labour market we got with the jobs report for February. The NFIB business survey revealed another sentiment decline among small US businesses with the uncertainty index climbing to the second highest level on record since the 70s. That said, business sentiment remains above levels prior to the presidential election.

Some positive data signs are also worth noting on our own continent. The ECB wage tracker continues to indicate slowing wage growth and thus price pressures, while the Sentix index, which has been a good indicator of PMI directions recently, surprised to the topside, indicating further improvement in economic activity over the recent month.

In Japan, the Shunto, spring wage negotiations, came off to a strong start as many of the big corporates decided to fully meet their labour unions' quite high wage demands. Strong wage growth is a prerequisite for further rate hikes from the Bank of Japan. We expect them on hold on Wednesday, though, not least supported by the recent yen strength.

We also have the Bank of England (BoE) and the Fed on hold. On the FOMC meeting, all eyes will be on the communication on the outlook for further rate cuts as well as the updated rate and economic projections. The Fed could also provide signals about further tapering or even completely ending QT over coming months. We think the BoE will stick to its previous guidance of gradual removal of policy restraint. Swiss inflation remains muted, which is also why we expect a 25bp rate cut to 0.25% from the SNB.

On the data front, we kick off the week with key Chinese housing data for both January and February. We will also look out for retail sales in China and in the US. We can draw no conclusions on the German fiscal package yet, as the CDU/CSU, SPD and The Greens have yet to agree. We will also look out for the votes in the Bundestag and Bundesrat (Upper House) on the German fiscal package.

Caught in the ‘Net’

A single event or trend never occurs in isolation. Reactions to it, as well as independent forces working in the opposite direction, mean the net overall effect can be uncertain and changeable.

This week we release our Market Outlook for March, updating our economic and financial forecasts. As well as the abrupt shift in market sentiment over the past few weeks, stemming from developments overseas, forecasting has been challenged by the prevalence of forces that are working in opposite directions on the same outcome. The net effect of these opposing forces can go either way, and it is often hard to know which direction will prevail.

The US tariffs are a case in point. They are likely to boost US inflation at the same time as being negative for growth. Which consideration will weigh more in the Federal Reserve’s monetary policy decision? You can rely on quantitative analysis to the extent possible, but often there is an element of judgement to these assessments. While it is hard to be sure, given the associated deterioration in market and consumer sentiment, we have – like market pricing – put more weight on the implications for growth and brought forward our expected timing of future Fed rate cuts.

More broadly, we cannot assess the net effect of tariffs and other US policies without also considering how the tariffed countries will react. This was one of the messages from our December/January Market Outlook, as expanded in a note with Westpac economist Illiana Jain. For Australia, the most salient reaction is how China will respond to the tariffs, particularly via domestic stimulus. More recently, countervailing tariffs – though not by Australia – and increased defence spending in Europe all come into the mix as responses to Trump administration policies.

The importance of how others react is also highlighted in the geopolitical sphere. Recent weeks have seen a clear break in how the US is perceived by its longstanding allies, and in the reliance those allies can place on US defence cooperation. We had already factored in the imperative for higher defence spending into our thinking to some degree, including in Europe. This was one of the shifts tilting the balance of global saving versus global investment relative to the pre-pandemic period that informed our house view that the global structure of interest rates is likely to average higher in future than it did in the period between the GFC and the pandemic. Developments in recent weeks reinforce the underpinnings of that view.

On the domestic front, we likewise see opposing forces with uncertain net effects. For consumption growth, we see a pick-up as tax cuts and declining inflation translate into stronger growth in real household incomes. Against those forces, though, population growth is slowing as the post-pandemic catch-up washes through. This could weigh on growth in total consumption even as per capita consumption and sentiment improve.

The unwind from the surge in population growth also complicates assessments of the outlook for the labour market. Recall that if population growth is high, employment growth needs to run very hard to keep pace with rising labour supply, else labour market slack will emerge. In the Australian context, a rising trend in the participation rate has added to this imperative. As the post-pandemic surge in population growth unwinds, that imperative will lessen.

At the same time, though, we know that the boost to employment from the ramp-up in the care economy will end, and employment growth in that sector will normalise. So we have a potential slowing in growth in labour demand at the same time as growth in labour supply (from population growth) is also slowing. The net of these two shifts is uncertain, and it could evolve over time and perhaps even change sign.

On top of the complexities of balancing two shifts in trend with uncertain net effects, any situation where trends are shifting presents measurement issues. A sharply changing growth rate is also one that is hard to measure accurately in real time. Interpreting the data to infer a trend becomes more complicated in this situation. For the labour market, one way to look through these changes in trend is to focus on ratio measures such as employment-to-population or the unemployment rate, rather than employment growth. It remains the case, though, that the dynamics of labour supply will reflect the net of the opposing forces of slowing population growth and a still-rising trend in participation.

There is a broader point here: when considering the effect of a shock, you cannot trace through its effect alone. It is important to factor in the reactions and whether there are other independent (ie not explicit reactions) forces that are offsetting. You also need to hold your assessment of the sign of the net effect lightly and recognise that small changes in relative strengths could flip that sign. This sounds like the general equilibrium thinking economists are trained to do. Most of the time, though, strategic behaviour by conscious actors is a better way to frame the situation.

Importantly, if the net effects of two or more opposing forces flips in sign (or could do so), you need to acknowledge that possibility, rather than getting caught in a narrative favouring one direction. Understanding those forces and how they might evolve can in any case be more useful for your own decision-making than a fixed view of their net effect.

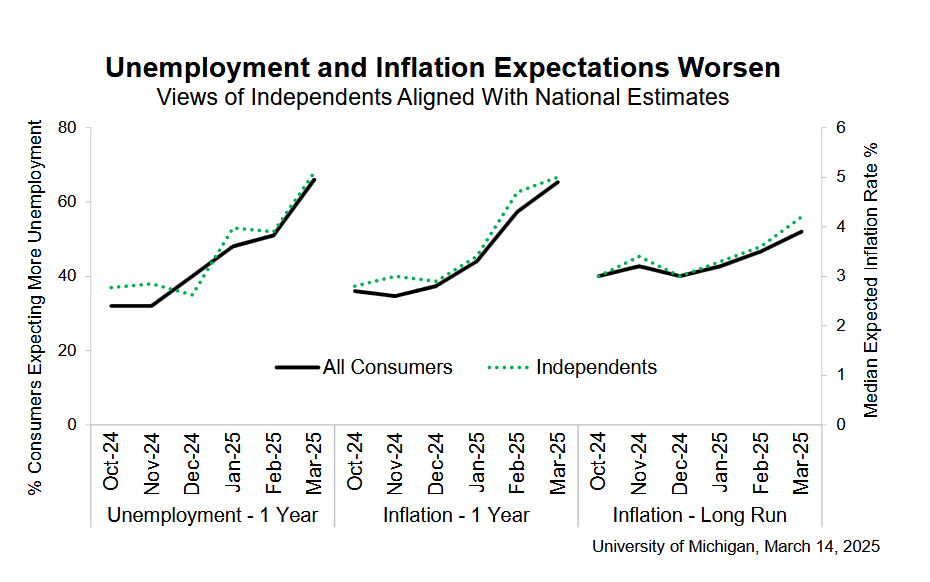

US Michigan consumer sentiment plunges to 57.9, inflation expectation jumps to 4.9%

US consumer confidence took another sharp downturn in March, with University of Michigan Consumer Sentiment Index falling from 64.7 to 57.9, well below expectations of 63.8. Current conditions dipped slightly from 65.7 to 63.5, but Expectations saw a much steeper fall from 64.0 to 54.2.

Of particular concern is the dramatic jump in inflation expectations. Year-ahead inflation expectations rose from 4.3% to 4.9%, the highest level since November 2022. This marks the third consecutive month of unusually large increases of 0.5 percentage points or more, suggesting that consumers are beginning to view inflation as a more entrenched issue.

Even more alarming, long-term inflation expectations surged from 3.5% to 3.9%, the largest month-over-month increase since 1993.

The report also revealed a rare bipartisan consensus regarding the weakening economic outlook. The University of Michigan noted that consumers across all political affiliations cited uncertainty over policy and economic conditions as a major concern, making it difficult to plan for the future.

Even among Republicans, who had shown greater confidence following the election, expectations dropped by 10%. Independents and Democrats posted even steeper declines of 12% and 24%, respectively.

Full University of Michigan Consumer Sentiment release here.

XAU/USD: Gold Cracks $3,000 Milestone

Gold broke above psychological $3000 barrier on Friday. Historical move through a milestone came a bit faster than expected, although I predicted this in my comments and live presentations last year, as a bigger picture, particularly fundamental, was clearly pointing to such scenario.

Thursday’s fresh acceleration higher took out previous record high and boosted signals for attack at $3000 that materialized today.

The latest negative developments in geopolitical and economic fields accelerated migration into safety, which will likely persist as there are no significant encouraging signals on the horizon.

Trade war is gaining pace and threatening to further hurt already fragile conditions in most large economies, with deepening economic crisis to spill over through the smaller economies.

Geopolitical situation, like another key driver, is darkening, with signals of more Fed rate cuts adding to supportive signals.

However, clear break higher is likely to take some time, due to significance of $3000 barrier, with initial technical support at $2980 (hourly higher base) remaining intact for now.

Shallow correction, in the first scenario, should stay above $2980, while deeper pullback should find firm ground above former record high ($2956) to keep larger bulls in play.

Close above $3000 is needed to validate bullish signals and unmask targets at $3032 and $3050 (Fibo projections 161.8% and 176.4% respectively).

Res: 3004; 3017; 3032; 3050.

Sup: 2986; 2980; 2956; 2942.