Sample Category Title

Gold: The Ultimate Trump Hedge

The Chinese markets opened for the first time after a long Lunar New Year holiday, and they opened down on a set of weaker-than-expected PMI figures, on the news of 10% tariff on its exports toward Trump’s USA, and a further escalation of the trade war with the tit-for-tat measures announced yesterday from Beijing, including 15% tariffs on US coal and LNG imports and an antitrust probe into Google. But losses in the CSI 300 index remained measured, as the 10% tariffs from the US were considered as being quite modest – compared to the chatter of up to 60% tariffs, and China’s response to the US was also seen moderated. Many simply pointed out that 10% tariff could be absorbed by yuan devaluation and that Google is banned in China since 2010 for not censoring search results in accordance with Chinese government regulations.

Across the Pacific Ocean, Google hit a record high yesterday regardless of the Chinese threat. Magnificent 7 saw dip buying and rebounded near 1.80%. Palantir was the star of the day with a 24% rally in its share price after announcing lot better-than-expected quarterly results and amassing rating and PT upgrades from big banks on its capacity to cash in on the AI boom. In Europe, German Infineon also jumped 10% on better-than-expected revenue forecast from the company due to favourable currency effects and recovery from car industry.

Overall, the Stoxx 600 was also better bid on Tuesday on rising confidence that the EU could negotiate trade terms with Trump and avoid tariffs. Plus, the French PM Bayrou is expected to survive a no-confidence vote today and adopt a budget plan. Such outcome would further narrow the German, French yield spread and encourage a recovery in euro’s valuation, though the upside is seen limited by the European Central Bank (ECB) doves.

In the US, the S&P500 and Nasdaq 100 consolidated gains above the 50-DMA level on relief that Trump’s tariff tantrum quickly fizzled out, and also on the back of lower-than-expected job openings in the US that hinted that – after big increases in the recent months - the trend is back to softening. Softer job openings data hints at softer pressure for higher wages and potentially more supportive Federal Reserve (Fed) policy. As such, the US yields eased and the dollar softened yesterday. The EURUSD regained the 1.03 mark and Cable approached the 1.25 psychological resistance. Traders will focus on the US ADP report and ISM data today. A set of softer-than-expected figures could further pull the US dollar lower.

On the equities front, sentiment is much less cheery this morning as Google and AMD results – released after the bell – didn’t enchant investors. Google announced better-than-expected earnings per share but a slight miss on the revenue growth. More importantly, growth in Google Cloud was *just* 30% (lower than the 32% expected by analysts) and slowing. The combination of slowing cloud revenue and massive AI investment – which will reach reportedly $75bn at Google this year (!) – raises a few eyebrows among investors. By few eyebrows, I mean a 7% drop in the afterhours trading as reaction to the latest results.

AMD, on the other hand, posted better-than-expected earnings and revenue in Q4, its data center revenue nearly doubled last year but fell short of analyst expectations, leading to a nearly 9% drop in AMD’s stock price in the AH trading.

Discontent with Google and AMD results is weighing on US futures this morning, along with Trump risks and worries.

Note that, investors may look more relaxed now than they did at the start of the week, but havens continue to see increased demand on the back of growing global uncertainties under Trump’s hectic lead and with the prospects that the first weeks under Trump is just a foretaste of what’s to come in the next four years. And there is not a better hedge than gold for protecting a portfolio from Trump worries: the more chaotic international relations become, the greater the demand—especially from central banks looking to reduce US exposure should Trump turn his focus on them. As a result, gold hit a record high for the fourth straight session, reaching $2,860 per ounce in Asia for the first time ever. At this pace, Trump makes $3,000 look like an easy target…

In energy, US crude tipped a toe below the $71pb level on de-escalating tensions with Mexico and Canada, but recovered some of the losses on Trump’s renewed pressure on Iran. While the geopolitical risks remain tilted to the upside, Trump’s trade policies are looking bad for global growth prospects and the latter should keep the medium-term upside potential limited. Top sellers are expected to join in between $73/75pb range to make a fresh attempt on the $70pb psychological support in the foreseeable future.

US ADP Data Sets Stage for Nonfarm Payrolls on Friday

In focus today

Today, we receive US private sector employment data from ADP, which will provide markets with the first sense of what to expect from Friday's nonfarm payrolls. ISM Services data is also due for release today, the flash services PMI released earlier surprised to the downside. The Fed's Barkin and Goolsbee will give speeches in the evening.

In the euro area, the final January services and composite PMI will be released. Earlier this week, the final manufacturing PMI was released, showing an increase to 46.6 from the preliminary 46.1, indicating more positive sentiment compared to previous months.

Economic and market news

What happened overnight

Update on the Middle East, during a talk with Israel's Prime Minister, Trump stated that the US will "take over" the Gaza Strip and suggested resettling its 2.2m residents in Egypt and Jordan, despite their previous rejection. This proposal could disrupt decades of US policy and provoke outrage across the Arab world. Trump did not clarify how the US would take control of Gaza. In addition, he signed a memorandum aimed to impose "maximum pressure" on Iran and reduce its oil exports to zero. Following this announcement, Brent crude futures traded around USD 76 a barrel, well above Tuesday's low of USD 74.15.

What happened yesterday

In the US, the JOLTs report showed a weaker-than-expected 7.6M job openings (cons: 8.0M, prior 8.09M), indicating a softened labour demand in December following a strong rebound in November. This could serve as a dovish signal for the Fed, suggesting the economy is not overheating and may face reduced inflationary pressures. However, involuntary layoffs decreased and remain at historically low levels, while hiring was slightly higher than the previous months. Overall, conditions remain solid, keeping the Fed on the sidelines.

China's package of retaliation measures against tariffs includes export controls on five metals used in defence, clean energy and other industries. This is an area where China can significantly impact the US, indicating a readiness to engage in conflict if Trump is inclined to do so. On 13 February, we are holding a webinar where we will attempt to shed light on this situation.

In Sweden, the January decision to cut was unanimous, with all members agreeing that the December rate path and forecasts largely hold. However, a majority wants to see evidence of an accelerating economic recovery and more balanced inflation risks in the coming months. Overall, the minutes support our view that more cuts are likely, with a cut expected in May. We also see potential downside risks to the Riksbank's growth and inflation forecasts in the coming months.

Equities: Global equities were higher yesterday, ending close to the day's high and reversing most of the losses from Monday related to the trade war tensions between the US, Canada, and Mexico. What is slightly interesting here is that we saw a massive cyclical outperformance, with most defensives being lower. This also demonstrates a rather strong "buy the dip" mentality still present in the market. "Buy the dip" has been a profitable strategy for the last two and a half years, and we argue that trade tensions are not enough to turn this around. We would need weaker macroeconomic data to see a stop to the "buy the dip" mentality.

In the US yesterday, Dow +0.3%, S&P 500 +0.7%, Nasdaq +1.4% and Russell 2000 +1.4%. Asian markets are mixed this morning. Chinese mainland markets are lower as they reopen after the Lunar New Year, and Trump and Xi did not have the expected talks that could bring a last-minute halt to tariffs. That said, it appears very much like consensus believes the Chinese retaliatory tariffs hitting "just" USD 14bn worth of imports from the US (just 5.8% of China's total imports from the US) is next to nothing. This should also be seen in relation to the 10%, not 60%, tariffs from the US side. Hence, consensus is now starting to adjust down their estimates for the US/China tariffs. US and European futures are lower this morning, negatively affected by some big earnings reports that came out in the US after the closing bell yesterday.

FI: There were modest movements in European government bond yields yesterday with 10Y Bunds trading around the 2.4%-level. The Bund ASW-spread is once again tightening and is trading around -2bp. We have a target of -10bp to -15bp for the Bund ASW-spread in Q1. In the US, yields dropped late in the afternoon in US trading hours after an initial rise. Today, the US Treasury will publish more on their funding plans for Q2, and markets will be looking for the split between bonds and bills.

FX: EUR/USD has seen a modest relief rally following a barrage of tariff headlines over the weekend and at the start of this week, now trading above 1.0350. The SEK has picked up momentum and is having its best week so far this year. That goes for the NOK as well. Both EUR/SEK and EUR/NOK have made a new year low at 11.38 and 11.66, respectively. The CAD continues to recover after the tariff postponement, whereas MXN has stayed flat overnight. Talking about year lows, let us also mention USD/JPY that has dropped 2.5% this year and was on the verge to break below 153 yesterday.

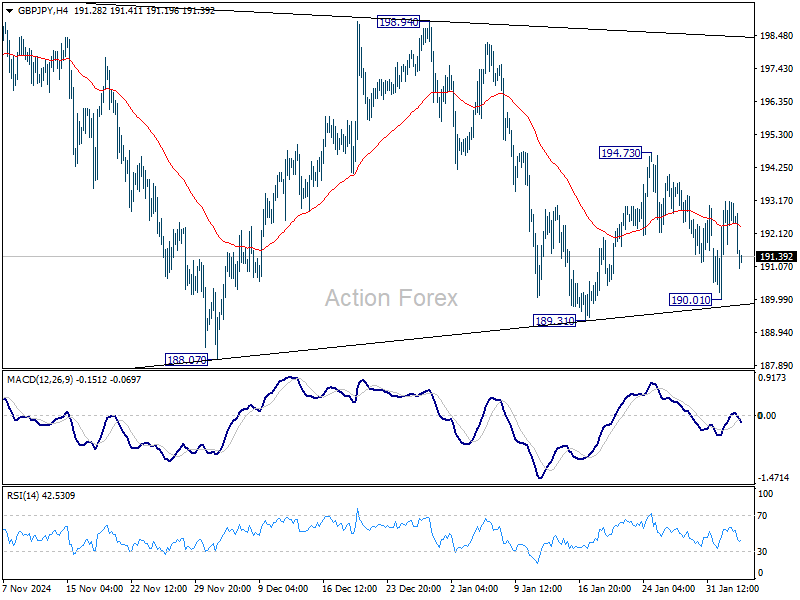

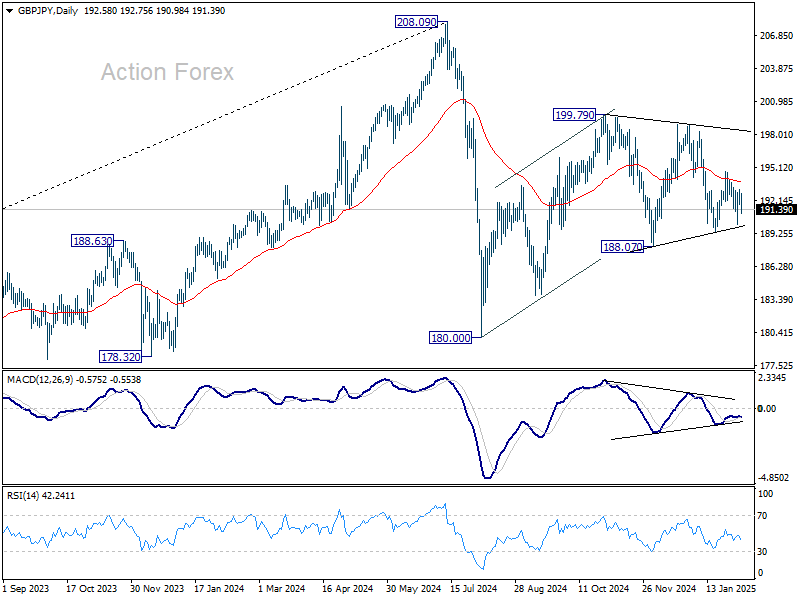

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.89; (P) 192.53; (R1) 193.28; More...

Intraday bias in GBP/JPY stays neutral at this point. On the downside, firm break of 189.31 will suggest that corrective pattern from 180.00 has completed. But before that, the pattern could still extend. Break of 194.73 will bring stronger rebound instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

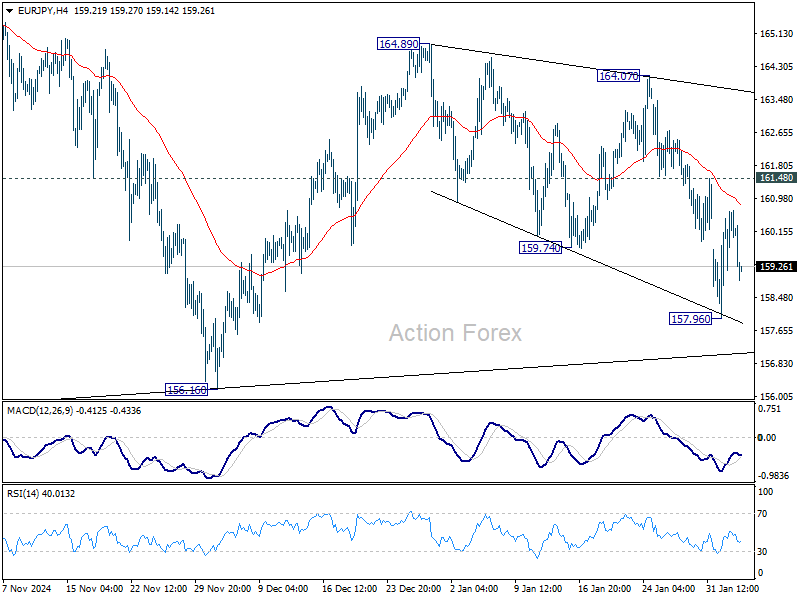

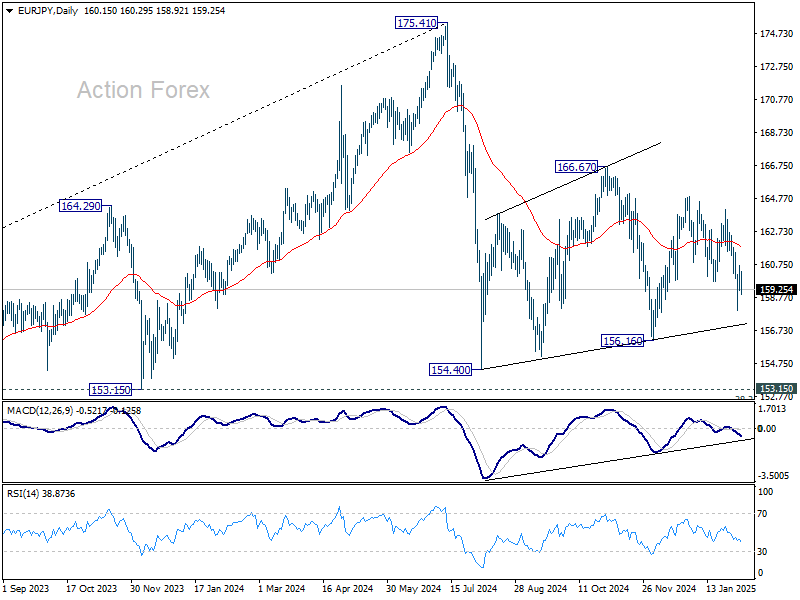

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.36; (P) 160.04; (R1) 160.88; More...

Intraday bias in EUR/JPY stays neutral at this point. Overall outlook is unchanged that consolidation pattern from 154.40 could still extend. On the downside, below 157.96 will target 156.16 support. However, break of 161.48 will turn bias back to the upside for 164.07 resistance.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

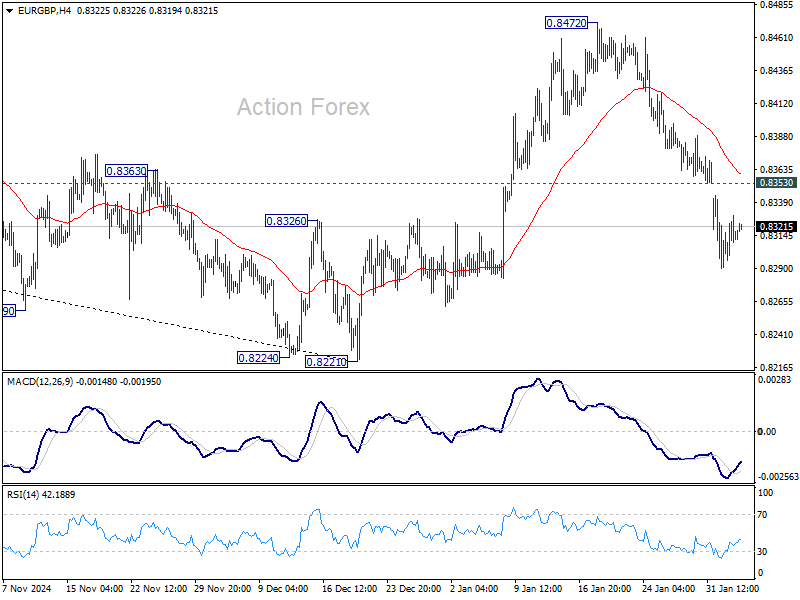

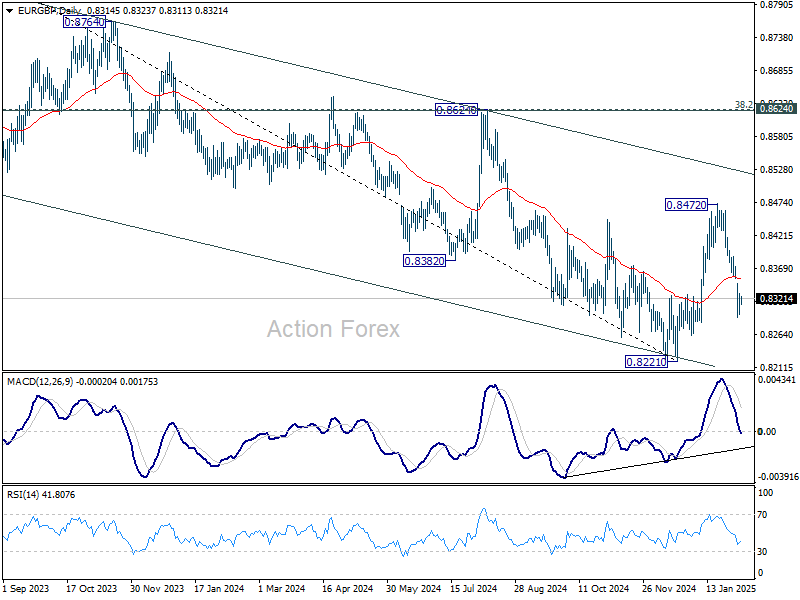

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8298; (P) 0.8315; (R1) 0.8331; More...

Further decline is expected in EUR/GBP with 0.8353 minor resistance intact. Corrective rebound from 0.8221 should have completed already. Fall from 0.8472 would target a retest of 0.8221 low. However, firm break of 0.8353 will turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.

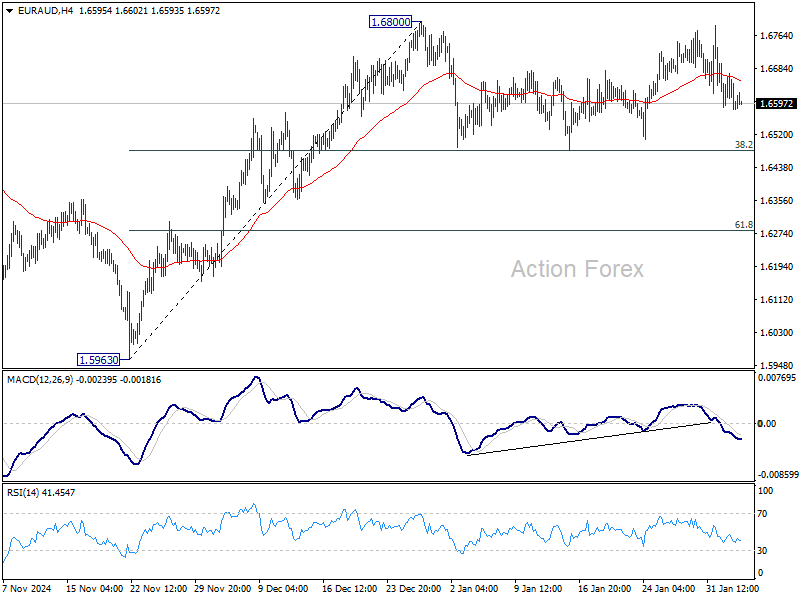

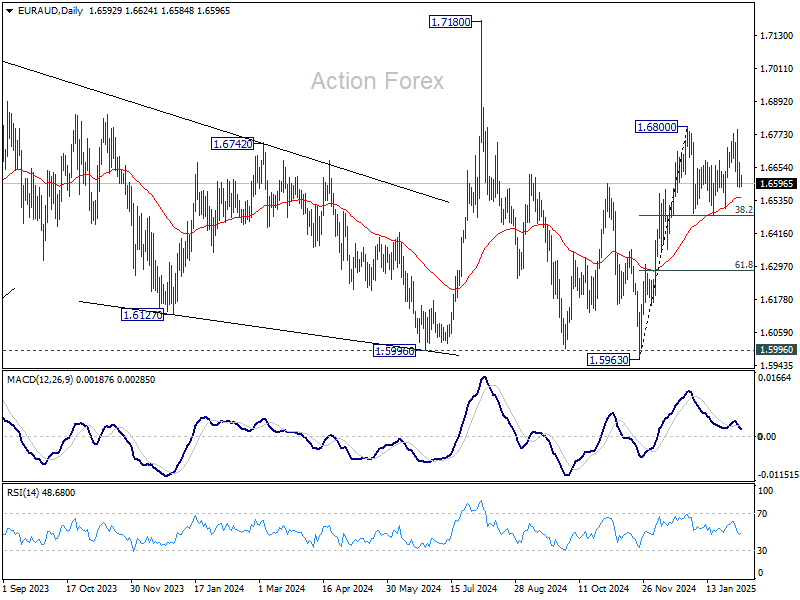

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6559; (P) 1.6616; (R1) 1.6649; More...

Intraday bias in EUR/AUD remains neutral as consolidations continue below 1.6800. Strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support (2024 low) despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

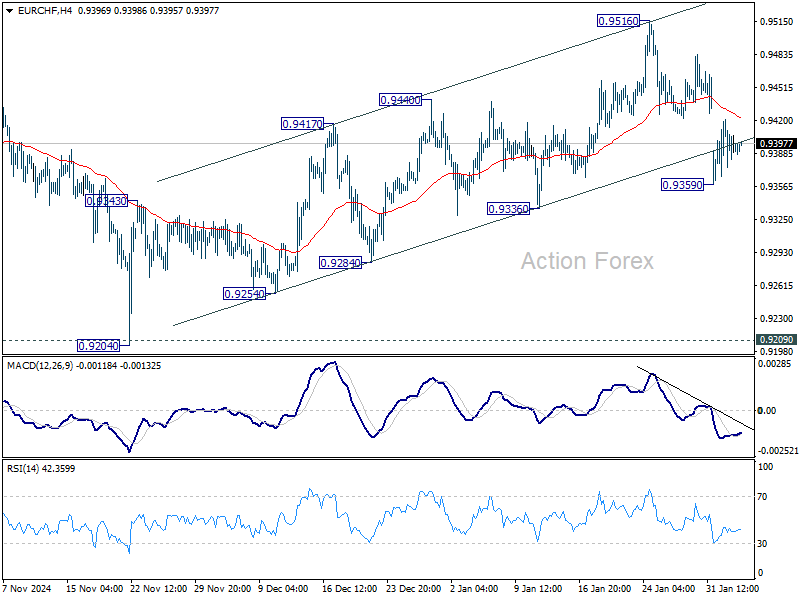

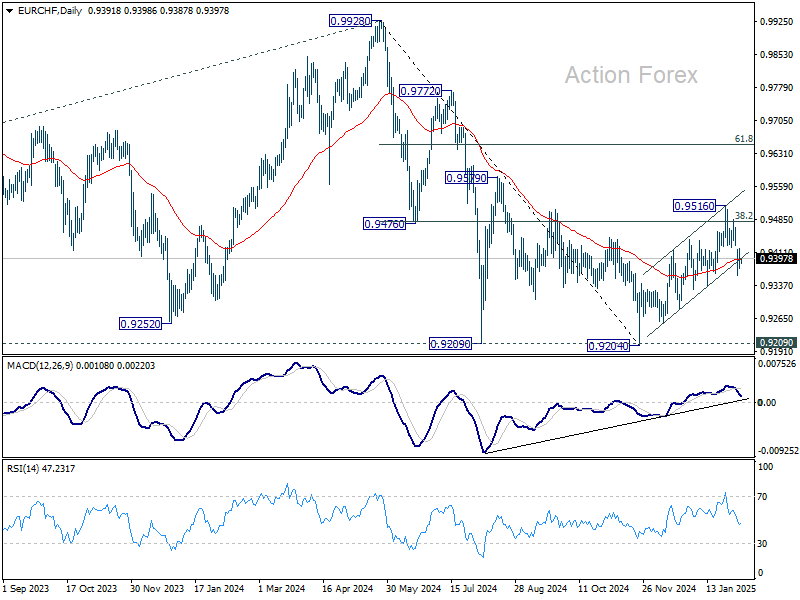

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9373; (P) 0.9397; (R1) 0.9419; More....

Intraday bias in EUR/CHF stays neutral for consolidations above 0.9359 temporary low. Risk will stay on the downside as long as 0.9516 resistance holds. Corrective rebound from 0.9204 might have completed at 0.9517 already. Firm break of 0.9336 support will solidify this bearish case and target a retest on 0.9204 low.

In the bigger picture, current development argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.

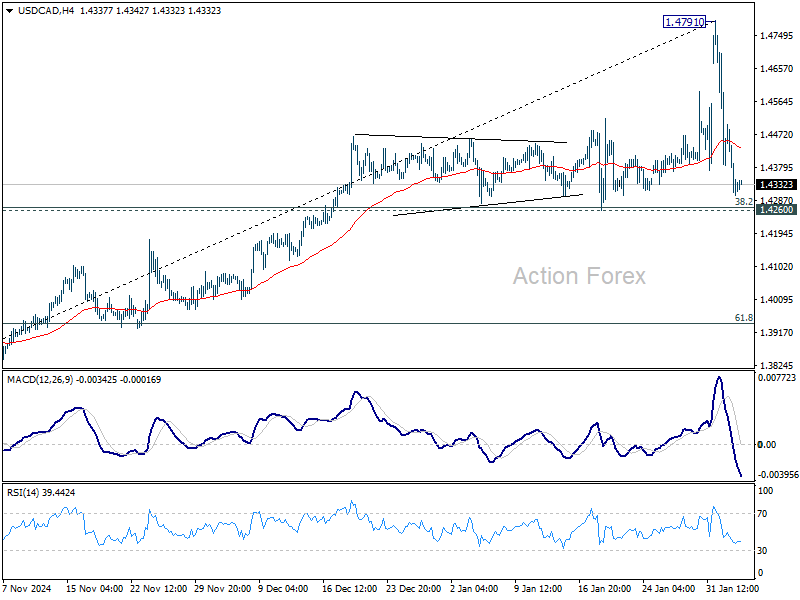

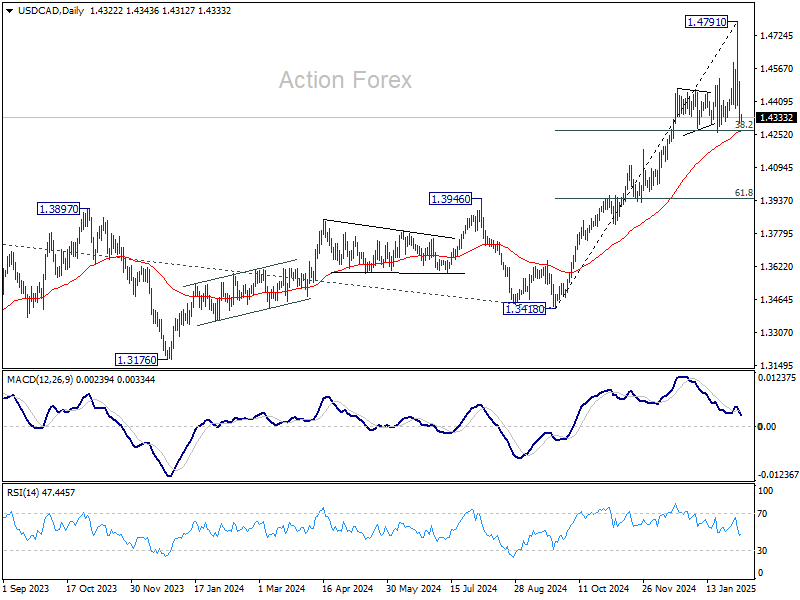

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4245; (P) 1.4374; (R1) 1.4446; More...

Intraday bias in USD/CAD stays neutral for more consolidations below 1.4791 short term top. Downside should be contained by 1.4260 cluster support (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4267), to bring rebound. Larger up trend is expected to resume through 1.4791 at a later stage. However, firm break of 1.4260 will indicate that deeper correction is underway.

In the bigger picture, the break of 1.4667/89 key resistance zone (2020/2015 highs) confirms long term uptrend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

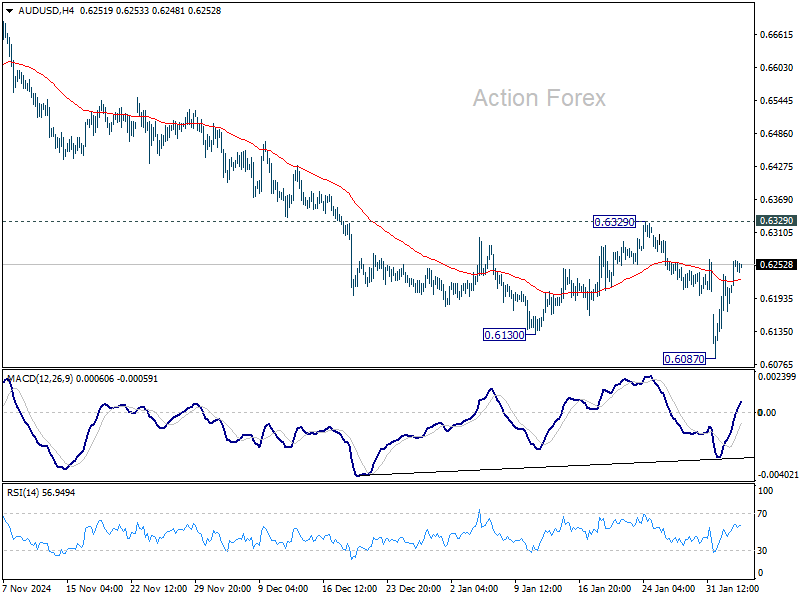

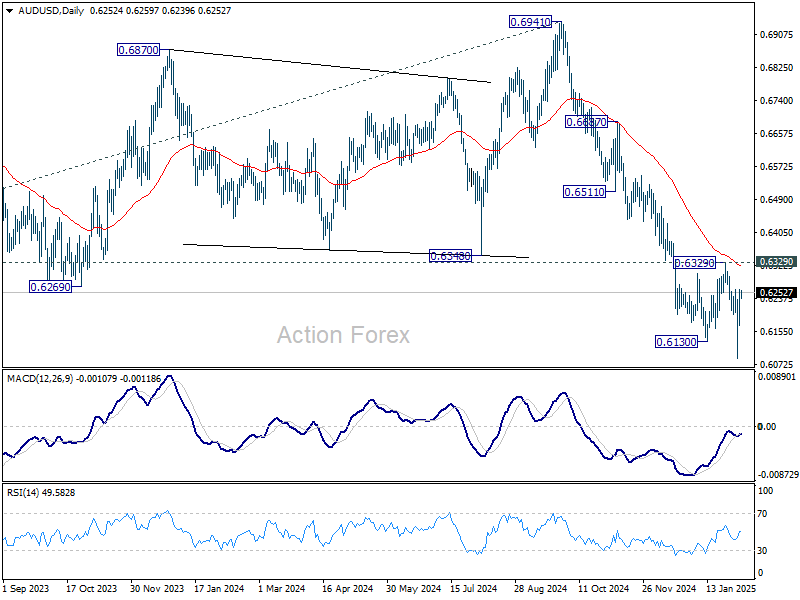

AUD/USD Daily Report

Daily Pivots: (S1) 0.6197; (P) 0.6230; (R1) 0.6288; More...

Intraday bias in AUD/USD stays neutral as consolidation continues above 0.6087. Further decline is expected as long as 0.6329 resistance holds. Break of 0.6087 will resume larger decline from 0.6941. However, firm break of 0.6329 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6511) holds.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0305; (P) 1.0346; (R1) 1.0421; More...

Intraday bias in EUR/USD remains neutral as consolidations from 1.0176 is extending. Outlook will stay bearish as long as 1.0531 resistance holds. On the downside, decisive break of 1.0176 will resume whole fall from 1.1213. Next target will be 61.8% projection of 1.1213 to 1.0176 from 1.0531 at 0.9890.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. For now, risk will stay on the downside as long as 1.0531 resistance holds, in case of rebound.