Sample Category Title

US PMI composite falls to 9-mth low, optimism holds despite slowing growth and rising costs

US PMI data for January painted a mixed picture. PMI Manufacturing rose from 49.4 to 50.1, reaching a seven-month high and signaling a return to slight expansion. However, PMI Services dropped sharply from 56.8 to 52.8, a nine-month low, dragging PMI Composite down from 55.4 to 52.4, also a nine-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlighted that US businesses are starting 2025 in an "upbeat mood," with optimism about the new administration driving stronger economic growth. Despite the slowdown in output growth, "sustained confidence" among businesses suggests this deceleration may be temporary. Encouragingly, hiring has surged, with job creation reaching its fastest pace in two and a half years, signaling resilience in the labor market.

However, inflationary pressures are resurfacing, posing risks to the economic outlook. Companies have reported "supplier-driven price hikes" and "wage growth amid poor staff availability." Inflation in input costs and selling prices has been "broad-based across goods and services," which, if sustained, could fuel concerns about hawkish policy approach from the Fed.

Sunset Market Commentary

Markets

Eurozone business activity returned to growth in January according to flash EMU PMI’s. The composite gauge ticked up from 49.6 from 50.2 (vs 49.7 expected). It’s only the first 50+ reading since August of last year. The rate of expansion was only marginal amid ongoing demand weakness and it was centered solely on services. The services PMI was broadly flat at 51.4 with that PMI over the past year being only below the 50 boom-bust mark in November 2024. The manufacturing PMI improved from 45.1 from 46.1, the least worse level since May of last year. There were overall signs of improvement with business activity in Germany stabilising, ending a six-month sequence of decline. France remained in contraction, but the pace of reduction eased to the weakest since last September. The rest of the EMU continued to outperform, seeing a further modest expansion of output, the thirteenth increase in a row. Details showed new orders decreasing, but at the smallest degree since August while international export orders are still in dire straits. Signs of improvement in activity led to a near-stabilisation of employment. The fastest increase in workforce numbers in the service sector for six months was almost sufficient to cancel out a marked reduction in manufacturing employment. Meanwhile, input costs rose sharply, with the rate of inflation hitting a 21- month high. In turn, companies also increased their selling prices at a sharper pace. Ahead of next week’s ECB meeting, the latter isn’t encouraging in light of the ongoing rate cut cycle. Finally, companies remained optimistic that output will increase over the coming year. European bonds sold off after PMI’s with the curve bear flattening. EU swap rates rose by 5.5 bps (2-yr) to 2.3 bps (30-yr). EUR/USD temporarily pushed from 1.0450 to beyond 1.05, but failed to cling to those levels. The overnight move from 1.04 to 1.0450 was triggered by USD-weakness after US President Trump threatened Fed chair Powell a first time into lowering rates. European stock markets extend their bullish run.

News & Views

UK January PMIs pointed “to a stagflationary environment which poses a growing policy quandary for the Bank of England”, S&P Global’s chief economist said in a sobering comment. While having improved on face value – the composite PMI picked up from 50.4 to 50.9 – it was only slightly above the 50 no-change level and well below the series long-run average of 53.6. The marginal improvement came on the account of a smaller contraction in the manufacturing industry (48.2 vs 47), in turn the result of output still declining but at a markedly slower pace since December. Services stabilized at 51.2. Orders books shrank for the fourth month in manufacturing and for the first time in 15 months in the services sector. The latter also outpaced manufacturing in shedding jobs. Companies blamed the forthcoming hike in employer’s National Insurance as well as the impact of a post-Budget slump in business confidence as reasons for staff cutbacks. Businesses reported a sharp and accelerated increase in overall cost burdens at the fastest rate in 1.5 years amid higher salary payments, energy costs and priced paid for imported raw materials. Prices charged to end-consumers rose the quickest since July 2023. Activity expectations weakened for a sixth month straight to the lowest since December 2022, posing downside economic reasons. Reasons stretched from unfavourable UK economic prospects, higher employment costs and a Budget-related tumble in investment spending plans. UK money markets pared their Bank of England easing bets after today’s PMIs. That’s offering the pound a lifeline against the likes of the euro. EUR/GBP trades unchanged around 0.843.

German newspaper Handelsblatt citing officials reported the government has lowered its 2025 forecast from 1.1% to just 0.3% amid signs of the economy showing little signs of recovering. Three leading German economic forecasters already projected growth rates between zero and 0.4% back in December. Europe’s largest economy shrank by 0.2% last year, posting a second straight yearly decline. The economy has shown up being the top concern of voters ahead of a national election on February 2023. The CDU/CSU is still having a comfortable but declining lead over other parties. It recently slipped below the 30% threshold with voters switching to the far-right AfD (22%) instead. Former government coalition parties SPD (socialists) and the Greens fluctuate around >15% and +/- 13% respectively. The liberals, whose opposition to break up the debt ceiling triggered the government collapse, flirt with 5%.

Elliott Wave Forecast: GOLD (XAUUSD) Forming 5 Waves from the 2656.3 Low

Hello fellow traders! In this technical article, we’ll be discussing GOLD (XAUUSD) and sharing some charts that we’ve presented to the members of ElliottWave-Forecast.

As our members know, GOLD is showing higher high sequences in the cycle from the December 18th low, which suggests a further rally in the commodity. Recently, GOLD completed a 3-wave pullback and made another leg up, reaching our target area. In the following text, we’ll take a closer look at the Elliott Wave count and explain how to find targets for wave (v).

GOLD (XAUUSD) H1 Update 01.23.2025

The commodity is forming a 5-wave pattern in the cycle from the 2656.3 low. We can already count 3 waves down, labeled as abc red. The current view suggests that as long as the price remains above the 2735.8 low, the (iv) blue pullback is considered complete. We believe (v) blue is now in progress, with the first target area projected at 2769.99–2708.55.

GOLD (XAUUSD) H1 Update 01.23.2025

GOLD continued its rally as expected. Wave (v) reached the first target at 2769.99–2708.55, calculated using the inverse 1.236–1.618 Fibonacci extension of wave (iv). Another method to project the target for wave (v) is (v) = (i), which comes at 2804.4. We expect the cycle from the 2656.6 low to soon complete as a 5-wave structure ((i) )black and anticipate a pullback in ((ii)). However, we do not recommend selling against the primary bullish trend. Once the ((ii)) pullback begins, we expect it to reach around the 50–61.8 Fibonacci retracement area measured from the 2656.6 low.

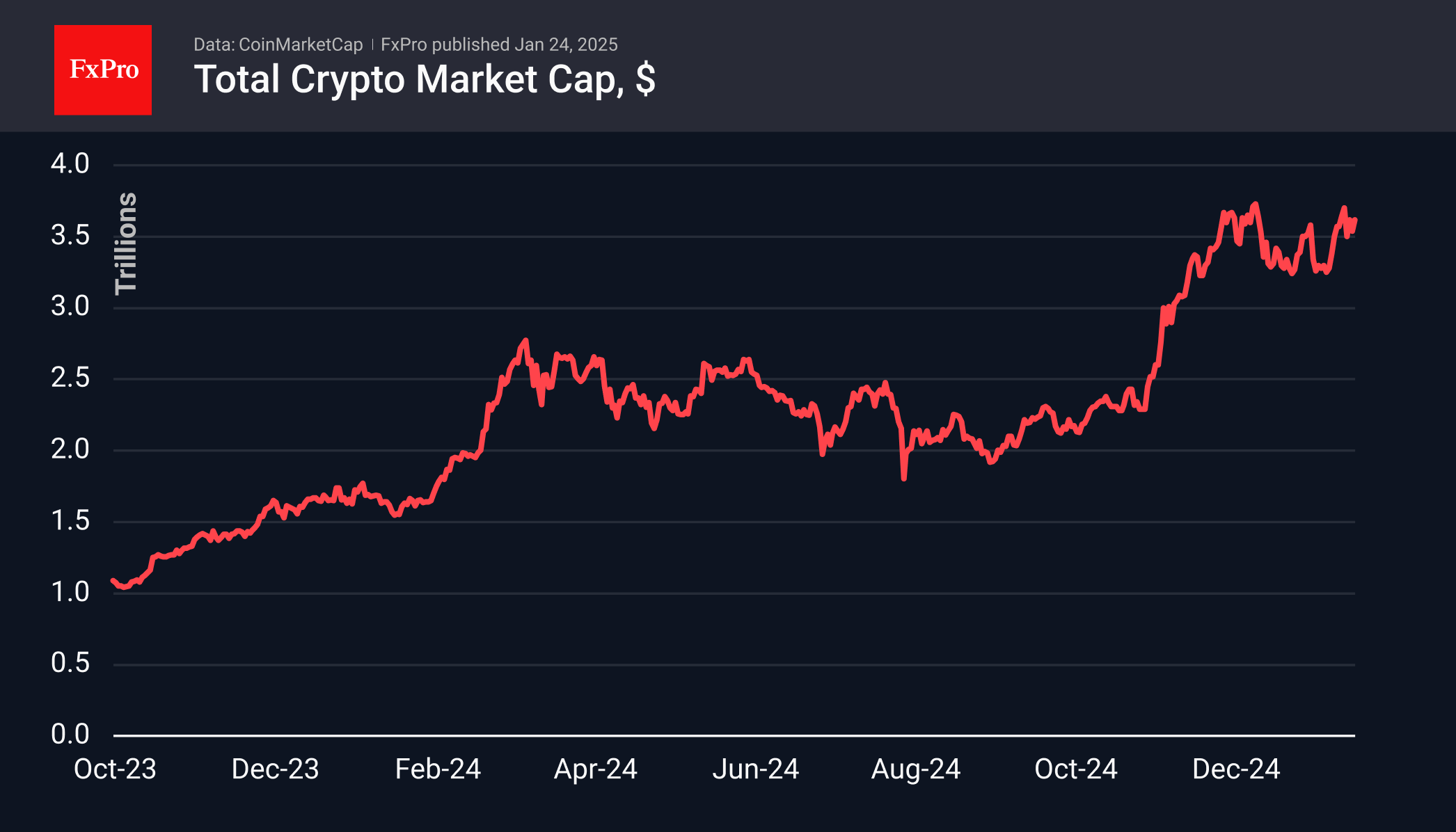

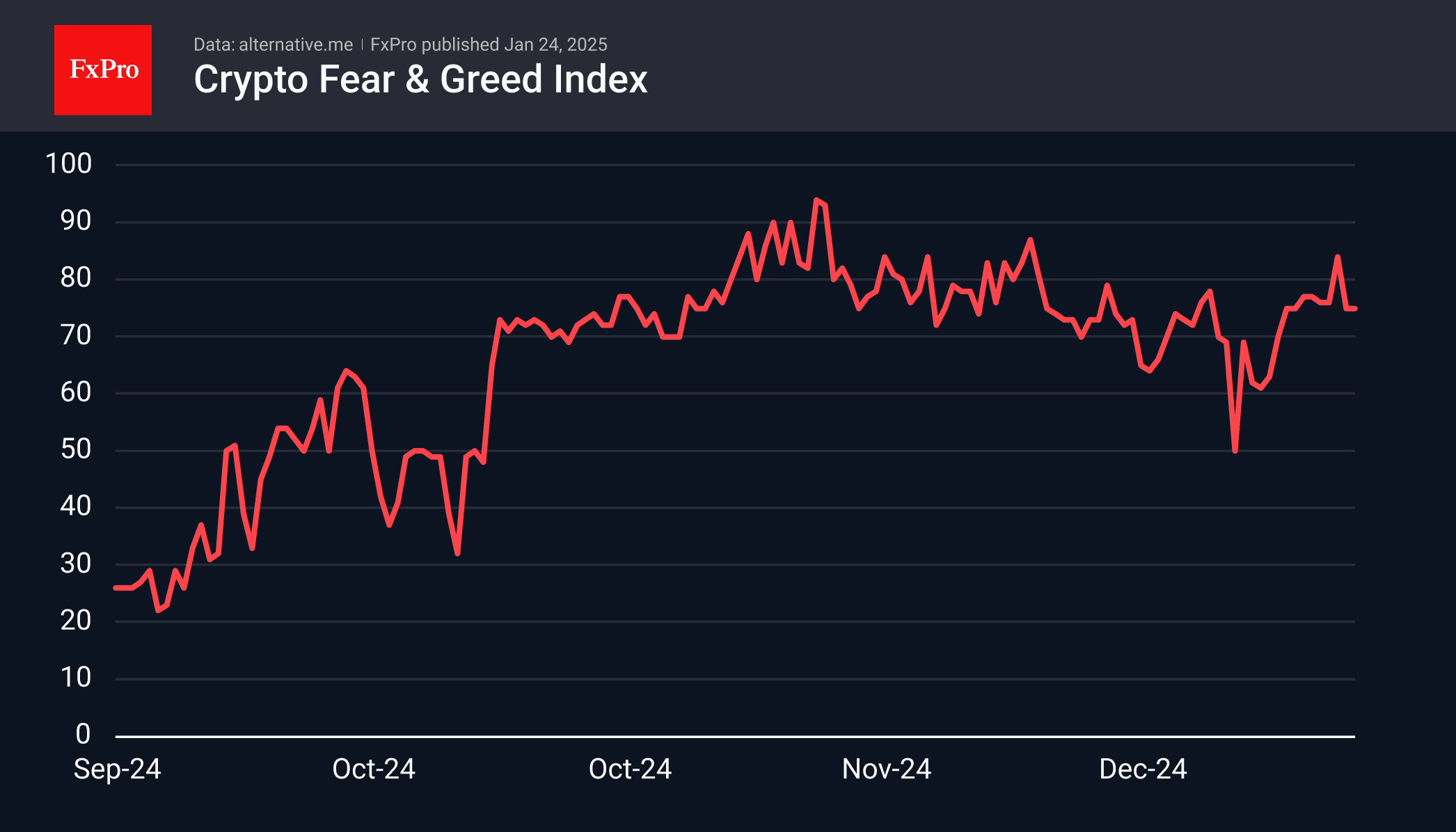

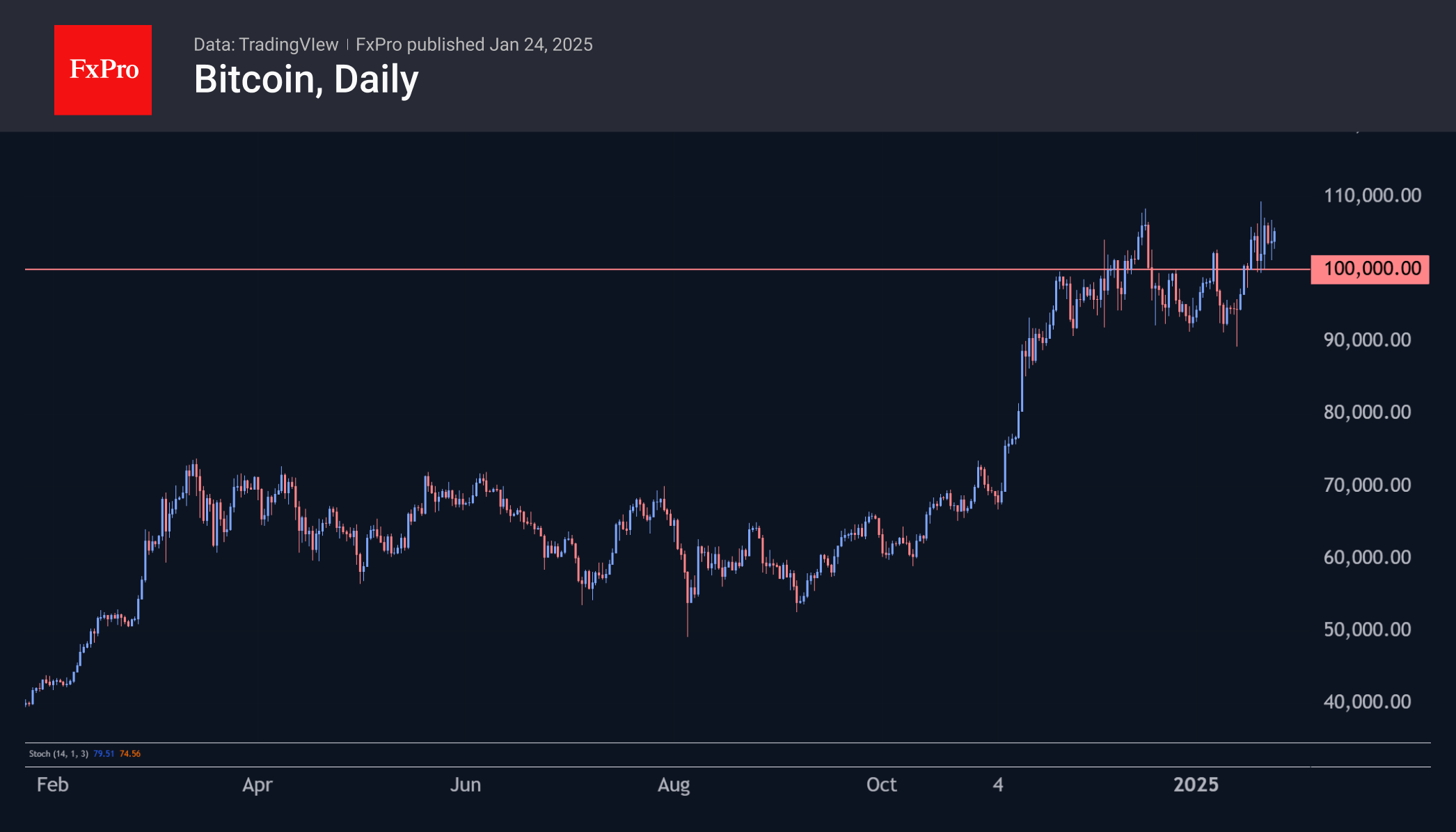

Crypto Market Has Increased Volatility

Market Picture

In the outgoing week, Bitcoin updated an all-time high, approaching a price of $110K and dragging the entire crypto market up with it. On Friday morning, capitalisation is moving up again, settling above $3.63 trillion. The market needs time to adjust to the current highs, and so far, there are more signs that this is a pause before further growth rather than the market hitting impenetrable resistance.

That said, the sentiment index has been cruising in the greed zone, only going to extreme greed once. As was the case in mid-December, high sentiment index values intensified the selling.

Bitcoin fell below $100K during the week, then approached $110K before gently re-emerging at 102K. The selling intensified on the approach to the peak of $110K in December and in January.

However, support has also shifted above $100K, meaning market participants are now getting used to a six-figure price. Additionally, the market continues to bounce around mentions of Bitcoin and cryptocurrency reserves by Washington officials, which adds volatility but doesn’t help with direction.

News Background

If investors of all categories, from private to institutional, decide to allocate between 2% and 5% of their portfolios to the first cryptocurrency, its value could reach the $700,000 mark, BlackRock CEO Larry Fink said.

Goldman Sachs CEO David Solomon commented that Bitcoin does not threaten the dollar’s status as a reserve currency, remaining a speculative asset. From a regulatory perspective, he said, the bank still cannot own and transact in the first cryptocurrency.

Trading in XRP and SOL futures on the CME could begin on 10 February if approved by regulators. Such information appeared on a subdomain of the CME Group platform. A spokesperson for the exchange said that the beta version of the website was in the public domain ‘by mistake,’ and no decision has yet been made to launch the contracts.

Investment firm Bitwise has filed an application to register the Dogecoin-based ETF (DOGE) with the Delaware (US) Department of State’s Division of Corporations. Decrypt notes that asset managers typically register legal entities with the state before filing formal applications with the SEC.

Member of the US House of Representatives Gerald Connolly called for an investigation into possible conflicts of interest in connection with cryptocurrency projects of Donald Trump. In his opinion, it potentially violates ethical norms and creates risks to national security.

BoJ Hikes Rates, Yen Pares Gains

The Japanese yen gained as much as 0.8% earlier today but has failed to consolidate these gains. In the European session, USD/JPY is trading at 156.03, dwon 0.02% on the day.

BoJ raises rates to highest since 2008

The Bank of Japan hiked its policy rate by 25 basis points earlier today, as expected. This brings the policy rate to 0.5%, its highest level since October 2008, during the global financial crisis. The Japanese yen climbed sharply after the decision but was unable to consolidate these gains.

The BoJ has been signaling that it planned to raise rates at today’s meeting, although the BoJ tends to surprise the markets and a rate hike, while expected, was not a given. The BoJ statement expressed hope that this year’s wage negotiations would result in strong wage increases, as was the case last year. Governor Ueda has said in the past that he would raise rates provided that inflation was driven by higher wages, which would show that inflation was sustainable. Wage growth has been moving higher and this resulted in today’s rate hike.

Japan’s inflation rate has been moving higher and the December inflation report, which came out today, showed core CPI climbed to 3%, up from 2.7% in November and in line with the market estimate. The core rate has hovered above the BoJ’s 2% target for 2.5 years and at today’s meeting, the BoJ upgraded its inflation outlook to above 2% until 2026.

Predictably, Governor Ueda didn’t provide a timeline for the next rate hike at his post-meeting press conference, but a May rate hike is on the table if the wage negotiations result in higher wages and inflation does not weaken unexpectedly. Another key factor in the timing of the next rate hike will be President Trump’s trade policy. Trump had promised to levy tariffs on US trading partners on his first day in office but has delayed the tariffs until at least Feb. 1. The BoJ will want to see which direction Trump’s trade policy is going before raising rates again.

USD/JPY Technical

- There is support at 154.78 and 153.27

- 156.49 and 158.00 are the next resistance lines

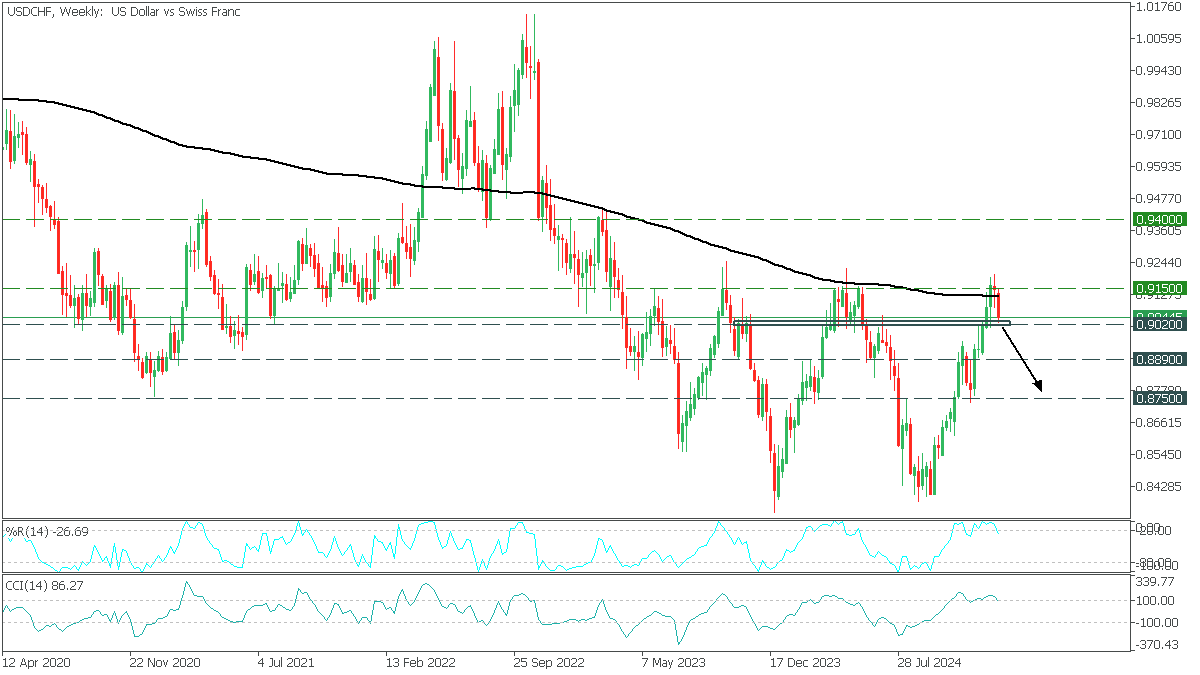

USDCHF: Another Fall?

USDCHF, Weekly

In the Weekly timeframe, USDCHF formed a triple-top pattern. The price bounced again from the critical resistance and MA200. The CCI and %R are out of the overbought zone, also confirming the possibility of a fall.

- We can consider selling USDCHF only in case of consolidation below 0.9020 with the target to 0.8890 and further to 0.8750;

GBPUSD Lifted by Strong Data, But More Work at the Upside Needed to Verify Positive Signal

Cable rose further on Friday, following better than expected UK PMI data, while the near term action remains underpinned by weaker dollar.

Fresh strength cracked daily Kijun-sen (1.2414) and approached next barrier at 1.2455 (50% retracement of 1.2811/1.2099 bear-leg) but started to face headwinds here.

Potential risk of recovery stall is presented by overbought stochastic and 14-d momentum remaining in negative territory, although bias expected to remain with bulls while the price stays above broken 20DMA (1.2354, former significant barrier, reverted to support).

On the other hand, more optimistic outlook could be seen on weekly chart, where a reversal pattern has formed, keeping in play hopes for further recovery.

In such scenario, weekly close above broken Fibo resistance at 1.2371 (38.2% of 1.2811/1.2099) will be a minimum requirement to keep fresh bulls in play, with lift above 1.2455 (50% retracement) and 1.2500 (psychological / 10WMA) to verify signal.

Fundamentals may not work in favor of pound, as BOE is likely to cut rates next month, but elevated inflation and soft data from labor sector would further harm the outlook.

Res: 1.2455; 1.2500; 1.2539; 1.2557

Sup: 1.2371; 1.2354; 1.2280; 1.2229

Japanese Yen Strengthens as Interest Rate Reaches Highest Level Since 2008

The USD/JPY pair declined to 155.13 on Friday, as the yen gained robust support following the Bank of Japan’s (BoJ) decision to raise its interest rate during the January meeting.

BoJ’s interest rate hike and economic outlook

The BoJ increased the cost of borrowing by 25 basis points, bringing the benchmark interest rate to 0.5% per annum. This marks the highest rate in Japan since the 2008 global financial crisis, with monetary policymakers voting 8 to 1 in favour of the decision.

The central bank views Japan’s economic recovery as moderate and aligned with forecasts, estimating potential GDP growth at 0.5%. Additionally, the BoJ noted encouraging signs from companies, with many planning to offer substantial wage increases during spring negotiations. This development is seen as a positive factor for stabilising inflation, which remains a key focus for the BoJ.

However, the central bank expressed concern about rising import prices caused by the weak yen and increasing rice prices. Despite the interest rate hike, real rates in Japan remain deeply negative; however, conditions seem favourable for a shift into positive territory.

The BoJ is expected to maintain the current interest rate at its March meeting. For now, the central bank has fulfilled its immediate goals, and policymakers will assess the impact of higher borrowing costs on the economy.

Technical analysis of USD/JPY

On the H4 chart, USD/JPY experienced a pullback from 156.56 and continues to develop a downward wave targeting 154.20. After reaching this level, there is potential for a corrective growth wave back to 156.56. The MACD indicator supports this scenario, with its signal line below the zero mark and sharply downwards, confirming the bearish momentum.

On the H1 chart, the pair is currently in the middle of a fifth wave of decline, with a target of 154.20. The market is forming a compact consolidation range near 155.55. A downward breakout from this range would likely lead to further declines to 154.20. After reaching this level, a corrective wave to 156.56 (a test from below) is possible. Looking further ahead, the development of a continued downward wave towards 153.20 is also possible. The Stochastic oscillator supports this view, with its signal line below 20 and pointing strongly downwards, reinforcing expectations of further bearish movement.

Conclusion

The Bank of Japan’s interest rate hike has provided substantial support to the yen, with USD/JPY trending lower as the market absorbs the decision. While the BoJ is expected to hold rates steady in the near term, its actions have set the stage for further currency strength. Technically, the pair remains in a downtrend, with immediate targets at 154.20 and 153.20. Investors will closely monitor Japan’s inflation dynamics, wage negotiations, and import price trends for additional cues on the yen’s trajectory.

USD/JPY: Japanese Yen Fails to Benefit More from BoJ Rate Hike

USDJPY dipped early Friday on widely expected BoJ rate hike by 25 basis points, but the weakness was so far short-lived, despite interest rate rising to the highest in 17 years.

Subsequent bounce (approx. 100 pips) suggests that the dollar remains well supported, particularly by wide gap between the monetary policies of Fed and BoJ.

Repeated failure at pivotal Fibo support at 154.97 (38.2% retracement of 148.64/158.87, reinforced by nearby 55DMA and trendline support) where a higher base is forming (still needs confirmation) signals that the pair lacks strength for final break lower.

Near-term action remains within the narrow range for the seventh consecutive day, still looking for direction signal after BoJ’s decision proved to be insufficient to spark stronger move lower.

Formation of bear trap pattern on daily chart adds to initial positive signal which would require more work at the upside to be confirmed (close above rent range top at 156.75 and 20 DMA at 156.94 to verify completion of higher base).

Alternative scenario would see firm break of Fibo support, 55 DMA and trendline support (154.97/50 zone) as strong negative signal, pointing to continuation of pullback from a multi-month peak (157.87).

Technical studies on daily chart remain mixed and lack clearer signal, though overall picture is still firmly bullish, suggesting that limited correction would precede fresh push higher.

Res: 156.46; 156.75; 156.94; 158.08

Sup: 154.97; 154.76; 154.50; 153.76

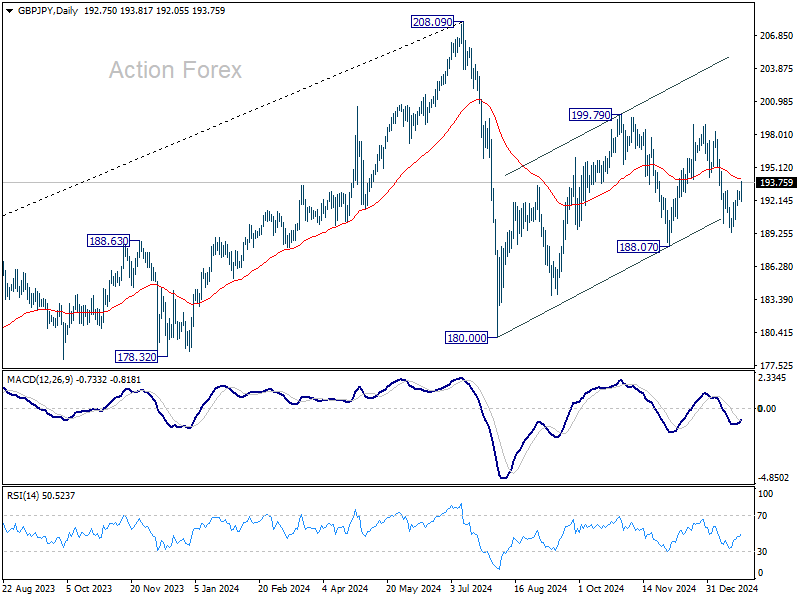

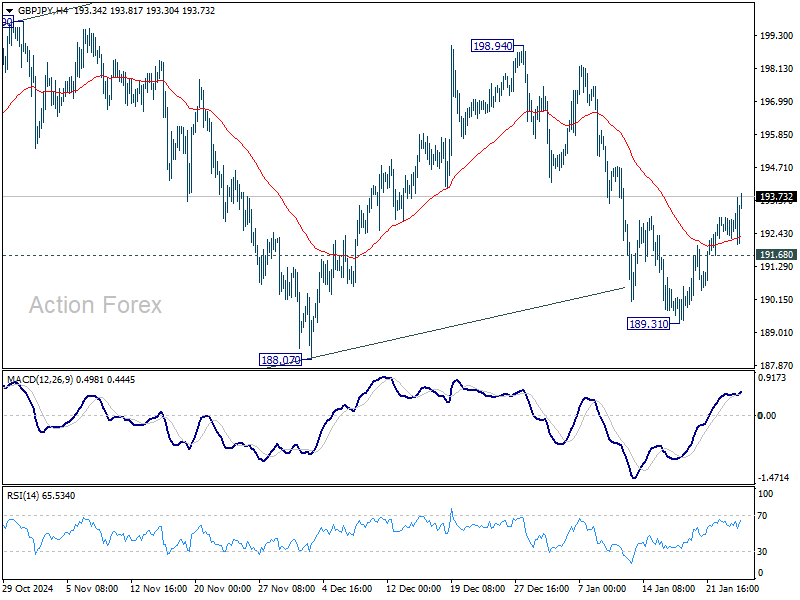

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.37; (P) 192.70; (R1) 193.11; More...

GBP/JPY's break of 193.01 resistance argues that fall from 198.94 might have completed, ahead of 188.07 support. Corrective pattern from 180.00 is probably extending with another rising leg. Intraday bias is back on the upside for 198.94/197.79 resistance zone. On the downside, below 191.68 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.