Sample Category Title

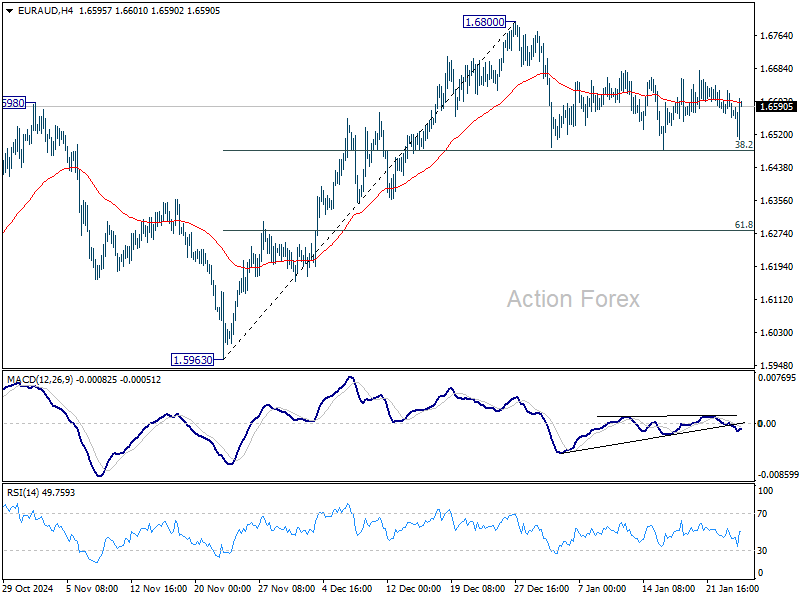

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6550; (P) 1.6590; (R1) 1.6615; More...

No change in EUR/AUD's outlook as it;s still bounded in consolidation below 1.6800. Strong support is still expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9432; (P) 0.9445; (R1) 0.9465; More....

EUR/CHF's rebound from 0.9204 is in reacceleration as seen in 4H MACD breaks through 0.9481 fibonacci resistance. Intraday bias stays on the upside for the moment. Sustained trading above 0.9481 will pave the way to 0.9651 fibonacci level. For now, further rally would remain in favor as long as 0.9424 support holds, in case of retreat.

In the bigger picture, considering bullish convergence condition in D MACD, a medium term bottom could be in place at 0.9204, after defending 0.9209 support. Sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 will pave the way to 61.8% retracement at 0.9651, either as trend reversal or just a correction to fall from 0.9228. This will be the favored case as long as 55 D EMA (now at 0.9385) holds.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4341; (P) 1.4378; (R1) 1.4421; More...

USD/CAD is still bounded in range trading below 1.4516 and intraday bias remains neutral. Further rise is expected as long as 1.4260 support holds. Break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4215) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

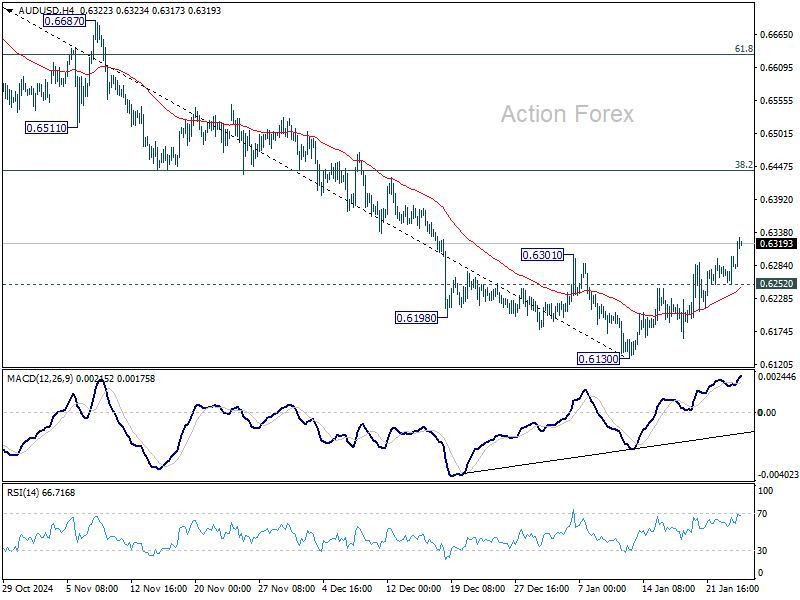

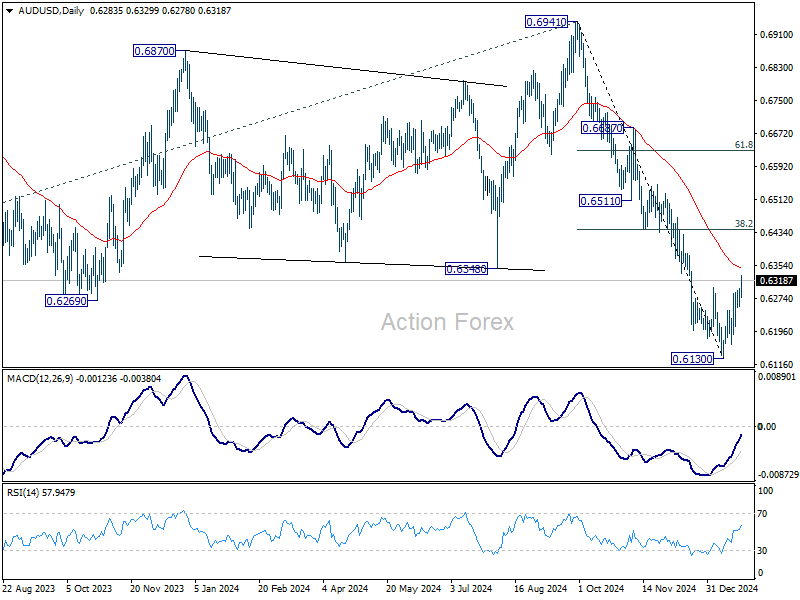

AUD/USD Daily Report

Daily Pivots: (S1) 0.6259; (P) 0.6280; (R1) 0.6304; More...

AUD/USD's rally from 0.6130 extended with break of 0.6301 resistance. Intraday bias is back on the upside for 55 D EMA (now at 0.6352), and possibly above. But strong resistance should be seen from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside. On the downside, break of 0.6252 minor support will bring retest of 0.6130 low instead.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

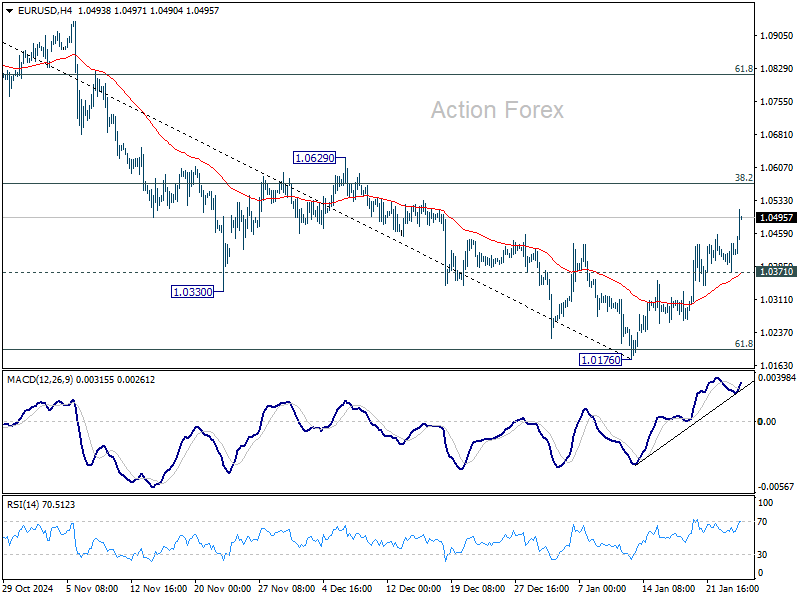

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0379; (P) 1.0409; (R1) 1.0445; More...

Intraday bias in EUR/USD is back on the upside as rebound from 1.0176 resumed by breaking through 1.0435 resistance. Strong resistance might be seen from 38.2% retracement of 1.1213 to 1.0176 at 1.0572 to limit upside. Break of 1.0371 minor support will bring retest of 1.0176 low. However, sustained break of 1.0572 will raise and chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

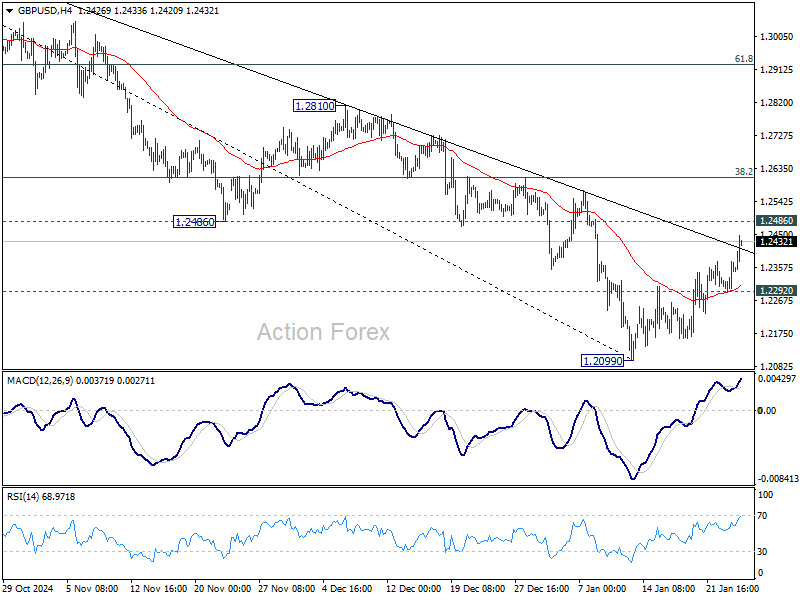

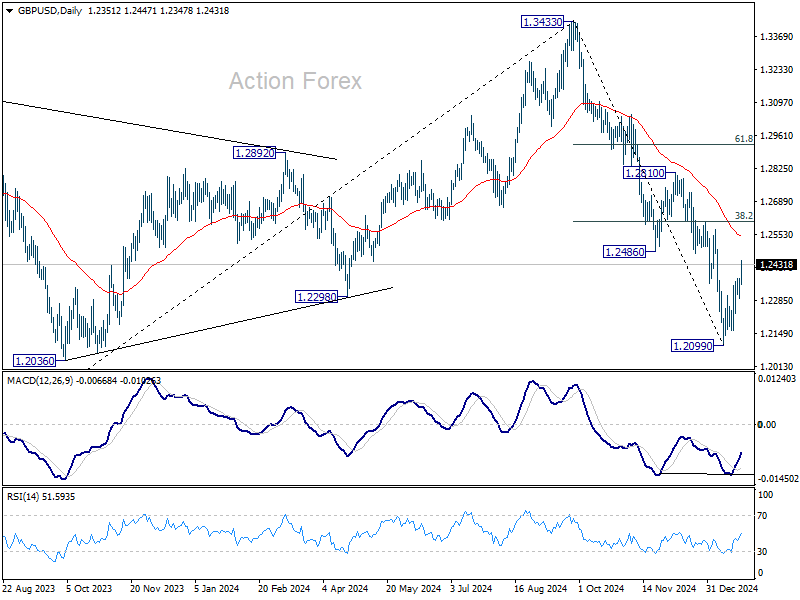

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2305; (P) 1.2340; (R1) 1.2388; More...

GBP/USD's recovery from 1.2099 extended higher but upside is still capped below 1.2486 support turned resistance. Intraday bias remains neutral and further decline is in favor. On the downside, below 1.2292 minor support will turn bias back to the downside for retesting 1.2099 low. However, firm break of 1.2486 will bring stronger rebound towards 1.2810 resistance instead.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

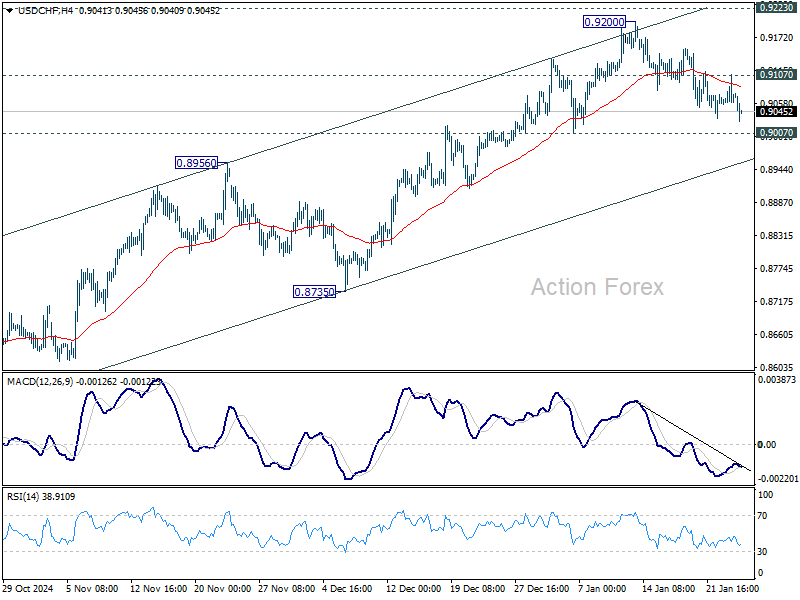

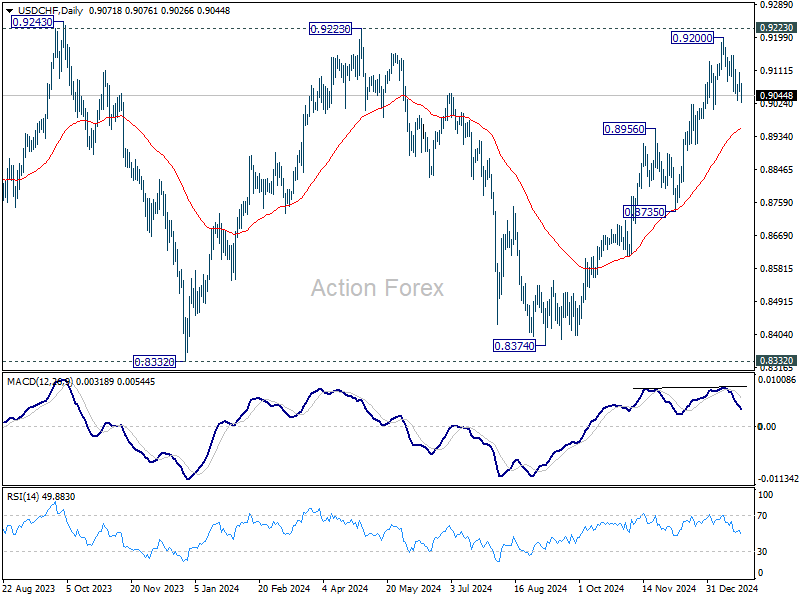

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9051; (P) 0.9080; (R1) 0.9103; More…

While USD/CHF pull back from 0.9200 extends lower, downside is still contained above 0.9007 support. Intraday bias remains neutral and further rise is in favor. Above 0.9107 minor resistance will turn bias back to the upside for retesting 0.9200 and 0.9223 key resistance. However, firm break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8954) and possibly below.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

UK PMI composite edges higher to 50.9, but stagflation risks cloud economic outlook

UK PMI Composite rose slightly from 50.4 to 50.9 in January, indicating marginal growth. Manufacturing PMI improved from 47.0 to 48.2, while services PMI ticked up from 51.1 to 51.2. Despite these increases, the overall outlook remains gloomy, with underlying concerns about economic weakness and inflationary pressures persisting.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, warned that the data "add to the gloom" surrounding the UK economy.

Companies are cutting jobs at the fastest rate since the global financial crisis in 2009, reflecting falling sales and bleak business prospects. Business optimism remains at its lowest levels in two years, accompanied by subdued activity across sectors.

Inflationary pressures have also "reignited," creating what Williamson described as a "stagflationary environment" and a "policy quandary" for BoE.

Eurozone PMI composite hits 50.2 as Germany returns to growth

Eurozone PMI data for January showed cautious improvement, with PMI Composite rising from 49.6 to 50.2, a five-month high, signaling a return to marginal growth. Manufacturing PMI increased to 46.1, its highest in eight months, while services PMI slipped slightly to 51.4 but remained in expansion.

Germany led the improvement, with its PMI Composite climbing from 48.0 to 50.1, marking a seven-month high and a return to expansionary territory. Meanwhile, France lagged behind, with its PMI Composite increasing to 48.3 but remaining below the 50 threshold, indicating continued contraction.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the data as "mildly encouraging." He noted that the private sector had entered a phase of cautious growth, with reduced drag from manufacturing and moderate expansion in services. Germany’s strong rebound played a key role in offsetting the continued weakness in France.

Inflationary pressures, however, remain a concern ahead of next week’s ECB meeting. Input prices in manufacturing rose for the first time in four months, driven by a weaker euro and Germany’s increased CO2 tax. In the services sector, cost inflation persisted, largely due to higher wages. Selling prices in services also remained elevated.

Due to persistent inflation risks and the fragile state of the economy, ECB is likely stick to its gradual pace of cutting interest rates.

Bank of Japan Raises Rates, Yen Strengthens

The Bank of Japan (BOJ) has raised short-term interest rates to 0.5%, the highest level in 17 years. While this move was anticipated, the currency market responded with a significant strengthening of the yen, with USD/JPY falling by approximately 0.6%.

At a press conference, BOJ Governor Ueda stated that there is no predetermined course for future rate adjustments. Meanwhile, media reports cite analysts’ opinions suggesting that the rate could be raised again before the end of 2025.

Technical analysis of the USD/JPY chart shows the formation of a descending channel (highlighted in red) at the start of 2025. The news of the rate hike enabled bears to launch another attack on the psychological level of 155 yen per dollar—a level that had previously served as support earlier this month. As of the morning of 24 January, bulls are managing to defend this level, but how long can they hold out if bearish pressure persists?

Key points to note:

→ The USD/JPY trend resembles a rounding-top pattern.

→ The yen's strength is also supported by the dollar’s weakness, influenced by some uncertainty surrounding the introduction of international trade tariffs promised by US President Trump.

Today, at 17:45 GMT+3, the Purchasing Managers' Index (PMI) figures will be released, potentially triggering heightened volatility in financial markets.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.