Sample Category Title

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.35% against the USD and closed at 1.2830.

On the macro front, UK's public sector net borrowing posted a more-than-expected deficit of £4.4 billion in March, after recording a revised surplus of £0.7 billion in the previous month, whereas markets were expecting a deficit of £1.5 billion.

In the Asian session, at GMT0300, the pair is trading at 1.2840, with the GBP trading 0.08% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2794, and a fall through could take it to the next support level of 1.2749. The pair is expected to find its first resistance at 1.2865, and a rise through could take it to the next resistance level of 1.2891.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese All Industry Activity Index Advanced In February

For the 24 hours to 23:00 GMT, the USD rose 1.05% against the JPY and closed at 110.96.

In the Asian session, at GMT0300, the pair is trading at 111.23, with the USD trading 0.24% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's all industry activity index rose more-than-anticipated by 0.7% MoM in February, compared to an advance of 0.1% in the prior month. Markets were expecting the index to rise 0.6%.

The pair is expected to find support at 110.26, and a fall through could take it to the next support level of 109.28. The pair is expected to find its first resistance at 111.79, and a rise through could take it to the next resistance level of 112.34.

Looking ahead, investors will concentrate on Bank of Japan's (BoJ) interest rate decision, due to be announced tomorrow.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Extends Its Gains, Ahead Of Switzerland’s ZEW Expectations Data

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the CHF and closed at 0.9933.

In the Asian session, at GMT0300, the pair is trading at 0.9923, with the USD trading 0.1% lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9904, and a fall through could take it to the next support level of 0.9884. The pair is expected to find its first resistance at 0.9956, and a rise through could take it to the next resistance level of 0.9988.

Ahead in the day, market participants will look forward to Switzerland's ZEW expectations index for April and UBS consumption indicator for March.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Higher, Ahead Of Canada’s Retail Sales Data

For the 24 hours to 23:00 GMT, the USD rose 0.43% against the CAD and closed at 1.3572.

In the Asian session, at GMT0300, the pair is trading at 1.3568, with the USD trading slightly lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3531, and a fall through could take it to the next support level of 1.3495. The pair is expected to find its first resistance at 1.3615, and a rise through could take it to the next resistance level of 1.3663.

Moving ahead, Canada's retail sales data for February, scheduled to release later in the day, will keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

BoJ Report Setting The Dollar Yen Up For A Tumble

Key Points:

- Technical bias signals a reversal could be on the cards.

- BoJ announcements are the key risk event to keep in mind.

- An upwards revision of GDP forecasts could spark a slip.

In light of the fact that the BoJ is going to be thrusting the Yen centre stage in the next 24 hours as a result of its interest rate announcement, it's worth taking a closer look at the USDJPY and what is likely to be on cards moving ahead. In particular, we should be cognisant of the current technical bias and how it will influence the pair's performance given the expectations of the BoJ's impending reports.

Starting with our technical bias, there is a fairly clear picture being painted on the daily chart which suggests a reversal to the downside is warranted. Specifically, even given the sizable rally seen in the prior session, buying pressure failed to push the pair above the 100 day moving average which provides a strong indication that we may have reached a near-term peak. Moreover, both the 12 and 20 day averages are in a bearish configuration which can only add to downside risks for the day to come.

Furthermore, if we take a closer look at some other technical instruments, the likelihood of an imminent slip seems rather substantial. For one, the zone of resistance that the Dollar Yen is currently struggling against falls in line with the 50.0% Fibonacci retracement which is acting as an effective cap on additional gains. In addition to this, the stochastics are moving into oversold territory which suggests that the bulls are exhausted and about to be slapped lower.

From a fundamental perspective, it may be somewhat counterintuitive to expect the Yen to strengthen materially against the USD given the likely content of the BoJ's policy statement and outlook report. The widely recognised inability of the bank to hit its 2% inflation target will almost certainly be reinforcedby the releases which should lead to some modest selling, even though much of this negative sentiment has already been priced in. However, what will likely be of greater interest will be the BoJ's GDP forecast for the coming fiscal year. Indeed, the 1.5% forecast is expected to be revised upwards, in line with the IMF and OECD revisions seen earlier in the year.

In the event we do see a GDP forecast in excess of 1.5%, buying pressure for the Yen should kick in which will drag the USDJPY lower in agreement with the already discussed technical bias. As a result, losses could see the pair as low as 106.86 within a few weeks as the next stage of the descending channel takes hold. Alternatively, if the forecast remains grim, we could see a near-term spike which could bring the pair to the upside of the channel before long-term bearishness resumes.

Ultimately, the outcome of the impending session is likely to come down to what the market weights more heavily out of the inflation or GDP expectations. However, at present, it appears that the GDP data is going to be the only new information injected into the situation which would usually make it the preeminent risk event for the day.

Aussie Dollar Sets Up In A Corrective Structure

Key Points:

- Price action constrained within a tightening wedge formation.

- RSI Oscillator nearing oversold levels.

- Watch for a move back above 0.7600 before a recommencement of the down trend.

The Aussie Dollar has had a relatively rough week to date as the pair has reacted to a range of wildly swinging sentiment around the USD, as well as a disappointing CPI result. This has provided the conditions for a fairly steady depreciation which has seen price action currently trading around the 0.7519 mark. However, despite the pair's relatively clear corrective structure (4-hr timeframe) there are some indications that we might be seeing the early stages of a turnaround.

Fundamentally, it was always going to be a rough week for the commodity exposed pair given the machinations exiting the Trump white house. It was therefore no surprise that the announcement of a new corporate tax plan would boost the greenback's sentiment. Additionally, the market was also looking for a relatively strong Australian inflation result, yet instead they received a slip to 0.5% q/q. So the fundamental downside pressure was always going to arrive. However, it would appear that the defining factors are likely to be technical in nature over the next 24 hours.

In particular, a cursory review of the charts clearly shows the rising trend line that is currently supporting price action. Subsequently, the lows are getting higher in a sign that should provide plenty of comfort to the bulls. Additionally, both the RSI Oscillator and the ADX are plumbing relatively low levels, with the RSI nearing oversold territory.

Subsequently, there are plenty of reasons to suspect that the Aussie Dollar is about to rally especially considering that, between the higher lows and lower highs we have a wedge formation in play. Given the aforementioned factors, we are likely to see a short term move back towards the 0.7630 mark. However, it is likely that this level could prove a turning point and lead to a continuation move to recommence the depreciation against the greenback.

Ultimately, any upside move is likely to only be a short term one before the pair recommences its steady decline. The technical indicators are relatively clear in the short term given the squeezing that is currently occurring. Subsequently, keep a keen eye out for a break above the top of the constraining wedge as this is likely to signal the start of the short term move back above the 0.76 handle and towards the 0.7630 mark.

Market Morning Briefing: The Markets Wait For Trump To Introduce A New Tax Plan Today

STOCKS

The US markets are up ahead of the Tax reform statement from Trump today. Dow (20996.12, +1.12%) looks bullish and could head towards 21200 in the near term. Markets await to see what tax reforms would be done and how and when this would play out.

Dax (12467.04, +0.10%) continues to sustain above 12390 but is close to an immediate resistance near 12532. Only a break above 12532 could bring in further upside and indicate a fresh bull move; else a sharp recovery from 12532 is possible in the near term.

Shanghai (3149.19, +0.47%) is trying to rise from levels above 3100 and if it sustains we could see a recovery towards 3175. Else some sideways consolidation in the 3150-3100 is possible in the near term.

Nikkei (19231.92, +0.80%) is headed towards 19620 in quick succession as Dollar-Yen continues to move up sharply. While there could be some scope of a rise in Dollar-Yen towards 112, Nikkei could be bullish for the coming sessions.

Nifty (9306.60, +0.96%) closed above 9300 in line with our expectation and could face crucial resistance within the 9300-9400 region. This could be a near term top and a sharp fall towards 9100 could follow soon.

COMMODITIES

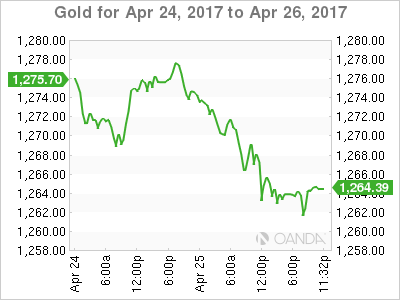

As mentioned earlier, we see chances of a corrective decline in Gold (1265) that can target 1260-65 at least. Our preferred scenario that the support at 1260-65 will hold is continuing to work well enough for now. The Support region may be expanded to 1239. At the same time, the Resistance at 1305 also looks strong in the near term. As such, we may see some more sideways movement between 1239-1305 early next week.

Silver (17.59) is Oversold on the near-term charts and while the market remains above 17.39, there will be chances of an eventual bounce that can break above 17.80. If that happens on a closing basis, a further rise to 18.33 may be seen swiftly.

Copper (2.57) has been stuck in the range of 2.50-2.67. A close below 2.50 could open up 2.48 and 2.45 levels respectively. Only above 2.67, higher resistances of 2.72 -80 can come into consideration. The bias would remain bearish while it is trading below 2.70-72 levels.

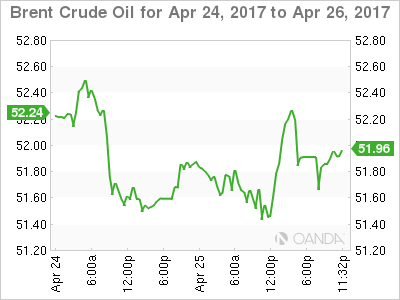

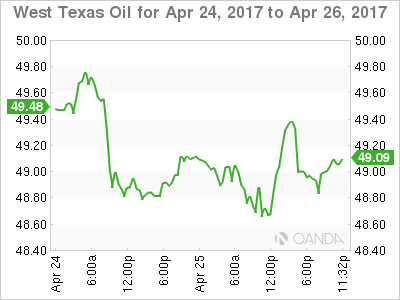

Brent (51.96) is trading within the range of 50-52 while WTI (49.41) is hovering around at our preferred supports of 48.80 levels. If these two rise further due to their near term oversold condition, then 52 levels for Brent and 50.80 levels for WTI would come into consideration .We have U.S Oil inventory data (Forecast: -1.1M Barrels) at 8.00 p.m today, which may add some more clarity towards the price action.

FOREX

The markets wait for Trump to introduce a new tax plan today, cutting the corporate tax to 15% from the existing 35%. Also the BOJ and ECB meet tomorrow can play a crucial role.

Our expectations of a major reversal in Dollar Index (98.78) will be either confirmed or negated within the next 24 hours as the combination of the Trump Tax policy announcement tonight and the ECB meet tomorrow will set the near term path. Chances of a whiplash around the major support of 98.50 before a turnaround can’t be ruled out. While first signal of a bullish rise comes on a break above 99.35, this bullish scenario has to be discarded on a sustained move below 98.50.

Euro (1.0938) is testing the higher resistances of 1.0930-50 contrary to expectations already but it remains to be seen if it manages to rise past and stay above 1.0950. As long as 1.0950 holds, the possibility of a downward correction to 1.07 remains open but on a firm break above 1.0950, the bearish option has to be reconsidered. The picture should be clear by tomorrow.

Pound (1.2840) continues its sideways consolidation in 1.2750-1.2900 with an apparent indifference to the global events and it may remain quiet for the rest of the week too.

Dollar-Yen (111.24) has rallied towards our target of 111.50-112.00 just as expected. Near 112.00 it may stall for a couple of sessions before deciding the next course of action. Immediate support comes at 110.00.

Aussie (0.7515) keeps oscillating in the range of 0.7450-0.7600 as expected but if the interim support of 0.7500 holds today, then a contraction can be seen in the price action which may give birth to a sharp trending move next week, direction unclear at the moment. Wait and watch.

Today’s session is going to be crucial for Dollar-Rupee (64.26). In case the market continues to remain above 64.22-18 AND rises above 64.40, we could be looking at chances of a strong rise in Dollar-Rupee. On the other hand, in case the market breaks below 64.22-18, then a further decline towards 64.00-63.80 may take place. Wait and watch.

INTEREST RATES

The US yields have risen sharply. The 5Yr (1.86%), 10YR (2.34%) and the 30YR (2.99%) are trading higher from 1.83%, 2.31% and 2.95% respectively. Near term looks potentially bullish. The 10Yr could move up towards 2.40% while the 30yr could test 3.0-3.10% in the coming sessions.

The German-US 2Yr (-1.97%) and the 10Yr (-1.96%) have fallen slightly. But we need a confirmed break below -2% to impact the Euro to move on the downside.

The German yields are by themselves heading towards immediate resistance levels and could come off a from there in the early sessions next week.

Crude Oil And Precious Metals Diverge

Crude Oil

Choppy trading in decent ranges was the theme of the overnight session in crude, with both Brent and WTI showing good two-way interest after last week's selloff. When the dust settled though, both contracts closed about 0.50 % higher for the day.

The API's surprise increase in crude inventories and the Russian energy minister wanting more data before committing to a cut extension in June both saw crude under pressure. However, the effect was short-lived, implying that positioning is now much more balanced than it was last week. It gives credence to our theme that the sell-off was driven by excessive short-term speculative longs, rather than a previously unknown structural change in the market.

Both Brent spot and WTI spot remain mired at the bottom of their recent ranges, although the odds have now risen for a short term bounce. Tonight's U.S. EIA Crude Inventories will now be the key to oils direction over the next 48 hours.

Brent spot has support at 51.20 and then 50.80 its 200-day moving average. Resistance lies at 52.50 initially.

WTI spot has support at 48.50, just under its 200-day average at 48.60, with resistance at 50.00.

Precious Metals

Gold

President Trump's tax and economic plans seem to be finally getting some flesh on them, with some detail on corporate tax cuts and the dropping of border tax plans. With diminishing geopolitical tensions and a less itchy tariff finger, this was all adrenaline to the U.S. stock market and greenback, but a sugar crash for gold which fell 17 dollars in the session to 1261.

Extended safe haven long positioning has been the primary driver of gold's rally above 1290 in recent times. But with repeated technical failures above that level and the world an apparently safer place the stage is being set for an apparent technical correction now.

Gold is trading at 1264 in early Asia, just above initial support at 1260. The 200-day moving average lies just below at 1254.35 with the significant longer term support at 1240. A break of the lower level suggests a much larger correction lower from a technical perspective.

Resistance sits at 1277 and 1280 initially, followed by the multi-day highs region around 1295.

Silver

Silver failed at its 200-day moving average at 17.9800 yet again overnight, marking the 3rd failure in a row. In fact Silver had an outside reversal day yesterday, trading above Monday's high before closing below Monday's low, a bearish formation technically. The only bright spot being a hint of bullish divergence with the daily stochastic and RSI.

Silver trades at 17.6230 in early again just above the overnight low at 17.5620 which is now initial support. Behind this, the next support is the 100-day moving average at 17.3790 followed by the 17th March low at 17.2380.

Resistance lies at the 200-DMA at 17.9800, then yesterday's high of 18.0120 and then the April high of 18.6550.

Summary

The charts suggest that the long positioning unwinds in crude oil has run its course for now ahead of tonight's crude inventories. Conversely, the technicals suggest there could be more pain ahead for precious metals as a resurgent dollar and a quieter world undermine the price action in gold and more particulalry silver.

US$ (DXY), Major Bottoming ?

Nearer term $ index outlook :

In the Apr 18th email, once again affirmed the bearish view since the Apr 11th email of declines back to 98.85 (Mar 27th low) and even below. The market has indeed continued lower since, currently testing that 98.85 low. With still no confirmation of even a short term bottom, there is scope for a downside break (see in red on daily chart below). But be warned further such declines may be limited and part of a more major bottoming. In the bigger picture, the view since Jan of at least a few months of wide consolidating, seen as a large correction (wave 4 in the rally from the May 2016 low at 91.90) and with eventual new highs above 103.80 after (within wave 5) remains in place. Note too that lots of support lies just below the 98.85 low at 96.35/60 (falling support line from Feb, base of large wedge-like pattern since Jan, bullish trendline from June 2014) and would be an "ideal" area to form that more important low (see in red on daily chart/2nd chart below). But I do use the term "ideal" as there is still no confirmation of that short term low (and larger bottoms begin with smaller ones) while there is always the potential of a downside acceleration (currently seen as a low risk, but a risk none the less). Nearby resistance is seen at 99.20/35 and the bearish trendline from Apr 10th (currently at 99.75/90). Bottom line : still no confirm of even a short term low, but downside below that 98.85 low may be limited and part of a more major bottoming.

Strategy/position:

Still short from the Apr 11th sell at 100.75. For now with the magnitude of further downside likely limited and part of a more major bottoming, will use an aggressive stop on a close 15 ticks above the multi-day bearish trendline (cur at 99.25/40). This also illustrates the difference between a "view" and a "position". In this case the preferred view is one of limited further downside as part of a potentially more major bottoming. However, there is still no confirmation of even a short term low and there is the potential of a downside acceleration. Though that potential is seen small, remaining short keeps the short position open temporarily while the aggressive stop will quickly get us out if such a downside acceleration does not occur nearby (limited risk).

Long term outlook:

As discussed above, still favor the view that the rangy trade since Jan is a large correction (potential near its completion) and with eventual new highs above 103.80 after. However, such gains above 103.80 (if they do indeed occur) may be limited and part of a more major topping (years ??, see weekly chart/3rd chart below). Lots of long term negatives add to this potential and include negative technicals (see sell mode/bearish divergence on the weekly macd) and the failure to build in the Jan highs above the Mar/Dec 2015 peaks at 100.50/poor upside momentum. Note too that another upleg above 103.80 would be seen as the final upleg in the rally from May 2016 (wave 5) and the final upleg from May 2011 (wave V), while long term resistance lies just above at the ceiling of the multi-year bull channel (currently at 104.75/25). At this point with gains above 103.80 favored, this view of a more major topping is just something to keep in the back of your mind/a longer term risk to be aware of. Bottom line : downside action since Jan seen as a large correction and with an eventual resumption of the longer term gains above 103.80 after (though still no confirmation that the downside is "complete").

Strategy/position:

For now with the market seen in process of a larger bottoming, looking to switch the longer term bias to bullish from neutral. However, with that nearer term scope for further downside/bottoming, would be patient for higher confidence of at least a short term low to switch (larger bottoms begin with smaller ones).

Current:

Near term : short Apr 11th at 100.75, aggressive stop on close 15 ticks above multi-day bear t-line.

Last : short Apr 4 at 100.55, stopped Apr 7 above wk long rising t-line (100.95, closed 101.20).

Longer term : downside from Jan seen as large correction, looking to switch back to bull ahead.

Last: :bull bias Feb 7th at 100.35 to neutral Mar 28th at 99.75.

Every Which Way But Down

There has been a huge shift in momentum for the USD overnight, as the market pivots back to Trump protectionism; Trump tax and fiscal spending updates. So much for the Trump trade being dead and buried, as US 10 year yields moved to 2.34%. Equity markets were euphoric with the NASDAQ breaking 6000 for the first time while gold slipped to 1260 as French election risk and North Korea tensions abate.

What initially started off as a post-French election relief rally has turned into a full-out global equity rally. Despite higher US yields, equity investors were ecstatic about the current market narratives, and Wall Street had a stellar day on the prospect of tax cuts being announced on Wednesday, strong corporate earnings and ongoing relief from the French election results.

On the perpetual market rumor mill, there was an ECB leak that implied no changes this Thursday but a possible adjustment in language at the June meeting. A Reuters story citing “sources” claimed that the ECB would send a signal in June towards a reduction in monetary stimulus. The decline in political risk in France was seen as supporting such a move.

The Tump protectionism play saw a stronger dollar against high yielders and commodity currency as market re-visit the US protectionism theme. Traders are viewing comments from US Commerce Secretary Wilbur Ross that stated a 20% tariff on Canadian softwood lumber imports is likely as a litmus test for Trump Protectionism and dealers were quick to sell off currencies with a significant portion of exports derived from the primary industry.

The Canadian Dollar

After cutting my chops on Bay Street (Toronto Canada), I can assure you the softwood lumber dispute is nothing new and has been making headwinds in one form or another since 1982. While the tariff is not economically damaging for Canada, the unnerve and over reaction on the Dollar Canada desks is likely due to the broader NAFTA and political considerations this move may have.

USDCAD Canadian Dollar Lower After Lumber Tariffs

Australian Dollar

Commodity currencies have come under pressure overnight, probably led by the move higher in USDCAD as the US protectionism theme rears its ugly head. However, the AUD has outperformed the CAD overnight post-Trump Canadian Softwood Tax. While risk sentiment is soaring, and with iron ore off its lows we should expect the Aussie to hold above the .7500 level but with today’s CPI the key local major event dealers are anxiously awaiting the news as it could have far-reaching RBA policy implications.

Japanese Yen

USDJPY was one of the best performers overnight, rallying from low 110s to a high of 111.20. With buoyant risk appetite, higher 10 year US yields and traders intrepidity leading the charge. The play is all about the anticipated Trump tax reform as traders continue to clamor for upside exposure

Euro

Huge uptick in two-way volumes overnight. EURUSD continued to be the main attraction as buying accelerated after the Reuters article suggested the ECB could reduce monetary stimulus in June. Removing the easing bias would be supportive of the Euro and even more so as investment flow seeks out relatively cheap European assets and election hedges should continue to unwind.