Sample Category Title

Market Update – Asian Session: Le Pen – Macron Runoff In France Soothes Concerns Over Eurozone Future

Friday US Session Highlights

(US) APR PRELIMINARY MARKIT MANUFACTURING PMI: 52.8 V 53.8E; new orders: 53.7 v 54.1 prior (lowest since Sept)

(US) MAR EXISTING HOME SALES: 5.71M V 5.60ME

(US) Fed's Kashkari (dove, dissenting vote): next rate move is not as important in the big picture; what matters in the long term is fiscal policy - comments in Minnesota

(US) New York Fed Nowcast: raises Q1 GDP forecast to 2.7% from 2.6% on 4/14; maintains Q2 GDP forecast at 2.1%, unchanged from 4/14

OPEC Committee reportedly finds that oil supply cut agreement compliance improved in March; calls for 6-month extension to output cuts - press

(US) Fed Vice Chairman Fischer: still feels 3 rate hikes is appropriate this year, but Fed is not tied to 3 rate hikes - CNBC interview

Politics

(FR) With 100% of votes in France Presidential Election counted: Macron 23.75%; Le Pen 21.53%; Fillon 19.91%; Melenchon 19.64%; Macron and Le Pen move on to run-off in 2 weeks

(US) White House and Congress remain at a standstill on funding the govt ahead of a potential shutdown on Friday - Politico

(US) House Speaker Ryan: Spending bill will be ready before the end of the week to avert a potential govt shutdown - press

(UK) According to the latest Comres poll, support for PM May's Conservative party was at 50% - highest since 1991 - press

(DE) Bid by Germany's Co-leader of euro-skeptic AfD party, Frauke Petry, to have a debate on the party's future was scrapped by party delegates - press

Weekend US/EU Corporate Headlines

BCR: Becton Dickinson to acquire Bard for $24B

Key economic data:

(TW) Taiwan Mar Unemployment Rate: 3.8% v 3.8%e

(TH) Thailand Mar Trade Balance: $1.6B v $1.7Be

Asia Session Notable Observations, Speakers and Press

First-round of presidential elections in France has produced the most market-friendly of outcomes, as centrist Macron and far-right Le Pen head for the runoff in 2 weeks. Macron is the heavy favorite and polls most favorably against the anti-euro FN candidate, pulling the single-currency from the precipice of populist revolts observed in US and UK over the past year. With 100% of the vote counted, Macron had 23.71% of the vote, followed by Le Pen at 21.91%. EUR/USD spiked up nearly 2 big figures to 1.09 in early trade before consolidating around 1.0850, USD/JPY rose nearly 150pips above 110.40, and safehaven Gold fell over $15 below $1,270. Indicated yields on the US Treasury 10-yr benchmark were up 8bps to reach 2.3% for the first time in over a week, while S&P futures rose nearly 20 handles above 2,365.

Nikkei225 is the best performing index among the majors thanks to weaker JPY, as Shanghai Composite is notably weaker. Selling attributed to smaller reverse repo injections as well as expectations for more deleveraging measures by regulators. Moody's has also warned about profitability pressure on China banks, while investors shrug positive comments from PBOC Gov Zhou.

Among corporates, Sony and JVC Kenwood in Japan were up over 4% and 8% after raising FY16 guidance following market close on Friday. Australia's Chorus was also lifted by inclusion into ASX200.

Geopolitical focus turns to the Korean peninsula with more saber-rattling by the North along with detainment of a US citizen by Pyongyang authorities. Investors are also watching Washington this week, as Congress and White House standoff on funding for a southern border wall come to a head.

China

(CN) China expected to implement more deleveraging measures - Chinese press

(CN) Moody's: China banks are facing profitability pressure

(CN) PBOC Gov Zhou: China's 2017 GDP target is "within reach"; Financial risks are under control - press

(CN) According to research firm Wind, 66% of China listed companies to report Q1 results saw net profit growth - Chinese press

Japan

(JP) Japan PM Abe's cabinet approval rating is near-flat at 50.4% - Japan press

(JP) Japan Fin MIn Aso: Trade imbalances cannot be fixed through FX adjustments alone - press

(JP) Nomura chief economist: Within the BOJ's inner circle, the willingness to stick to the ¥80T commitment is waning - Nikkei

Australia/New Zealand

(AU) UBS: Australia property prices have likely peaked; Will correct but not collapse - press

Korea

(KR) South Korea Defense Ministry spokesman Moon Sang-gyun: Discussions are underway on whether South Korea and the US Forces will conduct a joint military drill when Carl Vinson

(KR) North Korea state media claims its military was ready to sink USS Vinson in a show of military strength - press

(KR) North Korea has detained another US citizen; Brings the total of Americans held to 3 - US press

(KR) Top Trump administration officials will brief senators on April 26 about North Korean situation - financial press

Asian Equity Indices/Futures (00:00ET)

Nikkei +1.3%, Hang Seng -0.1%, Shanghai Composite -1.6%, ASX200 +0.3%, Kospi +0.2%

Equity Futures: S&P500 +0.8%; Nasdaq +0.8%, Dax -+1.3%, FTSE100 +0.4%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0820-1.0915; JPY 109.85-110.50; AUD 0.7540-0.7585; NZD 0.7020-0.7050; GBP 1.2780-1.2835

June Gold -0.9% at 1,277/oz; June Crude Oil +0.5% at $49.87/brl; July Copper +0.7% at $2.57/lb

(US) Weekly Baker Hughes US Rig Count: 857 v 847 w/w (+1.2%) (14th straight weekly rise)

OPEC/non-OPEC technical committee meeting said to call for six-month extension to oil output cut agreement - press

SPDR Gold Trust ETF daily holdings rise 4.3 tonnes to 858.7 tonnes

iShares Silver Trust ETF daily holdings fall to 10,119 tonnes from 10,149 tonnes prior; lowest since Apr 10th

(CN) PBOC SETS YUAN MID POINT AT 6.8673 V 6.8823 PRIOR; strongest setting since Apr 19th

(CN) PBOC to inject combined CNY30B v CNY100B prior in 7-day, 14-day and 28-day reverse repos, 5th straight injection

(JP) BOJ reduced 3-5yr maturity JGB purchases to ¥320B from ¥350B

(AU) Australia MoF sells A$300M in 4.5% 2033 bonds; avg yield 3.0205%; bid-to-cover 3.07x

(KR) South Korea MoF sells 20-yr bonds; avg yield 2.34% v 2.30% prior

Asia equities / Notables / movers

Australia

Sirtex Medical (SRX) -14.3%; ARAH Study Shows Statistically Significant Safety, Toxicity and Quality of Life Benefits for SIR-Spheres versus Sorafenib with No Difference in Survival

Worleyparsons (WOR) -0.7%; CEO: Not seeking to be acquired - AFR

Chorus Ltd (CNU) +2.8%; To replace Duet Group in S&P/ASX 200 Index at the open May 2nd

Japan

Toshiba (6502) +0.7%; To split off its four in-house companies into wholly-owned subsidiaries

Mitsubishi Motor (7211) +1.5%; To invest ¥10B to build a plant in China to supply engines for locally built Outlander SUVs - Nikkei

Kobe Steel (5406) -0.3%; FY17 results speculation

Sony (6758) +4.2%; Raises FY16/17 guidance

JVC Kenwood (6758) +8.5%; Raises FY16/17 guidance

Hong Kong

Da Ming International Holdings (1090) +2.3%; Q1 result

Beijing Jingkelong Company (0814) -2.9%; Q1 result

China State Construction Int'l Holdings (3311) -3.4%; Q1 result

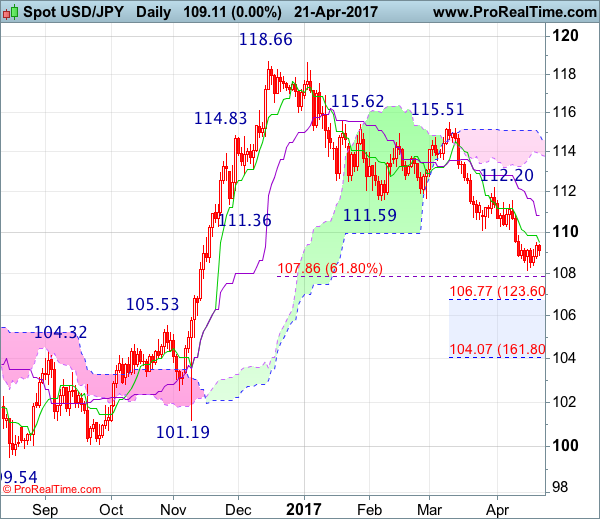

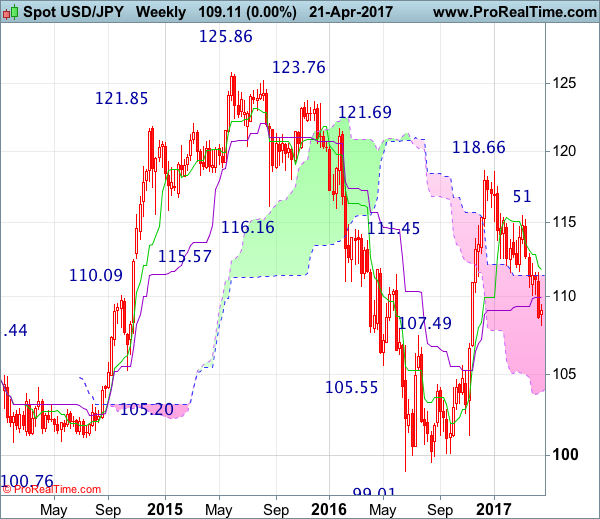

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

USD/JPY – 109.05

Although the greenback opened higher today and jumped to as high as 110.60, as long as this level holds, consolidation with mild downside bias is seen for weakness to the Tenkan-Sen (now at 109.37), however, a daily close below 108.65-70 is needed to signal the rebound from 108.13 has ended, bring retest of this level later, Looking ahead, only a drop below this level would extend recent decline from 118.66 top to 107.85-90 (61.8% Fibonacci retracement of 101.19-118.66) and possibly 107.40-50 but oversold condition should prevent sharp fall below 106.75-80 (1.236 time projection of 118.66-111.59 measuring from 115.51) and 105.90-00 should hold from here, bring rebound later.

On the upside, above said resistance at 110.60 would suggest a temporary low has been formed at 108.13, bring further gain to 111.00 but a daily close above resistance at 111.58 is needed to signal low has been formed, bring further gain towards resistance at 112.20, however, only a sustained breach above this level would provide confirmation, bring correction of recent entire selloff to 112.90 (previous resistance) and possibly towards another previous resistance at 113.54.

Recommendation : Hold short entered at 110.40 for 108.40 with stop above 110.65.

On the weekly chart, as the greenback opened higher this week and a window was formed, suggesting consolidation above last week’s low at 108.13 would be seen, above 110.60 would extend gain to the upper Kumo (now at 111.37), however, a weekly close above the Tenkan-Sen (now at 111.82) is needed to signal low has been formed, bring further gain towards resistance at 112.20-26. Looking ahead, a sustained breach above 120.20 would extend the rebound from 108.13 to 113.00, then test of 113.54 resistance and possibly 114.00-10 but price should falter well below resistance at 115.51.

On the downside, whilst pullback to 109.40-50 cannot be ruled out, reckon support at 108.88 would limit downside and bring another rebound later. Only a drop below 108.65-70 would suggest the rebound from 108.13 has ended, bring retest of this level, once this last week’s low is penetrated, this would extend recent selloff from 118.66 to 107.85-90 (61.8% Fibonacci retracement of 101.19-118.66), then towards 107.00, however, oversold condition should prevent sharp fall below 106.50-55 (61.8% Fibonacci retracement of 99.01-119.52) and reckon previous resistance at 105.53 (now support) would remain intact.

French Election: Macron And Le Pen Advance To The Second Round

The euro opened with a large positive gap against its major peers on Monday, following the outcome of the first round of the French presidential election. The two candidates that qualified for the second round are Emmanuel Macron and Marine Le Pen, with their percentages being roughly 24% and 21.5% respectively. The run-off is scheduled on the 7th of May.

The positive reaction in the euro may have been fueled by the fact that in practically every poll for the second round, Macron is leading the Eurosceptic Le Pen by a significant margin. This implies that market participants may have already begun pricing in a Le Pen loss in the run-off and therefore, a lower probability of any 'Frexit' referendum.

EUR/USD gapped up, to open above the key resistance (now turned into support) territory of 1.0800 (S1) and the longer-term downtrend line drawn from the peak of the 3rd of May 2016. Nevertheless, the rate hit 1.0910 (R2) and then retreated to challenge the aforementioned territory as a support this time.

If the pair manages to close the day above that crossroad, we would consider the outlook to have turned positive. The bulls may regain control at some point soon and if they prove strong enough to overcome the 1.0870 (R1) level again, they could aim for another test near 1.0910 (R2).

The euro was not the only asset that responded to the result. Risk appetite dominated the financial community, as European stock indices opened with notable positive gaps, and safe-havens like JPY and gold, started the week on the back foot. We think that this improved sentiment may also spill over to US equity markets, which could open in a similar fashion as their EU counterparts.

EUR/JPY opened with a large positive gap as well, hitting 120.55 (R2) before pulling back. The gap brought the rate above the short-term downtrend line taken from the high of the 13th of March, something that signals a near-term trend reversal in our view. Even if the pair corrects a bit lower, we expect any setback to remain limited above the aforementioned downtrend line. A possible rebound from near that zone is likely to see scope for another test near 120.55 (R2). A clear break above that level may pave the way for the key crossroad between the 121.70 (R3) hurdle and the downside resistance line taken from the peak of the 15th of December.

Moving forward, we see the case for the euro to remain supported on this outcome, at least for a few days. The key risk to our view is any new second-round polls showing Le Pen closing the gap on Macron.

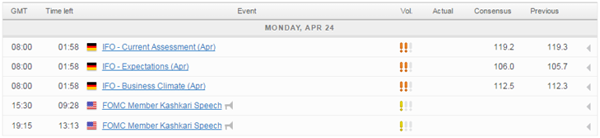

Today's highlights:

During the European morning, the only noteworthy indicator we get is Germany's Ifo survey for April. The consensus is for the current conditions index to have ticked down, while the expectations index is forecast to have risen somewhat. If there is any market reaction on this indicator, we would expect it to be positive for the euro and/or the German DAX, considering that improving expectations may overshadow a slight deterioration in current conditions.

We have only one speaker on today's schedule: Minneapolis Fed President Neel Kashkari.

As for the rest of the week:

On Tuesday, we have no major events on the economic calendar while on Wednesday, we get Australia's CPI data for Q1. On Thursday, we have a very busy day, as both the BoJ and the ECB will announce their rate decisions. Expectations are for both Banks to keep their policy unchanged. We think that investors may focus primarily on the ECB meeting, considering the relatively hawkish signals we received at the latest policy meeting and the subsequent reports showing that investors over-interpreted those signals. Finally on Friday, we get Japan's CPI data for March and Eurozone's preliminary CPI data for April. We also get the first estimate of Q1 GDP from both the US and the UK.

EUR/USD

Support: 1.0825 (S1), 1.0800 (S2), 1.0775 (S3)

Resistance: 1.0870 (R1), 1.0910 (R2), 1.0955 (R3)

EUR/JPY

Support: 119.00 (S1), 118.15 (S2), 117.50 (S3)

Resistance: 119.80 (R1), 120.55 (R2), 121.70 (R3)

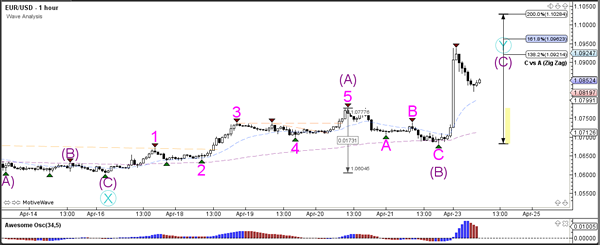

Daily Technical Analysis: EUR/USD Bullish Rally After 1st Round Of French Elections

Currency pair EUR/USD

The French voters choose novice centrist Macron and far right candidate Le Pen during the first round of the Presidential election in France, which took place on Sunday 23 April. None of the candidates reached the 50% threshold and hence a second round will occur with the two candidates on Sunday 7 May.

The EUR/USD reacted bullishly to the news, most likely due to the prospect of Macron winning the second round of the French Presidential elections. Macron is in favour of the EU and the Euro currency, which is exact opposite position of Le Pen. The EUR/USD broke above 1.09 and thereby changed the wave structure as a larger correction could be taking place.

The EUR/USD is building bullish momentum which could be part of a wave (purple).

Currency pair EUR/USD

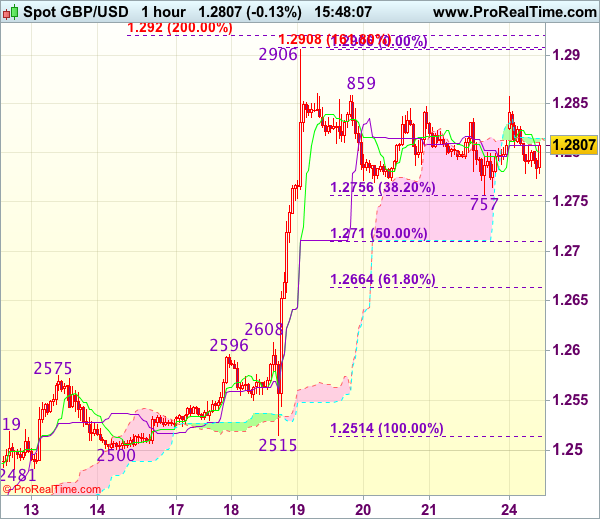

The GBP/USD is building a bull flag chart pattern (red/blue lines). A break above it could see price challenge the next Fibonacci level.

The GBP/USD retracement has respected the 38.2% Fibonacci retracement level at 1.2750. A break below the 61.8% Fibonacci level invalidates wave 4 (purple) where a break above the bull flag (red) could see a wave 5 (purple) develop.

Currency pair USD/JPY

The USD/JPY broke above the bear flag chart pattern (dotted orange) and resistance trend line (dotted red). The bullish price action could still be part of larger bearish retracement (waves Y) of the larger time frames.

The USD/JPY bullish momentum could be part of a 5 wave (orange) within wave 3 (brown). The wave 4 (orange) remains valid as long as price stays above the 61.8% Fibonacci level of wave 4 (orange).

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD gaps higher earlier today after Macron and Le Pen made it to the second round of French election, opened at 1.0903 but unable to stay consistently above 1.0873 – 1.0900 key resistance and traded lower around 1.0840 at the time I wrote this comment. From technical perspective as you can see on my daily chart below, if price close back below 1.0873 today, we may see another bearish pullback retesting the trend line support and 1.0650/00 region this week. I am not bullish yet on this pair, but a clear break and daily close above 1.0900 would expose 1.1000 – 1.1050 region. Overall I remain neutral.

GBPUSD

The GBPUSD had a bullish momentum last week topped at 1.2903 but closed a little bit lower at 1.2806. The bias is neutral in nearest term but as long stay above 1.2750 the double bottom bullish scenario should remain valid with nearest target seen at 1.3000 – 1.3050. On the downside, a clear break and daily close back below 1.2750 would interrupt the bullish scenario testing 1.2650 region.

USDJPY

The USDJPY gaps higher earlier today opened at 110.46 but traded lower around 110.00 at the time I wrote this comment after French election result. As you can see on my H1 chart below, price respecting the trend line resistance which keeps the major bearish trend remains valid. Immediate support is seen around 109.40. A clear break and daily close back below that area would expose 108.70 region. On the upside, a clear break and daily close above the trend line resistance and 110.50 could trigger further bullish pressure testing 111.00 area or higher.

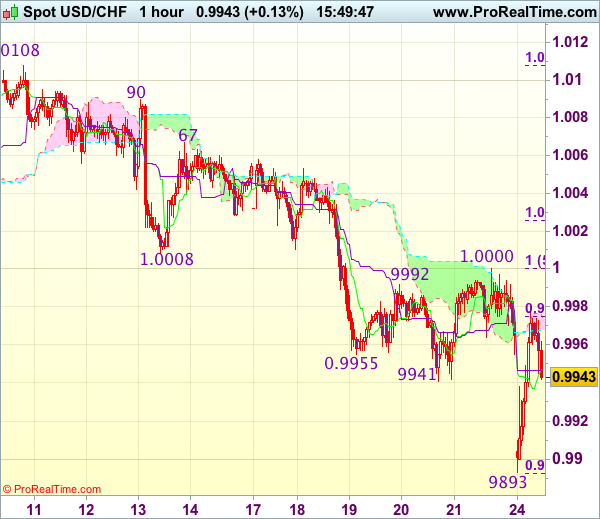

USDCHF

The USDCHF gaps lower earlier today after French election, opened at 0.9904 but traded a little bit higher around 0.9940 at the time I wrote this comment. The bias is neutral in nearest term but as long as stay below 1.0020 price is still in a bearish phase testing 0.9880 and 0.9813 area. Immediate resistance is seen around 0.9965. A clear break above that area could trigger further bullish pressure testing 1.0020 which is a good place to sell with a tight stop loss. Overall I remain neutral.

Trade Idea : USD/CHF – Stand aside

USD/CHF - 0.9935

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9955

Kijun-Sen level : 0.9947

Ichimoku cloud top : 0.9973

Ichimoku cloud bottom : 0.9968

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback met renewed selling interest at 1.0000 on Friday and dropped again to as low as 0.9893 earlier today, having said that, the subsequent rebound from there suggests consolidation above this level would be seen and another bounce to 0.9980-85 cannot be ruled out, however, reckon 1.0000 (said resistance and 50% Fibonacci retracement of 1.0108-0.9893) would limit upside and bring another decline later. Below said support at 0.9893 would extend the fall from 1.0108 top to 0.9865-70 (2 times extension of 1.0108-1.0008 measuring from 1.0067) but support at 0.9831 would hold, bring rebound later.

In view of this, would be prudent to stand aside in the meantime. Above previous support at 1.0008 would suggest low is formed instead, bring rebound to 1.0025-30 (61.8% Fibonacci retracement of 1.0108-0.9893) but price should falter below resistance at 1.0067.

Market Concerns Eased After Macron’s First Round Victory

The first-round voting of the French presidential election was revealed on Sunday night April 23. The two top candidates: independent centrist Macron and the far-right wing Le Pen, won 23.7% and 21.7% of votes respectively. Fillion and the far-left wing Jean-Luc Mélenchon got around 19% of votes. The result was in line with expectations, black swans didn't appear.

The terror attack that occurred on April 20 in Paris was likely to give Le Pen one last push just a few days ahead of the election. However, the votes Le Pen got were even lower than the recent polls of 23%, indicating the probability of her presidency is lower than expectations.

As Macron got the first place in the first-round of voting, surpassing Le Pen with 2% of votes, market concerns over the EU's collapse after Le Pen's presidency has been eased to an extent.

The consensus was that Macron and the Le Pen would likely get into the second round with Macron likely winning the final vote. The outcome is in line with the first half of the consensus. Markets are now focused on the second-round of voting with the first-round outcome lifting market confidence and expectations on Macron's victory in the second-round on May 7.

The voting ratio was around 80%, higher than the forecast of 70%, indicating French civilians' high concerns on the futures of France and the EU.

The outcome of the first-round voting pushed the EUR up and weighed on safe havens after the release of the outcome. EUR/USD soared more than 180 points, hitting the highest level of 1.0918 since November 11, 2016. Spot gold plunged from 1284.17 to a 2-week low of 1265.38. EUR/JPY hit a 1-month high of 120.72. USD/JPY hit a 2-week high of 110.53.

Trade Idea : GBP/USD – Buy at 1.2710

GBP/USD - 1.2822

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2801

Kijun-Sen level : 1.2808

Ichimoku cloud top : 1.2815

Ichimoku cloud bottom : 1.2815

Original strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2710, Target: 1.2850, Stop: 1.2675

Position : -

Target : -

Stop : -

Although cable recovered initially to 1.2858, as price has retreated again again after faltering below resistance at 1.2859, suggesting further consolidation would be seen and another test of Friday’s low at 1.2757 cannot be ruled out, however, reckon downside should be limited to 1.2700-10 (50% Fibonacci retracement of 1.2515-1.2906) and bring another rally, break of 1.2759 would signal the pullback from 1.2906 has ended, bring retest of this level, break there would extend recent upmove to 1.2920-30 (2 times extension of 1.2365-1.2575 measuring from 1.2500), then 1.2950 but loss of near term upward momentum should prevent sharp move beyond 1.2990-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance).

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as downside should be limited to 1.2710 (50% Fibonacci retracement of 1.2515-1.2906), bring another rise. Below 1.2700 would defer and signal top has been formed, risk correction to 1.2660-65 (61.8% Fibonacci retracement of 1.2515-1.2906) and price should stay well above 1.2608-16 (previous resistance now support).

Macron Early Victory Over Populism Boosts The EUR

European equity markets are poised to start the week on a positive note on Monday after the first round of the French elections suggested that the populist wave that engulfed the UK and US in 2016 has not quite breached the borders of the eurozone countries.

While it's clear that populism is growing in the region as it is elsewhere, the victory for Emmanuel Macron in the first round may well have crushed the chances of Marine Le Pen in two weeks' time. Even when the polls had Le Pen taking the first round, Macron was comfortably expected to win the head to head but with the centrist candidate having toppled her on Sunday, the leader of the National Front would appear to have a monumental job on her hands.

While the result on Sunday was largely in line with what the latest polls had been projecting, we did see a more cautious approach from investors heading into it having learned their lessons from last year. The relief rally in the euro overnight are a clear sign of this, with it having hit its late March highs above 1.09 against the dollar before paring gains.

Obviously there is still two weeks to go until the second round of voting and while Macron looks highly likely to succeed, the populist vote has surprised us in the past and may well again. It will be interesting to see whether the same complacency that left us surprised last June – when the UK voted to leave the EU – creeps back into the markets in the coming weeks or if the same caution that spurred the relief rally overnight lingers.

French President Marcon, in waiting

With this week and particularly today looking a little quiet on the economic calendar – barring the ECB meeting on Thursday and a couple of other releases – we're likely to see focus remain on the situation in France and Le Pen's efforts to prove the pollsters wrong. As was the case in the Netherlands, the first round of voting will be seen as a success for those seeking the status quo in the eurozone and with the AfD in Germany standing little chance in September, a similar result in two weeks may see the region survive the year unscathed. Assuming, of course, we don't see elections in Italy.

Top Events To Watch The Week Ahead

First round results of French presidential elections

The Euro surged to a fresh five-month peak at 1.0932 during early trading on Monday, after Centrist Emmanuel Macron moved one step closer to the French presidency when he won the first round of the elections. With this market-friendly outcome reducing the risk of a Trump-style shocker, investors have rediscovered their appetite for riskier assets. While the current risk-on rally may support the Euro in the short-term, gains could still be limited as anxiety mounts ahead of the second round of the elections on 7 May. Although speculation remains heightened over Macron claiming the title of the French president, I think that the lingering threat of a shock victory by Le Pen may limit gains on the Euro.

U.S. tax reforms

'Big TAX REFORM AND TAX REDUCTION will be announced next Wednesday.' This tweet came from Trump over the weekend. Markets have been waiting for these reforms for a long time now, and most of the gains in U.S. equities were built on these promises. The 100th day of Trump's presidency will be on Saturday, 29 April, and so far, he struggled to advance on most of his campaign promises. Will he finally deliver?

I think next week is going to be a crucial test for the new U.S. administration, especially now that markets have grown skeptical of its ability to deliver. U.S. stock indices closed slightly lower on Friday, in a sign that Trump comments are no longer effective. However, if the President’s proposed reforms were reasonable and can pass the Congress, there’s a high chance for equities rally to revive.

U.S. Growth

After a bunch of negative data from the U.S. economy, GDP is now expected to halve in Q1 relative to Q4 2016. Consumer spending is likely to be the primary driver of the slowdown given that retails sales fell for two consecutive months. Investors will then shift their focus on how the Federal Reserve will act on slowing growth. It seems now the probability of three rate hikes in 2017 is fading and based on that the USD might continue to feel the pressure.