Sample Category Title

Trade Idea: GBP/USD – Buy at 1.2710

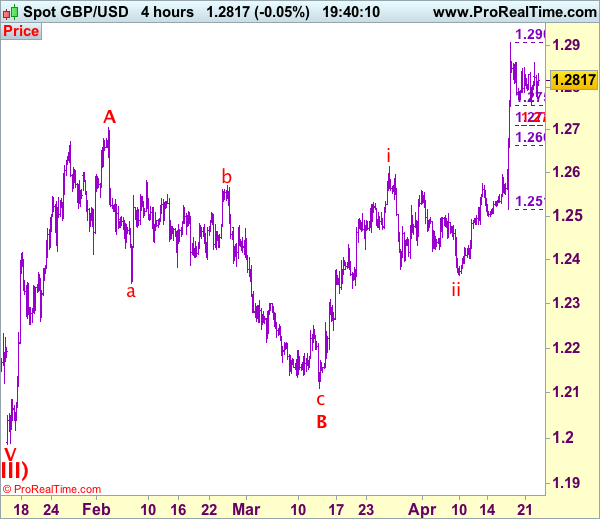

GBP/USD – 1.2816

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

Original strategy :

Buy at 1.2710, Target: 1.2910, Stop: 1.2650

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.2710, Target: 1.2910, Stop: 1.2650

Position: -

Target: -

Stop:-

Although cable staged a brief bounce to 1.2858, as price has retreated after failing to penetrate minor resistance at 1.2859, retaining our view that further consolidation below last week’s high at 1.2906 would be seen and risk of another corrective fall to 1.2757 (38.2% Fibonacci retracement of 1.2515-1.2906) is seen, however, reckon 1.2710 (50% Fibonacci retracement as well as 100% projection of a leg from1.2906) would limit downside and bring another rise later, above said resistance at 1.2858-59 would suggest the pullback from 1.2906 has ended instead, bring further gain to 1.2870, then retest of 1.2906. We are keeping our view that the wave c as well as larger degree wave B has ended at 1.2109, hence impulsive wave C has commenced from there with wave i of C ended at 1.2616, follow by a correction to 1.2365 (end of wave ii) and wave iii rally is unfolding, hence further gain to 1.2940-50 and possibly psychological resistance at 1.3000 would be seen, however, near term overbought condition should limit upside to 1.3050-60.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst initial pullback to 1.2750-55 is likely, reckon downside would be limited and 1.2700-10 (50% Fibonacci retracement of 1.2515-1.2906) should contain weakness and bring another rally later. Below 1.2690-00 would defer and risk correction to 1.2660-65 but another previous resistance at 1.2616 (wave i top) should remain intact.

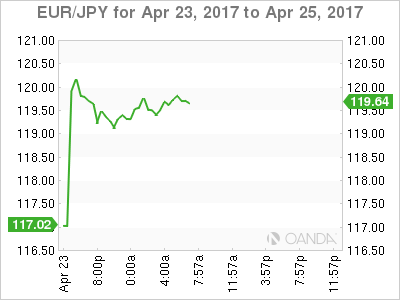

Trade Idea: GBP/JPY – Stand aside

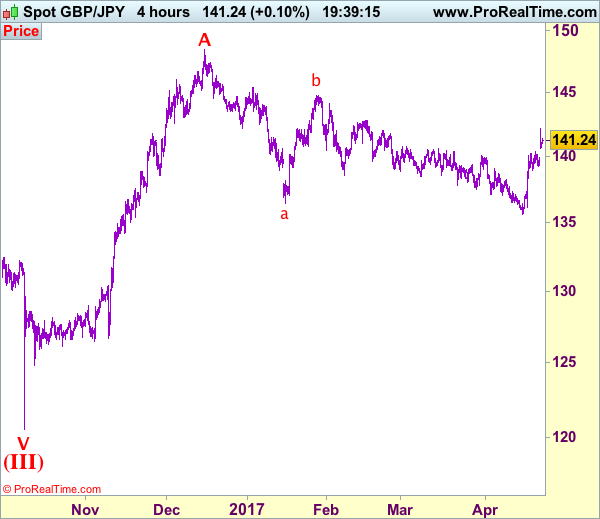

GBP/JPY - 141.20

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Exit long entered at 139.10,

Position: - Long at 139.10

Target: -

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although sterling did surge in line with our previous bullishness and price rose to as high as 142.10 earlier today, the subsequent retreat suggests consolidation below this level would be seen and pullback to 140.60-65 cannot be ruled out, however, reckon downside would be limited to 140.00 and price should stay well above support at 139.20 (Friday’s low), bring another rise later.

In view of this, would not chase this rise here and would be prudent to buy sterling on subsequent pullback. Above 141.70-80 would bring retest said intra-day resistance at 142.10 but break there is needed to revive bullishness and extend the rise from 135.60 low to 142.50, then towards 142.90-00 later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Technical Outlook: GBPUSD Remains Within Narrow Consolidation, Risk Of Deeper Pullback Exists

Cable is holding around 1.2800 handle after being dragged higher by strength of Euro and hit session high at 1.2838.

Near-term action remains within consolidation range established between 1.2755 and 1.2845, after the pair soared to fresh six-month high at 1.2904 last week.

Neutral near-term studies suggest extended sideways mode, however, risk of deeper correction exists, as daily RSI and slow stochastic are hovering around overbought borders and may generate bearish signal on reversal.

Consolidation range low at 1.2755 marks Fibo 38.2% of 1.2513/1.2904 rally, firm break of which is needed to trigger stronger pullback and open supports at 1.2700 (round-figure) and 1.2663 (Fibo 61.8% retracement).

At the upside, the upper 20d Bollinger band is capping near-term action (currently at 1.2862) and break above it would signal fresh attack at 1.2905 high. Violation of the latter would expose psychological 1.3000 barrier for retest.

Res: 1.2838, 1.2862, 1.2904, 1.2950

Sup: 1.2800, 1.2772, 1.2755, 1.2709

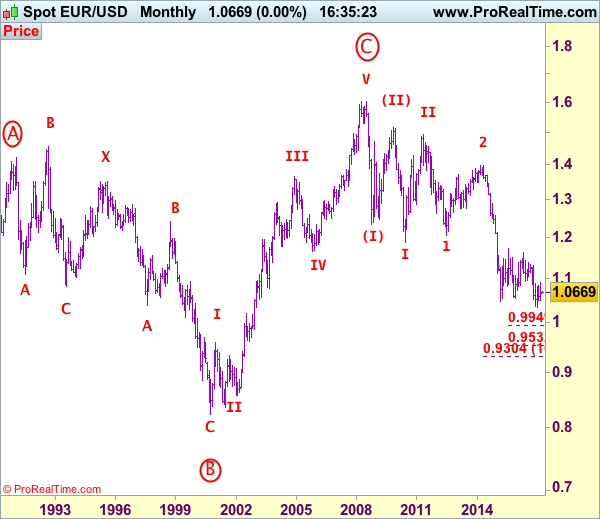

EUR/USD Elliott Wave Analysis

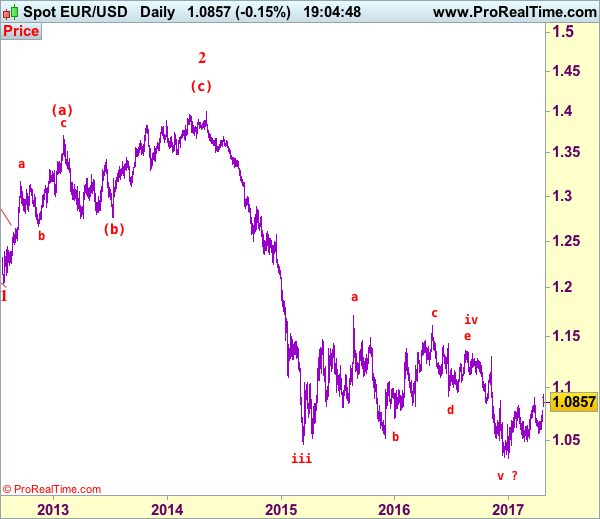

EUR/USD – 1.0854

EUR/USD: Wave (c) of 2 ended at 1.3993 and wave 3 of III has commenced for weakness to 1.0411 (1.236 of wave 1), then 1.0000.

The single currency found renewed buying interest at 1.0682 and has rallied, price opened sharply higher today and broke above indicated previous resistance at 1.0906, suggesting the erratic rise from 1.0340 (tentatively wave v of larger defer wave 3) is stallion progress, hence further gain to 1.1000 would be seen, above there would encourage for further rise to 1.1050, however, reckon upside would be limited to 1.1125-30 (61.8% Fibonacci retracement of 1.1616-1.0340) and price should falter well below strong resistance at 1.1300, bring retreat later.

Our preferred count on the daily chart remains that a wave (II) from 1.2329 ended at 1.5145 with A-leg ended at 1.4720, followed by wave B at 1.2457, the wave C from there was also a 3 legged move and is labeled as (a): 1.3739, (b): 1.2885, the wave iii of the 5-waver (c) from 1.2885 has ended at 1.4339 and wave iv is a triangle ended at 1.3878 and wave v formed a top at 1.5145. The decline from there is a 5-waver (C) with minor wave (i) of I of (C) ended at 1.4218 with wave (ii) ended at 1.4580, wave (iii) ended at 1.3267 and wave (iv) ended at 1.3692 and wave (v) ended at 1.1876, this is also the low of wave I of (C) and wave II ended at 1.4940, hence wave III is now in progress with a diagonal wave 1 ended at 1.2042, the breach of previous support at 1.1876 (wave I trough) adds credence to our view that the wave 2 has ended at 1.3993, wave 3 has commenced for further weakness to 1.0411, then towards 1.0000.

On the downside, whilst pullback to 1.0800 cannot be ruled out, reckon previous resistance at 1.0778 would turn into support and contain euro’s downside, bring another rise later. Below 1.0735-40 would defer and risk test of support at 1.0678-82 but only a drop below there would suggest top is formed instead, bring weakness to 1.0635-40, then 1.0602 support. Looking ahead, only a daily close below 1.002 would provide confirmation and revive bearishness for test of 1.0570 support first.

Recommendation: Buy at 1.0780 for 1.0980 with stop below 1.0680.

Euro's long-term uptrend started from 0.8228 (26 Oct 2000) with an impulsive structure. The rise from 0.8228 to 0.9593 (5 Jan 2001) is labeled as wave I, the retreat to 0.8352 (6 Jul 2001) is wave II and the rally to 1.3670 (31 Dec 2004) is wave III. Wave IV from there ended at 1.1640 (15 Nov 2005), the subsequent upmove to 1.6040 (July 15, 2008) is treated as wave V, the major selloff from the record high of 1.6040 to 1.2329 (October 27, 2008) signals a reversal has taken place with (I) leg ended at 1.2329 and once (II) ended at 1.5145, wave (III) itself is an extended move with I: 1.1876 and complex wave II ended at 1.4902, wave III has commenced with wave 1 and 2 ended at 1.2042 and 1.3993 respectively, wave 3 of III is now unfolding for weakness towards parity.

Euro Strengthens on French Election Result

- Euro strengthens on French election result

- Sterling remains strong as Gross Domestic Product (GDP) data awaited

- USD slips on softer data

The political establishment has been shunned in favour of a far-right woman and a party that only came into existence a year ago, with a leader who married his school teacher. Emmanuel Macron was ahead by a couple of percentage points from Marine Le Pen as the pair swung through into the second round. Those who know more than I do about French politics seem to believe Macron will take the Presidency but those in the know also told us that Trump would fail and 'Remain' would win the Brexit vote. We shall see. For now though, the Euro has gained a cent or so against most other currencies but was less successful against the emboldened Sterling.

For its part, the Pound had a very positive week last week. The calling of a UK election, which should favour the incumbent has boosted the Pound. Both ICM and Yougov polls suggest a solid majority for the Conservatives. UK data has done its part to assist the Sterling strength. This week brings an expected rise in UK economic growth data and perhaps more clarity on the Budget when Philip Hammond testifies to the Treasury Select Committee, potentially offering more insight into the strength of the UK economy.

The US Dollar, on the other hand, had a poor week. Weak retail sales and softer inflation, plus hints that tax reform plans could be delayed, all weighed on the USD. This week will bring further news on those tax reforms and perhaps developments on the replacement for Obamacare. All will influence the USD, as will an expected slip in US GDP data and a forecast dip in US Consumer Confidence. If the forecasters have got their sums right, there may be further weakness in the USD this week.

As well as the UK and US GDP data, we'll also get Canadian economic growth figures and the forecasts are mixed. The Canadian Dollar, which has slipped with its US counterpart, has some volatile trading due this week as those numbers emerge.

This week will include New Zealand's trade balance. Last month's data was wildly at odds with forecasts and quite negative. There is a belief that this month's figures will be an improvement and may even offer up a trade surplus. The Kiwi Dollar will be heavily influenced by that news.

And 'those things will kill you' was a standard expression for anyone who didn't smoke as they attempted to stop their friends from doing so. Now e-cigarettes are under the spotlight. One 'vaper' felt his e-cigarette getting hot in his pocket and when he removed it and threw it across the room, it exploded, punching a hole in his wall. And researchers at Johns Hopkins University believe the new devices are as damaging to health as tobacco. Apparently those things'll kill you in new ways.

Car humour

- Apparently I snore so loudly that it wakes my passengers.

- My son had his driving test the other day. He got 4 out of 5. The other chap managed to leap clear.

- Isn't it strange how you can feel reassured by seeing policemen walking the street, but paranoid when they are behind you in a car.

- He died doing the two things he loved most; checking Facebook while driving.

French Relief Sends Europe Soaring

The first round of the French Presidential election produced one of the most market-friendly outcomes with centrist Emmanuel Macron leading against the right wing Marine Le Pen.

The margin – Macron +23.75%, Le Pen +21.53% – suggests that he is the heavy favorite against the anti-euro Le Pen in round two on May 7.

This week, the BoJ and the ECB meet and neither is expected to change its monetary policy. The ECB will do little if anything given the easing of inflation last month along with the considerable risks of the French elections.

The BoJ's Governor Kuroda has already indicated on the weekend that stimulus is here to stay for sometime and given the yen's (¥110.00) recent strength, they cannot afford to discuss changes.

Also, in Europe, Q1 growth data will be released in the U.K and France, while Japan will release its slew of end-of-month numbers. In Australia, dealers get to pick apart the important quarterly CPI data.

The geopolitical focus again turns to the Korean peninsula with more saber rattling by the North.

Stateside, investors are also watching Washington this week, as Congress and White House standoff on funding for a southern border is expected to come to a head.

On Friday, U.S GDP is due and the economy is expected to expand at a +1.5% annualized rate in Q1 – the weakest pace in 12-months.

1. Chinese stocks buck the trend

Trading in Shanghai spoiled the global markets celebration of Macron's first round French presidential victory.

The selloff in Chinese equities deepened overnight as concern grows that authorities will step up measures to crack down on leveraged trading.

The Shanghai Composite dropped -1.4% to the lowest since Jan., after the index tumbled -2.3% last week.

In contrast, in Hong Kong, the Hang Seng increased +0.4% and the Hang Seng China Enterprises Index rallied +0.5%.

In Japan, the broad based Topix increased another +1%, after last week's first weekly advance in more than a month.

The “feel good” factor has volatility measures slumping – the gauge for the Eurostoxx plunged -29%, while the measure for the Nikkei 225 Stock Average lost -17%, the most in six-months.

In Europe, equity indices are trading sharply higher as risk-on prevails after Macron's first round win and German sentiment data (see below). Banking stocks are supporting the Eurostoxx and French banks have pushed the CAC 40 to outperform. Energy, commodity and mining stocks are also trading higher and supporting the FTSE 100.

U.S stocks are set to open in the 'black' (+1.1%).

Indices: Stoxx50 +3.9% at 3,579, FTSE +1.9% at 7,246, DAX +2.9% at 12,394, CAC-40 +4.6% at 5,292, IBEX-35 +3.4% at 10,730, FTSE MIB +4.0% at 20,530, SMI +1.5% at 8,684, S&P 500 Futures +1.1%.

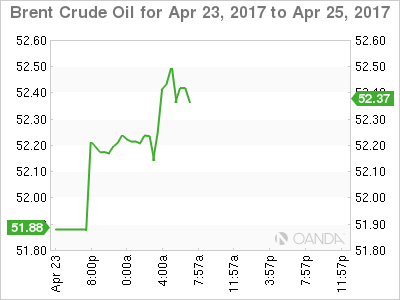

2. Oil recovers lost ground, but market remains under pressure, gold lower

Following last week's big losses, oil prices have recovered some lost ground overnight, driven by expectations that OPEC will extend a pledge to cut output to cover all of this year. However, a relentless rise in U.S drilling is expected to cap most market gains.

Brent crude futures have rallied +35c, or +0.67%, to +$52.31 per barrel, while U.S West Texas Intermediate (WTI) crude added +32c, or +0.64% to remain trading below the psychological +$50 handle at +$49.84 a barrel.

Oil prices fell steeply last week on the back of stubbornly high crude supplies, despite a pledge by OPEC to cut production by almost -1.8m bpd for six-months from Jan. 1.

Note: On the weekend, a panel made up of OPEC and other producers has recommended an extension of output cuts by another six-months from June.

Capping market gains are being capped by U.S drillers who added more rigs' for a 14th consecutive week last week, to 688 rigs.

Note: Both the Brent and WTI oil benchmarks are down more than -7.5% since Dec. 31, 2016.

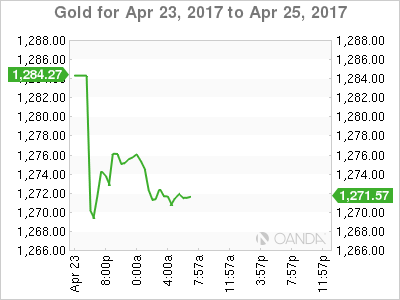

Gold has fallen after the French election result revives 'risk-on' sentiment. The precious metal is down over -1% at +$1,270.80 per ounce, after falling to a near two-week low of +$1,265.90 earlier.

3. Yields soar after French result

A percentage of the risk premium that has been priced into the fixed income market this year has been taken off ahead of the U.S open as Macron won the first round voting in the French presidential election and solidified his prospects of becoming the country's next leader.

German benchmark yields rose +9 bps and those in the U.K added +6 bps, while the yield on French 10-year notes dropped -11 bps to yield +0.83%, the lowest level since mid-Jan.

The spread between 10-year French OAT's and German bunds narrowed -20 bps to +49 bps.

Elsewhere, U.S 10-year yields have rallied +5 bps to +2.30%, while similar Aussie maturities yields jumped +6 bps to +2.60%.

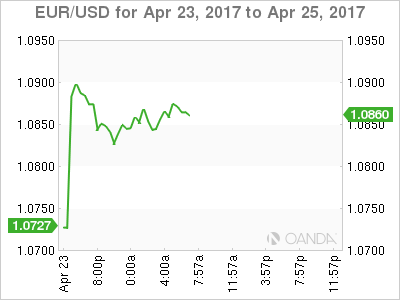

4. EUR supported after Macron win

With the French election first hurdle cleared, risks to the EUR (€1.0867) might move to the upside. The “bulls” believe that EUR needs to overcome last night's high area (€1.0933) to improve the medium term outlook, otherwise the pair will likely be stuck in a range until the round two results are known.

U.S fiscal policy is also expected to limit the EUR's upside in the short-term, so don't be surprised many to fall into a 'buy-the-dip' strategy with the potential to rise towards €1.12 or €1.13 into June assuming a Macron French Presidential win.

Elsewhere, USD/JPY has also benefitted from the risk-on environment to hold above the ¥110.00 level ahead of the U.S open.

5. German Ifo sentiment rises

Data this morning shows that German business sentiment has picked up further in April, beating forecasts in a sign that Europe's largest economy “is growing strongly.

The Ifo business climate index rose to 112.9 points from 112.4 points in Mar. – the highest level in six-years.

Digging deeper, the monthly survey showed that businesses were upbeat about their current situation, but slightly trimmed their six-month outlook. The mood among German construction companies has hit a record-high.

Note: Europe's largest economy is forecast to expand around +1.5% this year and +1.8% in 2018.

French Election Relief Rekindles Risk Sentiment

Financial markets received a solid boost during early trading on Monday, after Centrist Emmanuel Macron secured a position in the second round of the French presidential elections. With Macron's market-friendly, first round victory dissolving some risks associated around a potential anti-establishment shocker, the Euro lurched to fresh five-month highs above 1.0930. Although this risk-on sentiment could support the Euro in the short term, upside gains may face obstacles if uncertainty starts to mount once again ahead of the second round of voting on 7 May. While expectations remain somewhat elevated over Macron becoming the next French President, the live threat of an unexpected Trump-style victory by Marine Le Pen could still expose the Euro to downside shocks.

From a technical standpoint, although the sharp appreciation on the EURUSD has made prices bullish on the daily charts, questions should be asked about the longevity of the current rally. Bulls need to secure a daily close above 1.0900 to open a path towards 1.1000. In an alternative scenario, weakness below 1.0800 could open a path towards 1.0750 and lower.

Greenback stumbles into new week

The Dollar Index found itself pressured below 100.00 last week, after the combination of soft economic data and fading rate hike expectations enticed sellers to attack. Although U.S President Donald Trump has announced that a big tax reform and tax reduction will be announced this Wednesday, markets have received this news with a big pinch of salt. The skepticism over Trump's ability to deliver is becoming quite visible and the growing threat of fiscal spending falling short of expectations may potentially punish the Dollar further. From a technical standpoint, prices have commenced the trading week under renewed pressure and a break below 98.80 could open a path lower towards 98.50.

Stock markets uplifted by Macron

Global stocks were mostly higher during Monday's trading session, as participants mulled over the market-friendly outcome of the first round of the French Presidential elections. With Macron's impressive performance and victory in the first round easing some Frexit-related concerns, stocks in Asia and Europe marched into gains. The newly found appetite for risk should support Wall Street this afternoon. While stock markets have the ability to edge higher in the short term as a result of this relief, potential anxiety ahead of the second round of voting and ongoing Trump uncertainties still have the ability to limit gains.

Commodity spotlight – Gold

The renewed appetite for riskier assets has reduced Gold's glimmer on Monday, with the metal trading around $1270 as of writing. While the current risk-on environment has the ability to expose the yellow metal to further losses, bulls remain in control above $1260. With uncertainty likely to heighten ahead of the second round of the French elections in the coming fortnight and Brexit developments weighing on sentiment, bulls still have a chance to send prices higher. From a technical standpoint, the candlesticks are still trading within the daily bullish channel while the MACD points to the upside. A break back above $1280 could open a path higher towards $1280. A daily close below $1260 invalidates this daily bullish setup.

EUR/USD Consolidates Post French Election Surge

EUR/USD has rebounded since April 11, as a result of the weakening of the dollar.

The outcome of the first-round voting of the French presidential election was revealed on Sunday night April 23.

As consensus, the top two candidates: the independent centrist Macron and the far-right wing Le Pen, won 23.7% and 21.7% of votes respectively. They will the second-round of voting on May 7.

As Macron got the first place, surpassing Le Pen with 2% of votes, market concerns over the EU’s collapse after Le Pen’s presidency has been eased to an extent.

Markets’ confidence on Macron’s victory in the second-round has also been lifted.

The outcome of the first-round voting pushed the Euro up.

EUR/USD soared and broke the resistance level at 1.0800, hitting the highest level of 1.0918 since November 11 on Sunday night.

However, the price retraced afterwards, as the pressure at the 1.0900 resistance level is heavy.

The price has been consolidating during early European session.

The 4-hourly and the daily Stochastic Oscillator readings are both above 70, be aware of a correction prior to the next rally.

The resistance level is at 1.0880, followed by 1.0900 and 1.0920.

The support line is at 1.0835, followed by 1.0820 and 1.0800.

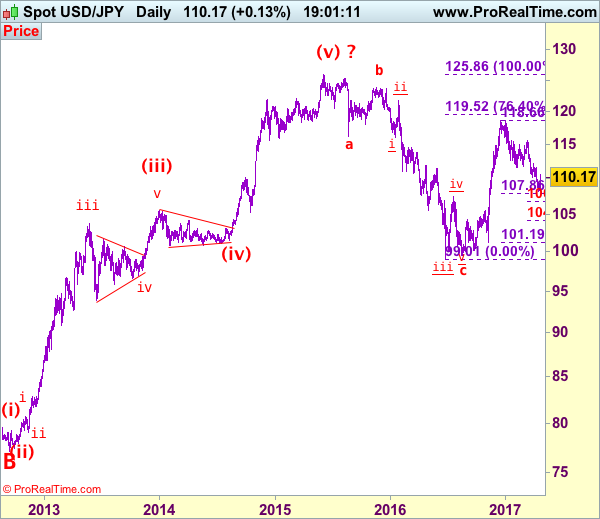

USD/JPY Elliott Wave Analysis

USD/JPY - 110.20

USD/JPY – Wave V of larger degree circle V has possibly ended at 75.31 and major correction has commenced and already met indicated target at 125.00.

Although the greenback opened higher today and jumped to 110.60, dollar’s broad-based weakness suggests upside would be limited and bring retreat later, below 109.85-90 would bring test of previous resistance at 109.49, however, a daily close below there is needed to suggest top is possibly formed, bring weakness to 108.88 but 108.40-45 would hold from here. Below 108.40-45 would bring retest of 108.13 but only break there would confirm early decline from 118.66 top has resumed and extend further fall to 107.85-90 (61.8% Fibonacci retracement of 101.19-118.66), then towards 107.10-20 but reckon 106.75-80 (1.236 times projection of 118.66-111.59 measuring from 115.51) would limit downside and 106.00 should hold, bring rebound later.

Our preferred count is that, triangle wave IV (with circle) ended at 101.45 and the circle wave V brought dollar down to the record low of 75.31 in 2011 and the subsequent rebound signal major correction has commenced with A leg ended at 84.19, followed by wave B at 77.14 and impulsive wave C is now unfolding (indicated upside target at 125.00 had been met) for gain towards 127.00 level. In the event dollar drops below support at 99.01, this would confirm medium term decline from 125.86 top (2015 high) has resumed for subsequent weakness to 98.00 and possibly 97.00.

Under this count, this wave C is unfolding as impulsive waves with (1) (2), 1 2 ended at 80.67, 79.07, 82.84 and 81.69 respectively, hence the extended wave 3 has ended at 103.74 and wave 4 correction of recent upmove should bring weakness to 92.57, then towards 90.88 but psychological support at 90.00 should limit downside and bring another rally later in wave 5, indicated target at 125.00 had been met and gain to 127.00 cannot be ruled out but reckon price would falter below 130.00.

On the upside, above 110.60 would extend the rebound from 108.13 to 111.00 but only a daily close above resistance at 111.58 would signal a temporary low has been formed at 108.13 instead, bring a stronger rebound to resistance at 112.20 first.

Recommendation: Hold short entered at 110.60 for 108.60 with stop above 110.60.

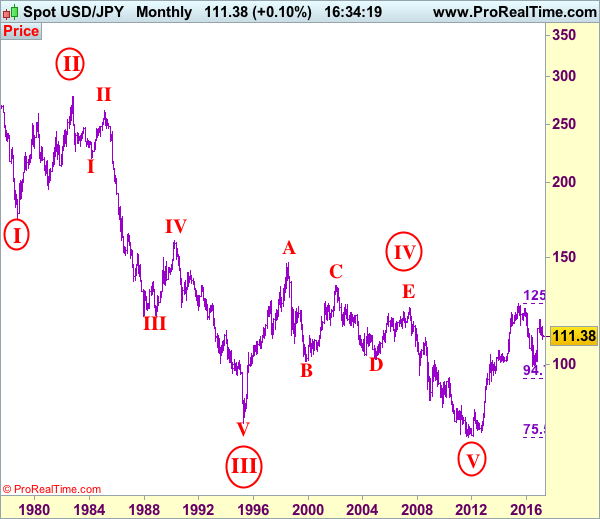

On the monthly chart, we have changed our preferred count that an impulsive wave is unfolding with major wave III with circle ended at 79.75, then followed by wave IV with circle and is labeled as a triangle with A: 147.64 (11 August, 1998), B: 101.25, C: 135.20, D: 101.67 and E leg ended at 124.14 to end the wave IV with circle. Hence, wave V with circle commenced from there and hit a record low of 75.31, however, the subsequent strong rebound signals this circle wave V has possibly ended there, hence gain to (indicated upside target at 122.00 and 125.00 had been met), the retreat from 125.86 suggests wave A of major correction has ended there and wave B correction back to 99.00, then 95.00 would be seen, however, reckon downside would be limited to 90.00, bring another rebound in wave C next year.

DAX Climbs On French Election, German Business Climate

The DAX has posted strong gains on the weekend, boosted by the results of the French presidential election. which showed Emmanuel Lacron and Marine Le Pen advancing to the second round. The DAX is currently trading at 12,398.50, up 2.9 percent since the Friday close. There was more positive news as German Ifo Business Climate improved to 112.9, beating the forecast of 112.4 points.

German business confidence levels continue to improve as Ifo Business Climate climbed to 112.9 in April, up for 112.3 a month earlier. This was its highest level since July 2011. This excellent reading underscores a strong German economy, which has been the locomotive pulling the eurozone, which as showed stronger growth in the first quarter. Germany releases consumer confidence and Preliminary CPI on Thursday.

Nervous stock markets eyed the Sunday French election with bated breath, but investors cheered the results, pushing the euro and European stock markets over the weekend. The best news was what didn’t happen in the first round, as the nightmarish scenario of a runoff between Le Pen and far-Left candidate Jean-Luc Mélenchon was averted. The first round featured 11 candidates, and the election whittled the field down to just 2 candidates – centrist Emmanuel Lacron and far-right Marie Le Pen. Lacron garnered 24% of the vote and Le Pen 22%, which was what most polls leading up to the election predicted. The runoff vote takes place on May 7 and French voters will have a clear choice between Lacron, who served as an economic minister, and Le Pen, who is running on an anti-EU platform. We can expect daily opinion polls to be market-movers, as was the case before the first round. Lacron goes into next week’s vote as a heavy favorite, and two candidates in the first round have thrown their support behind Lacron – center right François Fillon and Socialist Benoit Hamon.

What’s next for the Federal Reserve? The Fed has broadly hinted that it will gradually raise rates in 2017, but it’s unclear how many times Janet Yellen will press the rate trigger. Most analysts are expecting two more moves this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March have made the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. Will the Fed raise rates in June? The CME Group shows the odds of a June hike have dropped to 50%, compared to 64% earlier in April.