Sample Category Title

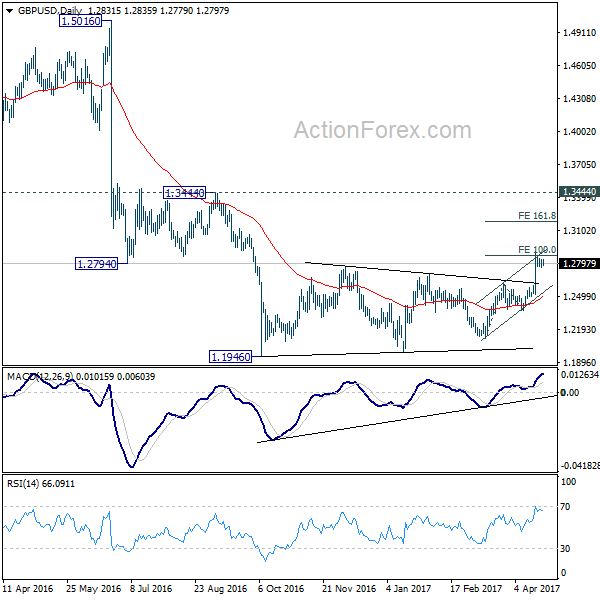

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2759; (P) 1.2797; (R1) 1.2838; More...

Intraday bias in GBP/USD remains neutral for consolidation below 1.2903 temporary top. With 1.2614 resistance turned support intact, further rally is expected. Firm break of 100% projection of 1.2108 to 1.2614 from 1.2365 at 1.2871 will target 161.8% retracement at 1.3184. Still, price actions from 1.1946 are seen as a correction. Hence we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2614 resistance turned support will turn bias back to the downside for 1.2365 support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

European Open Briefing: The Euro Rallied Following The Outcome Of The First Round Of The French Presidential Election

Global Markets:

- Asian stock markets: Nikkei up 1.25 %, Shanghai Composite fell 1.55 %, Hang Seng declined 0.20 %, ASX 200 gained 0.20 %

- Commodities: Gold at $1277 (-0.95 %), Silver at $16.90 (-0.25 %), WTI Oil at $49.90 (+0.50 %), Brent Oil at $52.80 (+0.65 %)

- Rates: US 10-year yield at 2.31, UK 10-year yield at 1.04, German 10-year yield at 0.25

News & Data:

- UK Rightmove House Price Index MoM (Apr): 1.10% (prev 1.30%)

- UK Rightmove House Price Index YoY (Apr): 2.20% (prev 2.30%)

- French poll: Macron, Le Pen through to second round – RTRS

- Euro jumps, shares firm on French election relief – RTRS

- U.S. stocks futures rally after centrist takes first round in French election – RTRS

CFTC Positioning Data:

- EUR short 22K vs 19K short last week. Shorts increase by 3K

- GBP short 99K vs 106K short last week. Shorts decreased by 7K

- JPY short 30K vs 35K short last week. Shorts trimmed by 5K

- CHF short 14K vs 10K short last week. Shorts increased by 4K

- CAD short 33K vs 32K short. Shorts increased by 1K

- AUD long 43K vs 45K long. Longs trimmed by 2K

- NZD short 15K vs 15K short last week. No change

Markets Update:

The Euro rallied following the outcome of the first round of the French presidential election. The centrist candidate Macron and far-right candidate Le Pen made it into the second round, and the market is expecting that Macron will not have any problems winning the race.

EUR/USD started the new trading week around 1.09, up 150 pips from the Friday close. During the Asian session, the currency pair retraced some of those gains, but found good support ahead of the 1.08 level. The short-term outlook is now positive, and a rally towards 1.10 is likely.

USD/JPY also benefited from the increased risk appetite and made it to 110.55 overnight. The currency pair came slightly under pressure after the Tokyo open, but support is now seen at 109.50.

Upcoming Events:

- 09:00 GMT – German IFO Business Climate

- 13:30 GMT – Canadian Wholesale Sales

- 16:30 GMT – FOMC Member Kashkari speaks

The Week Ahead:

Tuesday, April 25th

- 14:00 GMT – US House Price Index

- 15:00 GMT – US CB Consumer Confidence

- 15:00 GMT – US New Home Sales

- 15:00 GMT – US Richmond Manufacturing Index

Wednesday, April 26th

- 02:30 GMT – Australian CPI

- 13:30 GMT – Canadian Retail Sales

- 15:30 GMT – US Crude Oil Inventories

Thursday, April 27th

- 03:00 GMT – Bank of Japan Rate Decision

- 07:00 GMT – Swiss Trade Balance

- 07:30 GMT – Bank of Japan Press Conference

- 10:00 GMT – Euro Zone Consumer Confidence

- 12:45 GMT – ECB Rate Decision

- 13:00 GMT – German CPI

- 13:30 GMT – US Durable Goods Orders

- 13:30 GMT – US Initial Jobless Claims

- 13:30 GMT – ECB Press Conference

- 15:00 GMT – US Pending Home Sales

Friday, April 28th

- 00:30 GMT – Japanese CPI

- 00:30 GMT – Japanese Unemployment Rate

- 00:50 GMT – Japanese Industrial Production

- 00:50 GMT – Japanese Retail Sales

- 02:30 GMT – Australian PPI

- 06:30 GMT – French GDP

- 07:00 GMT – German Retail Sales

- 07:45 GMT – French CPI

- 09:00 GMT – SNB Chairman Jordan speaks

- 09:30 GMT – UK GDP

- 10:00 GMT – Euro Zone CPI

- 13:30 GMT – US GDP

- 13:30 GMT – Canadian GDP

- 15:00 GMT – US Michigan Consumer Sentiment

- 14:45 GMT – US Chicago PMI

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.79; (P) 109.11; (R1) 109.34; More....

The strong rebound and break of 110.10 resistance indicates short term bottoming at 108.12, on bullish convergence condition in 4 hour MACD. Intraday bias is turned back to the upside for 111.58 support turned resistance. Sustained break there will argue that fall from 118.65 is merely a corrective move and has completed. Outlook will then be turned bullish for 115.49 resistance and above. Meanwhile, below 108.87 minor support will turn bias to the downside and extend the whole decline from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. Current development suggests that it's not completed yet and is extending. In case of deeper decline, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

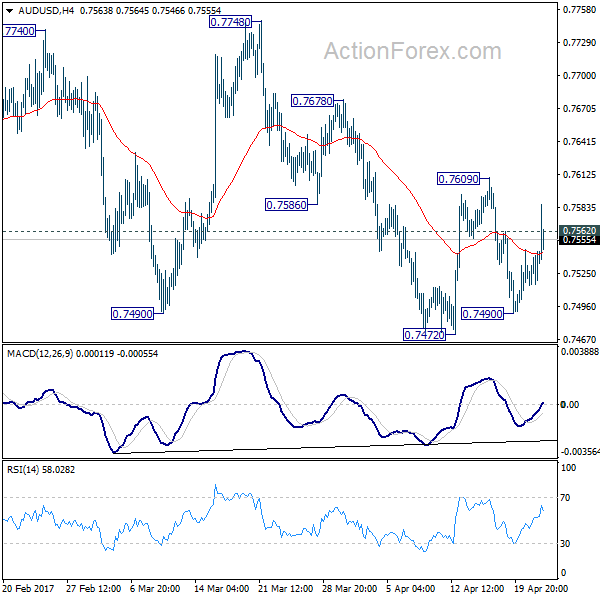

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7524; (P) 0.7535; (R1) 0.7553; More...

Intraday bias in AUD/USD is turned back to the upside with breaking of 0.7562 minor resistance. Break of 0.7609 resistance will indicate resumption of rise from 0.7472 and target 0.7748 high. That will also argue that whole rally from 0.7158 is resuming and put 0.7849 key resistance fibonacci level in focus. On the downside, below 0.71490 will now likely send AUD/USD through 0.7472 low.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8144) and above.

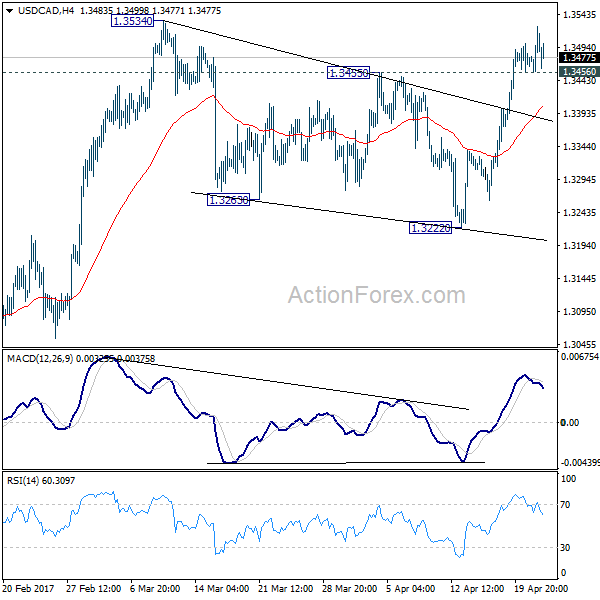

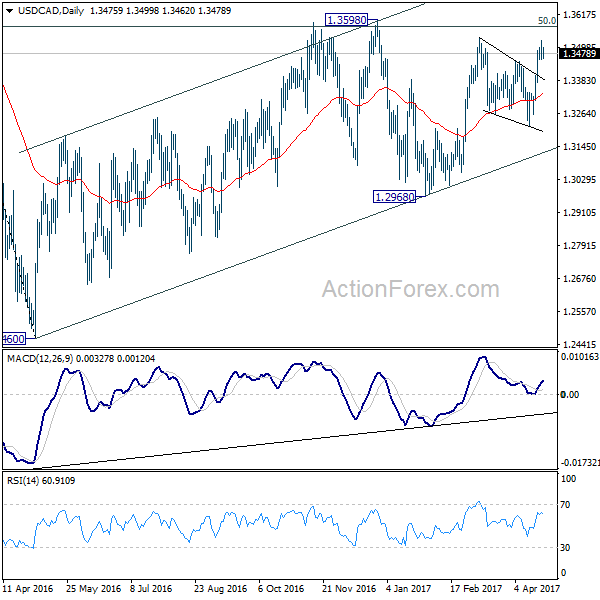

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3459; (P) 1.3492; (R1) 1.3527; More....

With 1.3456 minor support intact, intraday bias remains mildly on the upside for 1.3534 resistance. Break will target 1.3598 high next. Decisive break there will confirm resumption whole medium term rally from 12.460 and target next medium term fibonacci level at 1.3838. . On the downside, below 1.3456 minor support will turn intraday bias neutral and bring consolidation. But retreat should be contained well above 1.3222 support and bring another rally.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. However, break of 1.2968 will argue that the third leg has already started and should at least bring a retest of 1.2460 low. Meanwhile, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Weekly Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

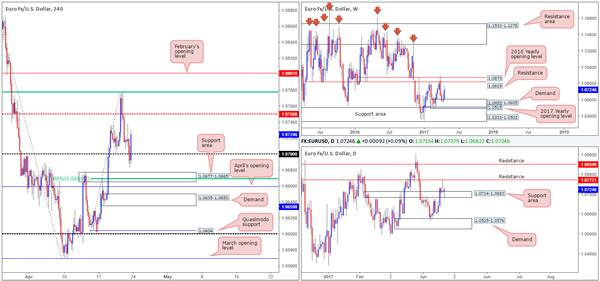

EUR/USD

Weekly gain/loss: + 122 pips

Weekly closing price: 1.0724

Downside momentum diminished last week as weekly buyers actively defended 1.0493-1.0605: a demand area that's beautifully positioned around the top edge of the 2017 yearly opening level at 1.0515/support zone at 1.0333-1.0502. Looking above, the next areas to keep an eyeball on this week are resistance at 1.0819 and the 2016 yearly opening level at 1.0873.

On Thursday, we saw daily price chalk up a selling wick off the underside of resistance planted at 1.0772. Some follow-through action was generated on Friday but was not sufficient enough to overcome the nearby support area seen at 1.0714-1.0683. In the event of a break above the current resistance this week, the next upside angle comes in at 1.0850 (another resistance), whereas a violation of the current support area could find the pair looking to test demand pegged at 1.0525-1.0576.

A brief look at recent dealings on the H4 chart shows the 1.07 handle suffered a rather brutal whipsaw going into Friday's US segment. Despite this, the major ended the day relatively unchanged, closing mid-range between the mid-level resistance at 1.0750 and 1.07.

Our suggestions: Thursday's response to the H4 61.8% Fib resistance (upper green line) at 1.0777 (taken from the high 1.0905) is interesting, given that it's bolstered by the noted daily resistance at 1.0772. Therefore, this region is a zone we'll be watching today for potential shorts. Below 1.07, nevertheless, we have a H4 support area sitting at 1.0677-1.0665 that fuses with a H4 61.8% Fib support at 1.0669. Furthermore, this zone is located just below the current daily support area, so a bounce from here is a possibility. However, traders may want to take into account that April's opening level at 1.0659 is waiting just below this, so be prepared for a possible fakeout!

The opening and early trading will, however, likely be dependent on the outcome of the French Presidential Election. Therefore, we'd advise trading cautiously, at least until the dust settles.

Data points to consider: German IFO business climate at 9am. FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.0677-1.0665 ([waiting for a reasonably sized H4 bull candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: 1.0777 neighborhood ([waiting for a lower-timeframe confirming signal to form is advised before pulling the trigger [see the top of this report] stop loss: dependent on where one confirms the area).

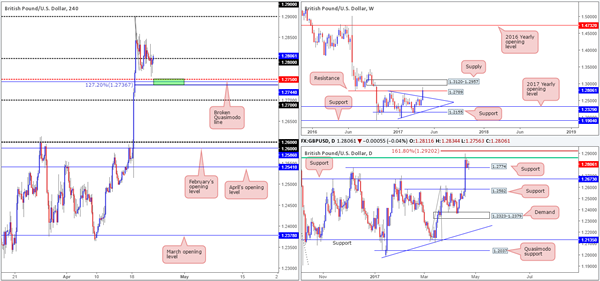

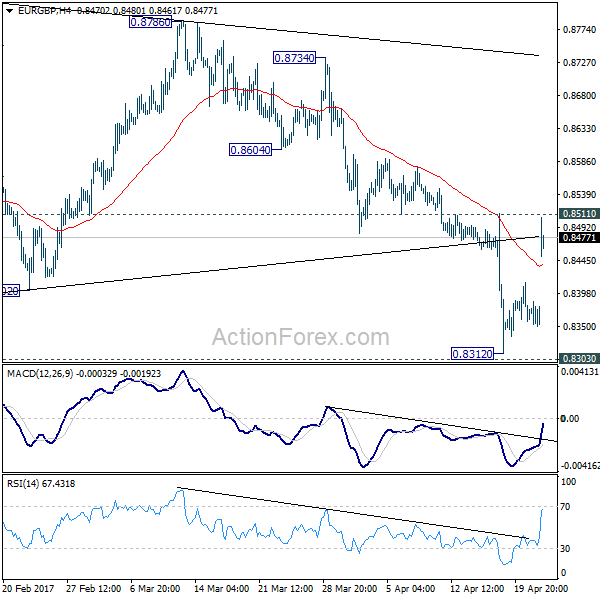

GBP/USD

Weekly gain/loss: + 285 pips

Weekly closing price: 1.2806

The weekly trendline resistance extended from the high 1.2774 was aggressively taken out last week, thus allowing weekly price to marginally close beyond resistance at 1.2789. This could, technically speaking, imply that the buyers might look to challenge supply this week at 1.3120-1.2957.

Since Tuesday, the daily candles have been consolidating between a support established from the 6th December high 1.2774 and a 61.8% Fib resistance (green line) at 1.2859 (taken from the high 1.3445). Also noteworthy here is the nearby 161.8% Fib extension at 1.2920 drawn from the low 1.2108 (brown line).

A quick recap of Friday's trading on the H4 chart shows that price dropped to a fresh low of 1.2756 going into the early hours of the US segment. Leaving the mid-level support 1.2750 unchallenged, the unit ended the week closing six pips above 1.28.

Based on this recent movement, the crosshairs are fixed on 1.2750 (green area) for an intraday bounce north today. Why here? Well, not only are mid-level numbers watched by the majority of the market, there's also a H4 AB=CD 127.2% Fib extension seen nearby at 1.2736 (drawn from the high 1.29) that unites closely with a broken Quasimodo line pegged at 1.2744.

Our suggestions: Our rationale behind looking for a bounce off 1.2736/1.2750, apart from the H4 confluence, is also the fact that this zone is planted directly beneath the current daily support. Therefore, it may perhaps be a fantastic base to help facilitate a fakeout! The only grumble, of course, is that weekly sellers could still be active from resistance mentioned above at 1.2789, hence the reason for not expecting much more than an intraday bounce from this region!

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: 1.2736/1.2750 ([dependent on the time of day, this small zone could be stable enough to consider an intraday trade long from] stop loss: at least five pips beyond the lower edge).

- Sells: Flat (stop loss: N/A).

AUD/USD

Weekly gain/loss: – 31 pips

Weekly closing price: 0.7543

As can be seen from the weekly chart, the bulls failed to generate much follow through after the prior week's bounce from the support area marked at 0.7524-0.7446. Should the buyers eventually regain consciousness here, however, the next upside hurdle can be seen at a trendline resistance taken from the high 0.7835, followed closely by supply at 0.7849-0.7752.

Thursday's bounce (and Friday's follow through) seen from the support area at 0.7449-0.7506 (housed within the above said weekly support area) is interesting. The reason? In the event that the bulls continue to bid price into positive territory from here, an AB=CD formation may complete (black arrows), which, as seen by the AB=CD 127.2% Fib ext. at 0.7645, ties in beautifully with supply at 0.7679-0.7640. For that reason, the bulls may still have a hand in this fight.

Switching gears and moving over to the H4 chart, nevertheless, our team has noted a group of potentially troublesome resistances ahead. First in line is the mid-level resistance at 0.7550, then a supply at 0.7562-0.7552, followed with an AB=CD 127.2% Fib ext. at 0.7560 chiseled from the low 0.7491, and finally a 61.8% Fib resistance at 0.7565 drawn from the high 0.7610.

Our suggestions: We're sure you'll agree with us that going long, despite what the higher-timeframe structures suggest, would be chancy owing to the said H4 resistances. And likewise, a short, although tempting given the confluence, would be just as much of a risk. With that in mind, we'll remain on the sidelines for the time being and reassess structure around Tuesday's open.

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/JPY

Weekly gain/loss: + 39 pips

Weekly closing price: 108.95

Looking at this market from the weekly scale, the pair clearly remains in bearish territory. Following the break of the support area at 111.44-110.10 two weeks back, the runway south still appears clear for the unit to test the support area coming in at 105.19-107.54 (holds an AB=CD 161.8% ext. at 107.14 taken from the high 118.66).

The story on the daily chart shows the demand at 108.55-109.17 to be pretty much dead and buried. We feel bids are incredibly fragile and will eventually lead to a test of the nearby support area at 107.15-107.90, which happens to also hold a 61.8% Fib support at 107.84 taken from the low 101.19.

Having put in a top just ahead of the mid-level resistance 109.50 on Thursday, the H4 candles continued to recede on Friday, eventually popping below the 109 handle into the close. There's H4 demand seen to the left of current price, but it does not really emphasize strength, mainly because of the huge tail seen marked with a green arrow on the 20th April at 108.72.

Our suggestions: Trading short beyond 109 seems to be a valid call. However, we would ideally like to see the H4 candles retest 109 as resistance beforehand and follow up with a H4 bear candle (preferably a full-bodied close). If this should come to fruition, the first take-profit target can be seen around the H4 demand at 108.32-108.45, followed closely by another H4 demand at 107.77-108.21 which sits on top of the aforementioned daily support area.

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 109 region ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

USD/CAD

Weekly gain/loss: + 170 pips

Weekly closing price: 1.3494

Weekly price has spent the best part of a month and a half teasing the underside of the 2017 yearly opening level at 1.3434. That was, of course, until the bulls came to life last week and closed above the monthly level. Despite the almost near-full-bodied candle, reinforcing this line is a well-defined double-top formation seen around the 1.3588 neighborhood (green circle). Therefore, the bears could still have a hand in this game yet!

Turning over a page to the daily timeframe, supply at 1.3494-1.3439 is seen hanging in there despite Friday's spike seen through the top edge of this zone. Even if this supply does give way, there's always a back-up supply seen just above it at 1.3598-1.3559.

The US dollar, as seen clearly on the H4 chart, made considerable ground against its Canadian counterpart on Friday following lower-than-expected inflation data. Price, however, failed to sustain gains beyond the 1.35 handle (likely due to the supply zone seen at 1.3534-1.3508) and ended the week tapping a broken Quasimodo line at 1.3490.

Our suggestions: H4 action is exceedingly restricted at the moment. Below 1.3490, there's demand sitting at 1.3458-1.3476, shadowed closely by a support area pegged at 1.3450-1.3437. To the upside, we have the 1.35 handle and the said supply to contend with. As a result, until these structures are cleared and some space is seen, we do not see much to hang our hat on in terms of a trade setup. So, for now at least, we'll hold fire and take a back seat.

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

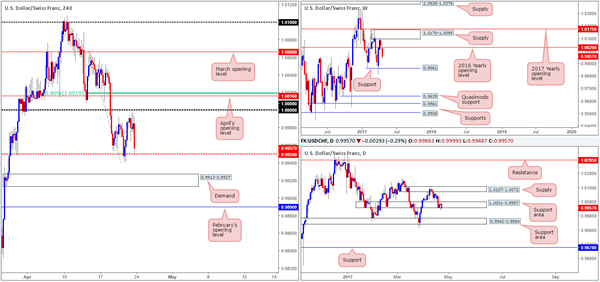

USD/CHF

Weekly gain/loss: – 89 pips

Weekly closing price: 0.9957

The USD/CHF clocked lower prices last week following an earlier test of weekly supply seen at 1.0170-1.0095. Consequent to this, the 2016 yearly opening level at 1.0029 was cleared, leaving downside relatively open until we reach weekly support at 0.9861.

The daily support area at 1.0001-0.9957 held ground on both Wednesday and Thursday last week, but, as you can see, failed miserably on Friday. The minor close seen beyond this area, coupled with weekly flow pointing to further selling, could be enough to convince investors that bids are weakening. The next area beyond this zone falls in at 0.9842-0.9884: another support area that houses the said weekly support level within.

Looking over at Friday's action on the H4 chart, the Swissy came within touching distance of connecting with parity (1.0000) during the London morning session. Bids eventually weakened here and saw price topple down to the mid-level support at 0.9950 into the closing bell. Although the higher timeframes indicate that the bears may be in the driving seat at the moment, selling into 0.9950 would not be something we'd advise. Under usual circumstances, we'd wait for this level to be taken out and attempt to trade the retest, but given nearby demand at 0.9913-0.9927, it's challenging.

Our suggestions: Unless one is willing to enter long from 0.9950 against possible weekly/daily sellers, we do not see much on offer. For us personally, we'll remain flat and reassess going into tomorrow's open.

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

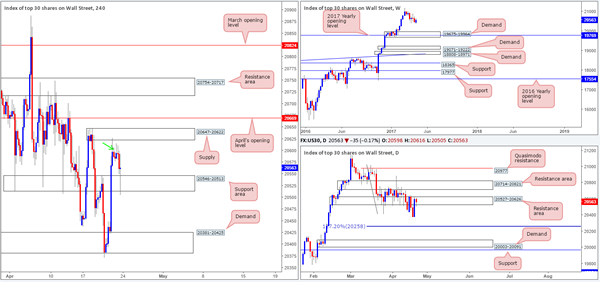

DOW 30:

Weekly gain/loss: + 93 points

Weekly closing price: 20563

(Trade update: Short taken from 20586 ended up as a breakeven trade).

As far as we can see, weekly action, despite gaining last week, still looks poised to extend the pullback seen from record highs of 21170 down to 19675-19964: a demand area that's bolstered by the 2017 yearly opening level at 19769.

Daily movement is currently seen retesting the resistance area at 20527-20626. Should the bears manage to defend this zone, the next downside target from this angle sits at 20258: an AB=CD 127.2 Fib ext. taken from the high 21022.

H4 supply, as expected, continued to hold ground on Friday, consequently forcing price to test the lower edge of a support area seen at 20546-20513. In order for our desk to become sellers here, we'd really like to see the current support area taken out. From that point, one can either choose to enter on the break, or conservatively wait for price to retest the broken barrier as resistance. We choose the latter.

Our suggestions: As highlighted above, we're looking for a H4 close to be seen below the current H4 support area. This, followed up with a retest and a H4 bear candle (preferably a full-bodied close), would, in our opinion, be enough to justify a short in this market, targeting the H4 demand picked at 20381-20425 as an initial take-profit target.

Data points to consider: FOMC member Kashkari speaks at 4.30 and again at 8.30pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to engulf the H4 support area at 20546-20513 and then look to trade any retest seen thereafter. Following the retest, a H4 bearish candle would be ideal. Stop loss: beyond the candle's wick).

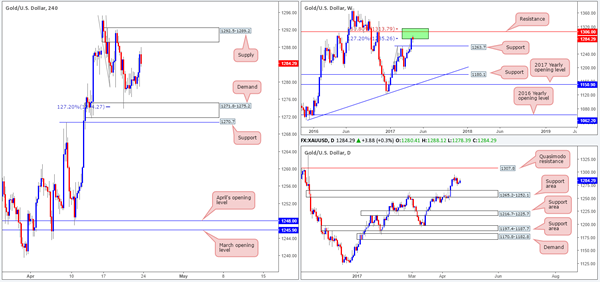

GOLD

Weekly gain/loss: – $3

Weekly closing price: 1284.2

Breaking a five-week bullish phase, the weekly bears elbowed their way into the market last week from within the walls of two Fibonacci extensions 161.8/127.2% at 1313.7/1285.2 taken from the low 1188.1 (green zone). Although there is a possibility that price may pop north to test nearby resistance at 1306.0, we feel the support at 1263.7 is likely to be challenged sometime soon.

Filtering down to the daily chart, the candles are seen loitering mid-range between a Quasimodo resistance at 1307.8 and a support area penciled in at 1265.2-1252.1. Of particular interest here is the weekly support mentioned above is located within the upper limits of this daily zone, and the daily Quasimodo resistance is sited directly above the said weekly resistance.

Wednesday's bounce seen from the H4 demand base at 1271.8-1275.2, more specifically the H4 AB=CD 127.2% ext. at 1274.2, saw the yellow metal gravitate to a high of 1288.1 by the week's end. With the US dollar now seen testing a minor H4 demand (99.65-99.83 – see the US dollar index), coupled with the position of price on the weekly chart (see above), this could point to a selloff in the gold market.

Our suggestions: Should our analysis be correct and gold does indeed turn bearish, we would not be willing to sell until price shakes hands with the H4 supply seen at 1292.5-1289.2. Still, since there's a chance that bullion could stretch north to test weekly resistance/daily Quasimodo resistance, we'd strongly recommend waiting for a H4 bear candle to form (preferably with a full-bodied close) and enter based on this momentum with stops positioned above the wick.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1292.5-1289.2 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8352; (P) 0.8369; (R1) 0.8387; More...

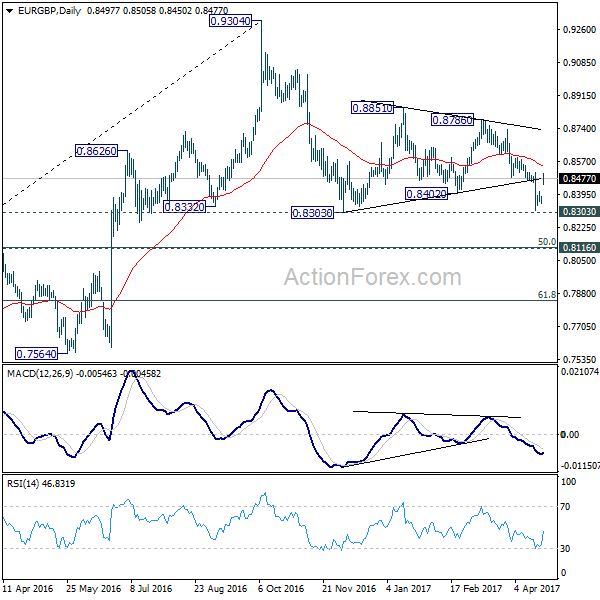

EUR/GBP rebounds strongly today following broad based strength in Euro. But upside is limited below 0.8511 resistance so far. Intraday bias remains neutral and further fall is still expected. Break of 0.8303 will extend the corrective fall from 0.9304 to 0.8116/20 key cluster support. We'd expect strong support there to completion the correction and bring rebound. Meanwhile, on the upside, break of 0.8511 will turn bias back to the upside for 0.8786 resistance instead.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is possibly ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

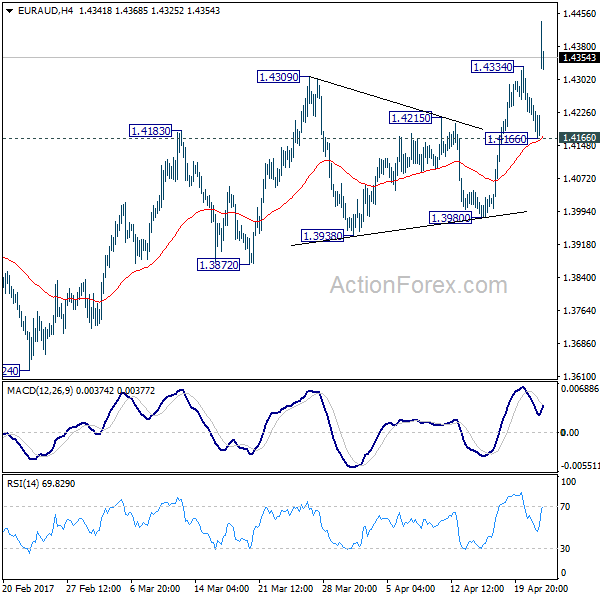

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4165; (P) 1.4213; (R1) 1.4259; More...

EUR/AUD's rally resumed by surging through 1.4334 to as high as 1.4437 so far. Intraday bias is back on the upside for 1.4721 key resistance. As noted before, we're holding on to the case off trend reversal after defending 1.3671 key support. Decisive break of 1.4721 should confirm. On the downside, break of 1.4166 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after defending 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0662; (P) 1.0686; (R1) 1.0701; More...

EUR/CHF surges sharply to as high as 1.0815 and the development argues that whole rise from 1.0629 is resuming. Intraday bias is back on the upside for 1.0823 resistance first. Decisive break there will carry larger bullish implications and will target 1.0897 resistance next. On the downside, break of 1.0718 support is needed to indicate short term reversal. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0823 resistance will affirm this bullish case. Further break of 1.0999 will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0652 support holds.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.17; (P) 139.66; (R1) 140.13; More....

GBP/JPY rises to as high as 141.88 so far today. The strong break of 140.08 resistance should affirm our bullish view. That is, consolidation pattern from 148.42 has completed with three waves down to 135.58, after hitting 135.39 fibonacci level. Intraday bias is back on the upside and current rise should extend to 144.77 resistance next. On the downside, break of 139.19 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.