Sample Category Title

Consensus-Beating UK Retail Sales Triggers a EUR/GBP Break Lower

Markets

Second tier US economic data outgunned yesterday’s ECB meeting. Strong retail sales, lower-than-expected weekly jobless claims and a sharp rebound in the Philly Fed business outlook sparked a test of the 4% barrier by the US 2-yr yield (+3.3 bps in the close) but it’ll take more for this psychologically important level to break. US money markets do increasingly begin to question whether the Fed will cut rates at both of the remaining meetings this year. Longer maturities including the 10-yr (+7.7 bps) and the 30-yr (+9.4 bps) underperformed amid ongoing economic resilience (even outright strength). German rates fell 2.4 bps at the front and added 4.4 bps at the back end of the curve. The ECB cut rates for a third time this cycle to 3.25% yesterday. The economic outlook deteriorated and inflation, after the expected reacceleration into the year’s end, should hit the 2% target sooner than previously expected. Risks in both cases are tilted to the downside. President Lagarde as usual used data dependency to refrain from any guidance but people familiar with the matter afterwards said that another cut in December was highly likely. Not only has that been market’s base case for some time now, they are also toying with the idea of a supersized Fed-style cut (50% chance). EUR/USD’s awful October month continued yesterday, with especially dollar strength pushing the pair below 1.0835 support. DXY advanced further north towards 104. It hasn’t seen that level ever since the poor July payrolls report of early August kicked off a bad spell for the greenback. Sterling seized the opportunity to wipe out Wednesday’s CPI losses against the euro. EUR/GBP returned towards the multi-year lows just north of 0.83. Consensus-beating UK retail sales this morning risk triggering a break lower. That would bring 0.82 on the radar. An article in the Financial Times by IMF head Georgieva grabs our attention this morning. She warned of an “unforgiving” economic backdrop for government finances, referring to a combination of low growth and high & rising debt. A growing share of government revenues was being used to cover interest payments while weak growth makes it difficult to tackle the mountain of debt. The IMF earlier this week estimated global debt to hit a record $100tn by the end of the year. And yet, many governments – most notably those from the US and China – continue to run substantial deficits. The fiscal debate is increasingly drawing attention as we are now in the final stretch towards the US elections. While its outcome is highly uncertain, it is clear that neither Trump nor Harris is keen to deliver on the budget consolidation the IMF is recommending.

News & Views

Chinese Q3 GDP in the third quarter grew 0.9% Q/Q compared to downwardly revised growth of 0.5% in Q2. Y/Y growth and YTD Y/Y growth printed at 4.6% and 4.8% respectively, close to expectations. Growth thus remains below the 5.0% full year target for 2024. Looking at the underlying developments, industrial production beat expectations with a rise of 5.4% Y/Y from 4.5%. Retail sales improved from Q2 rising from 2.1% from 3.2% (YTD Y/Y 3.3%) but nevertheless suggest lagging domestic demand. The housing market remains deep in negative territory. Property investment printed at -10.1% YTD Y/Y. Residential property sales were 24% lower compared to the Jan-Sept period of last year. The surveyed unemployment rate improved though, from 5.3% tot 5.1%. The data confirm the need of more stimulus to prevent a further decline of the domestic property market and to support domestic demand in an attempt to avoid a deflationary spiral. Official comments after the publication showed awareness that a complex international environment might be a factor of uncertainty for growth. The CSI 300 gains 1.6%, supported by a new PBOC funding schemes to support the stock market. The yuan gains modestly (USD/CNY 7.116).

Japanese inflation figures for September slowed from August, but less so than expected. CPI ex. fresh food prices but including oil products rose 2.4% Y/Y from 2.8%. The decline in core inflation was mainly due to government subsidies to mitigate gas and electricity prices. Core inflation ex-fresh food an energy even rose marginally from 2.0% to 2.1%. Markets expect the BoJ to stay on hold when deciding on interest rates at October 31 meeting but see a rising chance of a next rate hike in December or January. Aside the CPI data, Japanese vice finance minister of economic affairs assessed recent moves in the yen (decline to 150) as slightly one-sided that deserve ongoing monitoring. USD/JPY declines marginally this morning to trade near 149.85 currently.

ECB Cut Fuels Appetite, Weighs on Euro

The European Central Bank (ECB) lowered its interest rates by 25bp yesterday, in a widely expected and priced in move. Chief Christine Lagarde highlighted that inflation is coming under control, warned that there could be a temporary uptick, but the figures will be sustainably back to target by next year and that the Eurozone will unlikely enter recession. It was rather a dovish cut. Note that the bank said that it will maintain its meeting-by-meeting data-dependent approach in place and is not committed to a particular rate pattern, but the bank’s confidence that inflation is being tamed, and the morose economic data boost the probabilities of further rate cuts from the ECB in the coming meetings. The expectation now is that the ECB will cut its rates at every policy meeting until March. Next stop: December.

As such, the euro sold off after the ECB decision. The single currency is preparing to test the 83 cents level against sterling – which has also been weakening this month on rising dovish Bank of England (BoE) expectations and softening British inflation. The October budget is causing some weakness in sterling but the outlook remains more bullish for sterling than for the euro: the 82 cents level now seems within reach – under the condition that the Autumn budget doesn’t trigger chaos by the end of the month. Against the US dollar, the euro extended losses to 1.0811 yesterday and is consolidating near the 1.0840 level this morning. But some of the weakness could also be attributed to the strength of the US’ own economic data that showed a stronger-than-expected retail sales in September, a bigger-than-expected jump in Philadelphia Fed’s manufacturing index and jobless claims in line with expectations. Atlanta Fed’s GDP Now forecast will be revised today but the forecast already points at a 3.4% growth in the US GDP for Q3 – screaming that the Federal Reserve’s (Fed) 50bp cut was probably unnecessary last month. Somehow, none of the good news derails the Fed cut expectations for the November meeting. Activity on Fed funds futures gives around 90% for another 25bp cut next month, the US 2-year yield is hovering a touch below the 4% mark, the 10-year yield consolidates near 4.10%, but the US dollar index reached its 200-DMA yesterday for the first time since August. The greenback is overbought, but there is room for further recovery as most of the news that come from the US is looking good. Unlike in Europe.

The medium-term outlook for the EURUSD turns negative. The RSI indicator suggests that the pair has now stepped into the oversold market conditions and a period of consolidation and a minor correction would be healthy at the current levels. Nevertheless, price rallies should see resistance near the 1.0980/1.10 area that shelters the 1.10 psychological mark but also the major 38.2% Fibonacci retracement that should keep the actual bearish trend intact. On the downside, a sustainable move below the 1.0835, the major 61.8% Fibonacci retracement on the summer rally, should pave the way for a deeper selloff toward the 1.07/1.0730 range.

In the equities space, the Stoxx 600 reacted positively to the dovish ECB decision on Thursday. The prospect of further policy easing helped taming the disappointing ASML and LVMH results earlier this week and should help counterweight the gloomy economic outlook of the Eurozone and not-so-promising earnings season. After all, the European stocks are more cyclical than their major peers and should continue to benefit from a period of global monetary easing. And hey, the latest data from China printed a slower-than-expected growth in the latest quarter, but industrial production and retail sales jumped more than expected in September. Improvement in Chinese sales could improve the fortunes of the China-sensitive European luxury stocks.

On the other side of the Pacific Ocean, things are looking good – to say the least. The earnings season in the US there is going well. Netflix announced another surprise in subscriptions when it reported its Q3 results yesterday after the bell. The company added 5 mio new subscribers as the password sharing crackdown continued to operate its magic. Most of the new customers joined from Europe, Middle East and Africa. Netflix shares jumped 5% in the afterhours trading. Elsewhere, TSM announced an easy beat when it reported its Q3 earnings yesterday and boosted its forecasts. Its CEO reiterated that one of its clients said there is ‘insane demand’ for its chips that will be built by TSM. That client’s share (Nvidia) gained 0.89% yesterday on strong TSM earnings, it wasn’t much compared to the rallied that we are used to, but the stock hit a fresh record for the first time since June.

Overall, the S&P500 hit a fresh record yesterday, even though the index gave back gains on worries that the Fed’s rate cutting plans look farfetched with the amount of good economic and corporate data on the wire. The Bank of America’s latest fund manager survey showed that the S&P500 has reached the level of optimism last seen during the post-pandemic rally. Allocations to stocks surged and exposure to bonds fell in September. The high level of optimism means that there is room for it to fade. This being said, the VIX index is gently fading and the headlines give no particular reason to reverse appetite, for now.

Tensions Rise After Killing of Yahya Sinwar

In focus today

Swedish September LFS is expected to show a small increase in the unemployment rate to 8.4 % SA. That said, we will rather keep an eye on employment and hours worked which should recover after the summer lull.

Economic and market news

What happened overnight

In China, Q3 GDP grew 4.6% y/y in July-September, which is the slowest pace since early 2023, showcasing need for more support and undershooting Beijing's target of 5%. The monthly batch of data showed stronger than expected industrial production at 5.4% y/y (cons: 4.5%) and retail sales at 3.2% y/y (cons: 2.5%). Moreover, the Central Bank of China initiated its two-stage funding schemes in which they are utilizing newly created monetary policy tools to pump USD 112.38bn into the stock market.

In Japan, the core inflation (CPI excl. fresh food) for September was slightly above expectations (2.3%) printing 2.4% y/y. The slowdown from last month's figure of 2.8% was largely due to government intervention of temporary rollouts.

In the Middle East overnight, Hezbollah announced a 'new and escalating phase' in its confrontation with Israel, while Iran said the spirit of resistance would strengthen following Israel's reported killing of Hamas leader Yahya Sinwar on Thursday. Sinwar, who became Hamas' leader after Ismail Haniyeh's assassination in July, was seen as the mastermind behind the 7 October attack on Israel.

What happened yesterday

In the euro area, as expected ECB cut rates for the third time this year to bring the deposit rate to 3.25%. The weakness in the incoming economic data since the last governing council meeting was acknowledged by Lagarde, and that data led to a further confidence on the inflation path being on track which led to the rate cut. Yesterday's decision was unanimous. Markets traded mostly sideways through the press conference as no guidance of how aggressive, or potential end point of the cutting cycle was given. For more details, please see Flash: ECB Review - A rate cut - and awaiting more data, 17 October.

Prior to the ECB meeting, the final inflation data for September printed a 1.7% y/y confirming the low inflation momentum, driven by services, which supported the ECB's assessment.

In the US, the September retail sales growth surprised to the topside. Control group sales grew by +0.7% m/m SA. However, the seasonal adjustment factor provided unusually strong lift to the monthly figures, and the y/y growth rate in non-seasonally adjusted terms declined to 2.7% (from 3.9%). The bottom line is that US private consumption remains on a solid, but still cooling trend. Markets have also paid close attention to the jobless claims data. Surprisingly, the number of weekly initial claims declined to 241k (from 260k) even though the data should now cover at least the initial impact from hurricane Milton.

In Norway, Norges Bank's Ida Wolden Bache held a speech to the Centre for Monetary Economics (CME) BI in the Norwegian business school where she discussed the options that Norges Bank is considering when it comes to the liquidity regime shift starting in 2025 as the government will no longer sterilise the seignorage of Norges Bank by issuing bonds. The assumption has been that this will lead to a rise in reserves in the system (when the government spends money on the budget), but Bache opened the door for limiting the rise in the FX reserves as option number 2. Essentially this is a decision of whether the liabilities side or the asset side of the balance sheet should take the adjustment - and this could have a market impact. If they opt for an asset side control it would be positive for NOK FX and positive for FRA/Nowa. We therefore enter a tactical long

In Denmark, as expected the Central Bank followed ECB 1:1 and cut its policy interest rate by 25 bp to 2.85%.

In Turkey, the CBRT kept their key policy rate at 50% as expected by markets.

FI: Markets added to rate cut bets ahead of the December ECB meeting - now 30bp vs 25bp prior to the meeting - following Lagarde's dovish remarks on the disinflationary process and a Bloomberg story suggesting that ECB officials see another cut at the next meeting as 'highly likely'. 2Y German yields headed lower through the press conference, but the move reversed in the last part of the session with levels slightly higher by the close. Long-end rates rose across Europe and the US as US retail sales and claims data both came out stronger than expected. German ASW-spreads continued to grind lower with the Bund ASW-spread now trading just above 21bp.

FX: Industrial-sensitive currencies lead losses in yesterday's session with a dovish twist to the ECB communication driving additional EUR losses. EUR/USD continues to trend lower while USD/JPY has breached the 150-mark on higher US yields. The NOK found some much needed support in the latter part of the session which also contributed to a rebound in NOK/SEK.

Sterling Rallies After Strong UK Retail Sales, Yen Recovers on Japan’s Verbal Intervention

Sterling rises broadly today, driven by unexpectedly strong retail sales figures for September. This recovery suggests that the negative impact of weaker-than-expected CPI data earlier in the week has been fully absorbed by the market. While it now seems likely that BoE will proceed with interest rate cuts in November, the pace of monetary easing is expected to be more cautious compared to ECB or Fed, unless the UK economy experiences a more pronounced downturn.

Meanwhile, Yen also gained some strength today after USD/JPY pair briefly broke through the 150 psychological support. This triggered verbal intervention from Japanese officials, with Vice Finance Minister Atsushi Mimura cautioning about "one-sided, sudden moves" in the currency market. He emphasized that Japan is monitoring the situation closely for signs of speculative activity, signaling the government’s readiness to act if needed.

In broader market movements, sentiment across Asia received a lift following People’s Bank of China's implementation of specialized lending facilities aimed at supporting share buybacks and providing liquidity to institutional investors. These moves were part of the central bank's broader efforts to stabilize financial markets, initially outlined in a major announcement at the end of September.

For the week, Dollar is leading as the strongest currency, followed by Loonie and Sterling. On the other end of the spectrum, Swiss Franc is the weakest performer, with Euro and Kiwi not far behind. Aussie and Yen are positioning in the middle. However, with the current surge in momentum, Sterling has the potential to climb higher as the week comes to a close.

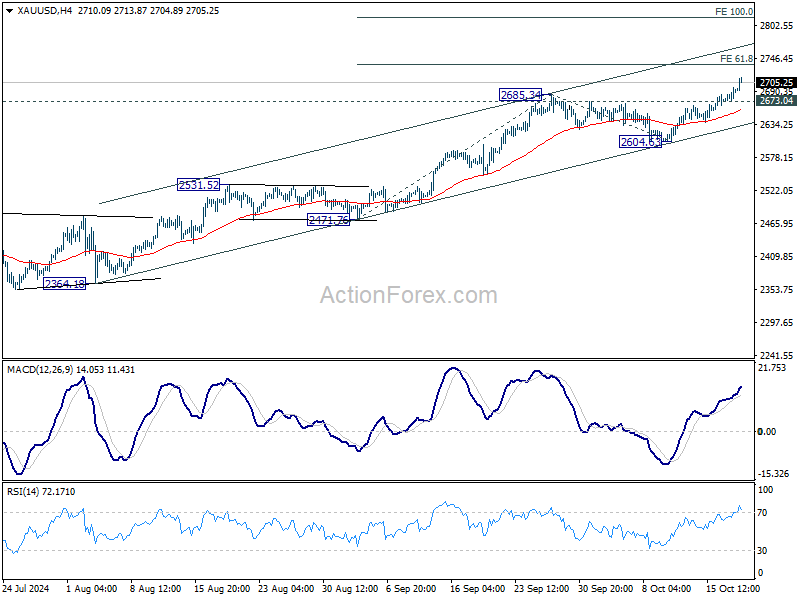

Technically, Gold powers through 2700 handle as its record run continues. Further rise is expected as long as 2673.04 minor support holds, to 61.8% projection of 2471.76 to 2685.34 from 2604.53 at 2736.62. Decisive break there could trigger upside acceleration to 100% projection at 2818.21 next.

In Asia, Nikkei rose 0.18%. Hong Kong HSI is up 2.84%. China Shanghai SSE is up 2.72%. Singapore Strait Times is up 0.41%. Japan 10-year JGB yield rose 0.0061 to 0.971. Overnight, DOW rose 0.37%. S&P 500 fell -0.02%. NASDAQ rose 0.04%. 10-year yield rose 0.080 to 4.096.

UK retail sales rises 0.3% mom in Sep, extended rebound in consumption

UK retail sales volumes rose by 0.3% mom in September, defying expectations of -0.3% decline. This marked the highest retail sales index level since July 2022, reflecting stronger-than-anticipated rebound in consumer activity.

Looking at the broader picture, sales volumes in Q3 surged by 1.9% compared to Q2, the joint-largest quarterly rise since July 2021. This upward momentum, shared with March 2024.

Japan's CPI core slows to 2.4%, core-core edges up

Japan's core CPI, which excludes fresh food, eased from 2.8% yoy to 2.4% yoy in September, slightly above expectations of 2.3% yoy. Despite the slowdown, core inflation has remained above BoJ's 2% target for well over two years.

The deceleration in price gains is largely attributed to government utility subsidies, which have helped lower household expenses. Headline CPI fell from 3.0% yoy to 2.5%, with gas prices subtracting 0.55 percentage points from the overall figure. This indicates that without government intervention, inflation would have remained higher.

Meanwhile, CPI measure that excludes both food and energy costs—often referred to as core-core CPI—increased from 2.0% yoy to 2.1% yoy, suggesting underlying inflation remains firm. However, service prices saw a slight decrease in momentum, slowing from 1.4% yoy to 1.3% yoy.

China’s Q3 GDP growth slows to 4.6%, stimulus impact yet to solidify

China’s economy grew 4.6% yoy in Q3, slowing slightly from 4.7% in Q2 but in line with market expectations. This marks the slowest pace of growth since early 2023, as external pressures and a challenging global environment continue to weigh on the country's economic performance. On a quarterly basis, GDP expanded by 0.9%.

The National Bureau of Statistics noted that the economy remained "generally stable with steady progress," highlighting continued increase in production and demand, alongside stable employment and prices.

The NBS emphasized that the effects of the government's stimulus policies were beginning to show, with "major indicators displaying positive changes recently."

However, the bureau also cautioned that the external environment was becoming "increasingly complicated and severe," underscoring the need to further solidify the foundation for sustained recovery.

Key economic data released alongside the GDP report suggested signs of resilience in some sectors. Industrial production increased by 5.4% yoy in September, surpassing expectations of 4.6% yoy. Retail sales also exceeded forecasts, rising 3.2% yoy compared to the expected 2.4% yoy. Fixed asset investment saw a 3.4% year-to-date increase, slightly above 3.3% expected by analysts.

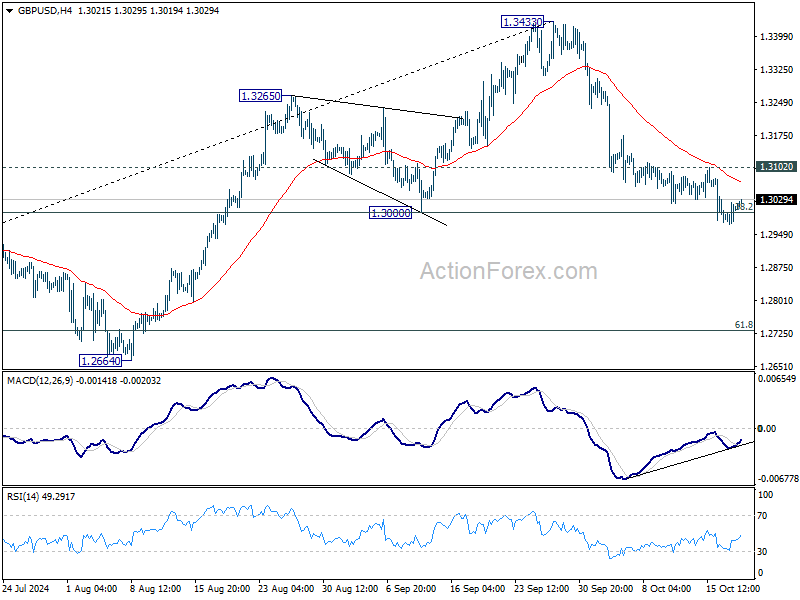

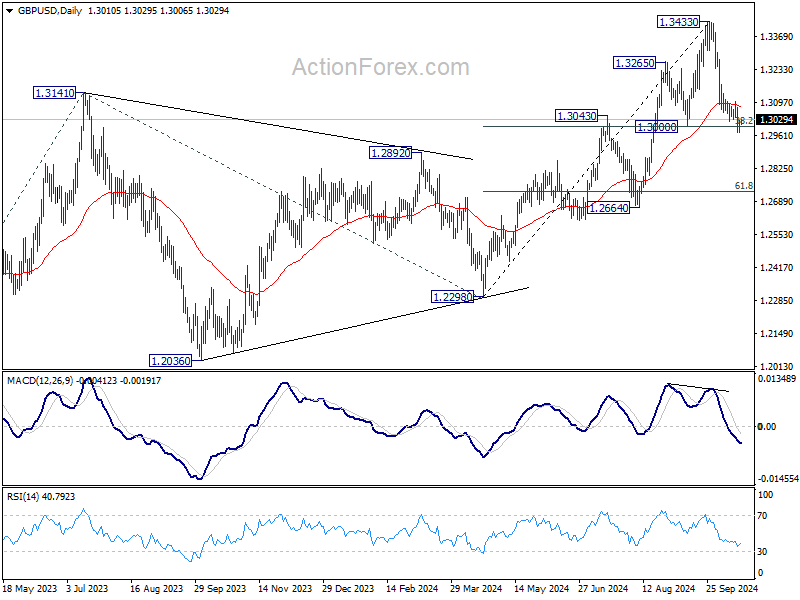

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2982; (P) 1.3003; (R1) 1.3031; More...

Intraday bias in GBP/USD is turned neutral with current recovery. On the downside, sustained trading below 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732. Nevertheless, strong bounce from current level, followed by break of 1.3102 minor resistance, will turn bias back to the upside for stronger rebound towards 1.3433.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

UK retail sales rises 0.3% mom in Sep, extended rebound in consumption

UK retail sales volumes rose by 0.3% mom in September, defying expectations of -0.3% decline. This marked the highest retail sales index level since July 2022, reflecting stronger-than-anticipated rebound in consumer activity.

Looking at the broader picture, sales volumes in Q3 surged by 1.9% compared to Q2, the joint-largest quarterly rise since July 2021. This upward momentum, shared with March 2024.

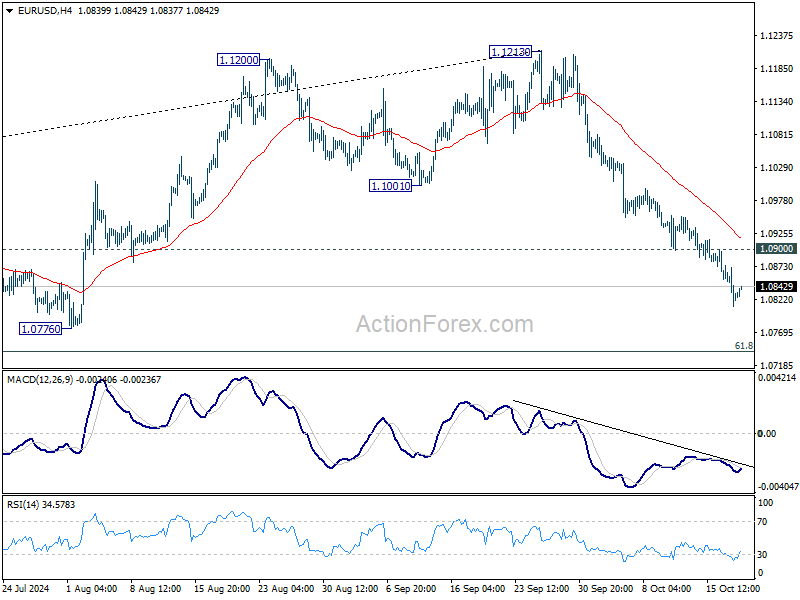

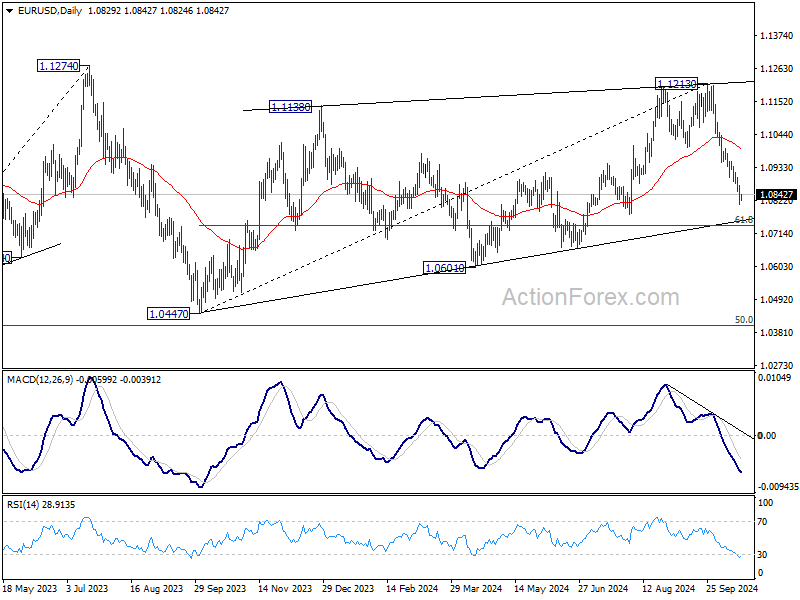

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0803; (P) 1.0839; (R1) 1.0866; More....

Intraday bias in EUR/USD stays on the downside for the moment. Fall from 1.1213 is in progress for 61.8% retracement of 1.0447 to 1.1213 at 1.0740 next. Firm break there will target 1.0601 support next. On the upside, above 1.0900 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

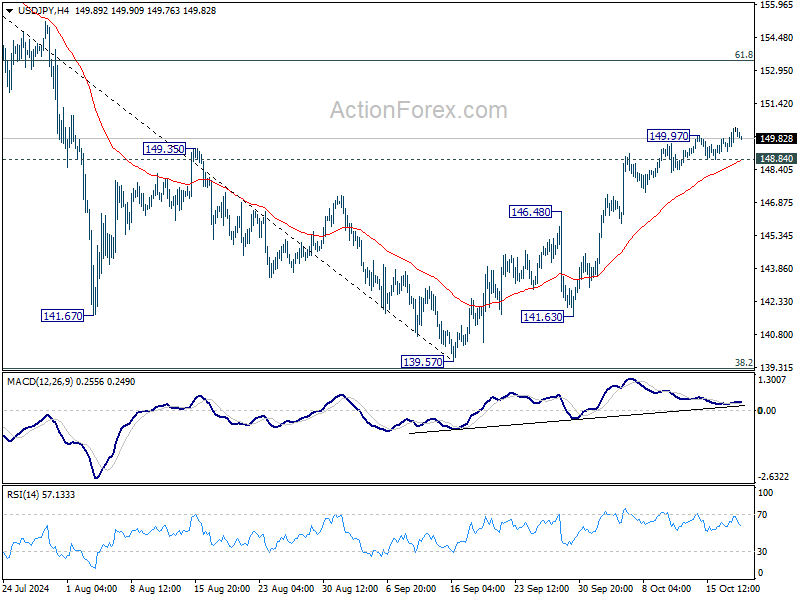

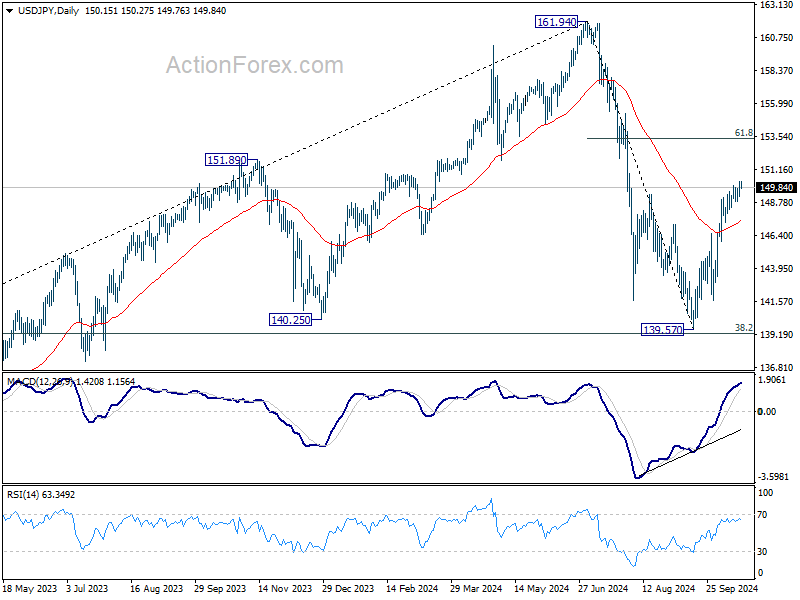

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.54; (P) 149.93; (R1) 150.62; More...

Intraday bias in USD/JPY is back on the upside with break of 149.97 temporary top. Current rise from 139.57 should target 61.8% retracement of 161.94 to 139.57 at 153.39 next. On the downside, below 148.84 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 146.48 resistance turned support holds.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2982; (P) 1.3003; (R1) 1.3031; More...

Intraday bias in GBP/USD is turned neutral with current recovery. On the downside, sustained trading below 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732. Nevertheless, strong bounce from current level, followed by break of 1.3102 minor resistance, will turn bias back to the upside for stronger rebound towards 1.3433.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

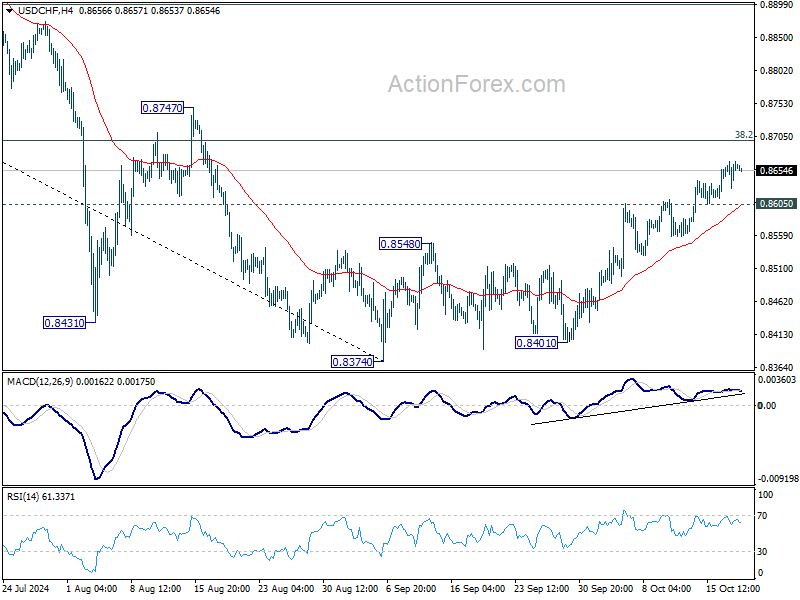

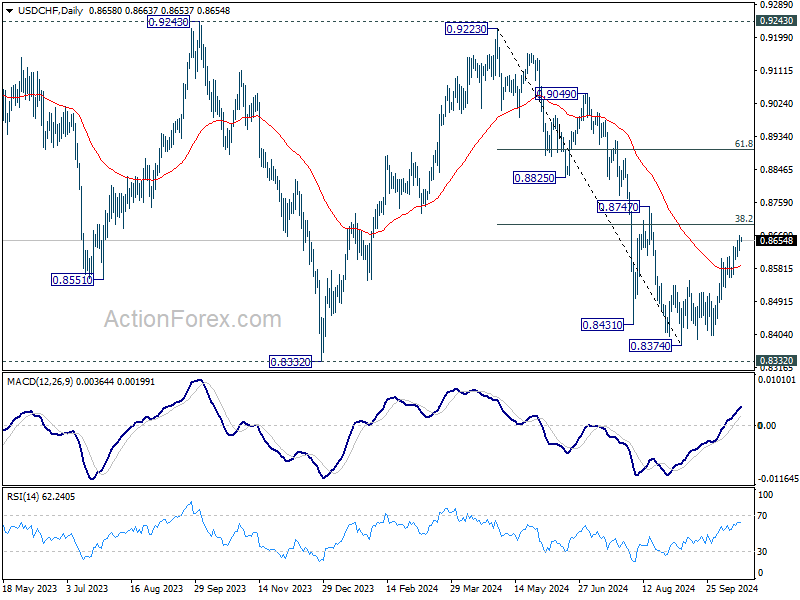

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8637; (P) 0.8653; (R1) 0.8677; More…

Intraday bias in USD/CHF stays on the upside as rise from 0.8374 is in progress. Sustained break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. On the downside, below 0.8605 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

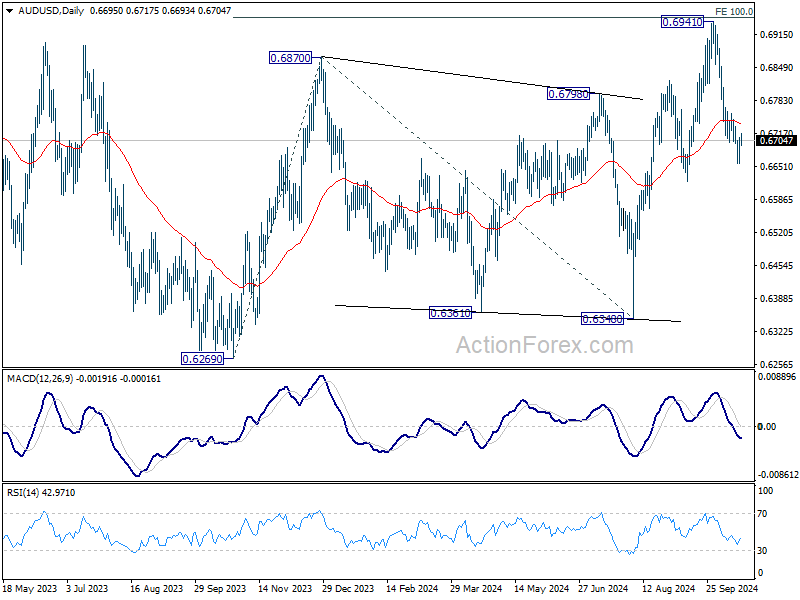

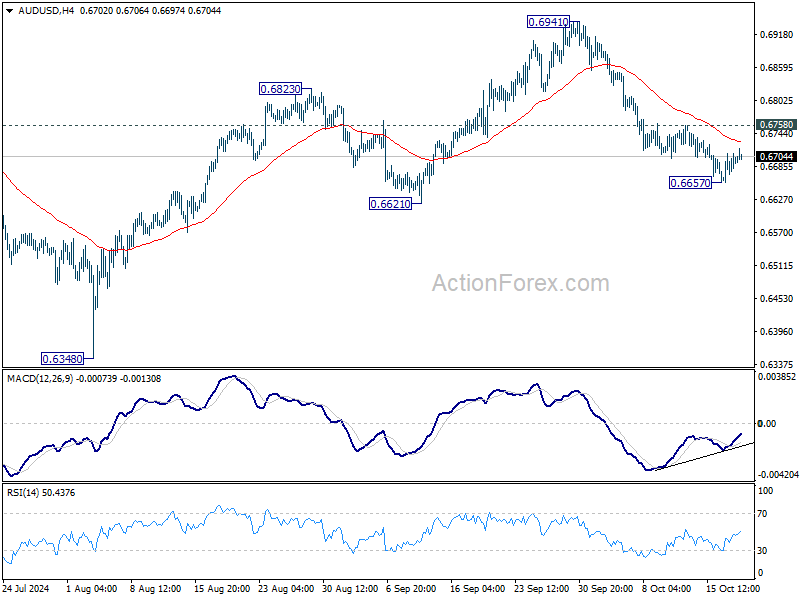

AUD/USD Daily Report

Daily Pivots: (S1) 0.6666; (P) 0.6689; (R1) 0.6718; More...

Intraday bias in AUD/USD remains neutral for consolidation above 0.6657 temporary low. Further decline is expected as long as 0.6758 resistance holds. Below 0.6657 will resume the fall from 0.6941 short term top to 0.6621 structural support. Decisive break there will pave the way back to 0.6348 support next. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.6758 will turn bias back to the upside for retesting 0.6941 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.