Sample Category Title

(ECB) Monetary policy decisions

The Governing Council today decided to lower the three key ECB interest rates by 25 basis points. In particular, the decision to lower the deposit facility rate – the rate through which the Governing Council steers the monetary policy stance – is based on its updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission. The incoming information on inflation shows that the disinflationary process is well on track. The inflation outlook is also affected by recent downside surprises in indicators of economic activity. Meanwhile, financing conditions remain restrictive.

Inflation is expected to rise in the coming months, before declining to target in the course of next year. Domestic inflation remains high, as wages are still rising at an elevated pace. At the same time, labour cost pressures are set to continue easing gradually, with profits partially buffering their impact on inflation.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The Governing Council today decided to lower the three key ECB interest rates by 25 basis points. Accordingly, the interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will be decreased to 3.25%, 3.40% and 3.65% respectively, with effect from 23 October 2024.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the PEPP, reducing the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

Refinancing operations

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

EUR/USD Technical: Overstretched Decline Heading into ECB Meeting

- A 25bps cut by the ECB is likely to have been fully priced in.

- The current high expectation of another ECB rate cut in December faces an increased repricing risk.

- Watch the 1.0780/0750 key medium-term support on the EUR/USD.

In the past four weeks, the EUR/USD has plummeted by 3.3% from its 25 September high of 1.1214 to today’s current intraday low of 1.0849 at this time of the writing ahead of the European Central Bank (ECB) monetary policy decision.

Based on a one-month rolling performance basis, the Euro is the second weakest major currency against the US dollar with a loss of 2.5%, above the Japanese yen which was the weakest major currency as it shed -6.4% against the US dollar.

25 bps cut is likely to have been fully priced in

The current price movement of the EUR/USD is likely to have fully priced in today’s 25 basis points (bps) cut by the ECB, its third cut in 2024 to bring the key deposit rate to 3.25% as headline inflation in the Eurozone decelerated to 1.7% y/y in September, below ECB’s target of 2% for the first time in more than three years.

In addition, lacklustre readings seen in September’s manufacturing and services PMIs data suggest increasing signs of a weakening economic condition in the Eurozone.

Hence, market participants are looking at one more rate cut of 25 bps by the ECB in December before 2024 ends.

Oversold and overstretched

Fig 1: Major & medium-term trends of EUR/USD as of 17 Oct 2024 (Source: TradingView)

Through the lens of technical analysis, the 4-week decline seen in the EUR/USD has led the daily RSI momentum indicator to reach its oversold region for the first time since 15 April 2024.

Current price action is also coming close to the major “Symmetrical Triangle” range support at 1.0780/0750 (see Fig 1).

In addition, the daily Bollinger Bandwidth indicator has risen sharply since 1 October 2024 which suggests an overstretched decline condition at this juncture that increases the odds of at least a short-term mean reversion rebound scenario.

If the 1.0780/0750 key medium-term pivotal support holds on the EUR/USD, it may shape a mean reversion rebound towards the 1.0950 intermediate resistance in the first step.

However, a breakdown and a daily close below 1.0750 see the continuation of the impulsive down move sequence to expose the next medium-term support at 1.0620.

AUD/USD Rises Following Strong Australian Employment Data

AUD/USD rebounded on Thursday after three consecutive days of declines. This was supported by robust employment data from Australia, which bolstered the hawkish outlook on the Reserve Bank of Australia's (RBA) monetary policy.

Key Employment Data Highlights:

- Job creation: the Australian economy added 64.1k jobs in September, significantly surpassing the expected 25.0k. This marked improvement suggests strong economic momentum

- Unemployment rate: the rate held steady at 4.1%, aligning with expectations and underscoring the labour market's resilience

- Labour force participation: the participation rate rose to a record 67.2% in September from 67.1% in August, beating the forecast of 67.1%. This increase reflects a growing workforce, which could sustain consumer spending and economic activity

These indicators of labour market strength make it less likely that the RBA will opt for rate cuts in the near term. Additionally, RBA Deputy Governor Sarah Hunter emphasised the central bank's commitment to controlling inflation, which continues to be a concern amid sustained price increases. Analysts now suggest that the RBA is unlikely to cut rates until at least the first half of the next year, considering the tight labour market conditions.

Technical analysis of AUD/USD

The AUD/USD pair is extending its downward movement towards a target of 0.6645. After testing the resistance at 0.6700 from below, it continues its decline. Once the 0.6645 level is reached, a new consolidation range is expected to form above this level. A breakout above this range could initiate a corrective phase towards 0.6790. This bearish trend is supported by the MACD indicator, which remains below zero and points downwards, indicating sustained downward momentum.

On the hourly chart, AUD/USD has completed a downward wave to 0.6660, followed by a corrective rise to 0.6700. The pair is expected to continue its decline to the 0.6645 level. After this target is met, a potential reversal could push the price towards 0.6710. The Stochastic oscillator supports this outlook, with its signal line below 50 and heading towards 20, suggesting that there may be further downside before any significant recovery.

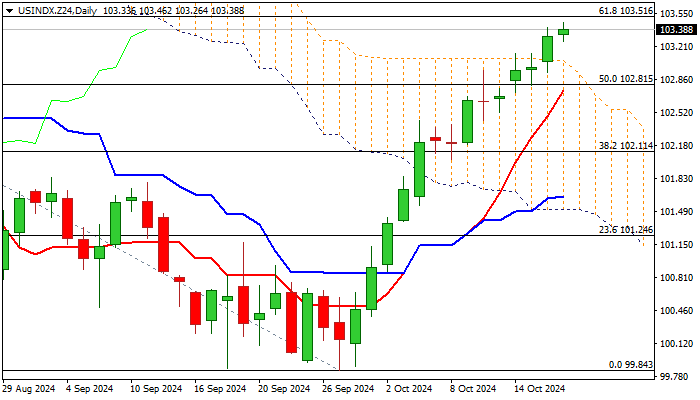

Dollar Outlook: Continues to Advance on Cooling Fed Rate Cut Bets, Trump Election Victory Expectations

The Dollar continues to trend higher against the basket of its major counterparts and trades at the highest since early August during European session on Thursday.

Possibility of election win by Republican candidate Donald Trump and negative impact of recent upbeat US economic data to further Fed rate cut expectations, were the key factors to support dollar.

The dollar index is in strong uptrend for the third straight week and has so far retraced over 50% of larger 105.78/99.84 fall.

Recent break above pivotal barriers at 102.95/103.05 (100DMA / top of thick daily cloud) generated strong bullish signals, contributing to bullish daily studies.

Bulls pressure next key barriers at 103.51/56 (Fibo 61.8% / 200DMA) but may face headwinds here due to overbought conditions on daily chart.

Limited dips to be ideally contained by 103.00/102.80 zone (broken 100DMA / cloud top / broken Fibo 50%) to offer better levels to re-enter bullish market.

Release of US weekly jobless claims and September retail sales will be in focus today.

Res: 103.56; 103.80; 104.00; 104.38.

Sup: 103.26; 103.00; 102.81; 102.44.

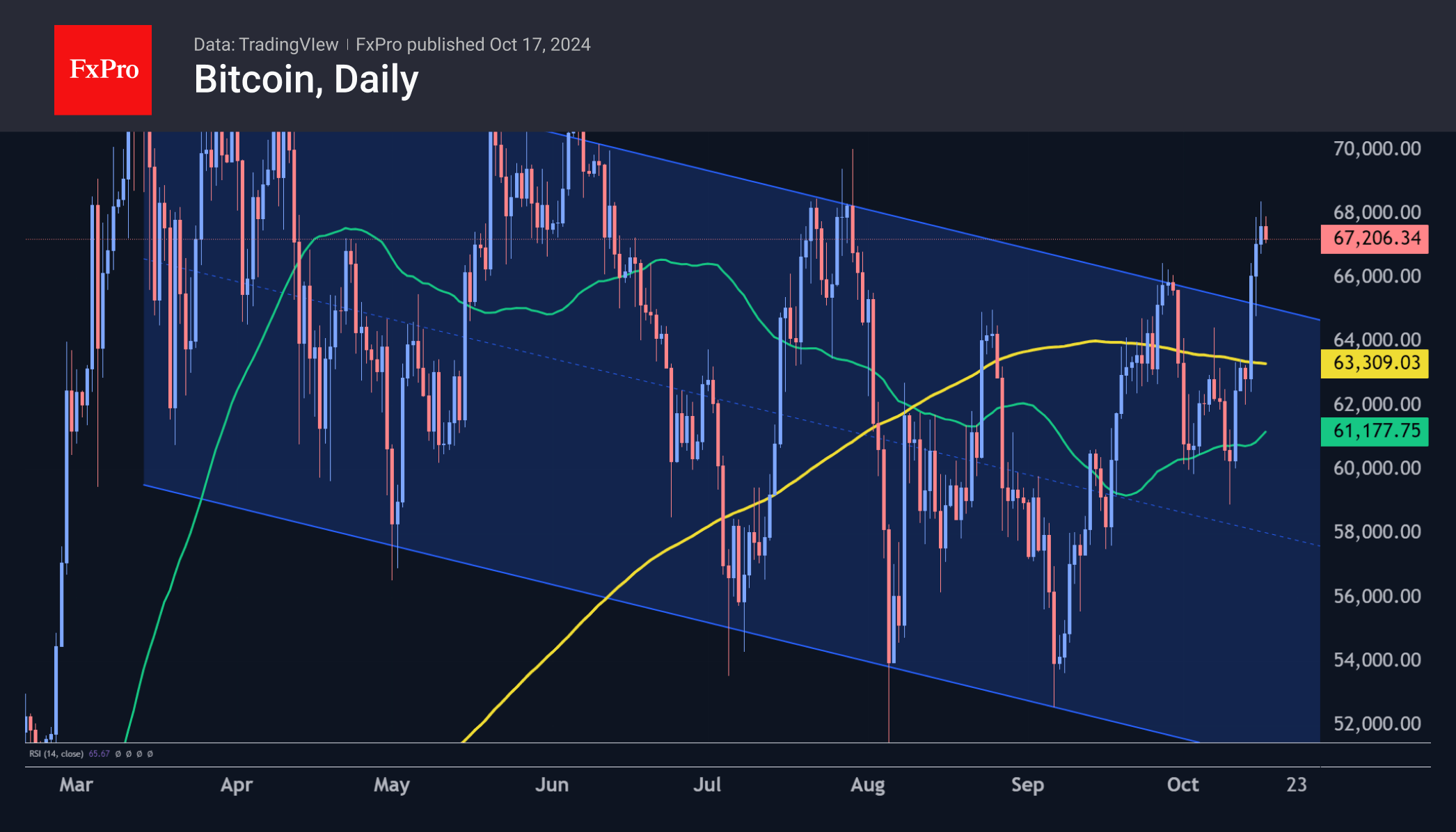

Bitcoin Price Set to Reach New High Before US Elections

According to the BTC/USD chart, Bitcoin's price reached $68,000 in mid-October, a level not seen since late July. Can this upward momentum continue?

Jeff Kendrick, head of digital asset research at Standard Chartered Bank, predicts that Bitcoin could rise to $73,800 before the US presidential elections in November, which would mark a new all-time high.

Kendrick highlights several factors that may drive Bitcoin's price higher:

→ Less stringent regulation: A more favourable regulatory environment, as indicated by recent news regarding BNY Mellon's accounting practices, could benefit Bitcoin's price.

→ MicroStrategy's ambitions: The company plans to transform into a "Bitcoin bank," potentially enabling it to generate revenue by lending cryptocurrency in the future.

Today's technical analysis of the BTC/USD chart reveals:

→ The price is forming a long-term upward channel (shown in blue).

→ Since March, price fluctuations have created a downward channel (shown in purple), which may be seen as an interim correction within the main bullish trend. Technical analysts might refer to this as a "bullish flag" pattern.

→ A significant price increase on October 14 led to the formation of a bullish Fair Value Gap (FVG), indicating buyer dominance over sellers.

Given these factors, it is reasonable to expect that the $63,000 to $65,000 range could serve as a launchpad for bulls aiming to break through the multi-month resistance represented by the upper boundary of the purple corrective channel.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under ASIC Rules respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

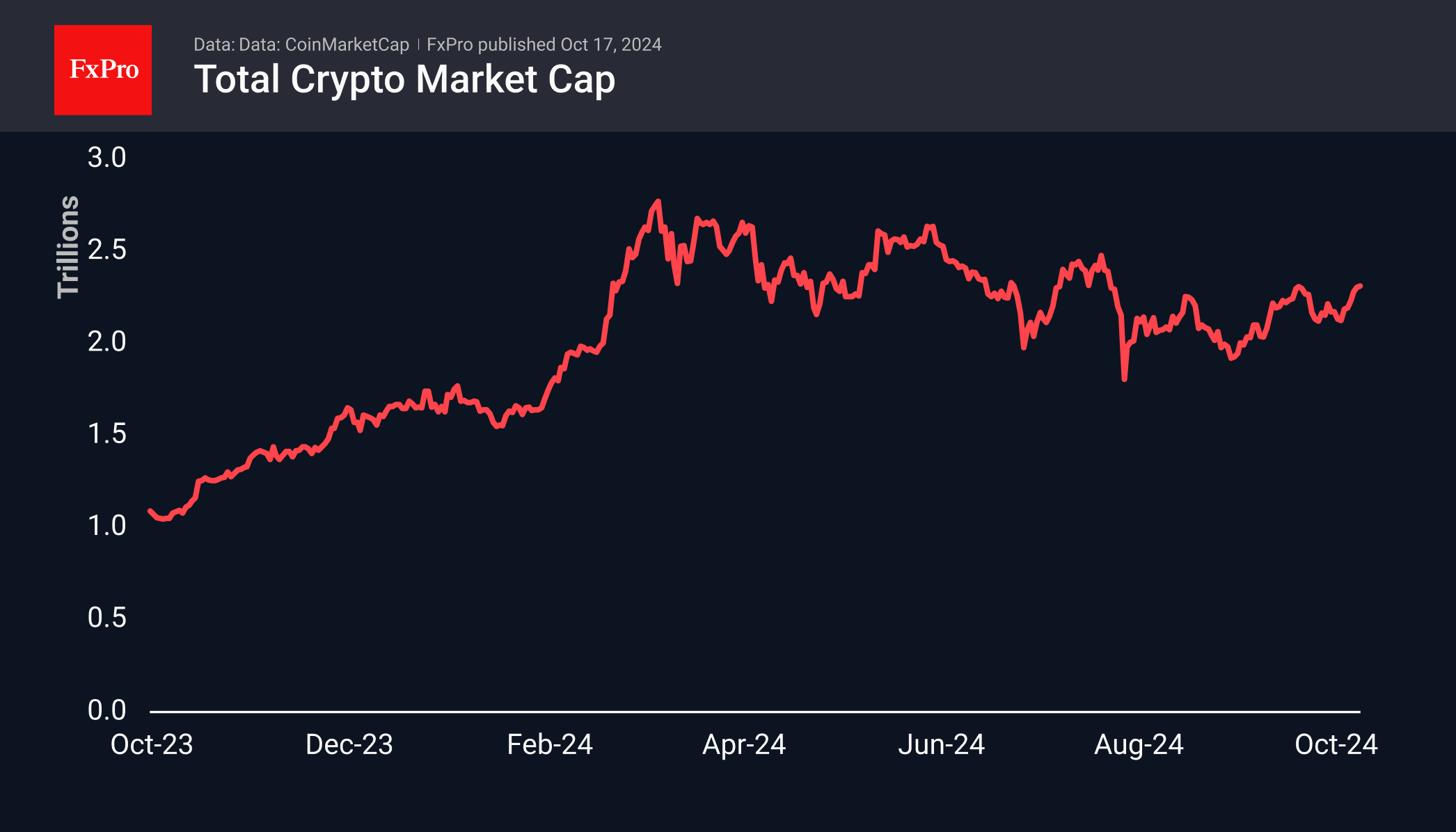

Crypto Market Stabilises at the Top

Market Picture

The cryptocurrency market remains steady at around $2.31 trillion in market capitalisation, mirroring the local highs of late September, while Bitcoin continues to climb. The pause in overall growth has led to a 2-point dip in the Cryptocurrency Market Sentiment Index, now at 71—still reflecting a high level of greed.

Bitcoin is currently at $67.1K, showing a 0.5% increase over the past 24 hours but a slight 0.5% decline since the day’s opening. These minor fluctuations largely mirror the stabilisation seen in stock indices. This pause benefits the Bitcoin bulls, allowing the market to cool off after the recent rally.

The upcoming ECB interest rate decisions and US retail sales figures, set to be released just before the US session begins, could potentially disrupt the market’s current stability.

News Background

Tesla has transferred its entire 11,509 BTC holdings, valued at approximately $760 million, to unknown addresses, as reported by Arkham Intelligence. Meanwhile, SpaceX, also owned by Elon Musk, continues to hold 8,285 BTC in Coinbase’s Prime Custody wallet service.

Since Bitcoin reached new highs in March, the gap between demand and ‘active supply’ has widened, a trend that Glassnode notes is historically a precursor to periods of heightened volatility.

According to its issuer, Tether, at the end of the third quarter of 2024, the USDT stablecoin was used by 330 million cryptocurrency wallets and on-chain accounts. The company compared the figure to the US population and attributed the increase in users to second-tier solutions and the development of the TON ecosystem.

The Kenya Revenue Authority is introducing a new control system that will integrate with cryptocurrency exchanges. This system will enable real-time tracking of crypto transactions to ensure timely tax collection.

Eurozone goods exports fall -2.4% yoy in Aug, imports down -2.3% yoy

Eurozone goods exports fell -2.4% yoy to EUR 216.7B in August. Goods imports fell -2.3% yoy to EUR 212.1B. Trade balance was a EUR 4.6B surplus. Intra- Eurozone trade fell -4.3% yoy to EUR 183.5B.

In seasonally adjusted term, goods exports fell -0.1% mom to EUR 237.9B. Goods imports rose 1.0% mom to EUR 226.8B. Trade balance reported EUR 11.0B surplus. Intra-Eurozone trade fell -0.5% mom to EUR 215.1B.

Eurozone CPI finalized at 1.7% in Sep, CPI core at 2.7%

Eurozone CPI in September was finalized at 1.7% yoy, down from August’s 2.2% yoy. Core CPI, which excludes volatile components like energy, food, alcohol, and tobacco, was finalized at 2.7% yoy, slightly lower than August’s 2.8% yoy.

The largest contributor to Eurozone CPI was the services sector, adding +1.76 percentage points to the annual rate, followed by food, alcohol, and tobacco (+0.47 pp). Non-energy industrial goods added +0.12 pp, while energy dragged inflation down by -0.60 pp as prices continued to ease.

On a broader level, EU inflation was also finalized lower at 2.1%, down from 2.4% in August. Inflation rates across member states varied significantly, with the lowest annual rates recorded in Ireland (0.0%), Lithuania (0.4%), and Slovenia and Italy (both at 0.7%).

In contrast, Romania (4.8%), Belgium (4.3%), and Poland (4.2%) registered the highest inflation rates. Compared to August, annual inflation fell in twenty Member States, remained stable in two, and rose in five.

EUR/USD: Holds Near Multi-Week Low Ahead of ECB’s Widely Expected 0.25% Rate Cut

The euro fell to the lowest in 2 ½ months in early European trading on Thursday, holding firmly in red for the fourth straight day, a part of larger three-week downtrend.

Markets await the ECB’s policy decision, due later today, with wide expectations that the central bank will deliver the third rate cut this year.

The ECB is likely to cut interest rates by 25 basis points today (Deposit rate to move to 3.25% from 3.50%) as inflation is under control and the economy is stagnating, partially due to high borrowing cost.

Markets also expect the ECB to cut rates three more times until March 2025, though confirmation for such action is unlikely to be heard from President Lagarde and other policymakers, as they stick to their mantra that any policy decision will be based on economic data ahead of every meeting.

Bearish picture on daily chart (strong negative momentum / Wednesday’s close below 200DMA / 10/100 bear-cross) and weakening weekly studies (14-w momentum indicator is breaking into negative zone / 5/200WMA death cross) support bearish scenario.

Bears eye immediate targets at 1.0835 Fibo 61.8% of 1.0601/1.1214) and 1.0809/00 (weekly cloud base / psychological), ahead of 1.0775 (Aug 1 higher low) and 1.0745 (Fibo 76.4%).

Broken 200DMA reverted to initial resistance (1.0872), followed by falling daily Tenkan-sen (1.0922) and the base of thick daily Ichimoku cloud (1.0968) which should cap corrective upticks to keep larger bears in play.

Res: 1.0872; 1.0907; 1.0935; 1.0968.

Sup: 1.0825; 1.0800; 1.0775; 1.0745.

ECB Expected to Cut Rates by 25 bps to 3.25%

Markets

Core bonds eked out some gains yesterday ahead of the ECB meeting and US data including retail sales and jobless claims scheduled for release today. Bunds outperformed Treasuries with yields losing around 4 bps across the curve. US yields lost between -0.8 (2-yr) and -2.4 bps (30-yr). Gilts rallied after September CPI decelerated more than expected. Even with underlying gauges still well above 2%, front-end yields in the UK tanked more than 11 bps as markets stacked up monetary easing bets. Sterling slipped but managed to claw back some of the losses against an overall weak euro as trading evolved. EUR/GBP rose from 0.833 to 0.836. Cable (GBP/USD) lost the 1.30 big figure (July interim high, September correction low & 38.2% retracement on the April-Sep 2024 rise). We don’t want to call it a formal technical break lower just yet. The pair may still rebound towards 1.32 to finish a developing head-and-shoulders pattern. The US dollar held the upper hand against all peers but CAD. DXY took out 103.34 (50% recovery on the YtD high to low). EUR/USD dropped further below 1.09 and closed in on intermediate support around 1.0835. The bottom of the bearish August-October double top formation is located around 1.08. The ECB is expected to cut rates by 25 bps to 3.25%. That’s a complete U-turn since ECB chair Lagarde basically ruled that out in September because of the short inter-meeting period. Ongoing disinflation and especially weak PMIs made many policymakers, led by Lagarde’s example, change tack. That’s data-dependency to the fullest – an argument we expect Lagarde to use to defend today’s decision. For that same reason she’s unable to offer much guidance for December, given there are two PMI’s, two CPI’s and Q3 wage data. That’s a recipe for volatility: markets currently expect 100 bps of cuts over the next four meetings (today included). Meanwhile inflation numbers are all but certain to pick up again in the coming months. One less dire PMI outcome and things may shift drastically. For the time being though, we hold on to our short-term target for EUR/USD around 1.08 amid ongoing (technical) USD strength. Front-end European yields discount enough rate cuts in our view, suggesting the recent October lows (around 2% for the German 2-yr, 2.2% for the swap equivalent) are a solid bottom.

News & Views

Data published by the Australian Bureau of Statistics this morning showed that the labour market remains strong. The economy added a net 64.1 k of jobs in September, up from 42.6 k in August. The rise was mainly due to a jump in full-time employment (+51.6k compared to a small decline of -5.9k in August). Measured by the overall change in employment, it was the sixth straight month that employment growth beat expectations. The unemployment rate was unchanged at 4.1%. According to the ABS, employment has risen by 3.1% in the past year, growing faster than the labour force. The participation rate also rose 0.1% to a record high 67.2%. “The record employment-to-population ratio and participation rate shows that there are still large numbers of people entering the labour force and finding work in a range of industries, as job vacancies continue to remain above pre-pandemic levels” ABS said. After the release of the report, money markets further reduced the chance of a first RBA rate cut in December to 30% from about 50%. Inflation in August declined to 2.7% Y/Y, within the RBA 2-3% target range, but this was mainly due to support measures of the government to cap electricity prices for consumers. The RBA probably will look through this decline and combined with an ongoing strong labour market, it won’t feel a rush to cut from the 4.35% currently. The Aussie dollar this morning rebounded modestly against a broadly strong dollar (AUD/USD 0.669).

At a press conference held this morning, China Housing Minister Ni Hong announced that the country will raise credit support for ‘white list’ housing projects to Rmb 4tn. The measure is part of series that were recently announced to address a deep-rooted real estate crisis in the country and prevent further negative spill-over effects to the economy. Until now, loans for the approved white list amounted to Rmb 2.23tn. White list projects can receive financing to facilitate that developers can further complete construction projects and deliver homes to buyers. For now, the reaction of Chinese markets to press conference was muted (CSI 300 +0.25%). The yuan is losing marginal ground against the dollar (USD/CNY 7.123).