Sample Category Title

BoJ’s Himino signals readiness for further rate hikes if economic confidence grows

BoJ Deputy Governor Ryozo Himino reaffirmed the central bank's commitment to adjusting its monetary policy if confidence in the economic outlook strengthens. In a speech, Himino stated that if BoJ gains "growing confidence" in its economic and price forecasts, it "will adjust the degree of monetary accommodation," signaling readiness for rate hikes ahead.

Himino outlined the baseline scenario for fiscal 2025 and 2026, describing it as a "reasonably balanced state" where inflation aligns with the price stability target, and economic growth "slightly above cruising speed". However, he cautioned against two risk scenarios: one where inflation remains above 2% and another where it falls well below 2% and fails to recover.

Addressing recent financial market volatility, Himino noted that Yen's appreciation might ease the import cost pressures faced by small and medium-sized enterprises, though it could reduce yen-denominated profits for export industries. He reassured that Japanese firms have developed competitive strengths. Stock price volatilities, while influential, should not significantly undermine business sentiment.

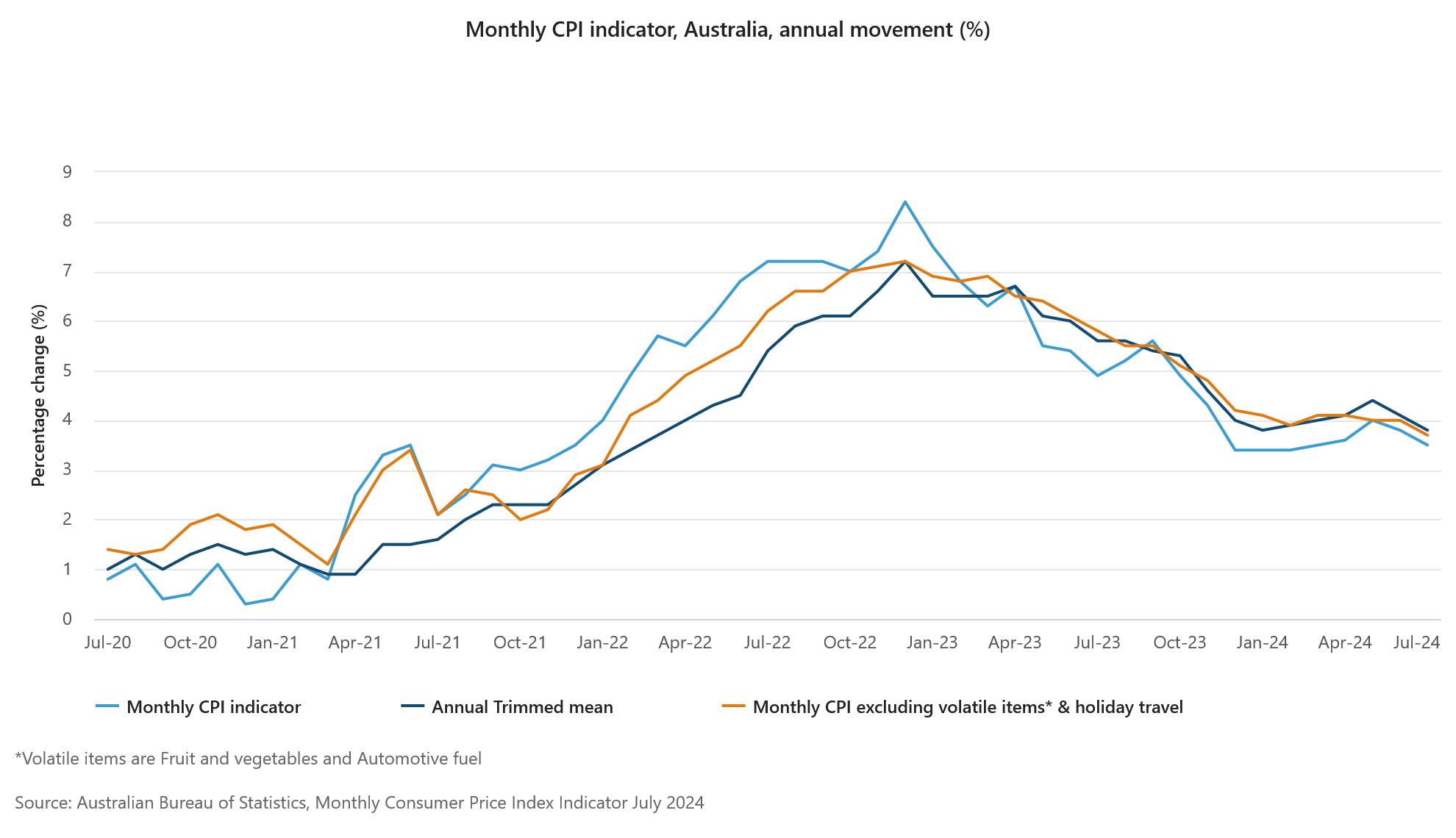

Australia’s monthly CPI slows to 3.5% in Jul, slightly above expectations

Australia's monthly CPI inflation slowed from 3.8% yoy in June to 3.5% yoy in July, above the expected 3.4% yoy. CPI excluding volatile items and holiday travel also eased, dropping from 4.0% yoy to 3.7% yoy. Additionally, the annual trimmed mean CPI, a measure that smooths out irregular price fluctuations, decreased from 4.1% yoy to 3.8% yoy.

The most significant contributors to the price increases were housing (+4.0%), food and non-alcoholic beverages (+3.8%), alcohol and tobacco (+7.2%), and transport (+3.4%). These sectors continue to exert upward pressure on inflation, despite the overall slowing trend.

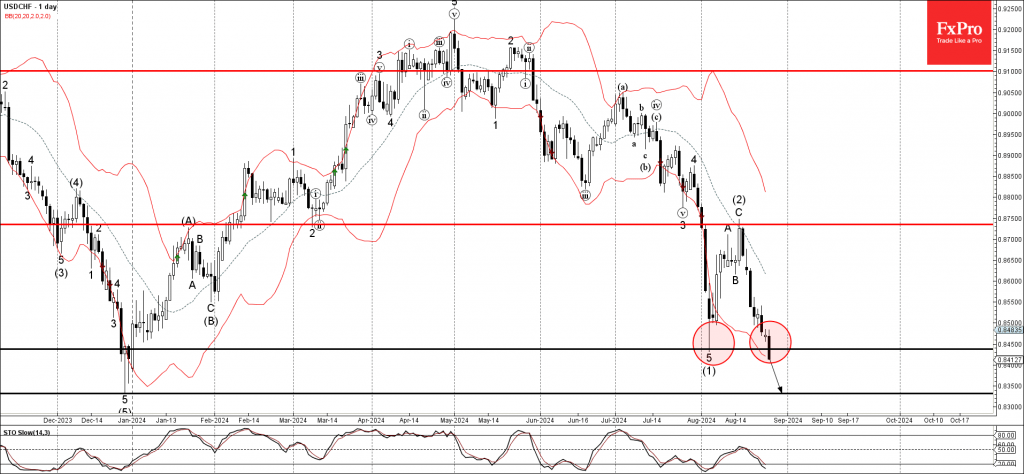

USDCHF Wave Analysis

- USDCHF broke key support level 0.8450

- Likely to fall to support level 0.8330

USDCHF currency pair today broke below the key support level 0.8450 (which stopped the previous sharp downward impulse wave (1) at the start of August).

The breakout of the support level 0.8450 should accelerate the active impulse wave (3) which started earlier from the pivotal resistance level 0.8750 (former support from March).

Given the continued bearish US dollar sentiment, USDCHF currency pair can then be expected to fall to the next support level 0.8330 (former multi-month low from December).

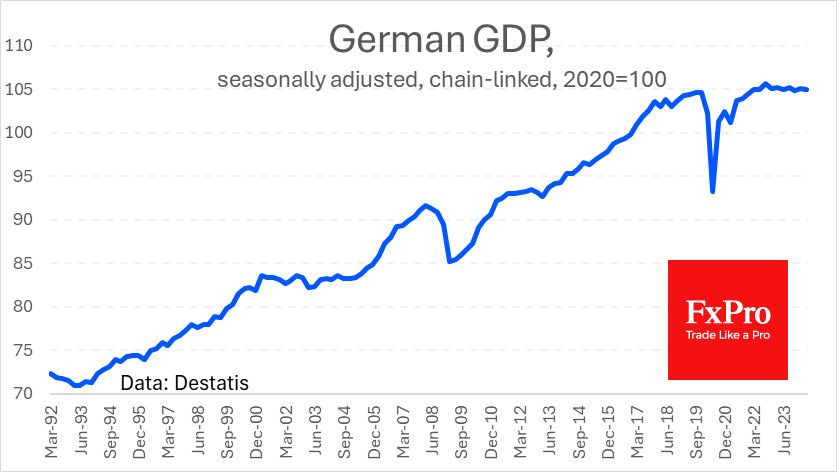

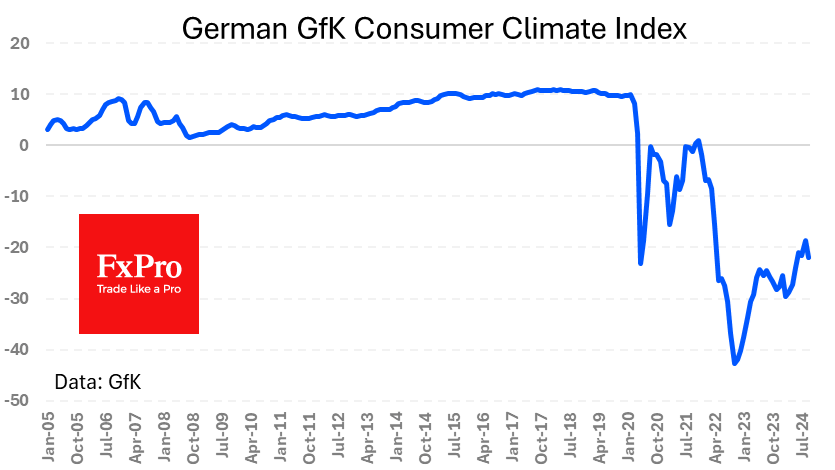

Germany’s Multi-Year Stagnation

The final reading confirmed a 0.1% contraction in the German economy in the second quarter, with a modest growth of 0.3% y/y and stagnation close to the same level of March 2022, just 0.3% above the 2019 peak vs 9.3% in the US over the same period.

The unpleasant surprise came from GfK’s assessment of the consumer climate, which showed a marked decline in September after six months of smooth growth. Deteriorating economic expectations and incomes, as well as a decline in the propensity to buy, dragged the index down. The company attributes the enthusiasm of the previous six months to the European Football Championship in Germany.

Impact on the Euro

Weak macroeconomic data from Germany negatively impact the Euro, not so much due to the size of the country’s economy, but because the Bundesbank is suppressing its traditionally hawkish stance on inflation. Put simply, German weakness could dramatically accelerate ECB rate cuts.

The flow of negative news has had less of an impact on the EURUSD due to the weakness of the US currency but is clearly visible in the pairing against the Pound. The EURGBP has lost around 2.2% in almost three weeks of declines, quickly returning to two-year lows after a rapid rise against the trend.

Australian Dollar Drifting Ahead of Aussie CPI

The Australian dollar is calm on Tuesday. AUD/USD is trading at 0.6773 in the North American session, up 0.03% on the day at the time of writing.

Australian CPI expected to drop to 3.4%

Australia’s CPI, which will be released early Wednesday, is expected to continue to decelerate. CPI eased from 4% to 3.8% in June and the July market estimate stands at 3.4%, which would be five-month low. If the inflation rate drops as expected or lower, it will support the case for the Reserve Bank of Australia to lower interest rates.

The RBA remains hawkish about rate policy and Governor Bullock has said that that the central bank won’t be cutting rates for at least six months. The RBA minutes from the August meeting noted that members had considered raising rates and that underlying inflation had fallen slowly and remained above the 2-3% target.

The markets are marching to a different tune and have priced in around 25 basis points in cuts by the end of the year and around 75 bps in cuts by May 2025. The RBA has said that it discussed raising rates at recent meeting but the markets are betting that cuts rather than hikes will be the next move. The RBA has held the cash rate at 4.5% since November 2023.

The Federal Reserve is poised to cut rates next month with a quarter-point move expected. Fed Chair Powell said on Friday that it was time to cut rates and the US dollar took it on the chin against the majors, with AUD/USD jumping 1.3%, its best daily performance this year. The US releases a key employment report on Sept. 6, two weeks before the rate decision, and a soft release will raise expectations for a half-point cut.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6779. Above, 0.6790 is a weak resistance line

- 0.6760 and 0.6749 are the next support levels

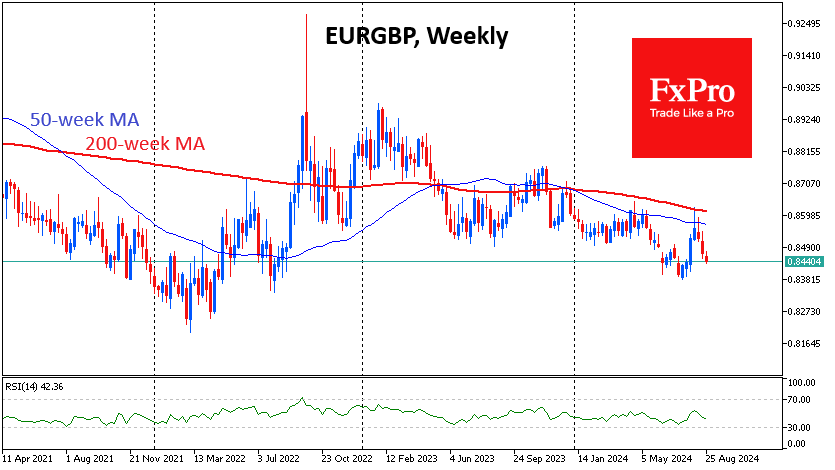

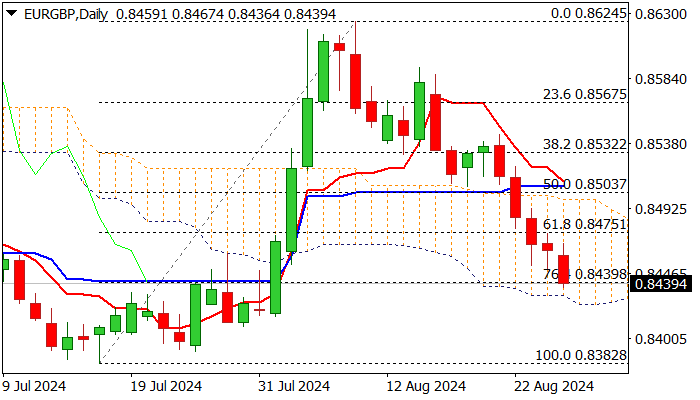

EUR/GBP Outlook: Steep Bear-Leg May Take A Breather Above Daily Cloud Base Support

EURGBP cracked Fibo support at 0.8439 (76.4% of 0.8382/0.8624 rally) and pressuring strong support at 0.8424 (base of thick daily cloud) in extension of five-day steep bear-leg off 0.8544 (Aug 21 lower top).

Technical picture on daily chart remains firmly bearish (strong negative momentum / multiple MA’s bear crosses), but oversold conditions and long tails of candlesticks of past two days signal that bears may face increased headwinds on approach to cloud base.

Upticks are likely to be limited and offer better selling opportunities, with initial barrier at 0.8469 (55DMA), followed by more significant 0.8500 zone (daily cloud top / converging 10/100DMA’s on track to form a bear cross / broken 50% retracement), which should cap stronger corrective upticks.

The pair is on track for the second consecutive monthly close below 200MMA, while long upper shadow on monthly candlestick points to strong offer and adds to bearish outlook.

Res: 0.8450; 0.8475; 0.8493; 0.8511.

Sup: 0.8424; 0.8400; 0.8382; 0.8339.

Sunset Market Commentary

Markets

Friday’s Jackson Hole speech by Fed chair Powell seems to have given the nod for a final holiday week stretching until the September 2nd Labour Day Holiday. US yields rebound 1.9 bps (2-yr) to 4.2 bps (30-yr), strengthening our bottoming out case after they failed to set a new bottom in the wake of Powell’s rather soft comments. The proof of the pudding will be in the eating though, with ISM’s and payrolls lined up after Labour Day. German Bunds underperformed even somewhat with yields up to 6 bps for higher at the 30-yr tenor. Hawkish Dutch ECB member Knot said that he wants to wait until he has the full data and information going into the September meeting to decide what outcome is appropriate. He wants to do the same again in October and December, suggesting the central bank will not be pre-committing to any policy action in advance. It’s likely a lesson learnt from flagging the June rate cut in advance and eventually having to implement it together with an increase of inflation forecasts and coming off the back of sticky Q1 wage data. We nevertheless align with money markets discounting a second 25 bps rate cut by the ECB at the September meeting. Weekend comments from for example chief economist Lane (“the return to target is not yet secure”) strengthen our feeling that an October follow-up move is not a done deal and that they could stick to a quarterly cutting pace barring any mayor downside economic surprises. In FX space, the dollar has more difficulties getting away from sell-off lows as looser global financial conditions are set to kick in. Especially against a rather strong sterling. The UK currency seems to benefiting from the interest rate advantage in coming months. Markets have taken clues from stronger activity data and from BoE Bailey comments in Jackson Hole suggesting that the inflation battle isn’t won. Taking the ECB’s advantage and moving when updated quarterly forecasts are available suggest a September skip and only a next move in November.

News & Views

The Hungarian central bank (MNB) left the policy rate unchanged at 6.75% today. Markets and analysts weren’t all at the same page with some expecting a reduction to 6.5%. The MNB noted the uptick of inflation in July to 4.1% on a headline level and 4.7% in core gauges, adding that the disinflation in market services continues to be slow. It anticipates core inflation to rise close to 5% by the end of the year. The central bank mentioned the early August turmoil as having affected domestic financial markets and risk perception vis-à-vis the country, despite improving fundamentals (including the persistent C/A surplus and the government deficit reduction measures). The MNB believes disciplined monetary policy, anchored inflation expectations and financial market stability are crucial for CPI to sustainably return to target. It did say that there may still be some scope for cautiously lowering interest rates in the coming period but that’s no new information per se. Deputy governor Virag earlier flagged an end of year target rate of 6.25-6.5%. The Hungarian forint marginally appreciated in the wake of the decision from EUR/HUF 394 to around 393 currently. Hungarian swap yields slightly pared earlier losses with changes now ranging between -2.2 bps at the front and +1 bp at the long end.

Bulgaria’s president Rumen Radev signed a decree today to hold another snap parliamentary election on October 27th. It’s the seventh one in just three years and follows the failure of the largest party GERB, PP and the ITN party to form a stable coalition government after the inconclusive June 8 elections. That June vote was the result of the GERB and PP coalition collapsing in March amid persistent infighting. Radev also appointed a caretaker government led by current caretaker prime minster Dimitar Glavchev for the interim period.

Graphs

EUR/HUF: forint marginally stronger as MNB holds policy rates level amid an inflation uptick

EU 30y swap rate: very long end of core yield curves underperforms following test of support levels.

Trade-weighted dollar (DXY): more difficulties getting out of trouble as looser financial conditions are about to set in

S&P 500: the last mile is always the hardest

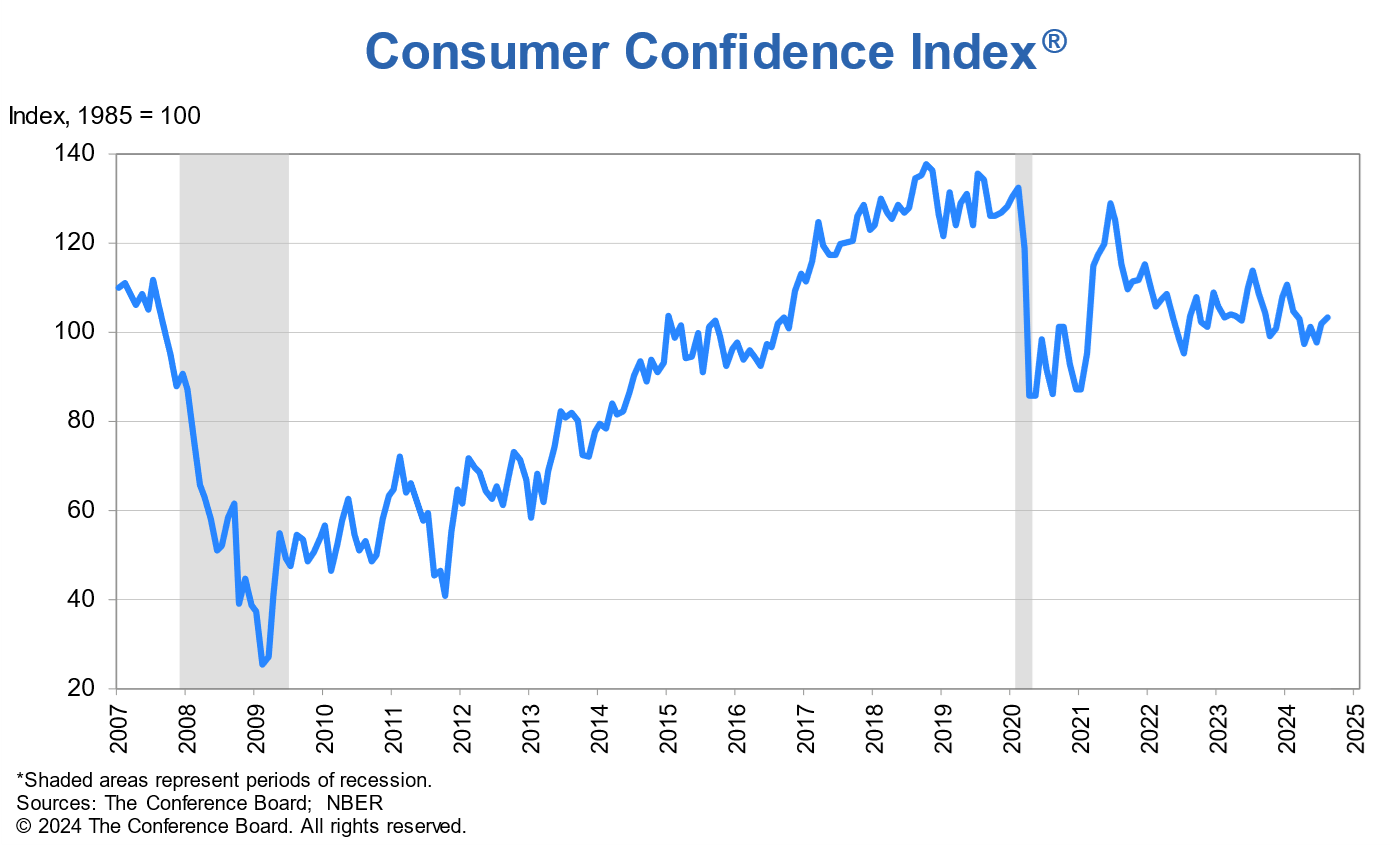

US consumer confidence rises to 103.3, mixed sentiment on business conditions and labor market

US Conference Board Consumer Confidence Index increased from 101.9 to 103.3 in August, surpassing expectations of 100.2. Present Situation Index also edged up from 133.1 to 134.4, while Expectations Index improved from 81.1 to 82.5.

"Overall consumer confidence rose in August but remained within the narrow range that has prevailed over the past two years," noted Dana M. Peterson, Chief Economist at The Conference Board.

Consumers showed "mixed feelings" about the economy. While they were more optimistic about current and future business conditions, concerns about the labor market persisted.

Assessments of the current job situation, though still positive, continued to weaken, with a more pessimistic outlook on future employment prospects. Additionally, consumers were slightly less positive about their future income, likely influenced by the recent rise in unemployment.

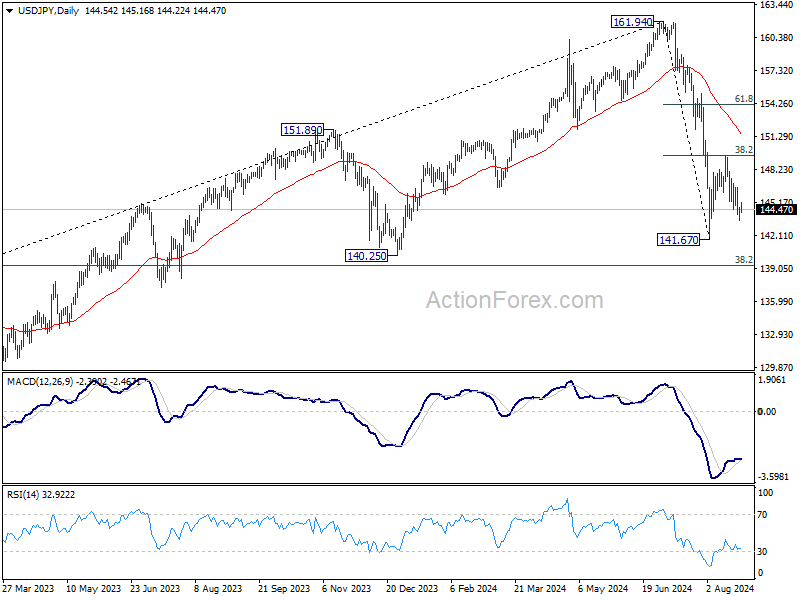

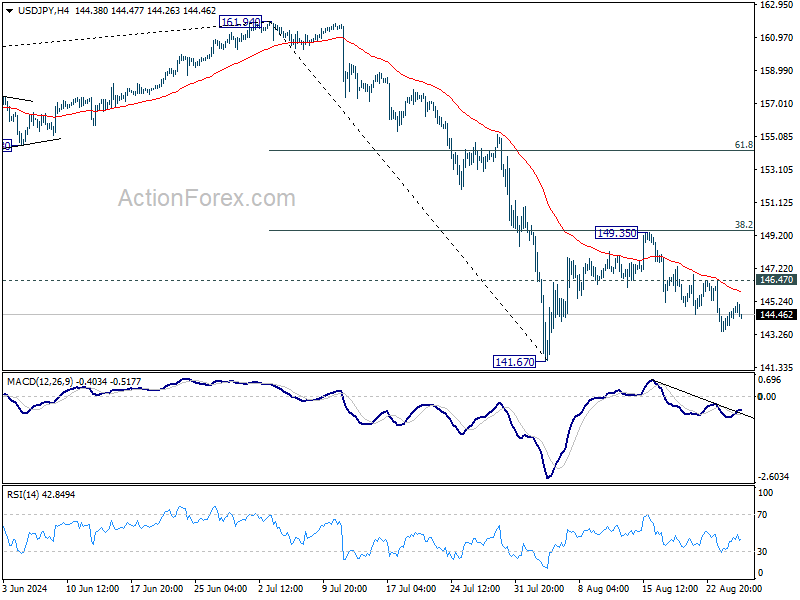

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.77; (P) 144.21; (R1) 144.98; More...

Further decline remains in favor in USD/JPY as long as 146.47 resistance holds, for retesting 141.67 low. Firm break there will resume the whole fall from 161.94 to 140.25 support next. On the upside, above 146.47 minor resistance will turn intraday bias back to the upside for 149.35 resistance instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.38) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.