Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8457; (P) 0.8472; (R1) 0.8487; More…..

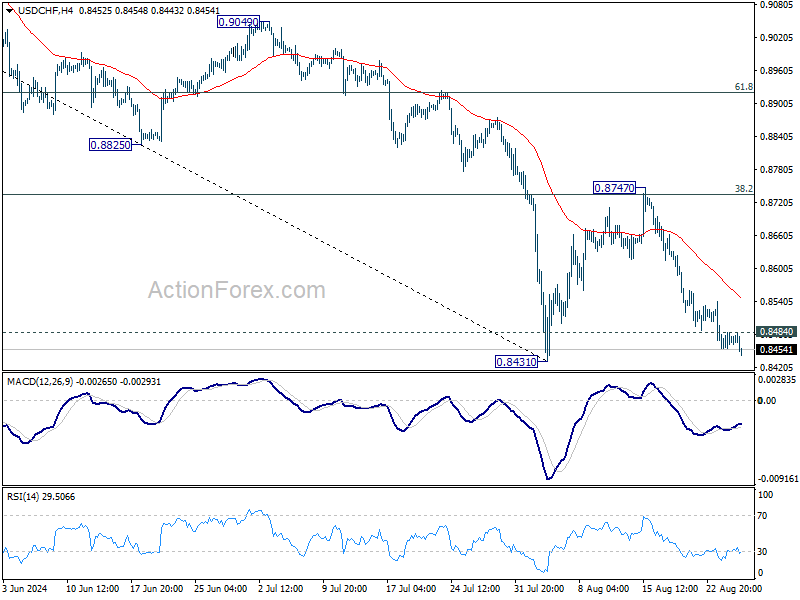

Intraday bias in USD/CHF remain son the downside for the moment. Decisive break of 0.8431 support will resume whole decline from 0.9223 towards 0.8332 low. On the upside, above 0.8484 minor resistance will turn intraday bias neutral. But risk will stay on the downside as long as 0.8747 resistance holds, in case of recovery.

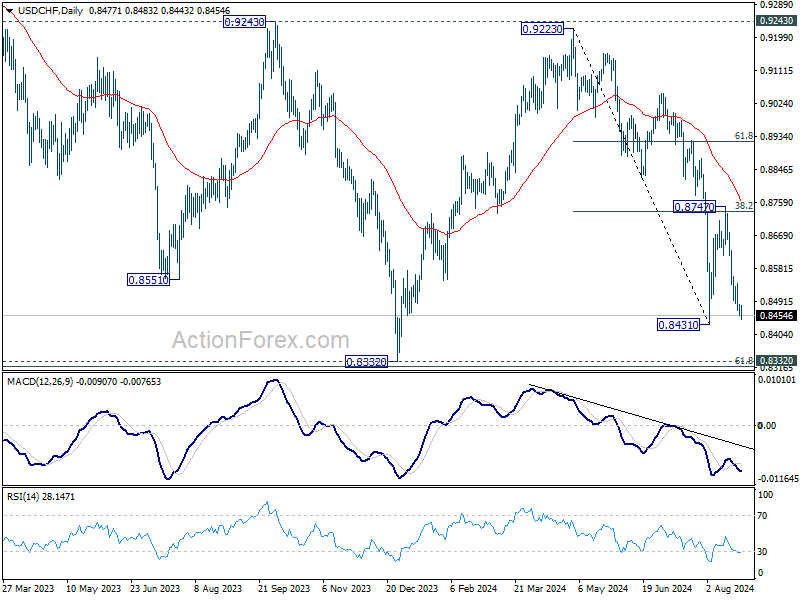

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3170; (P) 1.3197; (R1) 1.3215; More...

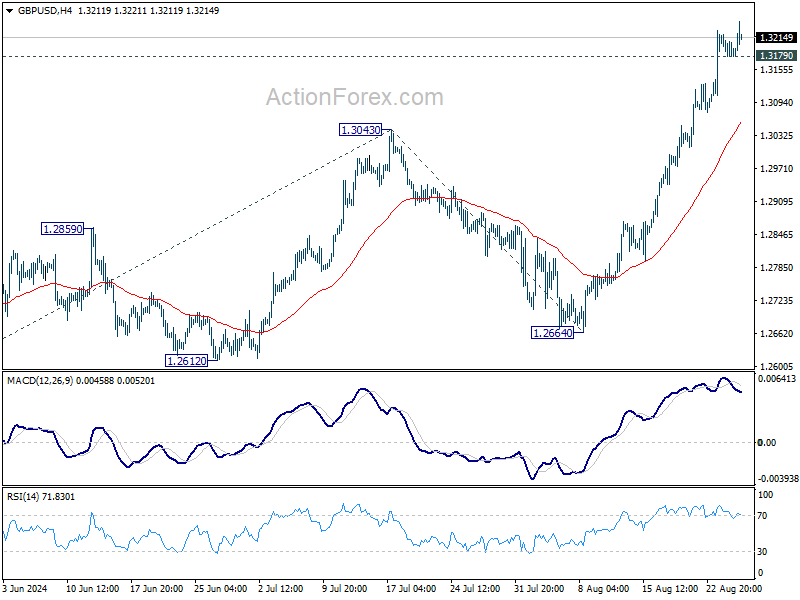

Intraday bias in GBP/USD stays on the upside at hits point. Current up trend should target 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. On the downside, below 1.3179 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

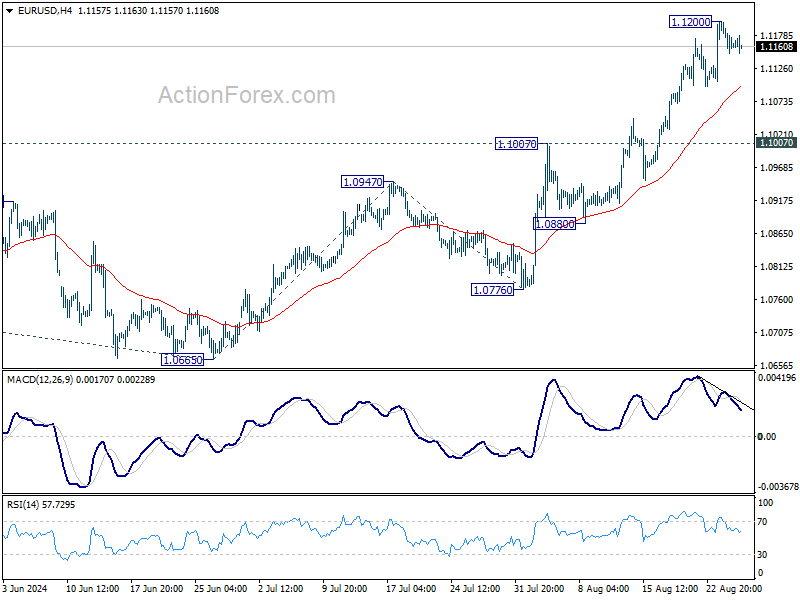

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1140; (P) 1.1171; (R1) 1.1192; More....

EUR/USD is extending consolidation below 1.1200 and intraday bias remains neutral. Downside of retreat should be contained above 1.0007 resistance turned support to bring another rally. Above 1.1200 will resume recent rally to 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

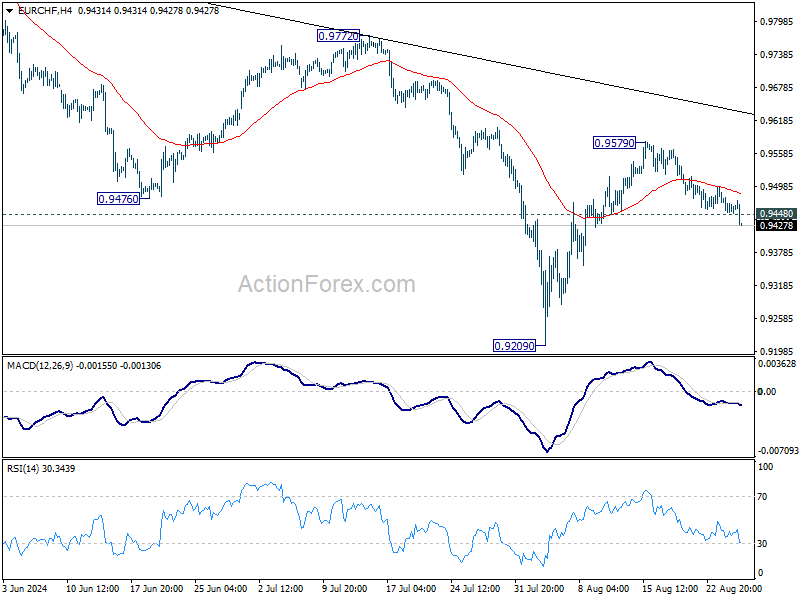

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9467; (R1) 0.9482; More....

EUR/CHF's break of 0.9448 support suggests that rebound from 0.9209 has completed at 0.9579, after rejection by 55 D EMA (now at 0.9569). That also keeps the whole decline from 0.9928 high intact. Intraday bias is back on the downside for retesting 0.9029 low next. For now, risk will stay on the downside as long as 0.9579 resistance holds, in case of recovery.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Euro Slips as German Recession Fears Mount, Aussie Awaits CPI

Euro weakened broadly today, weighed down by growing recession concerns in Germany. The Eurozone's largest economy confirmed -0.1% contraction in GDP in Q2. Consumer sentiment showing deeper-than-expected deterioration, particularly in economic expectations. This decline follows weak Ifo business climate released yesterday. The string of negative data points suggests that any economic recovery may be further delayed.

Meanwhile, Dollar and Yen are also weaker, trailing just behind Euro. However, as US session approaches, there is some buying interest emerging, especially with US consumer confidence data set to be a key driver for the day. Overall market sentiment will also be pivotal, particularly as investors watch to see if DOW can extend its recent rally after hitting a new record high yesterday, or if a correction is on the horizon.

In contrast, New Zealand Dollar leads the day, followed by Swiss Franc and Sterling, while Aussie and Loonie are mixed.

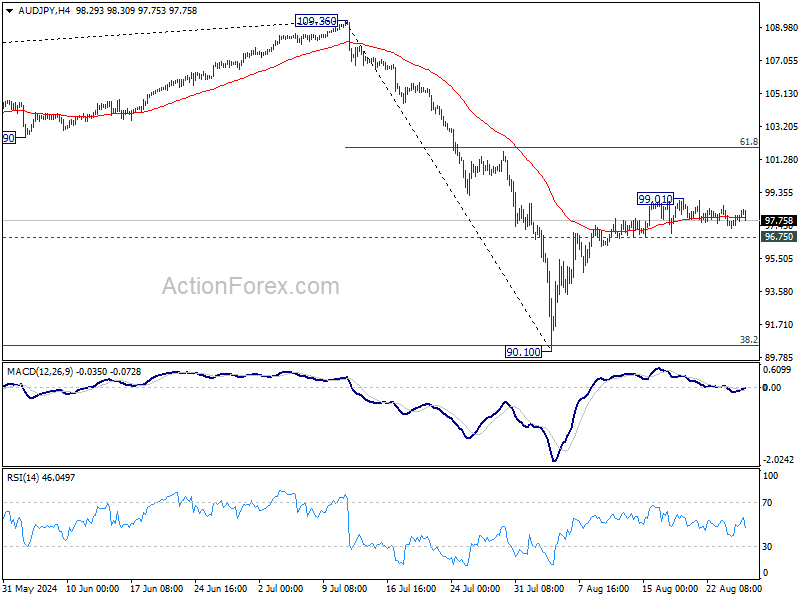

In the upcoming Asian session, Australia's monthly CPI data will be in focus. Expectations are for inflation to slow from 3.8% yoy in June to 3.4% yoy in July. RBA has made it clear that a rate cut is not on the cards for this year. Any upside surprises in the inflation data could push the timeline for policy easing even further into the future.

Technically, AUD/JPY turned side after rising to 99.01. For now, further rise is in favor as long as 96.75 support holds. Above 99.01 will resume the rebound from 90.10 to 61.8% retracement of 109.36 to 90.10 at 102.00. However, break of 99.01 will argue that the rebound has already completed and bring deeper fall back towards 90.10 support.

In Europe, at the time of writing, FTSE is up 0.32%. DAX is up 0.47%. CAC is up 0.02%. UK 10-year yield is up 0.0839 at 4.000. Germany 10-year yield is up 0.049 at 2.296. Earlier in Asia, Nikkei rose 0.47%. Hong Kong HSI rose 0.43%. China Shanghai SSE fell -0.24%. Singapore Strait Times rose 0.07%, Japan 10-year JGB yield fell -0.005 to 0.880.

ECB’s Knot calls for tighter fiscal policy to support inflation fight

In a panel discussion today, ECB Governing Council member Klaas Knot emphasized the need for a more restrictive fiscal policy to support the central bank’s efforts in curbing inflation.

Knot stated that the ECB has “assumed most of the burden of bringing inflation down,” but he added, “A more restrictive fiscal policy would have been desirable.”

He also highlighted the impact of interest-rate hikes on debt-servicing costs, suggesting that these should be offset by higher primary fiscal balances.

Knot pointed out that increased spending by the European Union should be balanced by reduced fiscal space at the national level, noting, “After all, the national and European taxpayer is ultimately one and the same person.”

German GfK consumer sentiment drops to -22, pushing back prospects of recovery

Germany's GfK Consumer Sentiment for September took a sharper downturn than expected, falling from -18.6 to -22.0, below the anticipated -18.3.

August saw significant drops in key indicators: economic expectations plummeted from 9.8 to 2.0, income expectations nosedived from 19.7 to 3.5, and the willingness to buy dipped further from -8.4 to -10.9. Conversely, the willingness to save increased from 8.0 to 10.7, indicating a cautious approach to spending.

According to Rolf Buerkl, consumer expert at NIM, "Apparently, the euphoria of German consumers triggered by the European Football Championship was only a brief flare-up and faded after the end of the tournament."

He added that "negative news about job security is making consumers more pessimistic and a fast recovery in consumer sentiment seems unlikely."

The decline in sentiment is exacerbated by slightly rising unemployment rates, an increase in corporate insolvencies, and staff reduction plans at various companies in Germany. Buerkl concluded, "Hopes for a stable and sustainable economic recovery must therefore be further postponed."

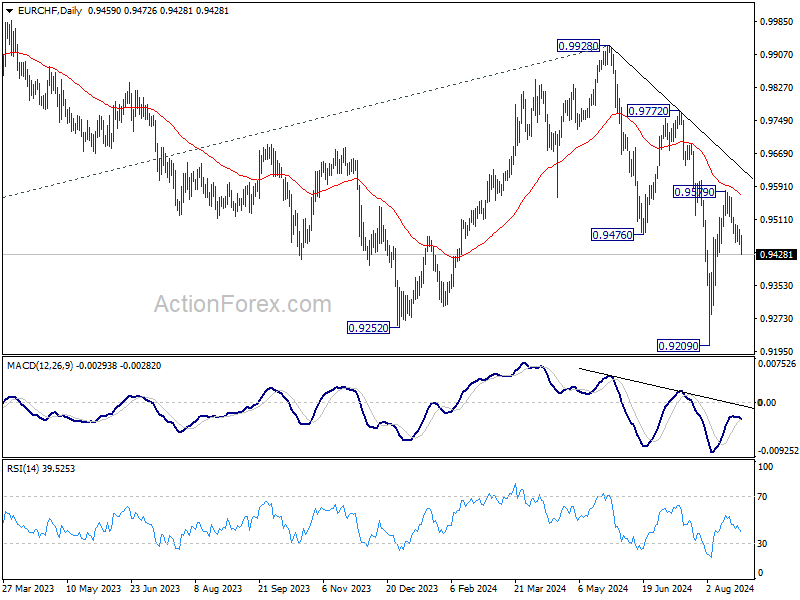

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9442; (P) 0.9467; (R1) 0.9482; More....

EUR/CHF's break of 0.9448 support suggests that rebound from 0.9209 has completed at 0.9579, after rejection by 55 D EMA (now at 0.9569). That also keeps the whole decline from 0.9928 high intact. Intraday bias is back on the downside for retesting 0.9029 low next. For now, risk will stay on the downside as long as 0.9579 resistance holds, in case of recovery.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 2.80% | 2.90% | 3.00% | 3.10% |

| 06:00 | EUR | German GfK Consumer Sentiment Sep | -22 | -18.3 | -18.6 | |

| 06:00 | EUR | Germany GDP Q/Q Q2 F | -0.10% | -0.10% | -0.10% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jun | 6.50% | 7.10% | 6.80% | 6.90% |

| 13:00 | USD | Housing Price Index M/M Jun | -0.10% | 0.20% | 0.00% | |

| 14:00 | USD | Consumer Confidence Aug | 100.2 | 100.3 |

British Pound (GBP) Price Action Ideas: Sterling Set for Correction? GBP/USD, EUR/GBP and GBP/JPY

- The British pound has been one of the best-performing currencies in recent weeks, driven by a good run of UK data and expectations that the Bank of England will not cut interest rates at its upcoming meeting.

- However, there are signs that a correction may be imminent, as the GBP/USD pair is trading in overbought territory and the RSI is flashing a warning sign.

- Other GBP pairs, such as GBP/JPY and EUR/GBP, are also worth watching in the near term.

The Bank of England (BoE) is one of the few Central Banks in the G7 with the exception of the Bank of Japan (BoJ) who are not expected to cut rates at its upcoming meeting. The divergence in rate policy as well as a good run of UK data has made sterling one of the best performers over the last couple of weeks.

Source: LSEG

Sterling has gained admirable ground against its counterparts, most notably against the weaker US Dollar. Sterling is trading at multi-month highs against the greenback while starting the week on the front foot against the Euro as well.

The Euro Area economy has not been as strong this year as the UK which has surprised many by the strength of the rebound. This morning the release of German data did not paint a pretty picture as Europe’s most industrialized economy continues to drag on the zone as a whole. Coupled with a more dovish European Central Bank (ECB) outlook and the run up to the September Central Bank meetings could see the Euro lose more ground to Sterling.

This morning we also heard from UK Prime Minister Keir Starmer who briefly touched on the October budget. The Prime Minister stressed that it will be a painful one but necessary for long term stability and improvement. Starmer said “Those with the broadest shoulders should pay the heaviest burden” which hints at a tax on the wealthy in the UK

In the short term, GBP pairs remain interesting with cable looking the most likely for a correction. GBP/JPY still has room to run to the upside but a stronger Yen has been capping gains of late. EUR/GBP remains under selling pressure in the medium term as well, but given that we are seeing a five-day winning streak for cable, I would not rule out a short-term pullback this week.

Technical Analysis

GBP/USD

From a technical perspective, GBP/USD has been on a tear since the August 8 low of 1.2665. The pair has since rallied around 600-odd pips to the upside to trade above the 1.3200 handle.

Yesterday’s bearish inside bar candle close did hint at a potential retracement but price has since taken out yesterday’s highs. Could this be a fakeout and the price still falls later in the day? Time will tell.

Another hint that a retracement may be imminent comes from the RSI period 14 which is currently in overbought territory. Now as always, this does not mean that the price will definitely fall as at times the RSI can remain above the 70 handle for extended periods as price continues to make higher highs.

However, the RSI can be useful when used correctly and provides another confluence supporting a short-term correction.

GBP/USD Daily Chart, August 27, 2024

Source: TradingView (click to enlarge)

Support

- 1.3180

- 1.3050

- 1.3000 (psychological level)

Resistance

- 1.3354

- 1.3500 (psychological level)

- 1.3750

GBP/JPY

GBP/JPY continues to work its way higher following the Yen unwind which impacted all Japanese Yen pairs. GBP/JPY dropped to a low of 180.112 on August 5 before beginning its recovery.

Since the pair has rallied all the way back above the 190.00 even if it has been a slow rise higher. The break of the descending trendline does bode well for GBP/JPY as the pair eyes a much anticipated retest of the 200.00 handle.

As things stand on the daily timeframe, a candlestick close above 191.400 would see a morning star candlestick pattern form which hints at further upside.

There are some serious hurdles ahead that the pair will need to overcome as price is currently testing the 200-day MA which rests at 192.00. A break above here will face resistance around the 195.00 handle before the 100-day MA at 197.00 comes into focus.

GBP/JPY Daily Chart, August 27, 2024

Source: TradingView (click to enlarge)

Support

- 189.56

- 188.40

- 185.00

Resistance

- 192.00

- 195.00

- 197.00

EUR/GBP

The technicals on EURGBP point to the pair setting up for a retracement sometime soon. The pair is currently on a five-day decline as Sterling appreciated while the Euro faced pressure.

EUR/GBP is edging lower towards the lows of late July before the 250 pip rally higher.The RSI is currently languishing between the neutral area and the oversold area. Any move lower from here could push the RSI into oversold territory.

0.8400 is also a key area of multi-month support which could be a factor and might be a hurdle too far at this stage.

A move higher from here will leave price having to navigate past the 50-day MA first at 0.8472 before the 100-day MA at 0.8500 comes into focus.

EUR/GBP Daily Chart, August 27, 2024

Source: TradingView (click to enlarge)

Support

- 0.8400

- 0.8342

- 0.8247

Resistance

- 0.8472

- 0.8500

- 0.8584

Yen Shrugs as Inflation BoJ Core CPI Dips

The Japanese yen has edged lower on Tuesday. In the European session, USD/JPY is trading at 144.76, up 0.17% on the day at the time of writing.

BoJ Core CPI slips to 1.8%

Is Japanese inflation falling? On Tuesday, two inflation indicators pointed to a deceleration in inflation in July. BoJ Core CPI, which is closely monitored by the Bank of Japan, dropped to 1.8%, down from 2.1% in June and its lowest level in three months. The Services Producer Price Index dropped to 2.8%, down from a revised 3.1% in June.

Japan’s inflation has been moving higher, which has supported the case for another rate hike from the Bank of Japan. The central bank has projected that inflation will hover around its 2% target until 2027. Today’s inflation releases could be temporary blips but if the next inflation reports also indicate that inflation is heading lower, it could complicate the BoJ’s plans to gradually normalize its ultra-loose policy.

The International Monetary Fund said on Friday that it supports the BoJ’s move to normalization and that the speed of further rate hikes will be ‘very data-dependent”, with a focus on inflation, wage growth and inflation expectations. We’ll get a look at Tokyo Core CPI on Friday, which is expected to remain unchanged at 2.2%.

The Jackson Hole Symposium was “mission accomplished” for the markets as Federal Chair Jerome Powell signaled that the Fed was ready to cut rates. Powell didn’t specify the September meeting as the kickoff for rate cuts, but the markets are confident that the Fed will cut by a quarter-point at the Sept. 18 meeting.

The US releases a key employment report on Sept. 6 and Goldman Sachs has said that if the jobs report is soft again then the Fed could respond with a 50-basis point cut, while a strong jobs release would support a 25-bps move.

USD/JPY Technical

- USD/JY is testing resistance at 144.98. Above, there is resistance at 145.42

- There is support at 144.21 and 143.77

ECB’s Knot calls for tighter fiscal policy to support inflation fight

In a panel discussion today, ECB Governing Council member Klaas Knot emphasized the need for a more restrictive fiscal policy to support the central bank's efforts in curbing inflation.

Knot stated that the ECB has "assumed most of the burden of bringing inflation down," but he added, "A more restrictive fiscal policy would have been desirable."

He also highlighted the impact of interest-rate hikes on debt-servicing costs, suggesting that these should be offset by higher primary fiscal balances.

Knot pointed out that increased spending by the European Union should be balanced by reduced fiscal space at the national level, noting, "After all, the national and European taxpayer is ultimately one and the same person."

GBP/USD Technical: Sterling Bulls in Control

- BoE Governor Bailey’s speech at the Jackson Hole Symposium reiterated BoE’s cautionary dovish monetary policy stance.

- Short-term interest rate markets are likely to price in a shallower and slower interest rate cut cycle in the UK.

- The potential further widening of the 2-year yield premium of UK gilts over US Treasury notes may support a further upmove in the GBP/USD.

- Watch the 1.3000 key medium-term support on the GBP/USD to maintain its ongoing medium-term uptrend phase.

The British pound sterling (GBP) has been the top performer among the major currencies, strengthening by 3.9% year-to-date as of 27 August against the US dollar.

The current strength of the GBP has been supported by a cautious dovish monetary policy stance adopted by the Bank of England (BoE) after its first 25 basis points (bps) cut on its policy Bank Rate in its recent August meeting to bring it down to 5% from a 16-year high of 5.25%, that had been left unchanged for a year.

BoE may adopt a shallower and slower interest rate cut cycle

BoE’s cautionary stance was reiterated last Friday, 23 August Jackson Hole Symposium where BoE Governor Bailey stated that further interest rate cuts in the UK should not be rushed because it was still too soon to be sure inflation was beaten even though longer-term inflationary pressures were easing,

Hence, going forward, it is likely to draw a wedge between US and UK interest rates where short-term interest rate markets are likely to price a shallower and slower interest rate cut cycle in the UK.

Bullish breakout after one year of range consolidation

Fig 1: GBP/USD medium-term trend as of 27 Aug 2024 (Source: TradingView, click to enlarge chart)

The price actions of the GBP/USD staged a bullish breakout last Tuesday, 20 August after it consolidated for almost one year of “Symmetrical Triangle” range configuration since 13 July 2023.

In addition, it has also cleared above its former long-term secular descending trendline resistance that capped prior rallies since July 2014.

Even though the daily RSI momentum indicator is now hovering at an overbought condition level of 74, there is no bearish divergence signal being flashed out at this juncture which suggests lower odds of a bearish reversal scenario for the GBP/USD.

Intermarket analysis also supports the potential start of a medium-term uptrend phase for the GBP/USD. The 2-year sovereign yield spread between UK gilts and US Treasury notes has staged a bullish breakout above its former major descending trendline resistance from 12 July 2023.

This observation suggests that the 2-year yield premium of UK gilts over US Treasury notes may widen further from 0.18% printed at this time of the writing which in turn may make UK fixed-income instruments more attractive over US.

Watch the 1.3000 key medium-term pivotal support on the GBP/USD with the next medium-term resistances coming in at 1.3400/3505 and 1.3750 next (see Fig 1).

On the other hand, a breakdown below 1.3000 invalidates the bullish tone to see another round of choppy corrective movements to expose the next medium-term supports at 1.2860 and 1.2635 (also close to the 200-day moving average).

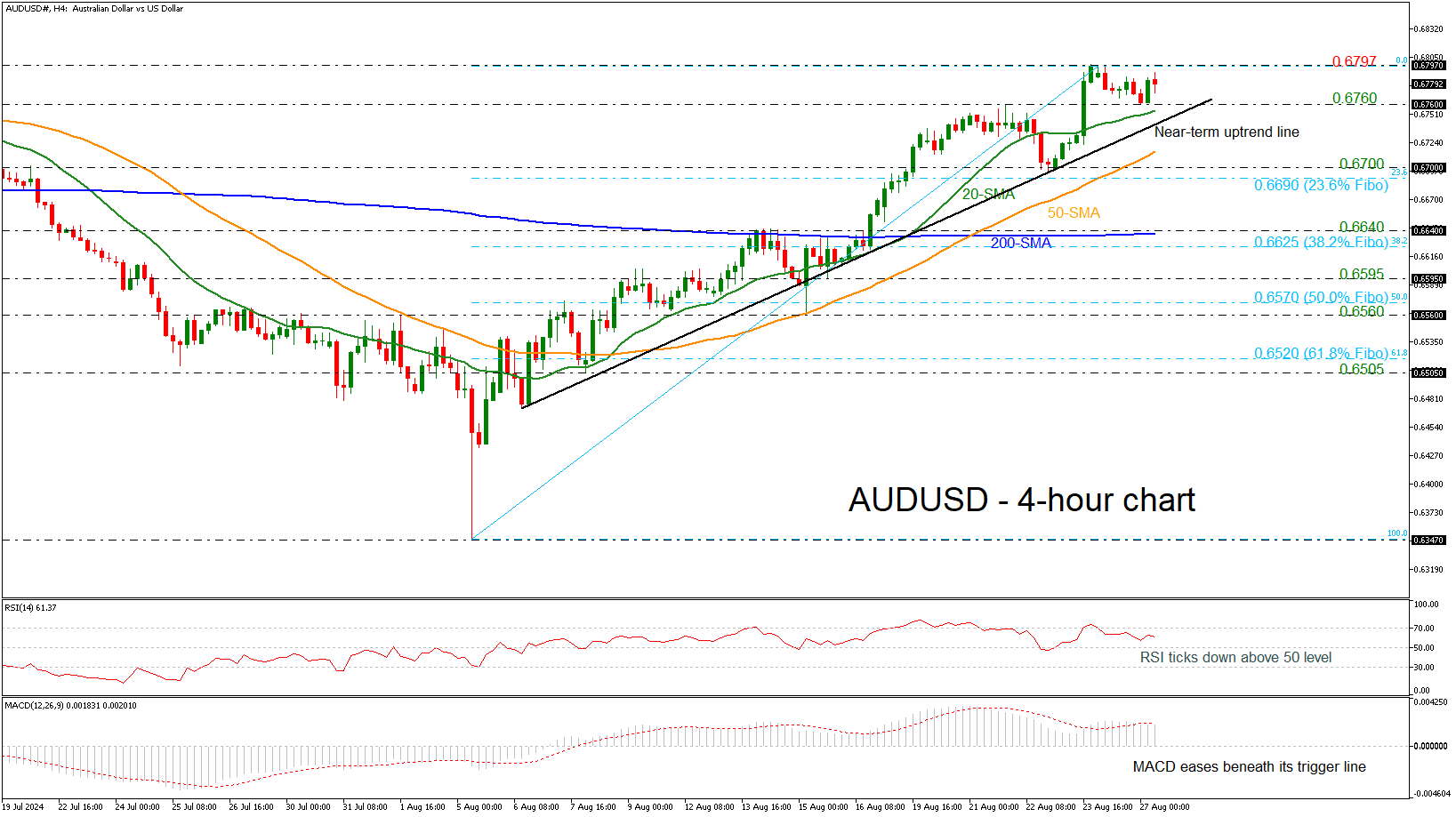

Will AUDUSD Continue Its Bullish Wave Trend?

- AUDUSD holds in tight range near its recent high

- RSI and MACD point down

AUDUSD has been stuck within a range bound pattern in the near term defined by the 0.6794 and 0.6760 levels, although the price has been maintaining a bullish tendency since the beginning of August.

However, the technical oscillators suggest a potential downside retracement. The RSI is ticking lower above the neutral 50 level, while the MACD is sliding beneath its trigger line in the positive area.

If the price continues its recent rebound from 0.6760, the next resistance could come from the previous high of 0.6797 before resting near December's peak of 0.6870.

Alternatively, should the price reverse back lower, the 20-period simple moving average (SMA) at 0.6750 and the ascending trend line near 0.6740 could act as the first levels of defense. Further declines could then push the market towards the 50-period SMA at 0.6715, ahead of the 0.6700–0.6690 region, which encapsulates the 23.6% Fibonacci retracement level of the upward move from 0.6347 to 0.6797.

In brief, AUDUSD looks positive as long as it stands above the uptrend line and the 200-period SMA in the 4-hour chart.