Sample Category Title

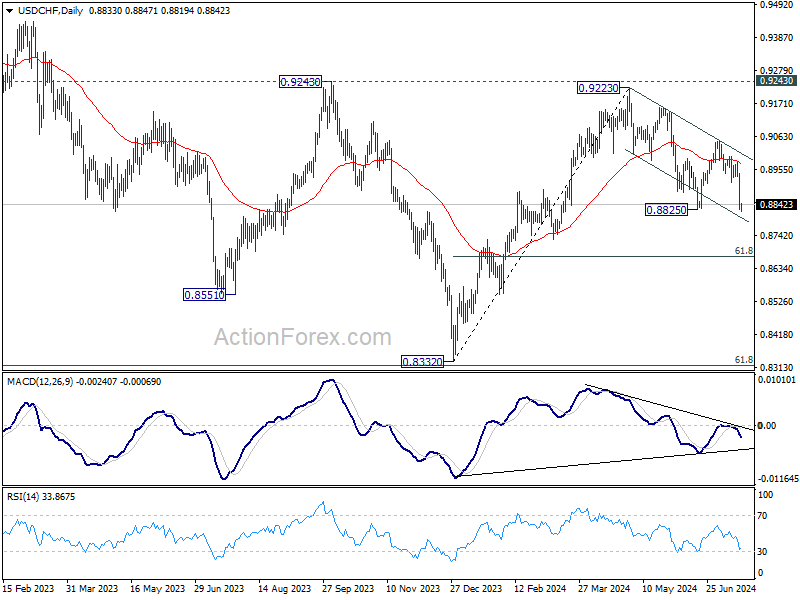

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8790; (P) 0.8871; (R1) 0.8915; More…

Intraday bias in USD/CHF stays on the downside as this point. Breach of 0.8825 support indicates that whole fall from 0.9223 is resuming. Deeper decline would be seen to 60% retracement of 0.8332 to 0.9223 at 0.8672 next. On the upside, above 0.8914 support turned resistance will turn intraday bias neutral first.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

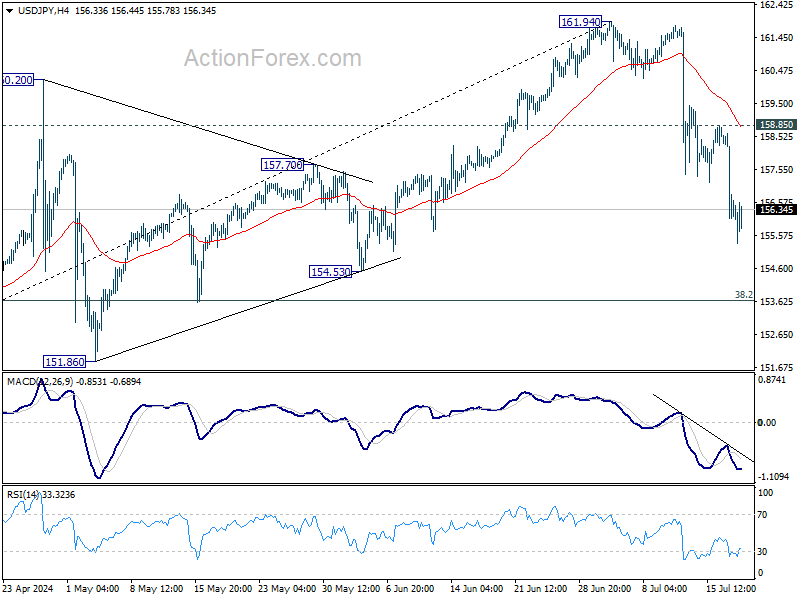

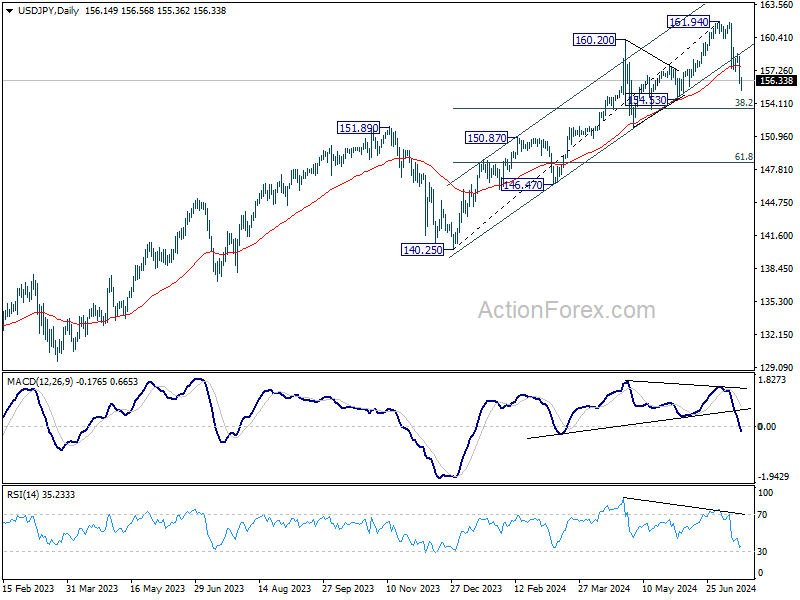

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.29; (P) 156.95; (R1) 157.84; More...

Intraday bias in USD/JPY stays on the downside for the moment. Current decline is seen as correcting whole rally from 140.25. Deeper fall should be seen to 38.2% retracement of 140.25 to 161.94 at 163.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

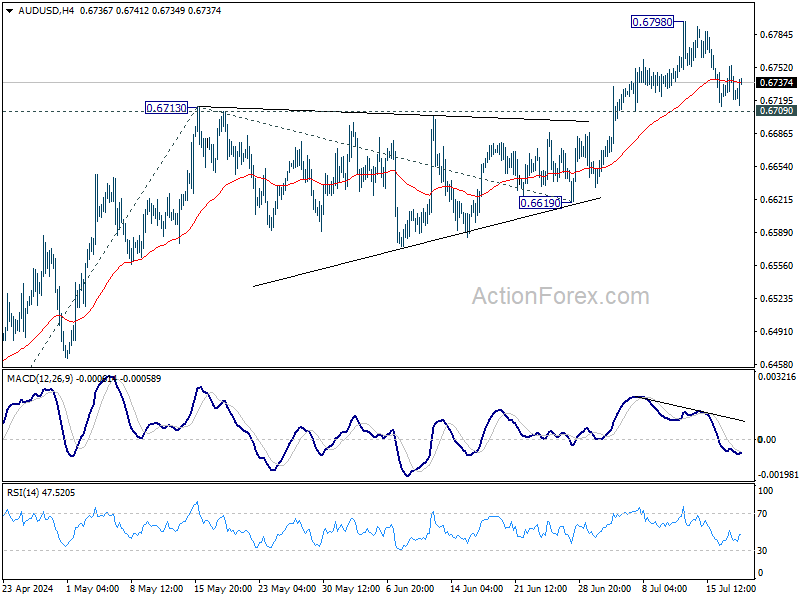

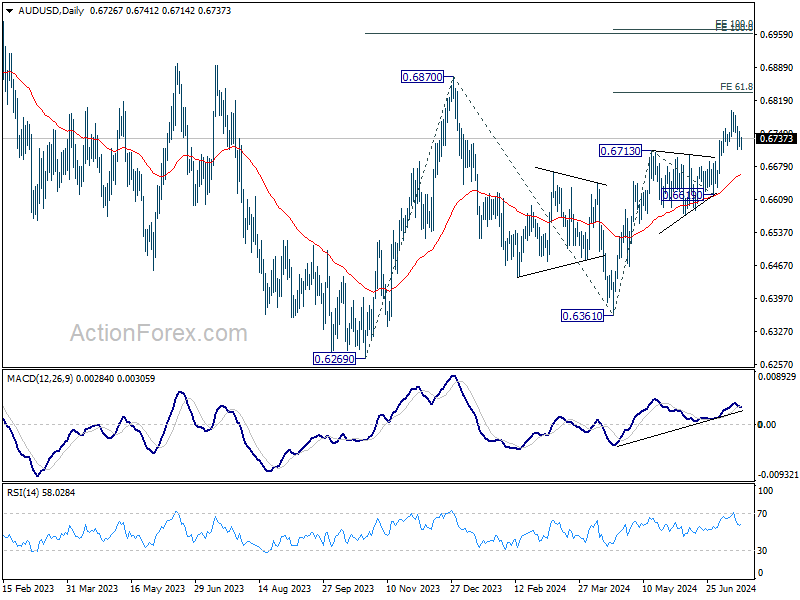

AUD/USD Daily Report

Daily Pivots: (S1) 0.6715; (P) 0.6735; (R1) 0.6749; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is expected as long as 0.6709 minor support holds. On the upside, above 0.6798 will resume the rally from 0.6361 and target 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. On the downside, however, firm break of 0.6709 support will turn intraday bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

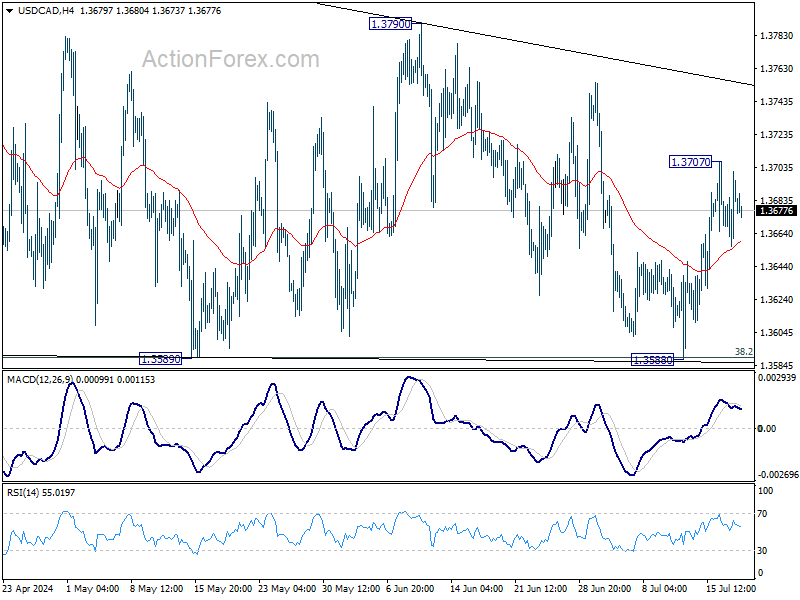

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3659; (P) 1.3681; (R1) 1.3704; More...

Intraday bias in USD/CAD remains neutral for the moment. Outlook is unchanged that corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Above 1.3707 will target 1.3790 resistance first. Break of 1.3790 will argue that larger rise from 1.3716 is ready to resume through 1.3845.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

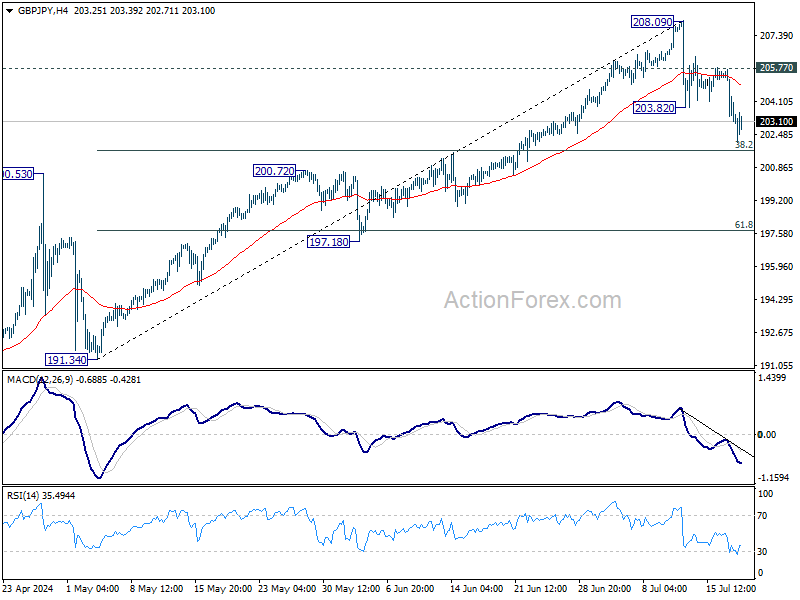

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.23; (P) 203.96; (R1) 204.91; More...

Intraday bias in GBP/JPY is back on the downside as fall from 208.09 resumed. Deeper decline would be seen to 38.2% retracement of 191.34 to 208.09 at 201.69. Strong support is expected there to bring rebound. On the upside, above 205.77 minor resistance will turn intraday bias will turn bias back to the upside for retesting 208.09. However, sustained break of 201.69 will argue that larger correction is already underway.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 200.72 resistance turned support holds, even in case of deep pullback.

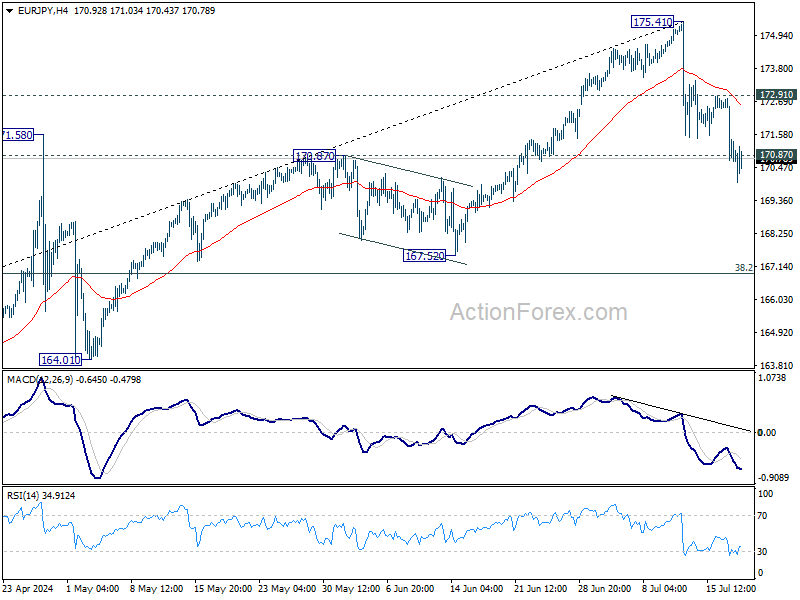

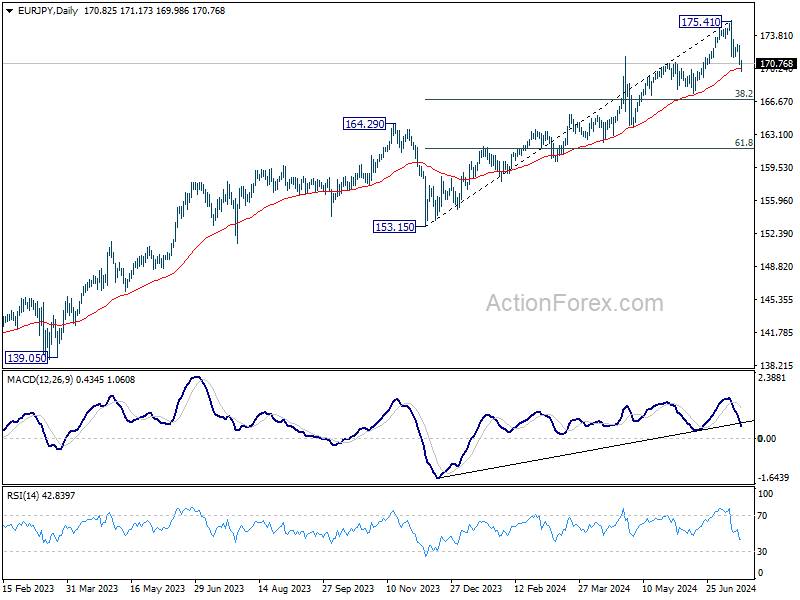

EUR/JPY Daily Outlook

Daily Pivots: (S1) 170.11; (P) 171.47; (R1) 172.23; More...

EUR/JPY's break of 170.87 resistance turned support argues that fall from 175.41 might be correcting whole rise from 153.15 already. Intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 170.30) will target 38.2% retracement of 153.15 to 175.41 at 166.90. On the upside, though, break of 172.91 resistance will revive near term bullishness and bring retest of 175.41 high.

In the bigger picture, medium term outlook will stay bullish as long as 164.29 resistance turned support holds. Long term up trend is still in favor to continue through 175.41 at a later stage. However, firm break of 164.29 will be a strong sign of bearish trend reversal.

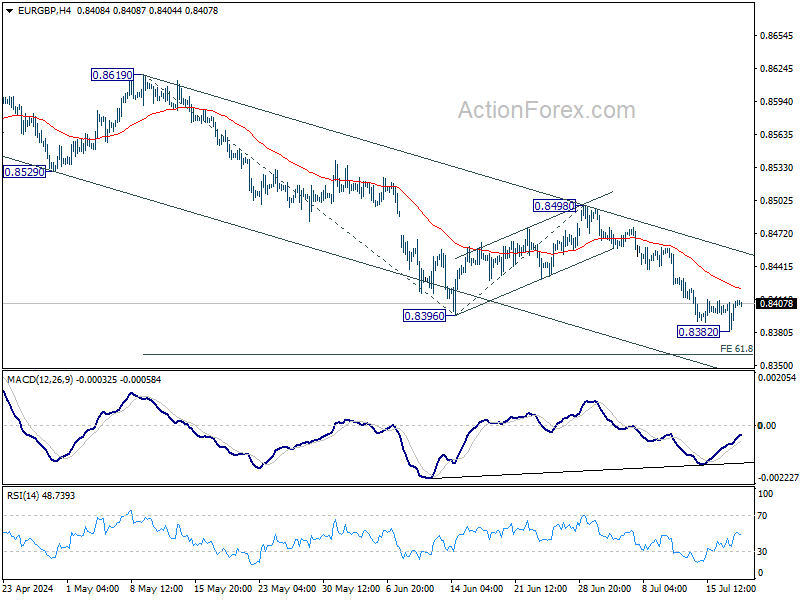

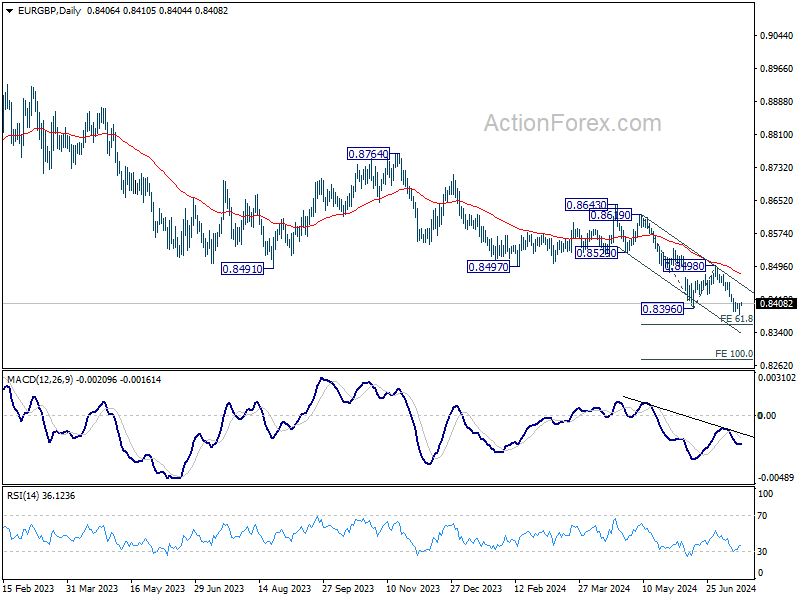

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8391; (P) 0.8401; (R1) 0.8419; More....

EUR/GBP recovered quickly after dipping to 0.8392 and intraday bias remains neutral. Further decline is in favor. But considering bullish convergence condition in 4H MACD, downside could be contained by 61.8% projection of 0.8619 to 0.8396 from 0.8498 at 0.8360 on first attempt. On the upside, break of 55 4H EMA (now at 0.8421) will turn bias back to the upside for stronger rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

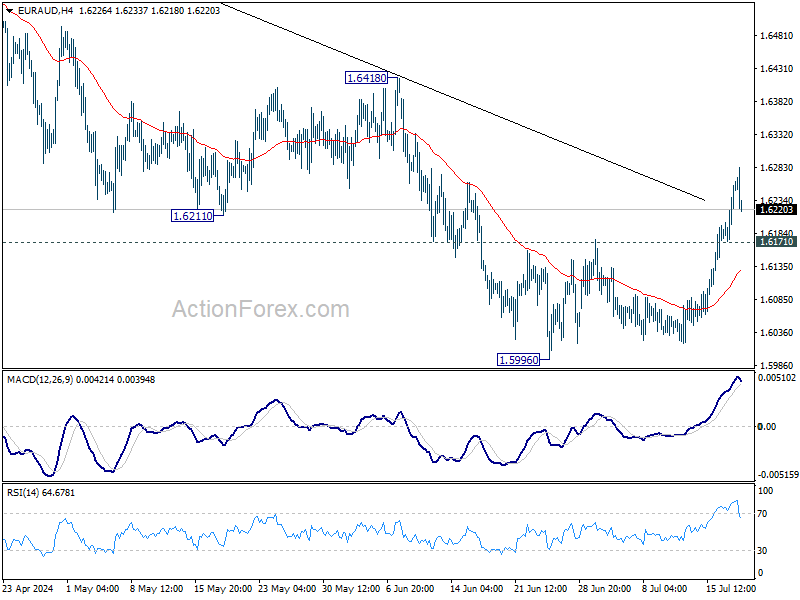

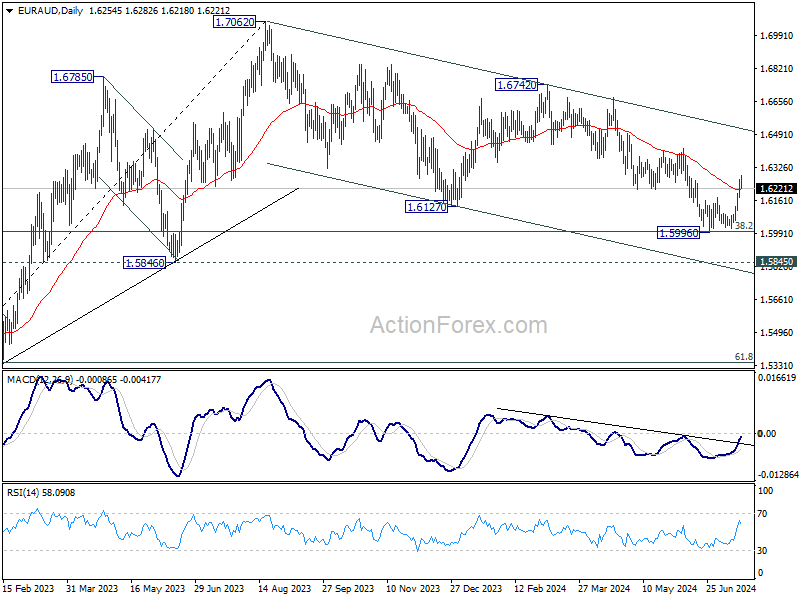

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6199; (P) 1.6232; (R1) 1.6289; More...

EUR/AUD's break of 1.6211 support turned resistance indicates short term bottoming at 1.5996. More importantly, correction from 1.7062 might have completed with three waves down to 1.5996, after hitting 1.6000 fibonacci support. Intraday bias is back on the upside for 1.6418 resistance. Firm break there will strengthen this bullish case. On the downside, though, below 1.6171 minor support will turn intraday bias neutral first.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6418 resistance will argue that the correction has completed.

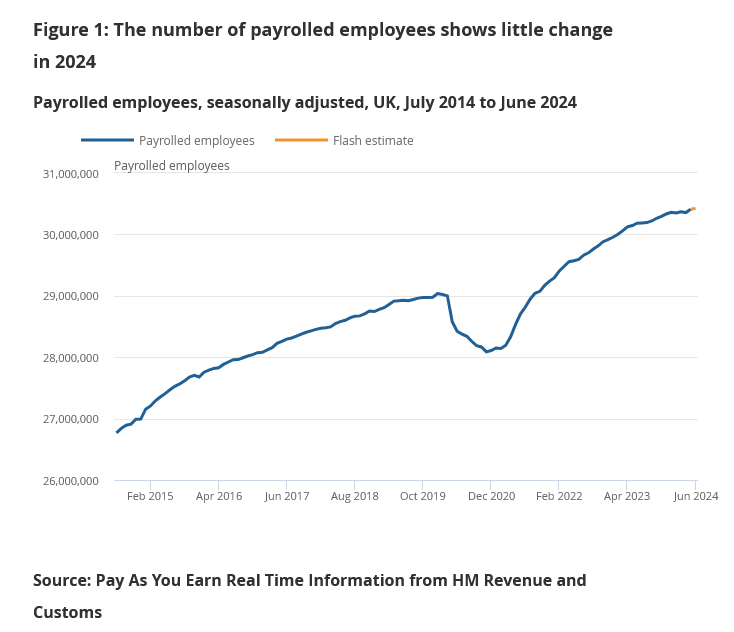

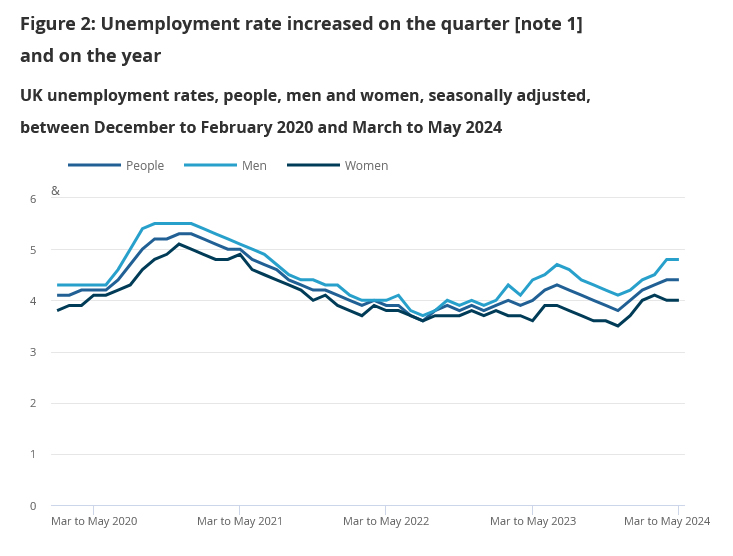

UK payrolled employment rises 16k in Jun, unemployment rate steady at 4.4% in May

In June, UK payrolled employment rose 16k or 0.1% mom. Median monthly pay increased 3.6%, sharply lower than prior month's 6.0% yoy. This sharper than usual slow down in pay growth is partly because of the comparison with June 2023, which figure was inflated by pay settlements made in the health sector. Claimant count rose 32.3k versus expectation of 23.4k.

In the three months to May, unemployment rate was unchanged at 4.4%, matched expectations. Growth of average earnings including bonus slowed from 5.9% yoy to 5.7% yoy. Growth of average earnings excluding bonus slowed from 6.0% yoy to 5.7% yoy. Both earnings growth matched expectations.

USD Selloff Accelerates, ECB Meets

While everyone is speculating on how the ongoing international trade war could worsen if Donald Trump returns to the White House, it was Joe Biden who delivered a blow to the market yesterday as his administration told allies that it’s considering severe restrictions if companies like the Japanese Tokyo Electron and Dutch ASML keep providing China the tools they need to access advanced chip technology. And indeed, despite restrictions, the surging sales to China accounted for almost half of ASML’s revenue in Q2 according to Bloomberg. As such, despite a breathtaking rise in orders from around $3.9bn to $6.1bn that the company announced yesterday, ASML shares tanked nearly 13%, pulling the Stoxx 50 down with it. Tokyo Electron dived 7% on Wednesday and another 9% today. Nvidia fell more than 6.5%, Broadcom dropped almost 8% as AMD crashed more than 10%. Even Tesla fell more than 3% despite Cathie Wood’s prediction that the robotaxi platform that Elon Musk is working on could boost the company’s stock price by 10-fold! Always humble and reasonable, this Cathie Wood. As such, the S&P500 fell from a record as the technology-heavy Nasdaq 100 fell almost 3% - printing its worse day since 2022.

Let’s see if earnings from Netflix and TSM could put a smile back on investors’ face and help TSM – which lost 8% yesterday – recover a part of these losses. But yesterday came as a proof that we don’t necessarily need Donald Trump in the White House to fuel the trade tensions with China and wreak havoc across allies. Biden is good at doing that job, too.

Yesterday’s big tech selloff hit sentiment in small caps too. The Russell 2000 gave back 1% as the US 2-year yield rebounded slightly on cautious comments from the Federal Reserve (Fed) Christopher Waller’s comments that the Fed is getting ‘closer’ to cutting rates but he needs more evidence that inflation is on a solid downside trajectory to back a concrete move.

The selloff in the US dollar index accelerated as the index pulled out a crucial Fibonacci support – the major 38.2% retracement on year-to-date rally. The sharp rise in the Japanese yen amid a suspected FX intervention, and the rally in sterling following a stronger-than-expected British inflation data helped fueling the bearish action in the greenback yesterday. As such, the US dollar index has now stepped into the medium-term bearish consolidation zone with potential for a further weakness. And the fundamentals including a full conviction that the Fed will start cutting the interest rates in September support the negative dollar outlook.

Cable cleared the 1.30 offers after a set of stronger-than-expected CPI figures hammered the expectations that the Bank of England (BoE) would cut rates in August meeting. Yes, the headline CPI is now at 2% in the UK but the services inflation remains sticky near 5.7% and given that services make up to 80% of the British economy, worries regarding the sticky services inflation are funded. What’s encouraging however is that the latest rise in British services inflation was due to a 10% rise in hotel and restaurant prices amid the effects of an almost 10% rise in the minimum wage and Taylor Swift tour. The Euro 2024 – where Brits played the final – will probably have a temporary boosting effect on services and beer inflation as well. But then, if all goes well, we shall start seeing the services inflation figures wane and help the BoE move toward rate cutting near fall. For now, the rapid rise of BoE hawks backs the appreciation of the British pound and could support a further advance in Cable. But given that the Fed rate cut bets went probably a bit far, and that the BoE rate cut bets dropped enough, the upside potential in Cable should be limited. Solid resistance is eyed near 1.3150/1.32 area.

Across the Channel, the EURUSD consolidates gains near 1.0930-1.0940 this morning. The European Central Bank (ECB) will probably announce no change to interest rates at today’s meeting. Any hint that the ECB could cut rates in September should slow down the euro purchases today, but investors are more convinced than not that the ECB will announce a second cut in September. Therefore, if today’s presser doesn’t bring new and unexpected elements on the table, the EURUSD outlook should remain slightly positive faced with the rising Fed cut expectations.

Elsewhere, US crude rallied yesterday on the back of an almost 5-mio-barrel fall in US oil inventories last week. Trump’s ambitions to boost the US oil production could be a turn off for oil bulls. But the Trump trade on oil is not that clear. Yes, Trump wants to pump more, but he also wants to scrap the shift toward alternative energy sources and keep demand for fossil fuel intact. Therefore, a Trump win could be more positive for oil than the contrary. In the short-run, the reflation-positive environment could reasonably keep the price of US crude on a positive track above the $80pb key support level and help the barrel of oil make another attempt on the $85pb level. Appetite above this level will likely remain limited, however, as higher oil prices boost inflation expectations and Fed hawks, and have a natural cooling effect on bullish bets.