Sample Category Title

Sterling Steady, Kiwi Rebounds, Gold Hits Record

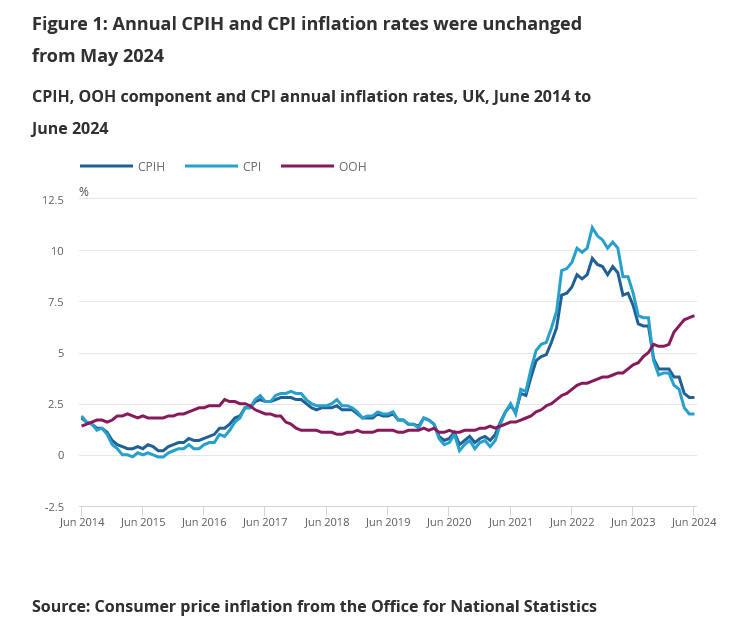

Forex markets have been relatively subdued today. Sterling remains steady after June's UK CPI data revealed that both headline and core inflation were unchanged from the previous month. Significantly, services inflation also failed to cool, which could keep BoE cautious about making a premature rate cut on August 1. Some key members of the MPC may prefer to see further progress in disinflation before taking any action.

Earlier in Asian session, New Zealand Dollar showed a surprising rebound despite lower-than-expected Q2 CPI figures. Many economists have now revised their forecasts, anticipating the first RBNZ rate cut in November. Kiwi's bounce can be seen as a "cover-on-news" move, as the Q2 inflation data was not disastrous enough to cause major concern.

For the week so far, Swiss franc is leading as the best performer, followed by Dollar and Euro. New Zealand Dollar remains the weakest, with Australian Dollar and Canadian Dollar also underperforming. Yen and Pound are positioned in the middle of the performance spectrum.

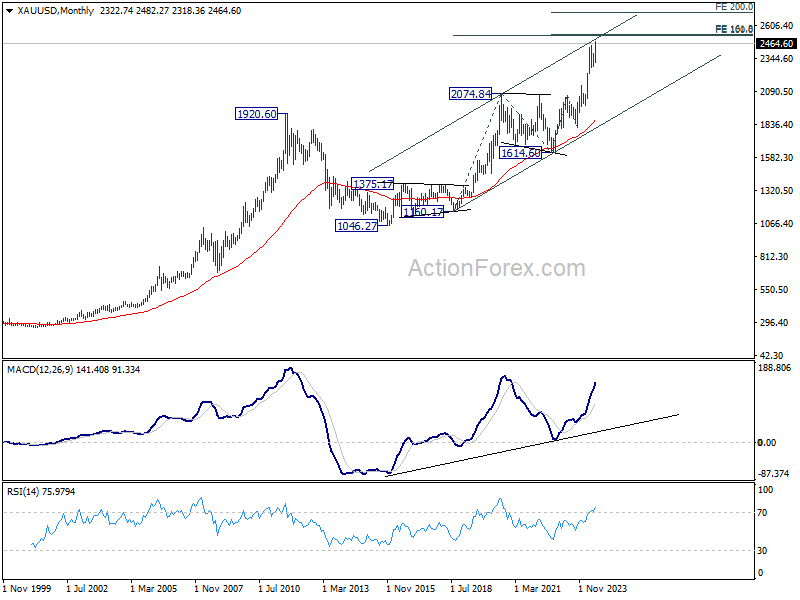

Technically, following up on our post yesterday, Gold did break to new record high. It's now facing a key cluster projection level at around 2500, with 100% projection of 1160.17 to 2074.84 from 1614.60 at 2529.27 and 161.8% projection of 1614.60 to 2062.95 from 1810.26 at 2535.96. Strong resistance could be seen from there to bring rebound.

However, decisive break above 2500/50 range could prompt upside acceleration to 200% projection of 1614.60 to 2062.95 from 1810.26 at 2706.96. For this upside acceleration to occur, broad-based selloff in Dollar might have to be seen, with EUR/USD breaking through 1.09 handle decisively.

In Asia, Nikkei fell -0.43%. Hong Kong HSI is up 0.01%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield rose 0.0103 to 1.035. Overnight, DOW surged 1.85%. S&P 500 rose 0.64%. NASDAQ rose 0.20%. 10-year yield fell -0.062 to 4.167.

UK CPI steady at 2% in Jun, core CPI unchanged at 3.5%

UK CPI was unchanged at 2.0% yoy in June, matched expectations. CPI core (excluding energy, food, alcohol and tobacco) was unchanged at 3.5% yoy, above expectation of 3.4% yoy. CPI goods annual rate fell from -1.3% yoy to 1.4% yoy. CPI services annual rate was unchanged at 5.7% yoy.

For the month, CPI rose 0.1% mom , matched expectations.

New Zealand's CPI slows to 3.3% in Q2, vs exp 3.5%

New Zealand's CPI for Q2 rose by 0.4% qoq, down from previous quarter's 0.6% qoq and missing the expected 0.5% qoq.

Tradeable inflation, which includes goods and services that are subject to international competition, fell by -0.5% qoq, an improvement from previous -0.7% qoq. Conversely, non-tradeable inflation, covering domestic goods and services, rose by 0.9% qoq, down from prior 1.6% qoq.

Over the past 12 months, CPI growth rate slowed from 4.0% yoy to 3.3% yoy, falling short of anticipated 3.5% yoy. This marks the lowest level since Q2 2021 but remains slightly above RBNZ's target band of 1-3%.

Tradeable inflation saw a significant decline from 1.6% yoy to 0.3% yoy, reflecting lower imported inflationary pressures. Non-tradeable inflation also eased, dropping from 5.8% yoy to 5.4% yoy, indicating some cooling in domestic price pressures.

Australia's Westpac leading index ticks up to -0.13%, below trend growth persists

Australia's Westpac leading index saw a slight improvement, rising from -0.28% to -0.13% in June. Despite this uptick, economic activity is expected to remain below trend until early 2025.

Westpac said while growth is expected to pick up slightly in the latter half of 2024 and into early 2025, it will still be modest, at an annual pace of 2.2%, and is about flat in per capita terms.

Fed's Kugler signals rate cuts later this year amid continued disinflation

In a speech overnight, Fed Governor Adriana Kugler noted that despite "a few bumps" earlier in the year, inflation has "continued to trend down" across "all price categories."

She mentioned that supply and demand are "gradually coming into better balance," with supply bottlenecks easing and demand moderating due to high interest rates and the depletion of households' excess savings.

Kugler also pointed out that the labor market has seen "substantial rebalancing," with nominal wage growth moderating. This trend suggests that inflation will continue moving toward Fed's 2% target.

Kugler indicated that if economic conditions continue to evolve favorably, with more rapid disinflation and resilient employment, "it will be appropriate to begin easing monetary policy later this year." However, she stressed that her approach will remain data-dependent.

She added that if the labor market cools too much and unemployment rises due to layoffs, it might be necessary to cut rates "sooner rather than later." On the other hand, if data do not confirm that inflation is moving sustainably toward 2%, it may be appropriate to "hold rates steady for a little longer."

IMF's Gourinchas suggests Fed can wait before cutting rates

IMF chief economist Pierre-Olivier Gourinchas stated in a Reuters interview that Fed can afford to "wait a little bit" before lowering interest rates. He expected that one Fed rate cut is likely this year but refrained from specifying the timing.

Gourinchas noted that the IMF expects US inflation to reach Fed's 2% target in the first half of 2025, ahead of Fed's internal projection of 2026. This suggests that there would not be an "extended period" before rate cuts become appropriate.

Looking ahead

Eurozone CPI final will be released in European session. Later in the day, US will release building permits and housing starts, industrial production and capacity utilization. Fed will also publish the beige book economic report.

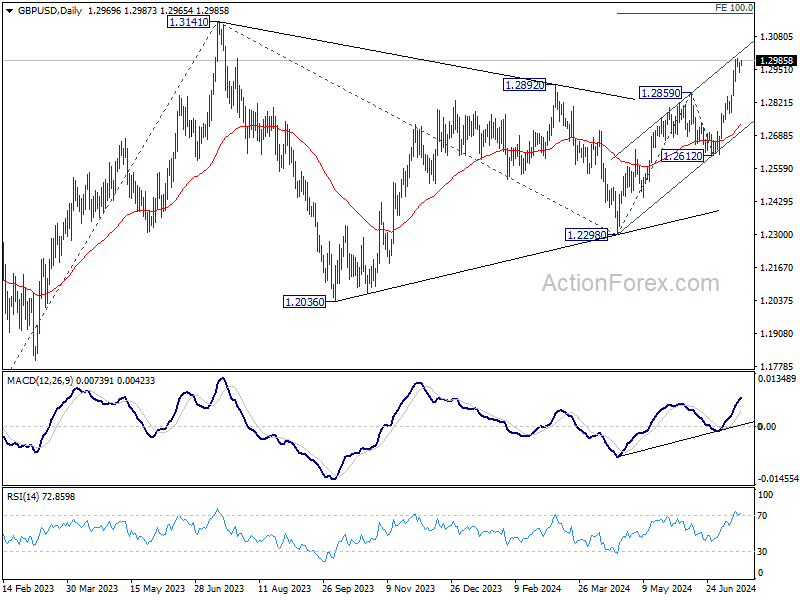

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2948; (P) 1.2965; (R1) 1.2992; More...

GBP/USD is staying in consolidation below 1.2994 temporary top and intraday bias remains neutral. Further rally is expected as long as 1.2859 resistance turned support holds. Above 1.2994 will resume the rally from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, break of 1.2859 will turn bias to the downside for deeper pullback.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 0.40% | 0.50% | 0.60% | |

| 22:45 | NZD | CPI Y/Y Q2 | 3.30% | 3.50% | 4.00% | |

| 01:00 | AUD | Westpac Leading Index M/M Jun | 0.00% | 0.00% | ||

| 06:00 | GBP | CPI M/M Jun | 0.10% | 0.10% | 0.30% | |

| 06:00 | GBP | CPI Y/Y Jun | 2.00% | 2.00% | 2.00% | |

| 06:00 | GBP | Core CPI Y/Y Jun | 3.50% | 3.40% | 3.50% | |

| 06:00 | GBP | RPI M/M Jun | 0.20% | 0.20% | 0.40% | |

| 06:00 | GBP | RPI Y/Y Jun | 2.90% | 2.90% | 3.00% | |

| 06:00 | GBP | PPI Input M/M Jun | -0.80% | 0.10% | 0.00% | -0.60% |

| 06:00 | GBP | PPI Input Y/Y Jun | -0.40% | -0.10% | -0.70% | |

| 06:00 | GBP | PPI Output M/M Jun | -0.30% | 0.10% | -0.10% | 0.00% |

| 06:00 | GBP | PPI Output Y/Y Jun | 1.40% | 1.70% | ||

| 06:00 | GBP | PPI Core Output M/M Jun | 0.10% | 0.20% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jun | 1.10% | 1.00% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 2.50% | 2.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 2.90% | 2.90% | ||

| 12:30 | USD | Building Permits Jun | 1.40M | 1.40M | ||

| 12:30 | USD | Housing Starts Jun | 1.30M | 1.28M | ||

| 13:15 | USD | Industrial Production M/M Jun | 0.30% | 0.90% | ||

| 13:15 | USD | Capacity Utilization Jun | 78.60% | 78.70% | ||

| 14:30 | USD | Crude Oil Inventories | -0.9M | -3.4M | ||

| 18:00 | USD | Beige Book |

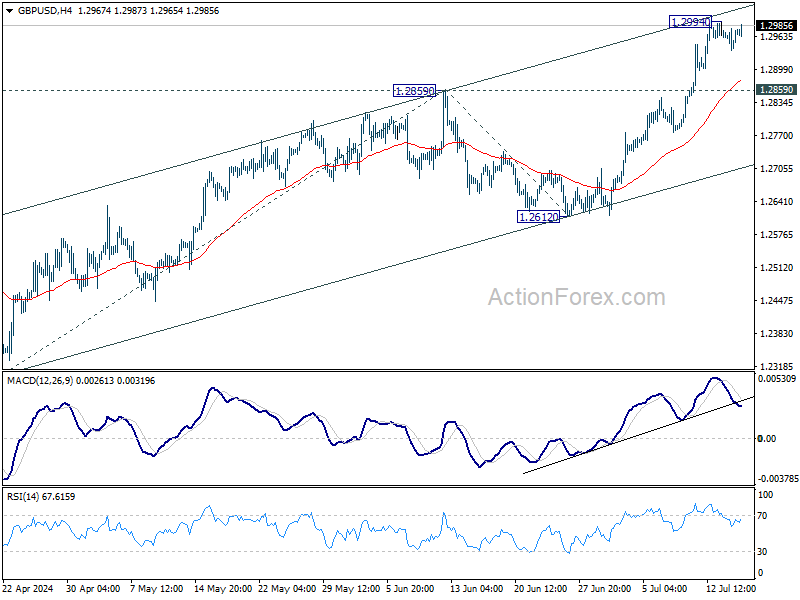

Cable Jumps as UK CPI Shows Stagnation

The S&P500 hit a fresh record this year for the 38th time on Tuesday, banks rallied on earnings which showed that the big banks’ trading revenue jumped nearly 20% in Q2 and investment banking revenues rose significantly on increased dealmaking. The technology-heavy Nasdaq 100 lagged, with smaller gains. The Russell 2000 rallied another 3.5%, on the other hand, hinting at a developing sector rotation from Big Tech to others. As such, the Russell 2000 gained more than 10% since last week, while the S&P500’s equal weight index rose faster than the technology-heavy, normal-weighted index. And all this, regardless of a better than expected retail sales data in the US and a jump in Atlanta Fed’s GDP forecast to 2.5% – which could’ve cool down the Federal Reserve (Fed) rate cut expectations, but did not.

Activity on Fed funds futures suggests that the market is now pricing in a 100% chance for a September rate cut from the Fed (odds of a 50bp cut are on the rise – yet unreasonable without a severe shock/stress). Yesterday’s retail sales data and the first few hours of Amazon Prime day sales – which climbed by almost 12% compared to last year – are not necessarily supportive of dovish Fed expectations. But the dovish Fed expectations are gaining momentum, the machine is running and it’s difficult to stop it.

And the thinking behind the sector rotation is simple: the upcoming rate cuts should give support to smaller and more cyclical pockets of the market, and convince investors to rotate from highly valued technology names to other sectors. Some say that the rising odds for a Donald Trump win in November election is also supportive of smaller and cyclical pockets of the market, provided that his domestic and growth-focused policies will benefit disproportionally to these sectors. But hey, another set of strong earnings could get investors to think twice. Plus, Mr. Vance – that Trump just revealed as his running mate earlier this week – is a tech and crypto investor. It’s said that Vance is one of the strongest blockchain advocate on Trump’s shortlist, it appears that he perceives cryptocurrencies as ‘the only realistic way to shake up big tech and finance’. No wonder Bitcoin is also having a good run since the assassination attempt on Donald Trump last weekend boosted his chances of returning to the White House, with Vance by his side.

Gold shines

Gold also hit a fresh record on the back of falling US yields – that decrease the opportunity cost of holding the non-interest bearing gold, and on the back of rising geopolitical tensions on news that Iran reportedly tried to kill Trump in the past weeks (although there has been no evidence that the weekend’s shooting has anything to do with them). It’s probably just a matter of time before we see the yellow metal hit the $2500 per ounce milestone. Some profit-taking could kick in at that level though, given that, at the current levels, gold is entering the overbought market territory, suggesting that the yellow metal may have been bought too fast in a too short period of time – as the rest of the assets that have been boosted by the super duo of Trump and Powell - and it would be healthy to see some minor downside correction.

FX and Oil

The US dollar index is still sitting on the major 38.2% Fibonacci support on this year’s rebound and should – based on the rising dovish Fed expectations – be in a position to clear this support and step into the medium-term bearish consolidation zone.

Cable jumped this morning as a kneejerk reaction to the latest inflation figures but gains rapidly faded. The data showed that inflation in Britain stagnated in June versus the expectation of a further easing. And higher-than-expected figures cooled down the expectation of an August rate cut from the Bank of England (BoE). But because the September Fed rate cut is already fully priced in, there is still room for a dovish BoE pricing into late summer – which means that we shall still see a limited upside potential in Cable: the 1.30 level could be hard to clear.

Across the Channel, the EURUSD is drilling the 1.09 offers to the upside and the euro bulls are targeting the 1.10 level. The Eurozone will reveal the latest inflation figures this morning which should show steady-to-slightly lower figures across the board.

What’s interesting is that crude oil is not benefiting from the actual Trump/Fed euphoria. The sluggish Chinese growth is weighing on the black gold since the week started. The barrel of US crude is back below its 100-DMA and is preparing to test an important Fibonacci support neat $80pb – the major 38.2% retracement on June to July rebound – to determine whether the price should stay on the actual rising path or sink into a medium-term bearish consolidation zone. Fundamentally, the reflation environment is supportive of oil prices, therefore we should see a decent support into the $80pb technical and psychological level.

UK CPI steady at 2% in Jun, core CPI unchanged at 3.5%

UK CPI was unchanged at 2.0% yoy in June, matched expectations. CPI core (excluding energy, food, alcohol and tobacco) was unchanged at 3.5% yoy, above expectation of 3.4% yoy. CPI goods annual rate fell from -1.3% yoy to 1.4% yoy. CPI services annual rate was unchanged at 5.7% yoy.

For the month, CPI rose 0.1% mom , matched expectations.

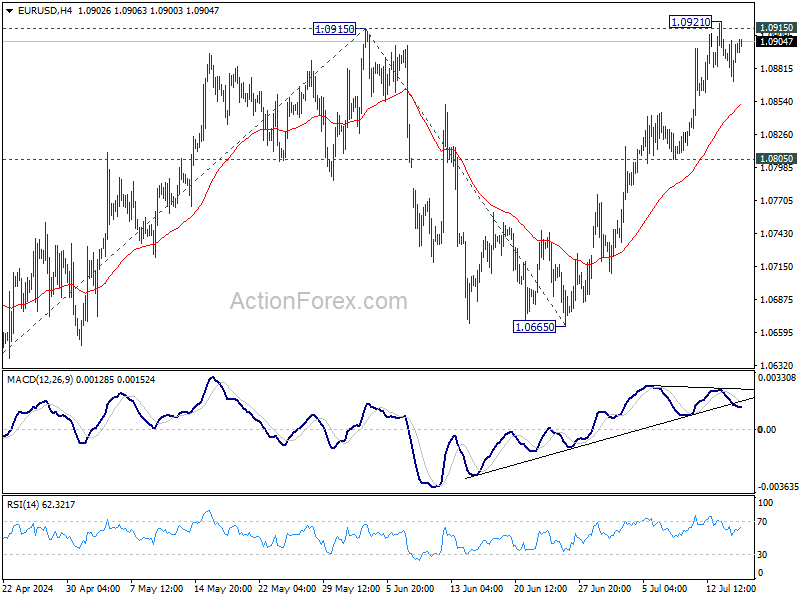

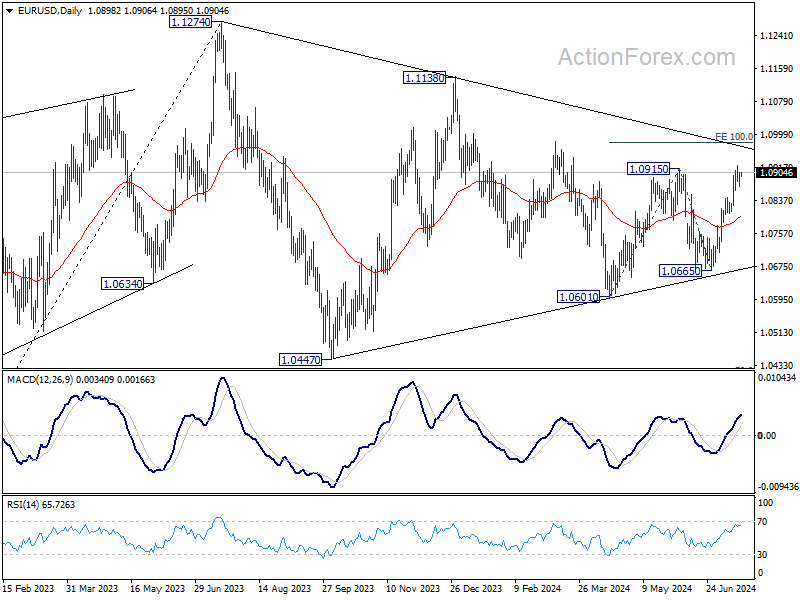

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0877; (P) 1.0900; (R1) 1.0916; More....

Intraday bias in EUR/USD remains neutral for the moment. Further rally is expected as long as 1.0805 support holds. Firm break of 1.0915/21 will will resume whole rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, break of 1.0805 will turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

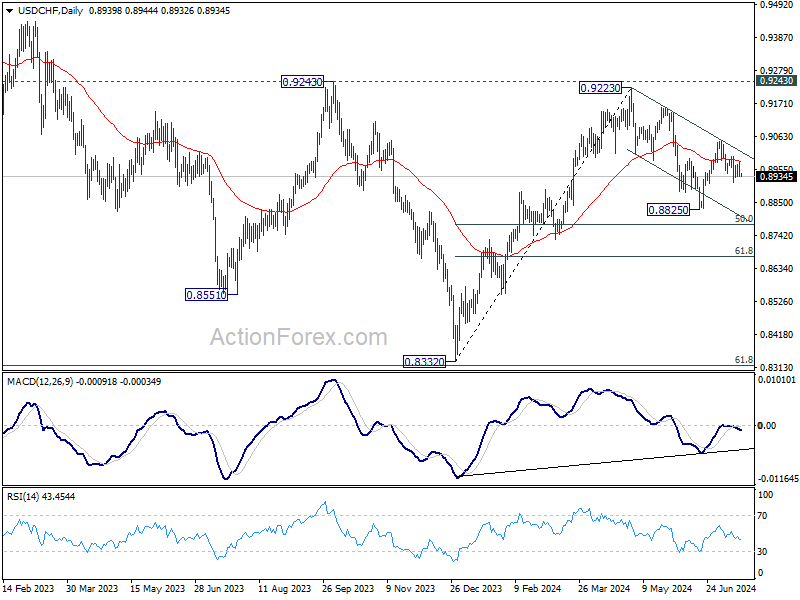

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8922; (P) 0.8951; (R1) 0.8967; More…

Intraday bias in USD/CHF remains neutral and further fall is in favor with 0.9000 resistance intact. Below 0.8914 will bring retest of 0.8825 low. However, break of 0.9000 will turn bias back to the upside for 0.9049 resistance instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

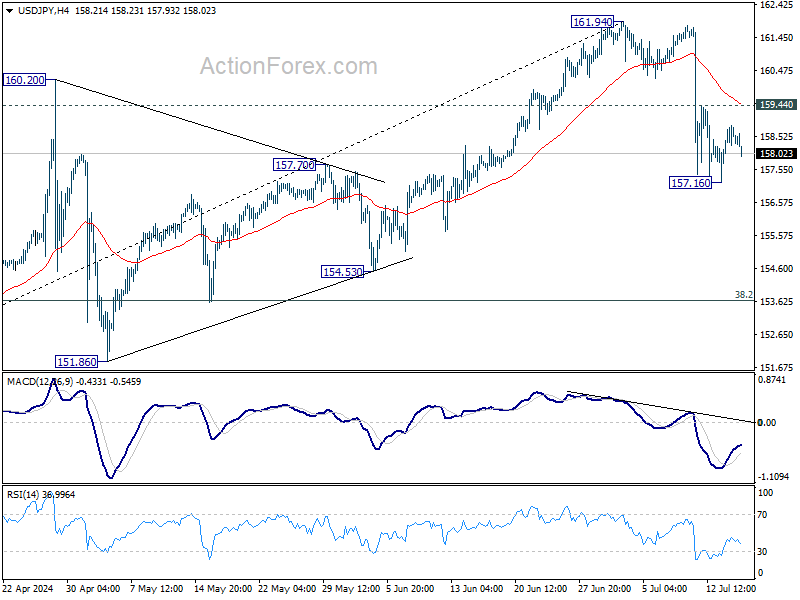

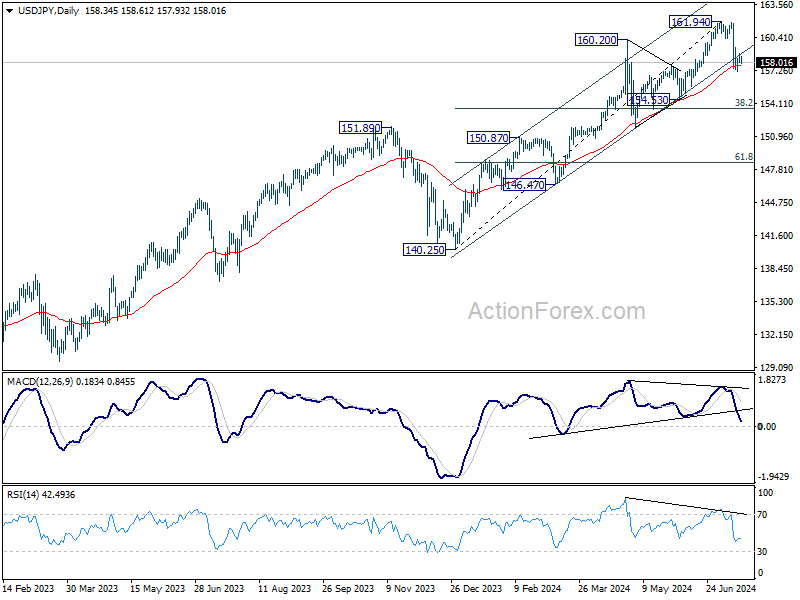

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.93; (P) 158.39; (R1) 158.88; More...

Intraday bias in USD/JPY remains neutral for the moment. On the downside, break of 157.16 and sustained trading below 55 D EMA (now at 157.72) will bring deeper correction to 38.2% retracement of 140.25 to 161.94 at 163.65. But strong support should be seen there to bring rebound. Meanwhile, break of 159.44 minor resistance will turn bias back to the upside for stronger rebound towards 161.94 high.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

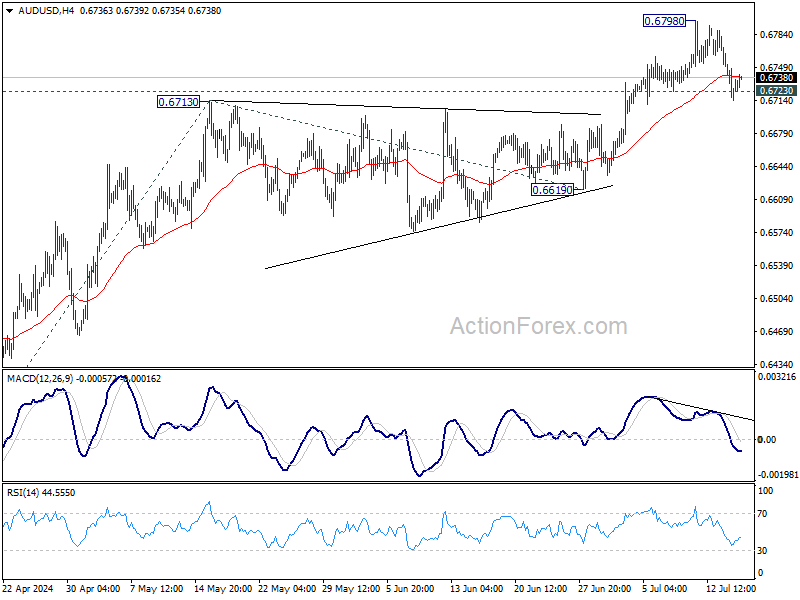

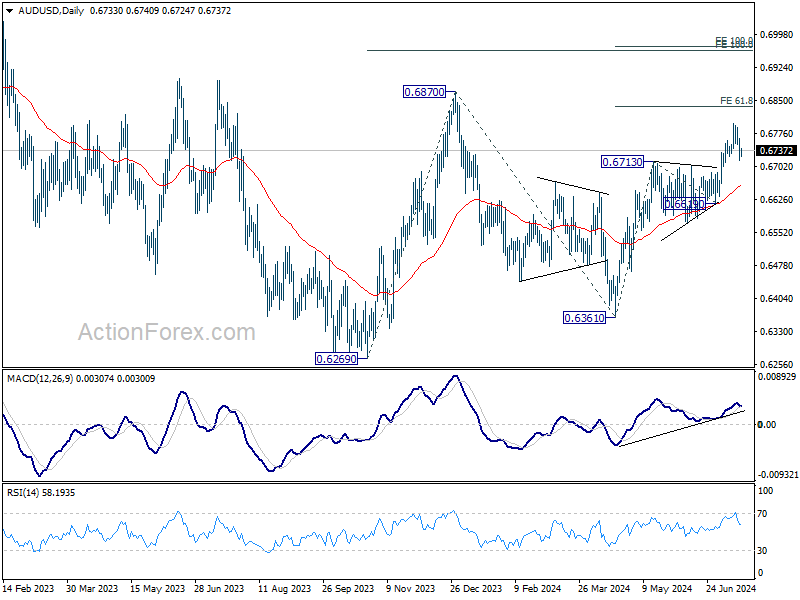

AUD/USD Daily Report

Daily Pivots: (S1) 0.6711; (P) 0.6738; (R1) 0.6761; More...

AUD/USD recovered quickly after breaching 0.6723 support and intraday bias remains neutral. Further rally is expected as long as 0.6723 minor support holds. On the upside, above 0.6798 will resume the rally from 0.6361 and target 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. On the downside, however, firm break of 0.6723 support will turn intraday bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

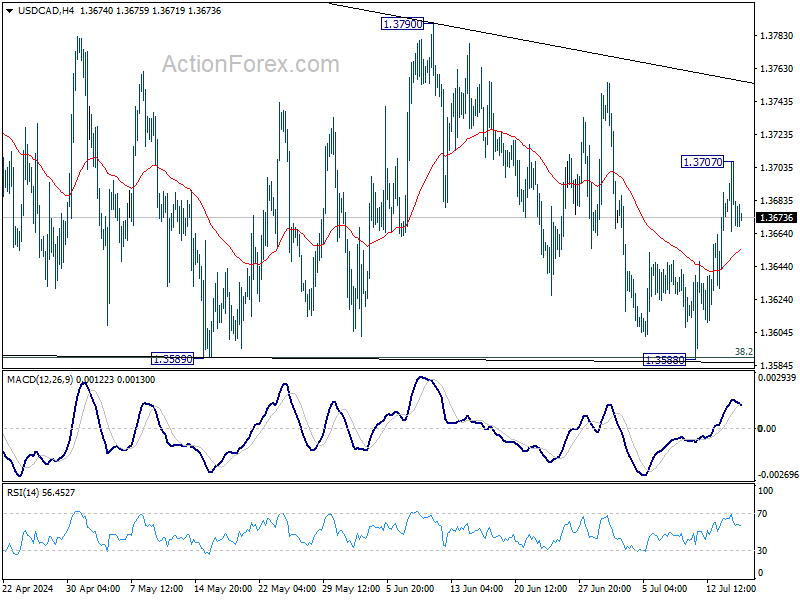

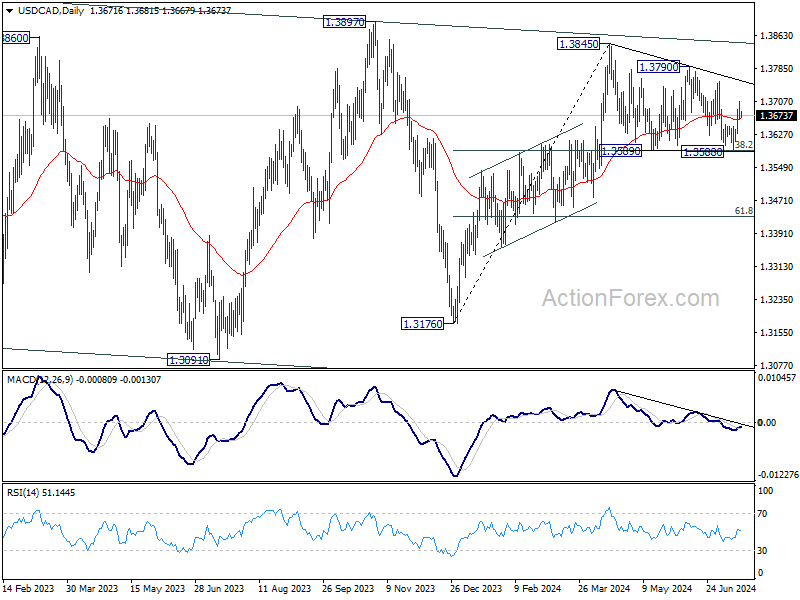

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3659; (P) 1.3683; (R1) 1.3699; More...

USD/CAD's rebound lost momentum after hitting 1.3707 and intraday bias is turned neutral first. Outlook is unchanged that corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Above 1.3707 will target 1.3790 resistance first. Break of 1.3790 will argue that larger rise from 1.3716 is ready to resume through 1.3845.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

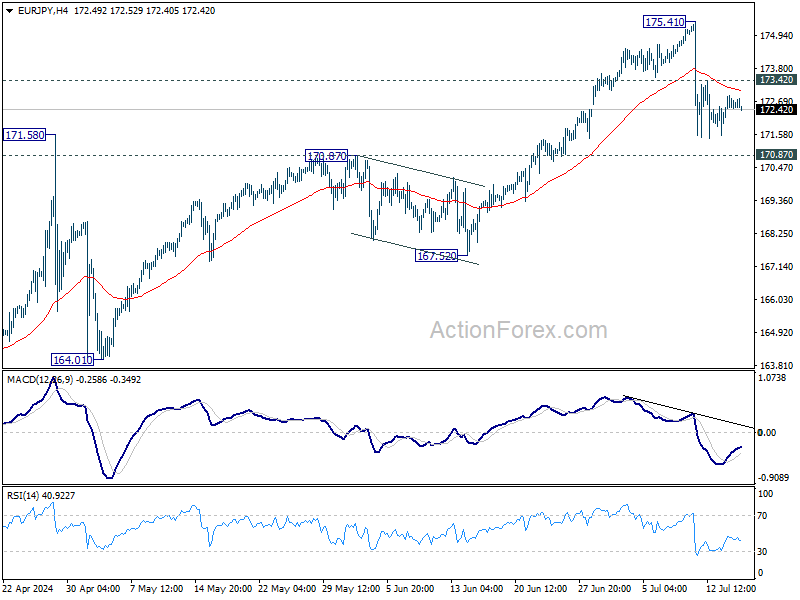

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.21; (P) 172.57; (R1) 173.00; More...

Intraday bias in EUR/JPY remains neutral at this point. Corrective fall from 175.41 could still extend lower. But downside should be contained by 170.87 and bring rebound. On the upside, above 173.42 will turn bias back to the upside for retesting 175.41. However, firm break of 170.87 will argue that larger correction is already underway and target 167.52 and possibly below.

In the bigger picture, as long as 170.87 resistance turned support holds, the long term up trend is still expected to continue. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. However, firm break of 170.87 will bring deeper fall to 167.52 support. Decisive break there will confirm that larger correction in in progress for 153.15/164.29 support zone.

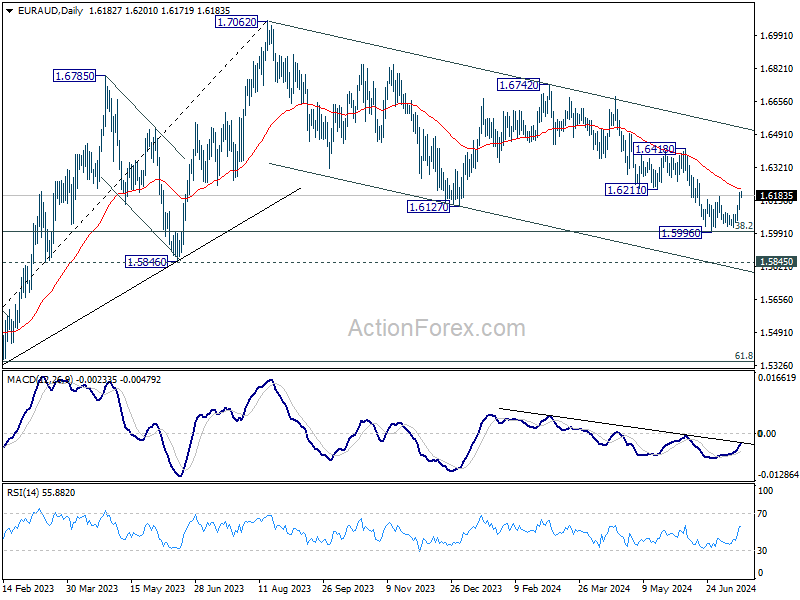

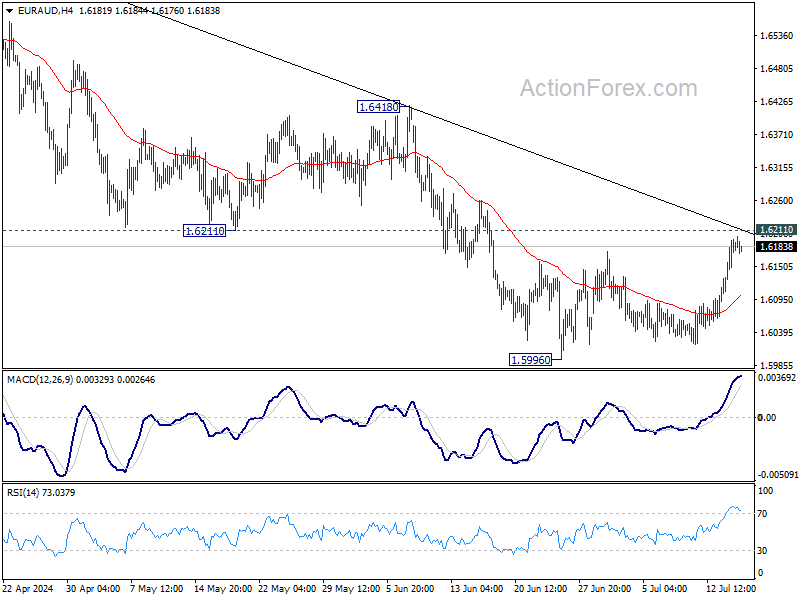

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6129; (P) 1.6164; (R1) 1.6219; More...

EUR/AUD is staying below 1.6211 support turned resistance despite current strong rebound. Intraday bias remains neutral and further decline is still in favor. On the downside, break of 1.5996 will resume larger fall to 1.5846 support next. However, firm break of 1.6211 will argue that larger corrective fall might have completed, and turn bias back to the upside for 1.6418 resistance next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6418 resistance will argue that the correction has completed.