Sample Category Title

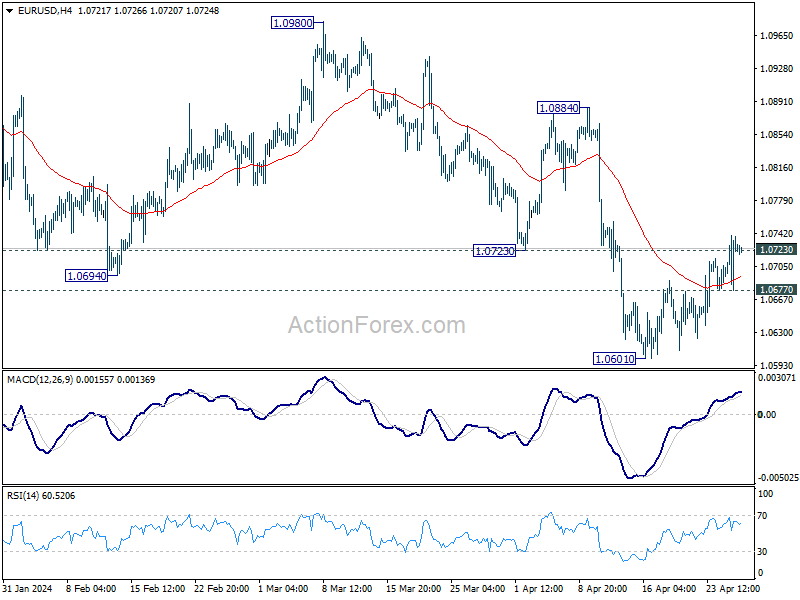

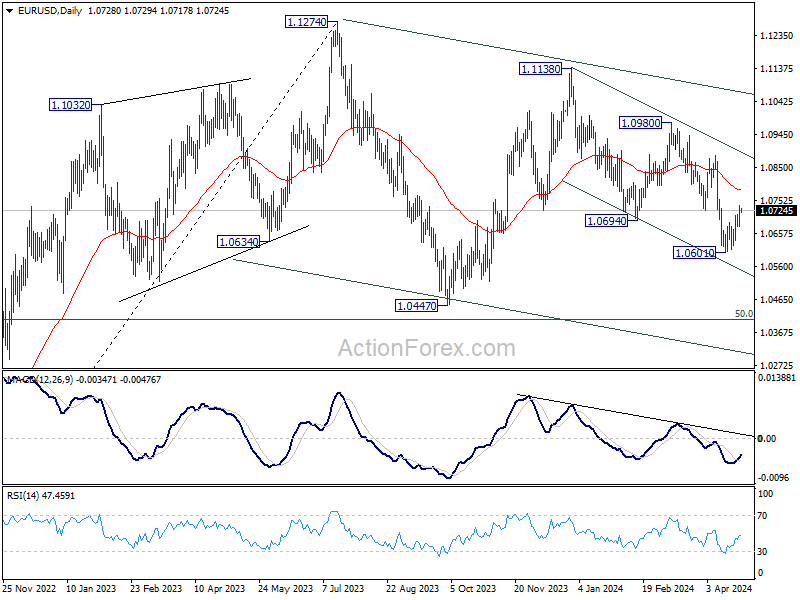

EUR/USD Daily Outlook

.Daily Pivots: (S1) 1.0692; (P) 1.0716; (R1) 1.0754; More...

Intraday bias in EUR/USD is back on the upside with break of 1.0723 support turned resistance. Stronger rebound would be seen to 55 D EMA (now at 1.0784). On the downside, break of 1.0677 minor support will turn intraday bias to the downside for retesting 1.0601 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

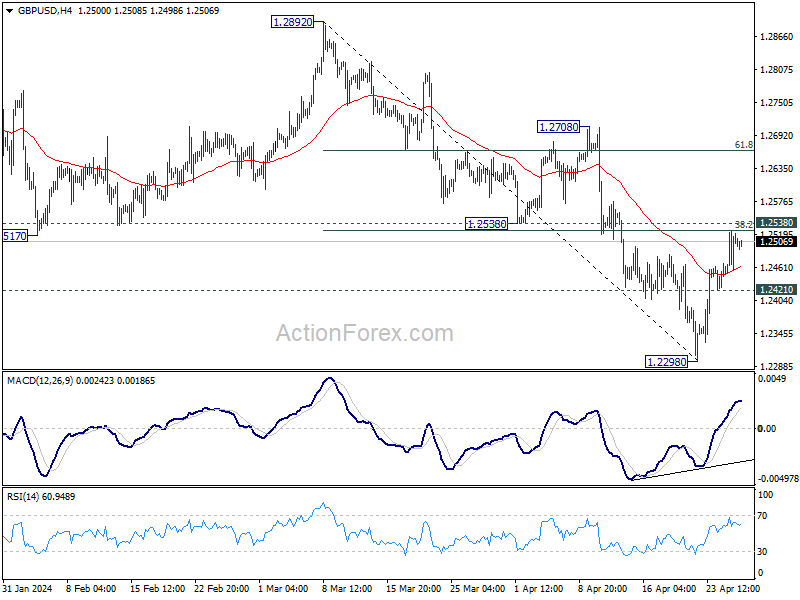

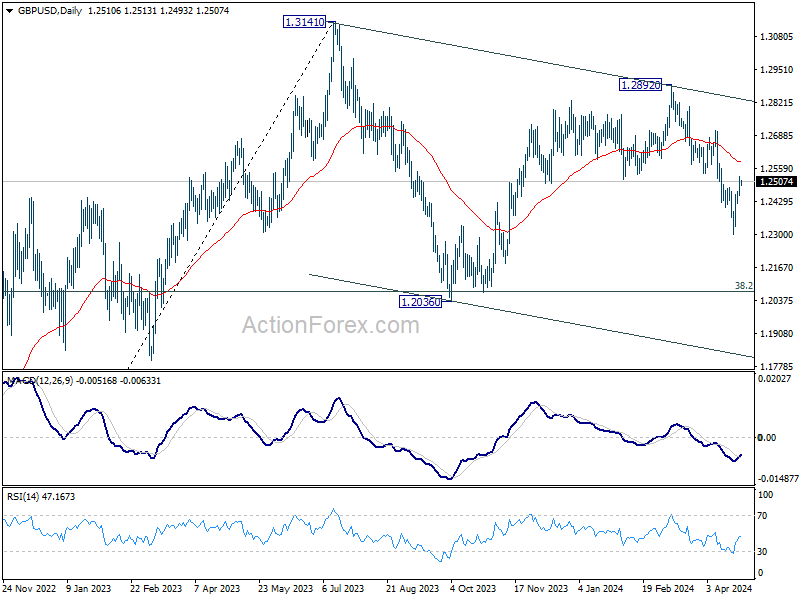

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2464; (P) 1.2495; (R1) 1.2543; More...

Intraday bias in GBP/USD remains neutral for the moment. Near term outlook stays bearish as long as 1.2538 support turned resistance holds. Break of 1.2421 minor support will argue that rebound from 1.2298 has completed and bring retest of this low. However, decisive break of 1.2538 will bring stronger rally to 55 D EMA (now at 1.2583) and above.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

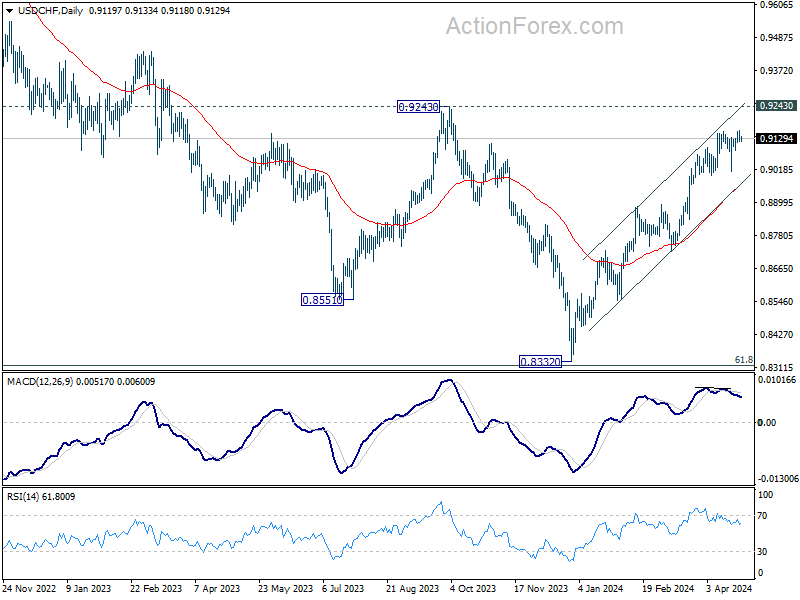

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9104; (P) 0.9137; (R1) 0.9155; More....

Intraday bias in USD/CHF is turned neutral again after it retreated after breaching 0.9151 resistance briefly. On the upside, firm break of 0.9151 will resume the rally from 0.8332 and should target 0.9243 key resistance next. On the downside, break of 0.9085 will turn bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

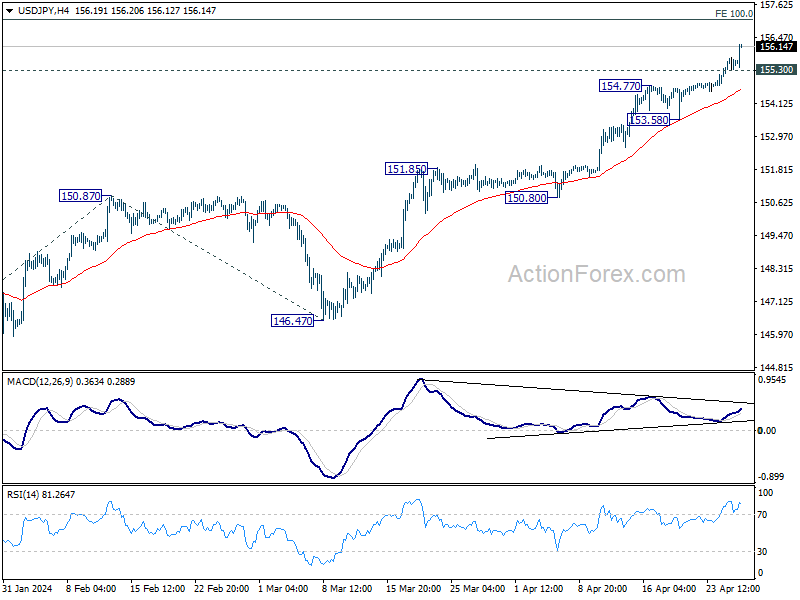

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.32; (P) 155.53; (R1) 155.87; More...

USD/JPY's fall continues today and intraday bias remains on the upside. Next target is 100% projection of 140.25 to 150.87 from 146.47 at 157.09. On the downside, below 155.30 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 153.58 support holds, in case of retreat.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Yen’s Free Fall Resumes Post-BoJ; Dollar Eyes PCE Inflation Data for Rescue

Japanese Yen resumes its free fall today, after a brief pause, and reaches new 34-year low against Dollar. Yen's weakness is also broad-based and evident against other major currencies, with EUR/JPY marching towards its 2008 high and GBP/JPY heading to its 2015 peak. It's clear that the absence of strong verbal interventions from Japanese officials has emboldened Yen bears. At the same time, BoJ's announcements failed to introduce any hawkish shifts that might have supported the currency.

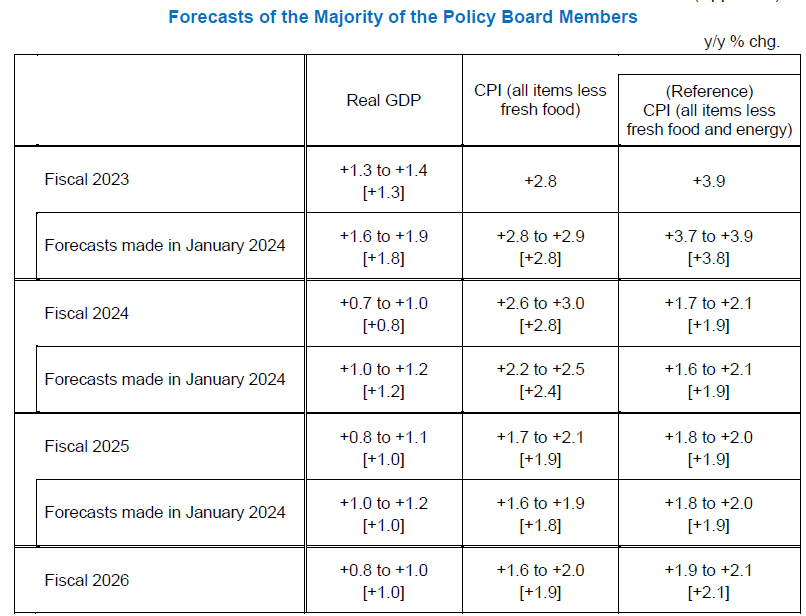

BoJ's updates included revised projections that see core-core inflation increasing to 2.1% by fiscal 2026, a development that BoJ views as a positive for inflation outlook. Meanwhile, there were substantial revisions in growth (downgraded) and inflation (upgraded) forecasts for fiscal 2024. Earlier data showed significant drop in Tokyo's inflation rates due to a one-off factor. But these are not the main drivers for Yen's decline.

Meanwhile, Dollar is positioned among the weakest performers after failing to sustain gains from a brief rebound overnight. Market focus is shifting to the upcoming US PCE inflation data. Stocks markets fell notably while treasury yield surged after yesterday's GDP report triggered repricing of Fed rate cut expectations. Odds of Fed keeping interest rates unchanged in September is now up at around. Be these developments have yet to provide a lasting boost to Dollar.

Technically, NASDAQ was rejected by 55 D EMA on first attempt, but there was no follow through selloff after initial dive overnight. While risk stays on the downside for now, the question is whether 38.2% retracement of 12543.85 to 16538.86 at 15015.67 (or simply 15k mark) could provide enough support. Firm break of 55 D EMA would set the range for a sideway consolidation pattern.

In Asia, at the time of writing, Nikkei is up 1.11%. Hong Kong HSI is up 1.94%. China Shanghai SSE is up 0.88%. Singapore Strait Times is down -0.05%. Overnight, DOW fell -0.98%. S&P 500 fell -0.46%. NASDAQ fell -0.64%. 10-year yield rose 0.054 to 4.706.

BoJ stands pat, lower growth and higher inflation this year

BoJ left overnight call rate unchanged at 0-0.10% as widely expected, by unanimous vote. The BOJ says it will continue its Japanese government bond (JGB) purchases "in accordance with the decisions made at the March 2024 monetary policy meeting."

Real GDP growth forecasts for fiscal 2024 was lowered sharply to 0.8%. But growth is expected to pick up moderately to 1.0% subsequently. CPI core forecasts was fiscal 2024 was raised to 2.8% and then slowed to 1.9% onwards. CPI core- core forecasts were left unchanged for both fiscal 2024 and 2025 at 1.9%. Fiscal 2026 CPI core-core is projected to pick up to 2.1%, which is a positive sign.

Real GDP growth forecasts:

- Fiscal 2024 at 0.8% (downgraded from 1.2%).

- Fiscal 2025 at 1.0% (unchanged).

- Fiscal 2026 at 1.0% (new).

CPI core forecasts:

- Fiscal 2024 at 2.8% (upgraded from 2.4%).

- Fiscal 2025 at 1.9% (upgraded from 1.8%).

- Fiscal 2026 at 1.9% (new).

CPI core-core forecasts:

- Fiscal 2024 at 1.9% (unchanged).

- Fiscal 2025 at 1.9% (unchanged).

- Fiscal 2026 at 2.1% (new).

Japan's Tokyo CPI falls sharply to 1.6% yoy in Apr, vs exp 2.2% yoy

Japan's Tokyo CPI showed significant slowdown in April. CPI core (excluding food) dropped from 2.4% yoy to 1.6%, substantially below the expected 2.2% yoy.

CPI core-core, which excludes both food and energy, also slowed from 2.9% yoy to 1.8% yoy, marking the slowest pace since September 2022.

Services inflation, a significant component of the CPI, decreased from 2.7% yoy to 1.6% yoy. This notable drop is largely attributed to policy interventions by the Tokyo metropolitan government to make some educational tuition free.

Overall headline CPI, which includes all items, also fell from 2.6% yoy to 1.8% yoy.

Looking ahead

Eurozone M3 money supply will be released in European session. Main focus will be on US personal income and spending, and PCE inflation later in the day.

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.32; (P) 155.53; (R1) 155.87; More...

USD/JPY's fall continues today and intraday bias remains on the upside. Next target is 100% projection of 140.25 to 150.87 from 146.47 at 157.09. On the downside, below 155.30 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 153.58 support holds, in case of retreat.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 100% projection of 127.20 to 151.89 from 140.25 at 164.94. Outlook will remain bullish as long as 150.87 resistance turned support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Apr | -19 | -20 | -21 | |

| 23:30 | JPY | Tokyo CPI Y/Y Apr | 1.80% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Apr | 1.60% | 2.20% | 2.40% | |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Apr | 1.80% | 2.90% | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | -1.80% | 0.10% | 1.10% | |

| 01:30 | AUD | PPI Q/Q Q1 | 0.90% | 0.90% | ||

| 01:30 | AUD | PPI Y/Y Q1 | 4.30% | 4.10% | ||

| 03:22 | JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 0.50% | 0.40% | ||

| 12:30 | USD | Personal Income M/M Mar | 0.50% | 0.30% | ||

| 12:30 | USD | Personal Spending Mar | 0.30% | 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Mar | 0.30% | 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Mar | 2.60% | 2.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Mar | 0.30% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Mar | 2.60% | 2.80% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Apr F | 77.9 | 77.9 |

BoJ stands pat, lower growth and higher inflation this year

BoJ left overnight call rate unchanged at 0-0.10% as widely expected, by unanimous vote. The BOJ says it will continue its Japanese government bond (JGB) purchases "in accordance with the decisions made at the March 2024 monetary policy meeting."

Real GDP growth forecasts for fiscal 2024 was lowered sharply to 0.8%. But growth is expected to pick up moderately to 1.0% subsequently. CPI core forecasts was fiscal 2024 was raised to 2.8% and then slowed to 1.9% onwards. CPI core- core forecasts were left unchanged for both fiscal 2024 and 2025 at 1.9%. Fiscal 2026 CPI core-core is projected to pick up to 2.1%, which is a positive sign.

Real GDP growth forecasts:

- Fiscal 2024 at 0.8% (downgraded from 1.2%).

- Fiscal 2025 at 1.0% (unchanged).

- Fiscal 2026 at 1.0% (new).

CPI core forecasts:

- Fiscal 2024 at 2.8% (upgraded from 2.4%).

- Fiscal 2025 at 1.9% (upgraded from 1.8%).

- Fiscal 2026 at 1.9% (new).

CPI core-core forecasts:

- Fiscal 2024 at 1.9% (unchanged).

- Fiscal 2025 at 1.9% (unchanged).

- Fiscal 2026 at 2.1% (new).

Cliff Notes: Inflation Risks Linger

Key insights from the week that was.

In Australia, the Q1 CPI printed 1.0% (3.6%yr) for headline inflation and 1.0% (4.0%yr) for underlying trimmed mean inflation, meaningfully higher than consensus and likely the RBA’s view too, based on our assessment of its June 2024 forecast (3.3%yr headline, 3.6%yr trimmed mean). The latest update is consistent with an ongoing moderation in consumer inflation, aided in large part by global disinflationary forces within tradables, but the detail did reveal some upside surprises in the quarter.

Electricity prices were not as weak as anticipated (–1.7% vs. –3.4% forecast), though it is worth emphasising that the Government’s Energy Bill Relief Fund remains an effective tool in shielding households from much worse outcomes. Additionally, the increase in pharmaceutical prices (7.1% vs. 4.7% forecast) and financial/ insurance premiums (2.0% vs. 1.4% forecast) were stronger than expected, while car prices also surprisingly lifted (1.0% vs. –0.6%). The upside surprises were generally not in categories that point to strong domestic demand, however.

As detailed by Chief Economist Luci Ellis in her note mid-week, evidence of a slower-than-expected pace of disinflation during the opening quarter have coincided with a firmer set of data prints on the labour market over recent months. The balance of risks points to the RBA Board retaining a cautious perspective over the next few months, as new information on the labour market, prices and economic growth are closely scrutinised for signs of upside risk to the inflation outlook.

All-in-all, we still anticipate that there will be no change to the RBA’s policy stance in May; however, we now expect policy to remain on hold for longer, with the first rate cut now forecast to occur in November rather than September. Thereafter, and assuming no further upside surprises to inflation, the RBA will have scope to lessen the contractionary setting of monetary policy at an incremental and measured pace. We expect 25bps of rate cuts per quarter through to Q4 2025, to a terminal rate of 3.10%.

Also critical to the medium-term economic outlook will be developments around fiscal policy. For an in-depth analysis on the national fiscal outlook ahead of the Federal Budget update in May, see our latest update published earlier today on WestpacIQ.

Offshore, the focus was on the US activity data showcasing a resilient economy. GDP expanded at an annualised rate of 1.6% in Q1, and while the headline result undershot expectations, the detail suggests this is not reflective of a weak domestic economy. Personal consumption rose 2.5% with services rising 4.0% – the fastest rise in services since 2021. A sharp rise in imports, centred on services, drove the weakness in the quarter. Excluding trade, GDP came in within expectations. Strong growth was accompanied by strong prices – the PCE ex. food and energy rose 3.7%yr and implies a 0.4%mth rise in core PCE out later today. This would mark a reacceleration in PCE inflation after two months of deceleration. All together, the US economy is in a strong position with consumption supporting inflation.

Durable goods orders rose 2.6%mth in March and 0.2%mth stripping out the volatile transportation and defence categories. Together with the tepid non-residential investment data from GDP, the outlook for growth in manufacturing and investment remains clouded by high borrowing costs. Recent data will likely prompt a more hawkish tone from the FOMC to temper inflation expectations, noting that it will take time for restrictive policy to cool inflation.

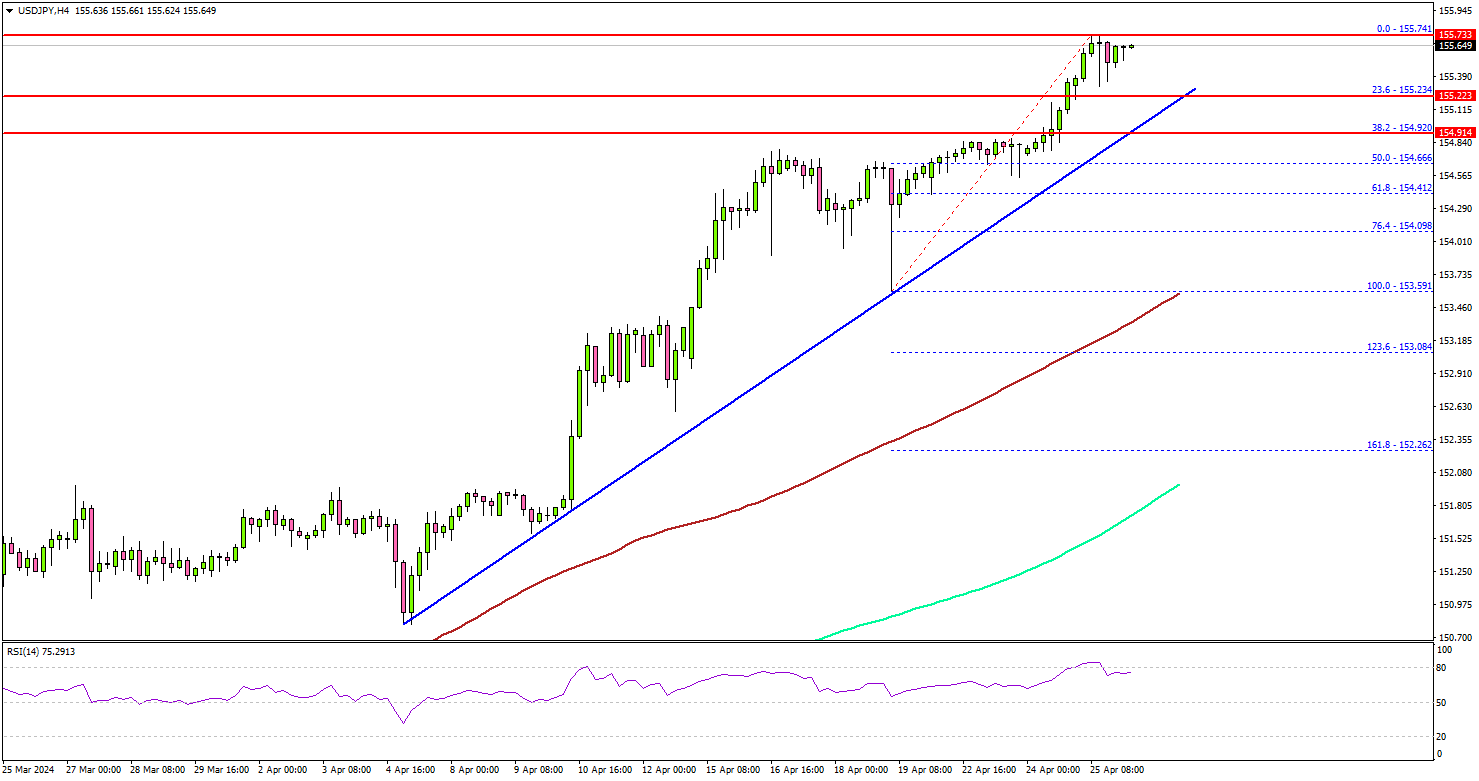

USD/JPY Sets New Multi-Decade High, Bulls In Control

Key Highlights

- USD/JPY rallied further above the 155.00 resistance.

- A major bullish trend line is forming with support at 155.20 on the 4-hour chart.

- EUR/USD is struggling to clear the 1.0750 resistance zone.

- Crude oil prices could decline and revisit the $81.00 level.

USD/JPY Technical Analysis

The US Dollar remained in a strong uptrend above 152.00 against the Japanese Yen. USD/JPY extended its increase above 155.00 and traded to a new multi-decade high.

Looking at the 4-hour chart, the pair traded above 155.50 and settled well above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). The pair seems to be consolidating gains above the 23.6% Fib retracement level of the upward move from the 153.59 swing low to the 155.74 high.

Immediate resistance is near the 155.75 level. The first key resistance is near the 156.00 zone. A clear move above the 156.00 resistance could send the pair further higher. In the stated case, USD/JPY bulls could even aim for a move toward 157.50.

Immediate support is near the 155.20 level. There is also a major bullish trend line forming with support at 155.20 on the same chart.

The next major support is at 154.90. If there is a downside break below the 154.90 support, the pair might test 154.00. The main support is now forming at 153.50. Any more losses might send the pair toward 152.00.

Looking at Oil, the price extended losses and it seems like the bears could aim for a move toward the $81.00 level in the near term.

Economic Releases

- US Personal Income for March 2024 (MoM) - Forecast +0.5%, versus +0.3% previous.

- US Personal Spending for March 2024 (MoM) - Forecast +0.6%, versus +0.8% previous.

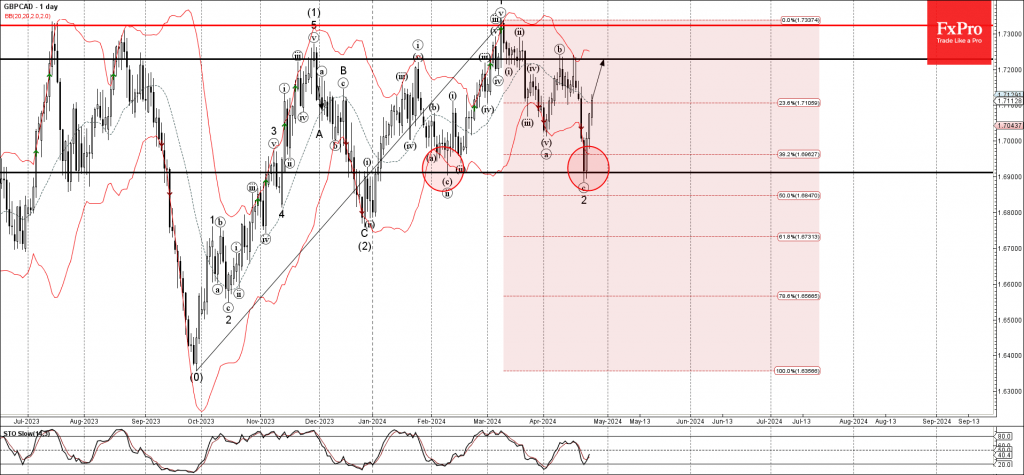

GBPCAD Wave Analysis

- GBPCAD reversed from key support level 1.6910

- Likely to rise to resistance level 1.7230

GBPCAD currency pair recently reversed up sharply from the key support level 1.6910, (former monthly low from February), standing well below the lower daily Bollinger Band.

The upward reversal from the support level 1.6910 created the strong daily Japanese candlesticks reversal pattern Bullish Engulfing – which stopped the pervious wave 2.

Give the strength of the support level 1.6910, GBPCAD currency pair can be expected to rise further to the next resistance level 1.7230 (which stopped the pervious wave b).

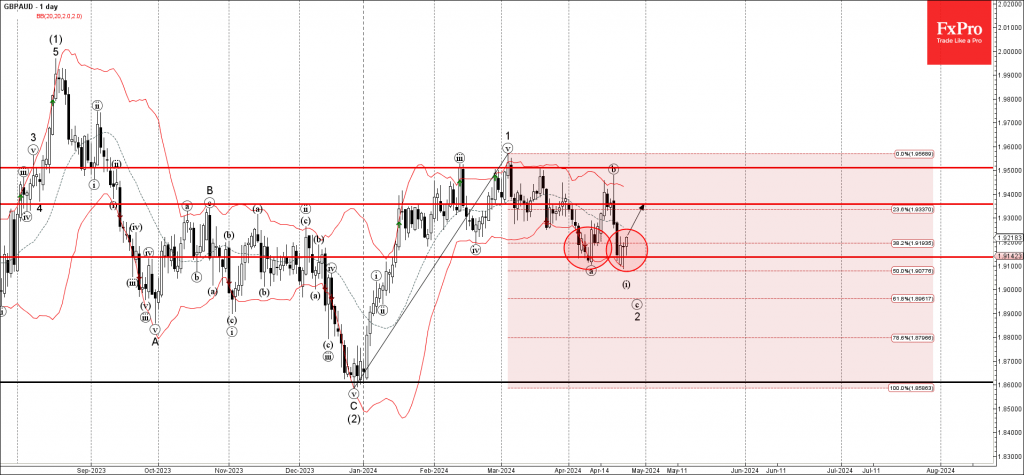

GBPAUD Wave Analysis

- GBPAUD reversed from support level 1.9135

- Likely to rise to resistance level 1.9360

GBPAUD currency pair recently reversed up from the pivotal support level 1.9135, which has been reversing the price from the start of April, intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the previous upward impulse 1 from December.

The upward reversal from the support level 1.9135 created the daily Japanese candlesticks reversal pattern Hammer Doji.

Give the strength of the support level 1.9135, GBPAUD currency pair can be expected to rise further to the next resistance level 1.9360.