Sample Category Title

Sunset Market Commentary

Markets

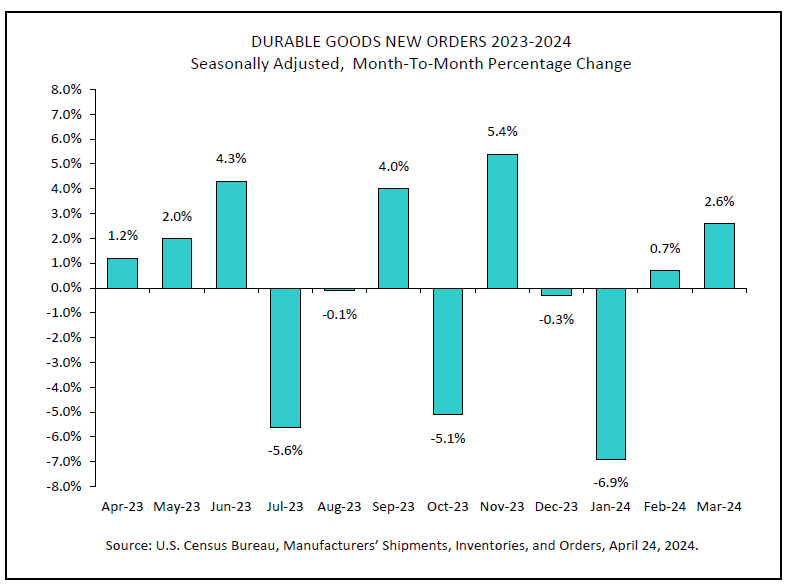

Core bonds lost ground with German Bunds underperforming US Treasuries today. It would be unfair to link the former exclusively to the better-than-expected German Ifo indicator but it did support yields moving higher. The headline series improved from 87.9 to 89.4 with an increase in current conditions (88.9) but especially in the expectations component (87.7 to 89.9, the highest since April last year). The Ifo brought a similar “there’s light at the end of the tunnel” message as yesterday’s PMIs with the same distinction being made in the ailing (but with improving prospects) manufacturing sector and the services sector as the current stronghold. German yields add between 3.7 and 7.1 bps. We suspect the technical charts offered some help too with the long end moving beyond the precious YtD highs to hit new ones. The 10-y tenor is fast approaching the 2.6% resistance area (62% recovery on the 2023Q4 decline). US yields recover a good part from the PMI-induced losses yesterday. The long end underperforms with the likes of the 10y yield adding about 4.5 bps. Shorter maturities rise 1.5 bps. US data today included durable goods orders which printed bang or near in line with consensus. The headline series jumped 2.6% on the back of firmer commercial aircraft and defense-related orders. Core gauges, including the one used in calculating the investment component in GDP readings, printed at 0.2%.

The Australian dollar outperforms in the G10 currency landscape today. Higher-than-expected Q1 inflation numbers released this morning question the Reserve Bank of Australia’s capacity to cut rates already this year. The market implied probability dropped from 93% to 46%, pushing Australian yields and the currency higher. AUD/USD appreciated to 0.653 but met with though resistance from the 200dMA there. The pair is currently trading back below 0.65. The US dollar trades with a minor strengthening bias. EUR/USD turned just south of 1.07, DXY ekes out a gain to 105.84. USD/JPY hit an intraday high of 155.17 – a new 34y high – but quickly swung back sub 155 again as fears linger further JPY deprecation this time may actually spark FX interventions by Japanese officials.

News & Views

Czech confidence improved both amongst consumer and among businesses. The composite indicator rose from 94.2 to 97, the best level since April 2023. Business confidence improved from 93 to 95.6 with solid increases in industry and selected services. Sentiment deteriorated in construction and (slightly) in trade. Consumer confidence increased for the fourth time in a row to 103.8. The number of respondents expecting a deterioration in the overall economic situation in the next twelve months decreased and less consumers assess their current financial situation worse than in the previous twelve months. The number of respondents expecting a deterioration in their financial situation in the next twelve months is unchanged. The share believing that the current time is not suitable for making major purchases was unchanged compared to the previous month. Better activity data and a cautious easing policy by the Czech national bank (CNB) for now only provided limited support for the koruna. EUR/CZK is trading near 25.25, still not that far from the lows recorded in February (25.51) and (25.44) earlier this month.

After rising for two consecutive months, the monthly business confidence indicator of the National Bank of Belgium fell in April. The noticeable rise in confidence seen in manufacturing in March has taken a big hit this month. The loss of confidence was mainly due to a significantly less encouraging assessment of stock levels and a sharp downward revision of demand expectations. Employment expectations were also downgraded, but to a much lesser extent. Confidence also weakened in the business-related services sector, albeit to a lesser extent. In the building industry and trade, the indicator is essentially holding steady. Despite the setback in April, the indicator of the underlying economic trend continues to rise slightly. The capacity utilization rate in the manufacturing industry marginally decreased quarter-on-quarter, from 74.4% in January 2024 to 73.8% in April 2024.

Graphs

AUD/USD: Aussie dollar extends recent recovery on stronger-than-expected Q1 inflation figures

European 10y swap yield pushes through to new year-to-date high as evidence of economy bottoming out grows

EUR/CZK: Czech crown not impressed by improving soft and hard economic data and restrained monetary easing

Nasdaq leaves correction mode for now after finding support at the start of the week

Canada: Retail Sales Registered Loss in February, Auto Sales Partially Recover

Retail sales declined by 0.1% month-on-month (m/m) in February, coming in weaker than Statistics Canada's advance estimate for a 0.1% gain. January's print was unchanged at -0.3% m/m.

Adjusted for inflation, the volume of retail sales was down 0.3% in January after two months of gains.

Sales at motor vehicle and parts dealers rose by 0.5%, erasing some of last month's losses. According to industry estimates, March is trending positive for auto sales.

Sales at gas stations were down 2.2% m/m despite higher prices at the pump.

Excluding auto sales and receipts at gas stations, core retail sales were flat on the month. In volume terms, receipts at gas stations were down by 3.9%.

- The biggest losses were reported at electronics and appliance stores (-2.8% m/m) and clothing and clothing accessories stores (-1.0% m/m).

- Offsetting these losses were gains at general merchandise stores (+1.1% m/m).

E-commerce sales (not included in the headline tally) were up 1.9% m/m in February.

Statistics Canada's advance reading suggests that retail sales were unchanged in March (with almost 62% of companies surveyed providing responses).

Key Implications

Today's decline in retail sales for February was more widespread than what we saw in January, reflecting weaker-than-expected performance in core measures and underscoring the challenges facing consumers amid rising costs of living and financing. Despite the overall softness, auto sales emerged as a bright spot, demonstrating their usual roly-poly resilience by bouncing from the previous month's decline. In addition, our internal credit and debit spend data point to an expansion in both goods and services spending in March, keeping our real consumption tracking in the range of 2.8% to 3.0% for the first quarter of 2024.

Relatively solid spending momentum has been supported by a still-sizeable excess deposits, robust population growth and a wealth effect. However, with the labour market losing steam, income growth is likely to moderate, dictating a slower pace of spending. .

AUD/USD Extends Gains as Inflation Higher Than Expected

The Australian dollar has edged higher on Wednesday. In the European session, AUD/USD is trading at 0.6504, up 0.27%. The Australian dollar rose as high as 0.6529 (0.64%) after the Australian inflation release but has pared about half of those gains.

Australia’s inflation dips less than forecast

Australia’s inflation rate slowed less than expected in the first quarter. Inflation rose 3.6% y/y in Q1, down sharply from 4.1% in the fourth quarter but above the market estimate of 3.4%. This was the lowest rate since Q4 2024 and the drop was widespread across most components of inflation.

Inflation accelerated in March on a quarterly basis (0.6% to 1%) and monthly (3.4% to 3.5%), as services inflation remains sticky. A key core inflation indicator, the trimmed mean, accelerated to 1% q/q, above the market estimate of 0.8%. Annually, the trimmed mean slowed to 4%, down from 4.2%.

The inflation numbers were higher than what the market was expecting and the Reserve Bank of Australia will be concerned, in particular with the 1% rise in the trimmed mean. The markets pared the probability of a rate cut in May to 3% after the inflation report and have not fully priced a quarter-point drop until February 2025.

The RBA is likely done with its rate-tightening cycle, which has boosted the cash rate to 4.25%, but has paused three straight times. The central bank has shown it can be patient and is unlikely to lower rates until underlying inflation eases and the tight labor market shows signs of cracks.

AUD/USD Technical

- AUD/USD tested support at 0.6487 earlier. Below, there is support at 0.6424

- 0.6555 and 0.6618 are the next resistance lines

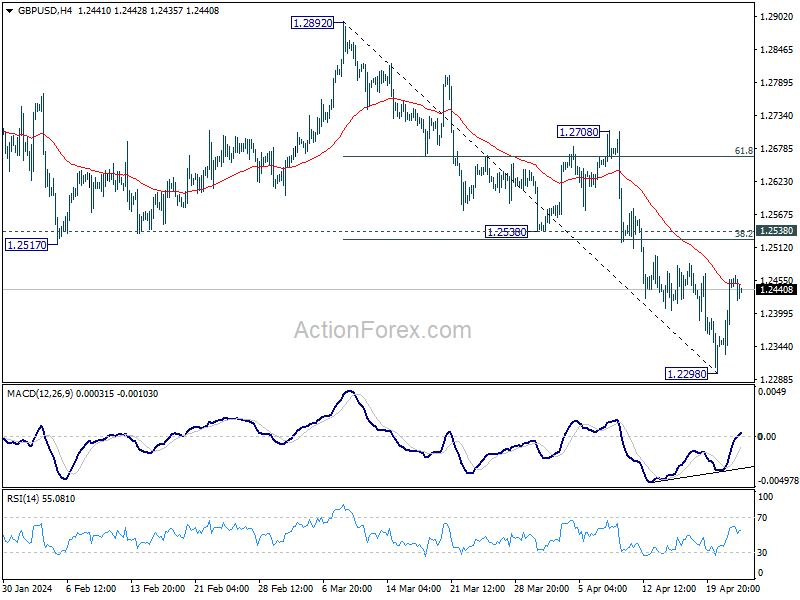

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2368; (P) 1.2414; (R1) 1.2495; More...

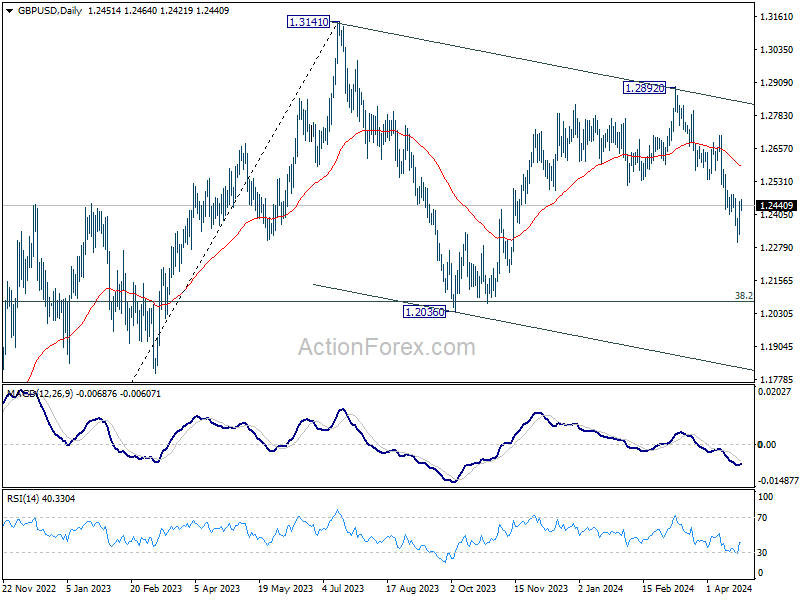

No change in GBP/USD's outlook and intraday bias stays neutral. While recovery from 1.2298 might extend higher, upside should be limited by 1.2538 support turned resistance. On the downside, below 1.2298 will resume the fall from 1.2892 to 1.2036 support next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

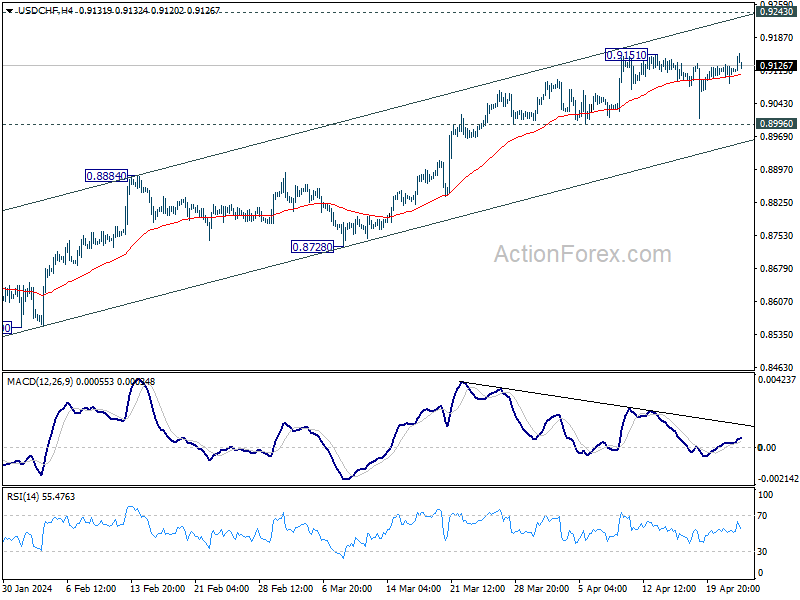

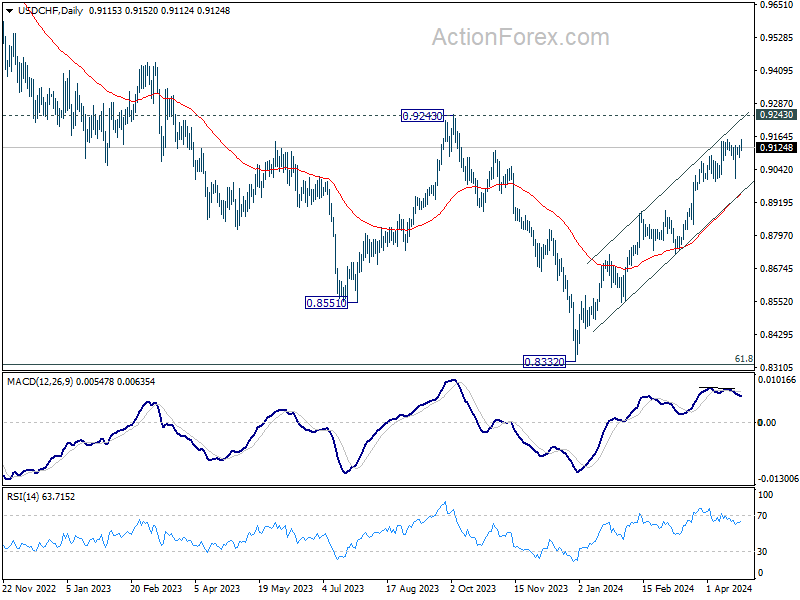

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9093; (P) 0.9113; (R1) 0.9138; More....

Intraday bias in USD/CHF remains neutral and outlook is unchanged. Further rally is expected as long as 0.8996 support holds. Break of 0.9151 will resume the larger rise from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will turn bias to the downside for 55 D EMA (now at 0.8953).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

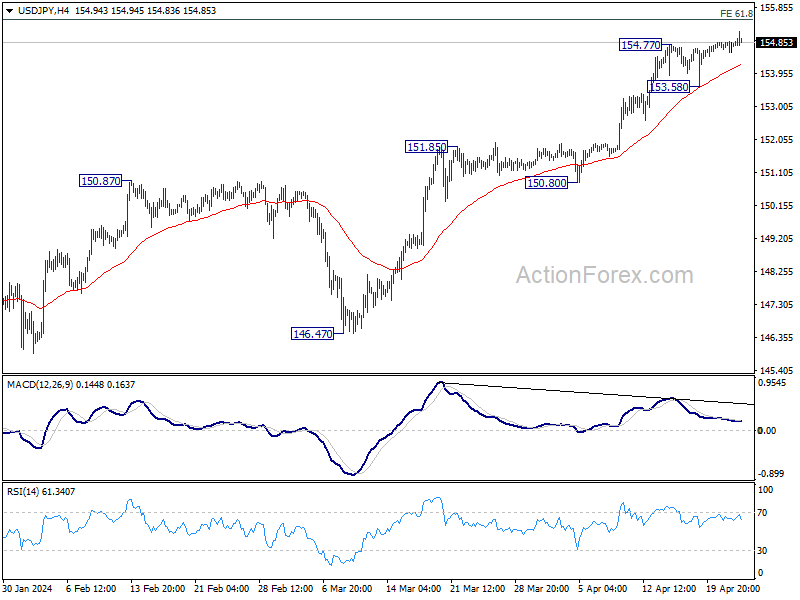

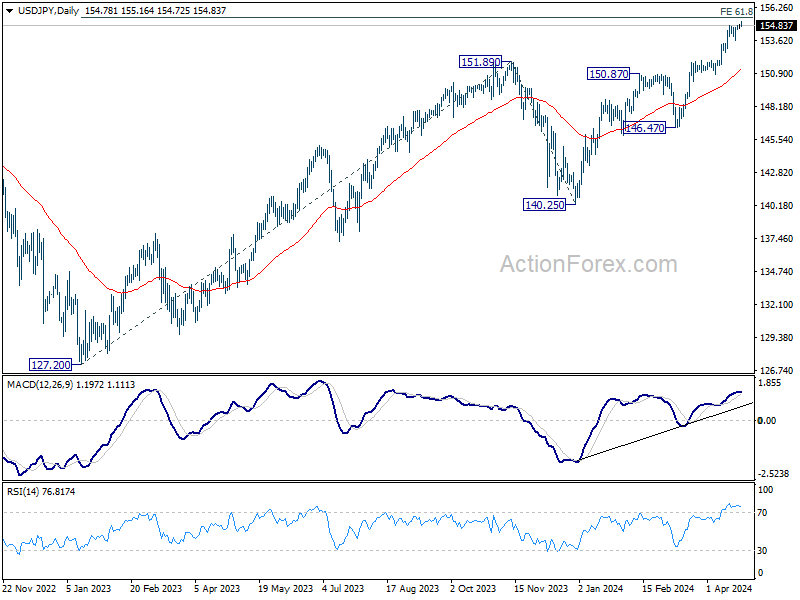

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.63; (P) 154.76; (R1) 154.95; More...

Outlook in USD/JPY is unchanged and intraday bias remains mildly on the upside for further rally. However, considering bearish divergence condition in 4H MACD, strong resistance should be seen from 155.20 fibonacci level to bring correction on first attempt. On the downside, break of 153.58 support will turn bias to the downside, for deeper pull back to 55 D EMA (now at 151.11).

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will remain bullish as long as 146.47 support holds, even in case of deep pullback.

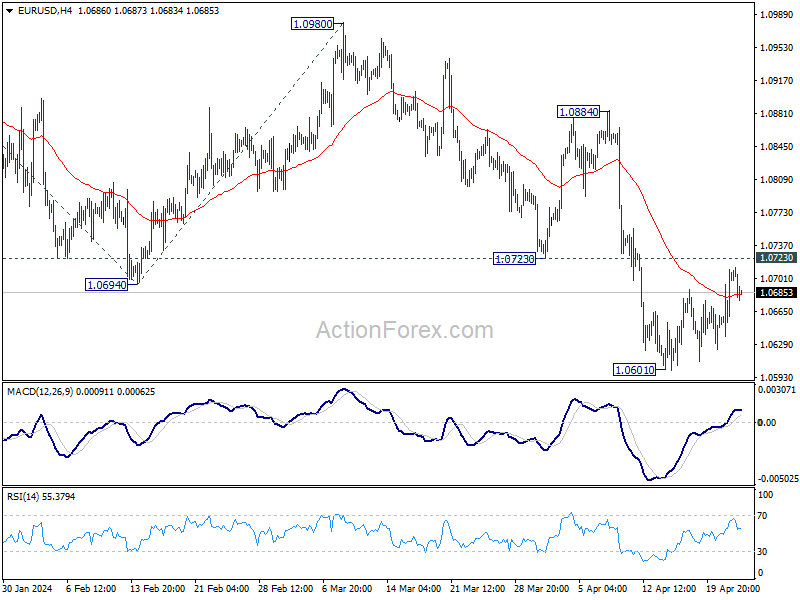

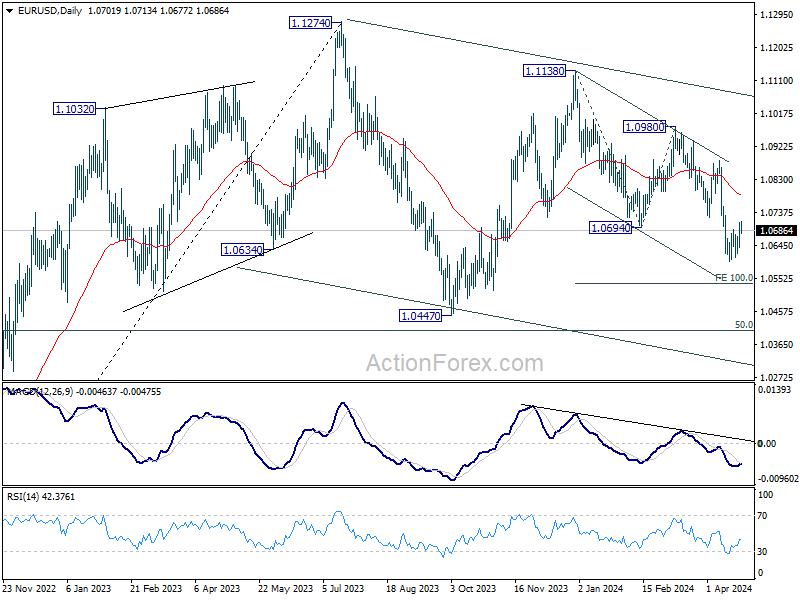

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0656; (P) 1.0684; (R1) 1.0729; More...

EUR/USD is still bounded in range trading above 1.0601 and intraday bias remains neutral. Strong resistance should be seen from 1.0723 to complete the corrective rise from 1.0601. Break of 1.0601 will resume the fall from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. Nevertheless, firm break of 1.0723 will bring stronger rebound to 55 D EMA (now at 1.0786) instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

Dollar Gains Following Durable Goods Data, Canadian Drops on Retail Sales Miss

Dollar is making a modest recovery in early US session, supported by slightly better-than-expected durable goods orders and recovery in benchmark Treasury yields. However, the overarching direction of the greenback for the near term remains uncertain, largely dependent on shifting risk sentiments. Current stock futures are showing mixed opening, leaving investors watching closely to see how these dynamics unfold throughout the trading day.

In the broader currency market, Australian Dollar and New Zealand Dollar are leading as the strongest performers for the day. Aussie particularly buoyed by stronger than expected CPI data, which are likely to push back the timetable for any rate cuts by RBA. Conversely, Canadian dollar is currently the weakest performer, following disappointing retail sales data, indicating softer consumer spending. Swiss Franc and Euro are also underperforming, while Japanese Yen and British Pound hold middle ground.

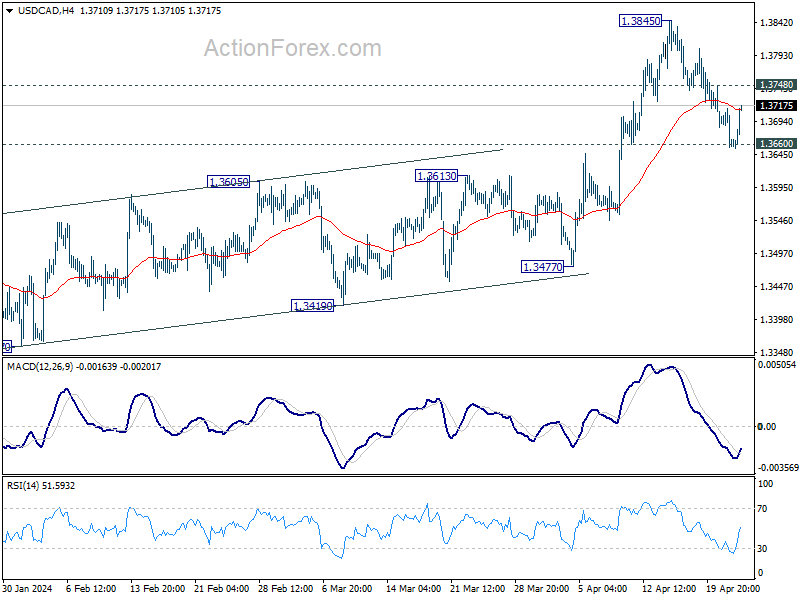

Technically, USD/CAD's recovery suggests that 1.3660 support is defended for now. Near term bullishness is retained. Break of 1.3748 minor resistance will bring stronger rally back to retest 1.3845. Further break there will resume larger rally from 1.3716.

In Europe, at the time of writing, FTSE is up 0.48%. DAX is up 0.15%. CAC is up 0.46%. UK 10-year yield is up 0.0921 at 4.337. Germany 10-year yield is up 0.066 at 2.575. Earlier in Asia, Nikkei rose 2.42%. Hong Kong HSI rose 2.21%. China Shanghai SSE rose 0.76%. Singapore Strait Times rose 0.62%. Japan 10-year JGB yield rose 0.0045 to 0.891.

US durable goods orders rises 2.6% mom in Mar, ex-transport orders up 0.2% mom

US durable goods orders rose 2.6% mom to USD 283.4B in March, above expectation of 2.5% mom. Ex-transport orders rose 0.2% mom to USD 187.5B, below expectation of 0.3% mom. Ex-defense orders rose 2.3% mom to USD 268.1B, above expectation of 2.0% mom. Transportation equipment orders rose 7.7% to USD 95.9B.

Canada's retail sales down -0.1% mom in Feb

Canada's retail sales fell -0.1% mom to CAD 66.7B in February, worse than expectation of 0.1% mom rise. Sales were down in five of nine subsectors and were led by decreases at gasoline stations and fuel vendors (-2.2% mom).

Core retail sales, which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers, were unchanged for the month.

Advance estimate indicates that retail sales was unchanged in March.

German Ifo business climate rises to 89.4, economy stabilizing thanks to service providers

German Ifo Business Climate rose from 87.8 to 89.4 in April, above expectation of 88.5. Current Assessment Index rose from 88.1 to 88.9, above expectation of 88.7. Expectations Index also improved from 87.5 to 89.9, above expectation of 88.9.

By sector, manufacturing rose from -9.9 to -8.5. Services rose from 0.4 to 3.2. Trade rose from -22.9 to -22.0. Construction rose from -33.2 to -28.5.

If said, "Companies were more satisfied with their current business. Their expectations also brightened. The economy is stabilizing, especially thanks to service providers."

ECB's Nagel cautions: June rate cut may not lead to further easing

At a conference today, Joachim Nagel, Bundesbank President and ECB Governing Council member, said that if data in the next six weeks bolster confidence in achieving ECB's 2% inflation target, he would support a reduction in interest rates in June. However, he emphasized that "such a step would not necessarily be followed by a series of rate cuts."

He stressed the current climate of uncertainty, noting, "Given the current uncertainty, we cannot pre-commit to a particular rate path." This approach underscores ECB's strategy of making decisions "meeting by meeting and based on incoming data."

Further, Nagel admitted of his reservations and expressed that he is "not fully convinced yet" that price growth is firmly on a path toward target. Core inflation, particularly within the services sector, remains elevated, driven by persistent strong wage growth, which tends to be more durable than goods inflation.

Nevertheless, by June "we will know a lot more," about the inflation path, he added.

Australia CPI slows less than expected in Q1, accelerates in Mar

In Q1, Australia's CPI slowed from 4.1% yoy to 3.6% yoy, exceeding market expectations of 3.4% yoy. Similarly, trimmed mean CPI, which excludes volatile price items and provides a clearer view of underlying inflation trends, also decelerated less than expected, moving from 4.2% yoy to 4.0% yoy, against predictions of 3.8% yoy.

The breakdown by category shows a general slowdown across the board. Goods inflation decreased from 3.8% yoy to 3.1% yoy, while services inflation eased from 4.6% yoy to 4.3% yoy. Tradeable inflation, which includes items that can be imported or exported, slowed more significantly from 1.5% yoy to 0.9% yoy. Non-tradeable inflation, representing goods and services not exposed to international markets, also saw a reduction from 5.4% yoy to 5.0% yoy.

However, on a quarterly basis, CPI rose by 1.0% qoq in Q1, marking an acceleration from the previous quarter's 0.6% qoq and outpacing expectations of a 0.8% rise. This quarterly increase suggests that, despite the annual slowdown, price pressures within the economy intensified at the start of the year. Trimmed mean CPI on a quarterly basis mirrored this trend, rising 1.0% qoq compared to the previous 0.8% qoq, also surpassing the expected 0.8% qoq.

Monthly figures reinforce the notion of persistent inflationary pressures, with CPI ticking up from 3.4% yoy to 3.5% yoy, again exceeding expectations.

New Zealand's goods exports rises 3.8% yoy in Mar, imports fell -25% yoy

New Zealand's goods exports rose 3.8% yoy to NZD 6.5B in March. Goods imports fell -25% yoy to NZD 5.9B. Monthly trade balance was a surplus of NZD 588m, versus expectation of NZD -505m deficit.

Exports to US and EU showed increases of 8.0% yoy and 3.6% yoy respectively. However, exports to major trading partners like China (-1.9% yoy), Australia (-3.7% yoy), and Japan (-15% yoy) declined.

On the import side, there were significant reductions across all major partners. Imports from EU saw the sharpest decline at -43% yoy, followed closely by US at -42% yoy. Imports from China, Australia, and South Korea were down -20% yoy, -13% yoy, and -21% yoy respectively.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0656; (P) 1.0684; (R1) 1.0729; More...

EUR/USD is still bounded in range trading above 1.0601 and intraday bias remains neutral. Strong resistance should be seen from 1.0723 to complete the corrective rise from 1.0601. Break of 1.0601 will resume the fall from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. Nevertheless, firm break of 1.0723 will bring stronger rebound to 55 D EMA (now at 1.0786) instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 588M | -505M | -218M | -315M |

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 2.30% | 2.10% | 2.10% | 2.20% |

| 01:30 | AUD | Monthly CPI Y/Y Mar | 3.50% | 3.40% | 3.40% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.00% | 0.80% | 0.60% | |

| 01:30 | AUD | CPI Y/Y Q1 | 3.60% | 3.40% | 4.10% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.00% | 0.80% | 0.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 4.00% | 3.80% | 4.20% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | 17.6 | 11.5 | ||

| 08:00 | EUR | Germany IFO Business Climate Apr | 89.4 | 88.5 | 87.8 | |

| 08:00 | EUR | Germany IFO Current Assessment Apr | 88.9 | 88.7 | 88.1 | |

| 08:00 | EUR | Germany IFO Expectations Apr | 89.9 | 88.9 | 87.5 | |

| 12:30 | USD | Durable Goods Orders Mar | 2.60% | 2.50% | 1.30% | |

| 12:30 | USD | Durable Goods Orders ex Transportation Mar | 0.20% | 0.30% | 0.50% | |

| 12:30 | USD | Durable Goods Orders ex Defense Mar | 2.30% | 2.00% | 2.20% | |

| 12:30 | CAD | Retail Sales M/M Feb | -0.10% | 0.10% | -0.30% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | -0.30% | 0.00% | 0.50% | 0.40% |

| 14:30 | USD | Crude Oil Inventories | 1.7M | 2.7M | ||

| 17:30 | CAD | BoC Summary of Deliberations |

US durable goods orders rises 2.6% mom in Mar, ex-transport orders up 0.2% mom

US durable goods orders rose 2.6% mom to USD 283.4B in March, above expectation of 2.5% mom. Ex-transport orders rose 0.2% mom to USD 187.5B, below expectation of 0.3% mom. Ex-defense orders rose 2.3% mom to USD 268.1B, above expectation of 2.0% mom. Transportation equipment orders rose 7.7% to USD 95.9B.