Sample Category Title

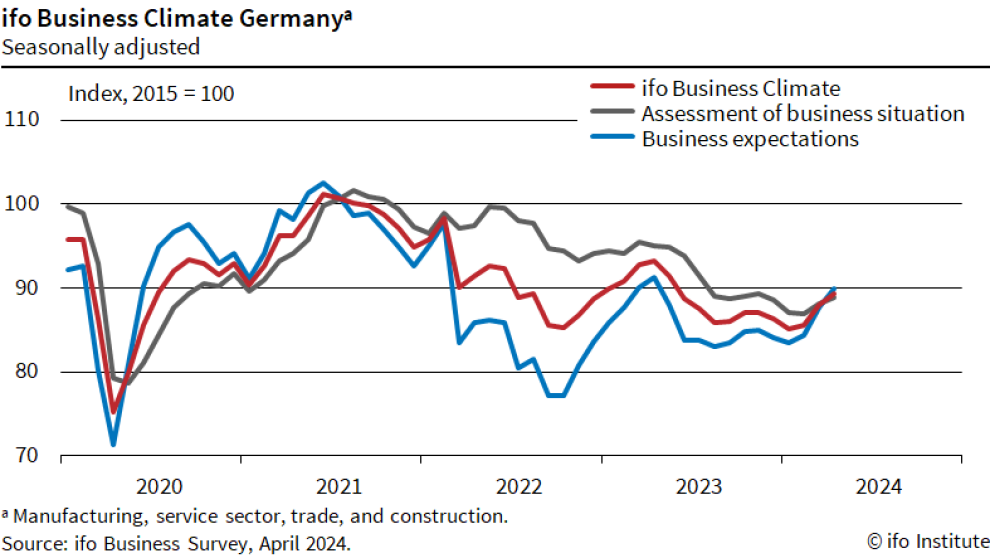

German Ifo business climate rises to 89.4, economy stabilizing thanks to service providers

German Ifo Business Climate rose from 87.8 to 89.4 in April, above expectation of 88.5. Current Assessment Index rose from 88.1 to 88.9, above expectation of 88.7. Expectations Index also improved from 87.5 to 89.9, above expectation of 88.9.

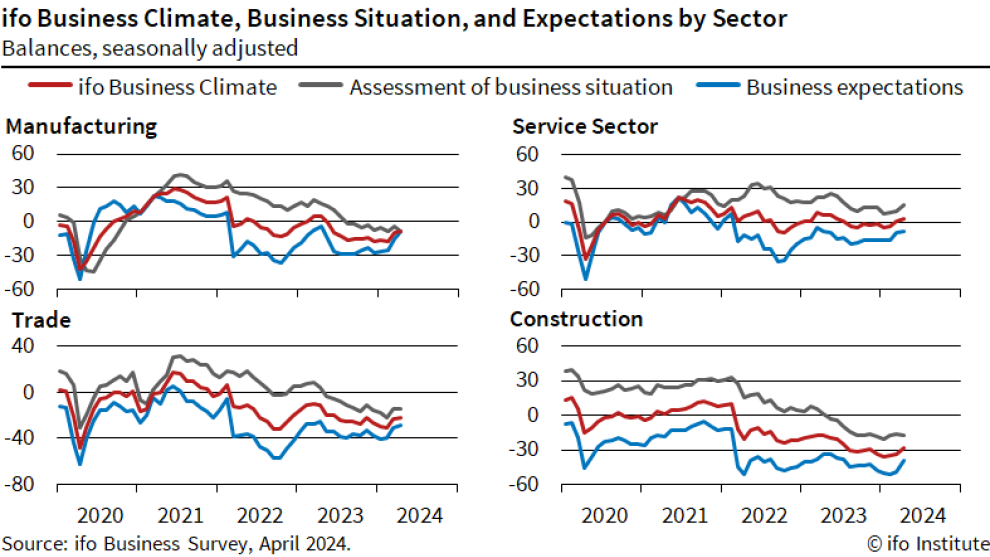

By sector, manufacturing rose from -9.9 to -8.5. Services rose from 0.4 to 3.2. Trade rose from -22.9 to -22.0. Construction rose from -33.2 to -28.5.

If said, "Companies were more satisfied with their current business. Their expectations also brightened. The economy is stabilizing, especially thanks to service providers."

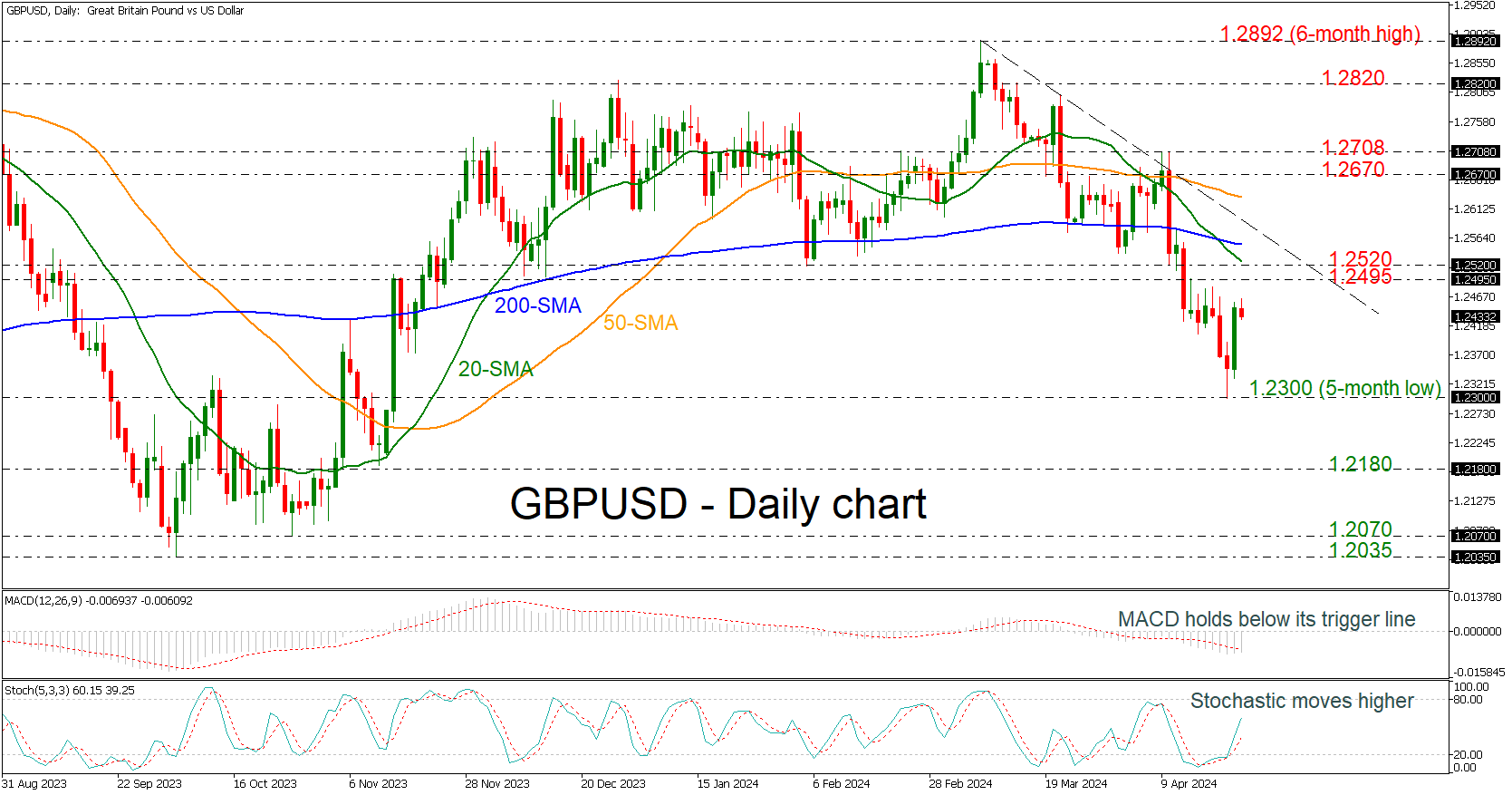

GBPUSD Bounces Off 1.2300 But Remains at Risk

- GBPUSD posts new 5-month low

- Price holds in bearish tendency

- MACD and stochastics suggest upside move

GBPUSD is recovering from the five-month low of 1.2300 that was posted on Monday and is heading towards the restrictive region of 1.2495-1.2520. The pair has started a bearish tendency since the price peaked at 1.2892 in the short-term timeframe.

According to technical oscillators, the MACD is trying to cross its trigger line to the upside beneath the zero level. Also, the stochastic oscillator is moving strongly higher following the rebound off the oversold territory.

If traders continue to buy the pair, then the price could meet the aforementioned region and the 20-day simple moving average (SMA) around 1.2520. Slightly higher, the 200-day SMA at 1.2555 and the near-term descending trend line at 1.2585 may block the upside movement.

On the other hand, a move lower again could retest the previous trough of 1.2300 before tumbling further towards the 1.2180 bottom, registered on November 10.

In a nutshell, GBPUSD is in a bearish mode in the short-term picture as it is standing beneath the downtrend line and the SMAs.

ECB’s Nagel cautions: June rate cut may not lead to further easing

At a conference today, Joachim Nagel, Bundesbank President and ECB Governing Council member, said that if data in the next six weeks bolster confidence in achieving ECB’s 2% inflation target, he would support a reduction in interest rates in June. However, he emphasized that "such a step would not necessarily be followed by a series of rate cuts.”

He stressed the current climate of uncertainty, noting, "Given the current uncertainty, we cannot pre-commit to a particular rate path." This approach underscores ECB's strategy of making decisions "meeting by meeting and based on incoming data."

Further, Nagel admitted of his reservations and expressed that he is "not fully convinced yet" that price growth is firmly on a path toward target. Core inflation, particularly within the services sector, remains elevated, driven by persistent strong wage growth, which tends to be more durable than goods inflation.

Nevertheless, by June "we will know a lot more," about the inflation path, he added.

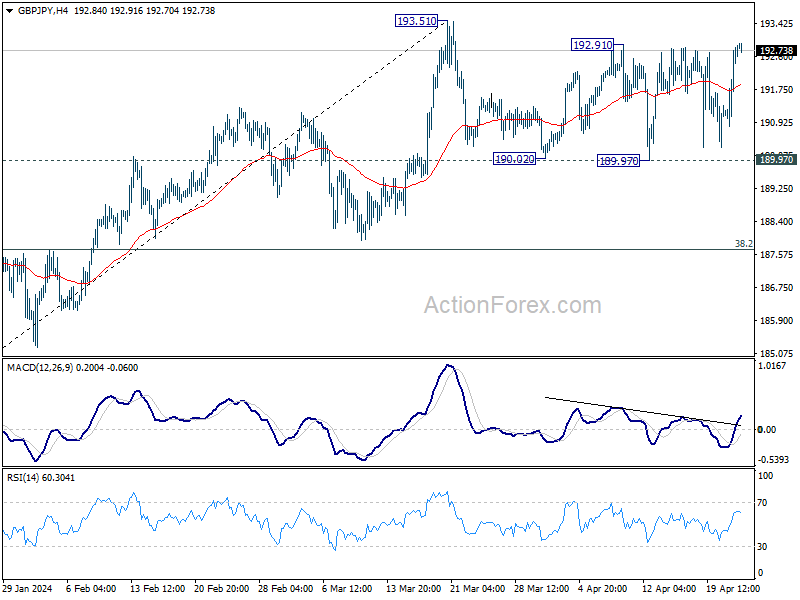

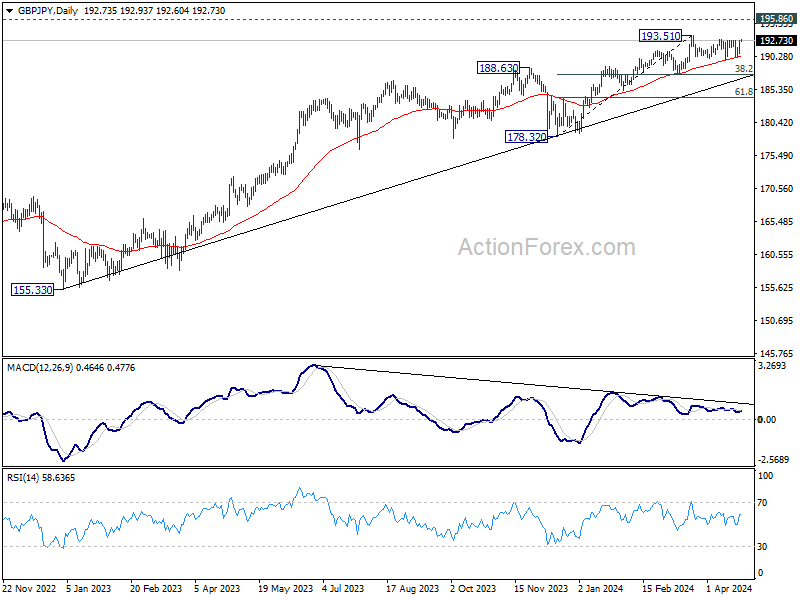

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.45; (P) 192.15; (R1) 193.47; More..

GBP/JPY is still bounded in range below 193.51 and intraday bias remains neutral. Further rally is expected with 189.97 support intact. On the upside, firm break of 193.51 will resume larger up trend to 195.86 long term resistance. Nevertheless, decisive break of 189.97 will indicate that it's at least correcting the rise from 178.32, and target 38.2% retracement of 178.32 to 193.51 at 187.70.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break of 187.94 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

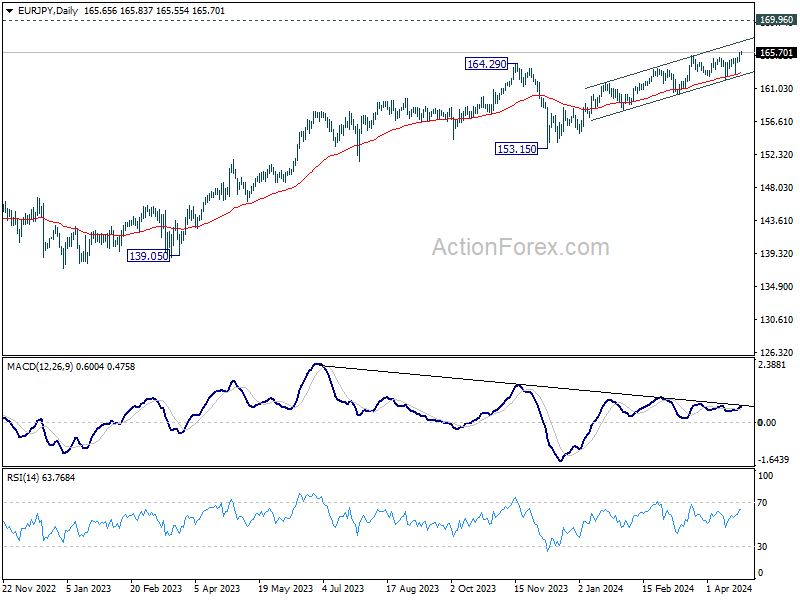

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.98; (P) 165.36; (R1) 166.09; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Current up trend should target 169.96 key resistance next. On the downside, break of 164.39 minor support will turn intraday bias neutral again first. But outlook will continue to stay bullish as long as 162.26 support holds, in case of retreat.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

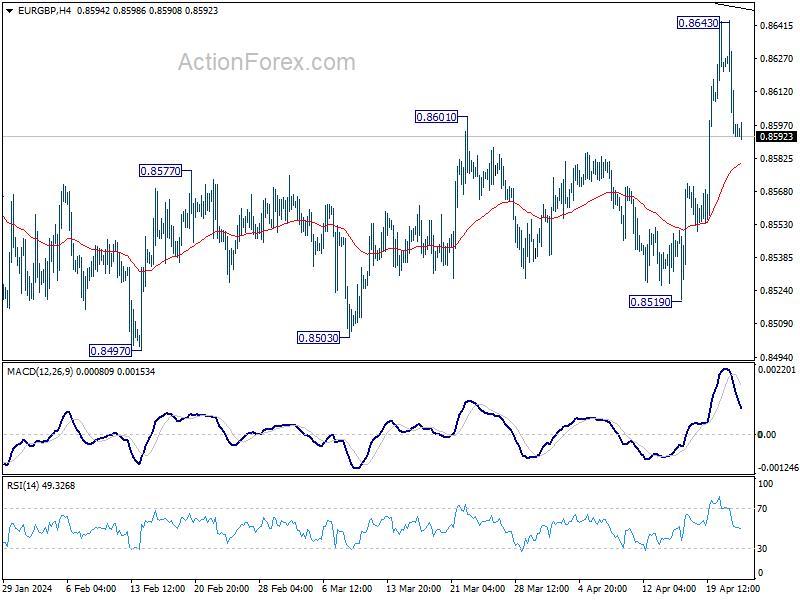

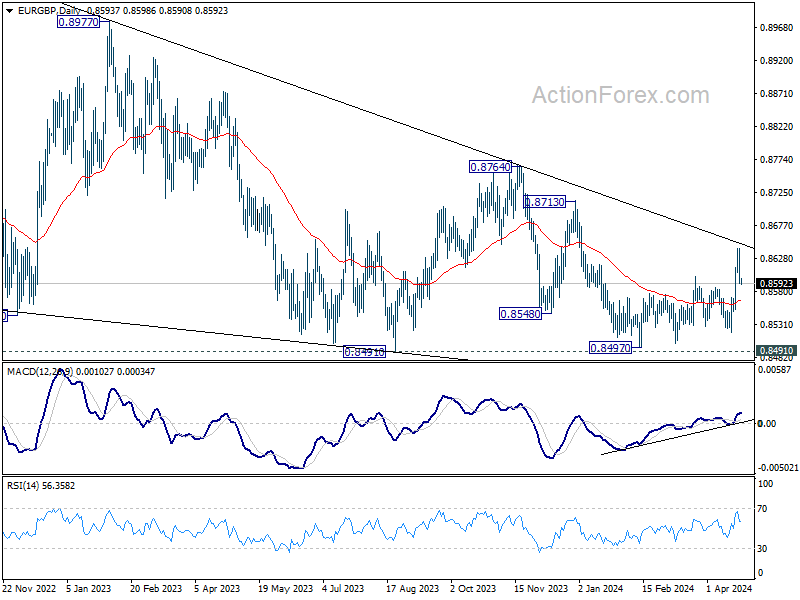

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8578; (P) 0.8611; (R1) 0.8630; More...

Intraday bias in EUR/GBP is turned neutral first with current retreat. On the upside, decisive break of medium term trend line resistance (now at 0.8649) will solidify the bullish case of trend reversal, and target 0.8764 resistance next. However, sustained break of 55 4H EMA (now at 0.8580) will indicate rejection by the trend line, and bring retest of 0.8491/7 support zone instead.

In the bigger picture, outlook is mixed up by current strong rebound. On the upside, sustained break of the trend medium term trend resistance will argue that the down trend from 0.9267 (2022 high) has completed as a triangle pattern. Further rise should then be seen through 0.8764 resistance next. However, rejection by the trend line will retain medium term bearishness for another fall through 0.8491 at a later stage.

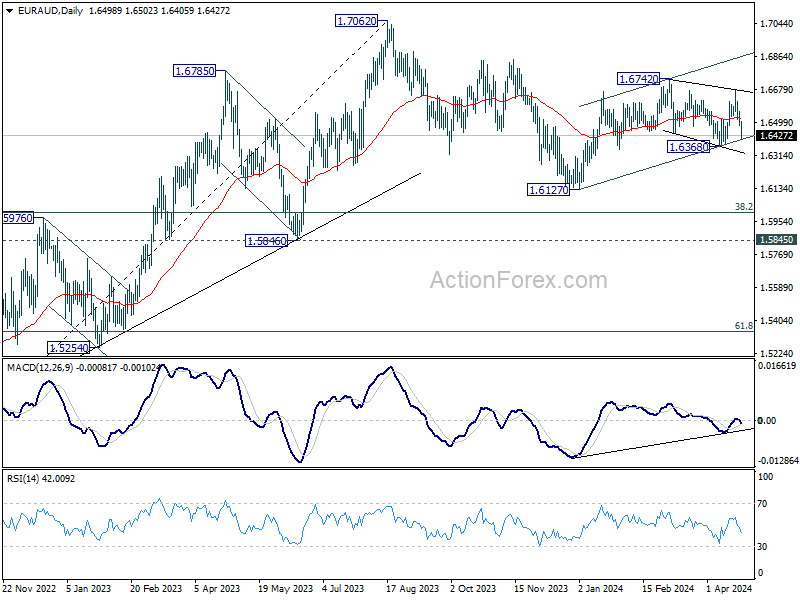

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6468; (P) 1.6516; (R1) 1.6545; More...

Outlook is mixed up by deeper than expected fall from 1.6679. On the downside, firm break of 1.6368 support will revive that case that rebound from 1.6127 has completed at 1.6742. Fall from there is seen as the third leg of the pattern from 1.7062. Deeper decline would then be seen to 1.6127 support and below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of another fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

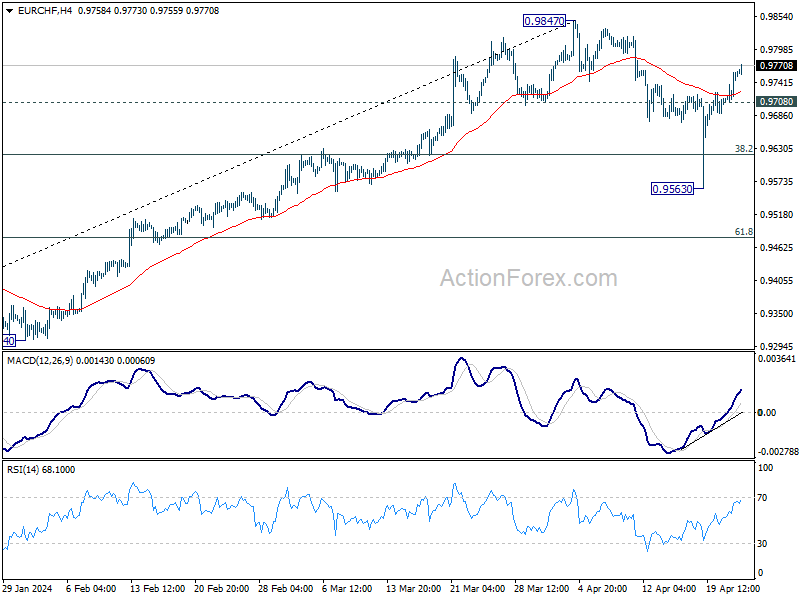

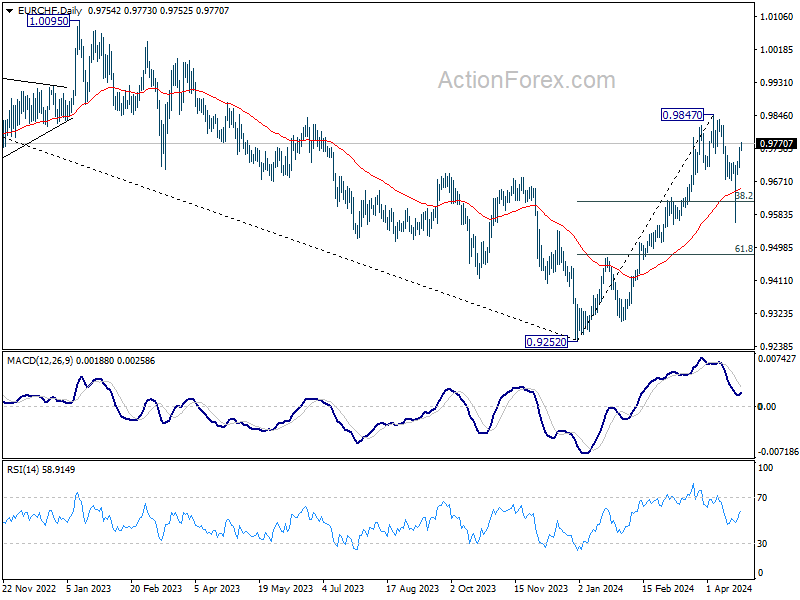

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9722; (P) 0.9741; (R1) 0.9780; More...

The strong break of 55 4H EMA suggest that EUR/CHF's pull back from 0.9847 has completed at 0.9563 already. Intraday bias is back on the upside for retesting 0.9847 high. Decisive break there will resume larger rally from 0.9252. On the downside, below 0.9708 minor support will turn intraday bias neutral again first.

In the bigger picture, while 55 D EMA (now at 0.9655) was breached, EUR/CHF rebounded strongly since then. Rise from 0.9252 medium term bottom should still be in progress. Break of 0.9847 will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. however, sustained trading below 55 D EMA will argue that the rebound has completed.

Stubbornly High Inflation Doesn’t Allow RBA to Cut Interest Rates Anytime Soon

Markets

Disappointing April US PMI’s triggered some short covering in US Treasuries. The composite PMI declined from 52.1 to 50.9 (vs 52 consensus) with both manufacturing (49.9 from 51.9) and services (50.9 from 51.7) contributing. Details showed inflows for new business falling for the first time in six months and firms’ future output expectation slipping to a 5-month low. Both suggest that the US economy could lose some further momentum in the second quarter of the year. Companies cut payrolls numbers (48.5 from 51.2) at the fastest pace since May 2020. Weaker demand and a less tight labour market fed through to an easing in rates of increase of selling prices. Details show dynamics of inflation changing from wage-related services-led price pressures to intensifying factory cost pressures (higher raw material and energy). Markets went into yesterday’s PMI’s following a string of strong activity/labour market data and higher CPI releases. This context made markets vulnerable to some milder positioning going into next week’s FOMC meeting. We don’t expect PMI’s to be trend-reversers though. Daily changes on the US yield curve eventually varied between -3.9 bps (2-yr) and +1.4 bps (30-yr) with yields closing off intraday lows. European bonds yesterday underperformed following consensus-beating PMI’s. The context was obviously different with Europe coming from a period of weakness. German yields added 1.5 bps to 2.5 bps. The combination of better EMU and worse US numbers propelled EUR/USD from 1.0639 to 1.0701 with the pair trying to sustainably regain the previous YTD low at 1.0694. Sterling was yesterday’s outperformer in FX space as BoE chief economist offered some counter weight to recent soft comments by BoE Baily and Ramsden, suggesting that the MPC is currently split on how long policy rates should remain at their current peak levels. EUR/GBP returned below 0.86. Today’s eco calendar contains German Ifo business climate, US durable goods orders, a record-volume $70bn 5-yr Note auction and an avalanche of Q1 earnings. After yesterday, we expect the yields and the dollar to temporarily lose some momentum.

News & Views

The National bank of Hungary (MNB) yesterday slowed the pace of rate cuts. The base rate was reduced by 50 bps to 7.75% compared to a 75 bps reduction in March. The MNB sees persistently moderating inflation. Rising real wage growth and strengthening confidence support a gradual economic recovery, mainly driven by domestic demand. (2-3% growth this year). Headline CPI inflation fell within the MNB’s tolerance band (3.6% Y/Y in March). Core inflation remained higher at 4.4%, but in line with the MNB March projection. The MNB expects the pace of price increases to rise temporarily in the middle of this year. The decline in core inflation might stop in Q2 and is expected to fluctuate between 4.5% and 5% in the remainder of the year. Financial stability considerations remain important in the MNB’s policy assessment. High FX reserves and the persistent improvement in the current account balance have contributed to the strengthening of the country's risk perception. Still, the risk premium on Hungarian assets has risen recently in a deteriorating international sentiment. The outlook for inflation combined with a volatile risk environment warrant a carful, patient approach to monetary policy, resulting in a slower pace or rate reductions than was the case earlier. KBC expects two additional 50 bps rate cuts in May and June, before a further slowdown of easing in H2. The forint yesterday gains modestly to close the session near EUR/HUF 393.

Australian Q1 CPI printed at 1.0% Q/Q and 3.6% Y/Y, compared to 0.6% Q/Q and 4.1% Y/Y in the final quarter of last year. The outcome disappointed expectations for a faster disinflation. Also underlying measures of inflation (trimmed mean 1.0% Q/Q and 4.0% Y/Y) printed higher than expected. In a quarterly perspective, price increases for food (+0.9%), housing (+0.7%), health (2.8%) and education (+5.9), contributed to the rise. Prices for clothing and footwear declined 1.1% Q/Q. Good prices were up 0.5% Q/Q, but services inflation still printed at a strong 1.4% Q/Q. Both headline and core (trimmed mean) inflation stay well above the RBA’s 2-3% target band. Stubbornly high inflation, especially for the likes of services/non-tradeable goods, doesn’t allow the RBA to cut interest rates anytime soon. Australian yields jumped higher this morning with the 3-y government bond yield adding 17 bps (to 4.01%). Markets now see only a small chance (< 30%) for a fist rate cut by the end of the year. The prospect for protracted interest rate support also propelled the Aussie dollar with AUD/USD regaining the 0.65 mark (0.652).

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June?) rate cut and seems to have broad backing. EMU disinflation will continue the next two months and bring headline CPI (temporary) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up move difficult.

US 10y yield

The March dot plot contained several hawkish elements including a symbolically higher neutral rate. In our view they set the stage for a later (September at the earliest) start of a possibly shallower cutting cycle. Upcoming CPI readings (through base effects) and resilient eco data should confirm this. US yields continue to enjoy a solid bottom across the maturity spectrum, setting fresh YTD highs.

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a technical break, opening the path to last year’s low at 1.0494.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

Elliott Wave Calling for FTSE to Extend Higher

Short Term Elliott Wave view on FTSE suggests that rally from 8.18.2023 low is unfolding as a 5 waves impulse. Up from 8.18.2023 low, wave 1 ended at 7745.82 and pullback in wave 2 ended at 7279.86. Up from there, wave ((i)) ended at 7764.37 and wave ((ii)) pullback ended at 7404.08. The Index then extended higher in wave ((iii)) towards 8015.63 as the 1 hour chart below shows. Wave ((iv)) pullback ended at 7882.68 and wave ((v)) ended at 8044.98. This completed wave 3 in higher degree.

Pullback in wave 4 took the form of Elliott Wave zigzag structure. Down from wave 3, wave ((a)) ended at 7952.12 and wave ((b)) rally ended at 8009.52. Final leg wave ((c)) lower ended at 7791.84 which completed wave 4. The Index has resumed higher again in wave 5. Up from wave 4, wave (i) ended at 7898.77 and wave (ii) ended at 7809.68. Wave (iii) higher ended at 8076.52 and pullback in wave (iv) ended at 8021.67. Expect the Index to extend higher in wave (v) of ((i)). It then should pullback in wave ((ii)) to correct cycle from 4.16.2024 low before it resumes higher. Near term, as far as pivot at 7791.84 low stays intact, expect dips to find buyers in 3, 7, or 11 swing for further upside.

FTSE 60 Minutes Elliott Wave Chart

FTSE Elliott Wave Video

https://www.youtube.com/watch?v=s6h2GOlKgo0