Sample Category Title

Tesla Jumps Despite Earnings Miss

Tesla’s Q1 results didn’t look good at all. The revenue dropped 9% - the first revenue drop in four years - and net income plunged by 55% compared to the same time last year. And these numbers were not only bad, but they were also worse than the expectations for the 3rd straight month. Yet investors looked past the ugly quarterly results from Tesla and sent the stock price 13% higher in the afterhours trading – yes there is no mistake, Tesla jumped 13% after announcing a revenue and earnings miss, as investors focused on plans to accelerate the launch of new models that include cheaper models. The post-earnings jump could be a flash in the pan given rising challenges the company faces.

Elsewhere, Apple eked out a small gain despite news that iPhone sales in China fell 19% in Q1 while Huawei’s rose almost 70%. Texas Instruments rose on a bullish revenue forecast for the current quarter hinting at a slower decline in chip demand from industrials and car industry. Spotify rallied 11% after its CFO said that ‘historical price increases have had minimal impacts on growth’ a few weeks after revealing plans to increase prices later this year. GM raised its 2024 profit outlook and Visa’s profit surged amid higher credit card spending. Meta, Ford and IBM will report today.

Overall, there was nothing worrying in company news yesterday, and even the bad news saw a positive market reaction, partly due to a decline in US yields yesterday following a set of lower than expected PMI figures from the S&P Global and a strong sale of 2-year treasury notes. According to the S&P’s survey, the expansion in US services was unexpectedly slower than expected in April, while manufacturing PMI slipped below 50, into contraction, whereas analysts had penciled a faster expansion. The dollar index fell as a reaction, and the greenback’s major peers strengthened.

Note that the EURUSD was already up before the release of the US PMI numbers yesterday, as the PMI data released in Europe revealed a surprise rise in German and French services; the German services expanded fast enough to push the composite PMI into the expansion zone. German manufacturing – which is the country’s main strength – came in weaker than expected, yet the better-than-expected Eurozone PMI combined with the worse-than-expected US PMI sent the EURUSD above the 1.07 level. We will be watching the German sentiment index, the 10-year bund auction, the US durable goods orders and the 5-year note auction today.

In Japan, the yen strengthened a little bid yesterday but the gains remained limited after news that the Bank of Japan (BoJ) will focus on the falling yen when it meets this week. But the yen’s medium-term bearish trajectory will be hard to reverse unless the BoJ gives hints of further rate increases in the foreseeable future. In Australia, the AUDUSD extended a rally to the 200-DMA after the inflation data came in stronger-than-expected and fueled the Reserve Bank of Australia (RBA) hawks. Trend and momentum indicators are about to turn positive, but the dollar’s weakness is subject to important risks this week as the Q1 GDP update and the core PCE index could easily reverse the recent weakness and send the dollar soaring again, on melting rate cut bets for the Federal Reserve (Fed).

Equities

News of improved activity boosted appetite in the Stoxx 600 ahead of closely watched bank earnings in the next few days. The European banks have been performing very well as high European Central Bank (ECB) rates boost earnings expectations and high capital returns attract investors. The severe retreat in ECB rate cut bets should continue to back optimism, but the banks should deliver to keep the rally going.

In the UK, the British FTSE 100 advanced to an all-time high and is expected to further benefit from the developing reflation trade that should back mining and energy stocks.

In the US, the lower US yields helped the S&P500 rebound yesterday. Technology stocks led gains but there are mixed views regarding the future of the US stock rally. Earnings expectations for the mega tech stocks are very high, and the market reaction could be unpredictable as forecasts matter at least as much as earnings and revenue prints.

In commodities, US crude jumped to $84pb as yesterday’s API report printed a 3-mio-barrel decline in weekly inventories, while gold rebounded after tipping a toe below the $2300 per ounce, in a move that’s reportedly caused by margin calls.

US PMIs, AUD Inflation and Tesla Impact Markets

In focus today

In Germany we await Ifo data for April. The current assessment of the economy remains weak, but expectations have risen lately so it will be important to follow if we finally see a turn in the assessment of the current activity.

Economic and market news

What happened overnight

In Australia, the Q1 inflation print came in higher than expected at 1.0% m/m (cons: 0.8%) and 3.6% y/y (cons: 3.5%), due to service price pressures remaining to the high side. For March alone inflation increased slightly to 3.5% against 3.4% in February. The markets now price in very low probability of a rate cut in August. AUD rates rose upon release and AUD/USD has strengthened modestly. Notably USD rates also rose around 1bp following the release with markets speculating in possible common denominators.

What happened yesterday

In the US, and as widely expected, the Senate passed the USD 95 billion bill which provides military aid for Ukraine, Israel and Taiwan. The bill came to a vote after the house passed the same bill on Saturday. House speaker Mike Johnson suddenly switched course last week after not letting the House vote about the bill for nearly two months.

The US PMIs surprised to the downside in both manufacturing and services driving a considerable move lower in USD yields. Composite PMI landed at 50.9 down from 52.1 in March. There was a notable decline in services output prices index (54.0; from 56.4), snapping the recent rising trend.

Tesla shares jumped after the US close - ending a 7-day streak of declines - as Tesla presented Q1 earnings and a plan to accelerate launch of more affordable cars. With markets closely monitoring earnings reports of especially tech-companies in the US the rise in Tesla spread to the rest of the tech cluster.

The euro area composite PMI rose more than expected to 51.4 (cons: 50.7, prior: 50.3) in April which suggests that the economy is now back in growth territory for the second consecutive month. The economy is driving at two speeds as the service PMIs rose to 52.9 (cons: 51.8, prior: 51.5) in an upward surprise while manufacturing PMI unexpectedly declined to 45.6 (cons: 46.5, prior: 46.1). The output price index in the service sector increased marginally to 55.1 from 55.7. The changes in service output prices have recently been a good indicator of the monthly change in core inflation.

In Sweden, Riksbank governor Thedéen spoke yesterday where he signalled that he has not made up his mind about when we the Riksbank will deliver the first rate cut. He said that before our next interest rate decision in two weeks' time, we need to analyse what the clearly lower inflation means for inflation in the longer term and weigh up the risks of inflation rising again." The lower inflation is positive for the Riksbank, but May is not a done deal.

In the UK, Bank of England's Pill talked with caution on impending rate cuts. He is one of the internal members who has voted with the majority for the entire cycle. Pill said little of news and the passage of time have brought a cut somewhat closer but also that a cut "remains some way off" and there is still "some way to go" before he is convinced of a sustainable return to target. EUR/GBP ended yesterday lower. Comments and data the past week suggest that a May cut is highly unlikely. We think June is still in play with both two inflation prints and two job reports before then set to convince the BoE of a more sustainable easing in inflation pressures. UK PMI's surprise to the topside. Composite at 54.0 (cons: 52.6, prior: 52.8), services at 54.9 (cons: 53.0, prior: 53.1), manufacturing at 48.7 (cons: 50.4, prior: 50.3). However, manufacturing back in contractionary territory. Input prices accelerated in April, however there was a moderation in the rate of prices charged inflation in the UK private sector.

In Hungary, the central bank (MNB) cut the key rate by 50 basis points to 7.75% as expected, which remains an EU-high. This marks a step down in terms of the pace of cuts, as previous cuts have been in the interval of 75-100 basis points. Policy guidance indicates a target for the key rate of 6.5-7% by summer, although different board members have stressed that they are in "no rush" to get there. As such, most likely the MNB will continue to cut interest rates at least over the coming meetings, unless the Forint weakens substantially and/or inflation re-accelerates.

Equities: Global equities climbed higher yesterday, pushing the discussion around corrections off the table. We witnessed broad-based gains with momentum, growth, long duration, and lower quality emerging as the significant victors. Special mention must be made of small caps, which did well yesterday and have performed surprisingly well during the yield run-up since early February. The earnings numbers did not change substantially yesterday, if anything they worsened slightly, but the narrative around earnings did. Commentators are now using equity market performance to gauge earnings instead of examining the numbers directly. In the US yesterday, the Dow was up by 0.7%, S&P 500 by 1.2%, Nasdaq by 1.6%, and Russell 2000 by 1.8%. Asian markets are trending higher this morning, led by Japan, South Korea, and Taiwan. Futures in the US and Europe are also up this morning.

FI: European rates ended marginally higher on the day, amid stronger than expected PMI figures out of Europe. Considering the surprising strength the market reaction was rather muted. That said, hawkish comments from BoE's Pill and US PMIs falling short led to some volatility in the afternoon. Generally, the long end underperformed the shorter end. Intra-euro area spreads traded in a tight range. The 10y German Bund yield ended at 2.50%. ECB rate cut expectations for this year was 2bp lower at 76bp.

FX: The USD weakened on the weaker-than-expected US PMI report, pushing EUR/USD above 1.07 for the first time in almost two weeks. Scandies found support in benign risk sentiment, and EUR/SEK is once again trading below 11.60. Stronger-than-expected UK data made EUR/GBP erase some of the past days' gains.

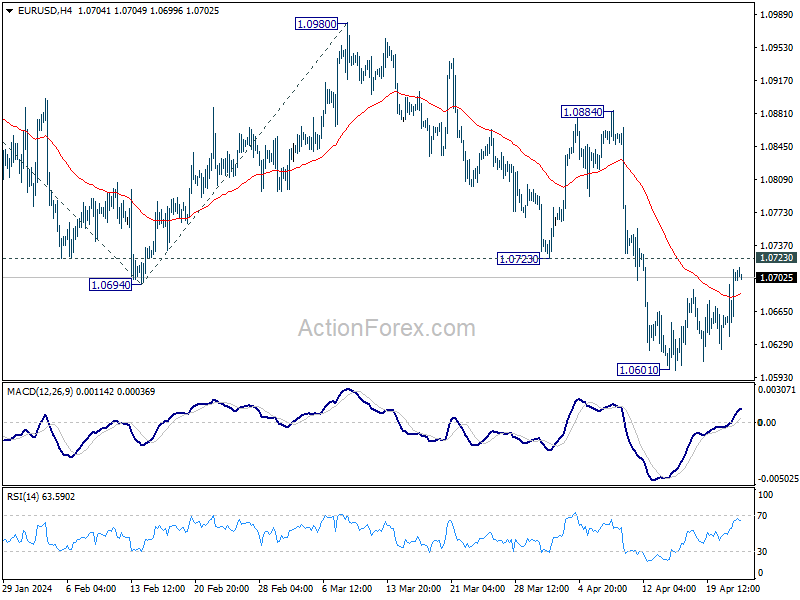

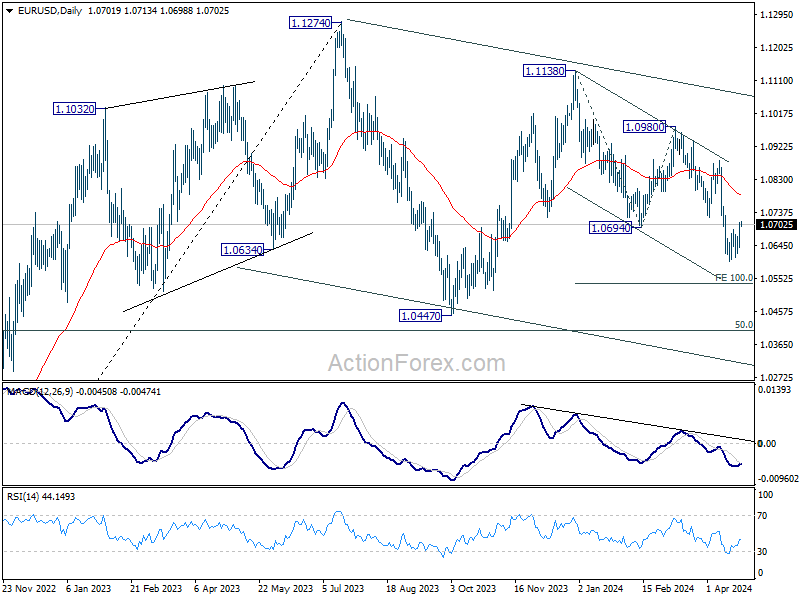

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0656; (P) 1.0684; (R1) 1.0729; More...

Outlook in EUR/USD is unchanged and intraday bias stays neutral first. Strong resistance should be seen from 1.0723 to complete the corrective rise from 1.0601. Break of 1.0601 will resume the fall from 1.1138 to 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536 next. Nevertheless, firm break of 1.0723 will bring stronger rebound to 55 D EMA (now at 1.0786) instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Current fall from 1.1138 is seen as the third leg. While deeper decline is would be seen to 1.0447 and possibly below, Strong support should emerge from 61.8% retracement of 0.9534 to 1.1274 at 1.0199 to complete the correction.

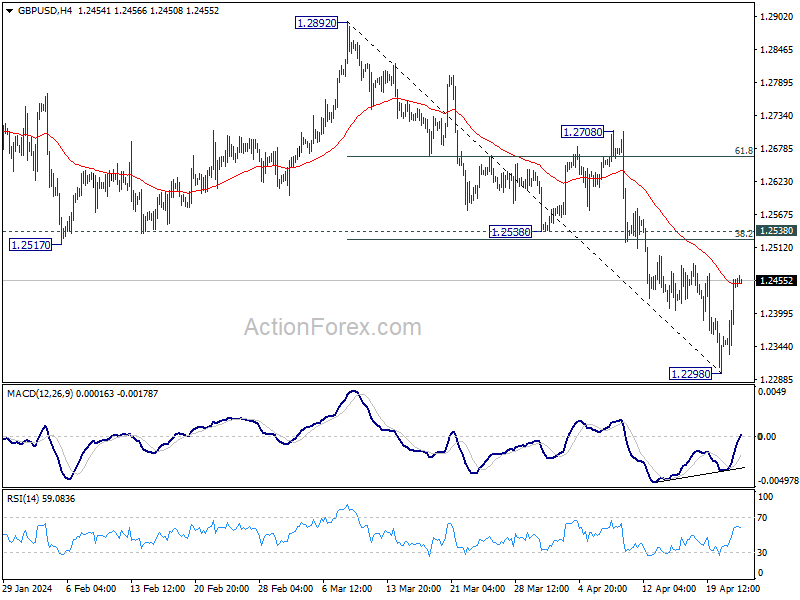

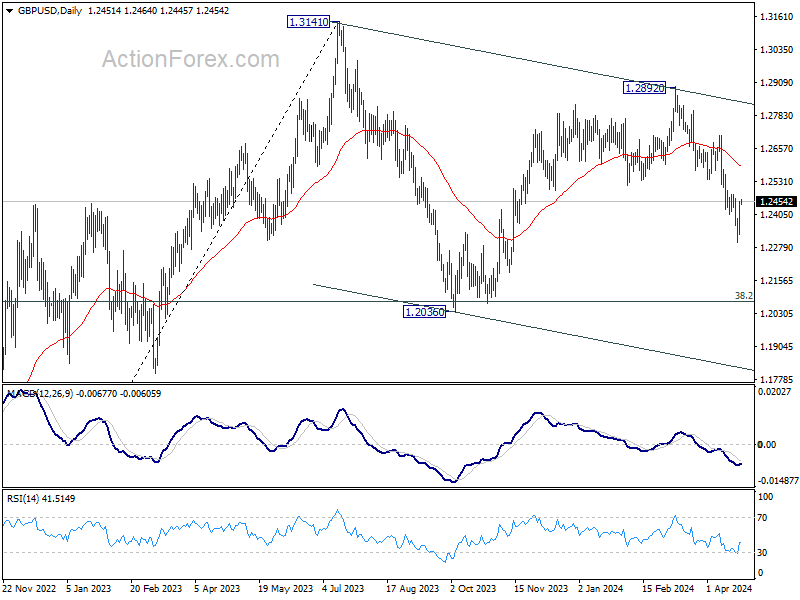

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2368; (P) 1.2414; (R1) 1.2495; More...

Intraday bias in GBP/USD stays neutral at this point. While recovery from 1.2298 might extend higher, upside should be limited by 1.2538 support turned resistance. On the downside, below 1.2298 will resume the fall from 1.2892 to 1.2036 support next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Fall from 1.2892 is seen as the third leg. Deeper decline would be seen to 1.2036 support and possibly below. But strong support should emerge from 61.8% retracement of 1.0351 to 1.2452 at 1.1417 to complete the correction.

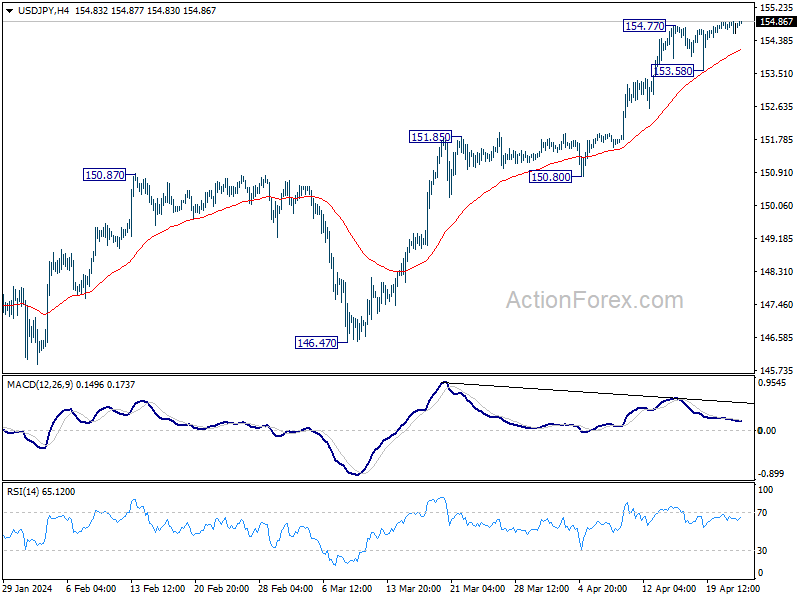

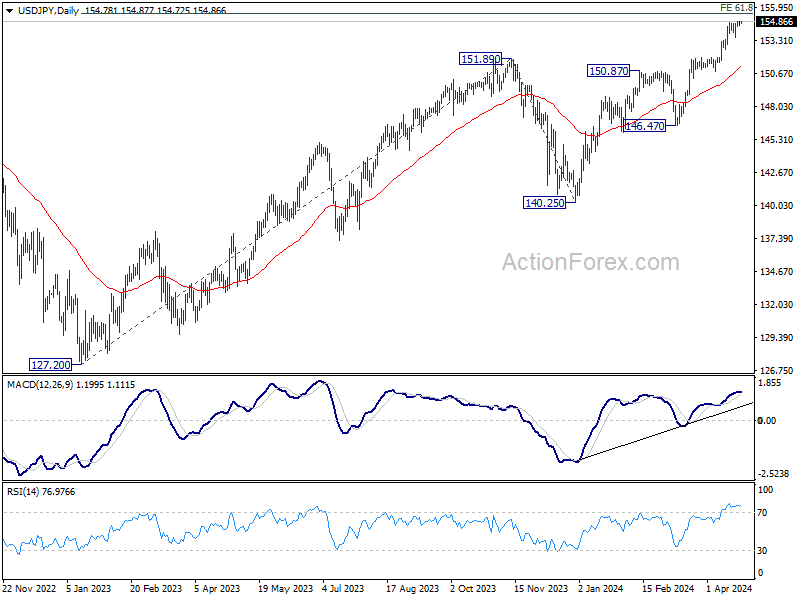

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.63; (P) 154.76; (R1) 154.95; More...

Intraday bias in USD/JPY stays mildly on the upside for further rally. However, considering bearish divergence condition in 4H MACD, strong resistance should be seen from 155.20 fibonacci level to bring correction on first attempt. On the downside, break of 153.58 support will turn bias to the downside, for deeper pull back to 55 D EMA (now at 151.11).

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will remain bullish as long as 146.47 support holds, even in case of deep pullback.

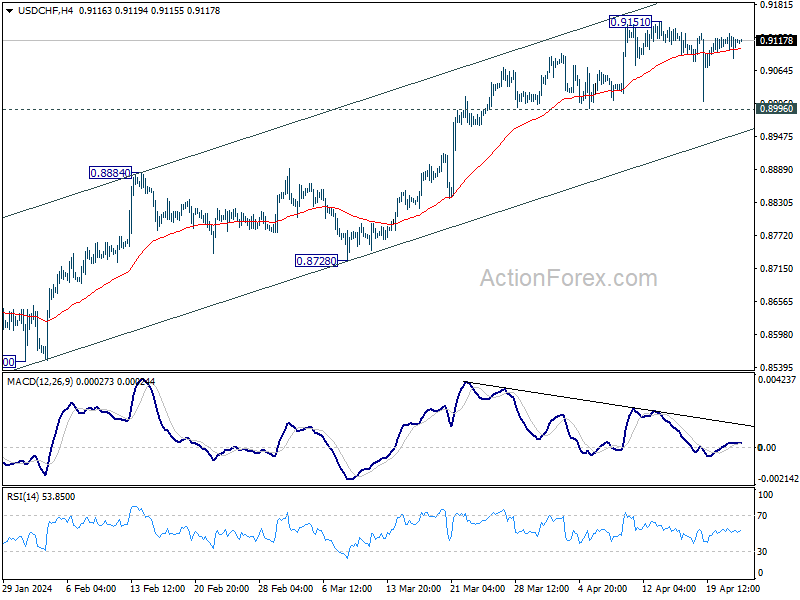

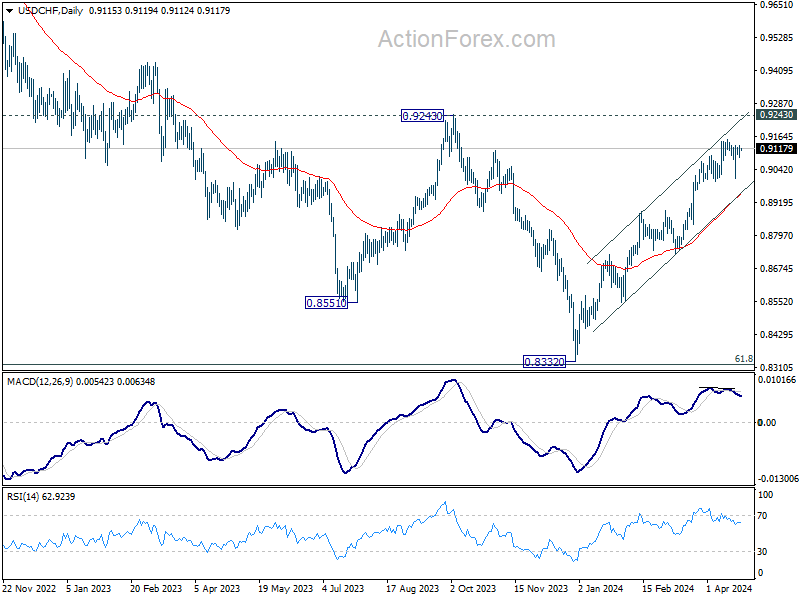

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9093; (P) 0.9113; (R1) 0.9138; More....

No change in USD/CHF's outlook as consolidation form 0.9151 is extending. Intraday bias remains neutral for the moment. Further rally is expected as long as 0.8996 support holds. Break of 0.9151 will resume the larger rise from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will turn bias to the downside for 55 D EMA (now at 0.8953).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

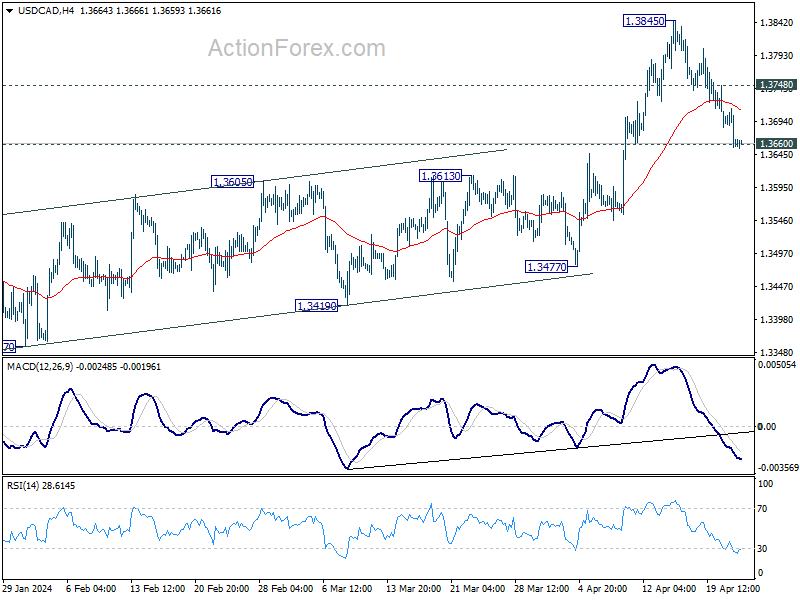

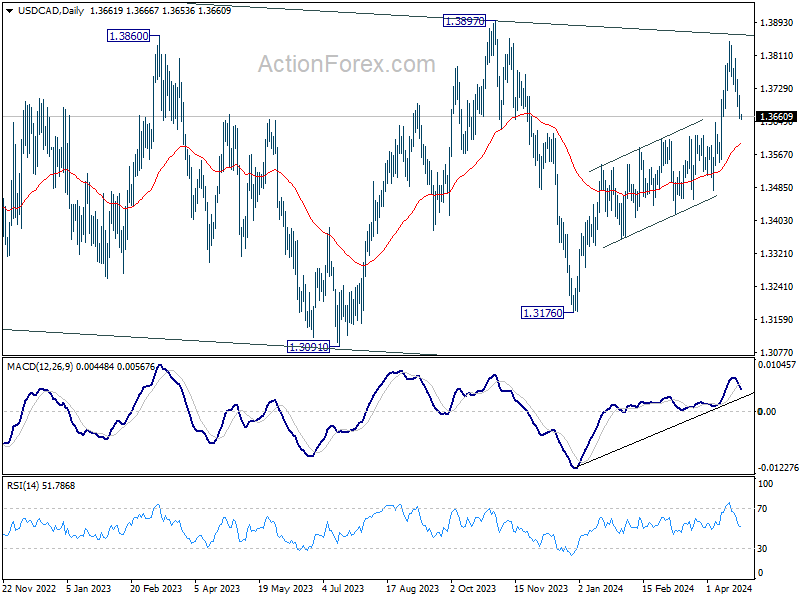

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3640; (P) 1.3679; (R1) 1.3701; More...

Intraday bias in USD/CAD remains neutral for the moment with focus on 1.3660 support. Strong rebound from current level will retain near term bullishness. Break of 1.3748 minor resistance will turn intraday bias back to the upside for retesting 1.3845 resistance. However, sustained break of 1.3660 will bring deeper fall to 55 D EMA (now at 1.3592) instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

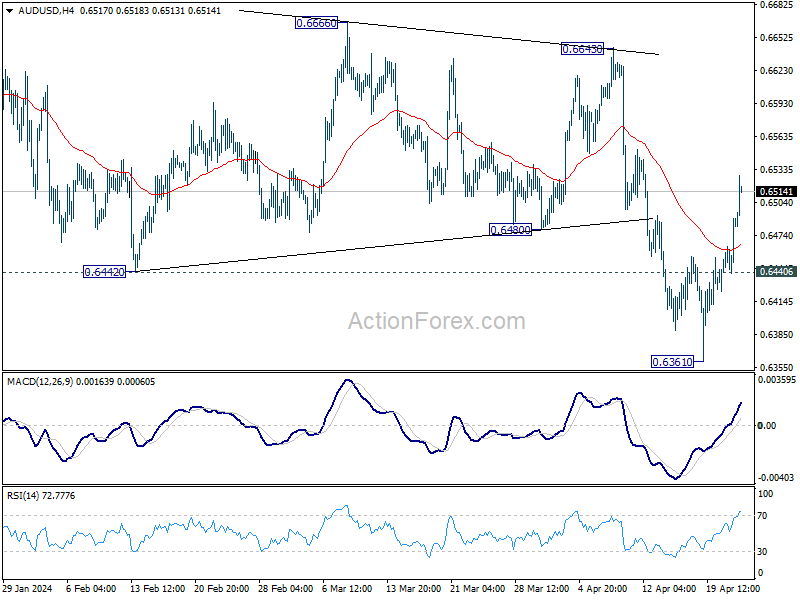

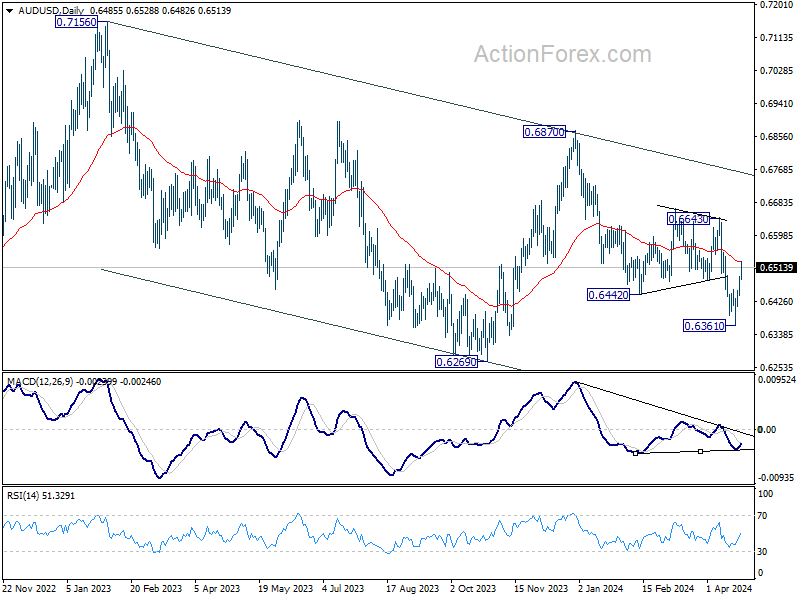

AUD/USD Daily Report

Daily Pivots: (S1) 0.6455; (P) 0.6473; (R1) 0.6504; More...

AUD/USD's strong break of 0.6480 support turned resistance confirms short term bottoming at 0.6361, and intraday bias is back on the upside. Sustained break of 55 D EMA (now at 0.6527) will bring further rally to 0.6643 resistance next. On the downside, though, break of 0.6440 minor support will indicate rejection by 55 D EMA and retain near term bearishness. Retest of 0.6361 low should be seen next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Aussie Propelled by CPI, Has Stock Market Correction Ended?

Australian Dollar is having a robust, broad-based rally today, boosted by unexpectedly strong CPI data. This inflation report is particularly notable given the unexpected reacceleration in monthly CPI in March, which contributed to the quarterly figure not slowing as much as anticipated. Meanwhile, both services and domestic inflation remain elevated. The set of data is unlikely to alter RBA's "not ruling anything in or out" stance at the upcoming meeting in May. The timing of the first rate cut is now pushed further to the end of the year, and there is even possibility that the next move is a rate hike.

Overall in the currency markets, New Zealand Dollar and Sterling also strengthened as the second and third strongest for the day, benefiting from improved risk sentiment this week. This uplift in market mood has sparked questions about whether the correction in global stocks observed this month has run its course, a key point of focus for the coming days.

Conversely, Canadian Dollar is currently the weakest performer today, with market participants awaiting BoC summary of deliberations. There is speculation that BoC may commence a policy easing cycle as early as June, although it is expected to be a finely balanced decision. Investors are keenly awaiting the meeting minutes for further clues on the discussion among board members.

Meanwhile, Yen and Dollar are the next weakest, reflective of the prevailing risk-on market sentiment. Euro and Swiss Franc are currently positioned in the middle of the performance chart.

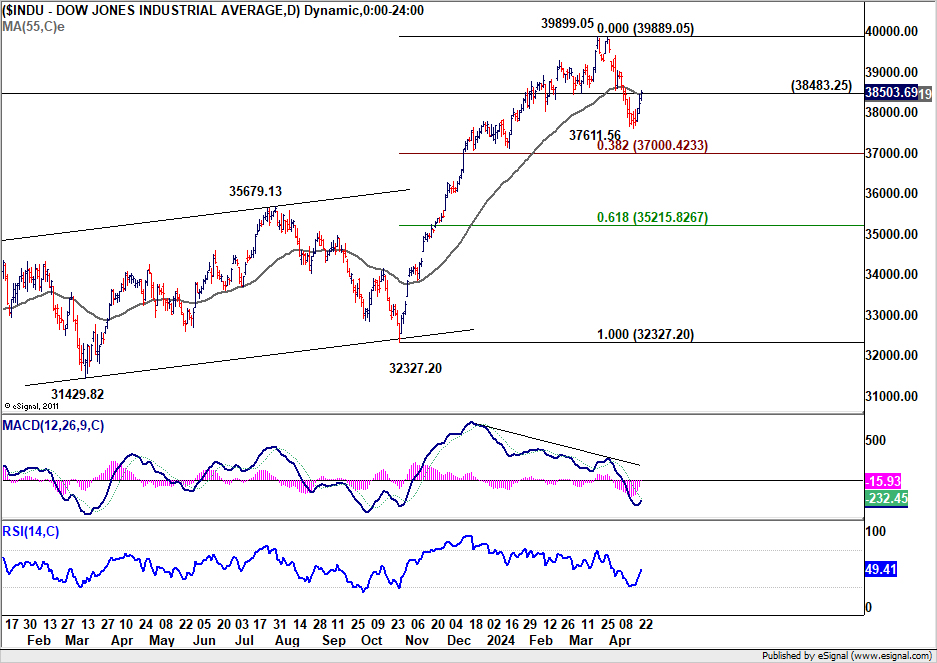

Technically, DOW's break of 38483.25 resistance argues that fall from 39899.05 has completed at 37611.56, ahead of 38.2% retracement of 32327.20 to 39899.05 at 37000.42. Rebound from there is now seen as the second leg of the corrective pattern from 39899.05. Sustained trading above 55 D EMA (now at 38461.65) will strengthen this case and bring stronger rally back towards 39889.05 high.

In Asia, at the time of writing, Nikkei is up 2.33%. Hong Kong HSI is up 1.99%. China Shanghai SSE is up 0.36%. Singapore Strait Times is up 0.98%. Japan 10-year JGB yield is up 0.0035 at 0.890. Overnight, DOW rose 0.69%. S&P 500 rose 1.20%. NASDAQ rose 1.59%. 10-year yield fell -0.025 to 4.598.

Australia CPI slows less than expected in Q1, accelerates in Mar

In Q1, Australia's CPI slowed from 4.1% yoy to 3.6% yoy, exceeding market expectations of 3.4% yoy. Similarly, trimmed mean CPI, which excludes volatile price items and provides a clearer view of underlying inflation trends, also decelerated less than expected, moving from 4.2% yoy to 4.0% yoy, against predictions of 3.8% yoy.

The breakdown by category shows a general slowdown across the board. Goods inflation decreased from 3.8% yoy to 3.1% yoy, while services inflation eased from 4.6% yoy to 4.3% yoy. Tradeable inflation, which includes items that can be imported or exported, slowed more significantly from 1.5% yoy to 0.9% yoy. Non-tradeable inflation, representing goods and services not exposed to international markets, also saw a reduction from 5.4% yoy to 5.0% yoy.

However, on a quarterly basis, CPI rose by 1.0% qoq in Q1, marking an acceleration from the previous quarter's 0.6% qoq and outpacing expectations of a 0.8% rise. This quarterly increase suggests that, despite the annual slowdown, price pressures within the economy intensified at the start of the year. Trimmed mean CPI on a quarterly basis mirrored this trend, rising 1.0% qoq compared to the previous 0.8% qoq, also surpassing the expected 0.8% qoq.

Monthly figures reinforce the notion of persistent inflationary pressures, with CPI ticking up from 3.4% yoy to 3.5% yoy, again exceeding expectations.

New Zealand's goods exports rises 3.8% yoy in Mar, imports fell -25% yoy

New Zealand's goods exports rose 3.8% yoy to NZD 6.5B in March. Goods imports fell -25% yoy to NZD 5.9B. Monthly trade balance was a surplus of NZD 588m, versus expectation of NZD -505m deficit.

Exports to US and EU showed increases of 8.0% yoy and 3.6% yoy respectively. However, exports to major trading partners like China (-1.9% yoy), Australia (-3.7% yoy), and Japan (-15% yoy) declined.

On the import side, there were significant reductions across all major partners. Imports from EU saw the sharpest decline at -43% yoy, followed closely by US at -42% yoy. Imports from China, Australia, and South Korea were down -20% yoy, -13% yoy, and -21% yoy respectively.

Looking ahead

Swiss Credit Suisse eocnomic expetations and German Ifo business climate will be released in European session. US durable goods orders will be released later in US session. Canada will release retail sales and BoC summary of deliberations.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6455; (P) 0.6473; (R1) 0.6504; More...

AUD/USD's strong break of 0.6480 support turned resistance confirms short term bottoming at 0.6361, and intraday bias is back on the upside. Sustained break of 55 D EMA (now at 0.6527) will bring further rally to 0.6643 resistance next. On the downside, though, break of 0.6440 minor support will indicate rejection by 55 D EMA and retain near term bearishness. Retest of 0.6361 low should be seen next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 588M | -505M | -218M | -315M |

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 2.30% | 2.10% | 2.10% | 2.20% |

| 01:30 | AUD | Monthly CPI Y/Y Mar | 3.50% | 3.40% | 3.40% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.00% | 0.80% | 0.60% | |

| 01:30 | AUD | CPI Y/Y Q1 | 3.60% | 3.40% | 4.10% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.00% | 0.80% | 0.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 4.00% | 3.80% | 4.20% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | 11.5 | |||

| 08:00 | EUR | Germany IFO Business Climate Apr | 88.5 | 87.8 | ||

| 08:00 | EUR | Germany IFO Current Assessment Apr | 88.7 | 88.1 | ||

| 08:00 | EUR | Germany IFO Expectations Apr | 88.9 | 87.5 | ||

| 12:30 | USD | Durable Goods Orders Mar | 2.50% | 1.30% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Mar | 0.30% | 0.50% | ||

| 12:30 | USD | Durable Goods Orders ex Defense Mar | 2.00% | 2.20% | ||

| 12:30 | CAD | Retail Sales M/M Feb | 0.10% | -0.30% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Feb | 0.00% | 0.50% | ||

| 14:30 | USD | Crude Oil Inventories | 1.7M | 2.7M | ||

| 17:30 | CAD | BoC Summary of Deliberations |

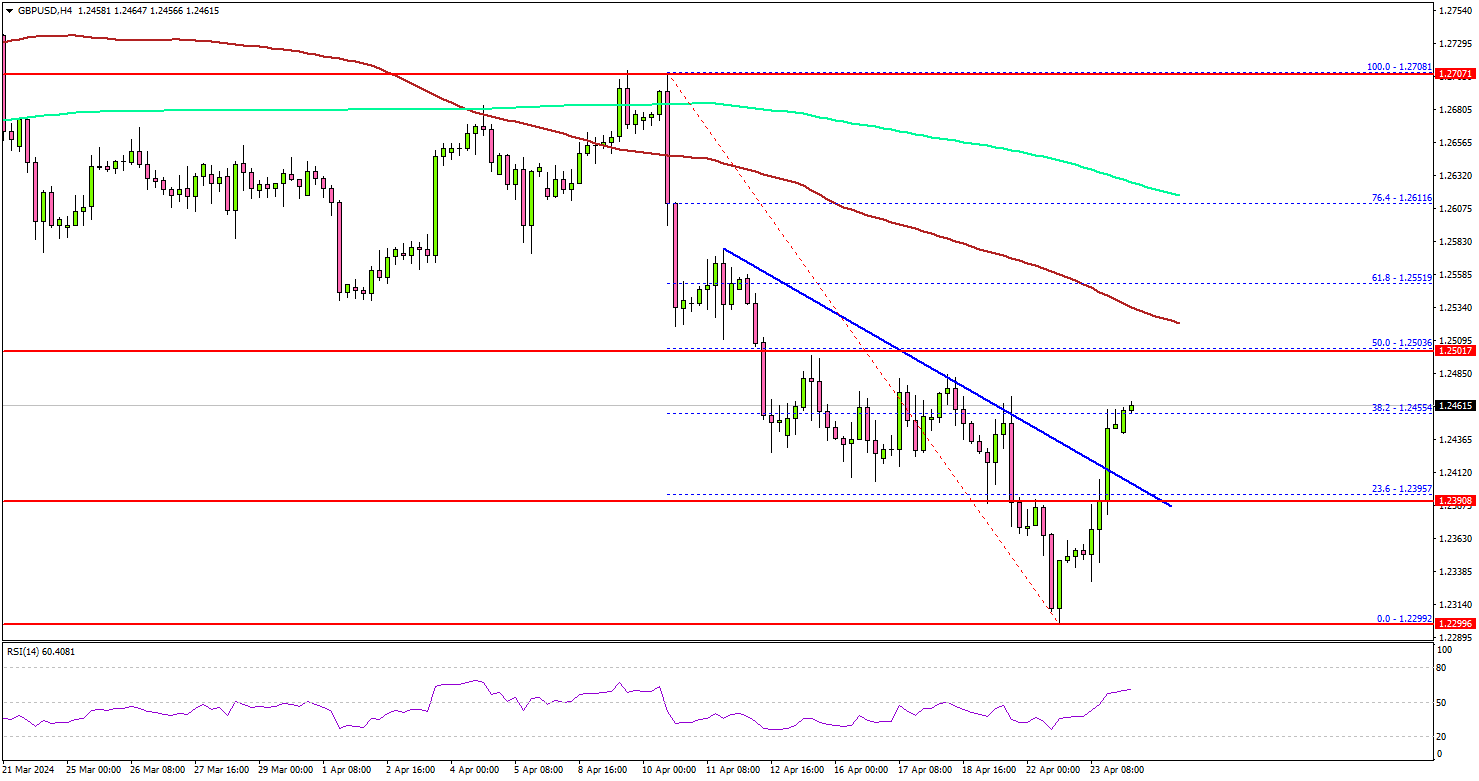

GBP/USD Could Rally If It Clears This Barrier

Key Highlights

- GBP/USD is recovering higher from the 1.2300 support.

- It broke a connecting bearish trend line with resistance at 1.2420 on the 4-hour chart.

- EUR/USD is consolidating and aiming for a move above 1.0750.

- Crude oil prices found support near the $81.50 zone.

GBP/USD Technical Analysis

The British Pound extended losses and traded below the 1.2450 support against the US Dollar. GBP/USD tested the 1.2300 zone and recently started a recovery wave.

Looking at the 4-hour chart, the pair traded as low as 1.2299 and settled well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

It is now recovering higher above 1.2380. GBP/USD surpassed the 23.6% Fib retracement level of the downward move from the 1.2708 swing high to the 1.2299 low. It also broke a connecting bearish trend line with resistance at 1.2420 on the same chart.

Immediate resistance is near the 1.2450 level. The first key resistance is near the 1.2500 zone. It is close to the 50% Fib retracement level of the downward move from the 1.2708 swing high to the 1.2299 low and the 100 simple moving average (red, 4-hour).

A clear move above the 1.2500 resistance could send the pair further higher. In the stated case, GBP/USD bulls could even aim for a move toward 1.2650.

Immediate support is near the 1.2400 level. The next major support is at 1.2380. If there is a downside break below the 1.2380 support, the pair might test 1.2350. The main support is now forming at 1.2300. Any more losses might send the pair toward 1.2120.

Looking at Oil, the price extended losses before it found support near $81.50 and recently started an upside correction.

Economic Releases

- US Durable Goods Orders for March 2024 – Forecast +1.5% versus +1.4% previous.

- US Durable Goods Orders ex Defense for March 2024 – Forecast +2.5% versus +2.2% previous.