Sample Category Title

Slow Grind on Disinflation, RBA on Hold

Inflation was a bit higher than expected in the March quarter. It is declining, but it has a way to go for the RBA to be confident of returning to the 2–3% target range on the desired timetable. We expect the Board to keep rates on hold in May, and have pushed out the date of the first rate cut to November this year, previously September.

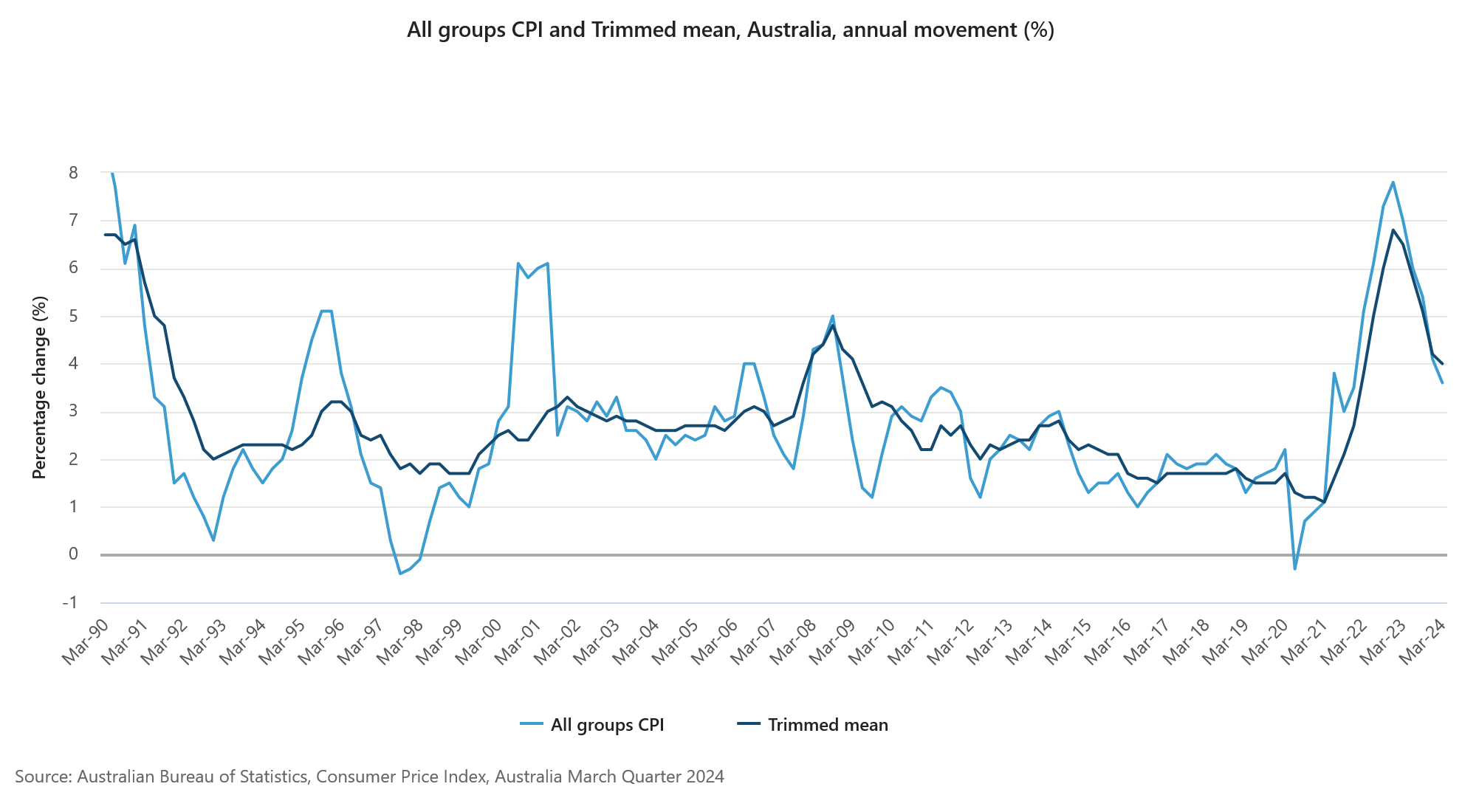

Inflation continued to unwind in the March quarter, but not quite as much as expected. Headline CPI and the key trimmed mean measure both printed at 1.0% in the quarter, against Westpac Economics’ expectation of 0.8% for both measures.

This brings headline inflation on a year-ended basis firmly into the 3s, in striking distance of the RBA’s 2–3% target range, but the key trimmed mean measure is still at 4%. The RBA does not publish a full quarterly profile for its inflation forecasts. However, based on its view for the year-ended to June quarter (3.3% year-ended for headline and 3.6% for trimmed mean), we assess today’s release as implying a somewhat slower trajectory of disinflation than the RBA would like. The RBA might also be sensitive to the lack of progress in disinflation through the March quarter evidenced in the monthly indicator.

Today’s release continues the general pattern of unwinding upstream pressures and soft domestic demand driving some parts of the inflation basket lower. Tradables inflation is back to pre-pandemic norms. Services inflation declined, but remains high. The overall shape of the outcome was qualitatively similar to our expectations, but there were a range of upside surprises in the detail.

The biggest surprises were not in areas that would suggest that inflation is being driven by strong demand. Car prices were up unexpectedly, consistent with the renewed increase in delivery times. Pharmaceutical prices and insurance costs are also not suggesting an inflation driven by consumer demand.

The main other upside surprise in the recent data flow has been the labour market, where unemployment has stayed a bit lower, and employment growth a bit stronger than earlier expected. While the Board is watching labour market developments closely, it is not trying to achieve the required disinflation primarily by weakening the labour market. Labour costs are elevated but they are not the main driver of the inflation surge.

Accordingly, we assess that the RBA will keep rates steady at its upcoming meeting. It will probably continue to be cautious about services inflation and domestic pressures broadly for a few months yet. We therefore do not expect any change to the messaging about not ruling anything in or out for another few months.

Given the slower progress on disinflation this quarter and the lower starting point for labour market slack, we now expect the first rate cut to occur after the November meeting, rather than September as previously expected. As always, this view is data-dependent and there are risks on both sides of a November timing.

Australia CPI slows less than expected in Q1, accelerates in Mar

In Q1, Australia's CPI slowed from 4.1% yoy to 3.6% yoy, exceeding market expectations of 3.4% yoy. Similarly, trimmed mean CPI, which excludes volatile price items and provides a clearer view of underlying inflation trends, also decelerated less than expected, moving from 4.2% yoy to 4.0% yoy, against predictions of 3.8% yoy.

The breakdown by category shows a general slowdown across the board. Goods inflation decreased from 3.8% yoy to 3.1% yoy, while services inflation eased from 4.6% yoy to 4.3% yoy. Tradeable inflation, which includes items that can be imported or exported, slowed more significantly from 1.5% yoy to 0.9% yoy. Non-tradeable inflation, representing goods and services not exposed to international markets, also saw a reduction from 5.4% yoy to 5.0% yoy.

However, on a quarterly basis, CPI rose by 1.0% qoq in Q1, marking an acceleration from the previous quarter's 0.6% qoq and outpacing expectations of a 0.8% rise. This quarterly increase suggests that, despite the annual slowdown, price pressures within the economy intensified at the start of the year. Trimmed mean CPI on a quarterly basis mirrored this trend, rising 1.0% qoq compared to the previous 0.8% qoq, also surpassing the expected 0.8% qoq.

Monthly figures reinforce the notion of persistent inflationary pressures, with CPI ticking up from 3.4% yoy to 3.5% yoy, again exceeding expectations.

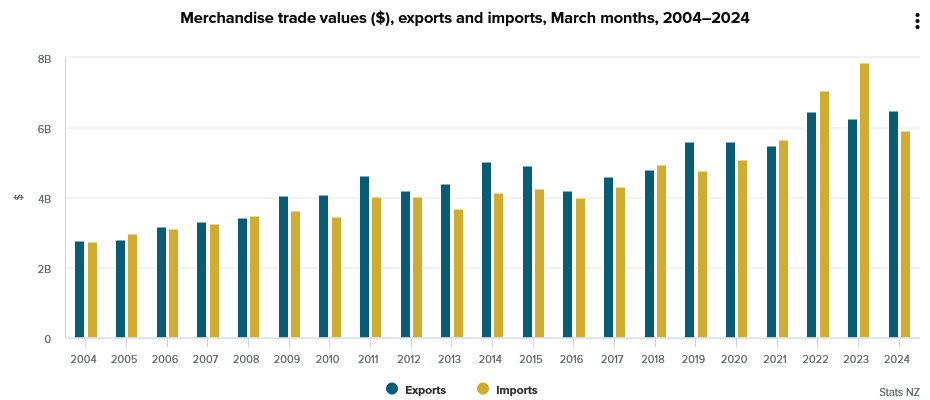

New Zealand’s goods exports rises 3.8% yoy in Mar, imports fell -25% yoy

New Zealand's goods exports rose 3.8% yoy to NZD 6.5B in March. Goods imports fell -25% yoy to NZD 5.9B. Monthly trade balance was a surplus of NZD 588m, versus expectation of NZD -505m deficit.

Exports to US and EU showed increases of 8.0% yoy and 3.6% yoy respectively. However, exports to major trading partners like China (-1.9% yoy), Australia (-3.7% yoy), and Japan (-15% yoy) declined.

On the import side, there were significant reductions across all major partners. Imports from EU saw the sharpest decline at -43% yoy, followed closely by US at -42% yoy. Imports from China, Australia, and South Korea were down -20% yoy, -13% yoy, and -21% yoy respectively.

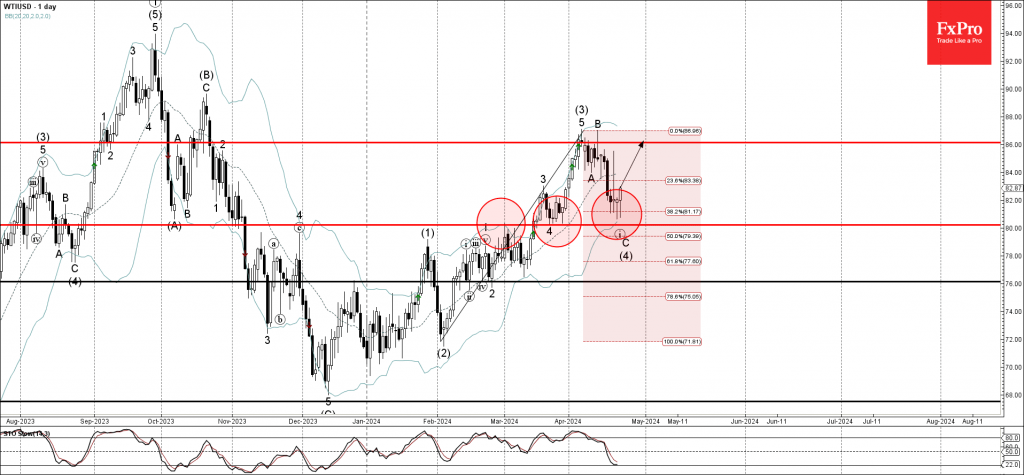

WTI Crude Oil Wave Analysis

- WTI crude oil reversed from support zone

- Likely to rise to resistance level 86.00

WTI crude oil recently reversed up from the support zone lying between the round support level 80.00 (low of wave (iv) from March), lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from February.

The upward reversal from the support level 80.00 stopped the previous ABC correction (4) – forming the daily Hammer.

Give the strength of the support level 80.00, WTI crude oil can be expected to rise further to the next resistance level 86.00 (which stopped waves (3) and B).

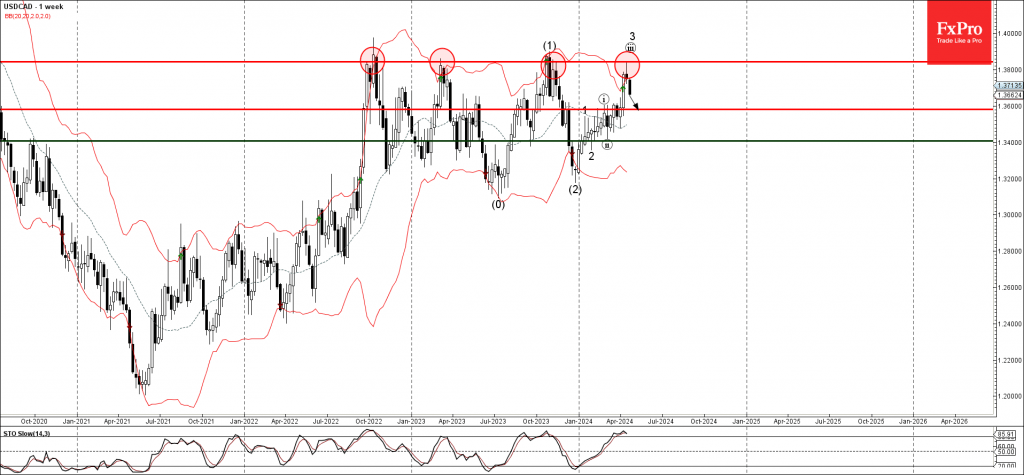

USDCAD Wave Analysis

- USDCAD reversed from long-term resistance level 1.3840

- Likely to fall to support level 1.3600

USDCAD currency pair continues to fall after the pair reversed down with the weekly Shooting Star from the major long-term resistance level 1.3840, which has been reversing the pair from 2022.

The resistance level 1.3840 was strengthened by the upper weekly Bollinger Band.

Give the overbought weekly Stochastic, USDCAD currency pair can be expected to fall further to the next support level 1.3600.

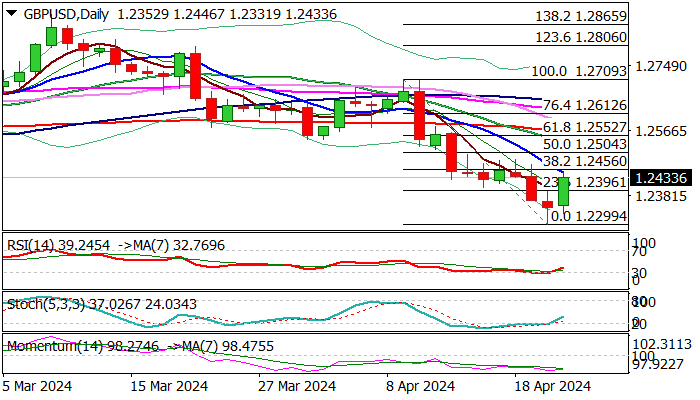

GBP/USD: Cable Bounces After Solid Data/Hawkish BoE

Cable bounces from new multi-month low on Tuesday, boosted by better than expected UK services PMI data and hawkish stance from BoE policymakers, who signaled that rate cut might be delayed, as the central bank sees too early cut more harmful than to start easing policy too late.

Brightened near-term outlook so far lifted the price above initial barrier at 1.2400, with pivotal 1.2446/56 resistance zone (falling 10DMA / Fibo 38.2% of 1.2709/1.2299) being under increased pressure.

Close above these levels is needed to generate initial reversal signal and open way for further recovery towards next targets at 1.2500/60 zone (round-figure / Fibo 61.8% / 200DMA).

Daily studies are still in predominantly bearish setup and warn of limited correction before larger bears regain control, with sustained break of 200DMA seen as a game changer.

Res: 1.2446; 1.2504; 1.2536; 1.2565.

Sup: 1.2396; 1.2331; 1.2299; 1.2210.

Sunset Market Commentary

Markets

EMU PMI’s confirmed the economy is gradually leaving contraction/stagnation territory that reigned in in the second half of last year and during the first months of 2024. The composite output index rose from 50.3 in March to 51.4 in April, the second consecutive reading >50 after 9 months in contraction territory and the best level since May last year. The rise in de headline index still hides divergent sector performances. Activity in the services sector accelerated to a 52.9 from 51.5 and the manufacturing index declined further from 46.1 to 45.6 but with a moderation in the downturn. Job growth accelerated and business confidence remained elevated by recent standards. With respect to inflation, price pressures picked up across the eurozone, often linked to higher wages. Input costs and selling prices also rose at faster rates, reflecting stubborn price pressures in the service sector. Regarding individual countries, Germany returned to growth (composite PMI 50.5) for the first time in 10 months. France stranded at 49.9. EMU bond markets initially reacted in a guarded way, but yields later in de session gradually turned north again. EMU swap yields added between 1.5 bps (2-y) and 2.5 bps (10-y). US yields also added between 1.5 (2-y) and 4 bps (30-y) going into the publication of the US PMI’s. Gilts underperform with yields rising up to 8 bps (5-y). The April composite PMI also improved more than expected (54.0 from 52.8). However, the rise in UK yields mostly occurred this afternoon as BoE chief economist Pill kept a balanced approach of the timing of BoE rate cuts (MPC remains focused on inflation, erring to the side of caution on rate cuts). Equities perform well (Eurostoxx 50 +1.0%, S&P 500 + 0.3%). On FX markets, EUR/USD briefly tested the 1.0695 resistance (previous YtD low) after the release of the first EMU PMI’s. However, gains initially were difficult to maintain. USD/JPY was blocked in an extremely tight range just below the 155 big figure as Japanese officials including Fin Min Suzuki stepped up verbal interventions. Sterling gained modest ground on the a strong PMI and higher yields. Even so, EUR/GBP still holds above the 0.86 barrier (0.861).

At the moment of concluding this report, US April composite PMI surprisingly dropped from 52.1 to 50.9 with both manufacturing (49.9 from 51.9) and services (50.9 from 51.7) contributing to the decline. Yields (US and EMU) return earlier gains. The dollar makes a step backward too, with EUR/USD revisiting the 1.0695 area.

News & Views

The UK’s Debt Management Office beefed up its debt issuance plans for the 2024-2025 fiscal year by £12.4bn. Total issuance is forecast to be £277.7bn, the second-largest on record. The announcement followed the release of the Office for National Statistics of the 2023-2024 budget deficit which showed a bigger than earlier forecasted shortfall of £120.7bn or 4.4% of GDP. The Office for Budget Responsibility last month estimated a deficit for FY 23-24 of £114.1bn (4.2% of GDP) with lower receipt from income tax and national insurance contributions explaining for most of the gap. The additional borrowing requirement will be met mostly by increased short-dated (+£5.4bn) and medium-term gilts (£3.9bn). The numbers highlight the budgetary challenges the UK faces and undermine the Sunak government’s wish list of tax cuts in the run-up to the elections this year. A recent YouGov voting intention poll (Apr 16-17) showed Sunak’s Conservative Party trailing the Labour party by a significant margin (21% vs 44%). Reform UK – the former Brexit party – gained traction from end 2023 on, securing a third place with 14% of the votes.

Reuters citing two government officials reported that Greece plans an early repayment between €2.5 and €5bn of bailout loans to euro area countries, probably in the second half of the year. The loans date back to debt crisis starting in 2010 that engulfed the EMU. The IMF and euro area countries lent Greece some €280bn with the former paid back two years ahead of schedule in 2022. But +/- 70% of the country’s debt is still in hands outside the public. One of the officials noted that the early repayment would make room for more bond issuances without increasing its debt pile while simultaneously adding liquidity to a shallow Greek bond market. The country today announced a 30-year bond sale for the first time since 2021. It last raised €4bn from the public in January and is targeting a total of €10bn for the whole year.

Graphs

EMU 10-yr swap continues challenging YTD top as EMU economy is leaving stagnation territory.

UK 2-y yield rebounds as BOE chief Economist Pill advocates caution on interest rate cuts as inflation risks persist.

Forint holding stable near EUR/HUF 394 as MNB slows pace of rate cuts to 50 bps steps (7.75% from 8.25% today).

Gold correcting of top levels as geopolitical uncertainty eases

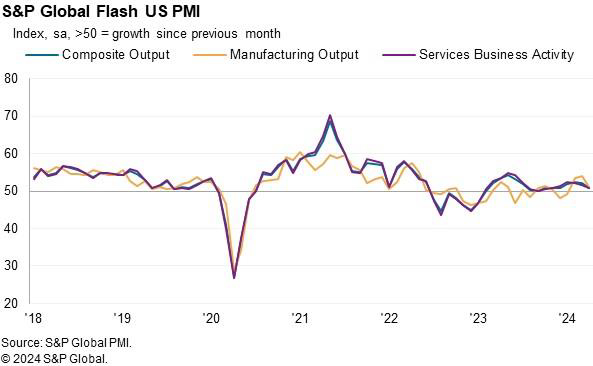

US PMI composite falls to 50.9, economic upturn loses momentum

US PMI Manufacturing fell from 51.9 to 49.9 in April. PMI Services fell from 51.7 to 50.9. PMI Composite fell from 52.1 to 50.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The US economic upturn lost momentum at the start of the second quarter, with the flash PMI survey respondents reporting below-trend business activity growth in April. Further pace may be lost in the coming months, as April saw inflows of new business fall for the first time in six months and firms' future output expectations slipped to a five-month low amid heightened concern about the outlook.

"The more challenging business environment prompted companies to cut payroll numbers at a rate not seen since the global financial crisis if the early pandemic lockdown months are excluded.

"The deterioration of demand and cooling of the labor market fed through to lower price pressures, as April saw a welcome easing in rates of increase for selling prices for both goods and services.

"Notably, the drivers of inflation have changed. Manufacturing has now registered the steeper rate of price increases in three of the past four months, with factory cost pressures intensifying in April amid higher raw material and fuel prices, contrasting with the wage-related services-led price pressures seen throughout much of 2023."

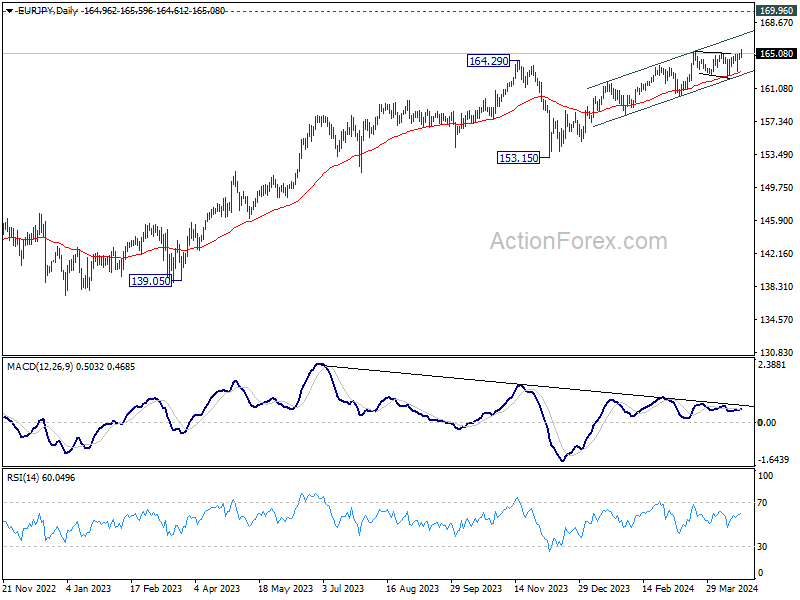

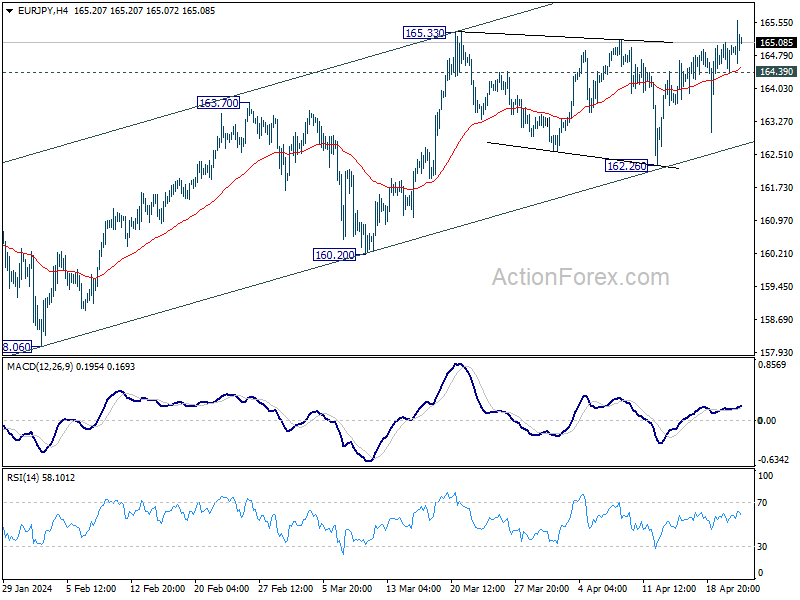

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 164.55; (P) 164.82; (R1) 165.25; More...

EUR/JPY's breach of 165.33 resistance argues that larger up trend is resuming. Intraday bias is back on the upside. Further rally would be seen to 169.96 key resistance next. Nevertheless, break of 164.39 minor support will turn intraday bias neutral again first.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 169.96 (2008 high). Break of 160.20 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.