Sample Category Title

High Expectations Play Tricks on Big Tech

Meta revealed better than expected earnings, a more-than-doubled profit from last year and a 27% rise in sales. Oh, and the revenue growth was up for the fifth quarter. But the share price tumbled 15% in the afterhours trading as investors didn’t like the weaker-than-expected revenue forecast for the current quarter and even less the news that the company will be spending more money to improve its AI capabilities. Meta is now expected to spend around $35 to 40 billion, versus $30-37 billion they said they would spend earlier. In fine, these investments will help the company keep more people longer on their platform and increase their ad revenue with a more intelligent and customized advertisement strategy, but additional spending news comes at a time investors were expecting Meta to start throwing magnificent results into the mix. And all we got is a lower revenue outlook and more spending. Price-wise, Meta will likely slip below its uptrending range building since end of 2022; it’s certainly not the end of the AI hype for Meta, but it’s sure a short-term disappointment.

Google, Microsoft and Intel are due to report today.

So far, we observe that the high expectations have played tricks on stock valuations and the first set of earnings reactions warn that even strong results from Big Tech may not suffice to send their stock prices higher – if we start seeing growth expectations level out. (I am looking at you Microsoft and Nvidia.)

Zooming out, the stumbling giant Meta is weighing on the mood this morning. US futures are down and the technology-heavy Nasdaq is leading losses with more than 1% fall at the time of writing.

The macroeconomic landscape is complex, with investors balancing between robust GDP growth and high earnings expectations for the Big Tech companies, all while considering the fading expectations for a Federal Reserve's (Fed) rate cut. A strong GDP reading would suggest that the US economy is sufficiently strong to support corporate earnings, but it could also delay expectations for a Fed rate cut. Conversely, a softer-than-expected GDP figure would likely increase expectations for a rate cut, especially if earnings disappoint due to inflated expectations. Overall, I believe that a softer-than-expected GDP would elicit a more positive market reaction, but the risks surrounding GDP lean towards a better-than-expected reading. According to a consensus of analyst estimates on Bloomberg, Q1 growth is expected to be around 2.5%, while the Atlanta Fed’s GDPNow projection stands at approximately 2.7%.

The US dollar index rebounded yesterday after trading near a two-week low. The EURUSD remained bid into the 1.0680 support, fueled by better than expected German sentiment data – which showed that business sentiment rose to the highest level in a year. But a set of rating assessments are expected to challenge the rising debt risks in France and Italy, and could limit the upside potential along with a potentially stronger US dollar dependent on today’s first glimpse at the Q1 growth.

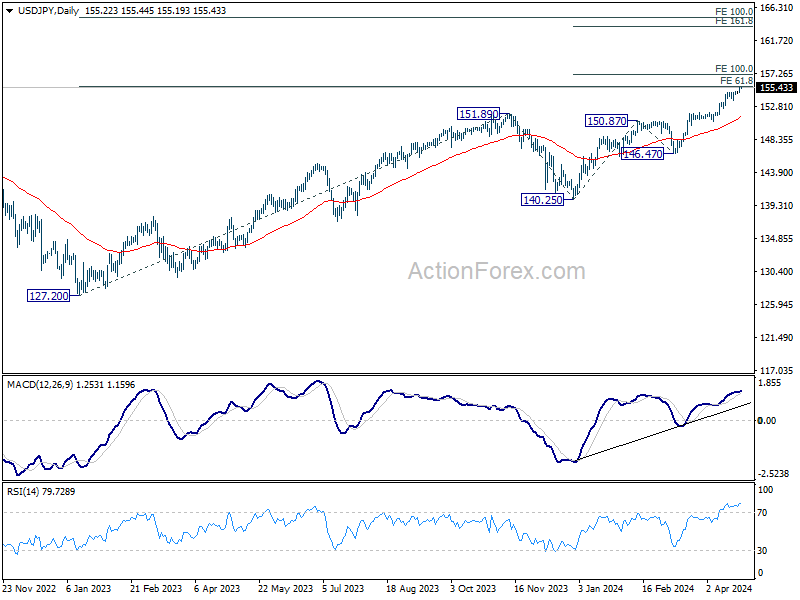

The dollar appreciation is a problem for many economies, but it has become a major headache for the Bank of Japan (BoJ). The USDJPY spiked and extended gains above the 155 mark. The BoJ will lean on to the USD strength at this week’s policy meeting and will – potentially – intervene to slow the yen selloff. What’s interesting is that we know that next hours will likely bring an announcement to tackle the yen depreciation, but the yen shorts are not afraid. They know that an FX intervention alone won’t reverse the yen’s falling course unless accompanied by a hawkish BoJ policy outlook. Therefore, even an intervention could backfire and fail to prevent a further rise in USDJPY to the 160 level.

JPY Weakness Extends

In focus today

In the US, today's focus will be on Q1 flash GDP data, where consensus expects growth to moderate to 2.4% Q/Q AR (Q4 3.4%). Private consumption has remained on a gradually cooling, yet steady trend, while private manufacturing investments and public state and local investments are still supported by past stimulus measures. That said, April PMI data released earlier this week suggested that Q2 has started on a relatively weaker footing.

In the euro area, Isabel Schnabel will deliver the opening remarks for a monetary policy conference in Frankfurt. Christine Lagarde delivers a speech at a conference on the Capital Market Union in Paris. Today's list of ECB speakers also includes Vujcic, Nagel and Panetta. The ECB will also publish its economic bulletin today.

In Sweden, we get the last NIER Economic Tendency Survey (at 9.00 CET) before the Riksbank's upcoming policy rate decision 8 May. Companies' pricing plans will be of high importance. Overall, companies' price plans are now compatible with an inflation rate of 2% (being in line with pre-pandemic averages), but there is perhaps a question mark around the services sector, where we saw an uptick in price plans last month. Riksbank's Aino Bunge participates in a seminar on "Functioning Payments in Crisis and War". Despite the topic of the seminar, we will likely get some comments on monetary policy as Bunge will be available for journalists after the event (around 14.15 CET).

The Central Bank of Turkey announce their rate decision, after their monetary policy meeting. Market consensus is in favour of unchanged interest rate, with some forecasters eyeing a possible hike.

Economic and market news

What happened overnight

The JPY continues to weaken with USD/JPY hitting as high as 155.48 in overnight trading. The Japanese monetary and fiscal authorities have earlier said that they are concerned with the continuously weakening of the JPY, and have threatened to intervene in the market over several occasions, but we are still to see some action on the matter.

What happened yesterday

In the US, President Biden signed the USD 95 billion bill with military aid for Ukraine, Israel, and Taiwan. He later stated that some of the aid for Ukraine would be sent to them already Wednesday evening.

Yesterday's fixed income sell-off has pushed 10y UST yield near recent highs. 10Y UST yields ended up by 5bp in 4.65% for the day.

Meta, the company behind Facebook and Instagram, presented forecasts of higher AI expenses and lighter-than-expected revenue, leading to the share falling 10% in after-hours trading. Alphabet, the parent of Google, fell 3% in extended trading and Microsoft fell 2% as investors fear that they may have underestimated the costs of the AI race among big tech companies. Both companies will deliver financial statements for Q1 today.

In Germany, the Ifo indicator showed that business sentiment increased more than expected in April to 89.4 (cons: 88.8, prior: 87.9). Both the assessment of the current situation and future expectations rose more than expected. Note that the index still indicates that the German economy is in contractionary territory.

ECB's Nagel said that a June rate cut will not necessarily be followed by a series of rate cuts. He is still worried about a potential inflation rebound, especially service inflation, which has proved more persistent than goods inflation, and is driven by continued strong wage growth.

Yesterday's market movements

Equities. Global equities ended marginally higher yesterday after a bit of a roller-coaster ride in both Europe and US. It was a huge reporting day which helps explain the fairly rare mix of sector performance with financials, industrials and healthcare underperforming. The earnings season is peaking today, and that coupled with reports we saw in the afterhours yesterday means that we should prepare for yet another day micro dominating markets. In the US yesterday, Dow -0.1%, S&P 500 +0.02%, Nasdaq +0.1%, and Russell 2000 -0.4%. Asian markets are sharply down this morning, led lower by the afterhours earnings results from the US and even more so, the disappointing company guidance. European futuress are marginally lower this morning while US futures are dragged down by the tech sector.

FI: The Bund curve continued bear-steepening in yesterday's session with the 10Y tenor up by 9bp for the day, closing at a 5-month high of 2.59%. The repricing happened gradually through the day without a clear catalyst triggering the move. The 10Y German auction yesterday was well-bid with BTC at 2.5. However, with Eurozone PMI/IFO data showing strong signs of recovery, additional uncertainty on the disinflationary trajectory is now evident in the remarks coming out from the hawkish ECB members.

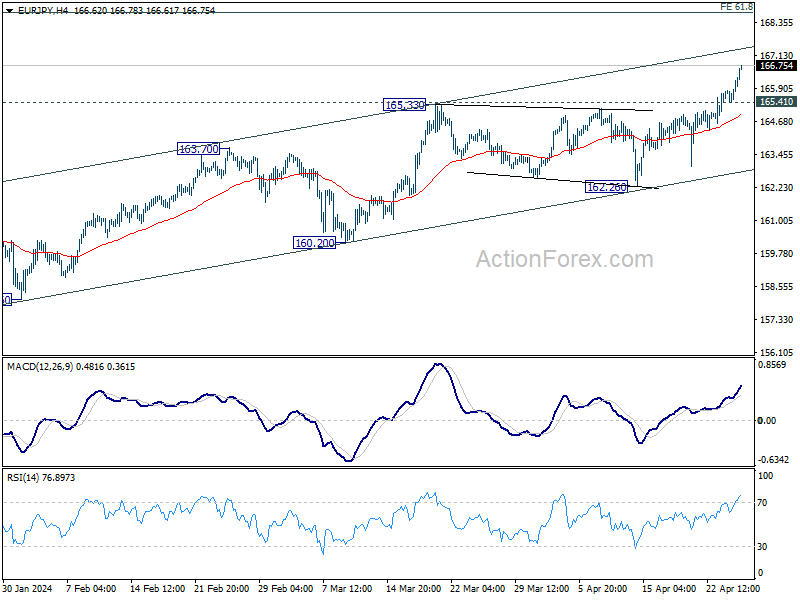

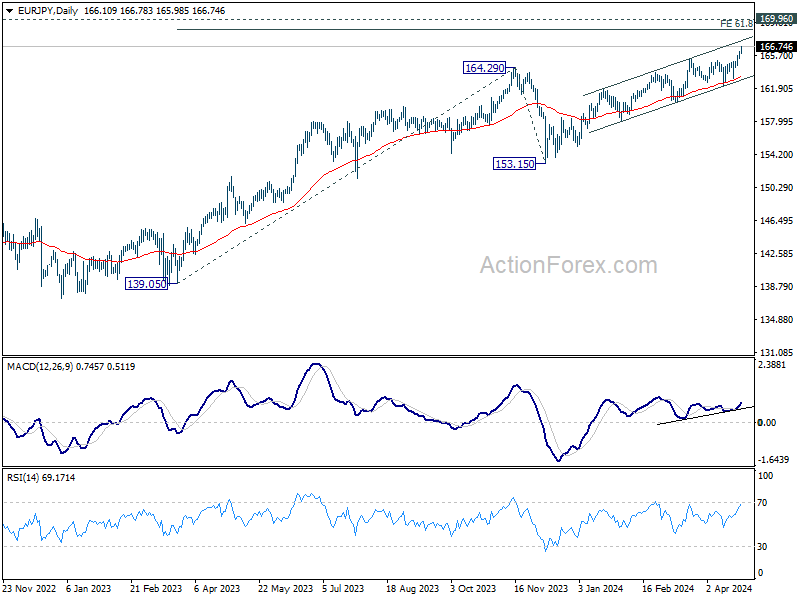

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.67; (P) 165.95; (R1) 166.50; More...

EUR/JPY's up trend continues to as high as 166.78 so far. Intraday bias stays on the upside for 168.72 projection level next. On the downside, below 165.41 minor support will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 61.8% projection of 139.05 to 164.29 from 153.15 at 168.72, or even further to 169.96 (2008 high). Break of 162.26 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

Yen Weakens Further as Market Eyes Possible 160 Mark, Dollar Awaits Key GDP Data

Japanese Yen's accelerated decline captured significant attention in Asian session, while the broader currency markets remained generally stable. Market participants interpret the apparent lack of urgency from Japanese officials to address Yen's fall as a tacit approval for its continued depreciation. This perspective gains significance following the recent trilateral meeting between Japan, South Korea, and the US, where the sharp decline of Yen was a subject of "serious concerns." Speculation is rife that Japan might tolerate Yen's fall to 160 mark against Dollar before taking any corrective actions.

Concurrently, Dollar is also soft as traders anticipate US Q1 GDP advance report. The US economy is expected to show 2.1% annualized growth in Q1, slowed from Q4's 3.4%. GDP price index is expected to jump from 1.6% to 3.0%. If these projections hold, they would suggest that the economy is continuing to expand at a healthy rate with little risk of recession. This scenario is likely to support Fed's cautious stance on interest rate cuts. A detailed breakdown showing robust consumer spending could even delay Fed's first rate cuts further.

In terms of weekly performance, Yen is currently the weakest among major currencies, followed by Dollar and Swiss Franc. In contrast, Australian Dollar leads as the strongest, followed by Kiwi and Euro, while Sterling and Canadian Dollar hold middle positions. This configuration aligns with the prevailing risk-on sentiment, evidenced by strong rebound in US stock indices and new record high in FTSE.

Technically, a focus today is whether AUD/USD, in reaction to broader risk sentiment, could break through 55 D EMA (now at 0.6526) decisively. In this case, fall from 0.6870 could have completed with three waves down to 0.6361 already. Stronger rally would be seen to 0.6643 resistance first. However, rejection by 55 D EMA, followed by break of 0.6440 minor support will retain near term bearishness, and resume the decline through 0.6361 instead.

In Asia, at the time of writing, Nikkei is down -1.98%. Hong Kong HSI is up 0.25%. China Shanghai SSE is up 0.13%. Singapore Strait Times is down -0.40%. Japan 10-year JGB yield is up 0.0019 at 0.893. Overnight, DOW fell -0.11%. S&P 500 rose 0.02%. NASDAQ rose 0.10%. 10-year yield rose 0.054 to 4.6552.

Yen's selloff intensifies as BoJ meeting commences

Yen's selloff is intensifying and breaking through 155 mark against Dollar as BoJ commences its two-day policy meeting. While no changes in policy are anticipated at this gathering, the continued decline of Yen could provoke hawkish remarks from Governor Kazuo Ueda. He has clearly indicated that a policy adjustment would be considered if weakening Yen's impact on inflation becomes too significant to overlook.

Attention is also turning towards BoJ's new economic projections. Inflation forecasts for fiscal years 2024 and 2025 are expected to be upgraded from current predictions of 2.4% and 1.8%, respectively. For fiscal 2026, forecasts could suggest that core inflation will align closely with BoJ's target of 2%.

Governmental response to Yen's decline has so far been constrained. Finance Minister Shunichi Suzuki reiterated today that there has been no alteration in the government's approach towards Yen's valuation, emphasizing that actions will be taken as appropriate. He added that the government is "carefully monitoring" currency market movements, but declined from further comments.

Technically, strong resistance could be seen from 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20 to limit USD/JPY's rally on the first attempt. However, firm break of this level will put 100% projection of 140.25 to 150.87 from 146.47 at 157.09 as next near term target.

BoC members divided on rate cut timing, united on gradual easing approach

BoC's April meeting summary revealed a "diversity of views" among its members concerning the timing of the first interest rate cut. Despite differing opinions, there was a unanimous agreement that any adjustment to monetary policy would "probably be gradual" once initiated.

Key concerns highlighted by some board members included the need for "more reassurance" regarding the diminishing risks associated with stalling of progress on slowing core inflation. These members observed that the Canadian economy is "performing well", mitigating the risk that the current restrictive monetary policy could excessively decelerate economic activity. However, they cautioned that stronger domestic demand, alongside robust economic growth in the US, "keep core inflation from slowing further" or might even cause it to "pick up again in the event of new surprises".

Conversely, other members argued that there is a tangible risk of maintaining a monetary policy that is "more restrictive than needed." This group emphasized the significant progress already achieved in reducing inflation, noting that the rates of inflation across most goods and services had "come down significantly," and the distribution of inflation rates among the CPI components had begun to "approach normal."

Despite these differing perspectives, the consensus was clear that any forthcoming policy easing would be implemented cautiously. "While there was a diversity of views about when conditions would likely warrant cutting the policy rate, they agreed that monetary policy easing would probably be gradual, given risks to the outlook and the slow path for returning inflation to target," the summary stated.

Looking ahead

German Gfk consumer climate and ECB monthly bulletin will be released in Euroepan session. Later in the day, US Q1 GDP advance is the main focus. Jobless claims, trade balance, and pending home sales will also be released.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.67; (P) 165.95; (R1) 166.50; More...

EUR/JPY's up trend continues to as high as 166.78 so far. Intraday bias stays on the upside for 168.72 projection level next. On the downside, below 165.41 minor support will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current rally is part of the up trend from 114.42 (2020 low), which is still in progress. Next target is 61.8% projection of 139.05 to 164.29 from 153.15 at 168.72, or even further to 169.96 (2008 high). Break of 162.26 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish in case of retreat.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany GfK Consumer Confidence May | -25.5 | -27.4 | ||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 19) | 210K | 212K | ||

| 12:30 | USD | GDP Annualized Q1 P | 2.10% | 3.40% | ||

| 12:30 | USD | GDP Price Index Q1 P | 3.00% | 1.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -91.2B | -90.3B | ||

| 12:30 | USD | Wholesale Inventories Mar P | 0.20% | 0.50% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | 0.90% | 1.60% | ||

| 14:30 | USD | Natural Gas Storage | 50B |

Elliott Wave Intraday Analysis on GBPUSD Shows 5 Waves Bullish Impulse

Elliott Wave view on GBPUSD suggests that rally from 10.4.2023 low takes the form of an impulsive structure. Up from 10.4.2023 low, wave (1) ended at 1.2828. Correction in wave (2) unfolded as an expanded flat Elliott Wave structure. Down from wave (1), wave A ended at 1.2519 and wave B ended at 1.2894. Down from there, wave C subdivided into 5 waves. Wave ((i)) ended at 1.2538 and wave ((ii)) ended at 1.2709. The 60 minutes chart below shows the move lower in wave C from wave ((ii)) high.

Pair then extended lower in wave ((iii)) towards 1.2405 and rally in wave ((iv)) ended at 1.2485. Final leg wave ((v)) ended at 1.23. This completed wave C of (2) of the expanded flat. The pair has turned higher in wave (3), and the rally shows a promising 5 waves impulse in short term. Up from wave (2), wave (i) ended at 1.236 and wave (ii) ended at 1.233. Wave (iii) higher ended at 1.2465 and wave (iv) pullback ended at 1.242. Expect wave (v) of ((i)) to complete soon. Pair should then pullback in wave ((ii)) to correct cycle from 4.22.2024 low before it resumes higher. Near term, as far as pivot at 1.23 low stays intact, expect pullback to find support in 3, 7, 11 swing for further upside.

GBPUSD 60 Minutes Elliott Wave Chart

GBPUSD Elliott Wave Video

https://www.youtube.com/watch?v=fsHdAHaPx0c

Yen’s selloff intensifies as BoJ meeting commences

Yen's selloff is intensifying and breaking through 155 mark against Dollar as BoJ commences its two-day policy meeting. While no changes in policy are anticipated at this gathering, the continued decline of Yen could provoke hawkish remarks from Governor Kazuo Ueda. He has clearly indicated that a policy adjustment would be considered if weakening Yen's impact on inflation becomes too significant to overlook.

Attention is also turning towards BoJ's new economic projections. Inflation forecasts for fiscal years 2024 and 2025 are expected to be upgraded from current predictions of 2.4% and 1.8%, respectively. For fiscal 2026, forecasts could suggest that core inflation will align closely with BoJ's target of 2%.

Governmental response to Yen's decline has so far been constrained. Finance Minister Shunichi Suzuki reiterated today that there has been no alteration in the government's approach towards Yen's valuation, emphasizing that actions will be taken as appropriate. He added that the government is "carefully monitoring" currency market movements, but declined from further comments.

Technically, strong resistance could be seen from 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20 to limit USD/JPY's rally on the first attempt. However, firm break of this level will put 100% projection of 140.25 to 150.87 from 146.47 at 157.09 as next near term target.

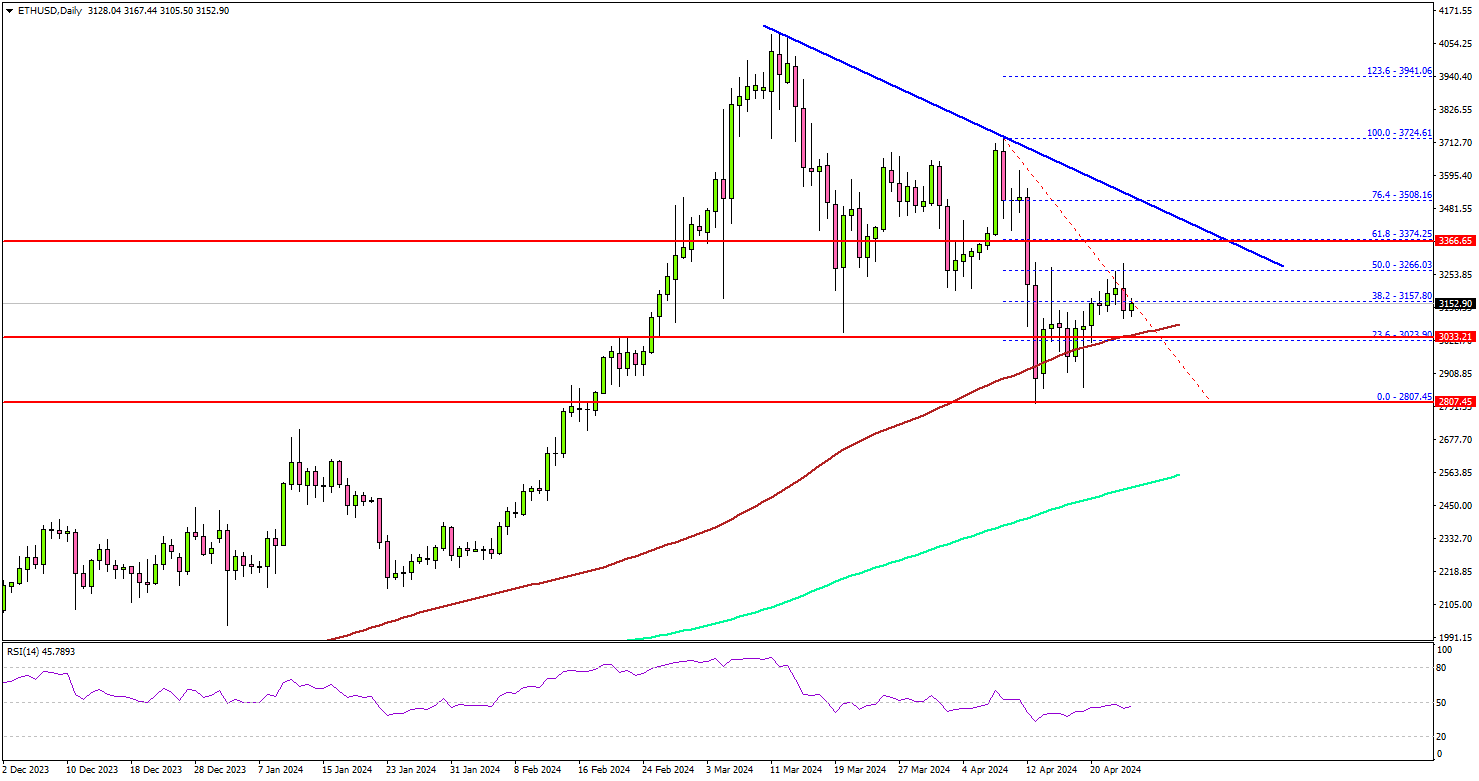

Ethereum (ETH) Could Rally If This Resistance Gives Way

Key Highlights

- Ethereum started a recovery wave from the $2,800 zone.

- ETH price is facing resistance near a key bearish trend line at $3,400 on the daily chart.

- Bitcoin price is struggling to gain pace for a move above the $67,500 resistance.

- Gold price found support at $2,290 and started a consolidation phase.

Ethereum Technical Analysis

Ethereum found strong bids near the $2,800 zone. ETH price started a decent upward move above the $3,000 resistance and recovered some losses, like Bitcoin.

Looking at the daily chart, the price climbed above the $3,150 resistance. There was a spike above the 50% Fib retracement level downward move from the $3,724 swing high to the $2,807 low.

The price is now stable above the 100-day simple moving average (red) and the 200-day simple moving average (green). However, it is facing resistance near a key bearish trend line at $3,400 on the daily chart.

The trend line is close to the 61.8% Fib retracement level downward move from the $3,724 swing high to the $2,807 low. A daily close above the $3,400 resistance zone could start a steady increase. In the stated case, the price may perhaps rise toward the $3,725 level. The next stop for the bulls may perhaps be near the $4,000 level.

If not, the price might start another decline and test the $3,120 support level. The next major support is near $3,025, below which the price could slide toward $2,800.

Looking at gold prices, the bulls were active near the $2,390 and the bulls might now aim for a fresh increase in the near term.

Economic Releases

- US Gross Domestic Product Q1 2024 (Preliminary) – Forecast 2.5% versus previous 3.4%.

- US Initial Jobless Claims - Forecast 214K, versus 212K previous.

BoC members divided on rate cut timing, united on gradual easing approach

BoC's April meeting summary revealed a "diversity of views" among its members concerning the timing of the first interest rate cut. Despite differing opinions, there was a unanimous agreement that any adjustment to monetary policy would "probably be gradual" once initiated.

Key concerns highlighted by some board members included the need for "more reassurance" regarding the diminishing risks associated with stalling of progress on slowing core inflation. These members observed that the Canadian economy is "performing well", mitigating the risk that the current restrictive monetary policy could excessively decelerate economic activity. However, they cautioned that stronger domestic demand, alongside robust economic growth in the US, "keep core inflation from slowing further" or might even cause it to "pick up again in the event of new surprises".

Conversely, other members argued that there is a tangible risk of maintaining a monetary policy that is "more restrictive than needed." This group emphasized the significant progress already achieved in reducing inflation, noting that the rates of inflation across most goods and services had "come down significantly," and the distribution of inflation rates among the CPI components had begun to "approach normal."

Despite these differing perspectives, the consensus was clear that any forthcoming policy easing would be implemented cautiously. "While there was a diversity of views about when conditions would likely warrant cutting the policy rate, they agreed that monetary policy easing would probably be gradual, given risks to the outlook and the slow path for returning inflation to target," the summary stated.

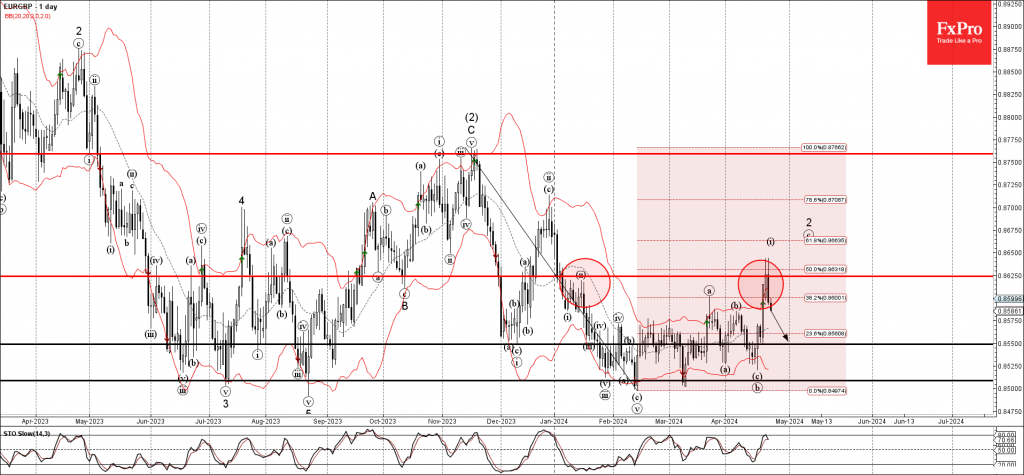

EURGBP Wave Analysis

- EURGBP reversed from resistance level 0.8625

- Likely to fall to support level 0.8550

EURGBP currency pair recently reversed down from the key resistance level 0.8625, which has been reversing the price from January, intersecting with the 50% Fibonacci correction of the previous downward impulse from November.

The downward reversal from the resistance level 0.8625 created the daily Japanese candlesticks reversal pattern Bearish Engulfing

Give the predominant daily downtrend and the bearish euro sentiment seen today, EURGBP currency pair can be expected to fall further to the next support level 0.8550.

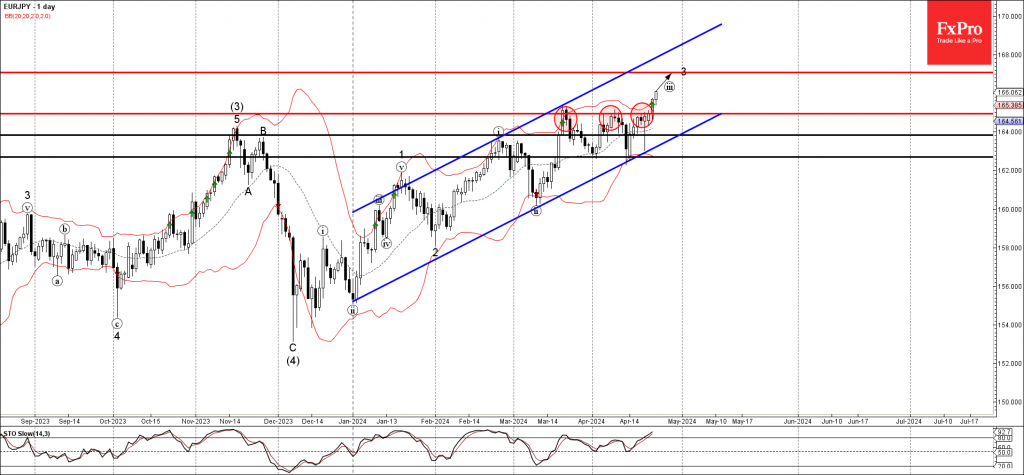

EURJPY Wave Analysis

- EURJPY under bullish pressure

- Likely to rise to resistance level 167.00

EURJPY currency pair under the bullish pressure after the price broke through the key resistance level 165.00, which has been reversing the price from March.

The breakout of the resistance level 165.00 accelerated the active impulse waves iii, 3 and (5).

Give the strength of the active uptrend and the continuation of the yen outflows, EURJPY currency pair can be expected to rise further to the next resistance level 167.00 (target price for the completion of the active impulse wave 3).