Sample Category Title

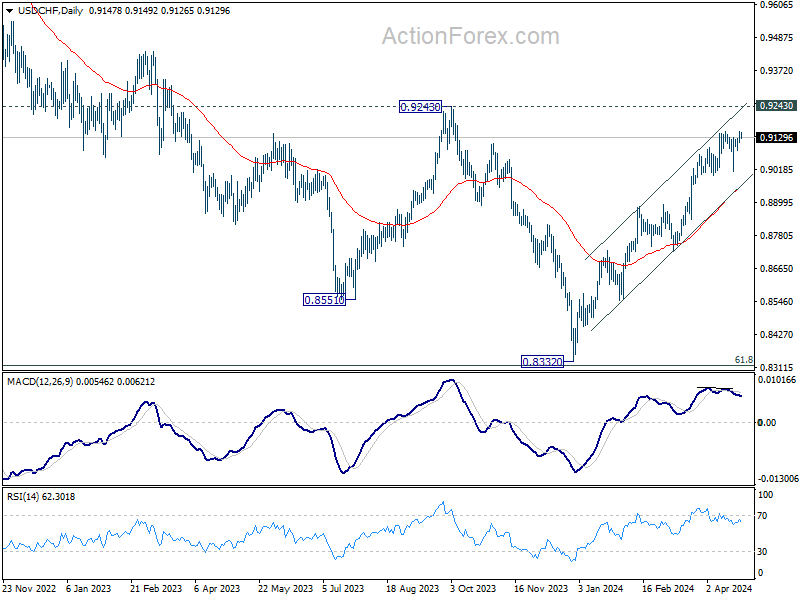

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9121; (P) 0.9138; (R1) 0.9167; More....

Intraday bias in USD/CHF remains neutral and more sideway trading could be seen. Further rally is expected as long as 0.8996 support holds. Break of 0.9151 will resume the larger rise from 0.8332 to 0.9243 resistance. However, firm break of 0.8996 will turn bias to the downside for 55 D EMA (now at 0.8953).

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish.

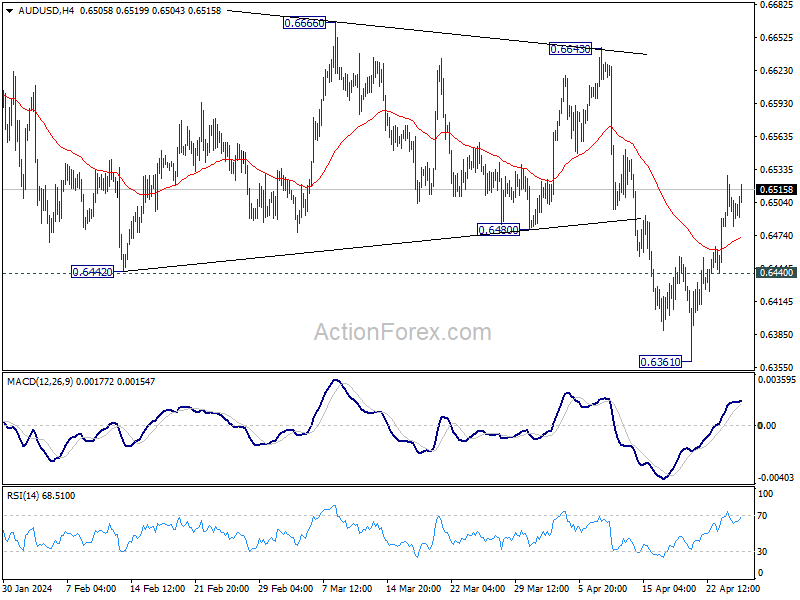

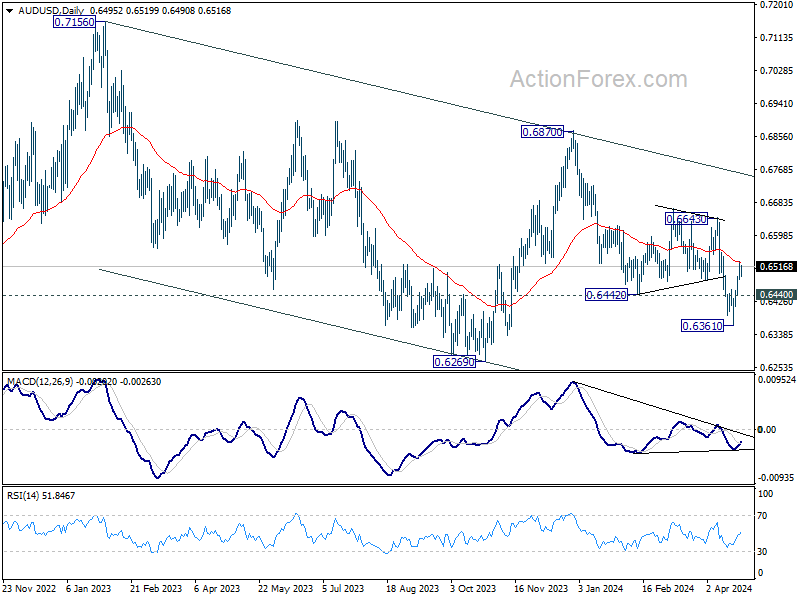

AUD/USD Daily Report

Daily Pivots: (S1) 0.6474; (P) 0.6502; (R1) 0.6526; More...

Intraday bias in AUD/USD remains on the upside for the moment. Sustained break of 55 D EMA (now at 0.6527) will argue that fall from 0.6870 has completed, and bring further rally to 0.6643 resistance next. On the downside, though, break of 0.6440 minor support will indicate rejection by 55 D EMA and retain near term bearishness. Retest of 0.6361 low should be seen next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

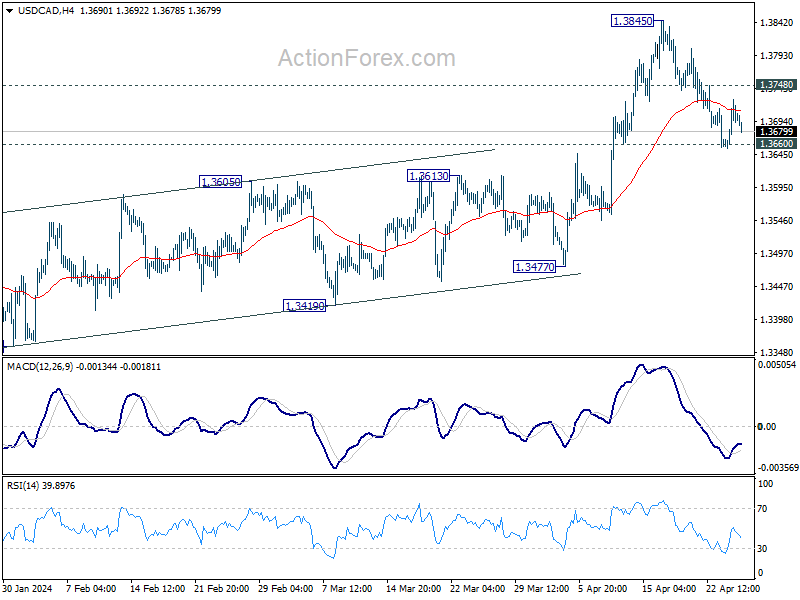

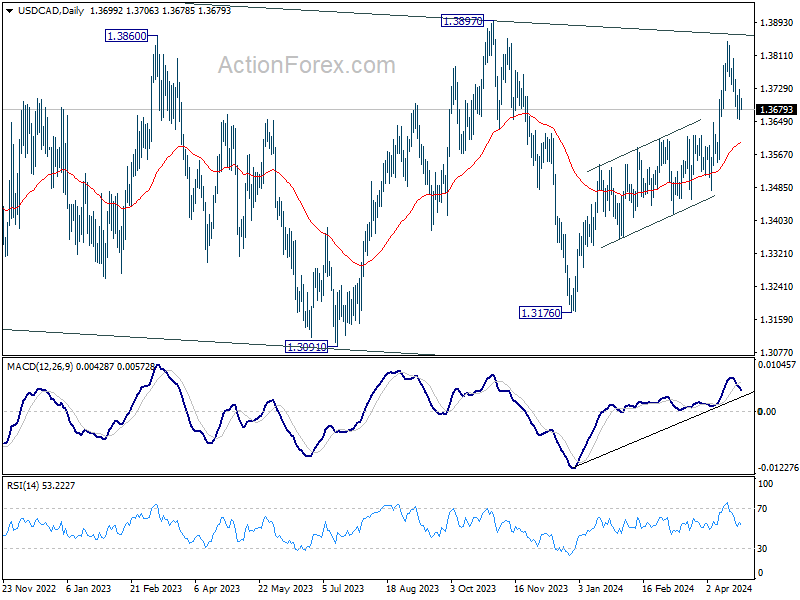

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3662; (P) 1.3696; (R1) 1.3736; More...

Intraday bias in USD/CAD stays neutral with focus on 1.3660 support. Strong rebound from current level will retain near term bullishness. Break of 1.3748 minor resistance will turn intraday bias back to the upside for retesting 1.3845 resistance. However, sustained break of 1.3660 will bring deeper fall to 55 D EMA (now at 1.3592) instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

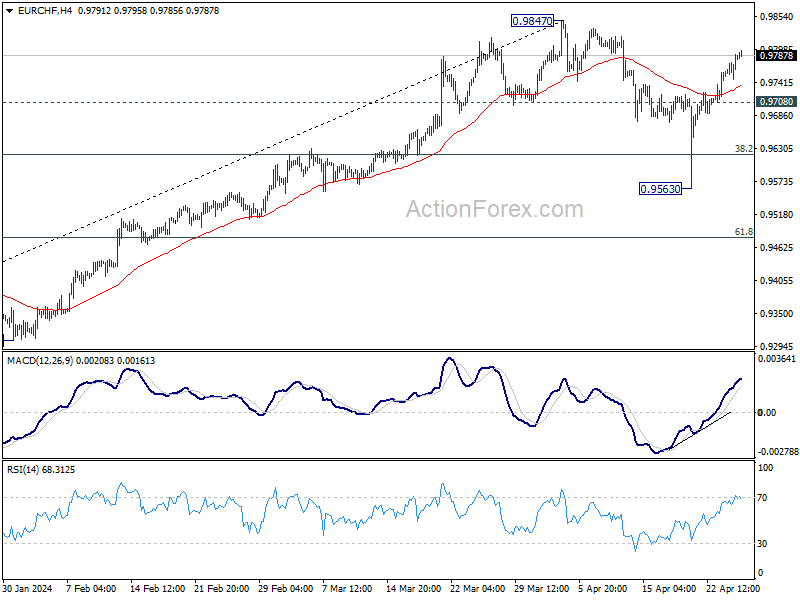

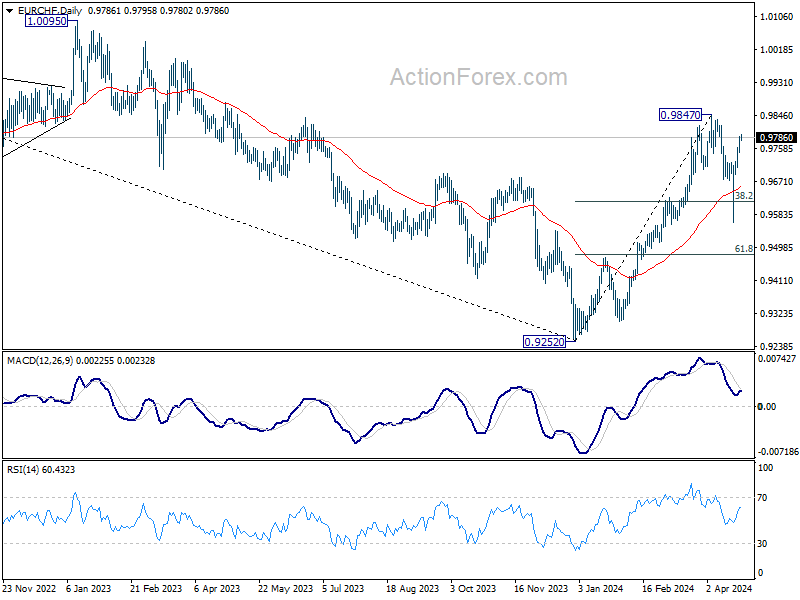

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9763; (P) 0.9778; (R1) 0.9808; More...

Intraday bias in EUR/CHF remains on the upside for retesting 0.9847 resistance. Decisive break there will resume larger rally from 0.9252 high. On the downside, below 0.9708 minor support will turn intraday bias neutral again first.

In the bigger picture, while 55 D EMA (now at 0.9655) was breached, EUR/CHF rebounded strongly since then. Rise from 0.9252 medium term bottom should still be in progress. Break of 0.9847 will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004. however, sustained trading below 55 D EMA will argue that the rebound has completed.

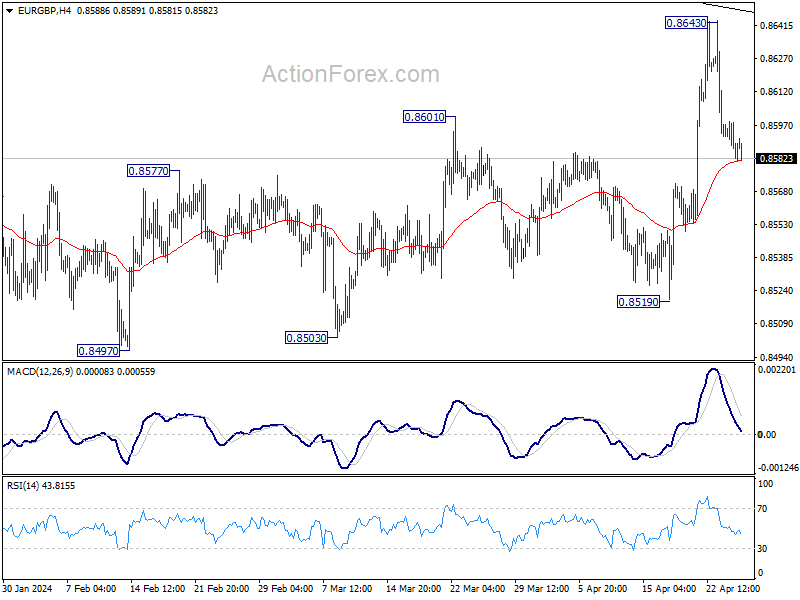

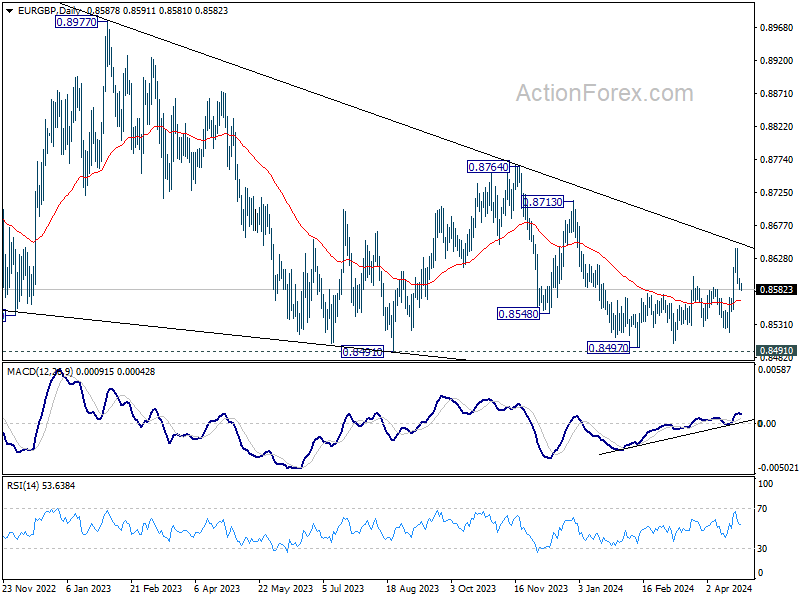

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8579; (P) 0.8589; (R1) 0.8595; More...

Intraday bias in EUR/GBP stays neutral at this point. On the upside, decisive break of medium term trend line resistance (now at 0.8649) will solidify the bullish case of trend reversal, and target 0.8764 resistance next. However, sustained break of 55 4H EMA (now at 0.8580) will indicate rejection by the trend line, and bring retest of 0.8491/7 support zone instead.

In the bigger picture, outlook is mixed up by current strong rebound. On the upside, sustained break of the trend medium term trend resistance will argue that the down trend from 0.9267 (2022 high) has completed as a triangle pattern. Further rise should then be seen through 0.8764 resistance next. However, rejection by the trend line will retain medium term bearishness for another fall through 0.8491 at a later stage.

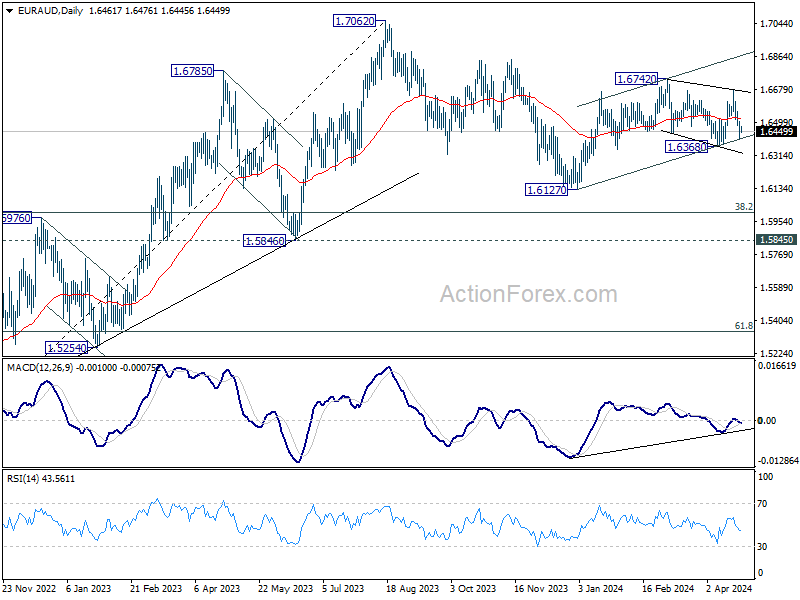

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6408; (P) 1.6467; (R1) 1.6525; More...

Intraday bias in EUR/AUD remains neutral at this point. On the downside, firm break of 1.6368 support will revive that case that rebound from 1.6127 has completed at 1.6742. Fall from there is seen as the third leg of the pattern from 1.7062. Deeper decline would then be seen to 1.6127 support and below.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of another fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

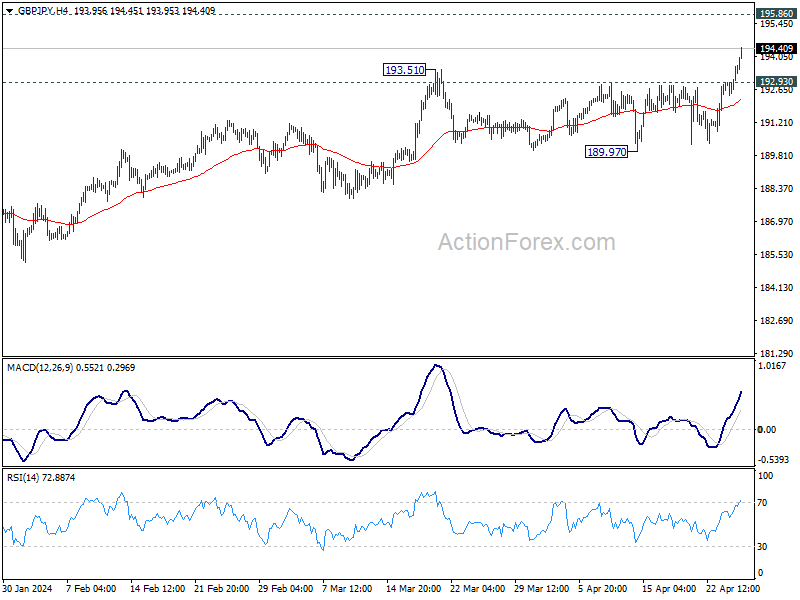

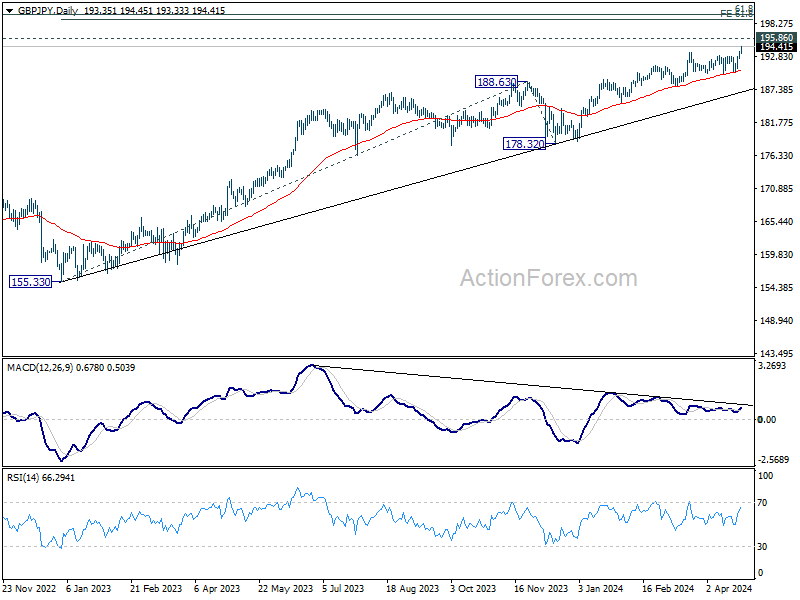

GBP/JPY Daily Outlook

Daily Pivots: (S1) 192.75; (P) 193.20; (R1) 194.07; More..

GBP/JPY's up trend resumed and reaches as high as 193.62 so far. Intraday bias is back on the upside for 195.86 long term resistance, and then 198.89 projection level. On the downside, below 192.93 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 189.97 support holds, in case of retreat.

In the bigger picture, current rally is part of the up trend from 123.94 (2020 low), and is in progress for 195.86 long term resistance (2015 high). Break there will target 61.8% projection of 155.33 to 188.63 from 178.32 at 198.89 next. Break of 189.97 support is needed to be the first sign of medium term topping. Otherwise, outlook will remain bullish in case of retreat.

Japanese Yen Moved Beyond USD/JPY 155 for the First Time Since 1990

Markets

Core bonds drifted away again yesterday. In the US, Treasuries reversed Tuesday’s (disappointing) PMI-induced spike higher. Weakening demand and a slight tail at the US Treasury’s record $70bn 5-yr Note sale kept UST’s near intraday lows going into the close. The longer end of the curve underperformed with the front end locked in the run-up to next week’s FOMC meeting and following a sharp, higher for longer, repositioning since mid-March. We argued before that at least some part of the market/investor community needs to be contemplating a rate hike instead of a cut as the Fed next move to push the US 2-yr yield back above the psychological 5% mark. US yields eventually added up to 4.4 bps for the 30-yr gauge which tested the YTD top at 4.8%. German Bunds extended their (consensus-beating Ifo) underperformance. German yield increased by 4.9 bps (2-yr) to 8.2 bps (30-yr). Unlike in the US, European money markets are still banking on (at least) three 25 bps ECB rate cuts this year. We continue to err on the hawkish side of this prognosis. The German 10-yr yield touched 2.6% for the first time since the end of November of last year. This level coincides with 62% retracement on the Q4 setback in yields. A break higher would be technically significant, opening the path for a full return to 3%. Contrary to Tuesday, EUR/USD failed to profit from the interest rate advantage with the pair closing near unchanged at 1.07. Major US and EMU equity benchmarks closed with minor losses.

Overnight risk sentiment is strongly negatively impacted by a disappointing outlook in Q1 Meta earnings. Nasdaq futures suffer losses of 1.5%. Main Japanese and South Korean bourses record similar losses. The risk environment doesn’t translate into stronger US Treasuries or a dollar, which both trade rather stable. The Japanese yen moved beyond USD/JPY 155 for the first time since 1990 yesterday with the pair currently changing hands at 155.66 in the run-up to tomorrow’s BoJ policy meeting (including new growth and inflation forecasts). We don’t think that any “hawkish” hints on “more” policy normalization down the road will be sufficient to save the ailing currency. It will likely take another hit which could prompt officials to move from verbal to effective interventions. As seen in the (recent) past, such moves often offer only temporary relief without backing from the BoJ.

News & Views

National Bank of Poland (NBP) policymaker Kotecki said that recent softer data is slowly tilting the interest rate debate in Poland toward rate cuts. Kotecki’s base scenario nevertheless remains one where interest rates stay at current level until the end of this year. Recent macro indicators “minimally increase the probability of a rate cut, since it’s clear that the economy isn’t accelerating and is far from overheating”. After touching 2% in March, Kotecki expects inflation to be between 5.5% and 6% at the end of the year as the government scaled back subsidies to mitigated energy bills. In this scenario, the NBP could start discussing mild rate cuts if at the end of the year if inflation data show price growth returning to the NBP’s target ‘for good’ in H2 2025 or in early 2026. After a 1% cumulative rate cuts in September and October last year, the NBP since then kept its policy rate unchanged at 5.75% and indicated that rates were likely to stay on hold as inflation risks persist.

South Korean growth beat expectations by a wide margin this morning. Activity accelerated to 1.3% Q/Q in Q1 2024 (vs 0.6% consensus) from 0.6% in Q4 2023, raising Y/Y growth from 2.2% to 3.4%. Growth in domestic demand was an important driver behind the solid growth performance with private expenditure rising 0.8% Q/Q. Government expenditure (0.7% Q/Q) and construction investment also added to the strong performance. Export growth continued at a solid 0.8% Q/Q. In a sector approach, manufacturing (1.2% Q/Q), construction (4.8% Q/Q) and services (0.7%) all show strong figures. In a first reaction, the Bank of Korea took a cautious approach. It admitted that growth seems to be stronger than int the February forecast and that current data will be incorporated in the new update in May. Still the BoK considers it too early to say if consumption has turned the corner. In March the BoK already acknowledged that there could be upside risk to its 2.1% forecast for this year. The BoK currently holds its policy rate at 3.5%. Stronger data might delay rate cuts that were expected for H2 this year.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June?) rate cut and seems to have broad backing. EMU disinflation will continue the next two months and bring headline CPI (temporary) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up move difficult.

US 10y yield

The March dot plot contained several hawkish elements including a symbolically higher neutral rate. In our view they set the stage for a later (September at the earliest) start of a possibly shallower cutting cycle. Upcoming CPI readings (through base effects) and resilient eco data should confirm this. US yields continue to enjoy a solid bottom across the maturity spectrum, setting fresh YTD highs.

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a technical break, opening the path to last year’s low at 1.0494.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

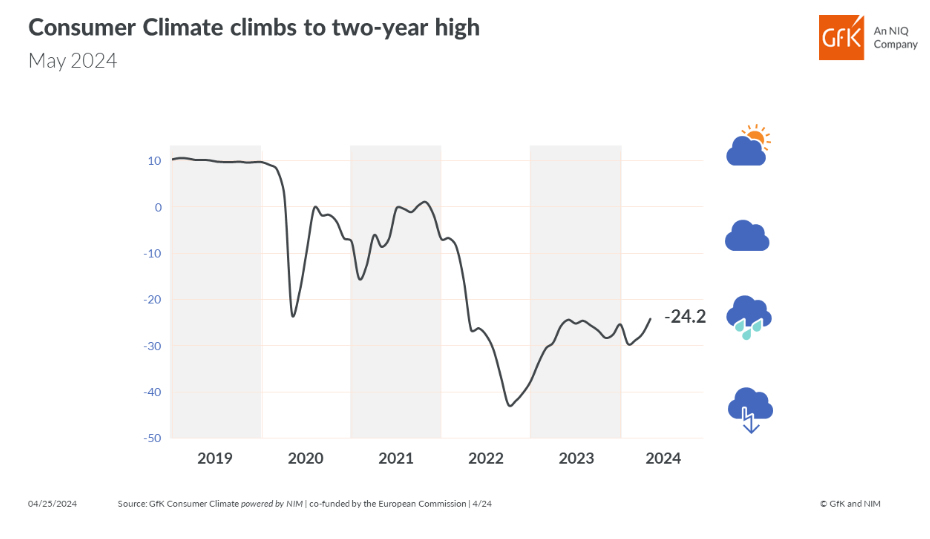

Germany’s Gfk consumer sentiment rises to -24.2, an extremely low two-year high

German Gfk Consumer Sentiment for May rose from -27.3 to -24.2, above expectation of -25.5. This marks the highest level in two years, although it remains significantly low by historical standards.

In April, economic expectations rose from -3.1 to 0.7. Income expectations rose from -1.5 to 10.7. Willingness to buy rose from -15.3 to -12.6. Willingness to save rose from 12.4 to 14.9.

Rolf Bürkl, consumer expert at NIM, attributed the stronger uplift in consumer sentiment mainly to the "noticeable increase in income expectations." He elaborated that these expectations are closely tied to actual developments in real income, buoyed by rising wages and salaries alongside recent dip in inflation rates. This combination has laid a solid foundation for increasing purchasing power among households.

High Expectations Play Tricks on Big Tech

Meta revealed better than expected earnings, a more-than-doubled profit from last year and a 27% rise in sales. Oh, and the revenue growth was up for the fifth quarter. But the share price tumbled 15% in the afterhours trading as investors didn’t like the weaker-than-expected revenue forecast for the current quarter and even less the news that the company will be spending more money to improve its AI capabilities. Meta is now expected to spend around $35 to 40 billion, versus $30-37 billion they said they would spend earlier. In fine, these investments will help the company keep more people longer on their platform and increase their ad revenue with a more intelligent and customized advertisement strategy, but additional spending news comes at a time investors were expecting Meta to start throwing magnificent results into the mix. And all we got is a lower revenue outlook and more spending. Price-wise, Meta will likely slip below its uptrending range building since end of 2022; it’s certainly not the end of the AI hype for Meta, but it’s sure a short-term disappointment.

Google, Microsoft and Intel are due to report today.

So far, we observe that the high expectations have played tricks on stock valuations and the first set of earnings reactions warn that even strong results from Big Tech may not suffice to send their stock prices higher – if we start seeing growth expectations level out. (I am looking at you Microsoft and Nvidia.)

Zooming out, the stumbling giant Meta is weighing on the mood this morning. US futures are down and the technology-heavy Nasdaq is leading losses with more than 1% fall at the time of writing.

The macroeconomic landscape is complex, with investors balancing between robust GDP growth and high earnings expectations for the Big Tech companies, all while considering the fading expectations for a Federal Reserve's (Fed) rate cut. A strong GDP reading would suggest that the US economy is sufficiently strong to support corporate earnings, but it could also delay expectations for a Fed rate cut. Conversely, a softer-than-expected GDP figure would likely increase expectations for a rate cut, especially if earnings disappoint due to inflated expectations. Overall, I believe that a softer-than-expected GDP would elicit a more positive market reaction, but the risks surrounding GDP lean towards a better-than-expected reading. According to a consensus of analyst estimates on Bloomberg, Q1 growth is expected to be around 2.5%, while the Atlanta Fed’s GDPNow projection stands at approximately 2.7%.

The US dollar index rebounded yesterday after trading near a two-week low. The EURUSD remained bid into the 1.0680 support, fueled by better than expected German sentiment data – which showed that business sentiment rose to the highest level in a year. But a set of rating assessments are expected to challenge the rising debt risks in France and Italy, and could limit the upside potential along with a potentially stronger US dollar dependent on today’s first glimpse at the Q1 growth.

The dollar appreciation is a problem for many economies, but it has become a major headache for the Bank of Japan (BoJ). The USDJPY spiked and extended gains above the 155 mark. The BoJ will lean on to the USD strength at this week’s policy meeting and will – potentially – intervene to slow the yen selloff. What’s interesting is that we know that next hours will likely bring an announcement to tackle the yen depreciation, but the yen shorts are not afraid. They know that an FX intervention alone won’t reverse the yen’s falling course unless accompanied by a hawkish BoJ policy outlook. Therefore, even an intervention could backfire and fail to prevent a further rise in USDJPY to the 160 level.