Sample Category Title

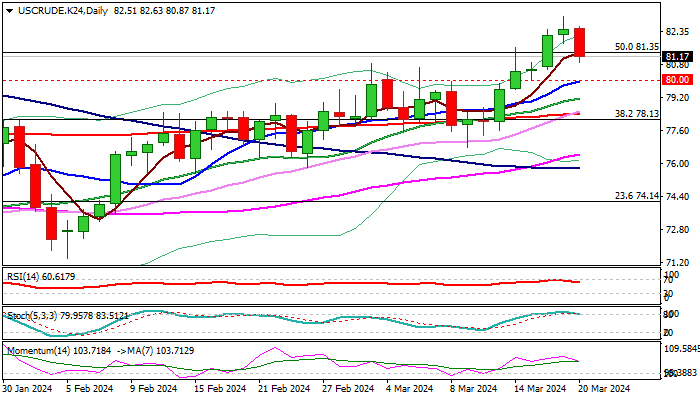

WTI Oil Price Falls on Profit Taking from New Multi-Month High

WTI oil price pulls back from new 4 ½ month high ($83.10), down 1.6% for the day so far, as traders collected profits ahead of Fed policy announcement.

The oil price accelerated higher recently on fresh concerns about oil supply, following attacks on Russian refining installations and persisting threats of stronger disruptions.

Stronger than expected drop in crude inventories (API report) and lower build in crude stocks compared to the previous week (EIA report) contributes to signals of a healthy demand, with improving economic data from the world’s largest oil importer China, adding to supportive factors.

From the technical point of view, oil price continues to move within a larger uptrend from $67.70 (Dec 2023 low), with daily studies being firmly bullish, but overbought, which sparked the latest sell-off.

Pullback is likely to be a shallow and ideally to be contained by psychological $80.00 support, reinforced by rising 10DMA, though deeper drop cannot be ruled out, with extended dips to find ground above $78.63/43 (Fibo 38.2% of $71.40/$83.10 / 200DMA respectively) to mark a healthy correction and keep larger bulls in play.

Res: 82.63; 83.10; 83.58; 84.57

Sup: 80.34; 80.00; 79.15; 78.63

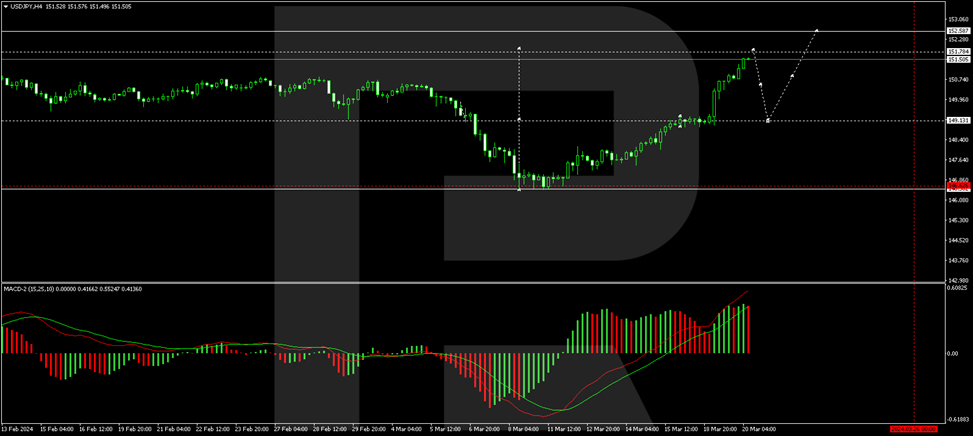

Japanese Yen (USD/JPY) Hits Four-Month Low

The USD/JPY pair surged to a four-month high as investors recalibrated their expectations for the Bank of Japan's future actions. The consensus is now that the BoJ's monetary policy will remain accommodative, even with the shift away from negative interest rates.

On Tuesday, the Bank of Japan announced its first interest rate hike in 17 years, indicating its expectation to observe favorable fiscal conditions for some time. However, the yen remains under pressure due to the significant interest rate differential between Japan and the United States.

Japan's negative interest rate period extended over eight years. The recent decision marks a historic move following a prolonged phase of quantitative monetary easing.

The market generally believes that the Bank of Japan's transition to a stable monetary policy is far from complete. This perspective is supported by the BoJ's "soft" statements and the subsequent reaction of the JPY.

The yen plunged by 1% against the US dollar immediately following the BoJ's decision and continues to weaken. The upward trend in the USD/JPY pair began in early January 2024 and has remained strong.

USD/JPY technical analysis

The H4 USD/JPY chart shows a consolidation range formed around the 149.13 level. With an upward breakout, the pair continues to develop a growth wave towards 151.77. A correction phase to 150.00 could follow, then a rise to 152.60. The MACD oscillator supports this scenario, with its signal line strictly pointing upwards and aiming for new highs.

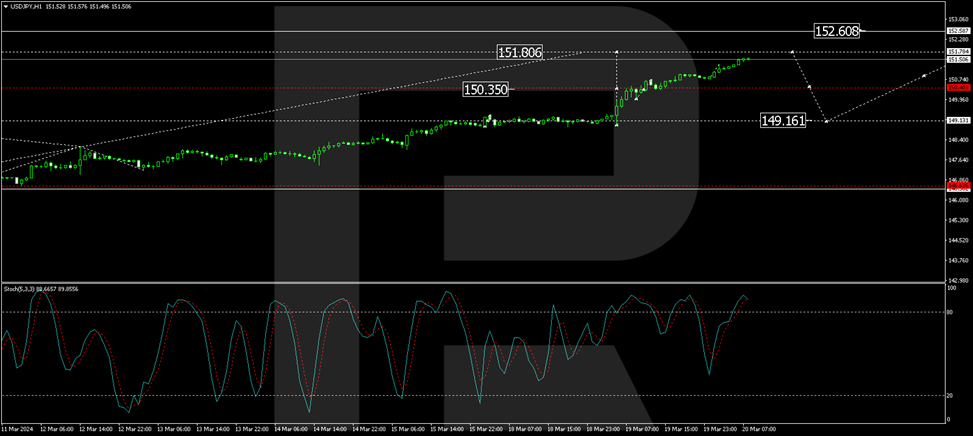

On the H1 USD/JPY chart, a narrow consolidation range has developed around the 150.40 level. Exiting upwards from this range, the growth wave continues towards 151.78. After reaching this level, a potential correction back to 150.40 (testing from above) is considered, followed by a new growth structure towards 152.60. The Stochastic oscillator corroborates this scenario, with its signal line above the 80 mark and preparing to drop to 50.

Sunset Market Commentary

Markets

The ECB and its Watchers XXIV conference and UK February CPI data provided a welcome interlude counting down to tonight’s Fed decision. ECB Lagarde basically held to the recent communication line. Moving into the dial back phase requires wage growth to slow further, a continued decline in inflation towards 2% and a confirmation in new internal projections. This suggests that the June meeting is the preferred time to start the easing cycle. ”Our decisions will have to remain data dependent and meeting-by-meeting, responding to new information as it comes in”. In this framework, the ECB isn’t able to pre-commit to a particular rate path, even after the first rate cut. Executive Board member Schnabel elaborated on a potential higher neutral rate due to structural factors including the climate transition, the digital transformation and changes in the geopolitical context. The comments had no lasting impact on European interest rate markets. In German yields trade between flat (2-y) and -2.5 bps (30-y).

UK February inflation data were close to expectations. Headline inflation eased to 0.6% M/M and 3.4% Y/Y from 4% (vs 3.5% expected). Core inflation also declined slightly more than expected to 4.5% from 5.1%. However, services inflation remains stubbornly hight at 6.1%. UK gilts are marginally outperforming US Treasuries and Bunds, declining between 1.5 bps (2-y) and 3 bps (5 & 10-y). Question remains whether these data are sufficient for the BoE to become more specific in its timing of rate cuts when they announce their policy decision tomorrow. Recall the MPC was highly divided in February. 6 members voted to leave the policy rate unchanged. Two members still considered it necessary to raise the policy rate (25 bps) as inflation remains too long above the target. On the other hand, one member already vote to cut rates. Money markets still see a first BoE rate cut at the August meeting. Looking at sterling, today’s inflation data didn’t inspire markets to prepare for a dovish twist. EUR/GBP briefly ‘jumped’ to the 0.8855 area immediately after the release, but EUR/GBP currently even trades marginally lower at 0.854.

US interest rate markets are almost paralyzed in the run-up to the Fed decision, with yield changes less than one bp across the curve. The dollar succeeds some follow through gains (DXY 104.1, EUR/USD 1.085). USD/JPY (151.75) is only a whisker away from the 2023 top. Equites, both in Europe and the US are little changed. With respect to the Fed meeting, markets look out whether/to what extent stubbornly high inflation will force Powell and co to upwardly revise their inflation forecasts and whether 3 rate cuts (25 bps) this year is still the mainstream scenario. We see no reason for the Fed to inspire markets to front-run on its easing cycle. On the contrary.

News & Views

Belgian consumer confidence held steady at -5 in March after wiping out an uptick towards the end of last year over the past two months. In the National Bank of Belgium’s survey, households displayed more pessimism in March about the outlook for the labour market over the next twelve months. Fears of a rise in unemployment popped up again even if there was little change in the expectations for the general economic situation. On a personal level, while their expectations for their own future financial situation remained virtually unchanged, households have raised their savings intentions, which had dipped last month. It’s this latter component that compensated for a worsening labour market outlook, resulting in the unchanged -5 headline figure.

Leo Varadkar unexpectedly announced his resignation as both Irish Prime Minister and leader of the governing Fine Gael party. Varadkar said there was no “real reason” behind his departure but it does come after the government suffered twin defeats in Irish referenda, for which the outgoing premier took responsibility. His party is also sliding in the polls to the benefit of Sinn Fein over Ireland’s acute housing crisis and concerns over immigration. Varadkar’s resignation doesn’t necessarily trigger general elections, which are scheduled for March 2025. He asked for a new leader of the party to be chosen on April 6 with the new prime minister then to be elected after parliament’s Easter break.

Will JP 225 Index Continue Its Record Rally?

- JP 225 index flirts with all-time highs

- Short-term technical signals remain encouraging

Japan’s 225 stock index (cash) is on the rise again, aiming to revive its five-month-old positive trend above the March record high of 40,564 after finding support near the 38,310 area.

The technical signals favor the upward move in the price as the RSI is sloping northwards and is still some distance off its 70 overbought mark. The stochastic oscillator continues to trend up, and the MACD is looking to rise above its red signal line, both backing the bullish scenario too.

If the market enters uncharted territory, the bulls could temporarily stop inside the 41,400-42,000 range, which is defined by two upward trendlines. Running higher, the index could gear up to 44,211, where the 261.8% Fibonacci extension of the latest downfall is positioned.

On the downside, the 20-day simple moving average (SMA) could come first into view at 39,432 ahead of the ascending trendline at 38,884. A break below the latter could lose steam somewhere between the 23.6% Fibonacci retracement of the five-month-old upleg at 38,160 and the 50-day SMA at 37,826. If the bears win the battle there, the door could open for the 37,000 round level and the 38.2% Fibonacci of 36,674.

Summing up, the uptrend in Japan’s 225 stock index may have more legs to continue higher in the coming sessions, with the confirmation signal expected to come above 40,564.

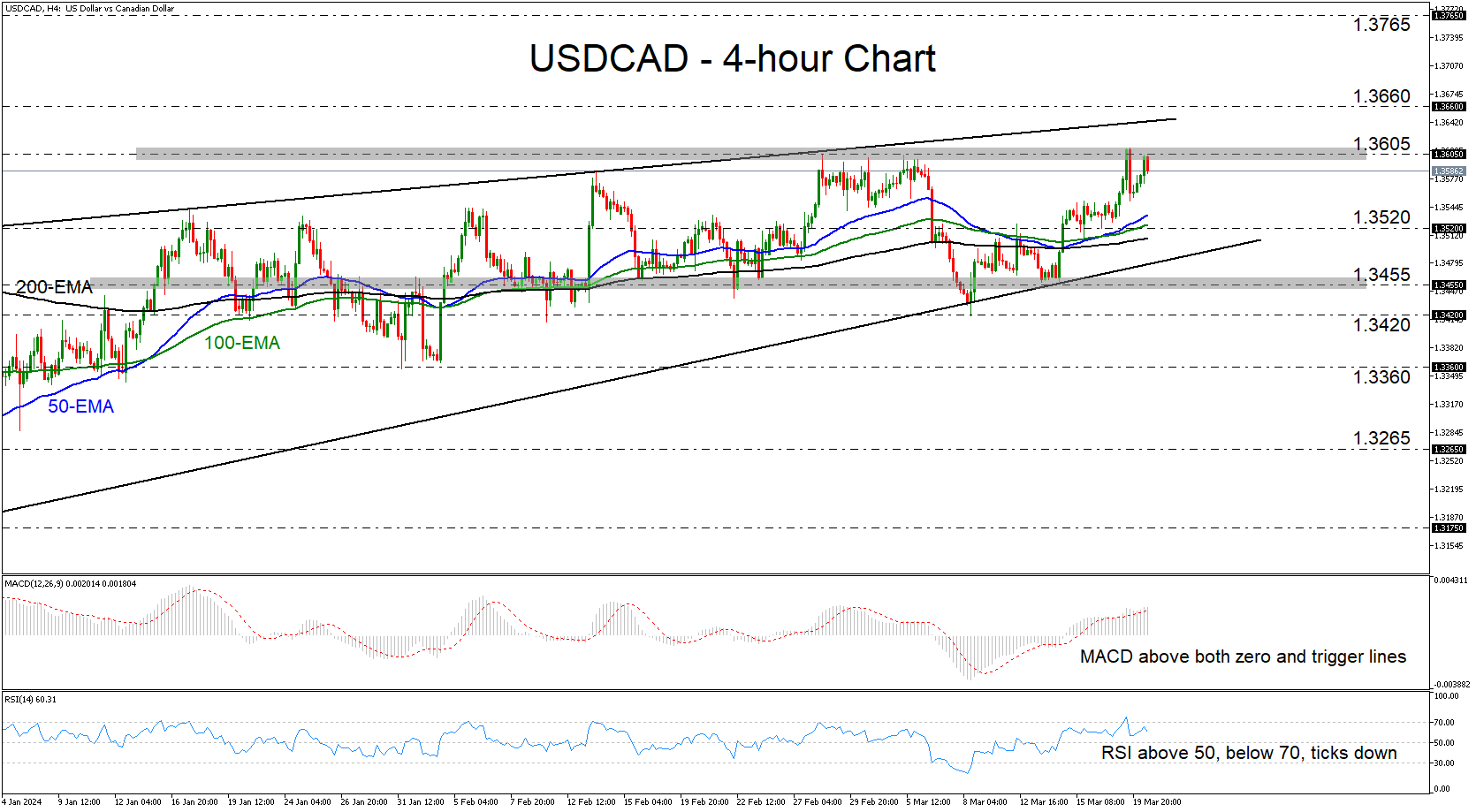

Time for USDCAD to Go for a Higher High?

- USDCAD rises after cooler than expected Canadian inflation

- A break above 1.3605 could signal uptrend continuation

- For the outlook to turn bearish, a dip below 1.3455 may be needed

USDCAD rose yesterday after the Canadian CPI numbers came in lower than expected. However, the pair found resistance near the key barrier of 1.3605 that’s been preventing the price from moving higher since February 28, and then it pulled back. Today, the bulls retook charge, but they were stopped near the 1.3605 obstacle again.

The MACD is lying above both its zero and trigger lines, detecting positive momentum, but the RSI, although above 50, ticked down from slightly below its 70 line. The RSI corroborates the notion that a break above 1.3605 may be needed for the outlook to brighten.

Such a break would confirm a higher high on all time frames and perhaps allow extensions towards the upside resistance line drawn from the high of January 17, or towards the 1.3660 barrier, which was last tested on November 27. If the bulls are not willing to stop there either, then they may climb all the way up to the 1.3765 territory marked by the high of November 22.

For the outlook to darken, the pair may need to slip all the way below the key support area of 1.3455. Such a dip would also confirm the break below the upside support line taken from the low of December 29. The bears may then aim for the 1.3420 barrier, the break of which could carry extensions towards the low of January 31 at around 1.3360.

Recapping, USDCAD moved higher after Canada’s lower than expected inflation numbers, but it is struggling to overcome the key resistance of 1.3605. Only a decisive break above that zone could be considered as a trend continuation signal.

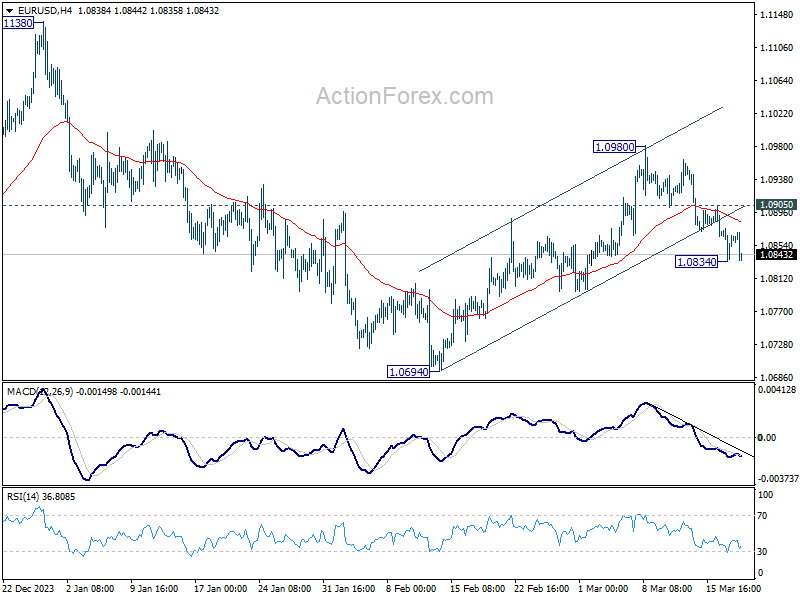

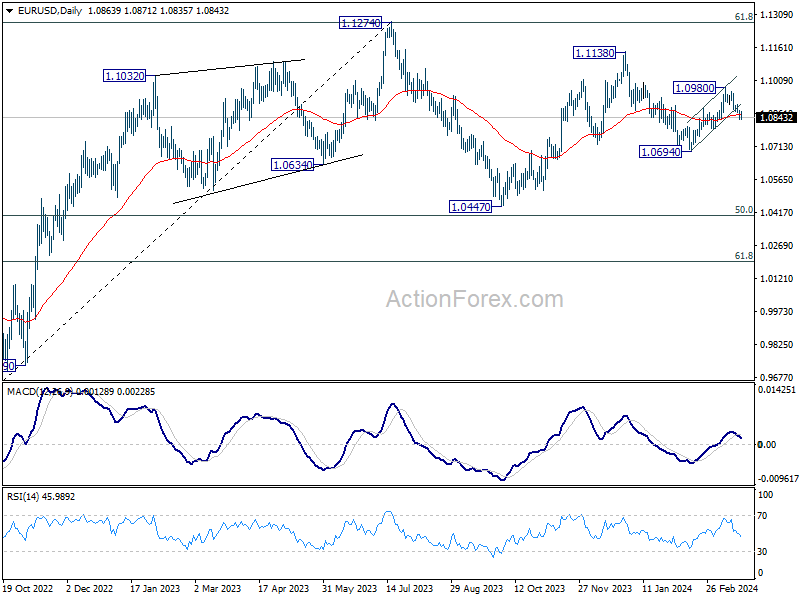

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0842; (P) 1.0859; (R1) 1.0884; More...

Intraday bias in EUR/USD remains neutral for consolidation above 1.0834 temporary low. Further decline is in favor as long as 1.0905 resistance holds. On the downside, sustained trading below 55 D EMA (now at 1.0856) will argue that rebound from 1.0694 has completed and bring retest of this low. However, above 1.0905 will turn bias back to the upside for 1.0980 resistance instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

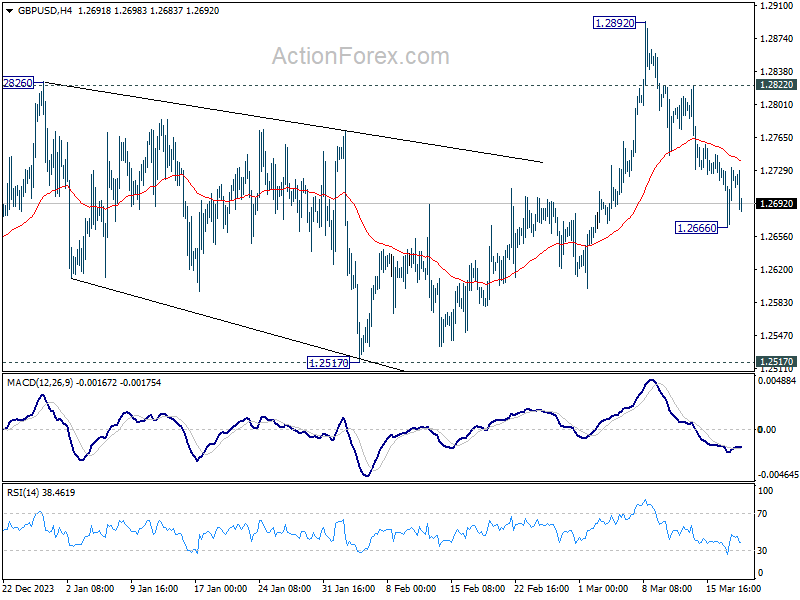

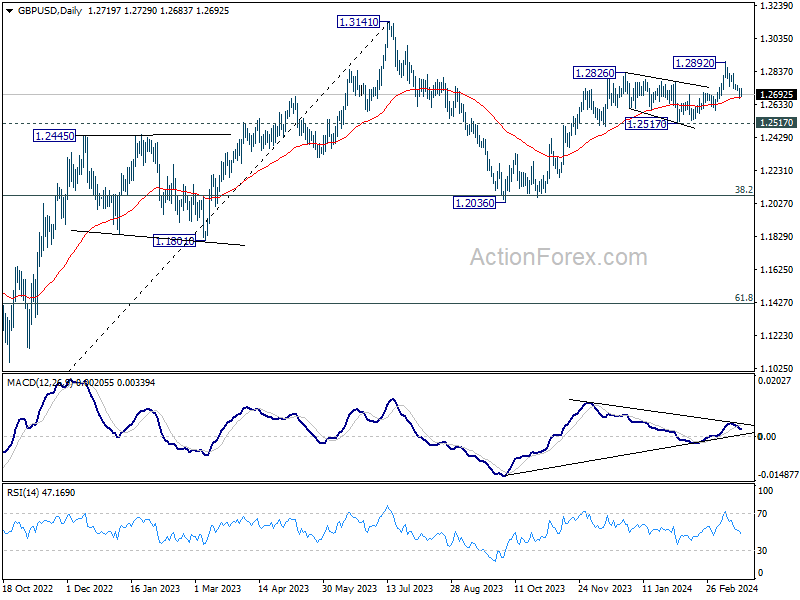

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2681; (P) 1.2708; (R1) 1.2747; More...

Intraday bias in GBP/USD remains neutral for consolidations above 1.2666 temporary low. Deeper decline is still in favor as long as 1.2822 resistance holds. On the downside, sustained break of 55 D EMA (now at 1.2677) will target 1.2517 structural support next.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

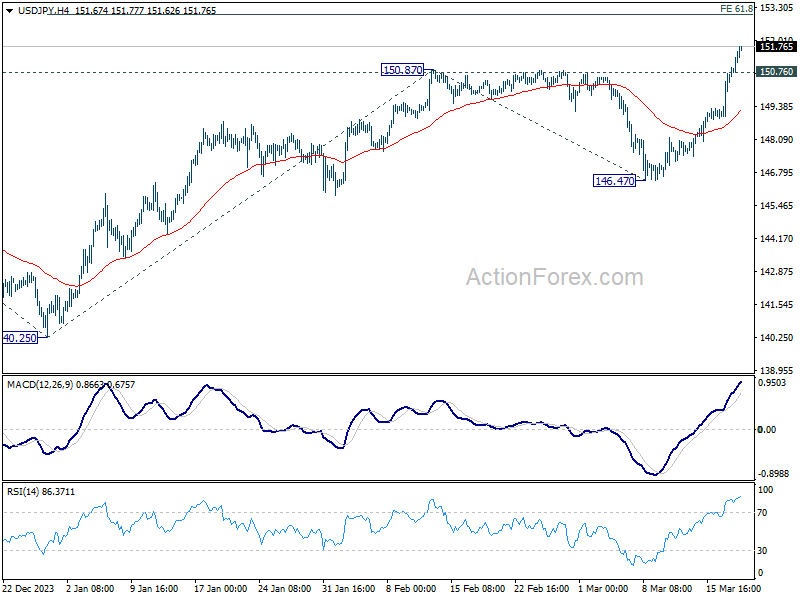

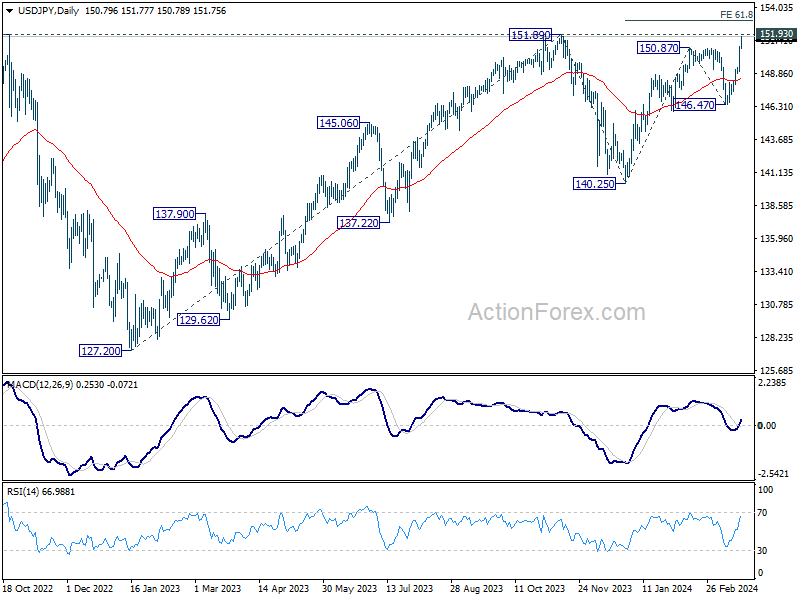

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.58; (P) 150.27; (R1) 151.55; More...

Intraday bias in USD/JPY remains on the upside at for 151.93 key resistance. Decisive break there will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. On the downside, below 150.76 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 55 4H EMA (now at 149.18) holds.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

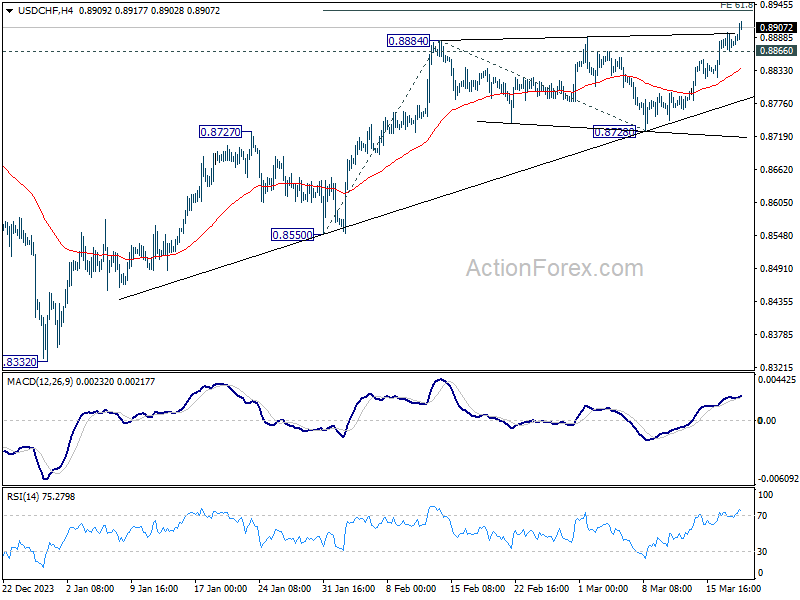

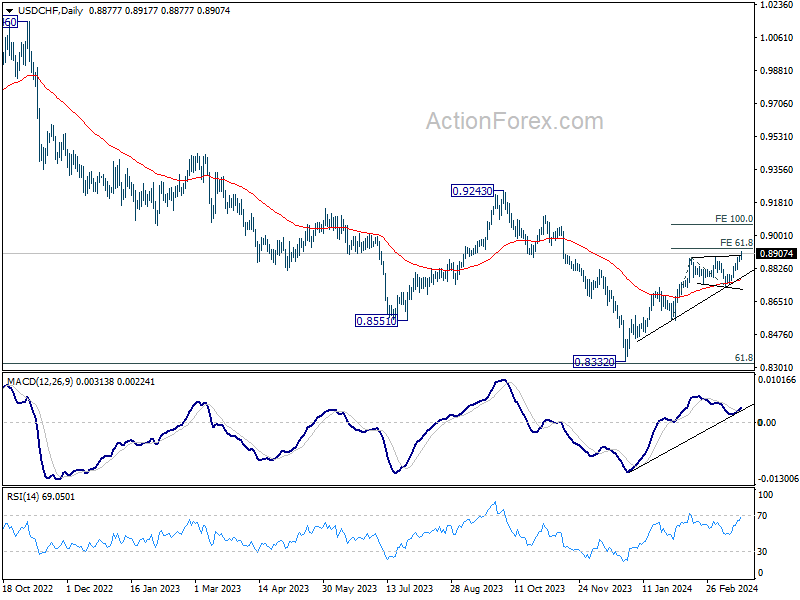

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8866; (P) 0.8882; (R1) 0.8898; More....

USD/CHF's rally from 0.8332 is still in progress and intraday bias stays on the upside for 61.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8934. Firm break there will target 100% projection at 0.9062 next. On the downside, break of 0.cminor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Dollar Holds Strength Ahead of Fed Dot Plot Update

Dollar stands firm as the day's strongest currency, with the financial markets on edge for the Fed's impending announcement. While interest rate is widely anticipated to hold steady at 5.25-5.50%, the spotlight is on the potential adjustments to Fed's dot plot. December's projections hinted at three rate cuts for the year, yet the consensus was narrowly divided—11 members forecasting three or more cuts, against 8 envisaging two or fewer. A pivotal shift of just two dots could recalibrate expectations to merely two rate cuts, a scenario that could bolster Dollar, at least in the short term.

In the broader market context, Australian and Canadian Dollars trail behind Dollar by some distance. Yen languishes as the day's weakest currency, followed closely by Kiwi. European majors, with Euro slightly ahead, occupy the middle ground, even as ECB President Christine Lagarde reaffirms conditional guidance towards a June rate cut. Swiss Franc faces downward pressure, partly due to risks of a dovish surprise SNB tomorrow. Sterling's progress is tempered by CPI figure that fell short of expectations and the looming BoE decision, also due tomorrow.

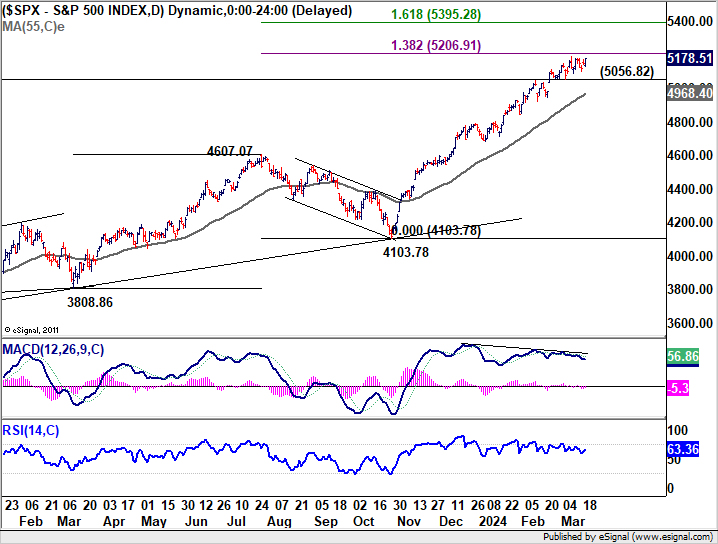

Technically, stock markets' reactions to FOMC are also important to monitor. Bearish divergence condition in D MACD in S&P 500 is a factor that could cap its rally at 138.2% projection of 3808.86 to 4607.07 from 4103.78 at 5206.91. Break of 5056.82 support will confirm short term topping and bring deeper correction to 55 D EMA (now at 4968.40). Nevertheless, decisive break of 5206.91 would pave the way to 161.8% projection at 5395.28 before topping.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is up 0.20%. CAC is down -0.64%. UK 10-year yield is down -0.0320 at 4.133. Germany 10-year yield is down -0.0228 at 2.433. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.08%. China Shanghai SSE rose 0.55%. Singapore Strait Times rose 0.12%.

ECB's Lagarde sets conditions for June rate cut

ECB President Christine Lagarde provided clarity in a speech on the conditions that would lead to a rate cut in June, highlighting reliance on "two important pieces of evidence" as pivotal to the central bank's confidence on dialing back monetary restrictions. .

Firstly, ECB anticipates receiving data on negotiated wage growth for Q1 by the end of May. Secondly, by June, ECB will have access to a new set of economic projections, enabling it to verify the validity of the inflation path forecasted in its March projection.

After the first move, Lagarde emphasized to "confirm on an ongoing basis" that incoming data aligns with its inflation outlook. This approach underscores a commitment to data-driven policy decisions, maintaining a "meeting-by-meeting" stance that eschews any pre-commitment to a fixed rate path.

Furthermore, Lagarde noted the enduring significance of ECB's policy framework in processing incoming data and determining the appropriate policy stance. However, she also mentioned that the relative importance of the three criteria guiding these decisions would require regular reassessment.

UK CPI slows to 3.4% in Feb, core down to 4.5%

UK CPI slowed from 4.0% yoy to 3.4% yoy in February, below expectation of 3.5% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 5.1% yoy to 4.5% yoy, below expectation of 4.6% yoy.

CPI goods annual rate slowed from 1.8% yoy to 1.1% yoy, while CPI services annual rate eased from 6.5% yoy to 6.1% yoy.

On a monthly basis, CPI rose 0.6% mom, below expectation of 0.7% mom.

New Zealand Westpac consumer confidence rises to 93.2 in Q1, yet pessimism lingers

New Zealand Westpac Consumer Confidence rose from 88.9 to 93.2 in Q1, marking its highest level in over two years. Despite this rise, the index continues to hover below the pivotal 100 mark, indicating prevailing sense of pessimism among New Zealanders regarding economic conditions. Present Conditions Index saw significant uplift from 77.1 to 85.1, while Expected Conditions Index advanced modestly from 96.7 to 98.6.

Westpac's analysis highlights that households are gradually feeling more optimistic about their financial situations, which has subsequently spurred an increase in "spending appetites". This positive shift in consumer sentiment is observed across all income brackets, with "middle-income households exhibiting" the most marked improvement.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8866; (P) 0.8882; (R1) 0.8898; More....

USD/CHF's rally from 0.8332 is still in progress and intraday bias stays on the upside for 61.8% projection of 0.8550 to 0.8884 from 0.8728 at 0.8934. Firm break there will target 100% projection at 0.9062 next. On the downside, break of 0.8866 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q1 | 93.2 | 88.9 | ||

| 21:45 | NZD | Current Account (NZD) Q4 | -7.84B | -7.80B | -11.47B | -10.97B |

| 07:00 | EUR | Germany PPI M/M Feb | -0.40% | -0.20% | 0.20% | |

| 07:00 | EUR | Germany PPI Y/Y Feb | -4.10% | -3.80% | -4.40% | |

| 07:00 | GBP | CPI M/M Feb | 0.60% | 0.70% | -0.60% | |

| 07:00 | GBP | CPI Y/Y Feb | 3.40% | 3.50% | 4.00% | |

| 07:00 | GBP | Core CPI Y/Y Feb | 4.50% | 4.60% | 5.10% | |

| 07:00 | GBP | RPI M/M Feb | 0.80% | 0.80% | -0.30% | |

| 07:00 | GBP | RPI Y/Y Feb | 4.50% | 4.50% | 4.90% | |

| 07:00 | GBP | PPI Input M/M Feb | -0.40% | 0.20% | -0.80% | -0.10% |

| 07:00 | GBP | PPI Input Y/Y Feb | -2.70% | -2.70% | -3.30% | -2.80% |

| 07:00 | GBP | PPI Output M/M Feb | 0.30% | 0.10% | -0.20% | 0.00% |

| 07:00 | GBP | PPI Output Y/Y Feb | 0.40% | -0.10% | -0.60% | -0.30% |

| 07:00 | GBP | PPI Core Output M/M Feb | 0.20% | 0.20% | 0.30% | |

| 07:00 | GBP | PPI Core Output Y/Y Feb | 0.30% | -0.40% | -0.30% | |

| 09:00 | EUR | Italy Industrial Output M/M Jan | -1.20% | 0.10% | 1.10% | |

| 14:30 | USD | Crude Oil Inventories | -0.9M | -1.5M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | -15 | -16 | ||

| 17:30 | CAD | BoC Summary of Deliberations | ||||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |