Sample Category Title

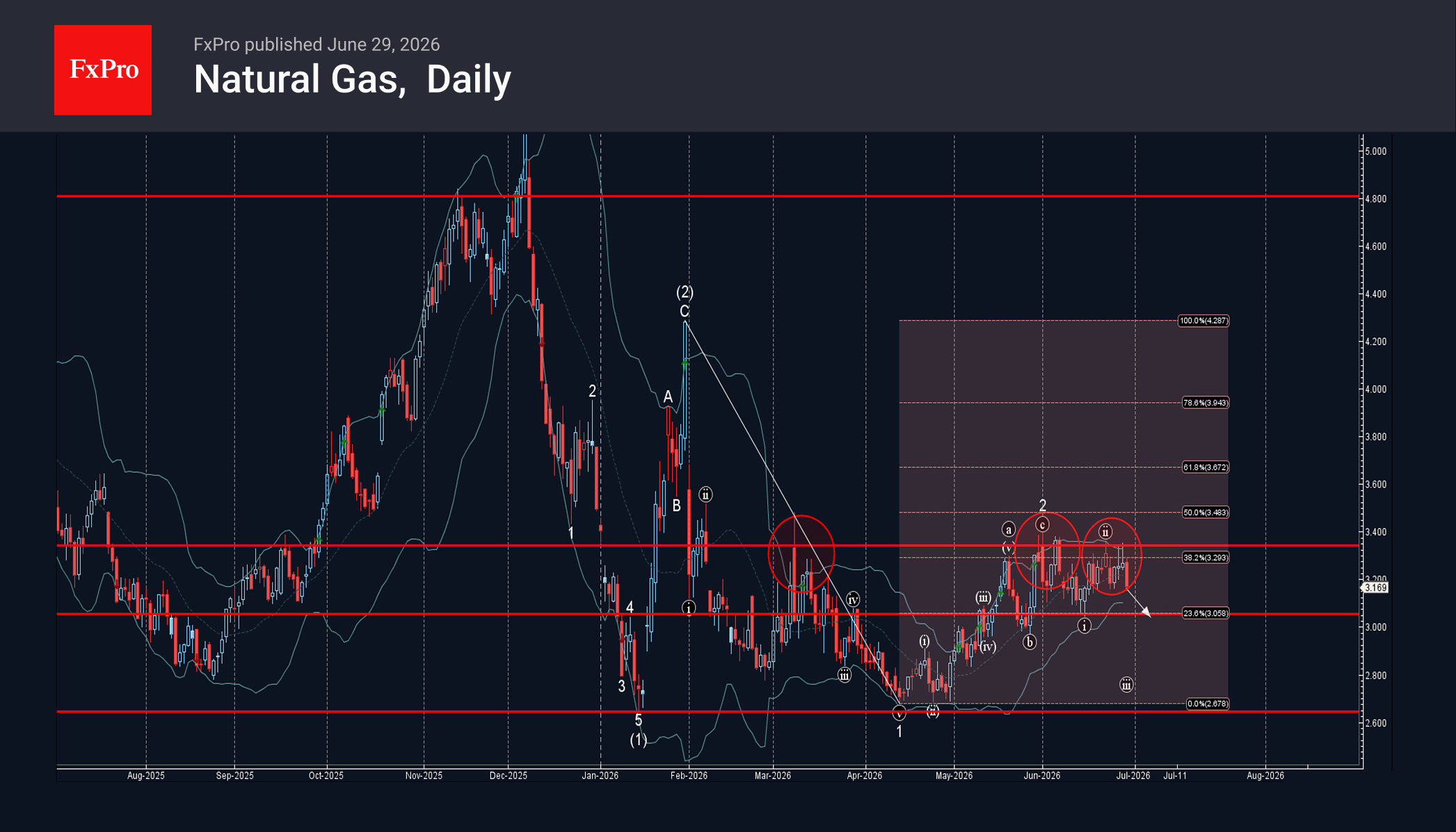

Natural Gas Wave Analysis

Natural Gas: ⬇️ Sell

– Natural Gas reversed from resistance zone

– Likely to fall to support level 3.055

Natural Gas recently reversed from the resistance zone between the pivotal resistance level 3.34 (which has been reversing the price from March), 38.2% Fibonacci correction of the downward impulse from January and the upper daily Bollinger Band.

The downward reversal from this resistance zone is likely to form the daily Japanese candlesticks reversal pattern Evening Star.

Given the clear daily downtrend, Natural Gas can be expected to fall to the next support level 3.055 (low of the previous minor impulse wave i).

Eco Data 6/30/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | 1.20% | 1.30% | 1.20% | |

| 23:30 | JPY | Unemployment Rate May | 2.50% | 2.50% | 2.50% | |

| 23:50 | JPY | Industrial Production M/M May P | 0.50% | 0.60% | 0.50% | |

| 01:00 | NZD | ANZ Activity Outlook Jun | 36.9 | 25.6 | ||

| 01:00 | NZD | ANZ Business Confidence Jun | 36.6 | 10 | ||

| 01:30 | AUD | Private Sector Credit M/M May | 0.70% | 0.60% | 0.70% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 01:30 | CNY | NBS Manufacturing PMI Jun | 50.3 | 50.2 | 50 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jun | 50.2 | 49.9 | 50.1 | |

| 05:00 | JPY | Housing Starts Y/Y May | 33.90% | 32.10% | 11.40% | |

| 06:00 | EUR | Germany Import Price Index M/M May | 0.70% | 0.60% | 1.20% | |

| 06:00 | EUR | Germany Retail Sales M/M May | 1.10% | 0.00% | -0.30% | |

| 06:00 | GBP | Current Account (GBP) Q1 | -22.1B | -21.5B | -18.4B | |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.60% | 0.60% | 0.60% | |

| 06:00 | GBP | GDP Y/Y Q1 | 0.90% | 1.10% | 1.10% | |

| 07:00 | CHF | KOF Leading Indicator May | 101.2 | 99.4 | 98 | 98.6 |

| 07:55 | EUR | Germany Unemployment Rate May | -1K | -1K | 6.30% | |

| 07:55 | EUR | Germany Unemployment Change May | -1K | 8K | -12K | |

| 12:00 | EUR | Germany CPI M/M Jun P | -0.30% | 0.10% | -0.20% | |

| 12:00 | EUR | Germany CPI Y/Y Jun P | 2.30% | 2.50% | 2.60% | |

| 12:30 | CAD | GDP M/M Apr | 0.50% | 0.40% | -0.10% | |

| 13:00 | USD | Housing Price Index M/M Apr | -0.10% | 0.20% | 0.10% | 0.20% |

| 13:45 | USD | Chicago PMI Jun | 56.7 | 60 | 62.7 | |

| 14:00 | USD | Consumer Confidence Jun | 91.2 | 94.2 | 93.1 |

| 23:01 | GBP |

| BRC Shop Price Index Y/Y Jun | |

| Actual | 1.20% |

| Consensus | 1.30% |

| Previous | 1.20% |

| 23:30 | JPY |

| Unemployment Rate May | |

| Actual | 2.50% |

| Consensus | 2.50% |

| Previous | 2.50% |

| 23:50 | JPY |

| Industrial Production M/M May P | |

| Actual | 0.50% |

| Consensus | 0.60% |

| Previous | 0.50% |

| 01:00 | NZD |

| ANZ Activity Outlook Jun | |

| Actual | 36.9 |

| Consensus | |

| Previous | 25.6 |

| 01:00 | NZD |

| ANZ Business Confidence Jun | |

| Actual | 36.6 |

| Consensus | |

| Previous | 10 |

| 01:30 | AUD |

| Private Sector Credit M/M May | |

| Actual | 0.70% |

| Consensus | 0.60% |

| Previous | 0.70% |

| 01:30 | AUD |

| RBA Meeting Minutes | |

| Actual | |

| Consensus | |

| Previous | |

| 01:30 | CNY |

| NBS Manufacturing PMI Jun | |

| Actual | 50.3 |

| Consensus | 50.2 |

| Previous | 50 |

| 01:30 | CNY |

| NBS Non-Manufacturing PMI Jun | |

| Actual | 50.2 |

| Consensus | 49.9 |

| Previous | 50.1 |

| 05:00 | JPY |

| Housing Starts Y/Y May | |

| Actual | 33.90% |

| Consensus | 32.10% |

| Previous | 11.40% |

| 06:00 | EUR |

| Germany Import Price Index M/M May | |

| Actual | 0.70% |

| Consensus | 0.60% |

| Previous | 1.20% |

| 06:00 | EUR |

| Germany Retail Sales M/M May | |

| Actual | 1.10% |

| Consensus | 0.00% |

| Previous | -0.30% |

| 06:00 | GBP |

| Current Account (GBP) Q1 | |

| Actual | -22.1B |

| Consensus | -21.5B |

| Previous | -18.4B |

| 06:00 | GBP |

| GDP Q/Q Q1 F | |

| Actual | 0.60% |

| Consensus | 0.60% |

| Previous | 0.60% |

| 06:00 | GBP |

| GDP Y/Y Q1 | |

| Actual | 0.90% |

| Consensus | 1.10% |

| Previous | 1.10% |

| 07:00 | CHF |

| KOF Leading Indicator May | |

| Actual | 101.2 |

| Consensus | 99.4 |

| Previous | 98 |

| Revised | 98.6 |

| 07:55 | EUR |

| Germany Unemployment Rate May | |

| Actual | -1K |

| Consensus | -1K |

| Previous | 6.30% |

| 07:55 | EUR |

| Germany Unemployment Change May | |

| Actual | -1K |

| Consensus | 8K |

| Previous | -12K |

| 12:00 | EUR |

| Germany CPI M/M Jun P | |

| Actual | -0.30% |

| Consensus | 0.10% |

| Previous | -0.20% |

| 12:00 | EUR |

| Germany CPI Y/Y Jun P | |

| Actual | 2.30% |

| Consensus | 2.50% |

| Previous | 2.60% |

| 12:30 | CAD |

| GDP M/M Apr | |

| Actual | 0.50% |

| Consensus | 0.40% |

| Previous | -0.10% |

| 13:00 | USD |

| Housing Price Index M/M Apr | |

| Actual | -0.10% |

| Consensus | 0.20% |

| Previous | 0.10% |

| Revised | 0.20% |

| 13:45 | USD |

| Chicago PMI Jun | |

| Actual | 56.7 |

| Consensus | 60 |

| Previous | 62.7 |

| 14:00 | USD |

| Consumer Confidence Jun | |

| Actual | 91.2 |

| Consensus | 94.2 |

| Previous | 93.1 |

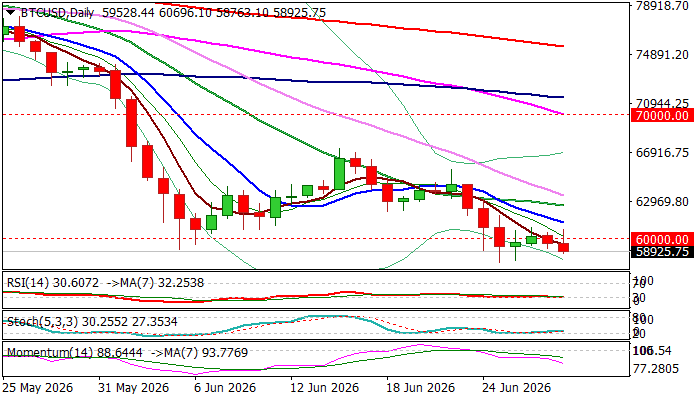

BTCUSD – 60K Barrier Limits Recovery Attempts as Larger Bears Hold Grip

BTCUSD falls below 60K mark after another failure to extend recovery from new 2026 low (57992) and register firm break above psychological barrier.

Near-term structure (hourly chart) showed some signs of strengthening that boosted expectations for recovery breaking above congestion in past few sessions.

However, hopes were so far short-lived as larger picture remains firmly bearish (daily chart) that kept barriers at 61300/600 zone (falling 10DMA / Fibo 38.2% of 67250/57992 / 200WMA) out of reach.

Increased risk of retesting 2026 low (57992) and nearby Fibo support at 57816 (61.8% of 15485/126299) should be expected if the price registers another close below 60K, with break lower to signal continuation of larger downtrend and expose next targets at 52500 (Sep 2024 low) and 50K (psychological).

Res: 60000; 60829; 61300; 61600

Sup: 59000; 57992; 57816; 56427

Sunset Market Commentary

Markets

Belgium and Spain kicked off the upcoming flurry of national member state HICP releases which culminate in the euro area print come Wednesday. Belgian (harmonized) CPI eased from 4.1% in May to 3% in June. Spanish prices rose by 0.6% m/m, quickening from May's 0.1%. That resulted in annual inflation unexpectedly matching May's 3.6% instead of dropping to the 3.4% consensus view. Core inflation (non-harmonized) fell from 3% to 2.9%, slightly below the 3% estimate. It's too early to determine the balance of risks for the euro area wide figure with heavyweights France, Germany and Italy due to report tomorrow. We did see the euro coming off the EUR/USD 1.1415 intraday highs after the Spanish release, be it in technically irrelevant trading. The pair is currently changing hands around that 1.14 big figure, extending a minor recovery that started last Thursday. The US dollar in general is marginally on offer today, losing against most peers. USD/JPY is one of the exceptions, nudging higher again towards the 2024 multi-decade high just shy of 162. Markets are testing Japanese (FX) policymakers. They should be wary of July 3, when US markets are closed in observance of Independence Day. Japan has shown appetite for interventions in liquidity-thinned trading circumstances – assuming the 162 barrier doesn't break sooner. The pound is enjoying a honeymoon period in between outgoing PM Starmer and his successor Burnham. EUR/GBP nears last week's lows and is on track for the weakest closing level since August 2025. Burnham is likely to take over July 17th. He used his first major speech since securing his seat in parliament to promise change. For one, he intends to transfer some business from London's Downing Street 10 to Manchester, dubbed No. 10 North. This power redistribution across the country should decentralize public finances and push regions to drive their own growth agendas. Burnham seeks to safeguard critical manufacturing and production capabilities, including in steel, defense, energy, food and farming and promised the biggest house-building since the postwar period. "To reduce the welfare bill in a way that is fair and lasting" was probably aimed at comforting markets that not all is borrow-to-spend. He also reaffirmed his commitment to the fiscal rules that current Chancellor Reeves has implemented. UK gilts shrugged with yields trading unchanged on the day. Rates in other (core) regions including in the US and the euro area trade with changes smaller than 2 bps. That stoicism isn't surprising given the backloaded eco calendar this week. Stock markets kick off the week in good spirits, especially in the US. The tech-heavy Nasdaq has been prone to some (end-of-quarter) rotational moves but eyes a 1.5% recovery today.

News & Views

Belgian inflation decreased by 0.3% M/M in June. The most significant price increases in June were registered for electricity (+2.5% M/M), private rents (+0.7%), package holidays (+0.9%) and natural gas (1.5%). However, motor fuels (-6.4%), plane tickets (-21.6%), holiday villages and campings (-6.2%), and clothing (-1.2%) have had a decreasing effect on the index. Headline CPI slowed from 4.08% Y/Y in May to 3.4%. The first inflation estimate according to the European Harmonised Index of Consumer Prices (HICP flash estimate) amounts to 3% in June 2026. Core inflation, which excludes energy products and unprocessed food, stood at 3.04%, down from 3.59% in May. Services inflation went from 5.88% to 5.1% while food inflation slowed from 1.2% to 0.06%.

Hungarian PM Magyar warned that the country's budget deficit is now expected to exceed 7% of GDP, even after securing EU funds. Without them, that would have likely been above 8% of GDP. The new government claims that huge pre-election spending wasn't fully reflected in the budget. The previous Orbán government had an official 3.7% deficit target which was later revised to 5% of GDP. The Hungarian government will conduct a full audit of public finances and submit a revised budget by the end of August. In light with meeting Maastricht criteria for potential euro adoption by 2030, they'll have to put in place significant medium term consolidation plans. The Hungarian forint loses some ground today with EUR/HUF rising from 353.50 to 355.

Quarter-End Calm Masks High-Stakes Week for Fed, ECB, BoJ and RBA

Financial markets began the week on a subdued note, with quarter-end positioning and caution ahead of a packed economic calendar keeping most major assets confined to familiar ranges. Geopolitical headlines surrounding the US-Iran conflict attracted little attention, while Brent crude held steady around USD 73 a barrel, suggesting investors are increasingly viewing Middle East tensions as a manageable risk rather than an immediate market driver.

Price action across asset classes reflected the lack of conviction. Asian equities ended mixed, with Japanese and South Korean shares little changed, while major European indices traded modestly lower. US futures pointed to a slightly firmer open. Currency markets were similarly directionless. New Zealand Dollar, Pound Sterling and Euro outperformed modestly, while Canadian Dollar, Japanese Yen and US Dollar lagged. Australian Dollar and Swiss Franc traded near the middle of the pack, with most major pairs and crosses remaining comfortably within last week's trading ranges.

The restrained tone is understandable given an unusually compressed trading week. US markets will close early ahead of the Independence Day holiday, leaving investors with less time to reposition before several major economic releases. Rather than responding to incremental headlines, markets appear content to wait for data capable of reshaping monetary policy expectations.

The centerpiece will be Thursday's US Non-Farm Payrolls report. Markets have scaled back expectations for aggressive Federal Reserve tightening after June's PCE inflation data eased concerns over a second wave of price pressures. One additional rate hike this year is now the prevailing expectation. However, another resilient employment report could quickly revive speculation that the Fed may need to tighten more aggressively, setting the tone for the Dollar, Treasury yields and broader risk sentiment heading into the third quarter.

The US data calendar also includes Wednesday's ISM Manufacturing survey. Beyond the headline index, investors will closely examine the relationship between new orders and inventories. Manufacturing activity has benefited in recent months from precautionary stockpiling during the disruption to Middle East shipping routes. If inventories remain elevated while new orders begin to soften, it could signal that manufacturers are entering an inventory adjustment phase that weighs on production later this year.

Elsewhere, Wednesday's Eurozone flash CPI will be critical for expectations surrounding the European Central Bank's August meeting. Recent survey data suggest inflation pressures continue to moderate, but another upside surprise could strengthen the case for additional policy tightening. In Japan, the Bank of Japan's Tankan survey will be scrutinized for evidence that stronger business conditions and price dynamics are providing further support for policymakers advocating a faster pace of normalization.

Attention will also turn to Tuesday's Reserve Bank of Australia meeting minutes. Policymakers have maintained a distinctly hawkish tone despite leaving rates unchanged, leaving markets divided over whether the tightening cycle has ended or whether another increase in August remains possible. Investors will be looking for clues on how high the hurdle has become for another rate hike.

The absence of strong market moves today should therefore not be mistaken for complacency. Instead, investors appear to have reached a temporary equilibrium, with quarter-end positioning giving way to a series of economic releases that will test expectations for the Fed, ECB, BoJ and RBA in quick succession.

USD/JPY Enters High-Stakes Game of Chicken Ahead of Non-Farm Payrolls

USD/JPY's climb toward 162.00 has become a high-stakes game of chicken. Japan appears reluctant to intervene before US Non-Farm Payrolls, but that patience may create an even greater intervention risk once the data is released and holiday-thinned liquidity takes over. Read More.

Gold's Rebound Lacks Conviction as Jobs Report Could Reopen Fed Hike Debate

Gold's recovery above $4000 looks more like hesitation than a genuine turnaround. With markets already pricing one Fed hike this year, Thursday's US jobs report could determine whether that consensus holds or shifts back toward more aggressive tightening. We examine how each payroll scenario could reshape the Dollar, Fed expectations, and Gold's technical outlook. Read More.

Eurozone Economic Sentiment Improves Further, But Hiring Expectations Weaken

Confidence is returning to the euro area, yet employers are turning more cautious. Discover why stronger sentiment has not translated into stronger hiring and what that says about the region's economic recovery. Read More.

BoE's Pill: Structural Changes Leave UK Inflation More Persistent

Why has UK inflation proved so difficult to bring back to target? BoE Chief Economist Huw Pill argues the answer lies in structural changes that have made price pressures more persistent, strengthening the case for interest rates to stay higher for longer. Read More.

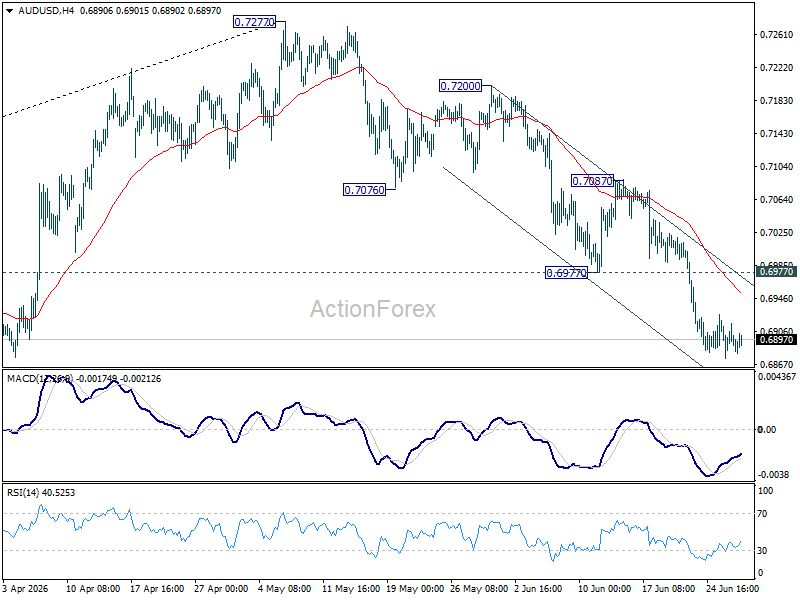

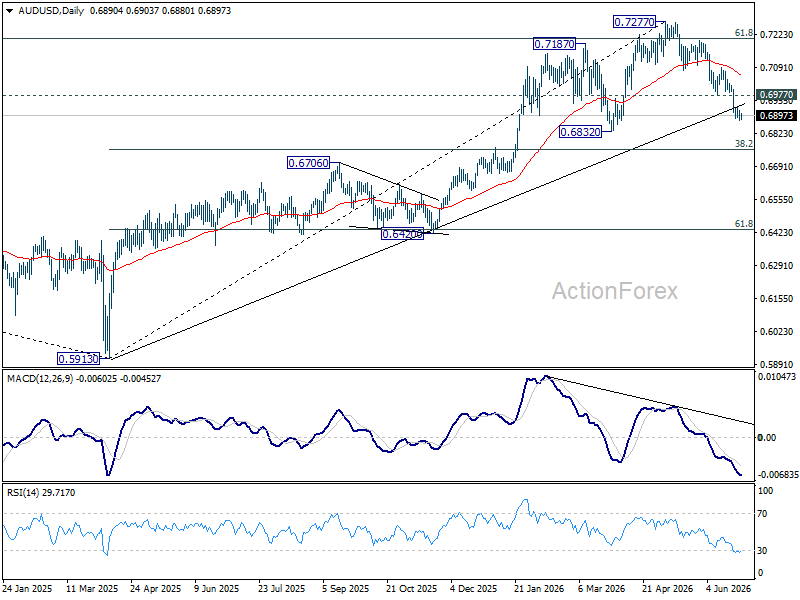

AUD/USD Daily Report

Further decline is expected in AUD/USD with 0.6977 support turned resistance intact. Current fall from 0.7277 should extend to 0.6832 support. Firm break there will target 0.6756 fibonacci level.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

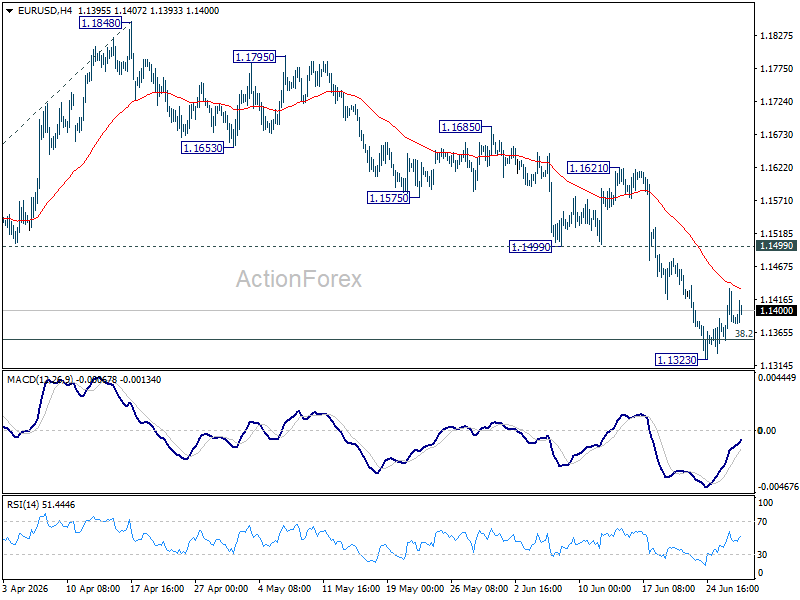

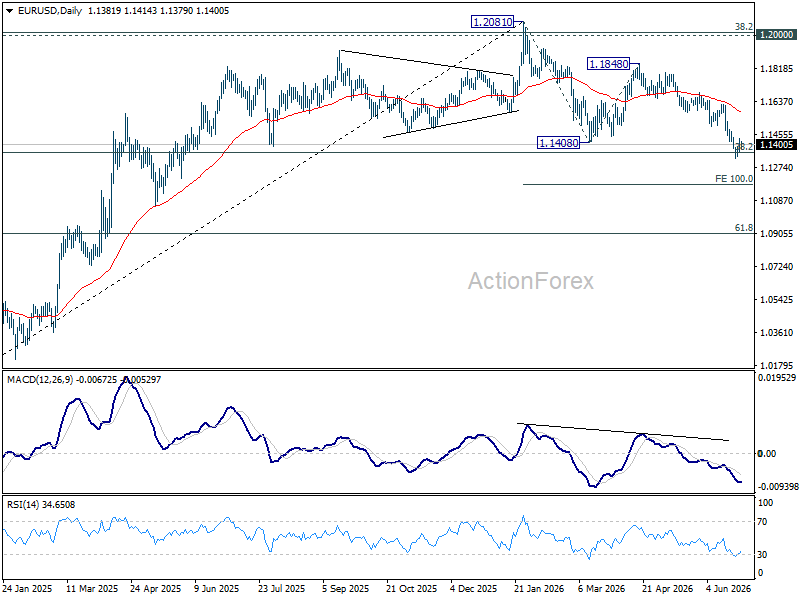

EUR/USD Daily Outlook

Intraday bias in EUR/USD stays neutral and more consolidations could be seen above 1.1323. Further fall is expected as long as 1.1499 support turned resistance holds. Break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

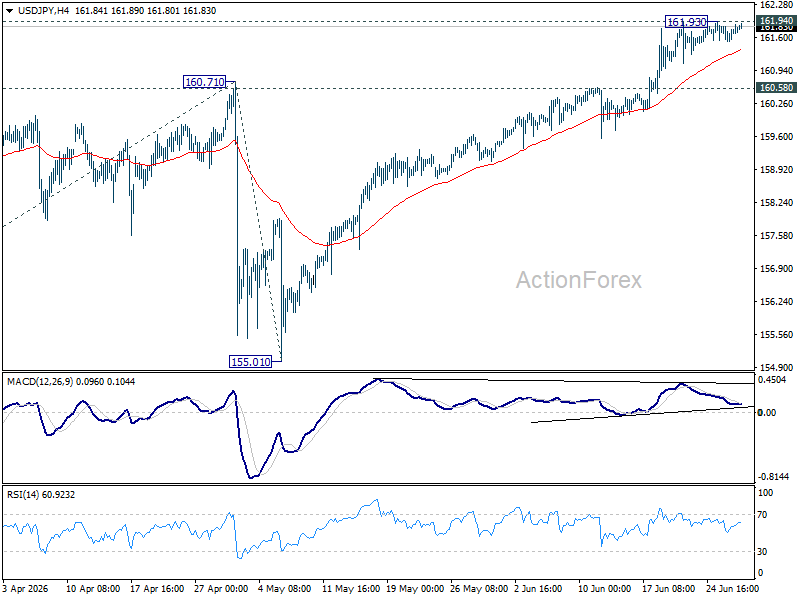

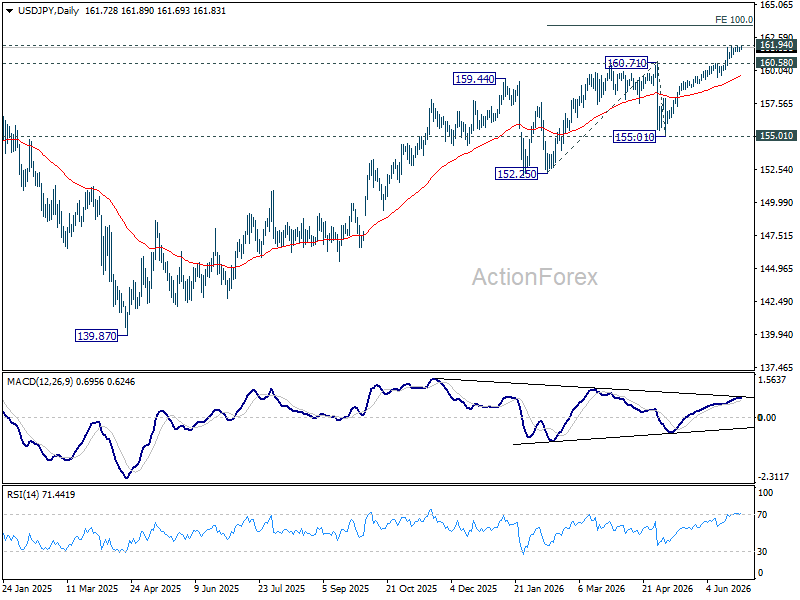

USD/JPY Daily Outlook

USD/JPY is staying in tight range below 161.94 key resistance and intraday bias remains neutral. On the downside, firm break of 160.58 support should confirm short term topping, on bearish divergence condition in 4H MACD. Deeper fall should then be seen to 55 D EMA (now at 159.71) and below. Nevertheless, decisive break of 161.94 high will resume the larger up trend to 100% projection of 152.25 to 160.71 from 155.01 at 163.47 next.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. This will remain the favored case as long as 55 W EMA (now at 155.40) holds.

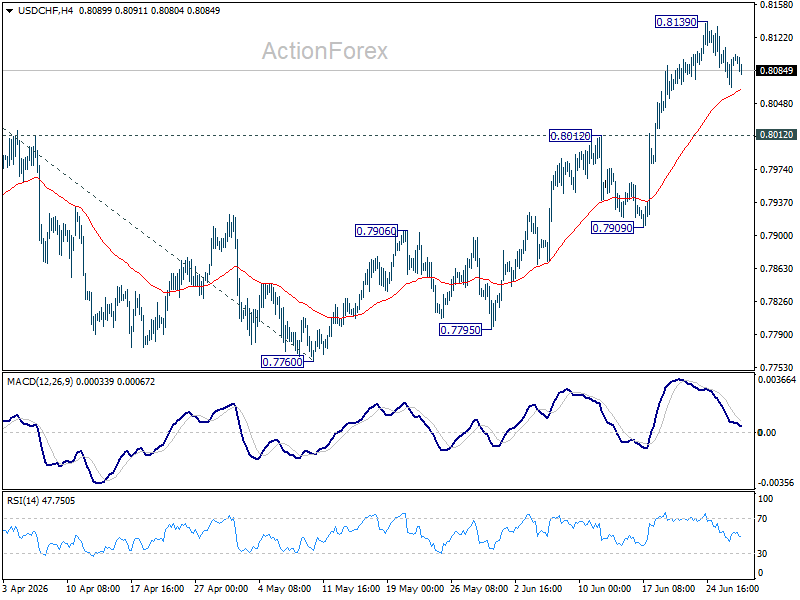

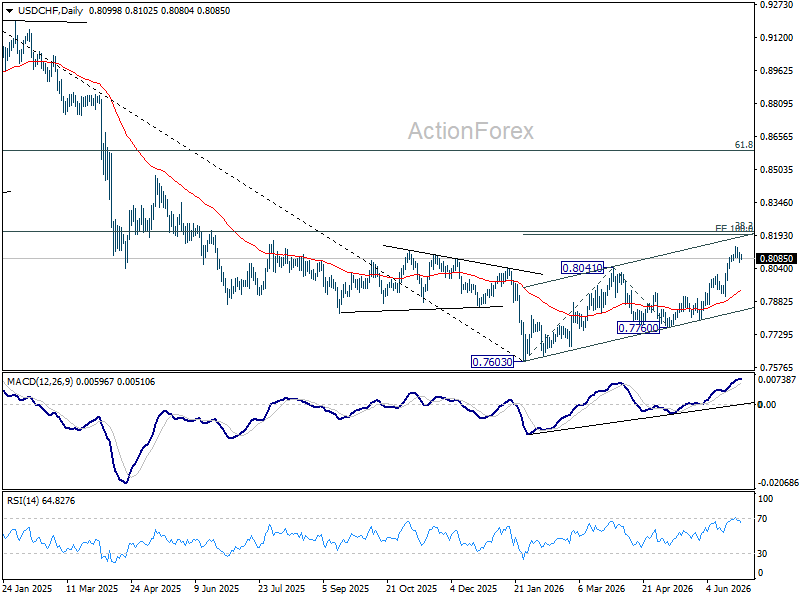

USD/CHF Daily Outlook

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.8139. Downside should be contained by 0.8012 resistance turned support to bring another rally. Above 0.8139 will target 100% projection 0.7603 to 0.8041 from 0.7600 at 0.8198 next.

In the bigger picture, while a medium term bottom was formed at 0.7603, it's still early to call for bullish trend reversal. As long as 38.2% retracement of 0.9200 (2025 high) to 0.7603 at 0.8213 holds, the larger down trend could still continue through 0.7603 at a later stage. However, firm break of 0.7603 will argue that the trend has reversed and turn focus to 0.8332 support turned resistance (2023 low) for confirmation.

AUD/USD Daily Report

Further decline is expected in AUD/USD with 0.6977 support turned resistance intact. Current fall from 0.7277 should extend to 0.6832 support. Firm break there will target 0.6756 fibonacci level.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

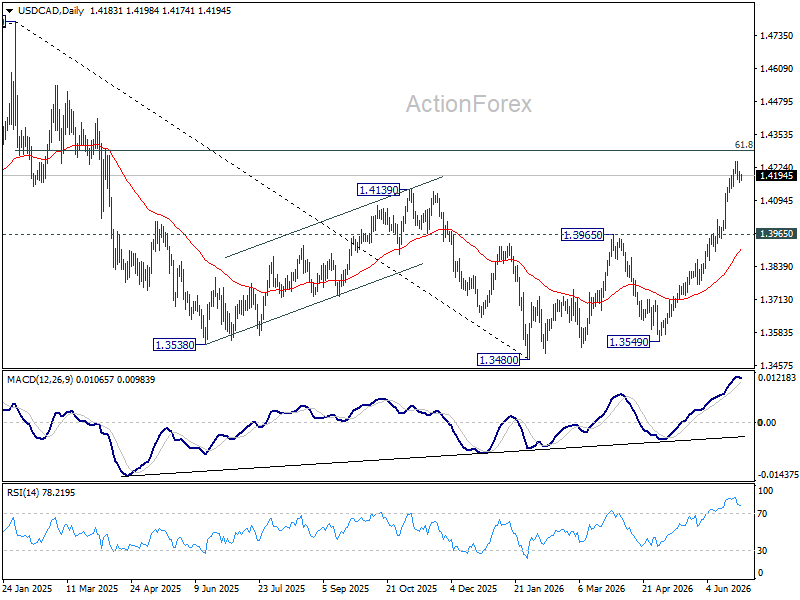

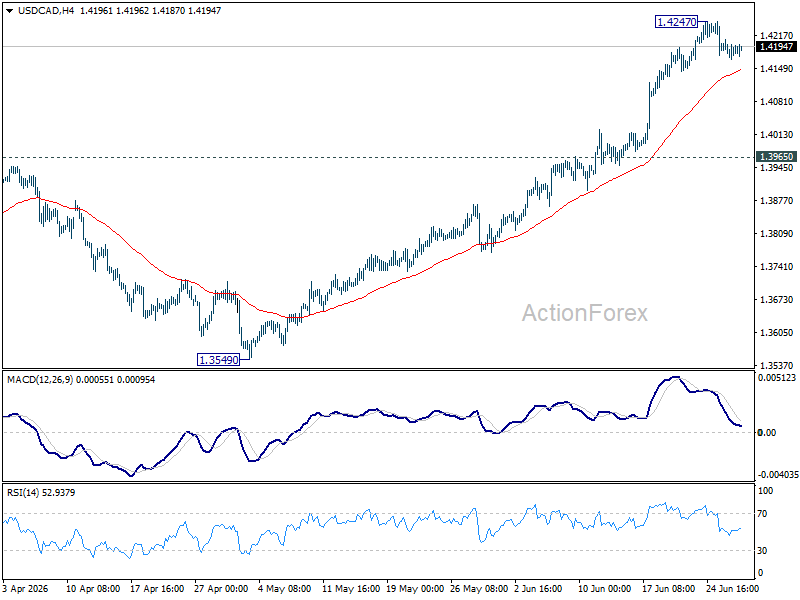

USD/CAD Daily Outlook

Intraday bias in USD/CAD stays neutral, and more consolidations could be seen below 1.4247 temporary top. While deeper pullback cannot be ruled out, downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.