Sample Category Title

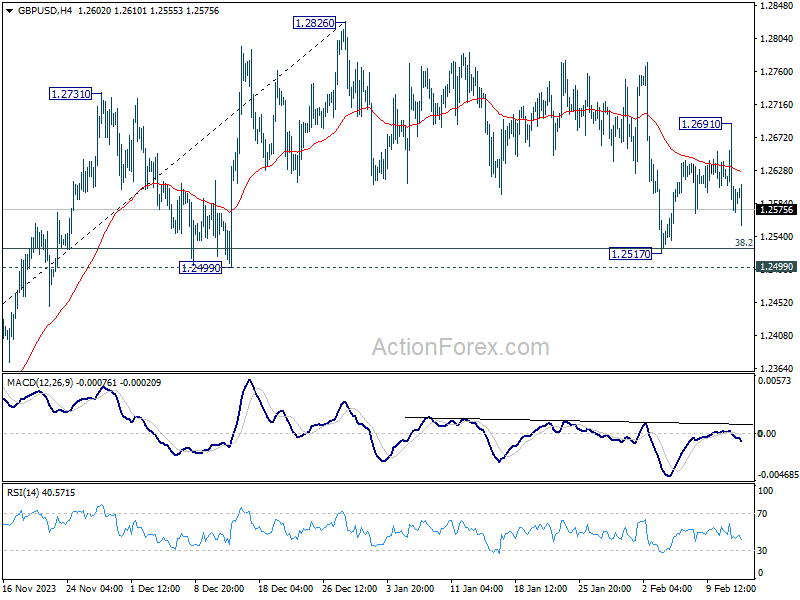

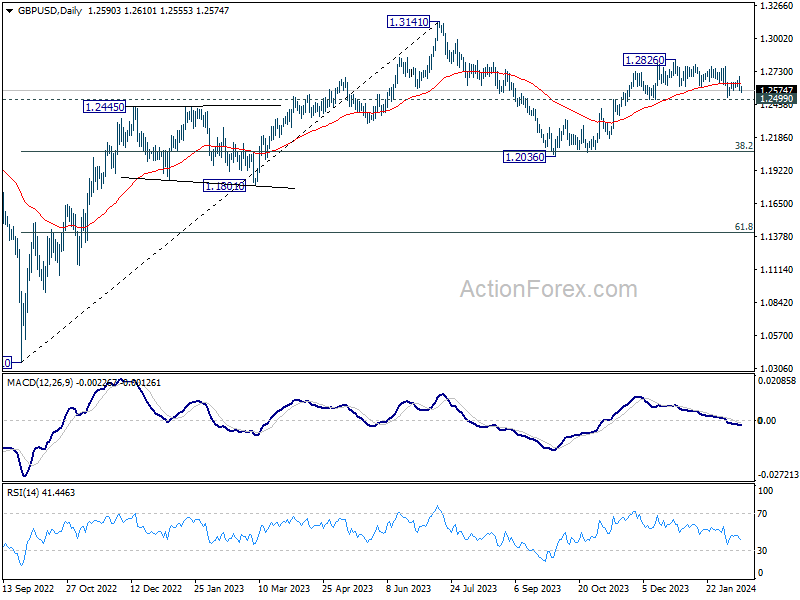

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2549; (P) 1.2617; (R1) 1.2661; More...

Intraday bias in GBP/USD remains neutral at this point. On the upside, firm break of 1.2691 resistance will affirm the case that correction from 1.2826 has completed at 1.2517, after drawing support from 1.2499. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, would could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

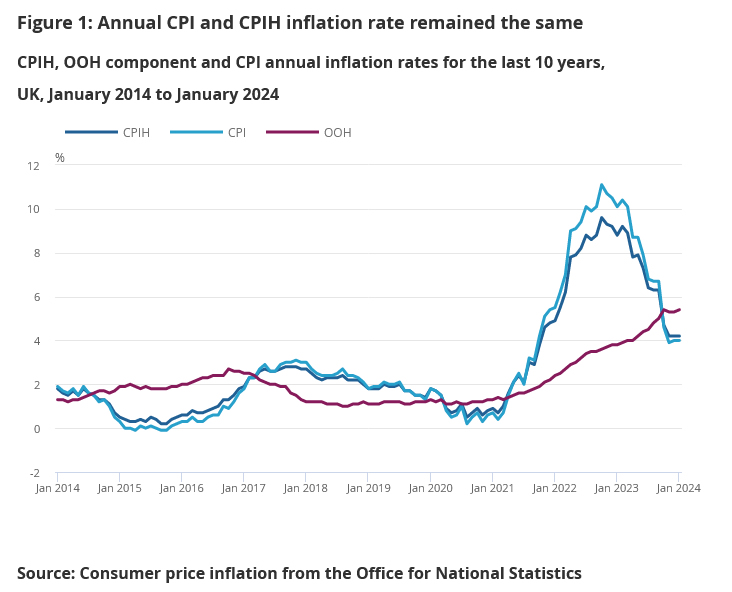

UK CPI and core unchanged in Jan, at 4.0% and 5.1%

UK CPI fell -0.6% mom in January, below expectation of -0.3% mom. Annually, CPI was unchanged at 4.0% yoy, below expectation of 4.1% yoy.

Core CPI (excluding energy, food, alcohol and tobacco) was also unchanged at 5.1% yoy, below expectation of 5.2% yoy. CPI goods slowed from 1.9% yoy to 1.8% yoy. CPI services accelerated from 6.4% yoy to 6.5% yoy.

The largest upward contribution to the monthly change in both CPI annual rates came from housing and household services (principally higher gas and electricity charges), while the largest downward contribution came from furniture and household goods, and food and non-alcoholic beverages.

UK Inflation in Focus Today

In focus today

This morning at 8:00 CET, UK inflation data for January is expected to rise in y/y terms across the headline, core and services measure. However, focus will be on the monthly seasonally adjusted developments.

In the euro area, industrial production figures for December will most likely come in lower due to the significant drop in German production.

Moreover, Japanese national accounts for Q4 are released overnight. Data have been mixed and we are looking for a modest pick-up in GDP growth following the 0.5% dip in Q3, supported by solid foreign demand. Consumption data on the other hand has been to the weak side.

Economic and market news

In the US, January CPI surprised to the upside, with core inflation at 0.39% m/m (consensus 0.3% m/m) while headline inflation was up 0.3% m/m (consensus 0.2% m/m). The surprise was fuelled by a broad-based increase in services prices, indicating that underlying momentum in inflation is picking up - for more detail, see Global Inflation Watch, 13 February. Additionally, the NFIB's small business optimism index decreased two points to 89.9 in January, while the survey also revealed a slight rebound in price plans.

In the UK, wage growth was stronger than expected in December at 6.2% (cons: 6.0%), while the unemployment rate surprisingly edged down to 3.8% in December (cons: 4.0%, prior: 3.9%). As wage growth was revised up in November (6.7%), the December print was only a small upside surprise, and importantly wage growth is still declining. This is the first complete release following the past months' use of experimental data. Given issues surrounding the data quality of the official measures, the MPC traditionally uses a range of indicators to assess the labour market including the KMPC/REC report, which showed broad easing last week. The fully transformed labour force survey will not be published until H2 2024. Note, we will get another job report before the March meeting.

In Germany, German ZEW expectations continue to rise more than expected in February to 19.9 (cons: 17.3), while the assessment of the economic situation declined more than expected to -81.7 (cons: -79.0). Similarly, to the Ifo survey, the decline in the economic situation corroborates that activity in Germany has not bottomed out yet despite the uptick in manufacturing PMIs. That said, with the global manufacturing cycle turning positive and the large rise in expectations there are rays of light for the German economy.

Equities: Global equities ended markedly lower yesterday as the US inflation print came out much hotter than expected. It was not surprising to see defensive value and min vol stocks outperform while VIX moved from 13 to 15. It was also not surprising to see small caps being sold off, but the magnitude - with Russel 2000 down almost 4% - shows that investors are extremely concerned about the CRE segment and US regional banks. While all sectors were lower this was not a classic defensive rotation based on higher recession probability. Banks, REITs and utilities underperformed together as the central bank fear came back (for the "wrong reasons") and investor behaviour looked very much like what we saw in Q3 last year. The big question is whether this will change the narrative that has dominated since late October? We think the short answer is no. In US yesterday Dow -1.4%, S&P 500 -1.4%, Nasdaq -1.8% and Russell 2000 -4.0%. Most Asian markets are lower this morning but not nearly to the same extent as on Wall Street yesterday. EM have not had the same inflation challenge as the western world as they did not overstimulate their economies during the Covid pandemic. Hence, these markets will be a lot less effected on days when fear of hawkish central banks dominate. European futures are lower this morning while US futures are mixed.

FI: It has been some tough days in the global bond market with rising bond yields with 2Y US Treasury yields rising more than 45bp and 10Y US Treasury yields rising more than 30bp since the start of February. This has been driven by the stronger than expected US labour market data as well as yesterday's US CPI data. There has been a spill-over effect to the European market where the 2Y and 10Y German government bond yields have risen some 30bp and 20bp in the 2Y and 10Y segments, respectively. Hence, the market continues to price out rate cuts from the Federal Reserve as well as ECB.

FX: The US CPI print triggered big FX moves in yesterday's session with not least the USD gaining and risk sensitive currencies including the Scandies suffering considerably. Also the CHF traded on the backfoot after much-lower-than-expected Swiss inflation figures while a hot UK labour market contributed to sending GBP higher against most currencies - also after the US inflation release. The rise in yields also contributed to sending USD/JPY above the 150-mark increasing the risk of (verbal) intervention from the Japanese authorities.

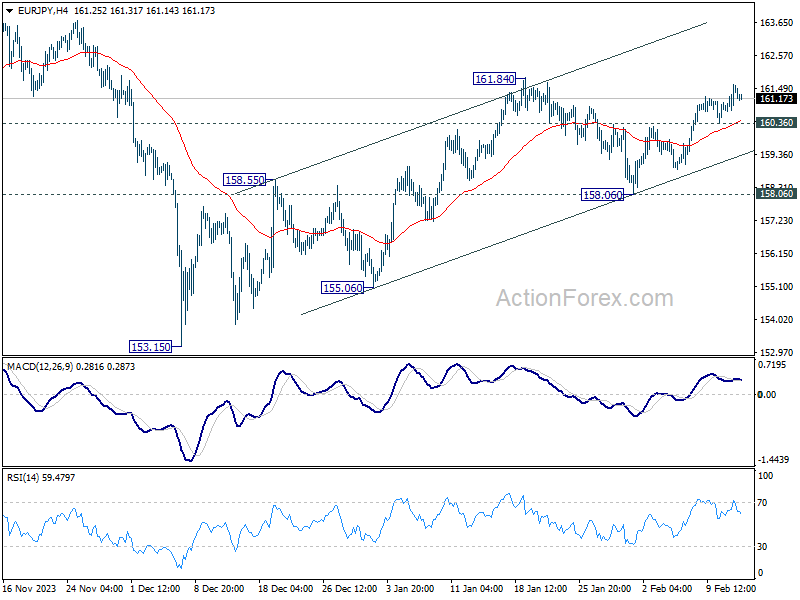

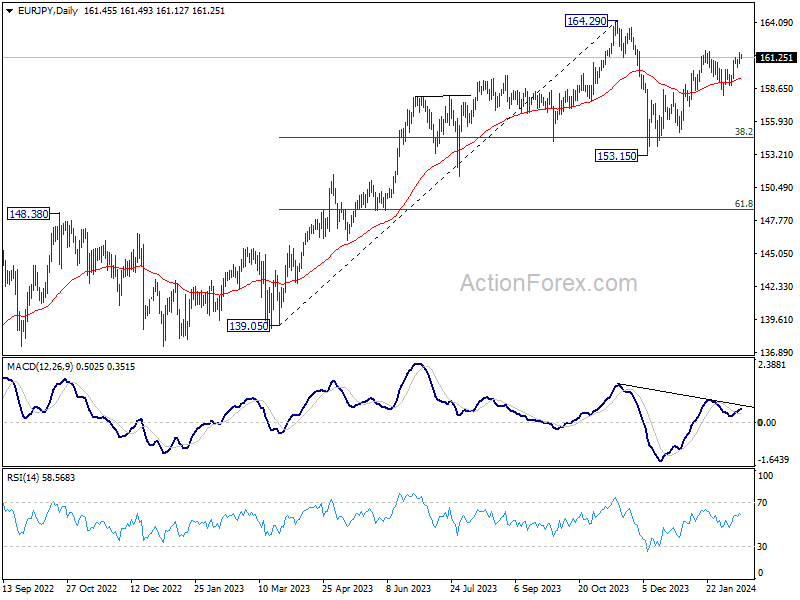

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.97; (P) 161.30; (R1) 161.82; More...

Intraday bias in EUR/JPY remains on the upside for retesting 161.84 resistance. Firm break there will confirm resumption of whole rise from 153.15. Next target is a retest on 164.29 high. On the downside, below 160.36 minor support will turn intraday bias neutral first. But further rally is expected as long as 158.06 support holds, in case of retreat.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

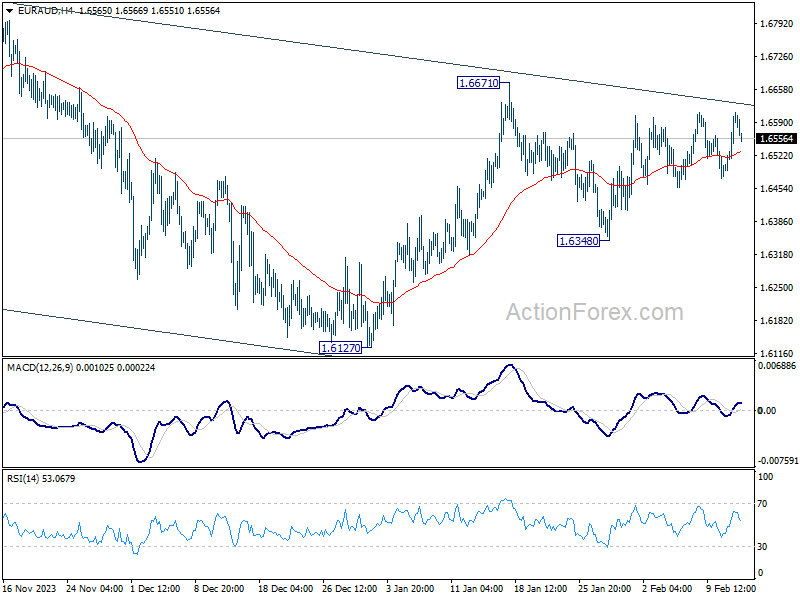

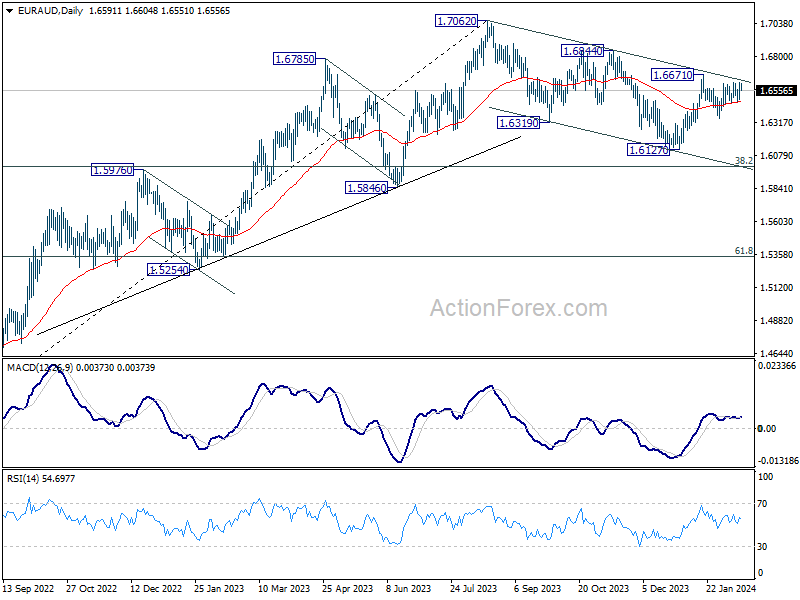

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6521; (P) 1.6566; (R1) 1.6640; More...

Intraday bias in EUR/AUD remains neutral as range trading continues. On the upside, decisive break of 1.6671 will revive the case that whole correction from 1.7062 has completed with three waves down to 1.6127. Further rally should then be seen to 1.6844 resistance for confirmation. Nevertheless, break of 1.6438 will bring deeper fall back to 1.6127 support instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

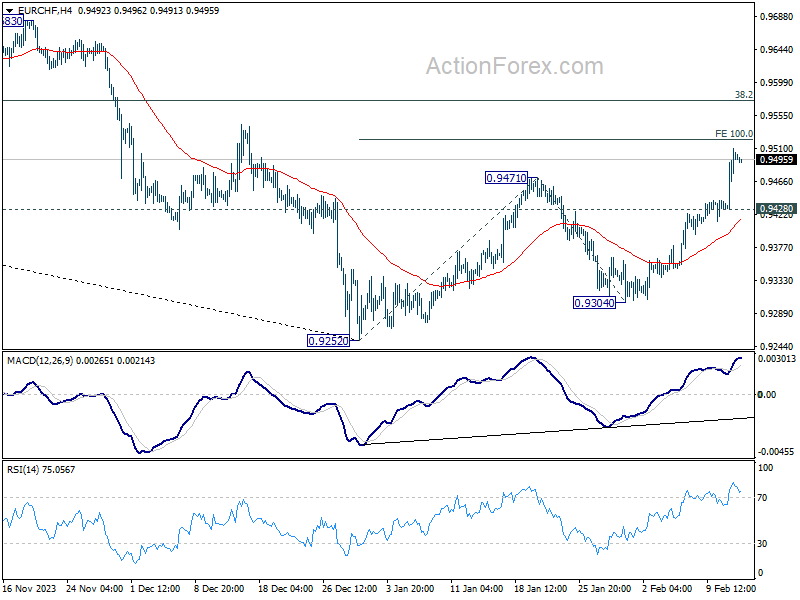

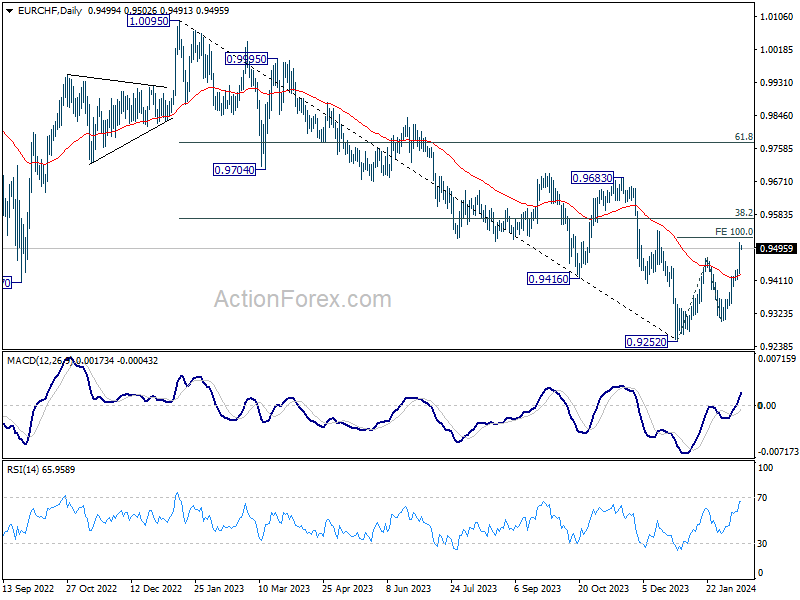

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9449; (P) 0.9481; (R1) 0.9531; More...

EUR/CHF's firm break of 0.9471 resistance confirms resumption of rise from 0.9252. Intraday bias stays on the upside for 100% projection of 0.9252 to 0.9471 from 0.9304 at 0.9523. On the downside, below 0.9428 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, price actions from 0.9252 are tentatively seen as a correction to the five-wave down trend from 1.0095 (2023 high). Further rise would be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. But overall medium term outlook will remain bearish as long as 0.9683 resistance holds.

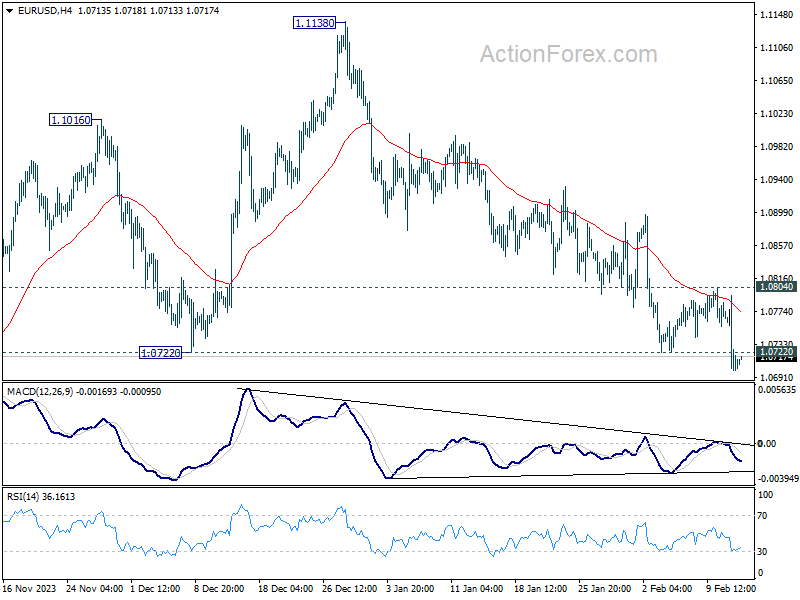

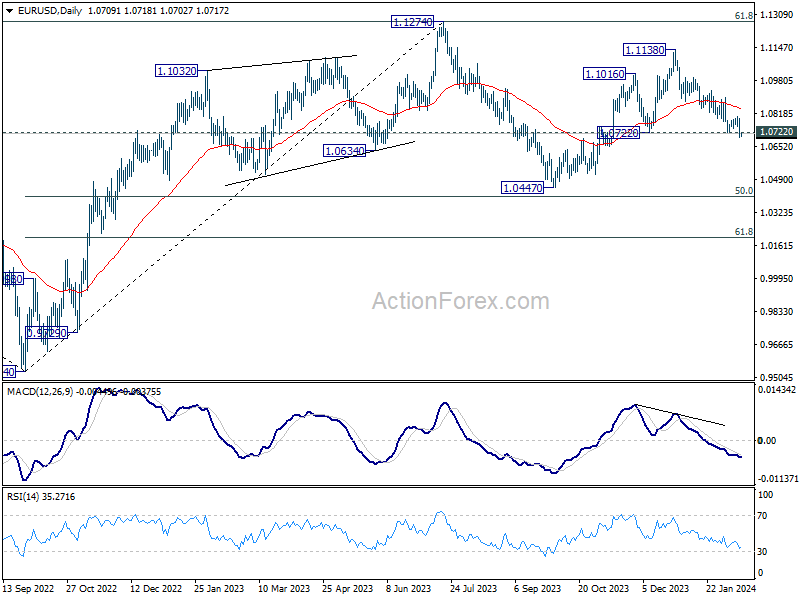

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0674; (P) 1.0736; (R1) 1.0772; More...

Intraday bias in EUR/USD remains on the downside development. Current development argues that whole rise from 1.0447 has already finished. Deeper decline would be seen back to this 1.0447 support. On the upside, break of 1.0804 resistance is needed to signal short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

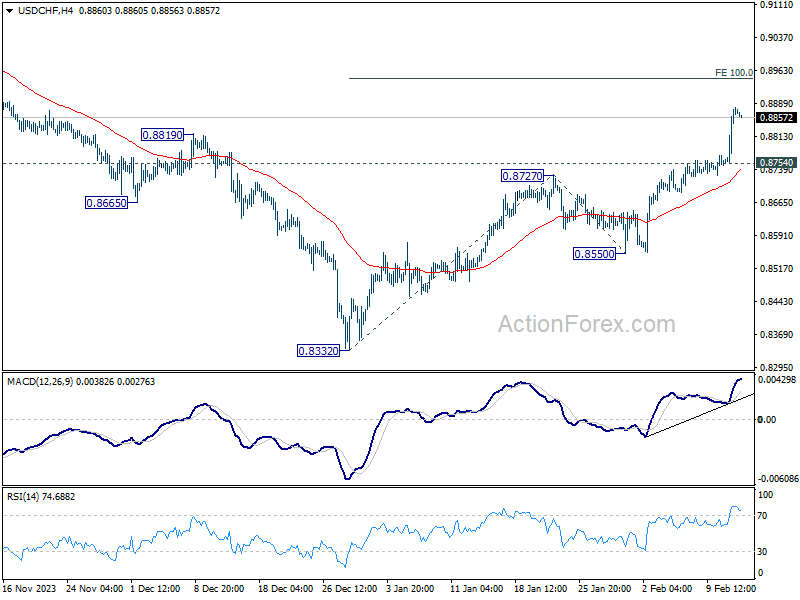

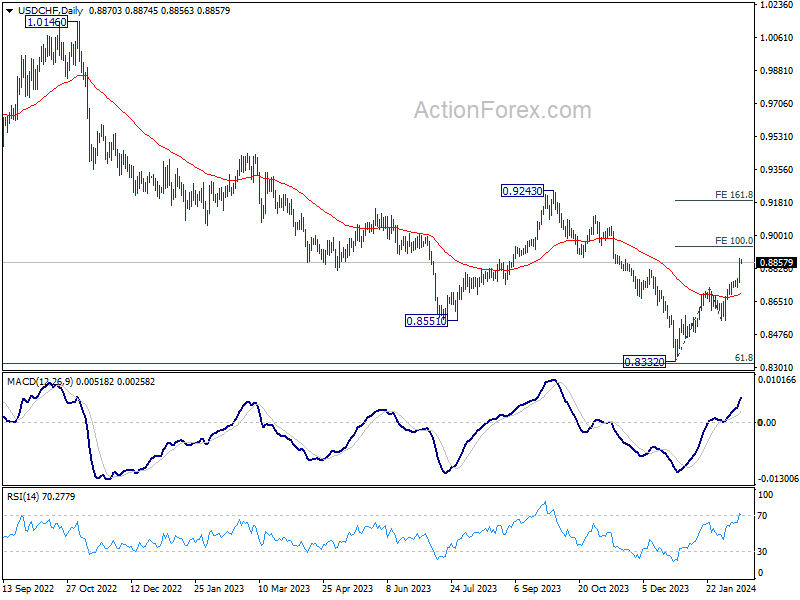

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8786; (P) 0.8833; (R1) 0.8919; More....

Intraday bias in USD/CHF remains on the upside at this point. Current rally from 0.8332 should target 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. Firm break there will pave the way to 161.8% projection at 0.9189. On the downside, below 0.8754 minor support will turn intraday bias neutral first. But retreat should be contained above 0.8550 support to bring another rally.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support, on bullish convergence condition in W MACD. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

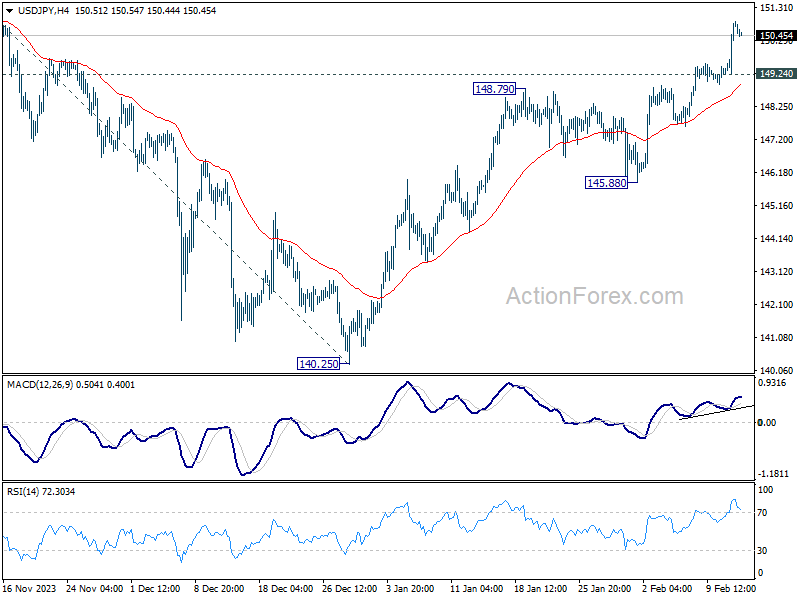

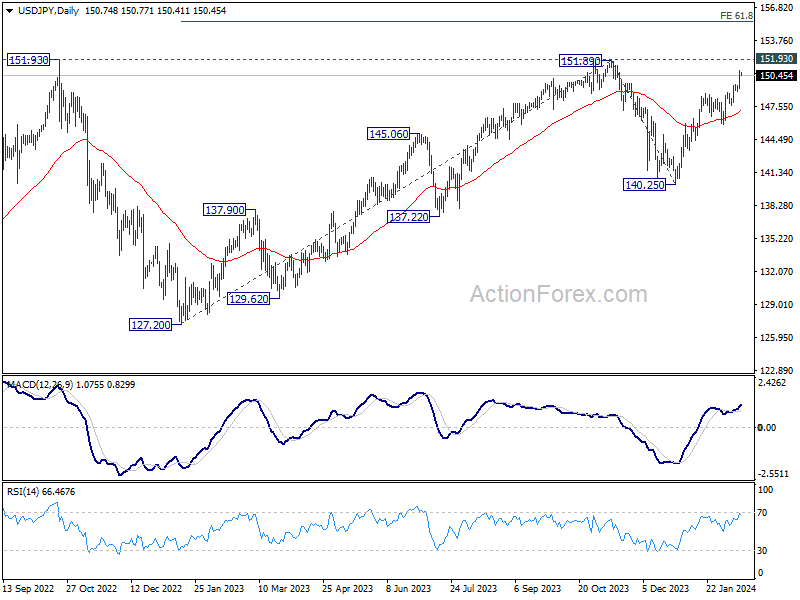

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.73; (P) 150.31; (R1) 151.37; More...

Intraday bias in USD/JPY remains on the upside at this point. Current rise from 140.25 will target 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. On the downside, below 149.24 minor support will turn bias neutral and bring consolidations, before staging another rally.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

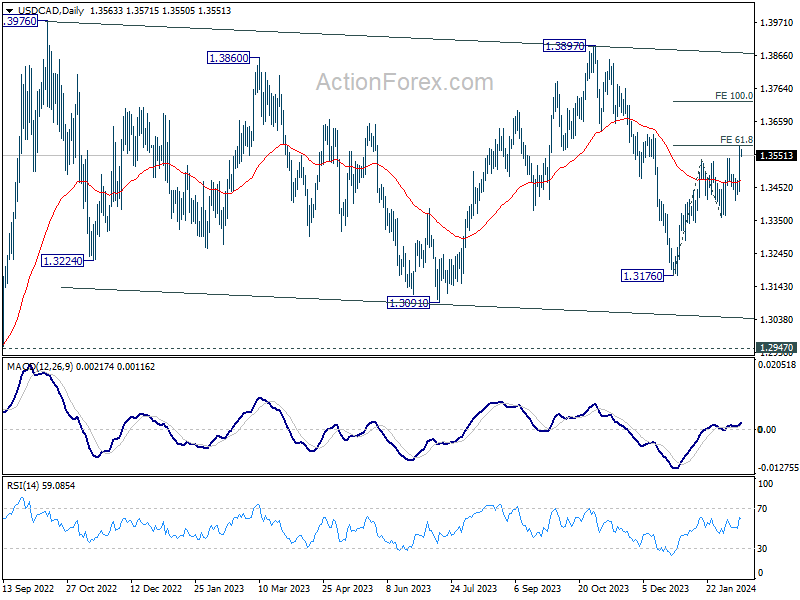

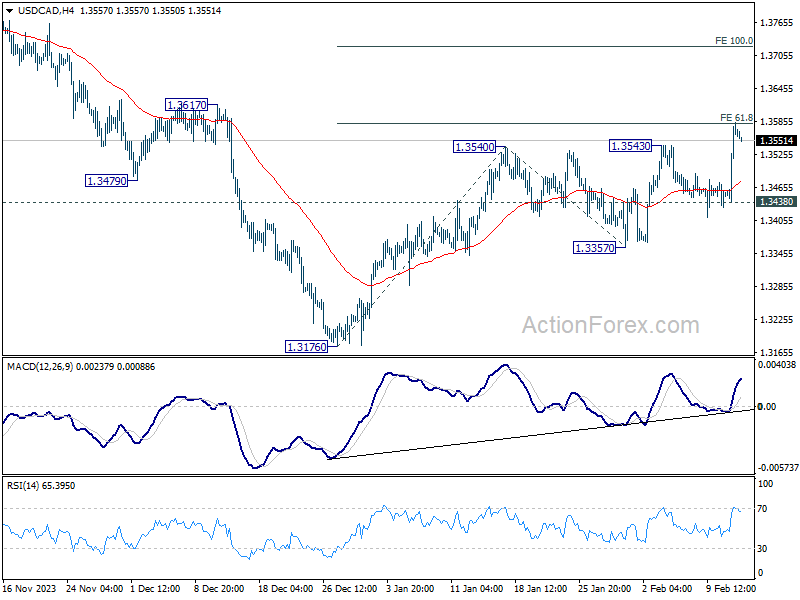

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3474; (P) 1.3530; (R1) 1.3620; More...

Intraday bias in USD/CAD is back on the upside as rise from 1.3176 resumed by breaking through 1.3543 resistance. Firm break of 61.8% projection of 1.3176 to 1.3540 from 1.3357 at 1.3582 will pave the way to 100% projection at 1.3721. On the downside, break of 1.3438 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.