Sample Category Title

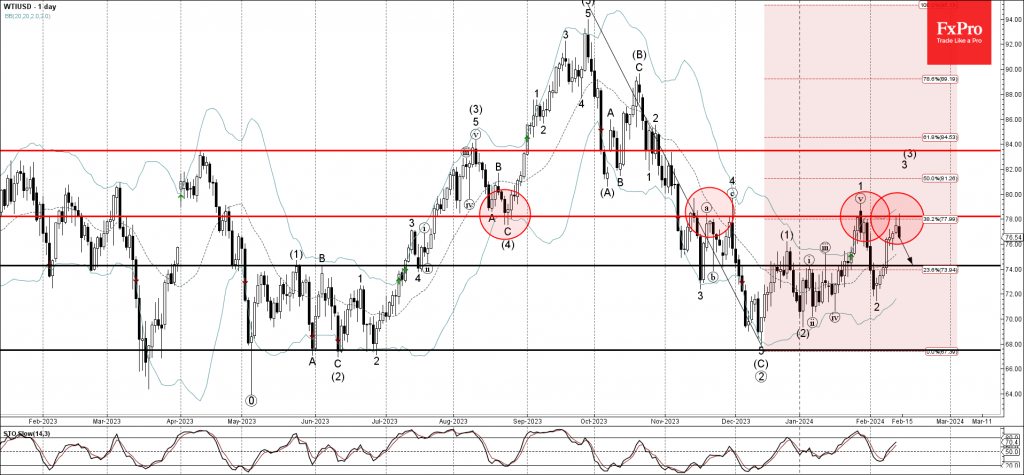

WTI Crude Oil Wave Analysis

- WTI crude oil reversed from resistance level 78.00

- Likely to fall to support level 74.00

WTI crude oil recently reversed down from the pivotal resistance level 78.00 (former support from August, which has been reversing the price from November), intersecting with by the upper daily Bollinger Band and the 38.2% Fibonacci correction of the downward impulse from September.

The downward reversal from the resistance level 78.00 stopped the previous impulse waves 3 and (3).

Given the improvement of the global risk sentiment, WTI crude oil can be expected to fall further to the next support level 74.00.

Sunset Market Commentary

Markets

Core bonds licked their wounds after yesterday’s smackdown with UK gilts outperforming both US Treasuries and bunds. Gilts on Tuesday suffered a one-two-punch from a stronger-than-expected UK labour market report first and from the US CPI inspired global sell-off second. Yields today ease 4 (30-y) to 11.1 bps (2-y), erasing much of the 6.7-14.6 bps surge yesterday. A sub-consensus January inflation print initiated the move. CPI dropped by 0.6% on a monthly basis, double the 0.3% expectations. The yearly figure therefore unexpectedly matched December’s 4% instead of rising to 4.1%. Core CPI (5.1%) in a similar way defied the anticipated acceleration to 5.2% while services inflation rose less than feared, from 6.4% to 6.5%. Other (producer) gauges fell short of the bar as well. While none of the readings pave the way for some quick BoE easing, it did offer some relief to the gilt market. There were even some minor spillovers to US Treasuries. Yields of the world’s largest economy return up to 5.7 bps at the front end of the curve. This compares to the +20 bps rise (3-y) yesterday. From a technical perspective, rates hold north of the resistance levels breached on Tuesday. German yields decline about 2 bps across the curve. Euro area economic growth was confirmed to have stagnated in Q4 of last year. But separate data offer a glimmer of hope with industrial production having rebounded 2.6% in December after an upwardly revise 0.4% in November. Employment growth also picked up in the region, rising by 0.3% q/q and further accelerating from the 0.1% in Q2 and 0.2% in Q3.

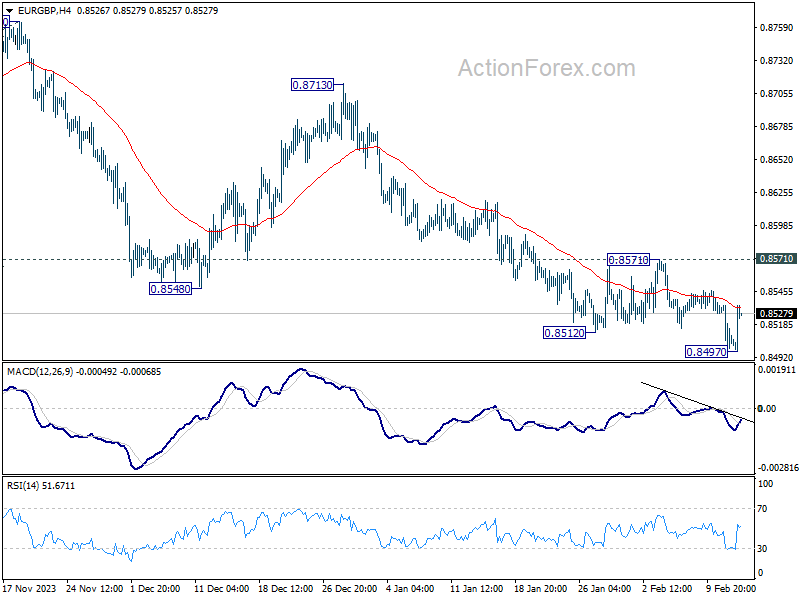

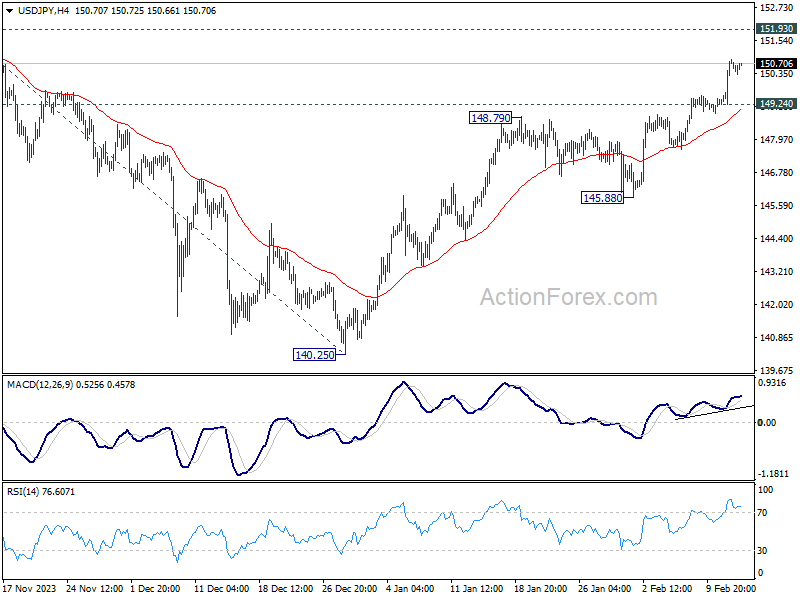

The pound lags peers in the FX market. UK CPI helped EUR/GBP to avoid an imminent break to the downside where critical references at 0.8504 & 0.8492 were the last line of defense ahead of a technical wasteland that stretches to 0.834. The pair is currently trading around 0.8526. Cable (GBP/USD) is losing the 1.26 barrier again. Tomorrow’s GDP and Friday’s retail sales are to seal GBP’s short-term fate. The dollar catches a breather but the likes of JPY are unable to capitalize. USD/JPY holds above 150, triggering verbal interventions from at least three high-ranking Japanese officials. EUR/USD is flirting with the 1.07 big figure with a break looking like it could happen anytime.

News & Views

Several countries in the CEE region today published a preliminary release of Q4 2023 GDP growth. Growth in Hungary printed unchanged both Q/Q and Y/Y. According to the Hungarian Statistical office, ‘the economic performance rose mostly in sections agriculture, human health and social work activities and information and communication. The falls in industry, construction and some market services, mainly wholesale and retail trade, offset the growth’. Overall 2023 GDP was 0.8% lower than in previous year. When assessing whether or not to step up the pace of interest rate cuts, the MNB has to put a sub-trend economic growth and easing inflationary pressures against considerations of financial stability. The forint today weakens from EUR/HUF 377.1 to 389.4. Q4 2023 growth in Poland (details on Feb 29) at 0.0% Q/Q and 1.0% Y/Y was close to expectations. Growth in Slovakia in Q4 last year was reported at 0.3% Q/Q and 1.2% Y/Y, mainly supported by the Y/Y increase in investments. In summary for the whole year, the economic performance was driven by investments and a positive foreign trade balance. Final household consumption remained depressed. Total employment grew 0.1% Q/Q 0.3% Y/Y.

News agency Reuters, referring to Bundesbank data analyzed by the IW German economic institute, reports that German direct investment in China rose by 4.3% to a record of €11.9 bn last year. Investment in China as a share of Germany's overall investments abroad rose to 10.3%, the highest level since 2014, while German direct investments elsewhere in Asia were stagnant at around 8%. Overall German foreign direct investment dropped last year to €116 billion from around € 170 billion in 2022 as its economy hovered on the brink of recession, the IW report is quoted. However, the data have to be nuanced as German investments in China in the last four years were financed entirely by reinvested profit and companies have also withdrawn capital. IW economist Juergen Matthes also indicated that one can assume a split between a few big companies and the majority of small and medium-sized companies enterprises with anecdotic evidence suggesting that the latter group is seeking to reduce their engagement with China or even to reduce it entirely. The study illustrates the dilemma German trade policy is facing as it ponders how to manage to risk of its economic exposure to China, its most important trading partner.

Fed’s Goolsbee: Rate cuts tie to confidence on path to inflation target

Chicago Fed President Austan Goolsbee at an even today that inflation would "still be consistent" with the path to 2% target even if it "comes in a bit higher for a few months".

He emphasized that rate cuts should be tied to "confidence in being on a path toward the target", and rejected to wait until inflation actually hit 2% before beginning to cut rates.

"I think it's worth acknowledging that if we stay this restrictive for too long, we will start having to worry about the employment side of the Fed's mandate," he added.

USD/CAD – Two-Month High Ahead of Thursday’s US Retail Sales Report

- US inflation data boosts the dollar

- Retail sales eyed on Thursday for signs of strong demand

- USDCAD may remain rangebound

The US dollar reached a two-month high against its Canadian counterpart on Wednesday on the back of some stronger economic data.

The inflation figures from the US propelled the greenback higher as traders were forced to scale back expectations for interest rate cuts from the Federal Reserve this year.

Next up for the US are retail sales figures for January, due on Thursday, which will give the latest impression of how strong demand is in the world’s largest economy.

The data since last summer has been particularly strong but it’s expected to have cooled in January. The fairytale scenario of a strong economy, lower inflation, and falling interest rates is now looking difficult to achieve so a weaker retail sales report this month may be welcomed.

Rangebound trade continuing in USDCAD?

After seeing resistance around the 50% Fibonacci retracement level on several occasions over the last month, USDCAD finally breached it on Tuesday.

USDCAD Daily

Source – OANDA

It’s still within the correction range though, with the 61.8 Fib now the primary focus. That it coincides with the early November lows makes it an additional level of interest.

That’s not to say it’s clear it will reverse lower from here. Far from it. The 50 Fib level was tested on repeat until it broke and the longer-term trend going back 18 months is rangebound. A rotation lower from a Fib level could suggest a breakout may come but it’s not the clear base case.

Pound Extends Losses After UK Inflation Unchanged

The British pound continues to lose ground on Wednesday. In the European session, GBP/USD is trading at 1.2546, down 0.35%.

UK inflation holds steady at 4.0%

The January inflation report showed that inflation didn’t budge but was lower than expected. UK CPI in January didn’t move the needle and held at 4.0% y/y, unchanged from December. This was below the market estimate of 4.2%. Monthly, CPI declined 0.6%, compared to a 0.4% in December. This was below the market estimate of -0.3%.]

Core CPI remained unchanged at 5.1% y/y for a third straight month and was below the market estimate of 5.2%. Monthly, core CPI declined by 0.9%, following a 0.6% gain and December. This was lower than the market estimate of -0.8%.

Inflation remains double the 2% target, although the Bank of England has made great progress since the dark days when inflation hit 11%. BoE policy makers will be pleased that inflation was lower than expected and the sharp drop in the monthly core CPI is a bright spot.

The Bank of England meets next on March 21th and is widely expected to hold the benchmark rate at 5.25%. The BoE has kept rates unchanged since August and there is pressure on the central bank to provide some relief to households and businesses and lower rates. A rate cut would help stimulate the lethargic UK economy but inflation is well above the 2% target and remains sticky, as evidenced by today’s inflation report. The markets have priced in a rate cut in June around 50-50, with a 74% probability of a rate cut in August, according to Refinitiv Eikon.

A busy week in the UK continues on Thursday, with the release of fourth-quarter GBP. The economy contracted by 0.1% in Q3 and is expected to remain unchanged in the fourth quarter. This would indicate two consecutive quarters of contraction which signals a technical recession. If the estimate is wide of the actual release, it could result in volatility for the British pound on Thursday.

GBP/USD Technical

- GBP/USD is testing support at 1.2541. Below, there is support at 1.2505

- There is resistance at 1.2617 and 1.2661x

GBP/USD: Cable Falls Further After Below-Forecast UK January Inflation

Cable extends weakness into second straight day, initially deflated by stronger dollar on unexpectedly hot US inflation on Tuesday, while today’s softer than expected UK CPI data raised bets for BoE rate cut by June and added pressure on sterling.

Wednesday’s drop broke below 200DMA (1.2562) and pressured pivotal Fibo support at 1.2525 (38.2% of 1.2037/1.2827 rally / Feb 5/6 lows).

Daily close below 200DMA is seen as a minimum requirement to keep fresh bears in play, while firm break of 1.2525 would generate reversal signal and open way towards next key supports at 1.2458/32 (daily cloud base / 50% retracement).

Falling 10DMA (1.2615) marks initial resistance, guarding upper pivots at1.2650 zone (converged daily Tenkan/Kijun-sen) and 1.2690 (daily cloud top).

Res: 1.2615; 1.2650; 1.2670; 1.2690.

Sup: 1.2525; 1.2500; 1.2488; 1.2432.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 188.87; (P) 189.48; (R1) 190.50; More...

Intraday bias in GBP/JPY is turned neutral with current retreat and some consolidations could be seen first. Downside should be contained well above 185.21 support to bring another rise. Break of 190.05 will resume larger up trend to 61.8% projection of 178.71 to 188.90 from 185.21 at 191.50.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

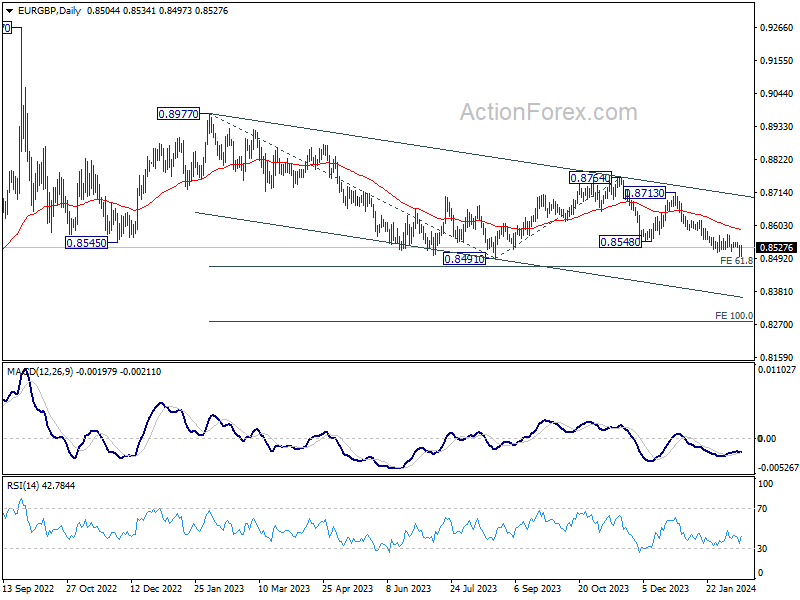

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8513; (R1) 0.8526; More...

Intraday bias in EUR/GBP is turned neutral with current recovery. But further decline is expected as long as 0.8571 resistance holds. Current fall is seen as part of the larger down trend. Break of 0.8497 will target 0.8464 projection level.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.73; (P) 150.31; (R1) 151.37; More...

USD/JPY's rally from 140.25 is still in progress and intraday bias stays on the upside for 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. On the downside, below 149.24 minor support will turn bias neutral and bring consolidations, before staging another rally.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.