Sample Category Title

BoC to Hold Key Overnight Rate Steady Next Week

Economic data releases since the Bank of Canada opted to forego an interest rate hike in September have been mixed, but we expect that they on net have made a hike at next week’s decision unlikely. Inflation has surprised on the upside relative to the central bank’s last forecasts in July. But most of that was driven by rising energy inflation more recently as global oil prices edged higher. The latest CPI data for September also looked decidedly better, with slower growth in the BoC’s preferred ‘core’ measures breaking a string of upside surprises.

Underlying inflation pressures in Canada are still running well above the 2% inflation target, but softer economic growth numbers and the central bank’s own Business Outlook Survey (BOS) suggest that price growth will continue to decelerate. The Q3 BOS showed Canadian businesses have not yet returned to ‘normal’ pricing practices, but the frequency and size of price adjustment has been moving back towards pre-pandemic trends. Easing cost pressures have contributed to that, but softening consumer demand has likely also played a big role as well. Indeed, 60% of consumers surveyed in the separate Canadian Survey on Consumer Expectations reported having reduced spending in Q3 to combat elevated inflation and rising interest expenses.

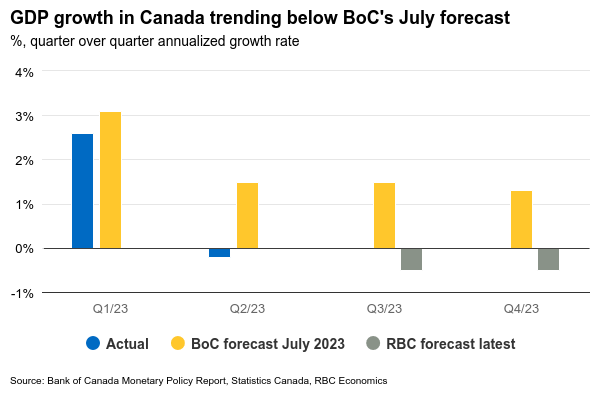

And interest rates are already at levels that should continue to slow consumer demand over time, as they pass through to increase household debt payments with a lag. Overall GDP growth is tracking well-below the BoC’s last forecasts in July, contracting 0.2% in Q2 instead of the 1.5% annualized growth the BoC expected. The change also looks substantially softer on a per-capita basis controlling for surging population growth. We are tracking another small GDP decline (-0.5%) in Q3 (BoC at +1.5%.) And labour markets are showing signs of softening with the unemployment rate up half a percentage point from the spring. Near-term inflation projections will very likely be revised higher given the rise in energy prices into the fall. But with signs the economy is cooling, we expect the BoC will likely maintain their call for a more gradual return back to the target inflation rate, somewhere in late 2024 or early 2025.

Week ahead data watch

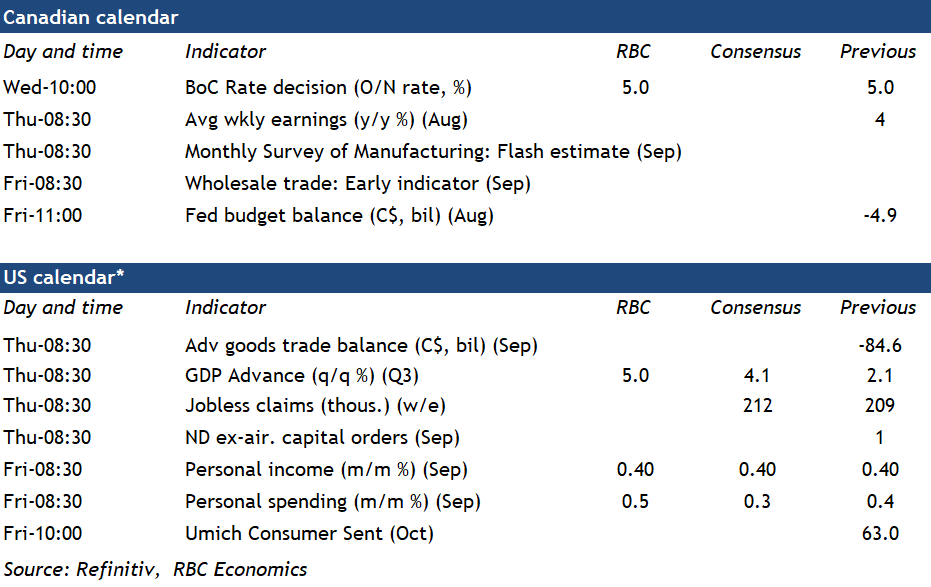

U.S. personal spending likely ticked up 0.5% in September due to strong retail sales (+0.7%) data for that month. We expect personal income to have edged up 0.4%, given earlier released September payroll report showed a deceleration in wage growth (+0.2%) during that month.

Q3 U.S. GDP is tracking a 5% quarter over quarter annualized increase on firm consumer spending, a larger net trade build and a jump in inventories.

For Canada, we look for more signs of softening labour demand from the August SEPH report. Job openings have been declining, and we expect that trend to continue. Employment growth from the latest Labour Force Survey was still robust, but the unemployment rate has ticked higher to 5.5% since spring, consistent with ongoing softening in labour demand.

A Low-Tolerance RBA Won’t Yet Have Seen Enough to Move

The main domestic data this week was the September labour force release. As colleague Westpac Economist Ryan Wells noted yesterday, the data were a mixed bag. Looking through the monthly noise, the labour market is continuing to cool gradually from its earlier tightness. There was nothing in the data to nudge the RBA in the direction of raising rates.

The Reserve Bank minutes released this week show a Board that has no appetite to let inflation stay high for any longer than their current forecasts imply. If the inflation outlook remains on its current trajectory, the Board will keep the cash rate where it is. If the data start pointing to material risks of higher outcomes than that, though, they are very willing to move.

Governor Bullock's fireside chat earlier this week had nothing in it to change our views about the path of policy. The Governor did take pains to emphasise that the Bank is aware that the policy tightening is making things difficult for some parts of the community. Ms Bullock will be speaking twice more between now and the November Board meeting. The event on Tuesday could be an opportunity to set out her thinking about the outlook or the framework for policy, given it is her first setpiece speech since becoming Governor. The appearance before Senate Estimates on Thursday is likely to cover a wider range of issues, though some senators might want to probe Ms Bullock and Assistant Governor Kent about any implications for policy of the CPI release the day before.

The RBA's four near-term inflation worries

Today we released the Westpac Economics preview for the September quarter inflation release. Senior Economist Justin Smirk notes that we are expecting both headline and trimmed mean inflation to print a 1.1% quarterly increase. It would have to be a significant upside surprise from this to dislodge the RBA Board from an unchanged rates decision in November. That said, there are several upside risks to inflation that would have the Bank's attention.

- Goods prices not unwinding quickly enough (receding risk). Much of the surge in inflation globally reflected the demand shifts and supply chain issues induced by the pandemic. This is now receding and, in some countries, core goods prices are outright falling. The Bank has from time to time flagged a risk that this reversal in prices would happen too slowly, but so far this risk doesn't seem to be materialising.

- Domestic demand and services price inflation remaining too high (steady, concerning). Even though consumer demand in Australia is weak overall, there are pockets of strong demand and cashedup households. In these areas, services businesses are managing to raise prices noticeably. Services inflation is still uncomfortably high, and the experience overseas has been that it can be quite sticky and slow to come down.

- Labour costs (receding). If domestic demand were to remain strong enough, this would tend to boost both services prices and wages growth. Heightened risks to the inflation outlook from this source was one of the factors the Bank cited to explain its decision to raise rates in June. But the October minutes show that the Board is now less worried about this possibility, noting "…that there were few signs of the risk of a price-wage spiral materialising". It also pointed to non-award wages growth moderating. Poor productivity outcomes are still a concern given their influence on unit labour costs. Overall though, the Bank is sounding more sanguine about wages recently, in light of the data flow on both wages themselves and the labour market.

- Energy costs (electricity receding, oil increasing). The Bank took some comfort from the smaller pass-through from default offers to actual electricity prices. In contrast, the Middle East conflict means oil prices have increased again. Short-term fluctuations in petrol prices would not induce the Board to shift policy. But sustained increases in energy costs, whether for geopolitical reasons or related to climate transition, would involve a more difficult trade-off.

Three broader risks

On top of these proximate risks to the inflation outlook, there are a range of more medium-term risks. Three of these are particularly front of mind currently.

First, housing prices have picked up, which is not what you would have expected given higher interest rate and weak income growth. Australia is not alone in this; it has been seen in a range of economies where population growth has picked up sharply, such as Canada. In principle, the resulting higher wealth would boost consumption and so domestic demand and inflation. But as the RBA minutes noted, this effect partly depends on housing turnover picking up. And further rapid price increases would be hard to square with the recent step down in auction clearance rates.

Second, the outlook for China is beset by headwinds. While activity has gained some momentum after an initially slow recovery from COVID lockdowns (despite problems in the property market), the medium-term outlook is more clouded. It is no longer in the phase of fast catch-up to the rest of the world or the most obvious destination for foreign investment into low-cost production. Its population is already ageing and shrinking and the policy environment is geared more to control than to growth. The implications for Australia's export base are material and we can expect markets to mark down the Australian dollar whenever these concerns come to the fore.

Third, long bond yields have risen to levels last seen more than a decade ago. In the short term, markets have been unsettled by the US congressional dramas and the conflict in the Middle East. But there is a longer-term element to this: if fiscal policy globally is less contractionary than it was in the period between the GFC and the pandemic, monetary policy does not have to offset this with lower interest rates. So it is possible that the structure of global interest rates will be a bit higher in future than it was in that period. To the extent that this is a risk rather than market participants' solid expectation, this could be one contributor to higher term premia.

Week Ahead – ECB Meeting and US GDP to Shake FX Markets

- Central bank decisions in Eurozone and Canada coming up

- But FX traders will likely focus more on the US GDP report

- Is the dollar set to realign with its superior fundamentals?

Dollar turns to GDP stats for fuel

The US economic machine continues to fire on all cylinders. Shielded by the government’s enormous deficit spending and the slow transmission of high interest rates because of fixed-rate mortgages, the United States has defied expectations of an economic slowdown and instead enjoyed a stellar performance this year.

Beyond the Biden administration’s heavy spending, a historically tight labor market has also helped support household incomes, keeping consumption on a solid footing. Overall, it appears that the US economy reaccelerated over the summer, something the upcoming GDP numbers will probably confirm on Thursday.

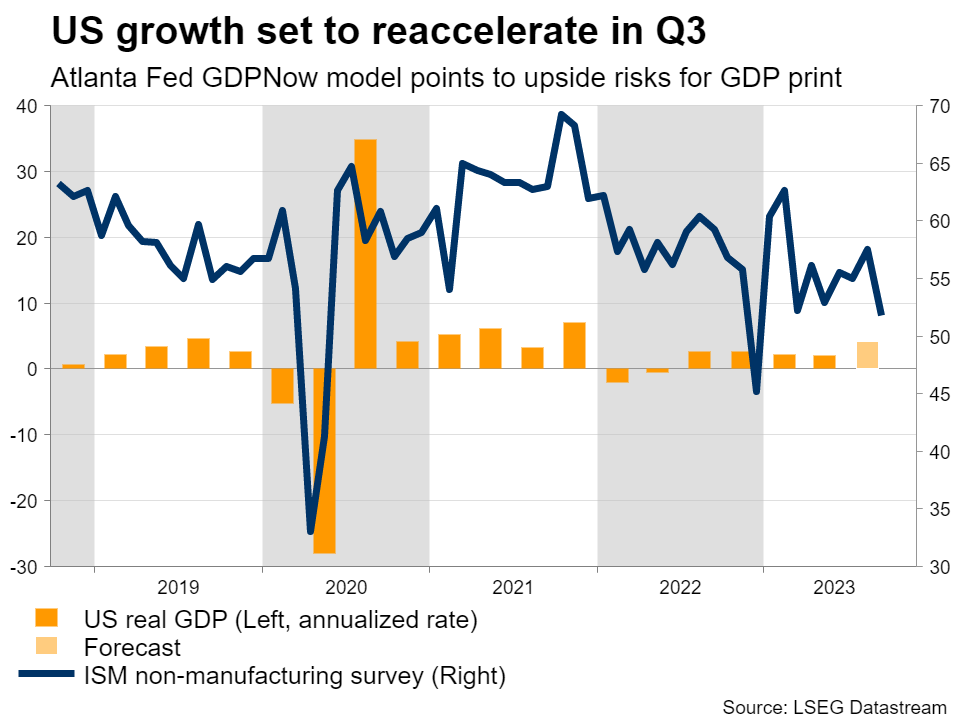

Economic growth is projected to have reached an annualized pace of 4.1% in the third quarter, almost double the 2.1% in the previous quarter. While this would be impressive in itself, there is even some scope for an upside surprise.

The Atlanta Fed has a model that estimates GDP in real time, and it currently points to growth of 5.4% during the quarter, much higher than official forecasts. This model has an accurate track record, so if anything, a positive GDP surprise seems more likely than a disappointment.

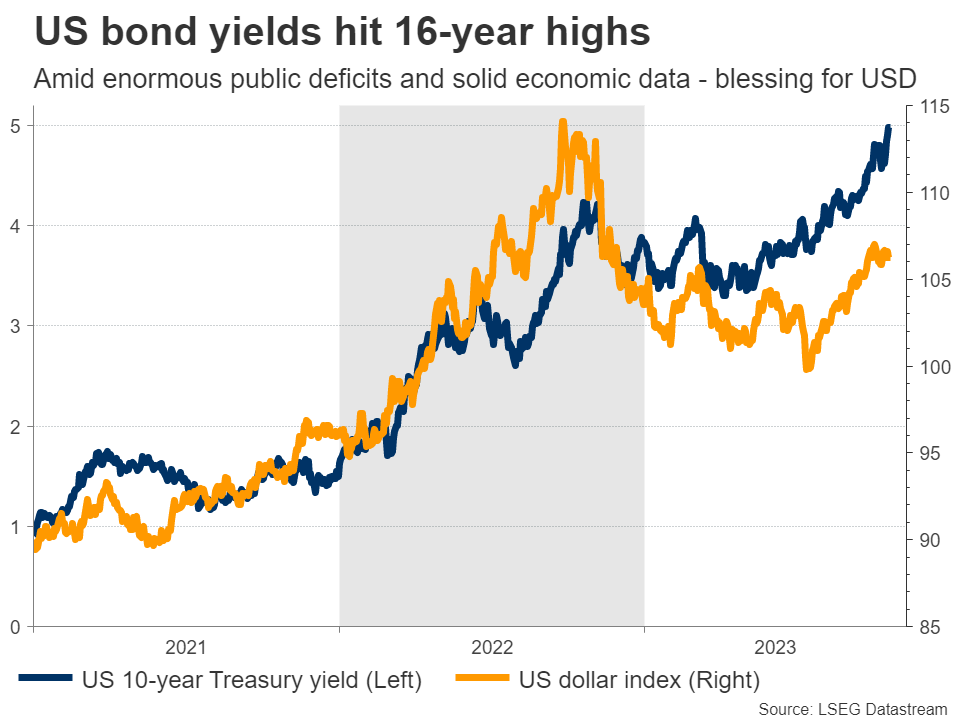

A stronger-than-expected GDP print could help the US dollar to resume its rally. The dollar’s uptrend has been fueled by a combination of solid economic fundamentals, the stunning rise in US yields, and the absence of any viable alternatives in the FX space. These factors are still in play, therefore, the outlook for the dollar remains bright.

Boasting the strongest economic growth among the G10 nations and the highest real interest rates, the dollar has turned into an attractive investment destination. In contrast, Europe and China are battling a severe economic slowdown, while the yen has been crushed by the Bank of Japan’s refusal to raise rates.

Of course, there are some risks on the horizon. Consumer savings from the pandemic have started to run out and US student debt repayments have resumed, which could dampen growth next year. But even accounting for these risks, the dollar still appears better positioned than its FX competitors, especially when adding its safe haven qualities into the calculation.

Aside from Thursday’s GDP report, there are several other US releases that could impact markets next week, including the S&P Global business surveys on Tuesday and the core PCE price index on Friday.

ECB meeting could be quiet

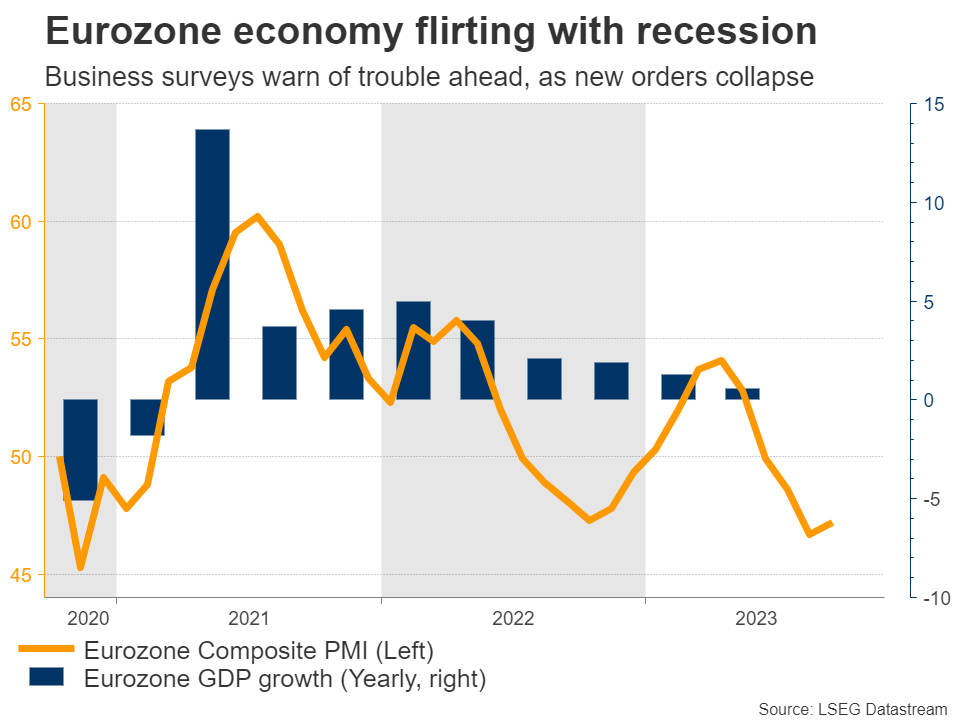

Crossing into the Eurozone, the central bank will announce its decision on Thursday. Markets are pricing in almost no chance of a rate increase, after the ECB signaled that rates have likely reached their peak for this cycle.

Incoming data releases point to an economy headed downhill, justifying this cautious approach. New business orders are falling at the fastest pace in three years, which is an ominous sign for economic activity. Meanwhile, consumers are being squeezed by rising mortgage costs and the resurgence in oil prices.

Hence, even though inflation is still elevated, the ECB is highly unlikely to raise rates again, as storm clouds of a recession are gathering. In fact, the key question now is how long it will take before the ECB begins to cut rates.

All told, this meeting might be a quiet event. With no scope for action, the focus will be on forward guidance. That said, policymakers probably won’t provide any concrete signals while the outlook is so uncertain. President Lagarde may strike a neutral tone, indicating that rates could remain at current levels for some time.

Instead, the latest business surveys on Tuesday might prove more important in shaping rate-cut bets and by extension for driving the euro. These PMI surveys are considered leading indicators, so if they continue to flash warning signs about a worsening economic slowdown, that could spell more trouble for the bruised euro.

Business surveys for October will also be released in the UK on Tuesday, alongside the latest batch of employment data. The British labor market lost jobs in the summer and a continuation of this trend could hammer the pound, as it would raise the risk of recession.

BoC to remain sidelined

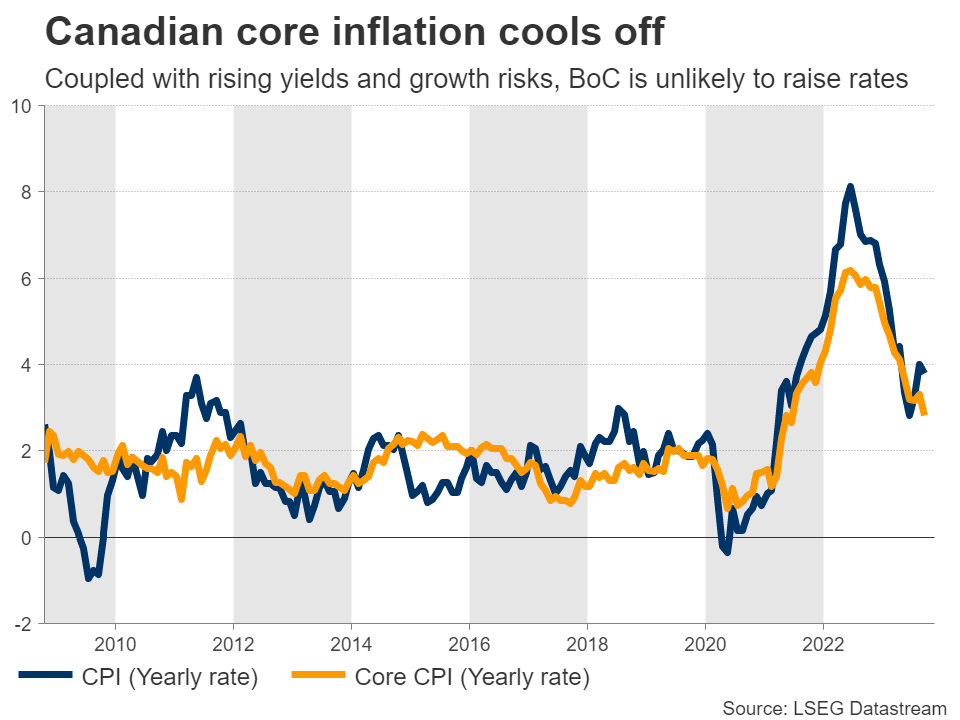

On Wednesday, the Bank of Canada will unveil its own decision and markets assign only a 15% probability to a rate increase. Inflation continues to cool, with the core CPI rate falling to 2.8% in September. Coupled with the steady rise in Canadian yields lately, which has similar effects to raising rates, this puts less pressure on the central bank to act again.

Reinforcing this notion are the gloomy signals from the BoC’s quarterly business survey. Canadian firms reported escalating concerns about weaker demand and noted fading pressure on wages, a combination that points to slower growth and colder inflation readings ahead.

Therefore, the BoC might disappoint those betting on an immediate rate increase next week, which argues for a negative reaction in the Canadian dollar. That said, the currency’s broader path will also depend on several other factors, such as the unfolding crisis in the Middle East and its implications for oil prices.

Finally on the data front, the quarterly inflation report from Australia will be released Wednesday, while in Japan, the latest Tokyo inflation prints are out on Friday.

Weekly Focus – Risk of Escalation in Middle East Drives Oil Prices Higher

Geopolitics has taken centre stage in financial markets once again. As the risk of escalation in Middle East grows, oil prices continue to drift higher (breaching USD 93 level), raising stagflationary concerns for the global economy. Israel continues its air attacks in Gaza and prepares for a ground operation. Meanwhile, the US has seen stepped up drone attacks targeting its military bases in Iraq and Syria. Further underlining the risk of an escalation, fighting is also taking place in the north of Israel between the Israeli Defence Forces and Lebanon's Hezbollah (Iran's proxy), and in the Syrian border region.

In order to anticipate how the conflict may evolve from here, we think it is crucial to understand the geopolitical and cultural context in the Middle East, most importantly, the different religious factions within Islam. In our Geopolitical radar - Risk of escalation in Middle East, Xi-Biden meeting in November, tensions rise on Baltic Sea, 19 October, we analyse who benefits and who loses from chaos in Middle East. Overall, we hear echoes familiar from Arab Spring, and think that the long-standing conflict between Muslim Brotherhood (supported by Turkey and Qatar) and its opponents (mainly Saudi Arabia, UAE and Egypt) may end up playing a role in how political instability spreads in the region.

Apart from geopolitics, attention remains on the rise in long yields, driven both by a rising term premium and a stronger than expected macro momentum. This week, Fed chair Powell echoed the slightly cautious tone of his colleagues' recent speeches, highlighting that the tightening financial conditions 'takes some pressure off the Fed' to continue hiking police rates and that the FOMC is 'proceeding carefully'. Next week, the market will keep a close eye on the US October flash PMIs on Tuesday and the Q3 flash GDP release on Thursday. We expect the former to show gradual cooling in services sector activity growth, while any further upticks in the manufacturing index are likely to remain modest for now. We expect GDP to have grown by 3.3% q/q AR, driven by still upbeat private consumption and structures investment. While growth has remained stronger than we have anticipated for now, we still foresee weakening towards the winter not least amid tightening financial conditions, and think the Fed is done with hiking rates.

Next week's main event will the ECB meeting on Thursday, where the Governing Council is widely expected to keep rates unchanged (see ECB Preview - Keeping a tightening bias with optionality, 17 October). As the ECB has opted to work with the 'patience' argument, it will now be crucial to follow the speed of the monetary policy transmission to predict their next move. If the speed is low, more patience will be needed and rates should be kept higher for longer, but if the speed is high, the first rate cut could come earlier. In this regard, the bank lending survey due on Tuesday will provide valuable input to this discussion through updated data on changes in lending standards and credit demand.

Flash PMIs will be released for euro area and the UK as well, we expect both to remain in contractionary territory across the board. We also get the rest of the UK labour market report on Tuesday after wage numbers were released this week. We expect the numbers to continue to show weakness as slack is set to gradually increase.

Sunset Market Commentary

Markets

The rejected tests of the psychologic 5% mark in the US 5-yr and 10-yr yields yesterday had their technical consequences today. In absence of economic data on both sides of the Atlantic and with Fed Chair Powell closing the curtain on the early November policy meeting, core bonds got some breathing space. Especially since genuine risk aversion is today’s main trading theme. Key European stock markets lose up to 1.5% for the German Dax. The EuroStoxx 50 sets a new sell-off low at 4040 with the YTD low at 3980 coming narrowly close. If any, the index is clearly in a sell-op-upticks pattern. The dollar fails to really cash on the situation with EUR/USD near opening levels at 1.0585 and USD/JPY fighting to live another day below 150. Gold rallies to its highest level since early August, trading just shy of $2000/ounce. Daily changes on the US yield curve range between -3.9 bps (3-yr) and +1 bp (30-yr). German yields trade between -5.9 bps lower (2-yr) and 2.3 bps higher (30-yr). The front end outperforms in the run-up to next week’s ECB meeting where the central bank is widely expected to skip on a rate hike, buying time to assess the data by the December policy update. Most ECB-members keep a very open approach (stable rates or higher) between now and March of next year. Only then, it might be (at the earliest) possible for them to firmly conclude that the disinflationary process is on track to meet the 2% inflation target on a sustainable basis. Despite the status quo, deliberations on making monetary policy more restrictive via extracting excess liquidity remain ongoing. More specifically, the central bank is looking into ending its reinvestment policy from its Pandemic Emergency Purchase Programme ahead of the currently flagged end of 2024. The Italian 10yr yield spread vs Germany widens marginally (+1 bp to 203 bps) ahead of tonight’s S&P rating update. The rating agency currently applies a BBB rating with a stable outlook. While a downgrade will likely be avoided, S&P might apply a negative outlook given deteriorating public finances. In coming weeks, Fitch (Nov 10) and Moody’s (Nov 17) give updates as well. Fitch holds a similar rating as S&P for the moment, while the Italian rating is already the lowest investment-grade rating at Moody’s (Baa3) including a negative outlook. It’s of the utmost importance for the country(‘s debt) to avoid a drop into junk territory. UK Gilts are well-bid as well this morning with the front end of the curve even outperforming Europe. UK Gilt yields fall by up to 8 bps (2-yr) this morning after weak UK retail sales round up this week’s economic update following dismal, but incomplete labour market figures and broadly in-line inflation data. They suggest a firm hold by the Bank of England even as the economy likely needs a firmer monetary policy to battle inflation. The other side of the medal is an outperformance at the very long end of the curve (30-yr +6 bps; testing last year’s high at 5.14%) through rising inflation expectations. EUR/GBP broke through the 0.87 resistance area (July & September high + 200d mavg).

News & Views

The monthly consumer survey of the National Bank of Belgium showed consumer sentiment unchanged at -5. After last month’s dip, saving intentions climbed significantly in October. Household confidence in the macroeconomic picture for the next twelve months slipped back to the level seen in August (-17 from -13). Households also expressed greater concern over future developments in the labour market (unemployment index from 12 to 15). On a personal level, households s revised their saving intentions upwards (13 from 7). Expectations for their own financial situation remained unchanged from last month. This month's survey was completed just prior to these terrorist attack in Brussels on 16 October, which, may influence the survey results.

The Chinese Ministry of Commerce today announced that it will require export permits for some graphite products that are used in batteries for electric vehicles. China is the biggest world producer and exporter of the materials. The Ministry said that the measure was “conducive to ensuring the security and stability of the global supply chain and industrial chain, and conducive to better safeguarding national security and interests". The move comes a few days after the US also announced controls on exports to China of AI-related ships. China said that the measure isn’t targeting any specific country. Aside from the US, mostly Asian countries including South Korean and Japan are importing graphite products from China.

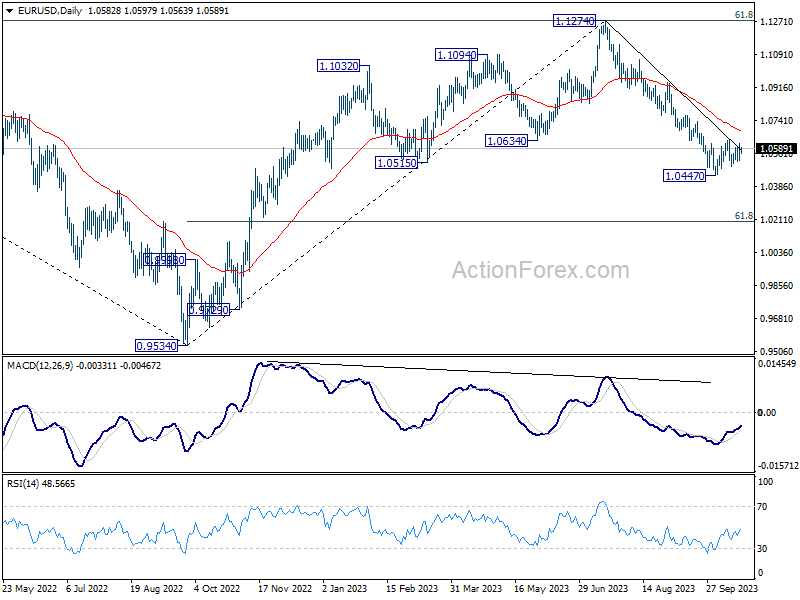

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0535; (P) 1.0575; (R1) 1.0623; More...

EUR/USD is still extending range trading and intraday bias stays neutral. Outlook remains bearish with 1.0639 resistance intact. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0684).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0684) holds, in case of rebound.

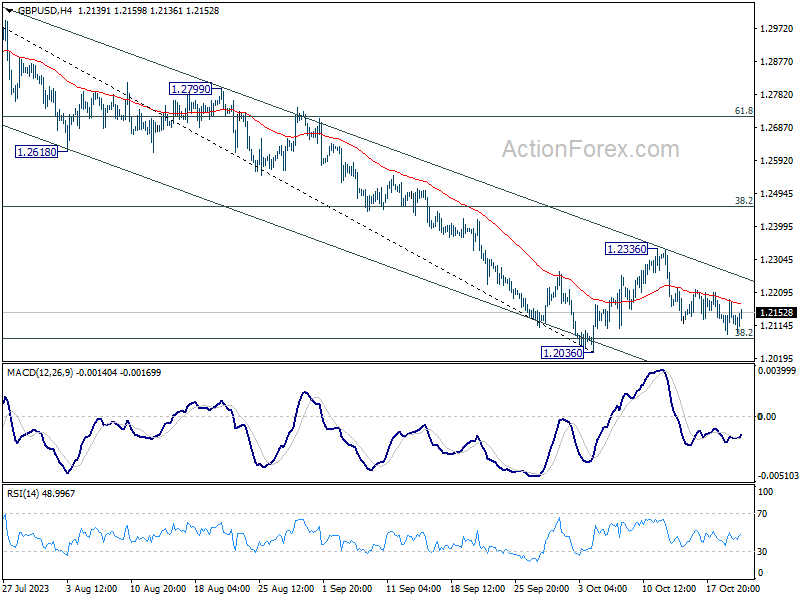

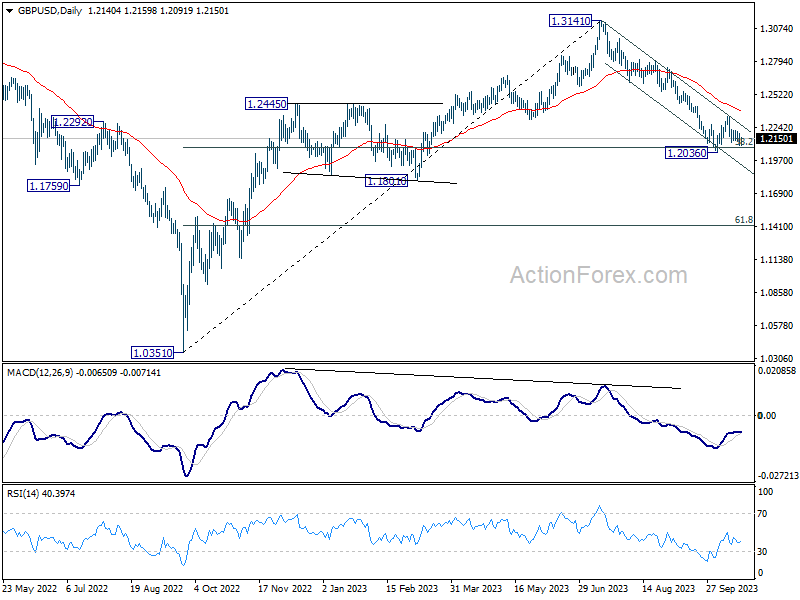

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2091; (P) 1.2142; (R1) 1.2193; More

Intraday bias in GBP/USD remains neutral for more consolidations. Also, outlook remains bearish with 1.2336 resistance intact. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will resume the rebound from 1.2036 to 55 D EMA (now at 1.2374).

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2374) holds, in case of rebound.

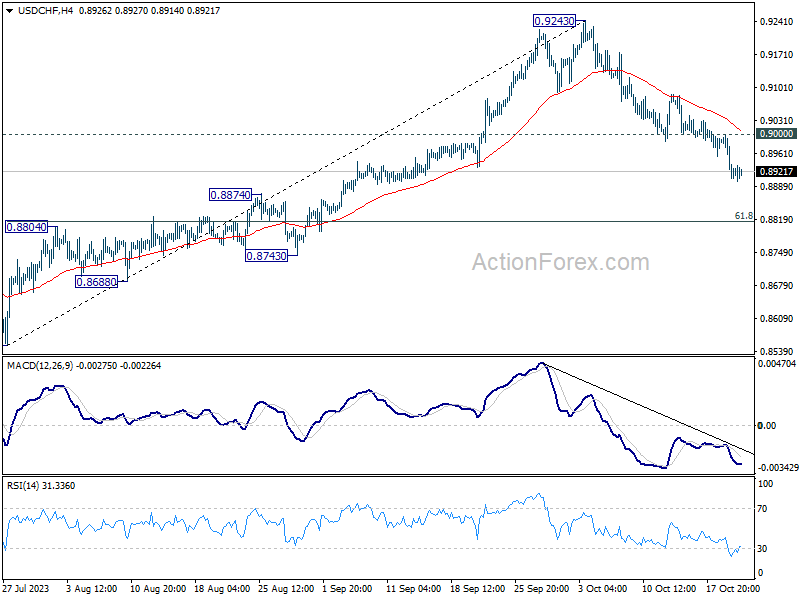

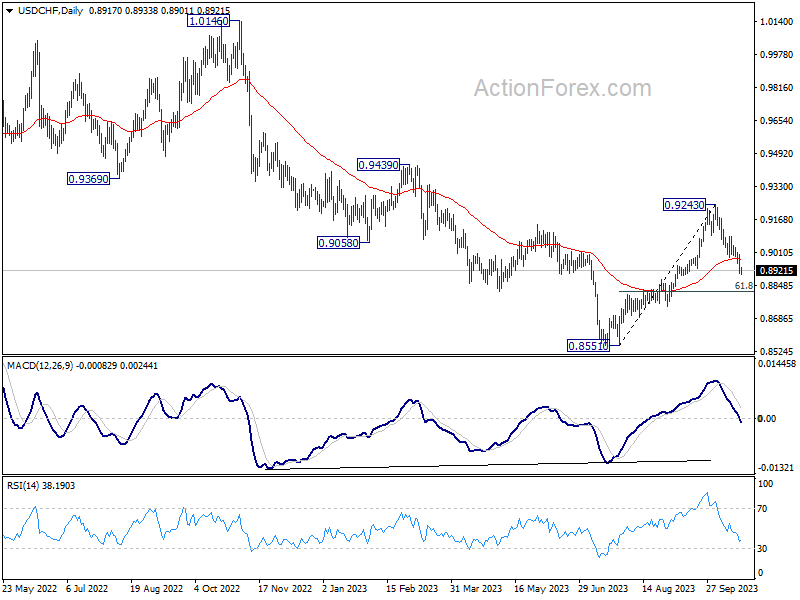

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8882; (P) 0.8942; (R1) 0.8975; More....

Intraday bias in USD/CHF stays on the downside at this point. Current fall from 0.9243 should target 61.8% retracement of 0.8551 to 0.9243 at 0.8815 next. Sustained break there will pave the way to retest 0.8551 low. On the upside, above 0.9000 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, the firm break of 55 D EMA (now at 0.8974) argues that rebound from 0.8551 might be completed as a correction at 0.9243. In other words, larger fall from 1.0146 (2022 high) is possibly not over yet. Risk will now stay on the downside as long as 0.9243 resistance holds. Firm break of 0.8551 will confirm down trend resumption.

Canada: Retail Sales Decline in August

Retail sales declined 0.1% month-on-month (m/m) in August, coming in better than Statistics Canada's advance estimate for a 0.3% m/m decline, but in line with expectations. July's print was revised up to 0.4% m/m from 0.3% m/m reported in the advance estimate.

Adjusting for inflation, the volume of retail sales was 0.6% lower on the month.

Sales at motor vehicle and parts dealers fell by 0.9% m/m - the second consecutive month of declines. Ex-auto, sales were up 0.1% m/m, above the consensus expectations for a decline of the same magnitude.

Sales growth at gasoline stations and fuel vendors were up 2.8% as gas prices accelerated thanks to a recent spike in oil prices. In volume terms, receipts were down 2.9% m/m in August.

Excluding sales at car dealerships and gas stations, core retail sales were down 0.3% in August. The 1.2% m/m decline in sales at food and beverage stores was the major driver of this loss, but most other categories were also in the red in August.

Only three other major categories reported gains in August: health and personal care stores (+1.2% m/m), electronics and appliance stores (+0.3% m/m), general merchandise stores (+0.3% m/m).

E-commerce sales also dwindled, losing 2.0% m/m in August following three consecutive months of strong gains.

According to Statistics Canada, approximately 12% of Canadian retailers reported that their business activities in August had been affected by the strike at the ports in British Columbia..

Based on the answer of 36.5% of companies surveyed, advanced estimate for the month of September points to a flat reading. This is better than are own estimate of consumer activity based on TD debit/credit card spending, which points to a decline in September.

Key Implications

Retail sales were weak in August, but with July's upward revisions this wasn't enough to put the third quarter's already modest consumer spending profile at risk. We expect personal consumption expenditure to be fairly anemic in the third quarter, advancing at only a 1-1.5% pace, in line with our internal spend data.

The balance of risks for the Canadian economy is slowly swinging to the downside as consumer confidence continues to be soured by the Bank of Canada's rate hikes and elevated inflation. This certainly allows the Bank to remain on the sidelines at next week's decision. We expect that moderating demand tempers inflation going forward, while keeping spending just slightly below sub-trend without sending disruptive ripples through the economy.

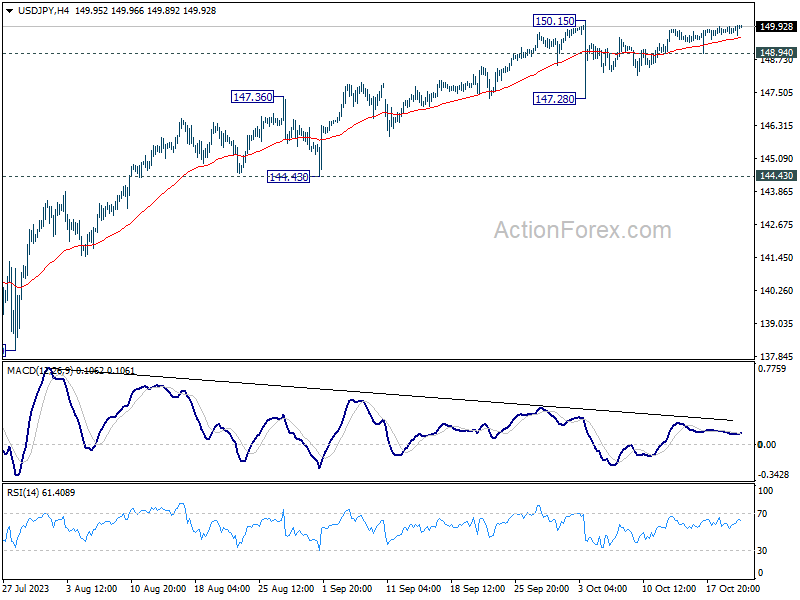

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.66; (P) 149.81; (R1) 149.96; More...

Intraday bias in USD/JPY stays neutral for the moment as range trading continues. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.