Sample Category Title

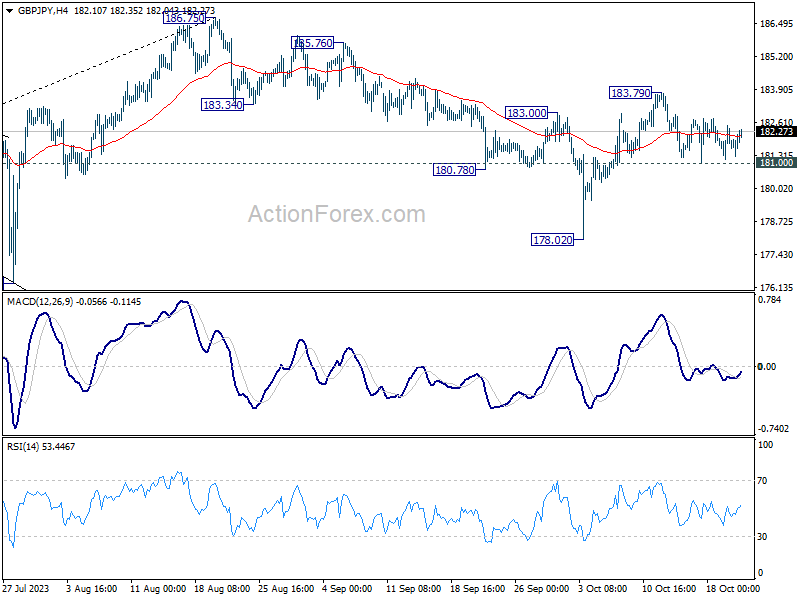

GBP/JPY Weekly Outlook

GBP/JPY stays in sideway trading below 183.79 last week and outlook is unchanged. Initial bias remains neutral this week first. The favored case is still that correction from 186.75 has completed at 178.02. Above 183.79 will resume the rise from 178.02 to retest 186.75 high. However, break of 181.00 will dampen this view, and turn bias back to the downside for 178.02 instead.

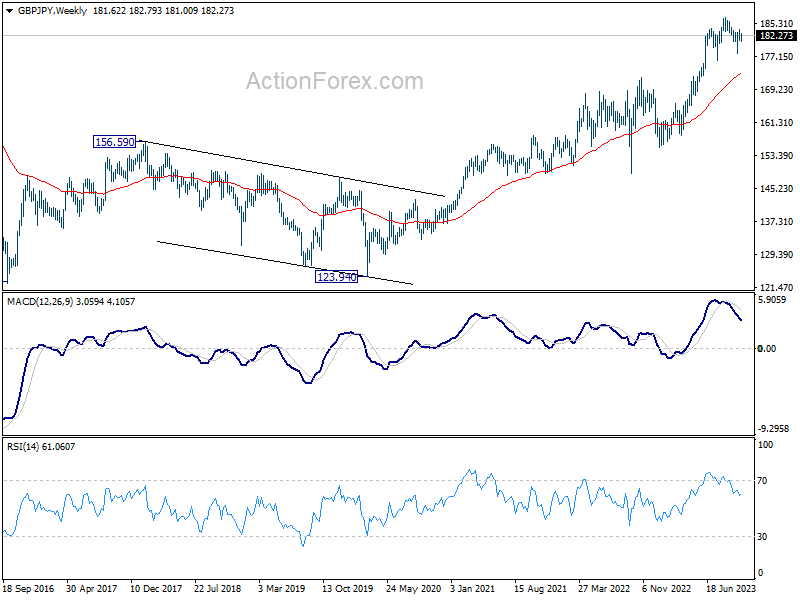

In the bigger picture, fall from 186.75 is seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

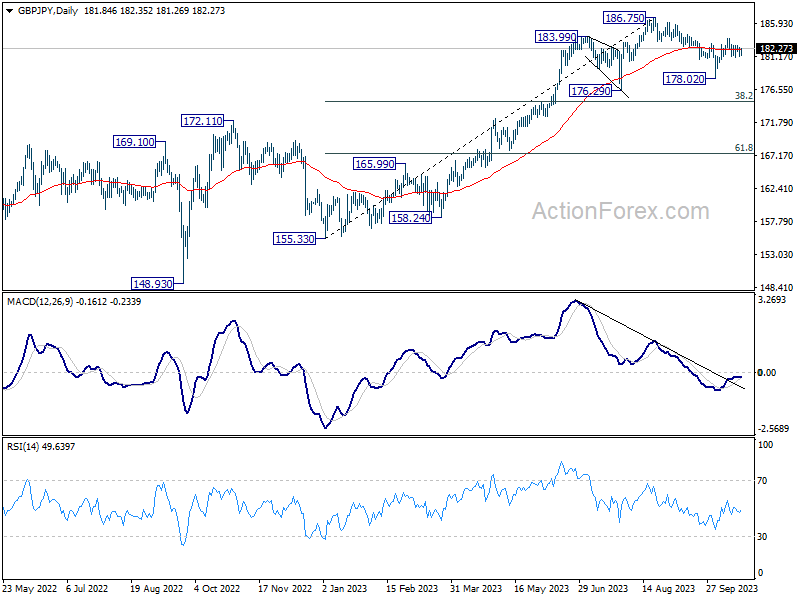

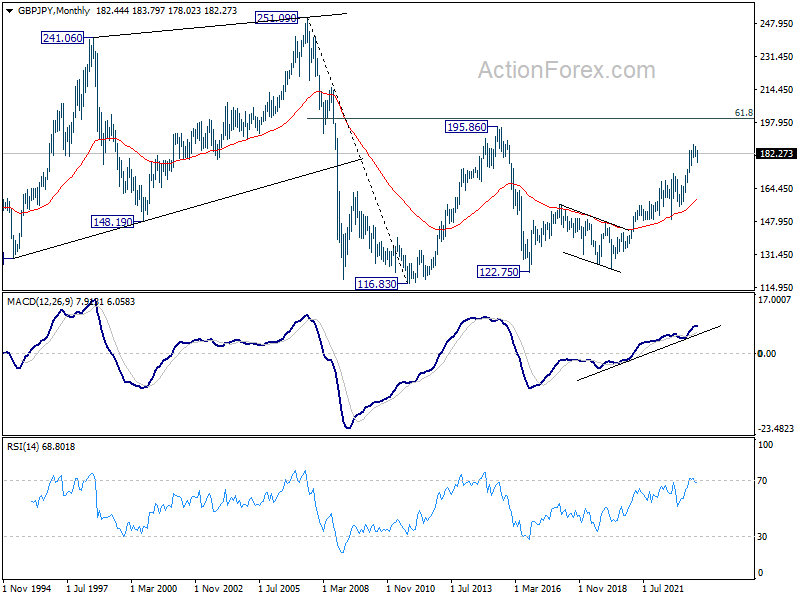

In the longer term picture, rise from 122.75 (2016 low) in still in progress but started losing upside momentum as seen in W MACD. Further rise will remain in favor, though, as long as 176.29 support holds, to retest 195.86 (2015 high).

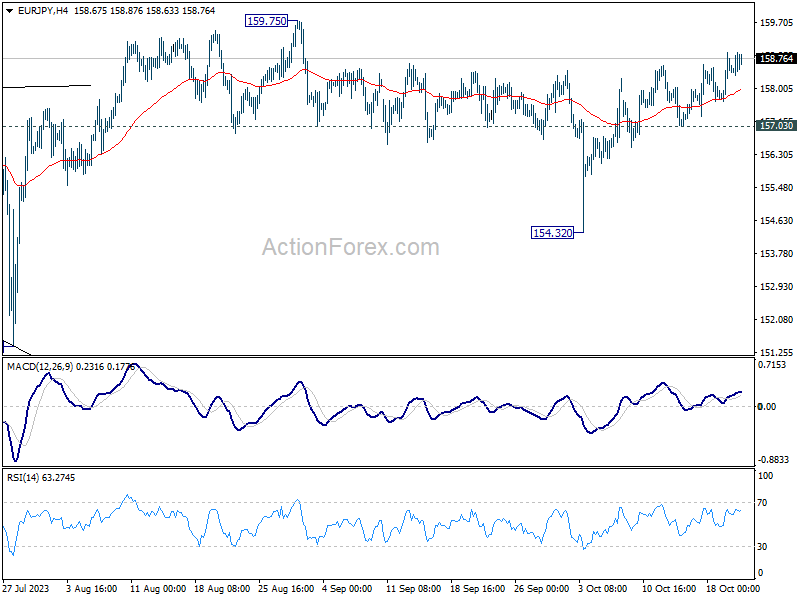

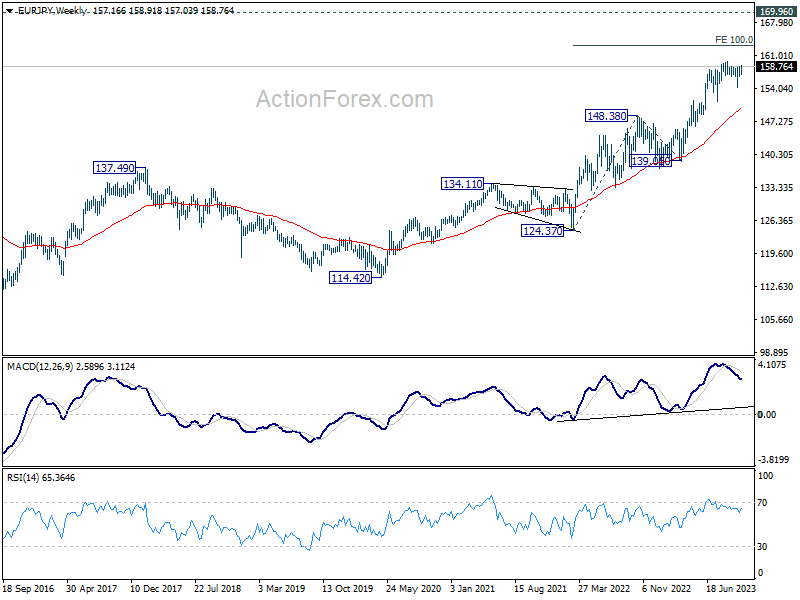

EUR/JPY Weekly Outlook

EUR/JPY spiraled higher last week as rebound from 154.32 extends. Initial bias stays on the upside this week for retesting 159.75 resistance. Decisive break there will resume larger up trend. On the downside, break of 157.03 support is needed to signal completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, price actions from 159.75 are views as a corrective pattern. As long as 151.39 support holds, rise from 114.42 (2020 low) is expected to continue through 159.75. Next target will be 100% projection of 124.37 to 148.38 from 139.05 at 163.06.

In the long term picture, rise from 109.03 (2016 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high).

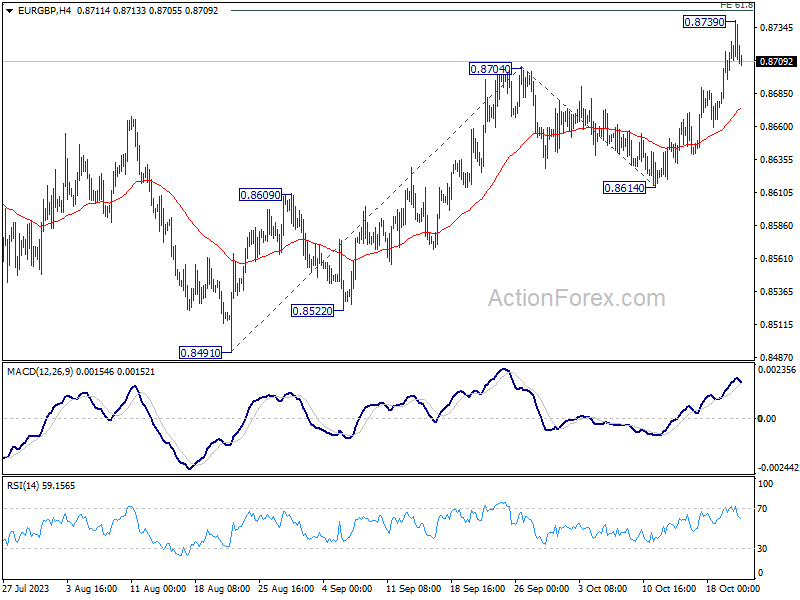

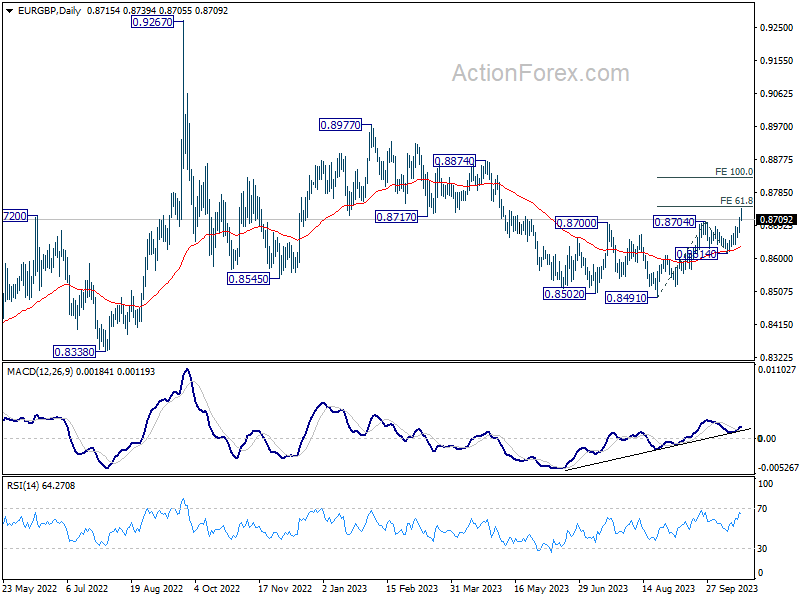

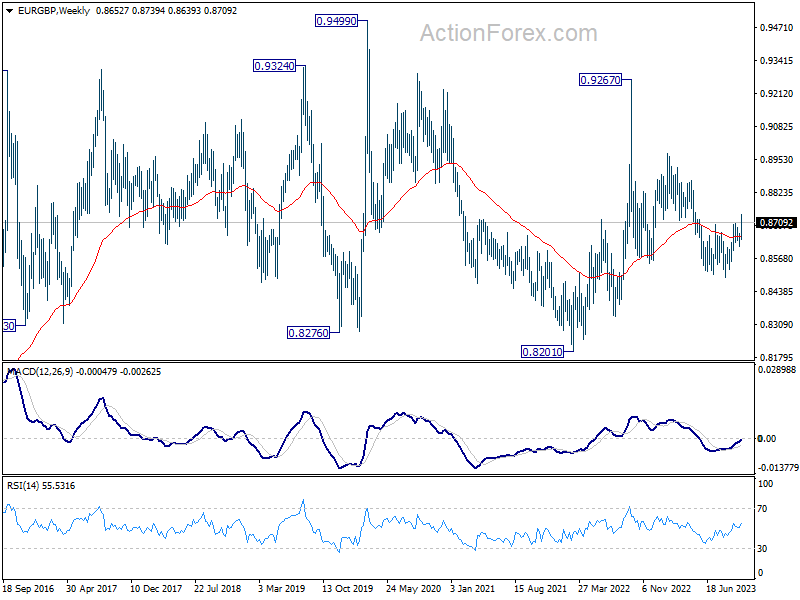

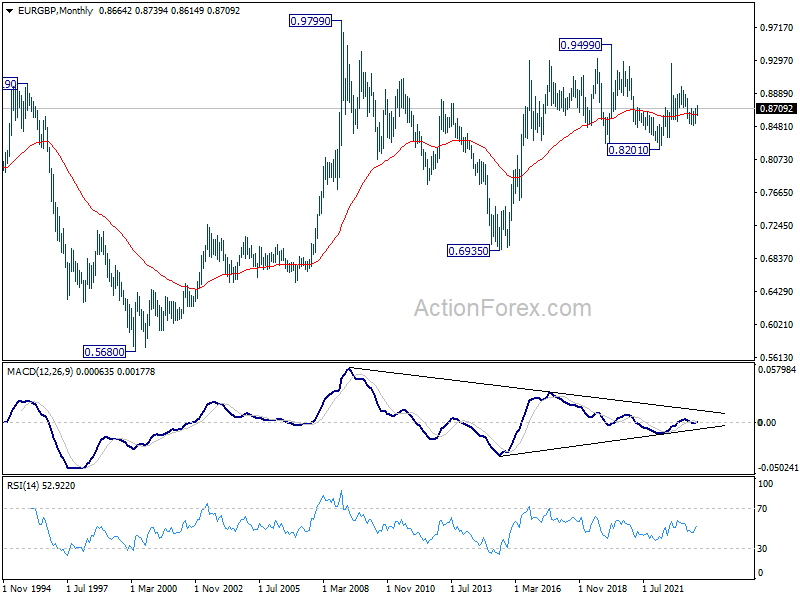

EUR/GBP Weekly Outlook

EUR/GBP's rise from 0.8491 resumed by breaking through 0.8704 resistance last week. But it retreated after hitting 0.8739, just ahead of 61.8% projection of 0.8491 to 0.8704 from 0.8614 at 0.8746. Initial bias is turned neutral this week for consolidations first. Downside of retreat should be contained well above 0.8614 support to bring another rally. Firm break of 0.8746 will target 100% projection at 0.8827 next.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will now remain the favored case as long as 0.8614 support holds.

In the long term picture, long term range pattern is extending. But rise from 0.6935 (2015 low) is expected to resume at a later stage, to 0.9799 (2009 high).

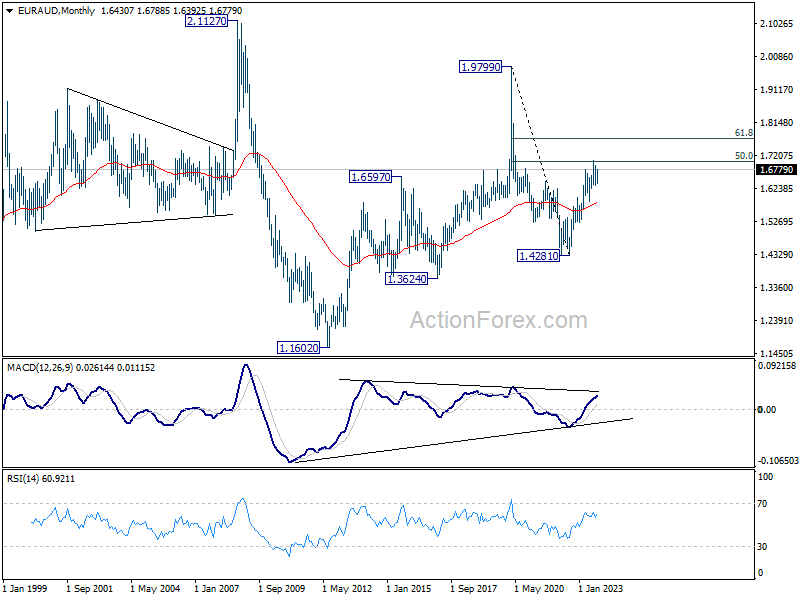

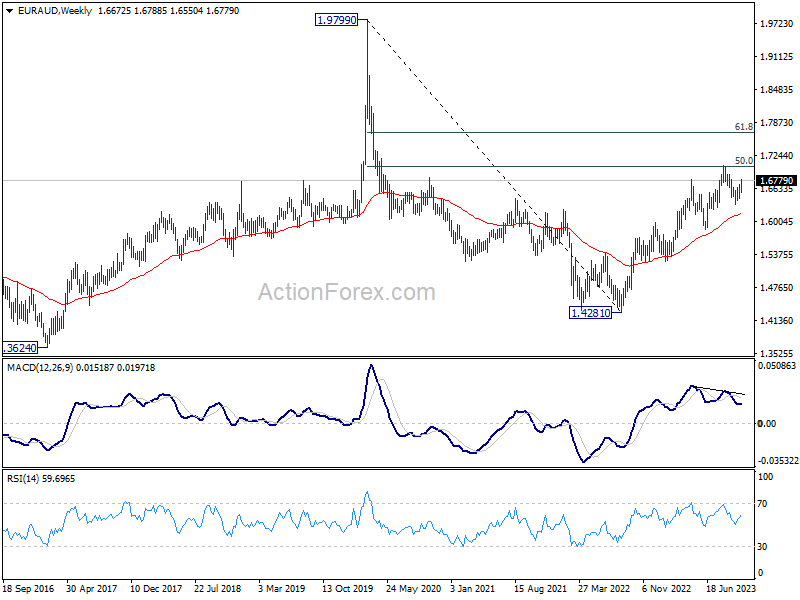

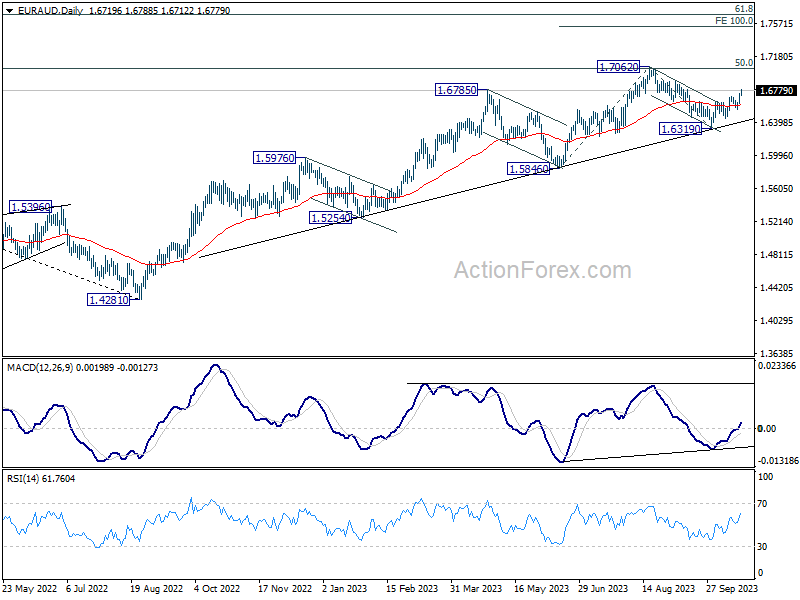

EUR/AUD Weekly Outlook

EUR/AUD's rise from 1.6319 continued last week and outlook is unchanged. Initial bias remains on the upside this week for retesting 1.7062 resistance. Decisive break there will confirm larger up trend resumption. Next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. On the downside, break of 1.6550 support is needed to indicate completion of the rebound. Otherwise, near term outlook will stay mildly bullish even in case of retreat.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. Sustained break of 1.7062 will pave the way to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. In any case, outlook will stay bullish as long as 1.6319 support holds.

In the longer term picture, loss of upside momentum as seen in 55 W MACD at this stage argues that rise from 1.4281 (2022 low) is more likely a corrective move. Further rise could still be seen as long as 1.5846 support holds. But upside will likely be limited by 61.8% retracement of 1.9799 to 1.4281 at 1.7691. Firm break of 1.5846 support will argue that the rise has completed, and another medium term down leg has started.

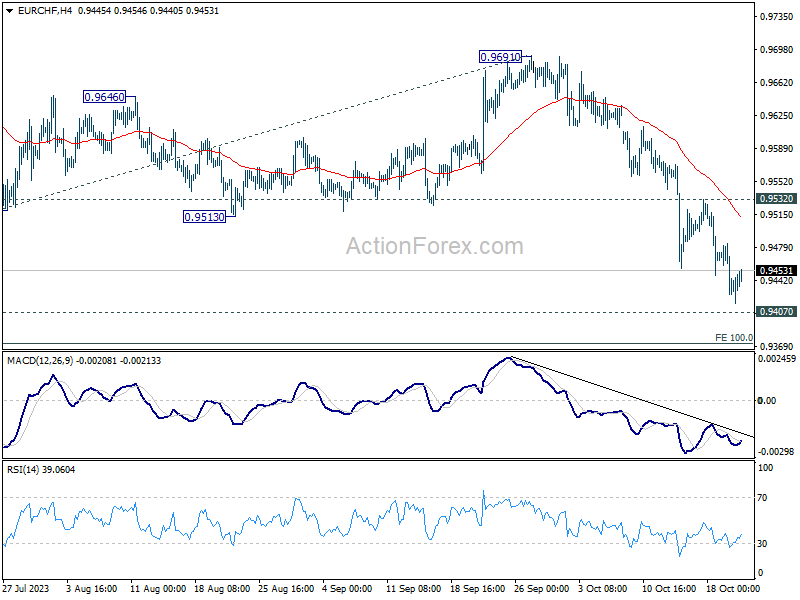

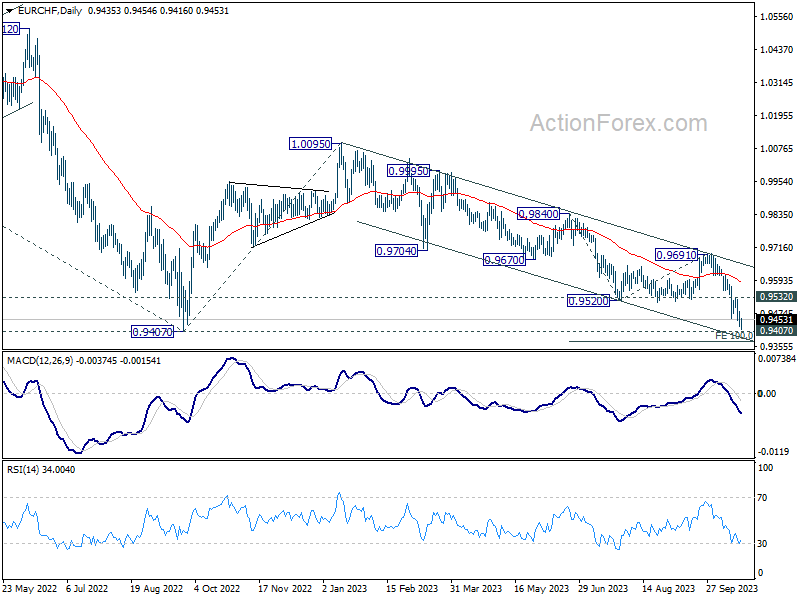

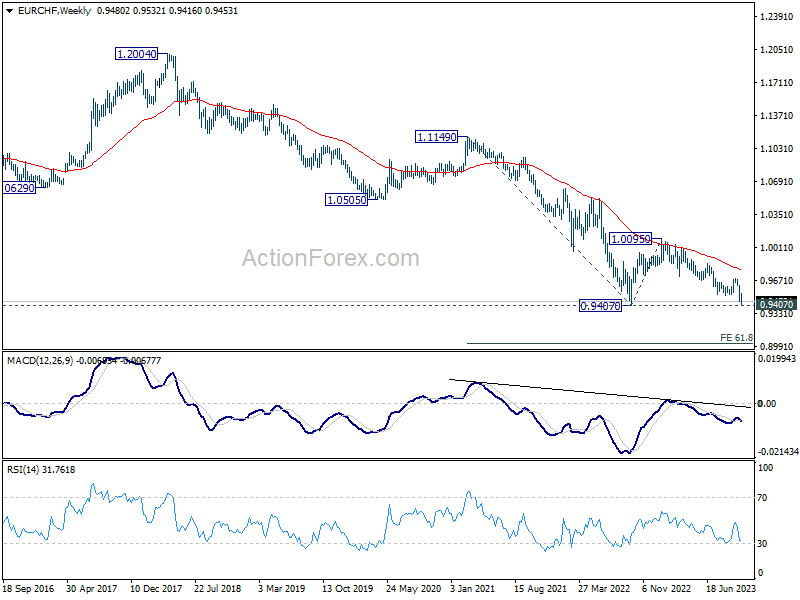

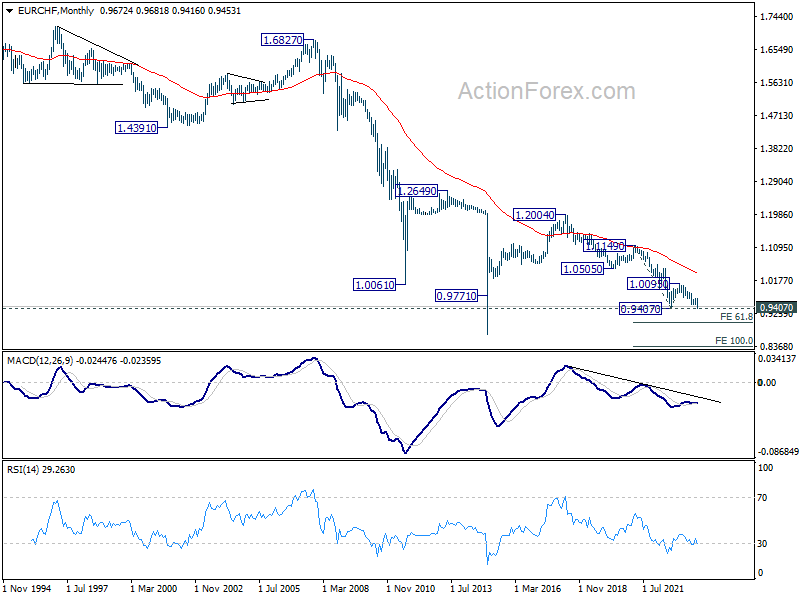

EUR/CHF Weekly Outlook

EUR/CHF's down trend continued last week and hit as low as 0.9416. With 4 hour MACD crossed above signal line, initial bias is turned neutral this week first. But outlook stays bearish as long as 0.9532 resistance holds. On the downside, decisive break of 0.9407 medium term bottom will confirm resumption of larger down trend. Next near term target will be 100% projection of 0.9840 to 0.9520 from 0.9691 at 0.9499, and then 161.8% projection at 0.9179.

In the bigger picture, down trend from 1.2004 (2018 high) is still in progress. Decisive break of 0.9407 will confirm resumption, and target 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0362). Break of 1.0095 resistance is needed to be the first sign of bottoming, or the multi-decade down trend is expected to continue.

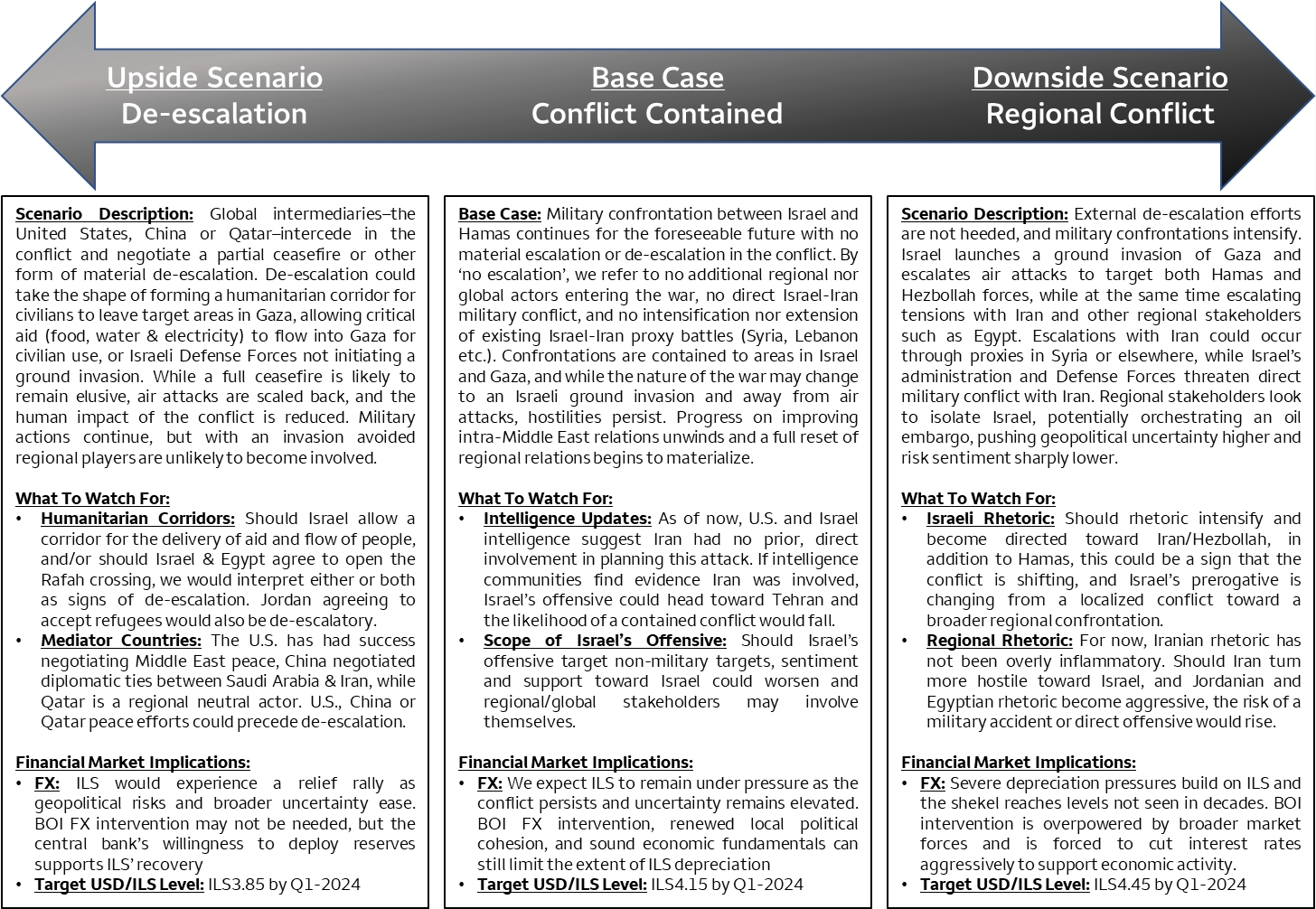

Israel-Gaza Conflict Scenario Analysis

Summary

Last week, we published our views on the medium-to-longer term implications of the Israel-Gaza conflict. Our views on the longer-term ramifications have not changed, and in this report, we offer a scenario analysis to gauge the potential evolution of the conflict. We include a non-exhaustive list of key signals that we are watching for how, or if, the intensity of the conflict is changing. We also provide views on how our USD/ILS exchange rate target could change should either of these scenarios appear to be materializing.

Weekly Economic & Financial Commentary: Impact of Middle East Developments on Rates and Inflation

Summary

United States: Higher Mortgage Rates Burn the Housing Market

- The recent run-up in mortgage rates is nudging the housing market back toward recession. Existing home sales in September sank to their slowest pace since 2010. Single-family building has been more resilient; however, builders are growing less confident in their ability to sustain sales.

- Next week: New Home Sales (Wed.), Real GDP Growth (Thu.), Personal Income & Spending (Fri.)

International: China's Economy Outperforms in Q3

- The challenges facing China's economy are abundant; however, China's economy was able to record solid growth in Q3. Incorporating Q3 data into China's growth prospects for this year leads us to believe China's economy could reach authorities' official growth target of 5%. With that said, China's fundamental and structural problems have not disappeared with just one quarter of solid growth.

- Next week: Bank of Canada (Wed.), European Central Bank (Thu.), Chilean Central Bank (Thu.)

Interest Rate Watch: Impact of Middle East Developments on Rates and Inflation

- Many financial market participants are looking over their shoulders wondering what could be the next catalyst to drive rates higher. What might we see in the rates market, given the conflict in the Middle East and potential inflation drivers from higher commodity prices and overall wartime expenditure from the federal government?

Topic of the Week: A Surge in Household Net Worth and Progress in Bridging the Wealth Gap

- This week, the Federal Reserve released its 2022 Survey of Consumer Finances (SCF) encompassing the time period between 2019 and 2022. The triennial report provides a comprehensive snapshot of the financial circumstances of households as it pertains to income, net worth, asset ownership and credit usage.

The Weekly Bottom Line: Treasury Yields Flirt with Multidecade Highs

U.S. Highlights

- Treasury yields continued their steep ascent this week, amidst a heavy week for Fed speakers. FOMC members broadly agreed that positive progress had been made on inflation, although few were willing to take the prospect of further policy tightening off the table.

- Previous increases in mortgage rates weighed heavily on the housing market in September, although new home construction rebounded from its August decline.

- The consumer appeared undeterred by higher borrowing costs in September, with retail sales growth doubling expectations.

Canadian Highlights

- Canada’s inflation moved back in the right direction in the month of September, which should give the Bank of Canada confidence in holding the policy rate at 5.00% next week.

- Markets have largely removed bets for further interest rate hikes in coming meetings, previously expecting at least one more hike by early next year. We also expect the policy rate to remain on hold until the middle of next year.

- The Bank of Canada’s quarterly business and consumer surveys pointed to downbeat sentiment on the state of the economy, while higher interest rates have consumers pressing the spending brakes.

U.S. – Treasury Yields Flirt with Multidecade Highs

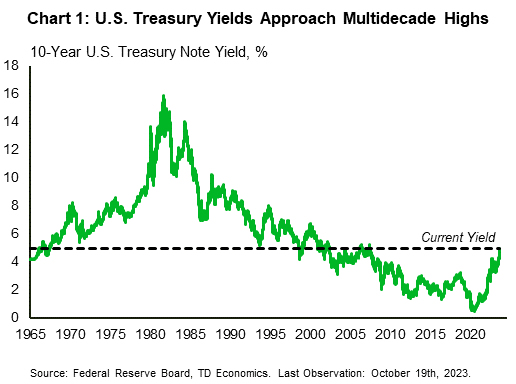

The steep ascent of U.S. Treasury yields continued unabated this week, as markets revised their expectations for yields, particularly over the longer term. The persistent political dysfunction in Congress amid rising deficits and heightened geopolitical tensions is likely playing a role in the increase in the term premium, which has recently contributed to the higher 10-Year yield. The term premium reflects the added compensation investors require for the unknowns associated with holding longer-term government debt. The 10-Year Treasury yield is now just under 5%, its highest level since before the Global Financial Crisis (Chart 1). Equities in turn fell this week, with the S&P 500 down 1.8% as of the time of writing.

Outside of financial markets, the real economy has seen divergent trends between economic sectors depending on their sensitivity to interest rates. The housing market softened further in September to reach a 13 year low, reflecting the strain of higher mortgage rates (see here). While existing home inventory levels improved on the month, supply remains low, which continued to place upward pressure on housing prices. Low resale listings have in turn increased the demand for new units, but elevated rates remain a headwind to homebuilding activity as well. While housing starts rose in September, they remain well below year-ago levels, primarily resulting from weakness in the more rate-sensitive multi-family segment.

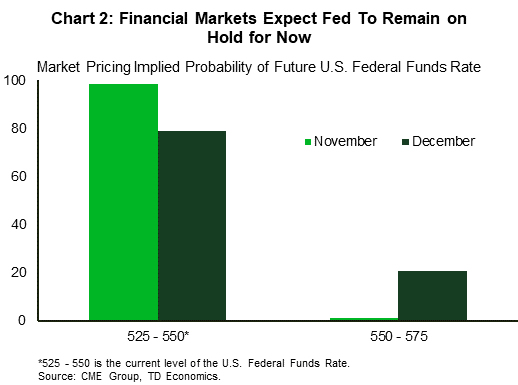

Despite higher interest rates, the health of the American consumer has remained robust (see here). Retail sales growth in September more than doubled expectations. Somewhat surprisingly, the most rate-sensitive segment of retail sales (Automobile & other motor vehicle dealers) saw its strongest growth in four months. However pent-up demand from the extended shortage of vehicles in previous years continues to be a factor. But, even excluding the more volatile categories, the retaChart 2: The chart shows the market pricing implied probability for the federal funds rate in November and December, lining up with the FOMC meeting dates. Markets broadly expect the Fed to maintain interest rates at their current level into the end of 2023. Implied odds for the Fed holding in November are nearly 100%, while odds for a hold in December are slightly lower at 80% as of the time of publication.il sales “control group” was very strong on the month. All in all, the resilience of the consumer has been a key growth contributor in 2023.

In terms of what this means for interest rate moves, we heard remarks from nearly every member of the FOMC this week, including Chair Powell. The balance of opinion was skewed towards maintaining a wait and see approach given the positive progress that has been made on inflation thus far, which pushed market pricing for a hold at the next meeting on November 1st to a virtual certainty (Chart 2). However, Powell also noted that additional evidence of persistently above trend growth or tightening labor market conditions could put inflation progress at risk and warrant further policy tightening. We currently expect that the resilience of the U.S. economy will lead to one last interest rate hike, but the recent tightening in financial conditions makes it a close call.

Next week we will see the advance estimate for third quarter GDP growth, which is expected to show eye-popping growth. Perhaps more importantly, the September consumer spending data will show how momentum is looking heading into the fourth quarter, along with the Fed’s preferred inflation metric. A moderation in both metrics would be welcome news for the Fed.

Canada – Inflation Deflates Bets for Interest Rate Hikes

The Bank of Canada's (BoC) October 25th interest rate decision is right around the corner, and markets have increased the odds for a stand pat deicsion. September's softer-than-expected inflation reading helped on that score, and likely gives Tiff Macklem & Co. some comfort to hold the policy rate at 5.00% next week. Next week's decision will be accompanied by a fresh set of forecasts in the Monetary Policy Report (MPR), which will be closely watched for the Bank's assesssment of how their recent rate hikes are affecting the economy. Canadian yields were taken on rollercoaster this week, with two-year yields finishing flat and the 10-year yield up around 12 basis points (bps). Although a lot of this week's curve move was influenced more by strong economic data stateside than developments in Canada.

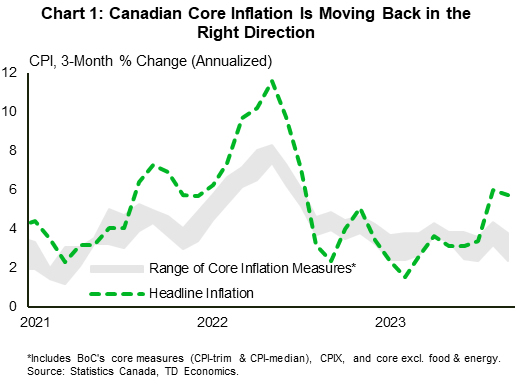

Canada's inflation data moved in the right direction in September, coming in below consensus estimates. More importantly, the BoC's preferred measures of core inflation also cooled. More encouragingly, the slowdown was also broad-based. Sticky inflation has been a thorn in the BoC's side, and a large driver of the additional interest rate hikes delivered back in June and July. Chart 1 shows that the range of various core measures are back inside the 3.5–4.0% range from the first half of 2023, still too high, but moving in the right direction. Of note, food inflation decelerated the most of all major categories. The price of gasoline is still higher relative to a year ago, but did moderate on a month-on-month basis. Services inflation was flat on the month while core goods prices continue to cool. Base-effects alone could see headline inflation in October push down to just north of 3% y/y.

Consumer and business sentiment is another mark in the cooling column. The BoC's companion business and consumer outlook surveys showed weakening sentiment in the third quarter this year. Businesses expect sales to slow over the coming year, which is weighing on plans for investment and employment. Inflation expectations amongst businesses and consumers alike have edged down but remain at elevated levels. On wage expectations, businesses report wage pressures have peaked but remain high. However, consumers' wage expectations are at the highest point since the inception of the survey. From the BoC's perspective, there is evidence in these surveys to suggest that economic conditions are cooling, which should help them achieve their inflation target.

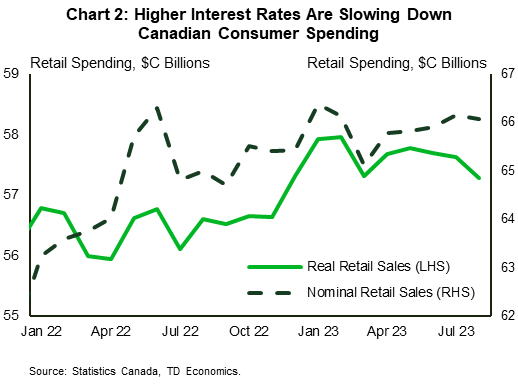

The hard data is bearing this out, as spending fatigue looks to be setting in for Canadian consumers. August retail sales dropped by 0.1% m/m, with volumes dropping by a larger magnitude (Chart 2). Declines were broad-based across industries. Given weak goods prices in September and early estimates of flat nominal spending, September sales volumes might register positive. That said, third quarter real spending is set to slow, with the outlook for the consumer weakening in coming quarters.

Week Ahead – ECB Set to Pause Tightening Cycle, a Big Week for Earnings

US

Now that Fed Chair Powell signaled that the Federal Open Market Committee will keep rates on hold at the next policy meeting, Wall Street will look to see how high growth will peak before the economy cools in Q4. Expectations are for the advance reading of Q3 GDP to rise from 2.1% to 4.3%. Investors will also want to see if the September income and spending data show the consumer is still in good shape, as both readings are expected to post 0.4% monthly gains.

Big earnings for the week will come from 3M, Alphabet, Amazon, Barclays, BNP Paribas, Boeing, Boston Scientific, Bristol-Myers Squibb, Chevron, Chipotle Mexican Grill, Coca-Cola, Colgate-Palmolive, Exxon Mobil, Ford Motor, General Electric, General Motors, Hershey, Intel, International Business Machines, Merck, Meta Platforms, Microsoft, Novartis, PG&E, United Parcel Service, United Rentals, Verizon Communications, Visa, and Volkswagen

Washington DC will remain in the spotlight as House Republicans continue to struggle to elect a new House speaker.

Eurozone

The ECB is expected to leave interest rates unchanged next week, as per the communication following its last meeting in September. The question for many traders is whether the central bank is in fact done or if it can be tempted into another increase. Recent moves in bond yields suggest investors are increasingly coming around to the idea of higher for longer. It will be interesting to see if the ECB addresses this or welcomes the recent moves. Flash PMIs will also be of interest considering the risk of recession going into next year.

UK

Delayed unemployment data and flash PMI surveys will be in focus next week. There’s still significant uncertainty around the UK from the sustainability of declining inflation – which Governor Bailey claimed will fall sharply in October – to high wages, weak retail sales, and the potential economic drag. Unemployment has been ticking higher in this time which may give the BoE comfort that wage growth will soon normalize. Central bank appearances later in the week will also be of interest.

Russia

Higher inflation is keeping up the pressure on the Russian central bank to raise rates, which it’s expected to do again next week, taking the Key Rate to 14% from 13%, currently. The rouble remains extremely weak so it may take more than a 1% increase to improve its fortunes and get inflation back under control.

South Africa

Inflation came in slightly above expectations in September and despite it still being well within the SARBs 3-6% target range, that will make policymakers a little uncomfortable. Against that backdrop, the PPI figures next week will be eyed for signs of further inflationary pressures in the pipeline.

Turkey

The focus next week will be on the CBRT rate decision, with there once more being a wide range of forecasts, but the consensus falling somewhere around a 5% hike. This comes amid inflation running at more than 60% in September and the lira continuing to hit record lows.

Switzerland

No major economic releases or events next week.

China

A quiet week on the economic calendar where we only have year-to-date industrial profits to September on Friday. It is expected to contract at a slower pace of -9% y/y versus -11.7% recorded in August.

The limelight will be on Country Garden, China’s biggest private property developer which is now in a “technical default” situation after it failed to honor the overdue coupon payments of US$15.4 million of an offshore dollar bond following its grace period which expired on 18 October. The focus now will be on the negotiation with its bondholders on restructuring the overdue coupon payments and the time taken for the company to deliver a blueprint.

Also, the grace period on another set of overdue coupon payments on offshore bonds is near expiration with one due on 27 October for US$40 million. A messy debt overhaul of Country Garden increases the systemic risk and social stability threat in China.

Several key earnings releases to take note of; CNOOC (Tuesday), China Life Insurance (Thursday), Sinopec (Thursday), China CITIC Bank (Thursday), Guangzhou Automobile (Thursday), China Construction Bank (Thursday), Agricultural Bank of China (Friday), Bank of China (Friday), China Merchants Bank (Friday), Ping An Insurance (Friday).

India

No key data releases.

Australia

On Tuesday, we will have flash manufacturing and services PMI numbers for October.

A rather hawkish rhetoric in the RBA minutes – in which one sentence stated, “the board has a low tolerance for a slow return of inflation to target than currently expected” – led to a jump in expectations of an interest rate hike in the next RBA meeting on 7 November. Based on data from the pricing of the ASX 30-day interbank cash rate futures as of 18 October, there’s a 23% chance (up from 3% a week ago) of an interest hike of 25 basis points (bps) to bring the official cash rate to 4.35% after a fourth consecutive pause in early October.

The release of Australia’s Q3 inflation data on Wednesday is likely to be pivotal in altering the expectations of a potential interest rate hike. A deceleration to 5.3% y/y is expected for Q3 from 6% in the previous quarter. The Q3 trimmed mean CPI is expected to fall to 5% y/y versus 5.9% in Q2.

However, the less lagging CPI indicator for September is expected to show another uptick in inflation to 5.4% versus 5.2% in August. That would be the second consecutive month of higher inflation which may put a hawkish RBA vibe back on the agenda.

New Zealand

ANZ-Roy consumer confidence data for October will be released on Friday where it is forecasted to decline to 82.6 from 86.4 in September. That would be the lowest reading since May 2023.

Japan

Flash manufacturing and services PMIs for October will be released on Tuesday with the former expected to improve slightly to 49 from 48.5 in September while growth in the latter is expected to dip slightly to 52.9 from 53.8.

On Friday, the leading Tokyo area inflation data for October is expected to show core CPI remaining at 2.5% y/y but growth in the core-core CPI (excluding fresh food and energy) dipping slightly to 2.2% y/y from 2.4%. That would be the slowest core-core inflationary growth in Tokyo since March 2023.

Singapore

A slew of key economic data releases starting on Monday with the CPI report for September. The headline inflation rate is expected to increase slightly to 4.2% y/y from 4% in August while the expectation for the core inflation rate is a dip to 3.1% y/y from 3.4%; a declining trend in place since May 2023.

Industrial production for September will be released on Thursday and a smaller contraction of -2.6% y/y is expected from -12.1% in August. That would be a significant improvement after it previously recorded its sharpest drop since November 2019.

On Friday, we have the preliminary Q3 unemployment rate which is expected to hold steady at 1.9%. PPI (factory gate prices) is expected to decline again in September at a rate of 3.0% y/y, almost the same pace as the -3.7% in August, and the softest since January 2023.

Economic Calendar

Sunday, Oct. 22

Economic Data/Events

- Federal elections in Switzerland

Monday, Oct. 23

Economic Data/Events

- Eurozone consumer confidence

- Singapore CPI

- Taiwan jobless rate, industrial production

- Thailand customs trade

- EU foreign ministers meet in Luxembourg

- Japan PM Kishida delivers policy speech at Diet session

- Singapore International Energy Week runs through Friday

- Australia PM Albanese visits the US and meets with President Biden on Wednesday

Tuesday, Oct. 24

Economic Data/Events

- US Flash PMIs

- European Flash PMIs: Eurozone, Germany, France, and the UK

- UK jobless claims, unemployment

- Mexico international reserves

- Megacap tech earnings from Microsoft and Alphabet

- UN Security Council expected to discuss the Middle East situation

- European Union expected to unveil plans for wind energy industry

- RBA Gov Bullock speaks at the Commonwealth Bank Annual Conference in Sydney

- Euro-area bank lending survey

- International Energy Agency releases its World Energy Outlook annual report

Wednesday, Oct. 25

Economic Data/Events

- US new home sales

- Australia CPI

- Canada rate decision: Expected to keep rates on hold at 5.00%

- Germany IFO business climate

- Russia industrial production

- Hong Kong Chief Executive Lee delivers his second policy address

Thursday, Oct. 26

Economic Data/Events

- ECB rate decision: Expected to keep main refinancing rate at 4.50%

- US Advance Q3 GDP Q/Q: 4.3%e v 2.1% prior, Personal Consumption 3.7%e v 0.8% prior, Sept wholesale inventories, Sept durable goods, weekly initial jobless claims

- Hong Kong trade

- Mexico unemployment

- Singapore industrial production, unemployment

- South Korea GDP

- Turkey rate decision: Expected to raise rates by 500bps to 35.00%

- Earnings from Intel and Amazon

- EU leaders summit in Brussels

- Outgoing BOE’s Cunliffe speaks on cross-border payments in Washington

Friday, Oct. 27

Economic Data/Events

- US personal spending and income, University of Michigan consumer sentiment, PCE Core Deflator

- China industrial profits

- Japan Tokyo CPI

- Mexico trade

- Russia rate decision: Policymakers will discuss the possibility of a further rate hike from the current level of 13%

- Singapore home prices

- Spain GDP

- Earnings from Exxon

Sovereign Rating Updates

- France (Fitch)

- Sweden (Fitch)

- Finland (S&P)

- Sweden (S&P)

- Belgium (Moody’s)

- EFSF (Moody’s)

- ESM (Moody’s)

- Italy (DBRS)

Summary 10/23 – 10/27

Monday, Oct 23, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 10:00 | EUR | German Buba Monthly Report | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -18 | -18 |

| 22:00 | AUD | Manufacturing PMI Oct P | 48.7 | |

| 22:00 | AUD | Services PMI Oct P | 51.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 10:00 | EUR | German Buba Monthly Report | |

| Forecast: | Previous: | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | |

| Forecast: -18 | Previous: -18 | ||

| 22:00 | AUD | Manufacturing PMI Oct P | |

| Forecast: | Previous: 48.7 | ||

| 22:00 | AUD | Services PMI Oct P | |

| Forecast: | Previous: 51.8 | ||

Tuesday, Oct 24, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Oct P | 48.9 | 48.5 |

| 06:00 | EUR | Germany Gfk Consumer Confidence Nov | -27.3 | -26.5 |

| 06:00 | GBP | Claimant Count Change Sep | 2.3K | 0.9K |

| 06:00 | GBP | ILO Unemployment Rate 3M Aug | 4.30% | 4.30% |

| 07:15 | EUR | France Manufacturing PMI Oct P | 44.8 | 44.2 |

| 07:15 | EUR | France Services PMI Oct P | 44.6 | 44.4 |

| 07:30 | EUR | Germany Manufacturing PMI Oct P | 40.1 | 39.6 |

| 07:30 | EUR | Germany Services PMI Oct P | 50.1 | 50.3 |

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | 43.7 | 43.4 |

| 08:00 | EUR | Eurozone Services PMI Oct P | 48.7 | 48.7 |

| 08:30 | GBP | Manufacturing PMI Oct P | 45.2 | 44.3 |

| 08:30 | GBP | Services PMI Oct P | 49.5 | 49.3 |

| 12:30 | CAD | New Housing Price Index M/M Sep | 0.10% | |

| 12:55 | USD | Redbook Index Y/Y (Oct 20) | 4.60% | |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Aug | 0.10% | |

| 13:45 | USD | Manufacturing PMI Oct P | 49.5 | 49.8 |

| 13:45 | USD | Services PMI Oct P | 49.9 | 50.1 |

| 13:45 | USD | Composite PMI Oct P | 50.2 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Oct P | |

| Forecast: 48.9 | Previous: 48.5 | ||

| 06:00 | EUR | Germany Gfk Consumer Confidence Nov | |

| Forecast: -27.3 | Previous: -26.5 | ||

| 06:00 | GBP | Claimant Count Change Sep | |

| Forecast: 2.3K | Previous: 0.9K | ||

| 06:00 | GBP | ILO Unemployment Rate 3M Aug | |

| Forecast: 4.30% | Previous: 4.30% | ||

| 07:15 | EUR | France Manufacturing PMI Oct P | |

| Forecast: 44.8 | Previous: 44.2 | ||

| 07:15 | EUR | France Services PMI Oct P | |

| Forecast: 44.6 | Previous: 44.4 | ||

| 07:30 | EUR | Germany Manufacturing PMI Oct P | |

| Forecast: 40.1 | Previous: 39.6 | ||

| 07:30 | EUR | Germany Services PMI Oct P | |

| Forecast: 50.1 | Previous: 50.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | |

| Forecast: 43.7 | Previous: 43.4 | ||

| 08:00 | EUR | Eurozone Services PMI Oct P | |

| Forecast: 48.7 | Previous: 48.7 | ||

| 08:30 | GBP | Manufacturing PMI Oct P | |

| Forecast: 45.2 | Previous: 44.3 | ||

| 08:30 | GBP | Services PMI Oct P | |

| Forecast: 49.5 | Previous: 49.3 | ||

| 12:30 | CAD | New Housing Price Index M/M Sep | |

| Forecast: | Previous: 0.10% | ||

| 12:55 | USD | Redbook Index Y/Y (Oct 20) | |

| Forecast: | Previous: 4.60% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Aug | |

| Forecast: | Previous: 0.10% | ||

| 13:45 | USD | Manufacturing PMI Oct P | |

| Forecast: 49.5 | Previous: 49.8 | ||

| 13:45 | USD | Services PMI Oct P | |

| Forecast: 49.9 | Previous: 50.1 | ||

| 13:45 | USD | Composite PMI Oct P | |

| Forecast: | Previous: 50.2 | ||

Wednesday, Oct 25, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | 5.30% | 5.20% |

| 00:30 | AUD | CPI Q/Q Q3 | 1.10% | 0.80% |

| 00:30 | AUD | CPI Y/Y Q3 | 5.30% | 6.00% |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 1.10% | 1.00% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 5.00% | 5.90% |

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | -27.6 | |

| 08:00 | EUR | Germany IFO Business Climate Oct | 85.9 | 85.7 |

| 08:00 | EUR | Germany IFO Current Assessment Oct | 88.5 | 88.7 |

| 08:00 | EUR | Germany IFO Expectations Oct | 83.3 | 82.9 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | -1.70% | -1.30% |

| 14:00 | USD | New Home Sales Sep | 684K | 675K |

| 14:00 | CAD | BoC Interest Rate Decision | 5.00% | 5.00% |

| 14:30 | USD | Crude Oil Inventories | -0.5M | -4.5M |

| 15:00 | CAD | BoC Press Conference | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | 2.00% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | |

| Forecast: 5.30% | Previous: 5.20% | ||

| 00:30 | AUD | CPI Q/Q Q3 | |

| Forecast: 1.10% | Previous: 0.80% | ||

| 00:30 | AUD | CPI Y/Y Q3 | |

| Forecast: 5.30% | Previous: 6.00% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | |

| Forecast: 1.10% | Previous: 1.00% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | |

| Forecast: 5.00% | Previous: 5.90% | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | |

| Forecast: | Previous: -27.6 | ||

| 08:00 | EUR | Germany IFO Business Climate Oct | |

| Forecast: 85.9 | Previous: 85.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Oct | |

| Forecast: 88.5 | Previous: 88.7 | ||

| 08:00 | EUR | Germany IFO Expectations Oct | |

| Forecast: 83.3 | Previous: 82.9 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | |

| Forecast: -1.70% | Previous: -1.30% | ||

| 14:00 | USD | New Home Sales Sep | |

| Forecast: 684K | Previous: 675K | ||

| 14:00 | CAD | BoC Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: -0.5M | Previous: -4.5M | ||

| 15:00 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | |

| Forecast: 2.00% | Previous: 2.10% | ||

Thursday, Oct 26, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Import Price Index Q/Q Q3 | 0.20% | -0.80% |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.50% | 4.50% |

| 12:30 | USD | Initial Jobless Claims (Oct 20) | 202K | 198K |

| 12:30 | USD | GDP Annualized Q3 P | 4.30% | 2.10% |

| 12:30 | USD | GDP Price Index Q3 P | 2.50% | 1.70% |

| 12:30 | USD | Goods Trade Balance (USD) Sep P | -85.5B | -84.6B |

| 12:30 | USD | Wholesale Inventories Sep P | 0.10% | -0.10% |

| 12:30 | USD | Durable Goods Orders Sep | 1.00% | 0.10% |

| 12:30 | USD | Durable Goods Orders ex TransportSep | 0.20% | 0.40% |

| 14:00 | USD | Pending Home Sales M/M Sep | 1.10% | -7.10% |

| 14:30 | USD | Natural Gas Storage | 97B | |

| 23:30 | JPY | Tokyo CPI Y/Y Oct | 2.80% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Oct | 2.50% | |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Oct | 3.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Import Price Index Q/Q Q3 | |

| Forecast: 0.20% | Previous: -0.80% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 20) | |

| Forecast: 202K | Previous: 198K | ||

| 12:30 | USD | GDP Annualized Q3 P | |

| Forecast: 4.30% | Previous: 2.10% | ||

| 12:30 | USD | GDP Price Index Q3 P | |

| Forecast: 2.50% | Previous: 1.70% | ||

| 12:30 | USD | Goods Trade Balance (USD) Sep P | |

| Forecast: -85.5B | Previous: -84.6B | ||

| 12:30 | USD | Wholesale Inventories Sep P | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:30 | USD | Durable Goods Orders Sep | |

| Forecast: 1.00% | Previous: 0.10% | ||

| 12:30 | USD | Durable Goods Orders ex TransportSep | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 14:00 | USD | Pending Home Sales M/M Sep | |

| Forecast: 1.10% | Previous: -7.10% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 97B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Oct | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Oct | |

| Forecast: | Previous: 2.50% | ||

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Oct | |

| Forecast: | Previous: 3.80% | ||

Friday, Oct 27, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q3 | 0.50% | |

| 00:30 | AUD | PPI Y/Y Q3 | 3.90% | |

| 12:30 | USD | Personal Income M/M Sep | 0.40% | 0.40% |

| 12:30 | USD | Personal Spending Sep | 0.40% | 0.40% |

| 12:30 | USD | PCE Price Index M/M Sep | 0.30% | 0.40% |

| 12:30 | USD | PCE Price Index Y/Y Sep | 3.40% | 3.50% |

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.30% | 0.10% |

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 3.70% | 3.90% |

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 63 | 63 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q3 | |

| Forecast: | Previous: 0.50% | ||

| 00:30 | AUD | PPI Y/Y Q3 | |

| Forecast: | Previous: 3.90% | ||

| 12:30 | USD | Personal Income M/M Sep | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 12:30 | USD | Personal Spending Sep | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 12:30 | USD | PCE Price Index M/M Sep | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 12:30 | USD | PCE Price Index Y/Y Sep | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Sep | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Sep | |

| Forecast: 3.70% | Previous: 3.90% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | |

| Forecast: 63 | Previous: 63 | ||