Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8882; (P) 0.8942; (R1) 0.8975; More....

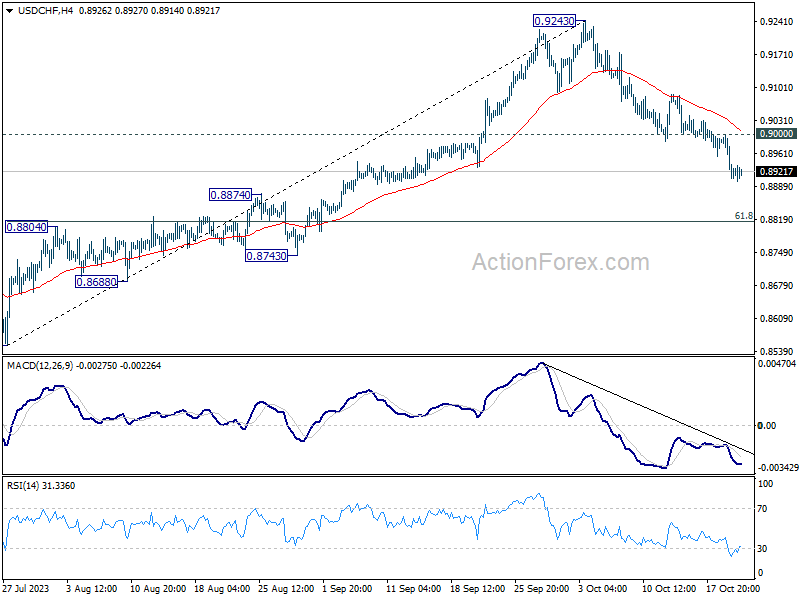

Intraday bias in USD/CHF stays on the downside at this point. Current fall from 0.9243 should target 61.8% retracement of 0.8551 to 0.9243 at 0.8815 next. Sustained break there will pave the way to retest 0.8551 low. On the upside, above 0.9000 minor resistance will turn bias neutral and bring consolidations first, before staging another decline.

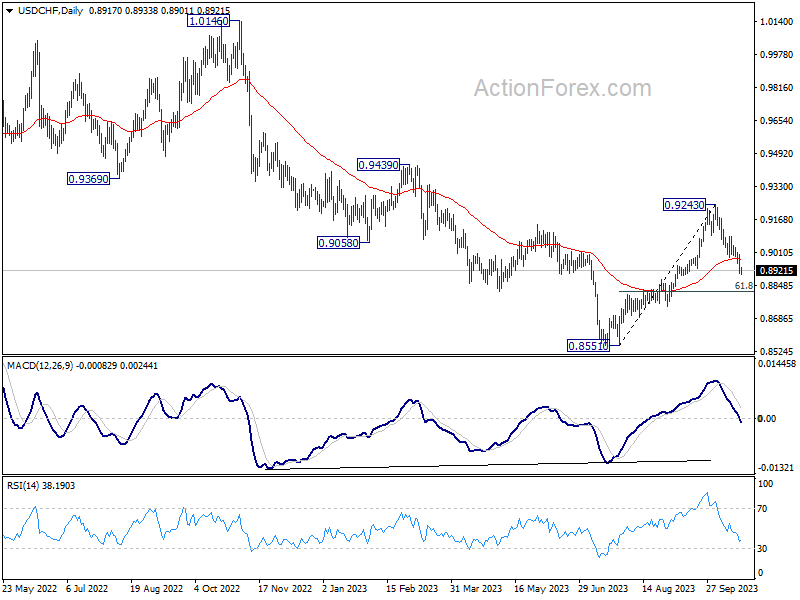

In the bigger picture, the firm break of 55 D EMA (now at 0.8974) argues that rebound from 0.8551 might be completed as a correction at 0.9243. In other words, larger fall from 1.0146 (2022 high) is possibly not over yet. Risk will now stay on the downside as long as 0.9243 resistance holds. Firm break of 0.8551 will confirm down trend resumption.

Canada: Retail Sales Decline in August

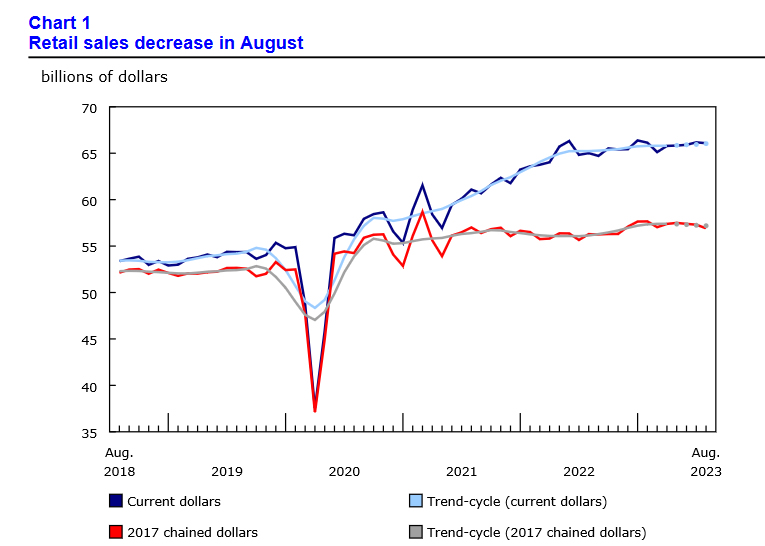

Retail sales declined 0.1% month-on-month (m/m) in August, coming in better than Statistics Canada's advance estimate for a 0.3% m/m decline, but in line with expectations. July's print was revised up to 0.4% m/m from 0.3% m/m reported in the advance estimate.

Adjusting for inflation, the volume of retail sales was 0.6% lower on the month.

Sales at motor vehicle and parts dealers fell by 0.9% m/m - the second consecutive month of declines. Ex-auto, sales were up 0.1% m/m, above the consensus expectations for a decline of the same magnitude.

Sales growth at gasoline stations and fuel vendors were up 2.8% as gas prices accelerated thanks to a recent spike in oil prices. In volume terms, receipts were down 2.9% m/m in August.

Excluding sales at car dealerships and gas stations, core retail sales were down 0.3% in August. The 1.2% m/m decline in sales at food and beverage stores was the major driver of this loss, but most other categories were also in the red in August.

Only three other major categories reported gains in August: health and personal care stores (+1.2% m/m), electronics and appliance stores (+0.3% m/m), general merchandise stores (+0.3% m/m).

E-commerce sales also dwindled, losing 2.0% m/m in August following three consecutive months of strong gains.

According to Statistics Canada, approximately 12% of Canadian retailers reported that their business activities in August had been affected by the strike at the ports in British Columbia..

Based on the answer of 36.5% of companies surveyed, advanced estimate for the month of September points to a flat reading. This is better than are own estimate of consumer activity based on TD debit/credit card spending, which points to a decline in September.

Key Implications

Retail sales were weak in August, but with July's upward revisions this wasn't enough to put the third quarter's already modest consumer spending profile at risk. We expect personal consumption expenditure to be fairly anemic in the third quarter, advancing at only a 1-1.5% pace, in line with our internal spend data.

The balance of risks for the Canadian economy is slowly swinging to the downside as consumer confidence continues to be soured by the Bank of Canada's rate hikes and elevated inflation. This certainly allows the Bank to remain on the sidelines at next week's decision. We expect that moderating demand tempers inflation going forward, while keeping spending just slightly below sub-trend without sending disruptive ripples through the economy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.66; (P) 149.81; (R1) 149.96; More...

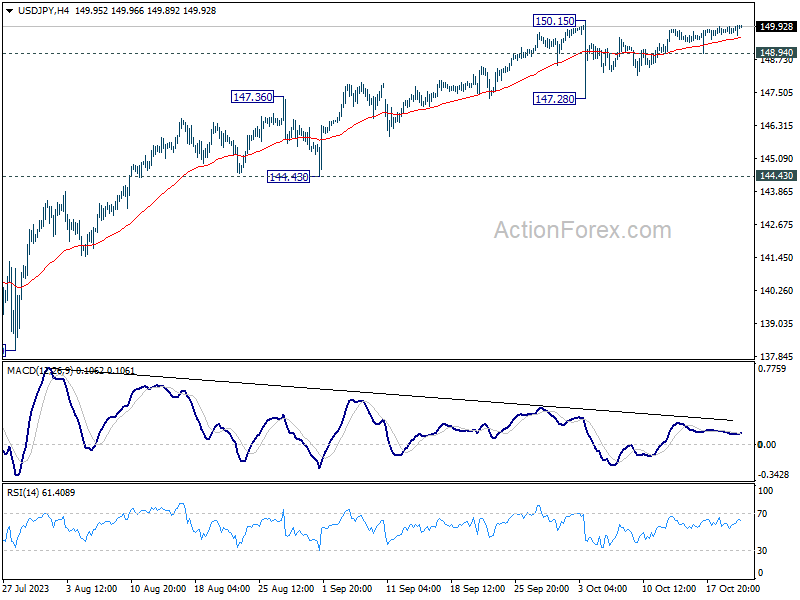

Intraday bias in USD/JPY stays neutral for the moment as range trading continues. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Gaza Strife Rattles Investor Confidence; Bitcoin Surpasses 30k Mark

Global stock markets continues to face turbulence today, with Asian indices wrapping up in the negative zone, European markets showcasing bearish sentiments, and US futures indicating a subdued opening. A heightened sense of caution permeates the investment community due to the intensifying conflict between Israel and Hamas in the Gaza strip, fueling concerns of possible escalation over the upcoming weekend. However, certain sectors like gold, oil, and treasuries seem to be pausing their rapid ascent, signaling a possible breather amidst the intense market volatility.

In the forex domain, Swiss Franc has managed to maintain its dominance as the week's top performer, trailed by Euro and Australian Dollar. On the flip side, Kiwi, Yen, and Canadian are struggling. Retail sales data failed to catalyze sustained move for Loonie and Sterling. Amidst this, Dollar is locked in a standoff with the Yen, hovering precariously close to 150 mark.

On the cryptocurrency front, Bitcoin managed to push past 30k handle today, potentially driven in part by investors seeking alternative safe havens. From a short-term perspective, the crypto asset is likely to see further rise as long as 28071 support holds, aiming next for the 31815 peak. A broader overview suggests that the support at 24739 has held firm, leading to a moderately bullish medium-term outlook with the expectation that rise from 15452 could resume later in the stage.

In Europe, at the time of writing, FTSE is down -1.08%. DAX is down -1.30%. Hong Kong HSI is down -1.20%. Germany 10-year yield is down -0.0074 at 2.908. Earlier in Asia, Nikkei dropped -0.54%. Hong Kong HSI dropped -0.72%. China Shanghai SSE dropped -0.74%. Singapore Strait Times dropped -0.74%. Japan 10-year JGB yield dropped -0.0026 to 0.844.

Fed's Bostic eyes late 2024 for possible rate cut, remains focused on curbing inflation

In an interview with CNBC, Atlanta Federal Reserve President Raphael Bostic emphasized that reigning in inflation remains a top priority, and the metric needs to approach the 2% mark before a rate cut can be seriously considered.

"Inflation is job one, we have to get that under control," Bostic asserted. But rate cut is possible next year and "I would say late 2024", he added.

"There's still a lot of momentum in the economy. My outlook says that inflation is going to come down but it's not going to like fall off a cliff," he explained.

"It'll be sort of a progression that's going to take some time. And so we're going to have to be cautious, we're going to have to be patient, but we're going to have to be resolute," added Bostic.

In the context of a broader economic outlook, Bostic dismissed the possibility of a recession. He projected a slowdown in economic activity but remained optimistic about the economy's resilience and the eventual return of inflation to the 2% target.

Canada retail sales fell -0.1% mom in Aug, sales volume down -0.7% mom

Canada retail sales fell -0.1% mom to CAD 66.1B in August, matched expectations. Sales were down in six of nine subsectors and were led by decreases at motor vehicle and parts dealers (-0.9%). Excluding gasoline stations, fuel, motor vehicles and parts, sales were down -0.3% mom. In volume terms, retail sales declined -0.7% mom.

Advance estimate suggests that sales were unchanged in September.

BoE's Bailey anticipates marked decrease in October's inflation figures

BoE Governor Andrew Bailey, in an interview with Belfast Telegraph, expressed that he "wasn't surprised" by the latest inflation report released on Wednesday. This report showcased consumer prices having ascended by 6.7% compared to the previous year in September, mirroring the growth rate observed in August.

Bailey's added the inflation rate was "not far off what we were expecting." Even more reassuring was the slight dip in core inflation, a development he found "quite encouraging."

He optimistically anticipates a "noticeable drop" in the headline inflation rate with the forthcoming October data. This anticipated decline can be attributed to the significant surge in energy prices last year, which will be excluded from the annual comparison.

However, Bailey warned, "Pay growth as measured is still well above anything that's consistent with the target."

UK retail sales volumes down -0.9% mom in Sep, value down -0.2% mom

UK retail sales volumes fell sharply by -0.9% mom in September, much worse than expectation of -0.4% mom. Sale volumes excluding automotive fuel dropped -1.0% mom.

Looking at some details, non-food stores sales volumes fell -1.9% mom. Non-store retailing sales volumes fell -2.2% mom. Foot stores sales volumes rose rose 0.2% mom. Automotive fuel sales volumes rose by 0.8% mom.

Looking at the quarterly picture, sales volumes fell by -0.8% in the three months to September when compared with the previous three months. Ex-fuel sales volumes fell -1.0%.

In value term, retail sales value dropped -0.2% mom. Sales value excluding automotive fuel fell -0.4% mom.

Japan's core CPI slips below 3% mark to 2.8% yoy

Inflationary momentum in Japan showed signs of easing in September, with all-item CPI decelerating to 3.0% yoy, down from 3.2% yoy in the prior month. Core CPI, which strips out the volatile food prices, also showed a downtrend, registering at 2.8% yoy, a dip from 3.1% yoy. Furthermore, core-core CPI, which excludes both food and energy prices, declined marginally from 4.3% yoy to 4.2% yoy.

Remarkably, core inflation dipped below the 3% mark for the first time since August 2022. Nevertheless, it remains above BoJ's 2% target, marking the 18th consecutive month of surpassing this benchmark.

The detailed breakdown of the data indicates that energy prices were a significant drag, plunging by -11.7% yoy. This downturn can be attributed to the government's proactive measures to trim utility bills, resulting in double-digit falls in electricity and city gas prices. On the contrary, food prices remained on an upward swing, posting 8.8% yoy increase.

There are reports suggesting an upward revision in BoJ's core CPI forecast for fiscal 2023. Sources familiar with the bank's deliberations indicate a possible revision from 2.5% to nearly 3.0%. All eyes will now be on BoJ 's policy meeting scheduled for Oct 31, where a new outlook report is anticipated.

New Zealand's exports down -18% yoy in Sep, China leads decline again

New Zealand's trade balance for September reveals a deficit of NZD -2.3B, driven by a notable fall in goods exports of -18% yoy, bringing the total to NZD 4.9B. The decline in imports was also significant, dropping by -15% yoy to NZD 7.2B.

A striking feature of this downturn is the notable reduction in exports to China, marking a deviation from the consistent growth observed over the past decade. International trade manager Alasdair Allen noted, "Over the past decade, exports to China have been steadily increasing, with a flat period during COVID-19, but in recent months this has started to shift."

Breaking down the export figures by country, China recorded a 20% yoy drop, equivalent to NZD 332 million, leading the downturn. Exports to Australia, US, EU, and Japan also experienced declines, calculated at -3.3%, -6.7%, -26%, and -12% yoy, respectively.

On the imports front, China once again played a significant role, with imports from the country decreasing by -17% yoy. Imports from EU and Australia also dropped by -1.5% yoy and -21% yoy respectively. Imports from South Korea contracted by -16% yoy. In contrast, imports from US saw a growth of 6.1% yoy.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.66; (P) 149.81; (R1) 149.96; More...

Intraday bias in USD/JPY stays neutral for the moment as range trading continues. On the downside, below 148.94 minor support will turn bias to the downside for another down leg towards 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -2329M | -2291M | -2273M | |

| 23:01 | GBP | GfK Consumer Confidence Oct | -30 | -20 | -21 | |

| 23:30 | JPY | National CPI Y/Y Sep | 3.00% | 3.20% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Sep | 2.80% | 2.80% | 3.10% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Sep | 4.20% | 4.30% | ||

| 06:00 | GBP | Retail Sales Y/Y Sep | -0.90% | -0.40% | 0.40% | |

| 06:00 | EUR | Germany PPI M/M Sep | -0.20% | 0.40% | 0.30% | |

| 06:00 | EUR | Germany PPI Y/Y Sep | -14.70% | -14.20% | -12.60% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 13.5B | 17.7B | 10.8B | 10.6B |

| 12:30 | CAD | Retail Sales M/M Aug | -0.10% | -0.10% | 0.30% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | 0.10% | -0.10% | 1.00% |

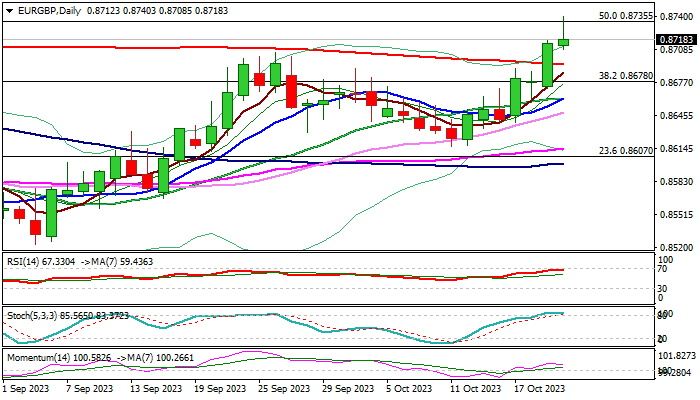

EUR/GBP: Rises to New Multi-Month High, But May Take a Breather Before Resuming

EURGBP extends steep upleg from 0.8616 trough into sixth straight day and hit the highest in more than five months on Friday.

Larger uptrend from 0.8492 (2023 low, posted on Aug 23) remains fully in play for the second consecutive month and received fresh support from much weaker than expected UK retail sales in September.

The rally cracked strong technical barrier at 0.8735 (50% retracement of 0.8978/0.8492) but faced headwinds as daily studies are overbought and profit-taking at the end of the week after strong rally in past few sessions may sideline bulls for consolidation.

The pair is on track for solid weekly gains, suggesting that bulls hold grip, with narrow consolidation to be ideally contained by former top of Sep 26 / 200DMA (0.8705 / 0.8695) to keep near-term bulls intact for firm break of 0.8735 pivot and acceleration towards 0.8800 zone (weekly Ichimoku cloud which is thickening after this week’s twist.

Caution on extended dips and close below 0.8678 (broken Fibo 38.2% / daily Tenkan-sen) which would dent bullish structure and make the downside more vulnerable.

Res: 0.8735; 0.8792; 0.8808; 0.8863.

Sup: 0.8705; 0.8695; 0.8678; 0.8662.

Fed’s Bostic eyes late 2024 for possible rate cut, remains focused on curbing inflation

In an interview with CNBC, Atlanta Federal Reserve President Raphael Bostic emphasized that reigning in inflation remains a top priority, and the metric needs to approach the 2% mark before a rate cut can be seriously considered.

"Inflation is job one, we have to get that under control," Bostic asserted. But rate cut is possible next year and "I would say late 2024", he added.

"There's still a lot of momentum in the economy. My outlook says that inflation is going to come down but it's not going to like fall off a cliff," he explained.

"It'll be sort of a progression that's going to take some time. And so we're going to have to be cautious, we're going to have to be patient, but we're going to have to be resolute," added Bostic.

In the context of a broader economic outlook, Bostic dismissed the possibility of a recession. He projected a slowdown in economic activity but remained optimistic about the economy's resilience and the eventual return of inflation to the 2% target.

Canada retail sales fell -0.1% mom in Aug, sales volume down -0.7% mom

Canada retail sales fell -0.1% mom to CAD 66.1B in August, matched expectations. Sales were down in six of nine subsectors and were led by decreases at motor vehicle and parts dealers (-0.9%). Excluding gasoline stations, fuel, motor vehicles and parts, sales were down -0.3% mom. In volume terms, retail sales declined -0.7% mom.

Advance estimate suggests that sales were unchanged in September.

Canadian Dollar Calm ahead of Retail Sales

- Canada to release retail sales later today

- Fed’s Powell says inflation still too high, lower growth needed

The Canadian dollar has edged higher on Friday. In the European session, USD/CAD is trading at 1.3688, down 0.23%. Canada releases retail sales later today, which could result in volatility from the Canadian dollar.

Canada’s retail sales expected to decline

Canada wraps up the week with the August retail sales report. The markets are bracing for a deceleration, with an estimate of -0.3% m/m, compared to a 0.3% gain in July. On a year-to-year basis, retail sales are projected to slow to 0.2%, down sharply from 2.0% in July.

The Bank of Canada is widely expected to hold rates at 5.0% for a second straight time at the October 25th meeting. The BoC has raised rates to high levels but has only hiked on two occasions in 2023, which indicates that on the whole, interest rates are where the central bank wants them.

I don’t expect to see the BoC trimming rates before mid-2024, but at the same time, the BoC will do its utmost to refrain from further tightening. The takeaway message is that we should expect rates to remain in restrictive territory for some time yet.

Last week’s inflation report showed a decrease of -0.1% for both headline and core CPI in September, which beat expectations. On a year-to-year basis, headline CPI dropped from 4.0% to 3.8% and the core rate eased to 2.8%, down from 3.3%.

Fed Chair Jerome Powell said on Thursday that inflation remained too high and that the 2% target would be difficult to reach if economic growth did not cool. Powell didn’t provide any hints about future rate policy, saying that rate decisions would be based on data and the economic outlook. The Fed has been sending out a “higher for longer” message, and Powell’s focus on high inflation seemed to reiterate this stance.

USD/CAD Technical

- USD/CAD is testing support at 1.3643. Below, there is support at 1.3585

- There is resistance at 1.3716 and 1.3774

Japanese Yen Stays Adrift, Core CPI Falls Below 3%

- Japanese core CPI falls below 3%

- Fed’s Powell says inflation too high, economy too strong

The Japanese yen is slightly lower on Friday. In the European session, USD/JPY is trading at 149.96, up 0.12%. The yen has shown little movement this week and continues to hover just shy of the symbolic 150 level. In early October, the yen breached 150 and then spiked sharply lower. It’s looking very likely that the yen will again breach 150 shortly.

Japan’s core inflation eases below 3%

Japanese core CPI, which excludes fresh food, slowed to 2.8% y/y in September, versus 3.1% in August but above the market consensus of 2.7%. The print fell below the 3% level for the first time since August 2022 but has now exceeded the Bank of Japan’s 2% target for 18 straight months. The “core-core” rate, which excludes fresh food and energy prices and is considered by the BoJ a better gauge of inflation trends, dropped from 4.3% to 4.2% in September, higher than the market consensus of 4.1%.

Inflation has been slowly easing, but the downtrend faces some possible headwinds. The yen continues to lose ground and tensions in the Middle East have raised fears that oil prices could hit $100 or higher. If oil prices rise or the yen continues to decline, the result will be higher inflation.

How will the Bank of Japan react to potential oil inflation and the weakening yen? The central bank holds a two-day meeting ending on October 31st and may have to revise its quarterly inflation and growth forecasts. The markets are on alert for the BoJ to phase out its massive stimulus but BoJ policy makers haven’t shown signs of shifting policy.

In the US, it’s a very light data calendar, highlighted by a speech from FOMC member Patrick Harker. On Thursday, Fed Chair Jerome Powell said that inflation was still too high and that growth would need to slow if inflation is to fall to the 2% target. Powell noted that further hikes might not be needed, as the rise in Treasury yields could help dampen growth and lower inflation.

USD/JPY Technical

- 150.22 is a weak resistance line, followed by resistance at 150.86.

- 149.19 and 148.55 are providing support

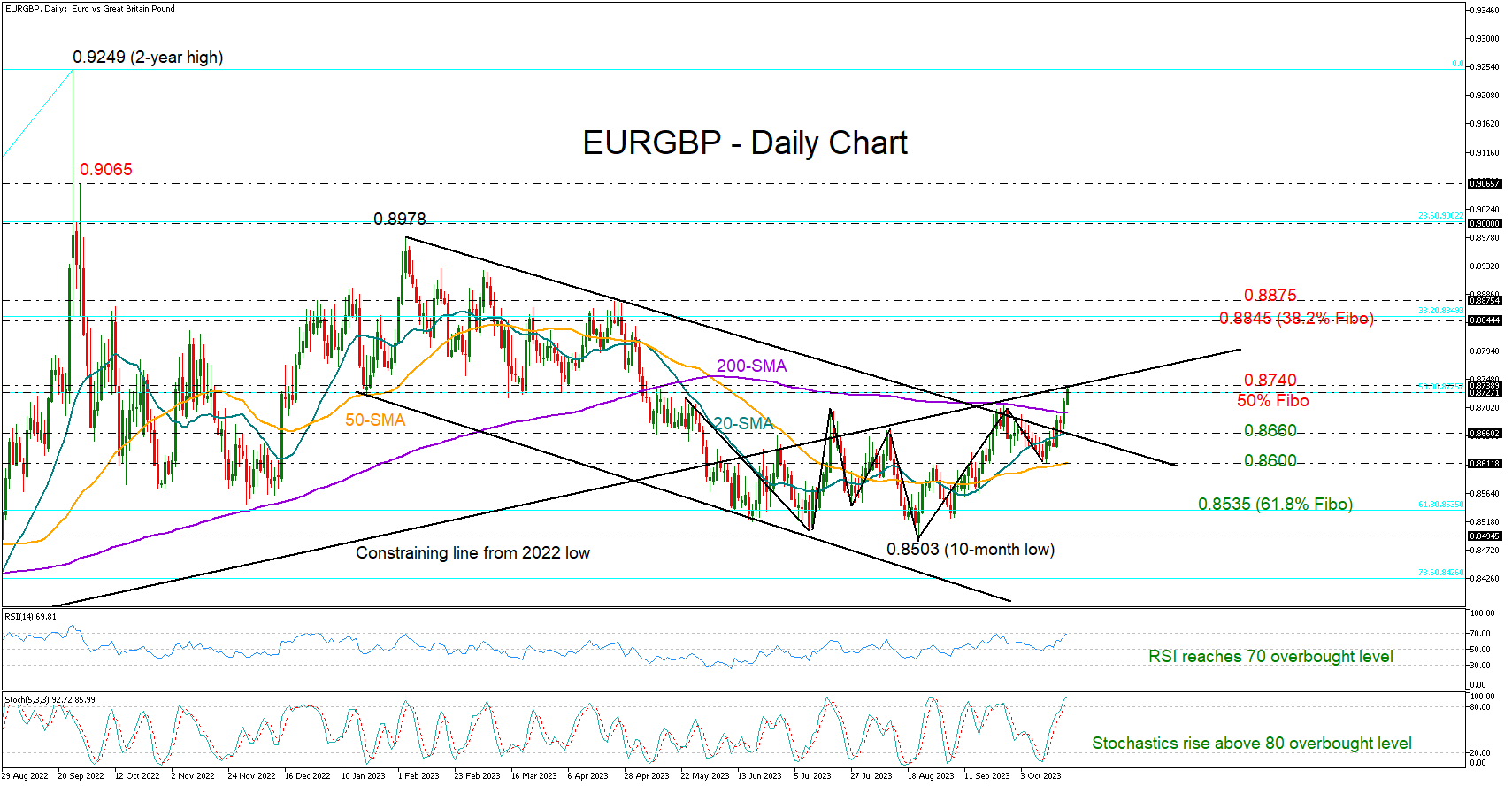

EURGBP Snaps Key Barriers, But One More Remains

- EURGBP heads for a strong weekly close

- Bull run faces another challenge at 0.8740

EURGBP recorded a couple of bullish achievements this week, ascending above the resistance trendline, which halted September’s bull run, and crawling above the 200-day simple moving average (SMA) for the first time since May.

The price resumed its bullish momentum on Friday to unlock a six-month high of 0.8736, but the 50% Fibonacci retracement of the 0.8201-0.9249 upleg at 0.8725 might prove challenging as the RSI and the stochastic oscillator hint at strengthening overbought conditions. It’s also worth noting that the upward-sloping line drawn from the 2022 trough came to block the way higher earlier today.

If the recovery continues above 0.8740, it may pick up steam towards the 38.2% Fibonacci level of 0.8850. The 0.8875 barrier from April is within breathing distance and will be closely watched too. Should it prove easy to overcome, the pair could head for the 0.8930 bar.

In the event sellers take over, initial support might develop around the 20-day simple moving average (SMA) at 0.8660 and near the broken resistance trendline. A drop below that base would neutralize the short-term picture, likely motivating another negative correction towards the 50-day SMA at 0.8611. Additional losses from there could aggressively squeeze the price towards the 61.8% Fibonacci of 0.8535.

All in all, EURGBP is looking cautiously bullish in the short-term picture. A decisive close above 0.8740 could bolster buying appetite, whilst a pullback below 0.8660, and more importantly beneath 0.8600, could create fresh selling interest.