Sample Category Title

Cliff Notes: Mixed Signals Keep Central Banks Data Dependent

Key insights from the week that was.

In Australia, the October RBA meeting minutes provided a detailed outline of the Board’s considerations for policy. The case to raise rates centred on the outlook for inflation and potential upside risks. The argument for remaining on hold rested on the fact that the full impact of policy tightening is still to be felt while inflation, labour market tightness and economic activity are all moderating (as discussed below). The arguments behind both options were familiar; with few material developments over the month, remaining on hold was, once again, recognised as the stronger policy option.

That said, there were some important shifts in rhetoric, most notably the assertion that “The Board has a low tolerance for a slower return of inflation to target than currently expected.” As outlined by Chief Economist Luci Ellis, this implies that if a significant upside surprise were to occur with regards to inflation, the Board is willing to respond by tightening. The RBA Board’s November discussion will benefit from a detailed update on inflation, with the Q3 CPI report due next week and new RBA staff forecasts to be tabled. As detailed in our Q3 CPI preview (available later today on WestpacIQ), considerable uncertainty remains over the inflation outlook, particularly the competing impacts of rising childcare costs and recent changes to childcare rebates. If inflation prints as we anticipate (1.1%qtr/5.3%yr for Q3), we believe the RBA will remain on hold through year end and well into 2024.

Moving on, the September Labour Force Survey provided a fairly mixed read on current labour market conditions. Broadly, the results did not shift the overarching view that the labour market is at a turning point -- no longer tightening, but yet to materially soften. This is highlighted by the gradual moderation in the pace of employment growth – which we currently judge as modestly below trend – in addition to two consecutive monthly declines in hours worked. However, that the participation rate fell sharply (–0.3ppts) whilst employment rose modestly serves as a reminder of the survey’s volatility month-to-month. We expect labour market conditions to continue cooling into year-end and slack to build more materially through 2024 as economic growth holds well below trend.

In Asia, Chinese Q3 GDP surprised to the upside coming in at 4.9%yr and 5.2% year-to-date, putting the 5% full-year growth target well within reach. Looking at the September monthly data, industrial production (IP) remains a bright spot, rising 4.5%yr with strength most apparent in materials. Strong export demand also continues to support IP as China expands the array of manufacturing components it produces.

Fixed asset investment rose 3.1%yr, held up by non-property related investment. The authorities' focus on productivity and efficiency is clear. Key sub-categories of high-tech investment continue to grow at between 10% and 40% even as their combined size nears that of property investment. Utilities investment is also up 25% year-to-date and other infrastructure around 6%. Unlike property, these sub-categories of investment are income and efficiency producing; hence their completion is just the start of their contribution to the economy. If China’s success with trade continues, further robust investment growth can easily be justified.

However, the property market remains a heavy weight -- property investment down 9.1% year-to-date in September, extending 2022’s decline. Recent stimulus measures, including cuts to the reserve requirement ratio and deposit requirements for homebuyers, are yet to take full effect and may be hindered by persistent pessimism around the property market, whether it be uncertainty around completion or future price increases.

The effectiveness of policy for property also threatens consumption via wealth. The September retail sales data highlight this risk. Total sales rose 5.5%yr, robust 13.8%yr growth in catering services a stark contrast to modest 4.6%yr growth in goods, implying households are financing higher spending on services by limiting or delaying discretionary spending on goods. The urban/rural split also suggests households in major cities remain cautious on the outlook.

Overall, Q3 GDP and the September monthly data imply current momentum in China’s economy is stronger than the market had anticipated, and there is no obvious reason why it will fail immediately. But risks around the consumer remain, particularly for young workers. So, while we have revised up our 2023 forecast from 5.0% to 5.3%, we have also lowered our 2024 forecast from 5.5% to 5.3% after which a deceleration to around 5.0% is likely in 2025.

There was also plenty for the Bank of England to ponder this week. Wages grew 8.1%yr, down from 8.5%yr previously. Private sector wages led the deceleration, easing to 7.1%yr from 7.7%yr. While the BoE has indicated that they are looking at measures beyond Average Weekly Earnings, a downshift should give them comfort that emerging labour market slack is cooling wages.

September's CPI in contrast remained steady at 6.7%yr, much to the disappointment of markets, but still below the BoE's 6.9%yr forecast. Goods disinflation persisted but was compensated for by services. The October result, out before the November meeting, ought to show a substantial easing in inflation coming off a high base caused by a spike in electricity prices in 2022. Easing wages and CPI trending down should give the BoE enough confidence to remain on hold at the November meeting.

Over in the US, retail sales surprised to the upside, total sales rising 0.7%mth and the control group 0.6%mth in September. August's figures were also revised up 0.2ppts for headline and 0.1ppt for the control group. The health of the labour market and long-term fixed rate mortgages continue to provide households with capacity to spend, even as already-weak consumer expectations for the economy deteriorate further. Providing an additional buffer, recent data revisions imply consumers have more pandemic savings left than previously thought.

FOMC Chair Powell’s appearance at the Economic Club of New York closed out the key economic events for the week. The focus of his prepared remarks was policy’s progress to date and a belief that there are risks in both tightening “too little” and “too much”. The extended Q&A that followed covered an array of possibilities and uncertainties for the outlook, but overall made clear that the FOMC are broadly comfortable with the current stance of policy as long as it continues to prove effective – i.e. inflation continues to trend down towards 2%yr. Also front of mind for the Committee is the potential impact on financial conditions of rising term interest rates which are assessed to be a consequence of an increased term premium, not fed funds rate or inflation expectations.

This rise in yields is having a similar effect to further increases in the fed funds rate, at the margin increasing the probability of inflation staying on course. The FOMC therefore looks set to remain on hold in November and thereafter will continue to assess conditions. We expect a further softening of the labour market and a sharp pullback in aggregate growth from Q4, which should justify the FOMC also remaining on hold in December and January. The degree of further improvement in inflation will subsequently dictate the timing and scale of cuts in 2024 and beyond.

NZDUSD Looking to End 5 Waves Move

Short Term Elliott Wave in NZDUSD shows pair is unfolding as a 5 waves move lower from 2.2.2023 high. Down from 2.2.2023 high, wave 1 ended at 0.6084 and rally in wave 2 ended at 0.6411. Pair resumed lower in wave 3 towards 0.58594. Bounce in wave 4 ended at 0.6054 as the 1 hour chart below. Pair has resumed lower in wave 5. Internal subdivision of wave 5 is unfolding as a 5 waves impulse. Down from wave 4, wave ((i)) ended at 0.60 and rally in wave ((ii)) ended at 0.6033.

Pair resumed lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 0.6 and rally in wave (ii) ended at 0.6025. Wave (iii) lower ended at 0.5897 and rally in wave (iv) ended at 0.5921. Final leg lower wave (v) ended at 0.5879 which completed wave ((iii)). Pair then rallied in wave ((iv)) and ended at 0.5929. Pair has resumed lower in wave ((v)). Down from wave ((iv)), wave (i) ended at 0.587 and rally in wave (ii) ended at 0.5919. Wave (iii) lower ended at 0.5814 and rally in wave (iv) ended at 0.5866.

Expect wave (v) to end with 1 more push lower which should complete wave ((v)) of 5 of (1). Afterwards, pair should rally in larger degree wave (2) to correct cycle from 2.2.2023 high. Near term, as far as pivot at 0.6954 stays intact, expect pair to extend lower before ending cycle from 2.2.2023 high.

NZDUSD 60 Minutes Elliott Wave Chart

NZDUSD Elliott Wave Video

https://www.youtube.com/watch?v=6_Lv-XiWYss

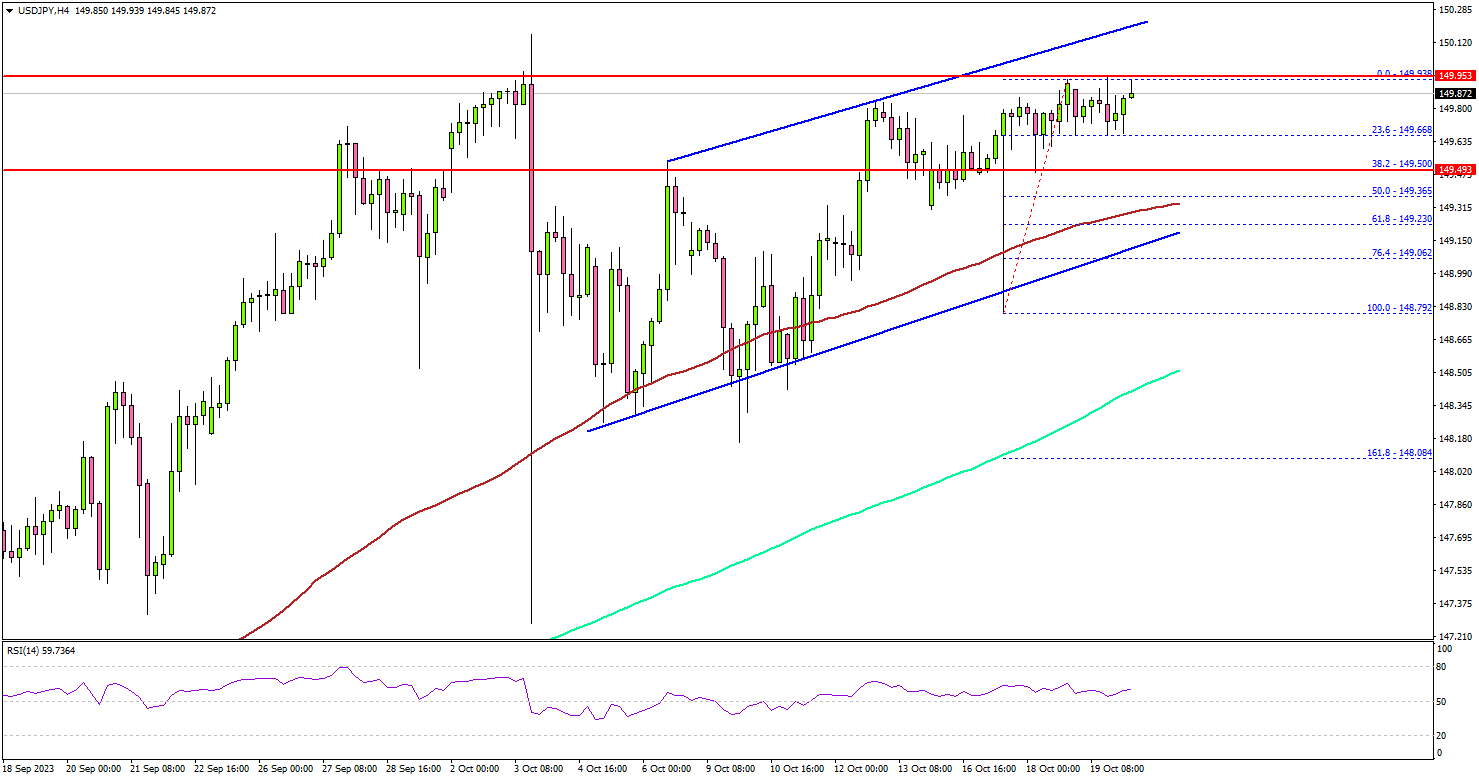

USD/JPY Targets Fresh High, Gold Price Could Revisit $2K

Key Highlights

- USD/JPY is consolidating gains above the 149.40 support.

- A key rising channel is forming with support near 149.20 on the 4-hour chart.

- Gold prices are showing bullish signs and might rise further toward $2,000.

- Israeli PM Benjamin Netanyahu stated on the ongoing conflict “It'll be a long war”.

USD/JPY Technical Analysis

The US Dollar remained strong above the 148.50 resistance against the Japanese Yen. USD/JPY is consolidating, and the bulls might aim for more gains above 150.00 amid the Israel-Hamas war and border concerns.

Looking at the 4-hour chart, the pair remained well-bid above the 149.00 pivot level. The pair settled well above the 149.00 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

If there is a downside correction, the pair might find bids near 149.50. It is close to the 50% Fib retracement level of the upward move from the 148.79 swing low to the 149.93 high.

The next key support is seen near the 149.20 level. There is also a key rising channel forming with support near 149.20, below which it could test 148.50. Any more losses might send the pair toward the 148.00 level.

On the upside, the pair might struggle to clear the 150.00 resistance. A close above the 150.00 level might send the pair toward the 151.20 level. The next key resistance is near 152.00, above which the pair could rise toward the 153.50 level.

Looking at gold prices, there was a strong increase above the $1,950 level and the current price action suggests high chances of more gains toward $2,000.

Economic Releases

- UK Retail Sales for Sep 2023 (YoY) - Forecast 0%, versus -1.4% previous.

- UK Retail Sales for Sep 2023 (MoM) - Forecast -0.1%, versus +0.4% previous.

Japan’s core CPI slips below 3% mark to 2.8% yoy

Inflationary momentum in Japan showed signs of easing in September, with all-item CPI decelerating to 3.0% yoy, down from 3.2% yoy in the prior month. Core CPI, which strips out the volatile food prices, also showed a downtrend, registering at 2.8% yoy, a dip from 3.1% yoy. Furthermore, core-core CPI, which excludes both food and energy prices, declined marginally from 4.3% yoy to 4.2% yoy.

Remarkably, core inflation dipped below the 3% mark for the first time since August 2022. Nevertheless, it remains above BoJ's 2% target, marking the 18th consecutive month of surpassing this benchmark.

The detailed breakdown of the data indicates that energy prices were a significant drag, plunging by -11.7% yoy. This downturn can be attributed to the government's proactive measures to trim utility bills, resulting in double-digit falls in electricity and city gas prices. On the contrary, food prices remained on an upward swing, posting 8.8% yoy increase.

There are reports suggesting an upward revision in BoJ's core CPI forecast for fiscal 2023. Sources familiar with the bank's deliberations indicate a possible revision from 2.5% to nearly 3.0%. All eyes will now be on BoJ 's policy meeting scheduled for Oct 31, where a new outlook report is anticipated.

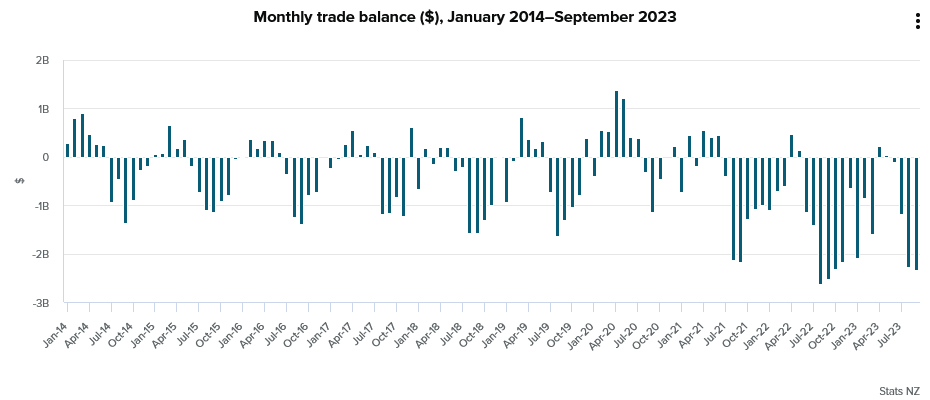

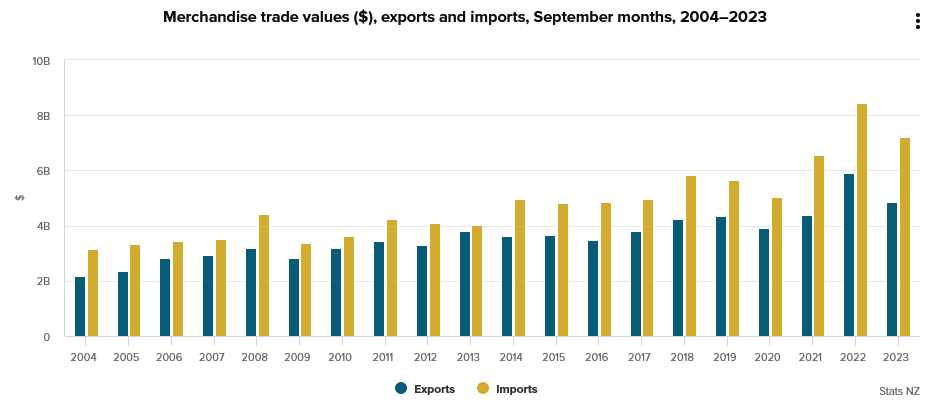

New Zealand’s exports down -18% yoy in Sep, China leads decline again

New Zealand's trade balance for September reveals a deficit of NZD -2.3B, driven by a notable fall in goods exports of -18% yoy, bringing the total to NZD 4.9B. The decline in imports was also significant, dropping by -15% yoy to NZD 7.2B.

A striking feature of this downturn is the notable reduction in exports to China, marking a deviation from the consistent growth observed over the past decade. International trade manager Alasdair Allen noted, "Over the past decade, exports to China have been steadily increasing, with a flat period during COVID-19, but in recent months this has started to shift."

Breaking down the export figures by country, China recorded a 20% yoy drop, equivalent to NZD 332 million, leading the downturn. Exports to Australia, US, EU, and Japan also experienced declines, calculated at -3.3%, -6.7%, -26%, and -12% yoy, respectively.

On the imports front, China once again played a significant role, with imports from the country decreasing by -17% yoy. Imports from EU and Australia also dropped by -1.5% yoy and -21% yoy respectively. Imports from South Korea contracted by -16% yoy. In contrast, imports from US saw a growth of 6.1% yoy.

Fed officials stress patience and vigilance amid rising treasury yields

Comments from some key Fed officials overnight underscore the central bank's cautious approach in the face of evolving economic conditions, particularly the rise in treasury yields and persistent inflation.

Philadelphia Fed President Patrick Harker asserted, "We are at the point where we can hold rates where they are." He acknowledged the recent data trends, noting, "So far, economic and financial conditions are evolving roughly as I expected," but added that some indicators have been "a tad stronger than my baseline forecast." Harker championed patience in monetary policy, suggesting that "a resolute, but patient, stance of monetary policy will allow us to achieve the soft landing that we all wish for our economy."

Dallas Fed President Lorie Logan emphasized the natural tightening effect of the recent uptick in treasury yields, stating they have "done some of this tightening work for us." While Logan recognized some progress in inflation management, she conceded, "it's still too high." Stressing the importance of the broader economic environment, she remarked, "It's important that we have continued restrictive financial conditions."

Chicago Fed President Austan Goolsbee approached the inflation debate from a historical perspective. He noted, "There's a widely held conventional wisdom that if you get the inflation rate down more than 5 percentage points you will have to have a big recession to do that." Contrary to this belief, Goolsbee expressed optimism, saying, "So far, we haven't had that recession, I'm still hopeful we can avoid it entirely."

Lastly, Atlanta Fed President Raphael Bostic laid clear his priorities, stating, "As for inflation, that is job one for now." He elucidated the broad impacts of inflation, observing that "Across the economy and demographic groups, inflation is the force that is most painful and drives more people to precariousness."

Fed’s Powell signals caution on rate hikes, notes yield surge as de facto tightening

Fed Chair Jerome Powell, in his speech at the Economic Club of New York, asserted that while the option for an additional rate hike remains open, a prudent and careful approach will be the governing principle. Market participants, digesting Powell's words, now overwhelmingly anticipate an extension of Fed's pause in November, a sentiment reflected in fed fund futures pointing towards a 100% chance of this outcome. Referring to the recent rise in yields, he said it might have an effect "at the margins" on reducing the necessity for further rate hikes.

Powell suggested that the surge in yields might be linked to growing concerns surrounding fiscal deficits and mentioned that the process of Quantitative Tightening could also be influencing it. Highlighting that the uptick in yields acts as a de facto policy tightening, Powell raised the possibility that this might reduce the need for aggressive rate hikes in the future.

Although inflation metrics have dipped during the summer, Powell emphasized, "inflation is still too high, and a few months of good data are only the beginning." The inflation outlook remains uncertain, marked by the unpredictability of its stabilization point in the upcoming quarters, and Powell concedes that, "the path is likely to be bumpy."

With an eye on economic growth and labor market dynamics, Powell indicated that persistent above-trend growth or sustained labor market tightness could trigger a reevaluation of the inflation outlook. Such developments "could warrant further tightening of monetary policy."

Underscoring the complexities and potential pitfalls ahead, Powell stated, Committee is "proceeding carefully." "We will make decisions about the extent of additional policy firming and how long policy will remain restrictive based on the totality of the incoming data, the evolving outlook, and the balance of risks," he added.

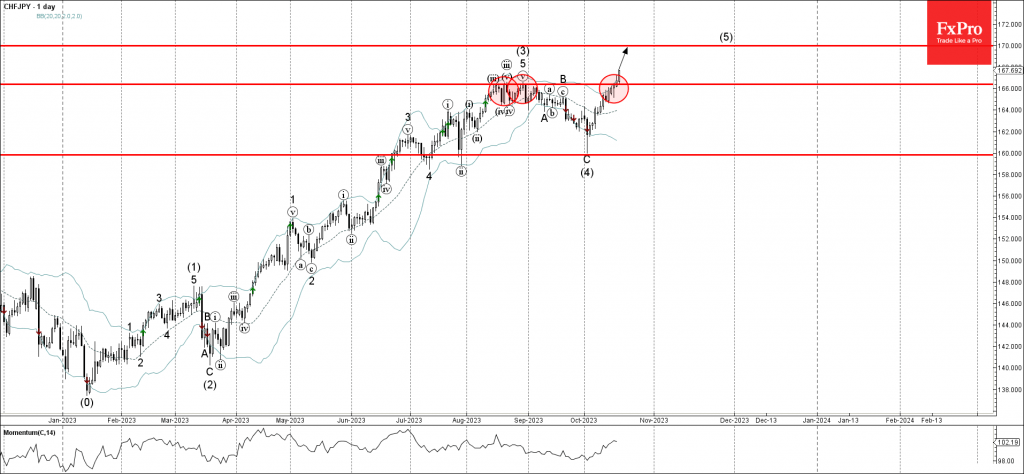

CHFJPY Wave Analysis

- CHFJPY under bullish pressure

- Likely to test resistance level 170.00

CHFJPY currency pair under the bullish pressure after the pair broke above the key resistance level 166.10 (which reversed the pair 3 times in August as can be seen below).

The breakout of the resistance level 166.10 accelerated the active intermediate impulse wave (5) from the start of October.

Given the clear daily uptrend and the accelerating upward momentum, CHFJPY can be expected to rise further toward the next resistance level 170.00 (target for the completion of the active impulse wave (5)).

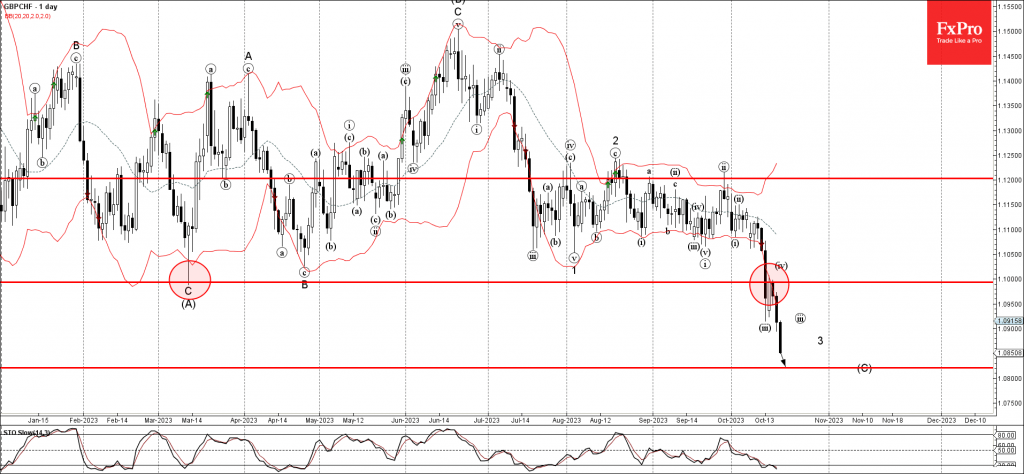

GBPCHF Wave Analysis

- GBPCHF falling inside minor impulse wave 3

- Likely to fall to support level 1.0820

GBPCHF currency pair continues to fall inside the minor impulse wave 3, which reversed earlier from the resistance level 1.1000 (former multi-month support level from March).

The active minor impulse wave 3 belongs to the intermediate impulse wave (C) from the middle of June.

Given the clear daily downtrend, GBPCHF can be expected to fall further toward the next support level 1.0820 (target for the completion of the active impulse wave (C)).

Dollar Declines Extend Post Powell, November No Longer Live But Future Rate Hikes Still on Table

Wall Street went on a mini rollercoaster ride during Fed Chair Powell’s speech. Powell’s comments were mostly in-line with other officials and support the belief that policy might not be “too tight” and future rate hikes may be needed. Powell’s comments support their higher for longer mantra, but fell short of signaling a rate hike was likely in December. Until inflation is much lower, the Fed will try to jawbone the market into thinking more hikes are possible.

Fed Chair Powell Key Quotes from prepared remarks:

- Additional evidence of a strong economy may merit hiking

- Geopolitical tensions are highly elevated and pose key risks

- FOMC proceeding carefully given risks, hikes so far

- Financial conditions moves can affect policy if persistent

The dollar extended declines after the release of Fed Chair Powell’s speech. Fed Chair Powell said, “Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy.” The initial market reaction was somewhat dovish as Powell acknowledged that persistent changes in in financial conditions could change the path of monetary policy. The bond market helped them take rates to restrictive territory that should break the economy and allow for inflation to fall to the Fed’s target.

Fed Chair Powell’s Q/A:

- At the margin, yield rise could mean less need to hike

- Fed has to let rise in yields play out, watch it

The long-end of the curve surged higher but pared gains, the 30-year Treasury yield settled around 5.05%, roughly 5.5 bps higher on the day. Powell noted that losses in commercial real estate are inevitable, but that they don’t see it causing broader problems. With the risk of an immediate rate hike off the table the dollar settled softer against all of its major trading partners.