Sample Category Title

New Zealand’s exports down -18% yoy in Sep, China leads decline again

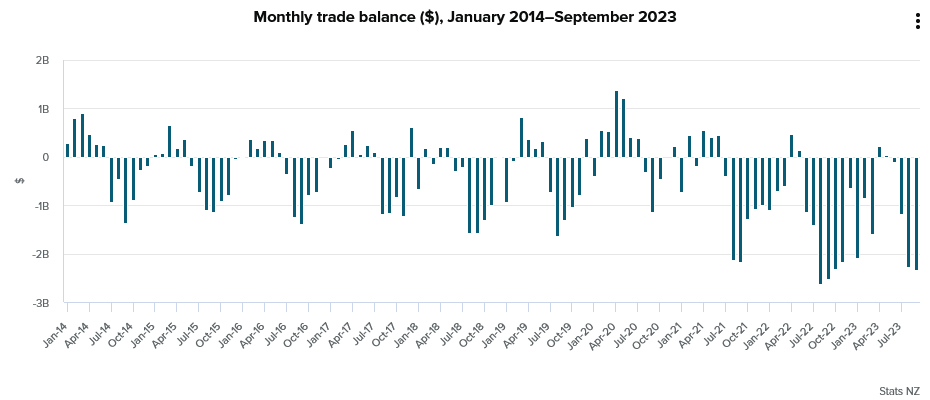

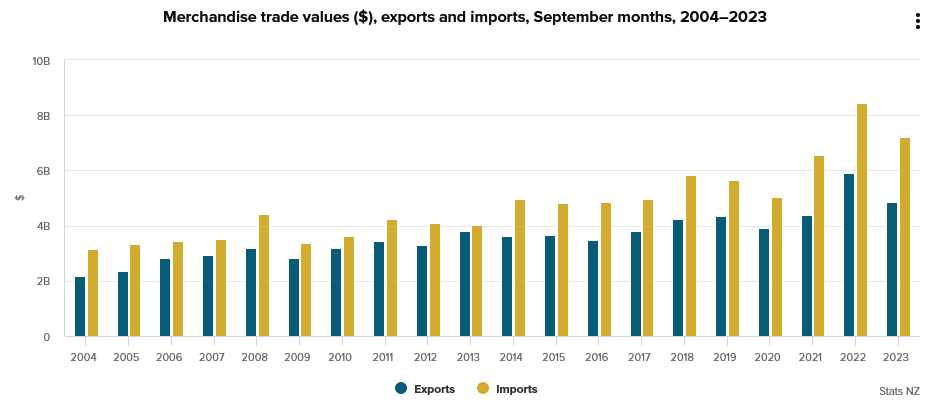

New Zealand's trade balance for September reveals a deficit of NZD -2.3B, driven by a notable fall in goods exports of -18% yoy, bringing the total to NZD 4.9B. The decline in imports was also significant, dropping by -15% yoy to NZD 7.2B.

A striking feature of this downturn is the notable reduction in exports to China, marking a deviation from the consistent growth observed over the past decade. International trade manager Alasdair Allen noted, "Over the past decade, exports to China have been steadily increasing, with a flat period during COVID-19, but in recent months this has started to shift."

Breaking down the export figures by country, China recorded a 20% yoy drop, equivalent to NZD 332 million, leading the downturn. Exports to Australia, US, EU, and Japan also experienced declines, calculated at -3.3%, -6.7%, -26%, and -12% yoy, respectively.

On the imports front, China once again played a significant role, with imports from the country decreasing by -17% yoy. Imports from EU and Australia also dropped by -1.5% yoy and -21% yoy respectively. Imports from South Korea contracted by -16% yoy. In contrast, imports from US saw a growth of 6.1% yoy.

Fed officials stress patience and vigilance amid rising treasury yields

Comments from some key Fed officials overnight underscore the central bank's cautious approach in the face of evolving economic conditions, particularly the rise in treasury yields and persistent inflation.

Philadelphia Fed President Patrick Harker asserted, "We are at the point where we can hold rates where they are." He acknowledged the recent data trends, noting, "So far, economic and financial conditions are evolving roughly as I expected," but added that some indicators have been "a tad stronger than my baseline forecast." Harker championed patience in monetary policy, suggesting that "a resolute, but patient, stance of monetary policy will allow us to achieve the soft landing that we all wish for our economy."

Dallas Fed President Lorie Logan emphasized the natural tightening effect of the recent uptick in treasury yields, stating they have "done some of this tightening work for us." While Logan recognized some progress in inflation management, she conceded, "it's still too high." Stressing the importance of the broader economic environment, she remarked, "It's important that we have continued restrictive financial conditions."

Chicago Fed President Austan Goolsbee approached the inflation debate from a historical perspective. He noted, "There's a widely held conventional wisdom that if you get the inflation rate down more than 5 percentage points you will have to have a big recession to do that." Contrary to this belief, Goolsbee expressed optimism, saying, "So far, we haven't had that recession, I'm still hopeful we can avoid it entirely."

Lastly, Atlanta Fed President Raphael Bostic laid clear his priorities, stating, "As for inflation, that is job one for now." He elucidated the broad impacts of inflation, observing that "Across the economy and demographic groups, inflation is the force that is most painful and drives more people to precariousness."

Fed’s Powell signals caution on rate hikes, notes yield surge as de facto tightening

Fed Chair Jerome Powell, in his speech at the Economic Club of New York, asserted that while the option for an additional rate hike remains open, a prudent and careful approach will be the governing principle. Market participants, digesting Powell's words, now overwhelmingly anticipate an extension of Fed's pause in November, a sentiment reflected in fed fund futures pointing towards a 100% chance of this outcome. Referring to the recent rise in yields, he said it might have an effect "at the margins" on reducing the necessity for further rate hikes.

Powell suggested that the surge in yields might be linked to growing concerns surrounding fiscal deficits and mentioned that the process of Quantitative Tightening could also be influencing it. Highlighting that the uptick in yields acts as a de facto policy tightening, Powell raised the possibility that this might reduce the need for aggressive rate hikes in the future.

Although inflation metrics have dipped during the summer, Powell emphasized, "inflation is still too high, and a few months of good data are only the beginning." The inflation outlook remains uncertain, marked by the unpredictability of its stabilization point in the upcoming quarters, and Powell concedes that, "the path is likely to be bumpy."

With an eye on economic growth and labor market dynamics, Powell indicated that persistent above-trend growth or sustained labor market tightness could trigger a reevaluation of the inflation outlook. Such developments "could warrant further tightening of monetary policy."

Underscoring the complexities and potential pitfalls ahead, Powell stated, Committee is "proceeding carefully." "We will make decisions about the extent of additional policy firming and how long policy will remain restrictive based on the totality of the incoming data, the evolving outlook, and the balance of risks," he added.

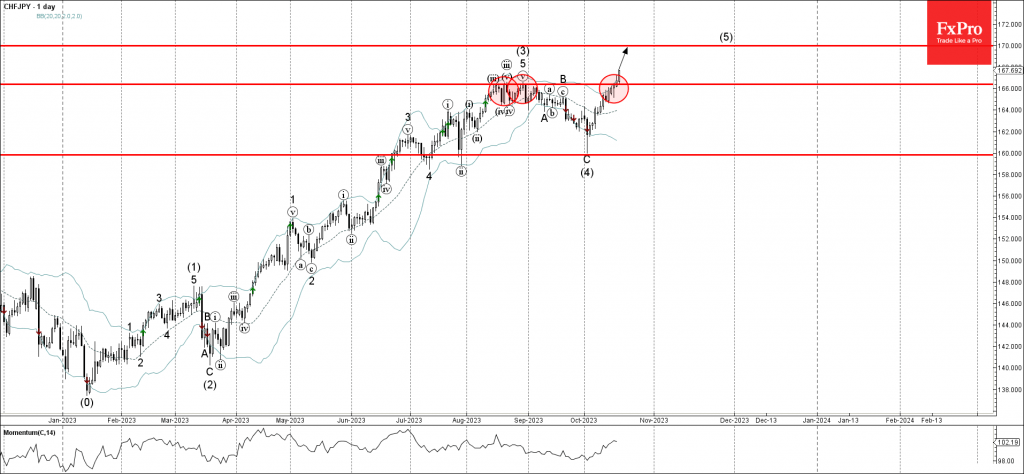

CHFJPY Wave Analysis

- CHFJPY under bullish pressure

- Likely to test resistance level 170.00

CHFJPY currency pair under the bullish pressure after the pair broke above the key resistance level 166.10 (which reversed the pair 3 times in August as can be seen below).

The breakout of the resistance level 166.10 accelerated the active intermediate impulse wave (5) from the start of October.

Given the clear daily uptrend and the accelerating upward momentum, CHFJPY can be expected to rise further toward the next resistance level 170.00 (target for the completion of the active impulse wave (5)).

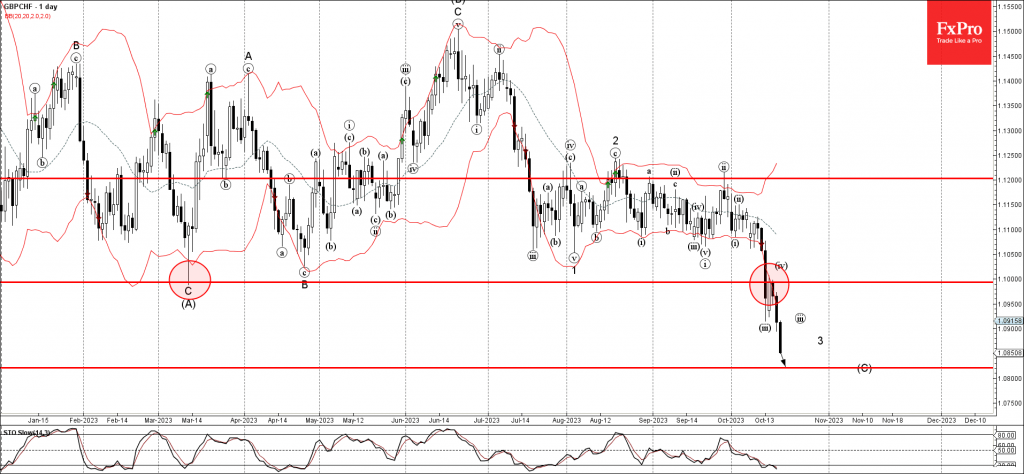

GBPCHF Wave Analysis

- GBPCHF falling inside minor impulse wave 3

- Likely to fall to support level 1.0820

GBPCHF currency pair continues to fall inside the minor impulse wave 3, which reversed earlier from the resistance level 1.1000 (former multi-month support level from March).

The active minor impulse wave 3 belongs to the intermediate impulse wave (C) from the middle of June.

Given the clear daily downtrend, GBPCHF can be expected to fall further toward the next support level 1.0820 (target for the completion of the active impulse wave (C)).

Dollar Declines Extend Post Powell, November No Longer Live But Future Rate Hikes Still on Table

Wall Street went on a mini rollercoaster ride during Fed Chair Powell’s speech. Powell’s comments were mostly in-line with other officials and support the belief that policy might not be “too tight” and future rate hikes may be needed. Powell’s comments support their higher for longer mantra, but fell short of signaling a rate hike was likely in December. Until inflation is much lower, the Fed will try to jawbone the market into thinking more hikes are possible.

Fed Chair Powell Key Quotes from prepared remarks:

- Additional evidence of a strong economy may merit hiking

- Geopolitical tensions are highly elevated and pose key risks

- FOMC proceeding carefully given risks, hikes so far

- Financial conditions moves can affect policy if persistent

The dollar extended declines after the release of Fed Chair Powell’s speech. Fed Chair Powell said, “Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy.” The initial market reaction was somewhat dovish as Powell acknowledged that persistent changes in in financial conditions could change the path of monetary policy. The bond market helped them take rates to restrictive territory that should break the economy and allow for inflation to fall to the Fed’s target.

Fed Chair Powell’s Q/A:

- At the margin, yield rise could mean less need to hike

- Fed has to let rise in yields play out, watch it

The long-end of the curve surged higher but pared gains, the 30-year Treasury yield settled around 5.05%, roughly 5.5 bps higher on the day. Powell noted that losses in commercial real estate are inevitable, but that they don’t see it causing broader problems. With the risk of an immediate rate hike off the table the dollar settled softer against all of its major trading partners.

Euro Rises, US Jobless Claims Drop

- US unemployment claims drop below 200K

- ECB’s Lagarde expresses concern over oil inflation

The euro has bounced back on Thursday, erasing the losses from a day earlier. In the North American session, EUR/USD is trading at 1.0573, up 0.36%.

The Middle East is back in the headlines as Israel and Hamas are engaged in fierce fighting. The market reaction has been muted, as investors haven’t snapped up the safe-haven US dollar. Still, there is growing concern that oil prices could top $100 if the conflict widens.

ECB President Lagarde had a closed meeting this week with eurozone financial ministers, according to a report in Bloomberg. Lagarde noted the risk of higher oil prices would affect Europe as well as the US. If oil prices jump higher, it will complicate the ECB’s efforts to push inflation back down to the 2% target.

US unemployment claims drop, Philly manufacturing improves

In the US, unemployment claims for the week of October 14th sizzled at 198,000. This was lower than the previous week’s release of 211,000 (revised) and lower than the consensus estimate of 212,000. The US labour market has been showing signs of softening as the Federal Reserve’s rate hikes continue to filter through the economy and dampen economic growth.

The manufacturing sector has been struggling throughout the major economies, and US exceptionalism hasn’t translated into strong manufacturing numbers. Earlier today, the Philadelphia Fed Manufacturing Index improved to -9 in October, up from -13.5 in September but missing the market consensus of -6.4. The index has managed only one gain over the past 13 months.

The markets are always interested in what Fed members have to say, hoping for some insights into Fed rate policy. A host of FOMC members will deliver remarks today, highlighted by a speech from Fed Chair Powell at an event in New York City.

Today’s lineup has added significance as the Fed will enter a blackout period ahead of the meeting on November 1st. The sharp rise in US Treasuries has led to some Fed members saying that inflation could fall without further hikes, and investors will be watching to see if that dovish message is repeated today by Powell and his colleagues.

EUR/USD Technical

- EUR/USD tested resistance at 1.0548 earlier. Above, there is resistance at 1.0600

- 1.0456 and 1.0404 are providing support

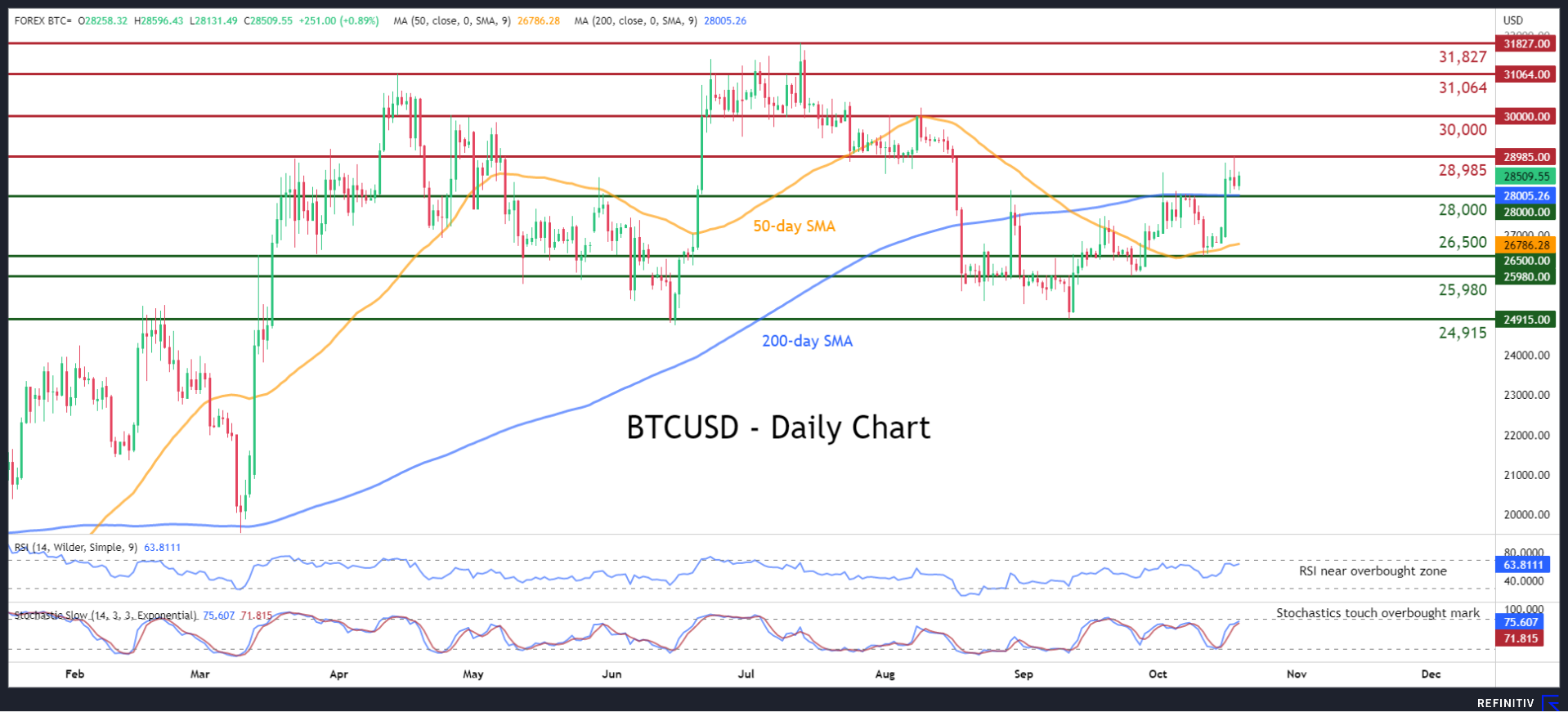

BTCUSD Consolidates Above 200-day SMA

- BTCUSD reclaims crucial 200-day SMA, posting 2-month high

- Trades flat in the past few daily sessions

- Momentum indicators are heavily tilted to the bullish side

BTCUSD (Bitcoin) had been forming a structure of higher highs and higher lows since its bounce off the September bottom of 24,915. Moreover, the price jumped above the 200-day simple moving average (SMA) after several failed attempts, but this bullish outbreak failed to trigger a rally.

If the bulls keep applying upside pressures, the price could initially test the recent two-month high of 28,985. Even higher, the crucial 30,000 psychological mark could curb further advances. A jump above that zone may pave the way for the April peak of 31,064.

On the flipside, bearish actions could send the price lower to test the 200-day SMA, currently at 28,000. Piercing through that floor, the digital coin may descend towards the October low of 26,500 ahead of the September support of 25,980. Should that barricade fail, the September bottom of 24,915 could provide downside protection.

Overall, BTCUSD has been in a steady advance in the past month, reaching a two-month peak on Wednesday. However, traders should be cautious as the price seems to be approaching overbought conditions.

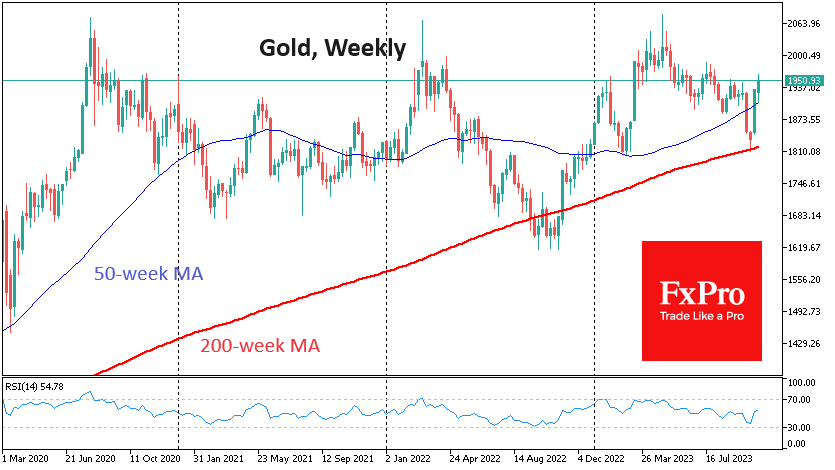

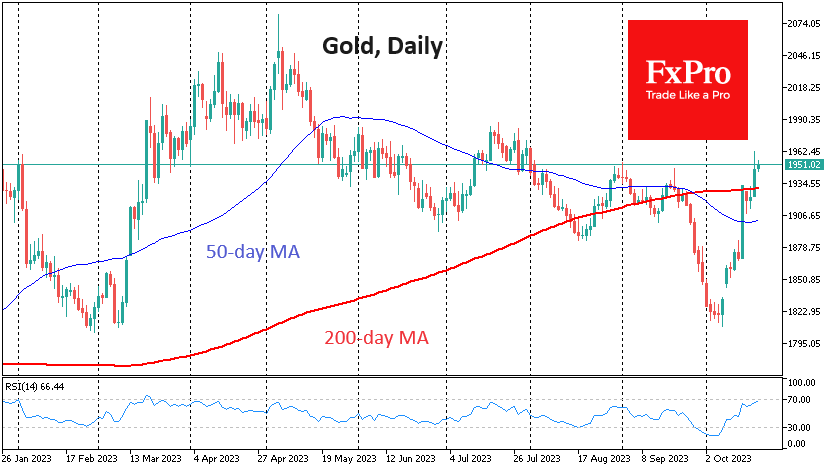

Gold Rises Against the Tide, But Energy Running Out

Gold is trading at nearly $1950 an ounce, having surged since the end of July after hitting $1810 just under two weeks ago on October 6th.

Gold lost value rapidly in late September as US Treasury yields rose. However, the fall and the rise in yields stopped after the employment report. This added to speculation that the Fed will not raise rates in November, although some members are leaning towards a December hike.

The war in the Middle East sparked gold’s momentum, forming a gap at the open on Monday, October 9th. It is continuing now but has already been priced in and is unlikely to be a major driver in the coming days. There is no strong capital outflow from equity or bond markets, so there is no basis for gold buying.

At the same time, bond prices have fallen again this week. 10-year Treasury yields close to 5% – the highest since the peak in 2007. They have not been consistently higher since 2002. This has begun to undermine risk appetite in the equity market, but this change has not yet reached gold, which ignores the main reason for its decline at the end of last month.

Gold also resists the renewed pullback in the dollar, which has recovered more than half of its losses from its early October peak. The upshot is that gold is now rising against the tide. It is likely to run out of steam sooner rather than later.

Technically, gold had necessary support on its side in the form of the 200-week average. The price touched the lows earlier in the month and quickly moved away from it. The local correction at the beginning of this week ended with a touch of the 50-week average.

In the smaller daily timeframes on Wednesday, gold consolidated above the 200-day moving average, fuelling impulsive buying and short covering, taking the price above $1960 at one point.

However, gold is now close to the overbought territory, making it vulnerable to a reversal under pressure from fundamental factors such as high bond yields and a strengthening dollar.

We also note that the war factor in the Middle East is hardly a reasonable long-term bullish bet for gold. The turbulent environment is scarcely conducive to sustained demand. The Russia-Ukraine conflict caused a similar spike in the price that we already have, but then there were fears of a supply disruption from a major producer. Even then, the price fell well below where it started before the “war rally”.