Sample Category Title

GBP/USD Flat as Retail Sales Eyed

- US unemployment claims fall below 200K

- UK retail sales expected to improve to -0.1%

The British pound is drifting on Thursday. In the North American session, GBP/USD is trading at 1.2142, almost unchanged.

The UK inflation report on Wednesday was a stark reminder that inflation remains stubborn and sticky. The Bank of England has raised the benchmark rate to 5.25%, but headline inflation was steady at 6.7% y/y and the core rate ticked lower to 6.1%, down from 6.2%. Both readings were higher than expected disappointed investors sent the British pound lower on Wednesday.

A key driver of headline inflation was rising motor fuel prices. The Israel-Hamas war has raised tensions throughout the Middle East and if there are disruptions in crude oil, inflation would likely rise due to higher motor fuel costs.

The UK wraps up the week with retail sales on Friday. The markets are braced for a weak September with a market estimate of -0.2%, following a 0.4% gain in August. On an annualized basis, retail sales declined by 1.4% in August, but are expected to improve to -0.1% in September.

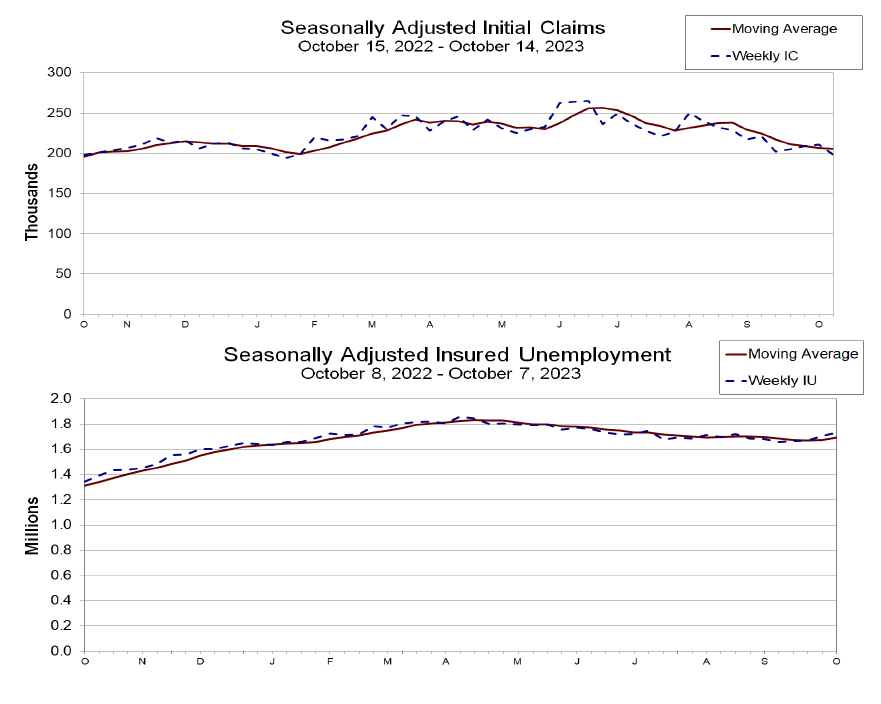

In the US, unemployment claims for the week of October 14th sizzled at 198,000. This was lower than the previous week’s release of 211,000 (revised) and lower than the consensus estimate of 212,000. The US labour market has been showing signs of softening as the Federal Reserve’s rate hikes continue to filter through the economy and dampen economic growth.

The markets are always interested in what Fed members have to say, hoping for some insights into Fed rate policy. A host of FOMC members will deliver remarks today, highlighted by a speech from Fed Chair Powell at an event in New York City. Today’s lineup has added significance as the Fed will enter a blackout period ahead of the meeting on November 1st. The sharp rise in US Treasuries has led to some Fed members saying that inflation could fall without further hikes, and investors will be watching to see if that dovish message is repeated today by Powell and his colleagues.

GBP/USD Technical

- There is resistance at 1.2163 and 1.2202

- 1.2066 and 1.1987 and providing support

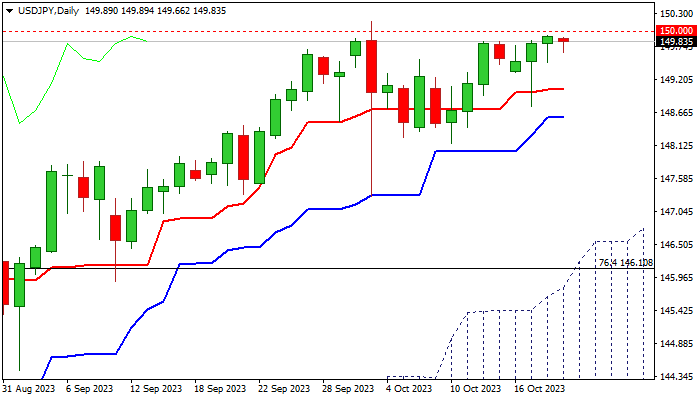

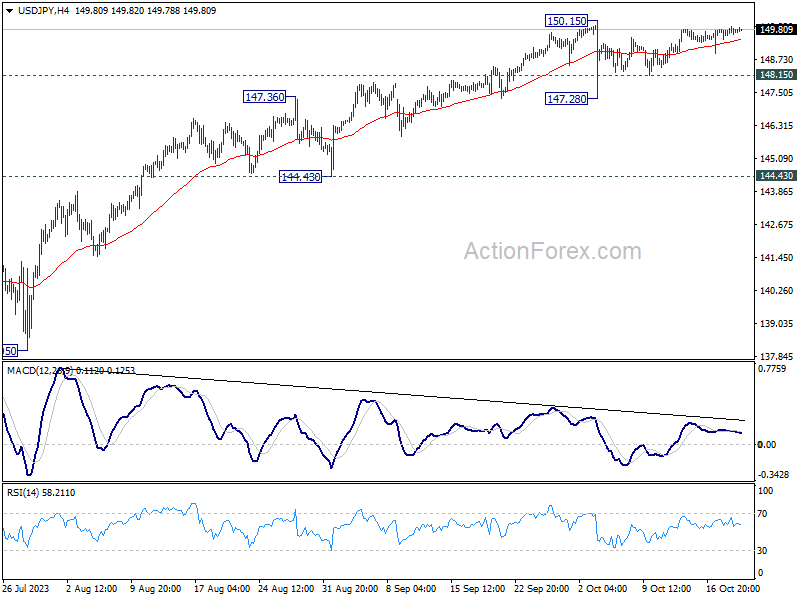

USD/JPY: Holds in a Narrow Range Directionless Mode and Seeks Direction Signals

USDJPY remains within a narrow range just below psychological 150 barrier, which was cracked earlier this month, but continues to offer solid resistance.

Near-term direction is clouded by mixed signals, as daily studies are in bullish configuration, but overbought and looming intervention keeps traders cautious.

Long tails of candlesticks of past two days point to strong bids, though the upside remains capped for now, while markets seek clearer direction signals.

Recent better than expected US retail sales and unexpected acceleration in job growth, counter expectations of economic slowdown due to high borrowing cost and add to uncertainty, ahead of coming Fed policy meeting on Nov 2.

Fed Chairman Powell, who will be speaking later today, along with other policymakers, still lacks the main information – whether inflation is on track to return to the central bank’s 2% target in estimated timeframe or not.

High uncertainty contributes to the Fed’s mixed view about the interest rates, after the policymakers decided to stay on hold in the last meeting, but left the door open for potential further tightening.

This keeps in play split expectations in which some see that the Fed is done with policy tightening, but others believe that battle with inflation is not over yet and expect more rate hikes, arguing expectations by the facts that economy is quite resilient despite high interest rates.

Geopolitics lately took the centre stage, as fresh conflict in the Middle East threatens to escalate and spill over, adding to growing uncertainty in already fragile situation.

Look for initial direction signals on break of break of Fridays’ spike low at 148.77 (bearish) or lift through 150.00/16 pivots (bullish).

Verification of negative signal would require sustained break of 148.16 (Oct 10 higher low) and confirmation on clear break below 147.29 (Oct 3 spike low).

Conversely, sustained break above 150.00/16 would signal that bulls are regaining traction for acceleration towards 151.94 (multi-decade high, posted on 21 Oct 2022).

Res: 150.00; 150.16; 150.82; 151.23.

Sup: 149.48; 148.77; 148.16; 147.29.

Sunset Market Commentary

Markets

“5% or not for yields across the entire scope of the US yield curve?”, that was the question for US bond markets today. Despite global (geopolitical and economic) uncertainty, there is still no safe haven run on US Treasuries. The wings (2-y 5.25% and 30-y 5.05%) already surpassed the 5% psychological barrier. A speech of Fed Chair Powell scheduled after finishing this report complicates an ‘unchained’ market reaction. US yields traded 3-5 bps higher in the run-up to the US data. The October Philly Fed index improved slightly less than expected from -13.5 to -9. However, especially subindices on current situation confirmed the picture of a resilient economy. US weekly jobless claims unexpectedly dropped below the 200k barrier (198k, lowest since January). Admittedly, these are not the most important data. Still it was a bit strange to see yields easing slightly post the release. Let’s call it Powell’s shadow. US yields currently add between 0.5 bps (2-y) and 3 bps (5-30-y). We assume Fed Chair Powell to join the assessment of the majority of Fed speakers of late. Vice Chair Jefferson and others indicated that the Fed could continue a wait-and-see approach at the November meeting. The US economy (domestic demand and the labour market in particular) remains stronger than what is needed to bring supply and demand to a balance that will allow inflation to return to target in a sustainable way. Inflation also remains sticky with higher oil prices posing additional upside risks. Still, it is likely that Powell will join his lieutenant indicating that recent rise in yields has done part of the Fed job’s, buying them time to make a new in depth assessment when new forecasts are available at the December meeting. Looking at recent price action, it’s far from sure such a ‘benign neglect’ attitude will trigger a U-turn in the ascent in LT yields. To be continued. In a session devoid of important news on this side of the Atlantic, changes in German yields currently are less than 1 bp. After a poor start, Eurostoxx 50 trades with a small loss (-0.2%) US indices opened marginally stronger. (Brent) oil stabilizes near $91/b.

A bit in lockstep with US Treasuries, the dollar still fails to fully play its safe haven role in times of uncertainty. DXY eases slightly to 106.30 in a technically insignificant move. Idem for EUR/USD. The pair (1.0575) reversed yesterday’s decline but first resistance at 1.064 stays out of reach. USD/JPY is still paralyzed in a tight range close to, just below 150. Interesting price action in sterling. Trying to overcome the EUR/GBP 0.8706 range top, the UK currency touched the weakest level against the euro since end May. Markets aren’t convinced at all that higher than expected September inflation will cause the BoE to resume its anti-inflation campaign at the November meeting after taking a pause (at 5.25%) last month. UK retail data to be published tomorrow might decide on the EUR/GBP break.

News & Views

Polish president Duda will meet with parliamentary leaders next week Tuesday and Wednesday following the elections of last weekend, his office communicated today. Poland and its watchers are keen to know who Duda will appoint first to form the country’s next government. Before the election outcome he said he’ll give the first shot to the party securing the most votes, which is the PiS. However, a united opposition led by former PM Tusk secured the majority of the votes, effectively preventing PiS from ruling another term. The leaders of the three parties seeking to form a coalition urged Duda to hand over the initiative to them straight away to quicken the process. But it’s unlikely the president (a PiS member himself) will adhere to the call, even as it could prove critical in the tight timeframe to unlock €8bn in European Recovery and Resilience Facility funds that are blocked for this year.

A leading, non-partisan UK think tank, Resolution Foundation, said a future British government should consider raising the Bank of England’s inflation target from 2% to 3%. Doing so would allow for higher nominal rates, offering the central bank more room to cut rates in a downturn. Combined with willingness to cut as deep as -1%, it reduces the need for government borrowing and bond-buying in times of crisis, research director and former BoE-economist James Smith explained. Resolution Foundation stressed that the change should only take place when the BoE returned to its current 2% goal to avoid tarnishing its credibility. And in an ideal situation it happens in coordination with other advanced economies to limit the fallout of higher inflation on sterling. But if that’s impossible, a weaker currency is a price worth paying, it concluded. UK inflation in September eased less than expected, to 6.7% and 6.1% for the headline and core gauge respectively.

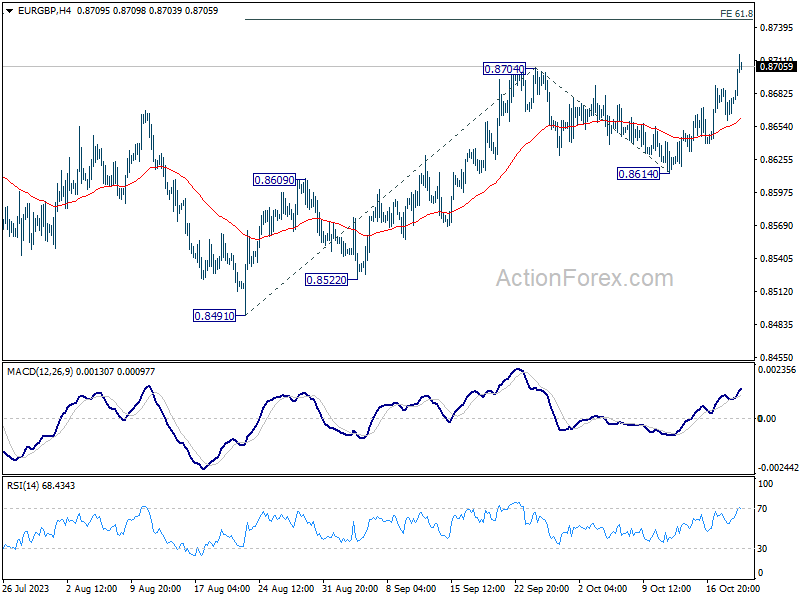

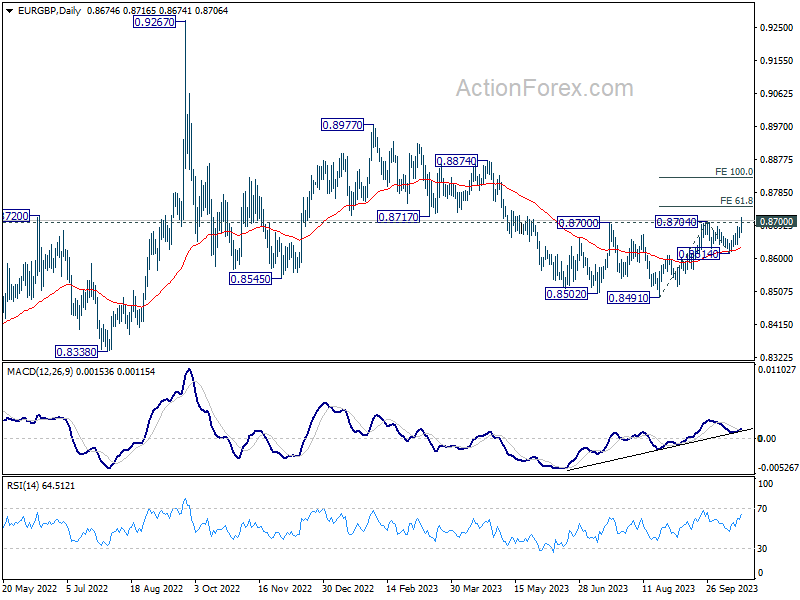

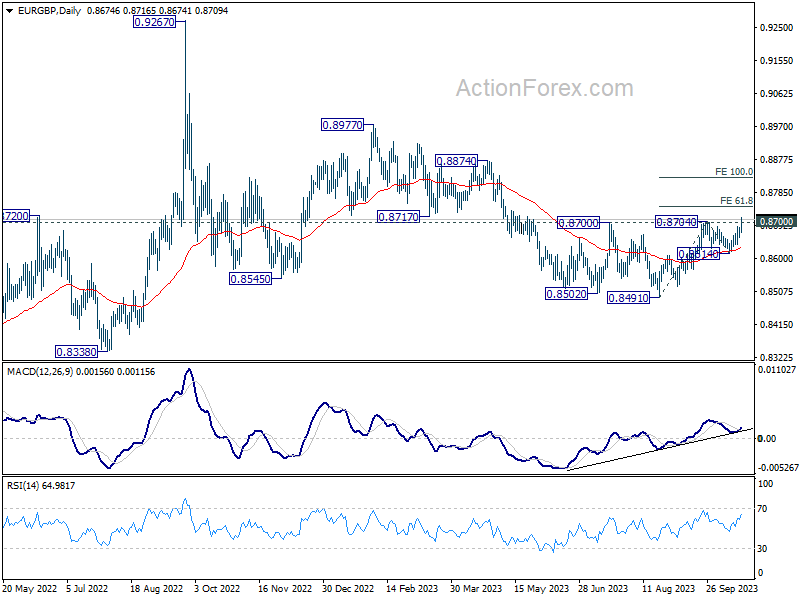

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8664; (P) 0.8676; (R1) 0.8692; More....

EUR/GBP's break of 0.8704 resistance confirms resumption of rise from 0.8491. The development also carries larger bullish implications. Intraday bias is back on the upside for 61.8% projection of 0.8491 to 0.8704 from 0.8614 at 0.8746. Decisive break there could prompt upside acceleration to 100% projection at 0.8827 next. For now, outlook will stay bullish as long as 0.8614 support holds, in case of retreat.

In the bigger picture, current development suggests that whole down trend from 0.9267 (2022 high) has completed with three down to to 0.8491. Rise from 0.8491 is seen as another leg inside that pattern from 0.9499 (2020 high). Further rally should be seen to 0.8977 resistance and above. This will now remain the favored case as long as 0.8614 support holds.

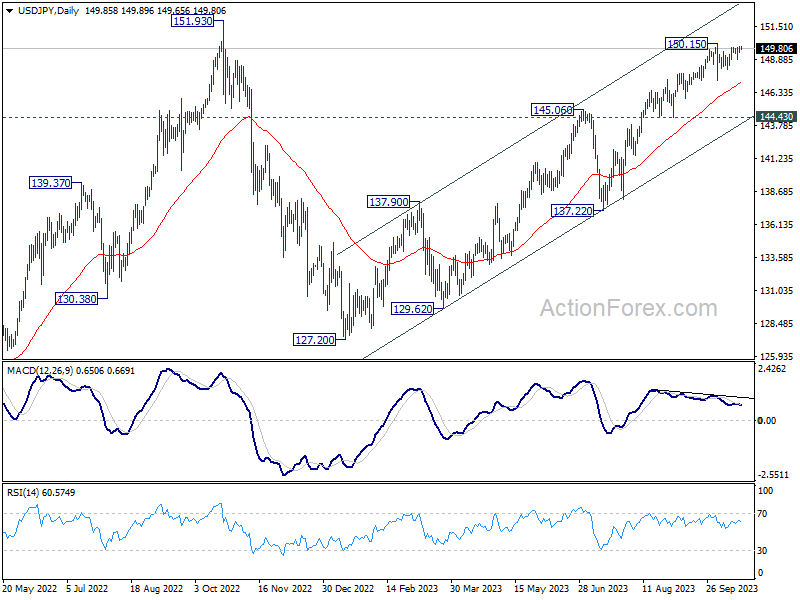

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.63; (P) 149.79; (R1) 150.08; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

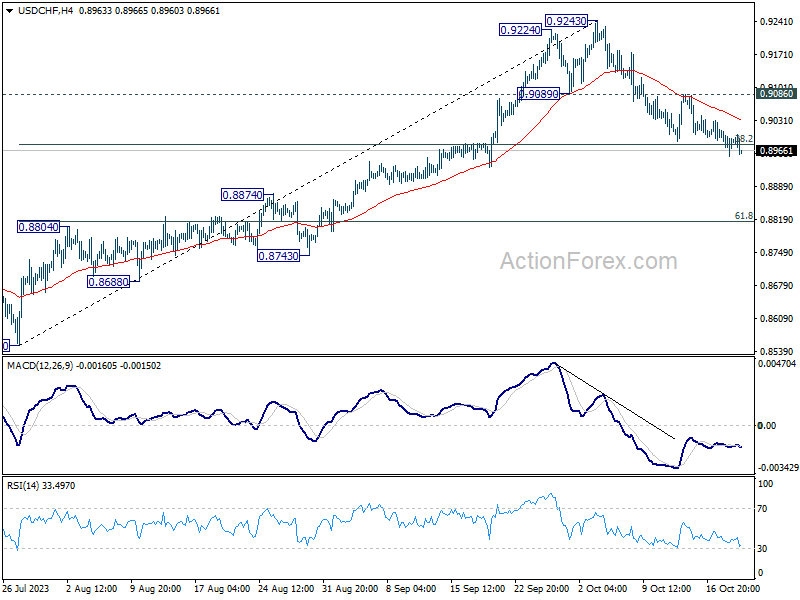

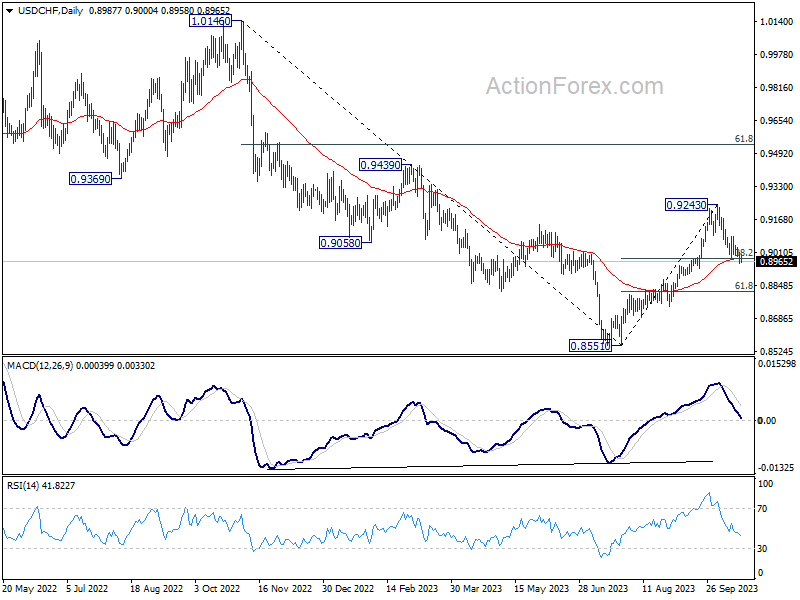

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8958; (P) 0.8987; (R1) 0.9021; More....

No change in USD/CHF's outlook as focus stays on 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Sustained break there will extend the fall from 0.9243 to 61.8% retracement at 0.8815. That would also carry larger bearish implications. On the upside, however, break of 0.9086 resistance will indicate that pull back from 0.9243 has completed, and turn bias to the upside for retesting this high.

In the bigger picture, as long as 55 D EMA (now at 0.8976) holds rise from 0.8551 is viewed as reversing whole down trend from 1.0146 (2022 high). On resumption, further rise should be seen to 61.8% retracement of 1.0146 to 0.8551 at 0.9537 and above. However, sustained break of 55 D EMA will revive medium term bearishness, for retesting 0.8551 low at a later stage.

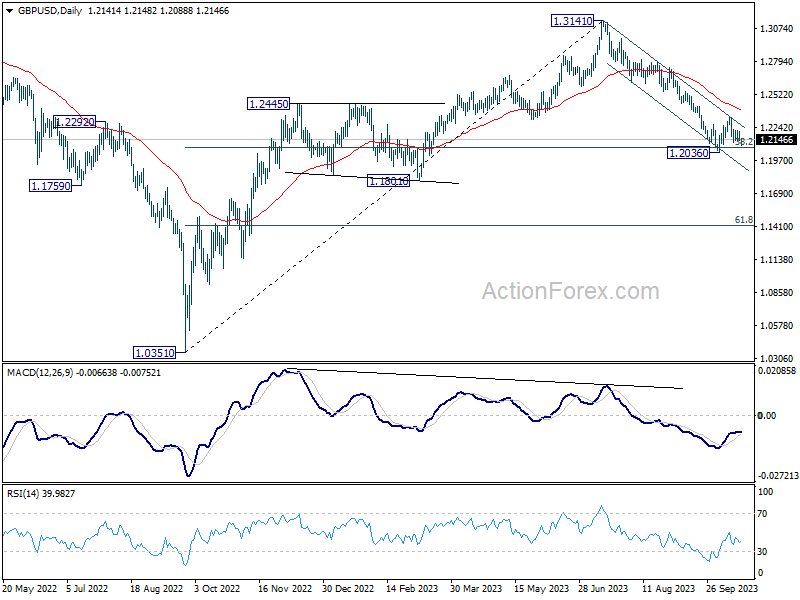

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2115; (P) 1.2163; (R1) 1.2189; More

Intraday bias in GBP/USD remains neutral for the moment. Consolidation from 1.2026 is still extending, and outlook stays bearish with 1.2336 resistance intact. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will resume the rebound from 1.2036 to 55 D EMA (now at 1.2383).

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2383) holds, in case of rebound.

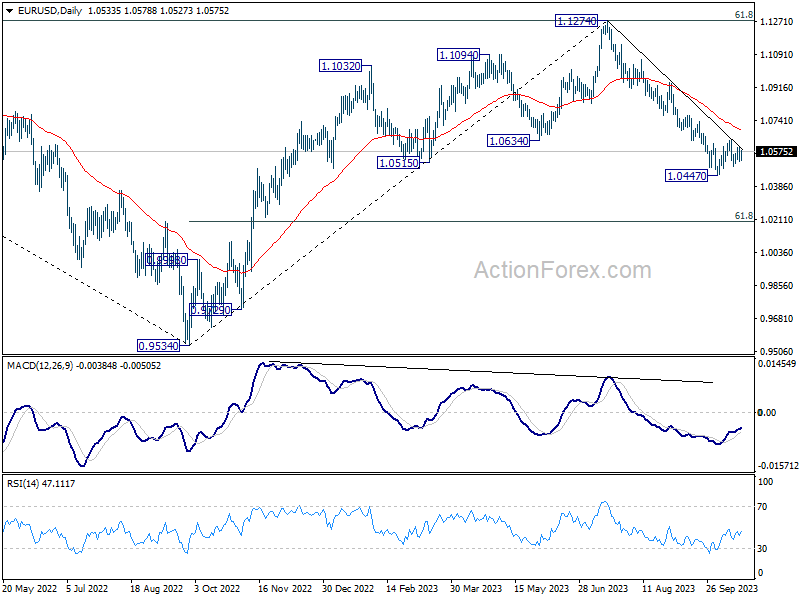

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0508; (P) 1.0551; (R1) 1.0579; More...

EUR/USD is still extending sideway trading between 1.0447 and 1.0639 and intraday bias stays neutral. Near term outlook stays bearish with 1.0639 resistance intact. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0692).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0692) holds, in case of rebound.

US 10-yr Yield Marches Towards 5%, But Dollar Fails to Match the Tempo

The global markets today are abuzz with the rapid rise of US benchmark treasury yields. Market pundits are keeping a keen eye on 10-year yield, which, given its present momentum, is poised to touch 5% level. All eyes will also be on how traders react at this critical psychological level. Simultaneously, anticipation is building around Fed Chair Jerome Powell's forthcoming speech at the Economic Club of New York. It's widely expected that he will reiterate the stance on maintaining "higher for longer" interest rates in response to inflationary pressures. However, it's crucial to understand that this ascent in yields isn't restricted to the US alone. Germany's 10-year yield has climbed to levels not seen since 2011, while Japan's 10-year JGB yield has touched its highest point since 2013.

In the realm of currency markets, Australian Dollar and New Zealand Dollar are bearing the brunt of market shifts, emerging as the day's weakest performers. While disappointing employment figures are an added burden for Aussie, Kiwi remains under the shadow of yesterday's CPI revelations. British Pound is also under duress, particularly against Euro and Swiss Franc, placing it as the day's third weakest currency. On the other end of the spectrum, Yen, Franc, and Euro are vying for the top positions, with Dollar lagging slightly behind, struggling to keep up the pace with 10-year yield.

Technically, EUR/GBP's break of 0.8700/4 resistance zone confirms resumption of rise from 0.8491. More importantly, the development suggest strengthens the case that corrective pattern from 0.9267 has completed with three waves down to 0.8941. Next near term target is 61.8% projection of 0.8419 to 0.8704 from 0.8614 at 0.8746. Decisive break there could prompt upside acceleration to 100% projection at 0.8827 next. A major question is whether this rally in EUR/GBP can inject vitality into EUR/USD, propelling it beyond 1.0639 resistance and heralding a stronger rebound.

In Europe, at the time of writing, FTSE is down -1.00%. DAX is down -0.19%. CAC is down -0.60%. Germany 10-year yield is down -0.008 at 2.922. Earlier in Asia, Nikkei fell -1.91%. Hong Kong HSI fell -2.46%. China Shanghai SSE fell -1.74%. Singapore Strait Times fell -1.18%. Japan 10-year JGB yield rose 0.0391 to 0.847.

US initial jobless claims fell to 198k, vs exp 210k

US initial jobless claims fell -13k to 198k in the week ending October 14, below expectation of 210k. Four-week moving average of initial claims dropped -1k to 206k.

Continuing claims rose 29k to 1743k in the week ending October 7. Four-week moving average of continuing claims rose 19k to 1694k.

BoJ's regional economic report unveils broadest upgrade since mid 2022

In the Regional Economic Report released today, BoJ upgraded the economic assessment for six regions, marking the most substantial uplift since July 2022. The regions experiencing this optimistic revision include Hokkaido, Tohoku, Hokuriku, Kanto-Koshinetsu, Chugoku, and Shikoku. Conversely, the economic outlook for Tokai, Kinki, and Kyushu-Okinawa remained steady.

This comprehensive upgrade underscores the resilience and adaptability of the Japanese economy. Despite the headwinds presented by decelerating recovery in overseas economies and rising prices domestically, all nine regions delineated a narrative of an economy that is either picking up momentum or recovering at a moderate pace.

On a related note, a separate report from branch managers indicated that many companies, due to a structural labor shortage, are gearing up to continue wage increments in the upcoming fiscal year. However, the magnitude of these wage hikes will largely depend on competitor trends and upcoming price movements, especially as the spring labor unions of next year approach.

Japan's export rose 4.3% yoy in Sep amid US and European demand

Japan saw a welcomed increase in exports in September, breaking a two-month declining trend and outpacing forecasts. Exports rose by 4.3% yoy to JPY 9198B, surpassing the anticipated growth of 3.1% yoy.

A closer examination of the trade partners reveals a contrasting scenario. Exports to China, Japan's prominent trading partner, dipped by -6.2% yoy, marking the tenth consecutive month of decline. A staggering -58% yoy drop in food shipments contributed significantly to this contraction. Conversely, trade ties with US and Europe exhibited robustness, with exports expanding by 13.0% yoy and 12.9% yoy respectively.

On the import front, Japan reported a decline of -16.3% yoy to JPY 9136B, a steeper fall than the anticipated -12.9% yoy. Trade dynamics shifted, with Japan posting a trade surplus of JPY 62.4B.

When assessed in seasonally adjusted terms, exports went up by 7.2% mom to JPY 8910B, while imports climbed by 5.4% mom, reaching JPY 9345B. Consequently, trade deficit was reduced to JPY -434B.

Australia employment grows a mere 6.7%, unemployment rate ticks down

Australia's job market portrayed a mixed picture in September, with a significant undershoot in employment growth countered by a lower-than-expected unemployment rate.

The country added a mere 6.7k jobs in the month, a far cry from the anticipated 20.3k. Delving deeper into the data, full-time employment took a hit, shrinking by -39.9k. However, this was partly offset by increase in part-time roles, which swelled by 46.5k.

Unemployment rate showed slight improvement, ticking down to 3.6% from previous 3.7%, despite expectations that it would remain steady. Yet, this decline could be attributed to a drop in participation rate, which receded from 67.0% to 66.7%. Meanwhile, total monthly hours worked contracted by -0.4% mom, equivalent to a reduction of 8 million hours.

Kate Lamb, ABS's head of labour statistics, highlighted that, when considering the last two months, the average monthly employment growth stood at 35k, in line with the yearly average growth. However, Lamb also drew attention to the declining unemployment rate in September, indicating it primarily resulted from a shift of people from the unemployed category to being outside the labor force altogether.

Furthermore, she noted, "The recent softening in hours worked, relative to employment growth, may suggest an easing in labour market strength."

Australia's business confidence shows uptick, but inflationary concerns persist

Australian businesses are displaying signs of renewed optimism, as revealed by NAB Quarterly Business Confidence index for Q3. The index improved, moving up from -4 in the second quarter to -1 in the third. Moreover, the gauge for Current Business Conditions also indicated better sentiment, rising from 11 to 13.

However, an undercurrent of concern persisted regarding cost dynamics. Labour cost growth experienced an increase, shifting up to 1.8% from the 1.3% witnessed in Q2. On the other hand, purchase costs growth showed a modest climb, reaching 1.4% from the 1.3% seen in the previous quarter. In a positive sign, fewer businesses highlighted materials as a limiting factor, with the percentage dropping to 32% from the 36% reported in Q2.

NAB's Chief Economist Alan Oster noted, "Price growth remained elevated in Q3. This is in line with our expectation for a reasonably strong inflation print of 1.1% for the quarter when the full Q3 CPI is released next week."

However, he tempered the immediate inflationary concerns with a longer-term view, adding, "Still, we do expect inflation to moderate gradually as the economy slows."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0508; (P) 1.0551; (R1) 1.0579; More...

EUR/USD is still extending sideway trading between 1.0447 and 1.0639 and intraday bias stays neutral. Near term outlook stays bearish with 1.0639 resistance intact. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0692).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0692) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.43T | -0.50T | -0.56T | -0.55T |

| 00:30 | AUD | NAB Business Confidence Q3 | -1 | -3 | -4 | |

| 00:30 | AUD | Employment Change Sep | 6.7K | 20.3K | 64.9K | 63.3K |

| 00:30 | AUD | Unemployment Rate Sep | 3.60% | 3.70% | 3.70% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 6.32B | 3.77B | 4.05B | 3.81B |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 27.7B | 20.9B | 21.0B | |

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.40% | 0.30% | 1.30% | |

| 12:30 | CAD | Raw Material Price Index Sep | 3.50% | 1.80% | 3.00% | |

| 12:30 | USD | Initial Jobless Claims (Oct 13) | 198K | 210K | 209K | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | -9 | -6.5 | -13.5 | |

| 14:00 | USD | Existing Home Sales Sep | 3.90M | 4.04M | ||

| 14:30 | USD | Natural Gas Storage | 82B | 84B |

US initial jobless claims fell to 198k, vs exp 210k

US initial jobless claims fell -13k to 198k in the week ending October 14, below expectation of 210k. Four-week moving average of initial claims dropped -1k to 206k.

Continuing claims rose 29k to 1743k in the week ending October 7. Four-week moving average of continuing claims rose 19k to 1694k.