Sample Category Title

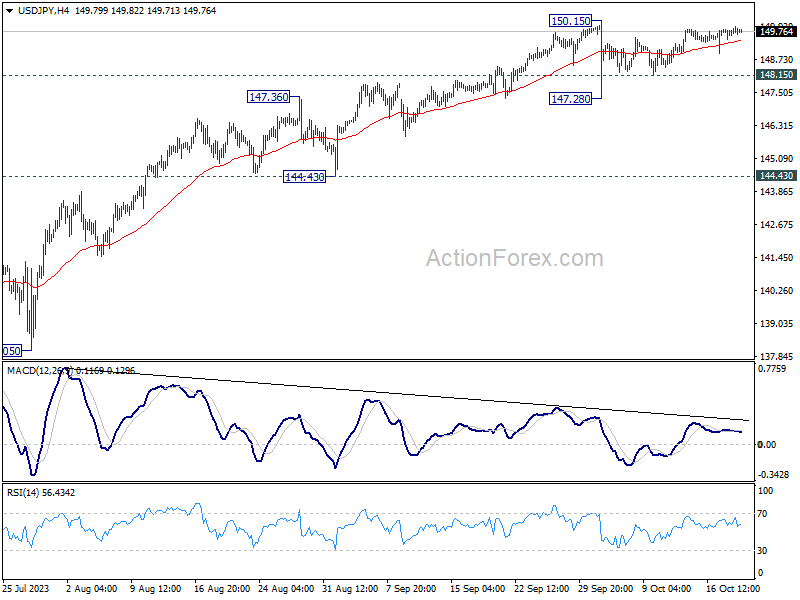

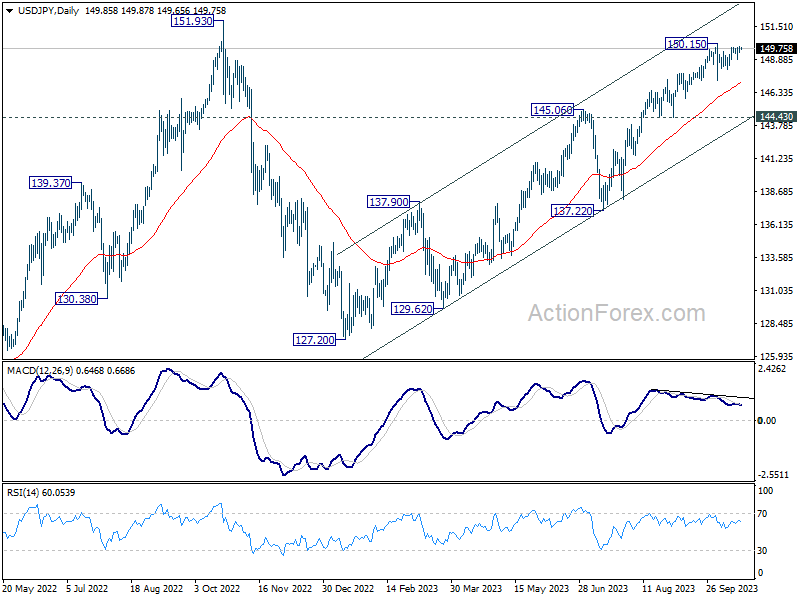

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.63; (P) 149.79; (R1) 150.08; More...

Intraday bias in USD/JPY remains neutral and range trading is still in progress. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

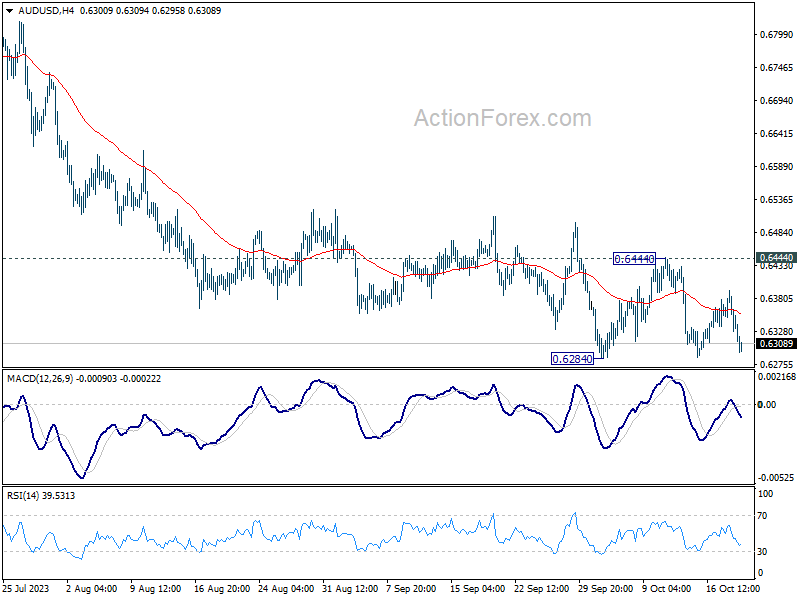

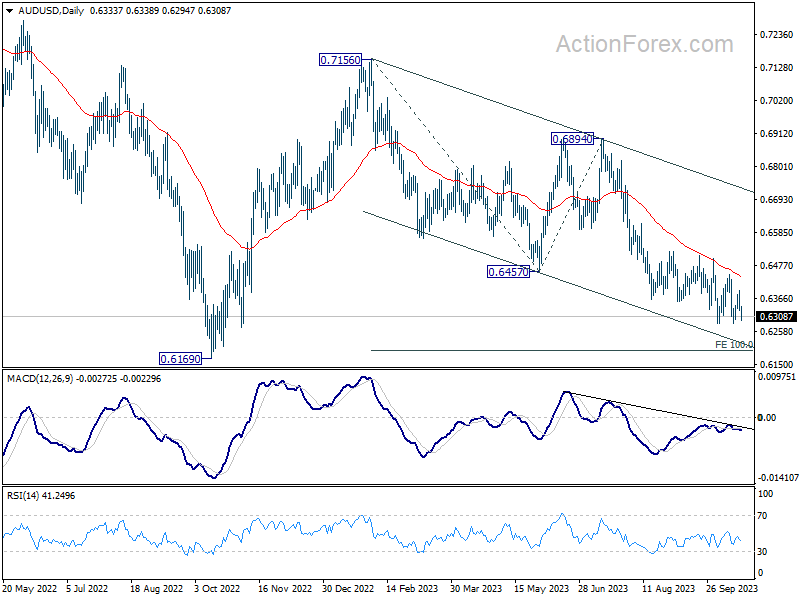

AUD/USD Daily Report

Daily Pivots: (S1) 0.6312; (P) 0.6352; (R1) 0.6377; More...

Intraday bias in AUD/USD stays neutral for the moment, and outlook remains bearish with 0.6444 resistance intact. On the downside, decisive break of 0.6284 will confirm resumption of whole decline from 0.7156. Next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support. Nevertheless, firm break of 0.6444 will confirm short term bottoming, and turn bias to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

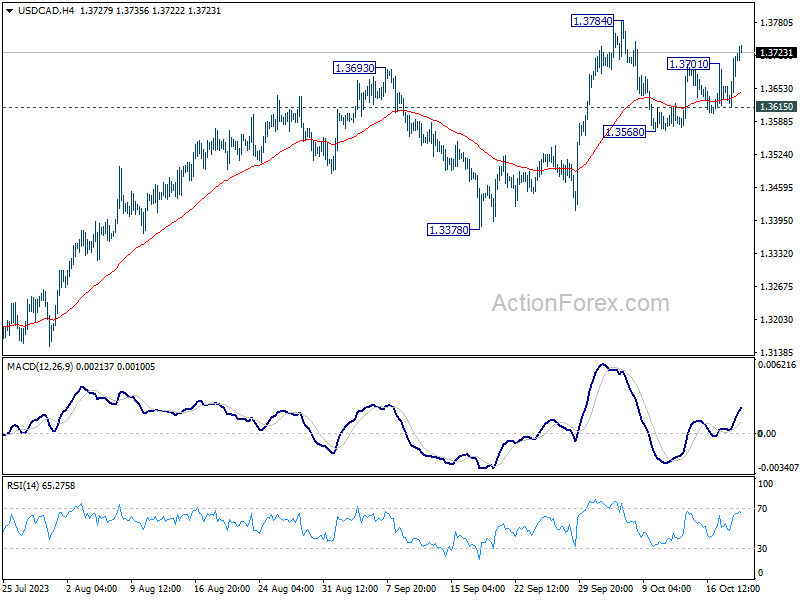

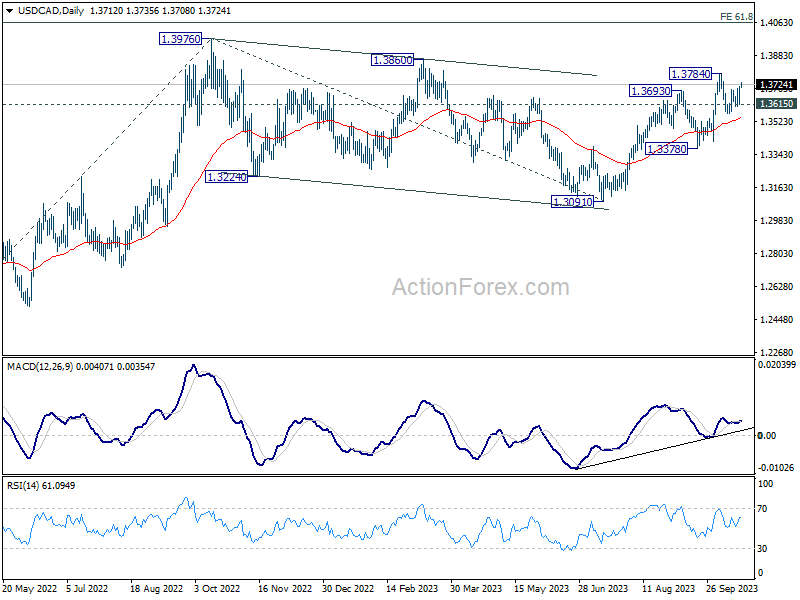

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3649; (P) 1.3684; (R1) 1.3750; More....

USD/CAD's rebound from 1.3568 resumed by breaking 1.3701 and intraday bias is back on the upside. Retest of 1.3784 resistance should be seen next. Break there will resume larger rise from 1.3091 to retest 1.3976 high. On the downside, however, break of 1.3615 support will bring another falling leg to extend the near term corrective pattern from 1.3784.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

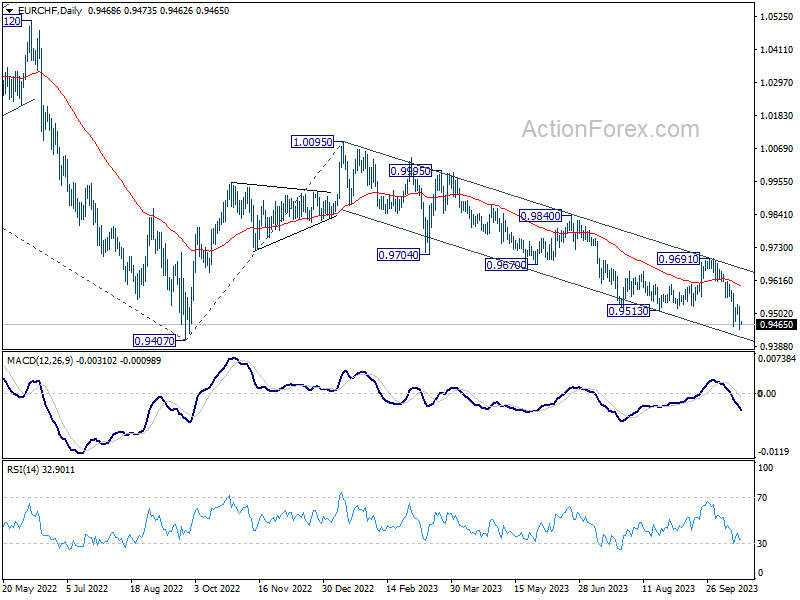

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9439; (P) 0.9483; (R1) 0.9518; More...

EUR/CHF's breach of 0.9455 indicates resumption of larger decline. Intraday bias is back on the downside. Current fall from 1.0095 should target 0.9407 medium term bottom. Nevertheless, break of 0.9532 resistance will indicate short term bottoming and bring stronger rebound.

In the bigger picture, medium term outlook remains bearish with the cross capped well below falling 55 W EMA (now at 0.9782). Firm break of 0.9407 (2022 low) will confirm resumption of larger down trend from 1.2004 (2018 high). Next target will be 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish.

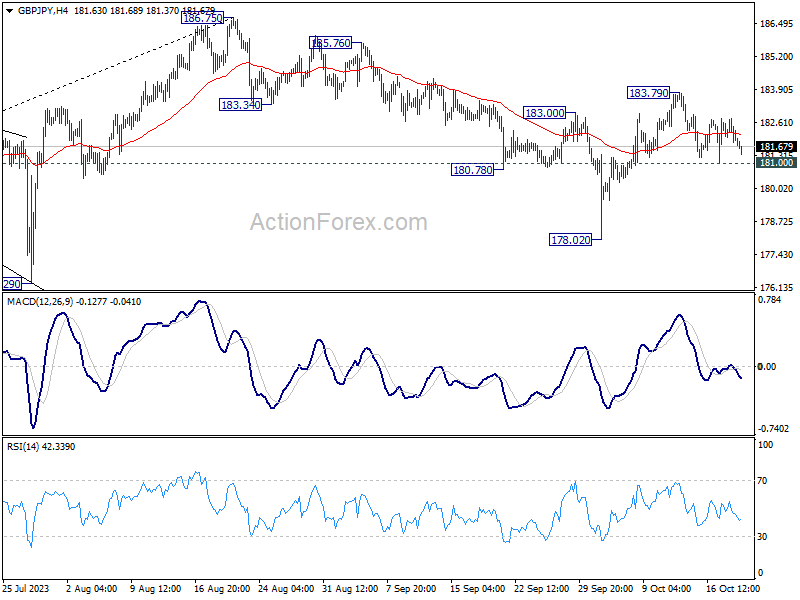

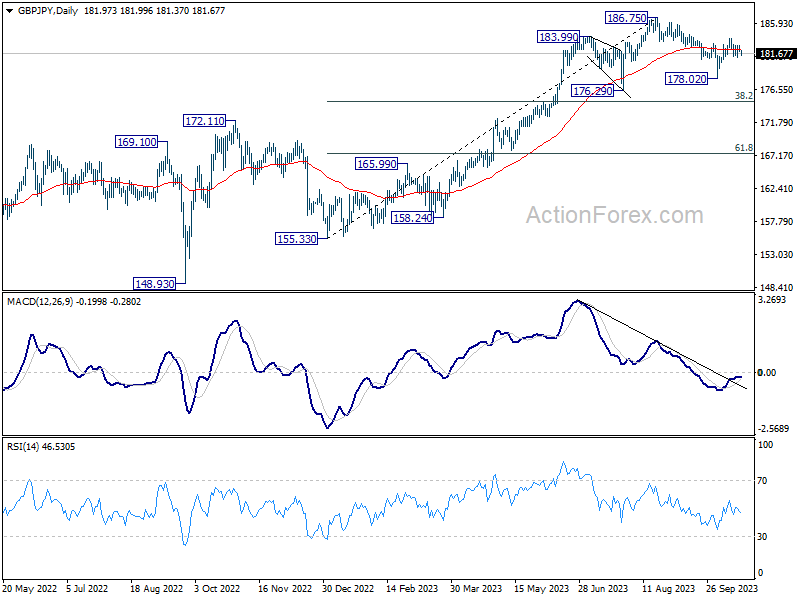

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.65; (P) 182.23; (R1) 182.61; More...

Intraday bias in GBP/JPY remains neutral for the moment. The favored case is still that correction from 186.75 has completed at 178.02. Above 183.79 will resume the rise from 178.02 to retest 186.75 high. However, break of 181.00 will dampen this view, and turn bias back to the downside for 178.02 instead.

In the bigger picture, fall from 186.75 is seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

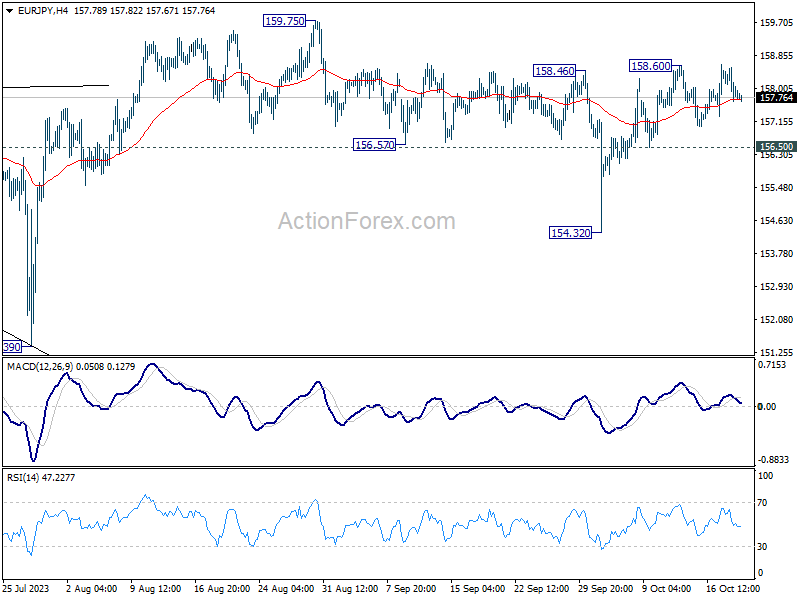

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.59; (P) 158.07; (R1) 158.45; More....

Intraday bias in EUR/JPY stays neutral for the moment. Outlook is also unchanged that correction from 159.75 should have completed at 154.32. Above 158.60 will resume the rise from 154.32 and target 159.75 high. However, break of 156.50 will dampen this view, and bring another fall to extend the corrective pattern from 159.75.

In the bigger picture, price actions from 159.75 are views as a corrective pattern. As long as 151.39 support holds, rise from 114.42 (2020 low) is expected to continue through 159.75 at a later stage. Nevertheless, firm break of 151.39 will confirm medium term topping, and bring lengthier and deeper correction.

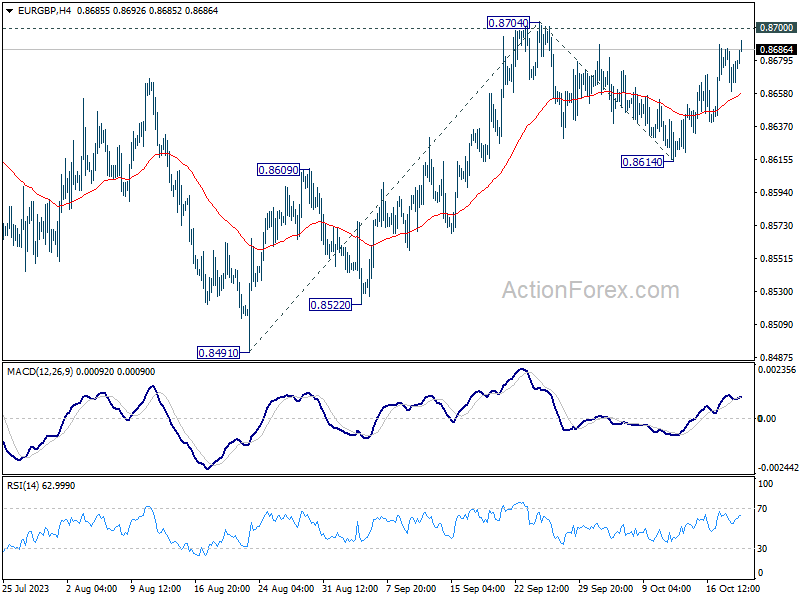

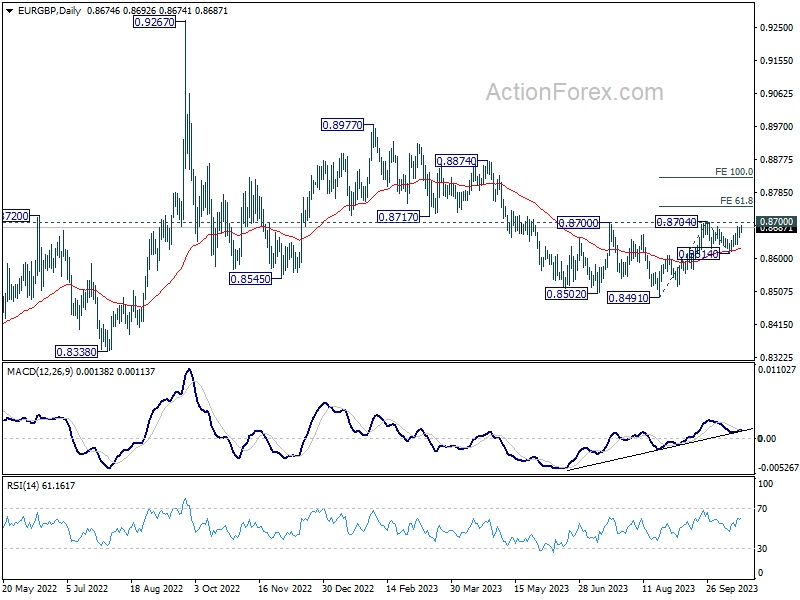

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8664; (P) 0.8676; (R1) 0.8692; More....

Intraday bias in EUR/GBP stays neutral for the moment. On the upside, decisive break of 0.8700/4 resistance will resume the rebound from 0.8491, and carry larger bullish implications. Nevertheless, break of 0.8614 will turn bias to the downside to extend the corrective pattern from 0.8704 with another leg.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

Risk Sentiment Remains Sour

Market movers today

A quiet day on the data front, with only US Philadelphia manufacturing index and weekly jobless claims due for release.

Fed chair Powell will discuss economic outlook at the Economic Club of New York this evening at 18:00 CET. With the FOMC's blackout period starting on Saturday, this will be a key opportunity to guide the market ahead of the November meeting. That said, market is already well priced for the Fed to remain on hold while keeping the door open for a final hike in December or January.

Other Fed speakers on the wires today include Jefferson, Goolsbee, Barr and Bostic.

People's Bank of China will likely maintain Loan Prime Rates unchanged overnight in line with the unchanged medium-term lending facility rate earlier this week.

The 60 second overview

Israel-Gaza conflict: Joe Biden visited Israel yesterday, with one key focus area being ensuring humanitarian aid to civilians in Gaza. Biden also discussed the issue in a phone call with Egyptian president Abdel Fattah El-Sisi who agreed to allow around 20 trucks of daily aid into Gaza via the Rafah crossing, which is the sole non-Israeli entry and exit point to the area. Earlier this week, Biden administration was reported to be preparing a USD100bn supplemental funding package to cover aid to both Israel and Ukraine as well as several domestic US issues. However, while such package would likely pass the democratic-controlled Senate, the House of Representatives is still unable to vote on any new bills, as it has not been able to elect a new speaker after ousting Kevin McCarthy. The current nominee Jim Jordan was rejected for the second time in a vote last night. And even if a new speaker was found, it remains unclear if especially the more hardliner republicans (who Jordan represents) would support a package linking Israel support to additional funding for Ukraine, even if the former has fairly broad-based support across Congress.

Fedspeak: Overall, market sentiment remained sour yesterday, with equity markets falling, 10y UST yield soon approaching 5% and broad USD strengthening. The most recent Fed speakers, including Waller and Harker yesterday, have communicated that the Fed has room to continue monitoring effects of past tightening by extending the September pause into November. But markets still price in an additional 14bp of tightening for the December and January meetings. NY Fed's Williams commented that he is 'not convinced yet neutral rate has risen' which would suggest that monetary policy is already clearly restrictive. One area where the impact is very visible is the housing market, as the MBS index of new mortgage applications for purchase has declined to the lowest level since 1995 amid 30y mortgage rate hitting 8% yesterday. That said, most of the September hard macro data still managed to surprise to the upside, which we discussed yesterday in our latest US Labour Market Monitor, 18 October.

Equities: Risk-off resurfaced on Wednesday. S&P -1.3%, Stoxx 600 -1.1% and small cap Russell 2000 a full -2.1% lower, taking the indices lower for the week. The negative trigger was yields, rising to a new year-high. It was not a growth-to-value rotation though but a cyclical sell-off. Materials (also driven by weak Chinese housing data) sold off with Boliden and SSAB down 4-6%. Note that the sell-off came despite unchanged industrial metal prices. Industrials and consumer discretionary also underperforming, losing -2-3%. US futures are continuing lower this morning.

FI: The upward surprise in UK inflation data drove GILT yields markedly higher yesterday with contagion effects on global bond markets. The 10Y GILT yield ended the day 15bp higher, while the 10Y Bund yield rose 4bp. Curves bear steepened across markets. BTP-Bund spreads widened ahead of S&P reviewing Italy on Friday, probably partly reflecting some uncertainty on how the Meloni government's proposal of fiscal easing worth an estimated EUR24bn next year could affect the credit assessment.

FX: Higher US yields, eroding risk appetite and rebalancing needs hit smaller currencies such the SEK and NOK. EUR/SEK and EUR/NOK escaped the recent range on the topside while both USD/SEK and USD/NOK moved back above 11.00. EUR/USD was relatively stable yet with a slight favour of the USD leg. USD/JPY still has its eyes on 150. EUR/GBP fell after the high inflation numbers, GBP gains proved transitory. CHF benefits from its safe-haven status as EUR/CHF pushes toward ATLs.

Credit: Yesterday, the negative sentiment in equity markets drove credit spreads wider, iTraxx Xover was 10.2bp wider at 455.2bp while iTraxx Main was 2.2bp wider at 85.7bp. That said, the primary credit market was active but the amount of deal activity was observed as limited. In the Nordic space, H&M printed a EUR500m 8Y green bond at MS+150bs. The books were above EUR3bn and IPT was at MS+165-170bp, these conditions indicate healthy investor appetite for selected names despite an increase in volatility, higher rates and lower indices.

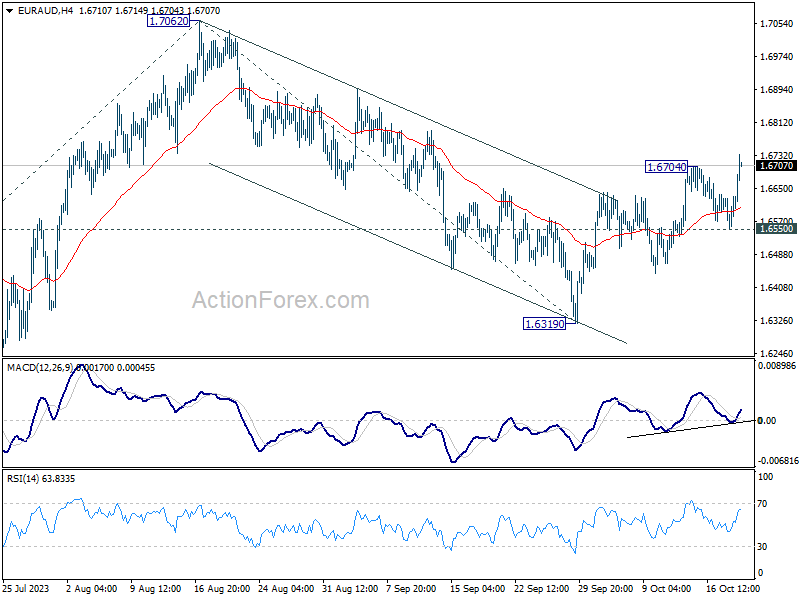

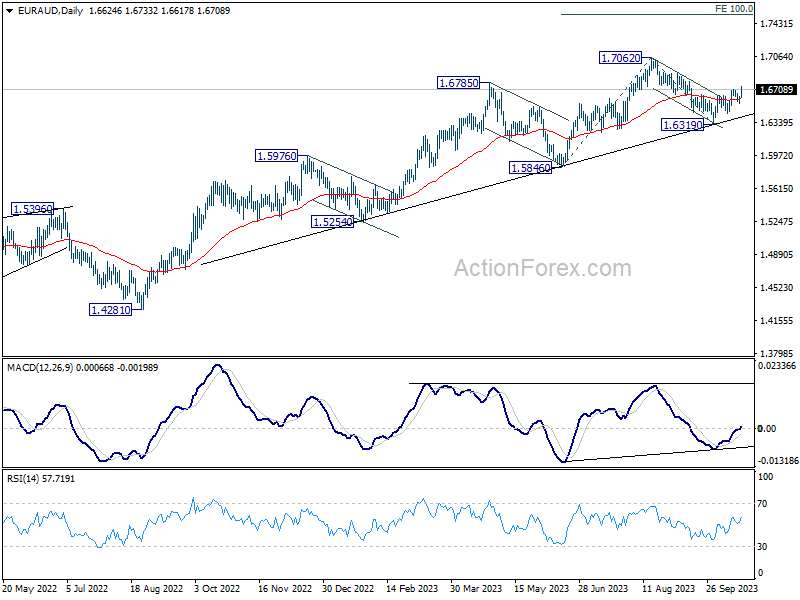

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6574; (P) 1.6609; (R1) 1.6663; More...

EUR/AUD's rally from 1.6319 resumed by taking out 1.6704 and intraday bias is back on the upside. Outlook is unchanged that correction from 1.7062 should have completed at 1.6319. Further rally is expected to retest 1.7062 high next. On the downside, however, break of 1.6550 support will dampen this view and turn bias back to the downside for 1.6319 instead.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. On resumption, next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. In any case, outlook will stay bullish as long as 1.6319 support holds.

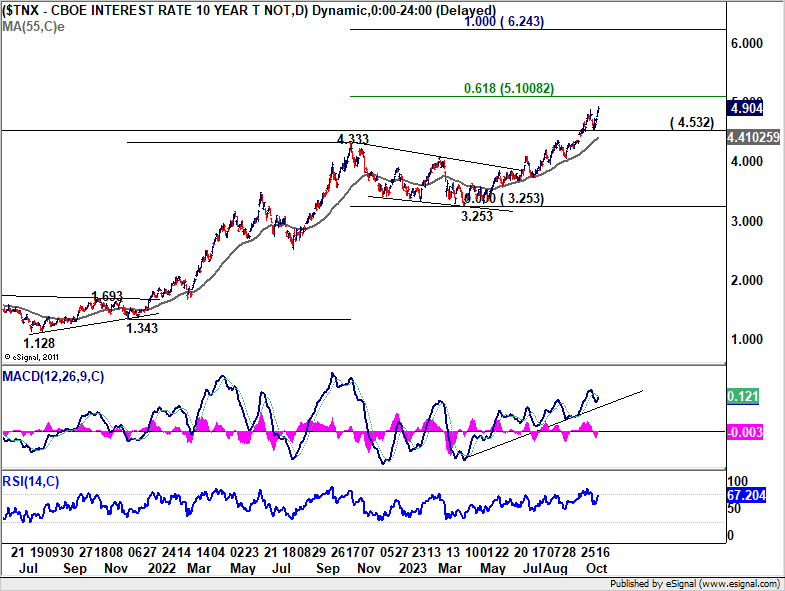

Treasury Yields Surge, Country Garden Wobbles, Global Markets on Guard

Financial markets are once again immersed in a phase of risk aversion, a sentiment spurred by the notable ascent of benchmark treasury yields. US 10-year yield is confidently moving closer to the 5% mark. Even Japan's 10-year JGB yield is hitting another decade high. The prevalent mood has propelled safe-haven currencies like Swiss Franc, Yen, and Dollar to be the standout performers of the day. In contrast, Aussie, Kiwi, and Loonie trail behind. Euro and Sterling find themselves in an intermediate position, though the former shows slight dominance.

All eyes are now turned to Fed Chair Jerome Powell's upcoming policy address to the Economic Club of New York. Anticipation is rife, with markets eager to glean insights into the potential for a further rate hike in the closing months of the year. However, expectations are tempered, with Powell likely to opt for a balanced approach, letting other FOMC members lead the discussion. Nonetheless, he is expected to reiterate the "higher for longer" narrative and underscoring the importance of data in shaping future policy decisions. The bond and stock markets' reaction to his address could play a pivotal role in steering Dollar's course.

In another significant development, Chinese property giant Country Garden is under scrutiny. Bondholders have reportedly sought urgent discussions following the company's failure to make a USD 15m coupon payment. This misstep puts the developer on the brink of default, thereby exacerbating the risk-averse mood permeating Asian markets.

From a technical perspective, 10-year yield resumed recent up trend by breaking through 4.887 resistance. Further rise is now expected to 61.8% projection of 1.343 to 4.333 from 3.253 at 5.100. Reaction from there would be crucial in driving overall risk sentiment. Sustained break of this 5.100 projection could spark steep selloff in stocks with contagion effects to push up Dollar. In any case, near term outlook in TNX will stay bullish as long as 4.532 support holds, in case of retreat.

In Asia, at the time of writing, Nikkei is down -1.68%. Hong Kong HSI is down -1.95%. China Shanghai SSE is down -1.21%. Singapore Strait Times is down -1.14%. 10-year JGB yield is up 0.033 at 0.841. Overnight, DOW dropped -0.98%. S&P 500 dropped -1.34%. NASDAQ dropped -1.62%. 10-year yield rose 0.057 to 4.904.

Japan's export rose 4.3% yoy in Sep amid US and European demand

Japan saw a welcomed increase in exports in September, breaking a two-month declining trend and outpacing forecasts. Exports rose by 4.3% yoy to JPY 9198B, surpassing the anticipated growth of 3.1% yoy.

A closer examination of the trade partners reveals a contrasting scenario. Exports to China, Japan's prominent trading partner, dipped by -6.2% yoy, marking the tenth consecutive month of decline. A staggering -58% yoy drop in food shipments contributed significantly to this contraction. Conversely, trade ties with US and Europe exhibited robustness, with exports expanding by 13.0% yoy and 12.9% yoy respectively.

On the import front, Japan reported a decline of -16.3% yoy to JPY 9136B, a steeper fall than the anticipated -12.9% yoy. Trade dynamics shifted, with Japan posting a trade surplus of JPY 62.4B.

When assessed in seasonally adjusted terms, exports went up by 7.2% mom to JPY 8910B, while imports climbed by 5.4% mom, reaching JPY 9345B. Consequently, trade deficit was reduced to JPY -434B.

Australia employment grows a mere 6.7%, unemployment rate ticks down

Australia's job market portrayed a mixed picture in September, with a significant undershoot in employment growth countered by a lower-than-expected unemployment rate.

The country added a mere 6.7k jobs in the month, a far cry from the anticipated 20.3k. Delving deeper into the data, full-time employment took a hit, shrinking by -39.9k. However, this was partly offset by increase in part-time roles, which swelled by 46.5k.

Unemployment rate showed slight improvement, ticking down to 3.6% from previous 3.7%, despite expectations that it would remain steady. Yet, this decline could be attributed to a drop in participation rate, which receded from 67.0% to 66.7%. Meanwhile, total monthly hours worked contracted by -0.4% mom, equivalent to a reduction of 8 million hours.

Kate Lamb, ABS's head of labour statistics, highlighted that, when considering the last two months, the average monthly employment growth stood at 35k, in line with the yearly average growth. However, Lamb also drew attention to the declining unemployment rate in September, indicating it primarily resulted from a shift of people from the unemployed category to being outside the labor force altogether.

Furthermore, she noted, "The recent softening in hours worked, relative to employment growth, may suggest an easing in labour market strength."

Australia's business confidence shows uptick, but inflationary concerns persist

Australian businesses are displaying signs of renewed optimism, as revealed by NAB Quarterly Business Confidence index for Q3. The index improved, moving up from -4 in the second quarter to -1 in the third. Moreover, the gauge for Current Business Conditions also indicated better sentiment, rising from 11 to 13.

However, an undercurrent of concern persisted regarding cost dynamics. Labour cost growth experienced an increase, shifting up to 1.8% from the 1.3% witnessed in Q2. On the other hand, purchase costs growth showed a modest climb, reaching 1.4% from the 1.3% seen in the previous quarter. In a positive sign, fewer businesses highlighted materials as a limiting factor, with the percentage dropping to 32% from the 36% reported in Q2.

NAB's Chief Economist Alan Oster noted, "Price growth remained elevated in Q3. This is in line with our expectation for a reasonably strong inflation print of 1.1% for the quarter when the full Q3 CPI is released next week."

However, he tempered the immediate inflationary concerns with a longer-term view, adding, "Still, we do expect inflation to moderate gradually as the economy slows."

Looking ahead

Swiss trade balance and Eurozone current account will be released in Euroepan session. Later in the day, US will publish jobless claims, Philly Fed survey and existing home sales. Canada will release IPPI and RMPI.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6574; (P) 1.6609; (R1) 1.6663; More...

EUR/AUD's rally from 1.6319 resumed by taking out 1.6704 and intraday bias is back on the upside. Outlook is unchanged that correction from 1.7062 should have completed at 1.6319. Further rally is expected to retest 1.7062 high next. On the downside, however, break of 1.6550 support will dampen this view and turn bias back to the downside for 1.6319 instead.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. On resumption, next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. In any case, outlook will stay bullish as long as 1.6319 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.43T | -0.50T | -0.56T | -0.55T |

| 00:30 | AUD | NAB Business Confidence Q3 | -1 | -3 | -4 | |

| 00:30 | AUD | Employment Change Sep | 6.7K | 20.3K | 64.9K | 63.3K |

| 00:30 | AUD | Unemployment Rate Sep | 3.60% | 3.70% | 3.70% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 3.77B | 4.05B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 20.9B | |||

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.30% | 1.30% | ||

| 12:30 | CAD | Raw Material Price Index Sep | 1.80% | 3.00% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 13) | 210K | 209K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | -6.5 | -13.5 | ||

| 14:00 | USD | Existing Home Sales Sep | 3.90M | 4.04M | ||

| 14:30 | USD | Natural Gas Storage | 82B | 84B |