Sample Category Title

Will Eurozone PMIs Corroborate Speculation of ECB Rate Cuts in 2024?

- Data since the last ECB meeting continue to point to a wounded Eurozone

- Investors see no more rate hikes and anticipate a series of cuts in 2024

- How will Tuesday’s preliminary PMIs (08:00 GMT) affect those bets and the euro?

Was ECB’s September hike the last one?

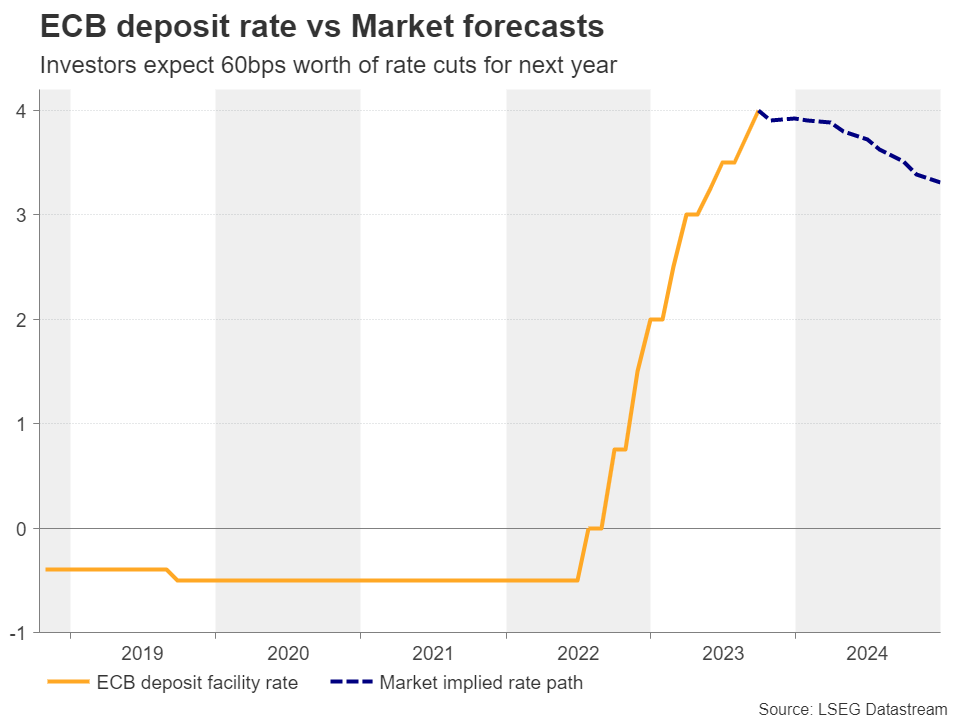

At its September meeting, the European Central Bank (ECB) decided to raise interest rates by another 25bps, lifting the deposit facility rate to a record high of 4%. Nonetheless, with data heading into the meeting pointing to profound cracks in the Euro area economy, officials hinted that this could be the last rate increase in this tightening cycle.

Thus, despite the delivery of a rate hike, the euro tumbled on the hints of that being the last one, and market participants began pricing in a series of rate cuts for 2024. Even after several policymakers, including President Lagarde, pushed against rate cut bets the following days, investors were not convinced.

Data and ECB rhetoric since then suggest so

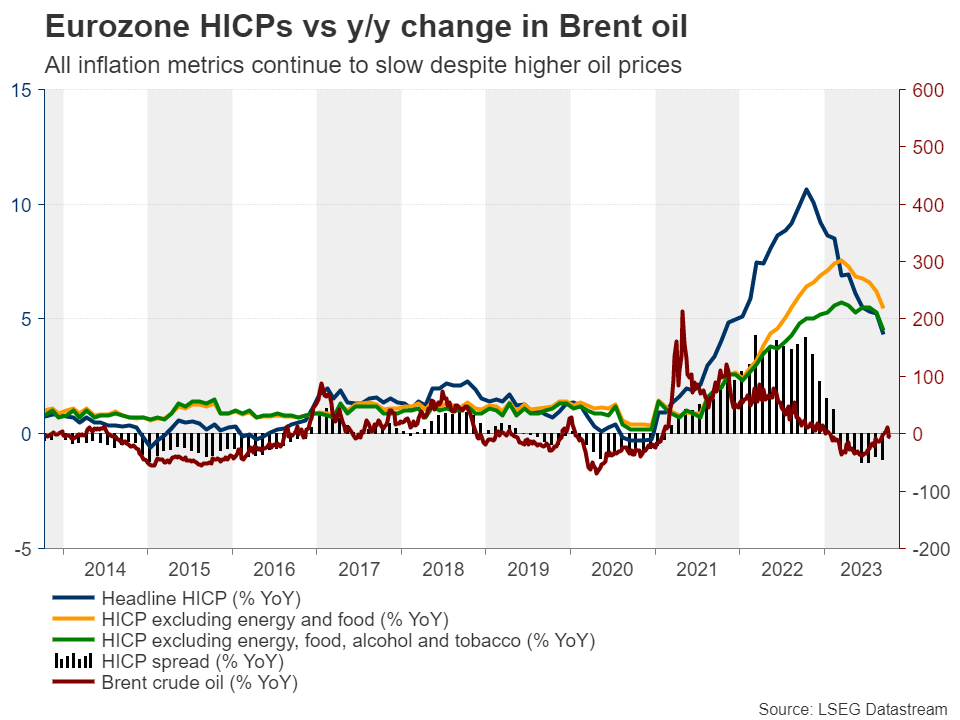

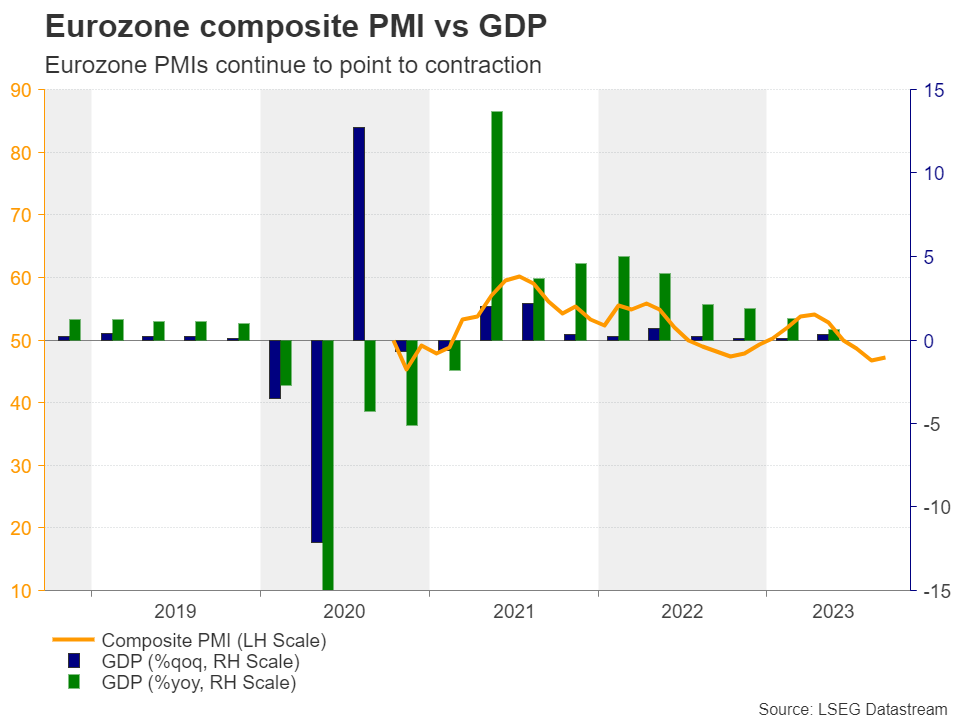

Since then, economic data has continued to point to an injured economy. Despite the improvement in the September PMIs, all indices remained below the 50 barrier that separates expansion from contraction, with the composite index rising only to 47.1 from 46.7.

Most importantly, the preliminary CPI numbers for last month showed that inflation slowed by more than expected, with the ultra-core rate that excludes energy, food, alcohol tobacco sliding to 4.5% y/y from 5.3%. Even the headline rate dropped to 4.3% y/y from 5.2%, despite the rally in oil prices during the month.

Although all the HICP rates are more than double the ECB’s objective of 2%, recent remarks by policymakers that inflation is on its way back to the target, even without more hikes, allowed market participants to assign a 95% probability for no action at next week’s gathering, with the remaining 5% pointing to one last 25bps increase. Even in December that probability does not rise much. It just goes to 12%, while for next year, investors are anticipating around 60bps worth of rate reductions, even though ECB officials have been arguing that for the inflation objective to be met, rates may need to be held steady.

Preliminary PMIs the next test for euro traders

It seems that market participants trust the economic data, which still points to a damaged economy. The conflict in the Middle East between Israel and Palestine could be also affecting their forecasts due to the extra uncertainty it poses to future economic performance. With that in mind, next week, euro traders may pay special attention to the preliminary PMIs for October, released on Tuesday ahead of Thursday’s ECB monetary policy decision.

Although some further improvement is unlikely to significantly raise the odds for another rate hike, it could well propel market participants to take more seriously the ‘steady for longer’ remarks by policymakers and thereby remove some of the basis points anticipated to be cut throughout 2024. On the other hand, numbers pointing to deepening wounds could add to recession fears and result in an even lower implied rate path.

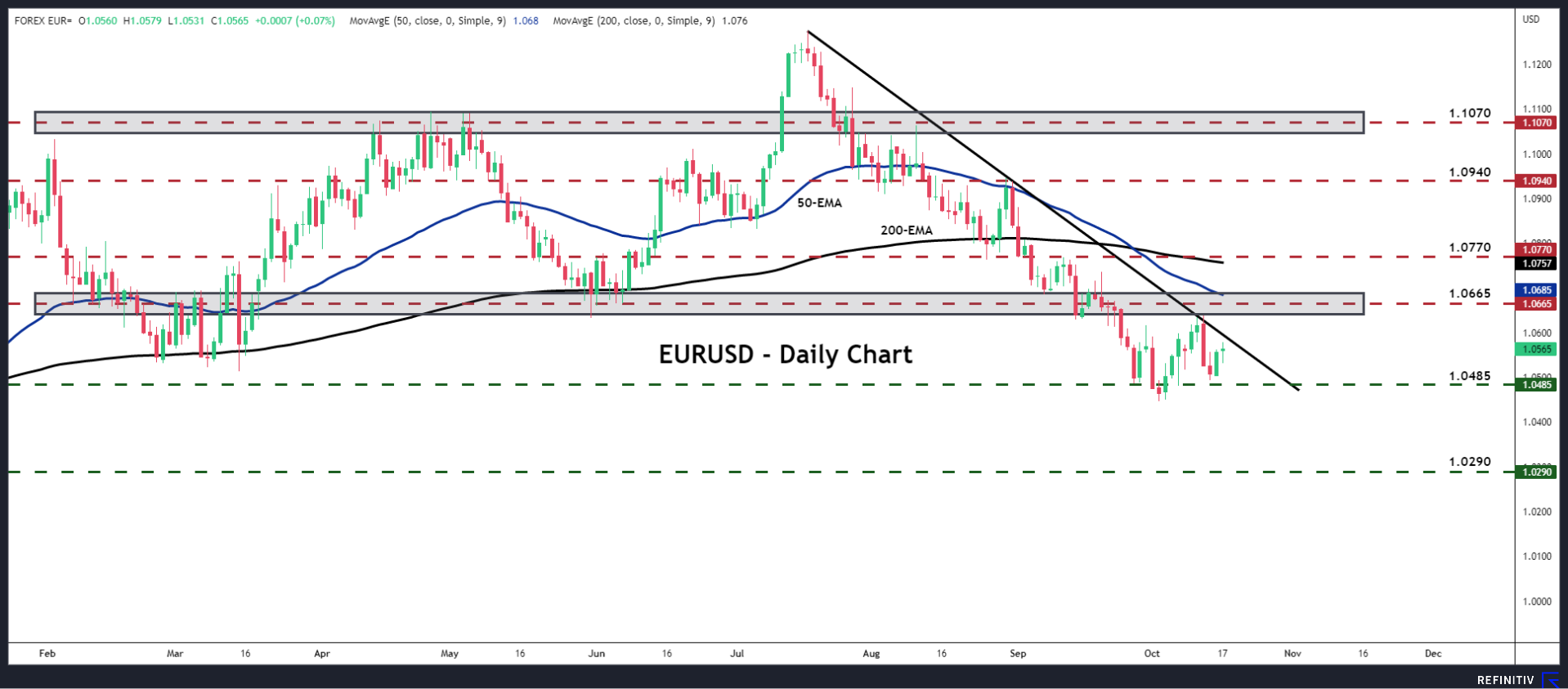

Euro/dollar continues to trade in a downtrend

As for the euro, it remains in a downtrend against its US counterpart, but due to some recent dovish remarks by Fed officials, who are also suggesting that they may have done raising rates, euro/dollar bears are finding it difficult to clearly breach the 1.0485 zone. That said, if economic data out of the Eurozone continues to disappoint, it may be a matter of time before that support barrier gives up and sets the stage for declines towards the 1.0290 zone, defined as support by the low of November 30, 2022.

Now, in the case of improving PMIs, euro/dollar could move higher, but as long as all three indices remain below 50, any recovery is likely to remain limited and short-lived below the downtrend line drawn from the high of July 18, or below the key resistance zone of 1.0665.

Sunset Market Commentary

Markets

Better than expected China Q3 growth data failed to inspire risk assets. US (real) yields nearing/touching cycle peak levels clearly dampened optimism. Geopolitical tensions also returned to the forefront as a meeting of US President Biden with Arab leaders was canceled after a deadly explosion at a hospital in Gaza. Uncertainty on upcoming developments in the conflict (and on diplomacy to prevent a further escalation) propelled Brent oil to the $93 p/b level (currently $92 p/b). A further rise in the oil price clearly serves as a ‘risk premium’ to the global economy at risk of both eroding already fragile growth and at the same time reinforcing price pressures. European equities are ceding between 0.5%-1.0%. US equities open up to 0.5% lower. As was often the case of late, even the combination of elevated geopolitical tensions and economic uncertainty still doesn’t trigger the usual safe haven run to core bonds. Even after yesterday’s sharp losses on stronger than expected US retail sales, bonds get little help from aggressive (safe haven) dip-buyers. Stronger than expected September US housing starts only help to put a floor for US yields. US yields currently trade between unchanged (2-y) and 5 bps higher (30-y). The 2-y yield continues testing yesterday’s multi-year close near 5.20%. Similar story for the 5-y (4.88%), 10-y (4.87%) and 30-y (4.98%). The former intraday briefly touched the highest level since July-2007. Fed’s Harker in an interview with the WSJ said he thinks the Fed can wait until early next year to assess whether previous hikes have done enough to bring inflation back under control. Question is whether he is expressing the majority view. European interest rate markets show a similar picture with the 2-y German yield ‘losing‘ 1 bp but the 30-y adding 4.0 bps. Moves in intra-EMU government bond spreads stay orderly. However, at 2.05%, the 10-y Italian spread against Germany is revisiting recent peak levels.

On FX markets, the dollar performance remains unconvincing. DXY gains marginally (106.30). EUR/USD (1.0555) is holding below the downtrend line since the August peak. USD/JPY is blocked close to just below the 150 barrier as investors ponder the chance of potential interventions. At the same time all kinds of rumours continue to swirl on the BOJ tweaking its ultra-easy policy in a not that distant future.

After a softer than expected (incomplete) UK labour market report, higher than expected UK September CPI (headline 0.5% M/M and 6.7% Y/Y (changed), core 6.1% Y/Y from 6.2%) reopened the debate on additional BoE tightening. While close to expectations, the report didn’t provide to faster disinflation the BoE is hoping for. Gilts underperform Treasuries and Bunds with UK yields rising between 7 bps (2-y) and 10 bps (5-y). Still, markets only see a limited 20% chance of the BoE again hiking rates already at November meeting. Sterling is holding stable against the dollar (1.218). EUR/GBP at 0.867 (for now) avoids a new test of the key 0.87 resistance.

News & Views

Riksbank deputy governor Floden said in a speech that inflationary pressures remain far too high: “It is becoming increasingly clear that monetary policy needs to stay contractionary for quite some time to come.” He warned that the weak krone isn’t helping the inflation fight. The rebound from the all-time low near EUR/SEK 12 to 11.60 currently isn’t sufficient to change fortunes. In separate comments, governor Thedeen added that he hoped that investors took inspiration from the Riksbank’s recent FX hedging strategy where it sells USD and EUR. He labels it risk management though and not interventions. Underlying and 3-month inflation is still too high, keeping the door wide open for an extra 25 bps rate hike at the central bank’s November 23 policy meeting. Money markets currently discount a 52.5% probability.

Iran foreign minister Amirabdollahian called for an immediate and complete embargo against Israel by Islamic countries, including an oil embargo. Brent crude temporary spiked to $93/b, but couldn’t hold on to gains dropping back to the low $91/b area currently.

Geo Tensions Lift Swiss Franc Modestly, Other Currencies Unperturbed

The tumultuous environment resulting from the Middle East tensions has prompted a noticeable upswing in Gold and Oil prices today, yet the forex markets remain relatively unaffected. Swiss Franc is currently leading the pack, its ascent likely attributed to the ongoing geopolitical unrest, though its rise is modest. US President Joe Biden's diplomatic mission to Israel aims to alleviate the regional tensions; however, the impact of this intervention remains uncertain.

Yen is claiming the spot as the second strongest performer, bolstered by 10-year JGB yield reaching its peak since 2013. This surge in yield is ostensibly linked to anticipations of BoJ revising its inflation forecast upwards, potentially allowing for more yield curve control flexibility.

Conversely, Australian Dollar's gains, initially sparked by encouraging Chinese economic indicators, were short-lived. Euro presently trails as the day's weakest currency, with New Zealand Dollar and Dollar following suit. British Pound is maintaining a neutral stance, seemingly unaffected by the marginally higher consumer inflation figures.

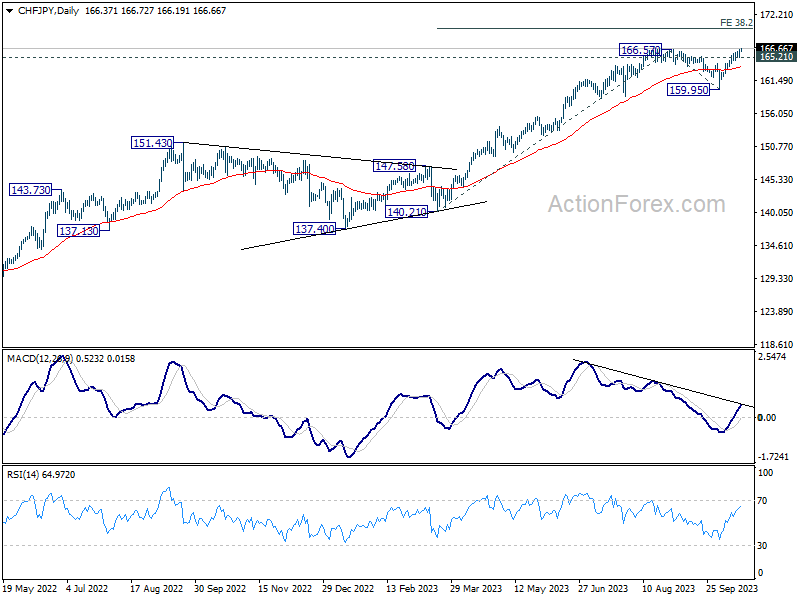

From a technical standpoint, CHF/JPY's break of 166.57 resistance suggests that long term up trend is trying to resume. Further rally is expected as long as 165.21 minor support holds. Next target is 38.2% projection of 140.21 to 166.57 from 159.95 at 170.01. However, break of 165.21 will delay the bullish case and bring more consolidations first.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -0.48%. CAC is down -0.44%. Germany 10-year yield is up 0.029 at 2.901. Earlier in Asia, Nikkei rose 0.01%. Hong Kong HSI dropped -0.23%. China Shanghai SSE dropped -0.80%. Singapore Strait Times dropped -1.11%. Japan 10-year JGB yield rose 0.0230 to 0.808.

Eurozone CPI finalized at 4.3% yoy in Sep, core CPI at 4.5% yoy

Eurozone CPI was finalized at 4.3% yoy in September, down from 5.2% yoy in August. Core CPI was finalized at 4.5% yoy, down from prior month's 5.3% yoy.

The highest contribution to the annual Eurozone inflation rate came from services (+2.05 percentage points, pp), followed by food, alcohol & tobacco (+1.78 pp), non-energy industrial goods (+1.06 pp) and energy (-0.55 pp).

EU CPI was finalized 4.9% yoy, down from August's 5.9% yoy. The lowest annual rates were registered in the Netherlands (-0.3%), Denmark (0.6%) and Belgium (0.7%). The highest annual rates were recorded in Hungary (12.2%), Romania (9.2%) and Slovakia (9.0%). Compared with August, annual inflation fell in twenty-one Member States, remained stable in one and rose in five.

UK CPI unchanged at 6.7% yoy in Sep, services inflation back at 3-decade high

UK CPI was unchanged at 6.7% yoy in September, above expectation of slowing to 6.6% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 6.2% yoy to 6.1% yoy, above expectation of 6.0% yoy.

CPI goods annual rate fell slightly from 6.3% to 6.2%. CPI services annual rate rose from 6.8% to 6.9%, joint highest rate (with May 2023) since March 1992.

On a monthly basis, CPI rose 0.5% mom, above expectation of 0.4% mom, quickly than prior month's 0.3% mom.

RBA's Bullock highlights sticky services inflation, housing and job market

RBA Governor Michele Bullock voiced concerns over stickiness in services inflation, rising house prices and tight labor market at an Australian Financial Security Authority event.

"We're seeing a slowdown in consumption," Bullock said, pointing out a decline in per capita consumption. This can be attributed to the central bank's policy measures, as indicated by her remark, "monetary policy is starting to bite." She elaborated that businesses were starting to find it hard to pass on cost increases as demand begins to taper.

However, the stickiness of inflation remains a significant concern. Bullock highlighted a stubborn rise in services inflation, which encompasses various sectors, from restaurants to hairdressers. "That inflation is running at a bit over 4 per cent," she noted, acknowledging it exceeds RBA's target and mirrors inflationary trends observed globally.

Additionally, housing prices are on the rise again, coupled with a tight employment market, contributing to inflationary pressures. These economic elements, combined with external factors such as the Israel-Gaza conflict escalating fuel costs, suggest that inflation might remain a persistent issue.

Australia's Westpac Index reports fourteenth month in red, despite marginal improvement.

Australia's economic outlook remains subdued as indicated by the Westpac Leading Index, which, though it rose slightly from -0.48% to -0.34% in September, continues to signal prolonged weak conditions. Fourteen successive months of subzero readings on the headline index growth rate project that the anaemic sub-trend growth momentum is anticipated to linger into 2024.

Westpac anticipates the nation's GDP growth to decelerate to 1.2% in 2023, maintaining this tepid pace into the initial half of 2024, with an annualized growth rate pegged at 1.1%. This projection is notably beneath the expected population growth, which is projected to hover around 2.3%.

The recent minutes from RBA's October meeting shed light on the central bank's discomfort with the current inflationary environment, revealing its "low tolerance" towards unexpected inflationary spikes.

As the market casts its gaze towards the upcoming RBA meeting slated for November 7, Westpac anticipates revisions in the near-term forecasts for headline inflation. However, adjustments to the central bank's medium-term view, a critical determinant for any further rate hike, are not expected.

However, this anticipation hinges significantly on the unveiling of the September quarter CPI, scheduled for release on October 25. Any significant surprises in this data could recalibrate expectations and potentially prompt the RBA to rethink its stance.

China's Q3 GDP growth beats expectations; IMF cautions on future prospects

China's economy exhibited resilience in Q3, with GDP growing at 4.9% yoy, outpacing anticipated 4.5% yoy increase. However, this growth rate reflects deceleration from 6.3% yoy expansion observed in Q2. On quarterly basis, the economy grew 1.3% qoq, marking an improvement from revised 0.5% qoq in the preceding quarter and outpacing anticipated 1.0% qoq expansion.

Industrial output in September echoed the positive trend, registering a 4.5% yoy uptick, marginally above 4.3% yoy forecast. Retail sales also followed suit, with 5.5% yoy increase, surpassing expected 4.9% yoy rise. However, fixed asset investments underperformed expectations, with year-to-date growth of 3.1% yoy, slightly below anticipated 3.2%.

Despite these seemingly positive indicators, China's National Bureau of Statistics sounded a note of caution. The NBS underscored the challenges posed by a complicated external environment and lackluster domestic demand, calling for enhanced efforts to fortify the economic recovery's foundation.

Separately, International Monetary Fund adjusted its growth outlook for China downward, citing a "losing steam" recovery impacted significantly by the property sector's frailty. IMF now projects China's economy to grow by 5% in 2023 and 4.2% in 2024, a downward revision from its earlier forecast of 5.2% and 4.5% respectively.

The IMF's report highlighted contraction in manufacturing purchasing managers' indexes from April to August, coupled with additional weaknesses in real estate sector, as pivotal factors behind the revised forecast.

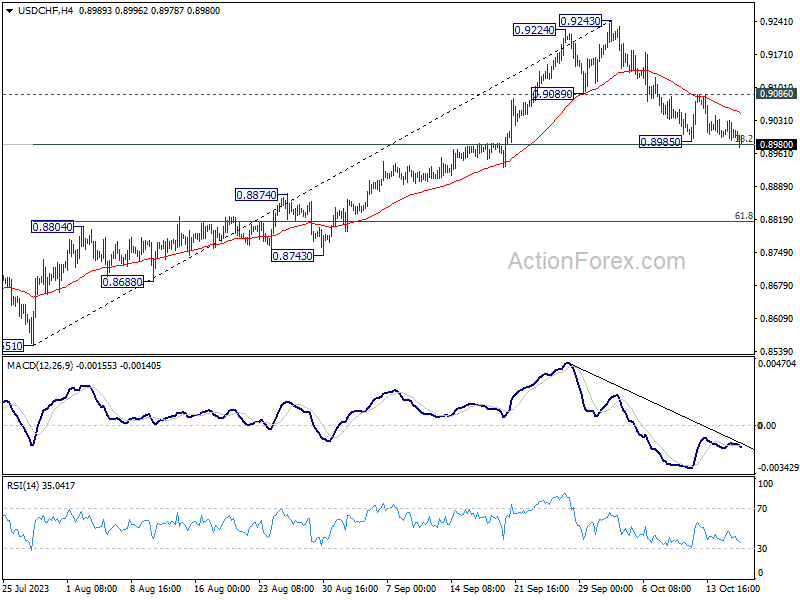

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8985; (P) 0.9008; (R1) 0.9027; More....

Immediate focus is now on 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Sustained break there will extend the fall from 0.9243 to 61.8% retracement at 0.8815. That would also carry larger bearish implications. On the upside, however, , break of 0.9086 resistance will indicate that pull back from 0.9243 has completed, and turn bias to the upside for retesting this high.

In the bigger picture, as long as 55 D EMA (now at 0.8976) holds rise from 0.8551 is viewed as reversing whole down trend from 1.0146 (2022 high). On resumption, further rise should be seen to 61.8% retracement of 1.0146 to 0.8551 at 0.9537 and above. However, sustained break of 55 D EMA will revive medium term bearishness, for retesting 0.8551 low at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.10% | -0.04% | ||

| 02:00 | CNY | GDP Y/Y Q3 | 4.90% | 4.50% | 6.30% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 5.50% | 4.90% | 4.60% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 4.50% | 4.30% | 4.50% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Sep | 3.10% | 3.20% | 3.20% | |

| 06:00 | GBP | CPI M/M Sep | 0.50% | 0.40% | 0.30% | |

| 06:00 | GBP | CPI Y/Y Sep | 6.70% | 6.60% | 6.70% | |

| 06:00 | GBP | Core CPI Y/Y Sep | 6.10% | 6.00% | 6.20% | |

| 06:00 | GBP | RPI M/M Sep | 0.50% | 0.50% | 0.60% | |

| 06:00 | GBP | RPI Y/Y Sep | 8.90% | 8.90% | 9.10% | |

| 06:00 | GBP | PPI Input M/M Sep | 0.40% | 0.20% | 0.40% | 0.80% |

| 06:00 | GBP | PPI Input Y/Y Sep | -2.60% | -2.30% | -2.00% | |

| 06:00 | GBP | PPI Output M/M Sep | 0.40% | 0.30% | 0.20% | |

| 06:00 | GBP | PPI Output Y/Y Sep | -0.10% | -0.40% | -0.50% | |

| 06:00 | GBP | PPI Core Output M/M Sep | 0% | -0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Sep | 0.70% | 1.60% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Sep F | 4.30% | 4.30% | 4.30% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep F | 4.50% | 4.50% | 4.50% | |

| 12:30 | USD | Building Permits M/M Sep | 1.47M | 1.45M | 1.54M | |

| 12:30 | USD | Housing Starts M/M Sep | 1.36M | 1.39M | 1.28M | |

| 14:30 | USD | Crude Oil Inventories | -0.5M | 10.2M | ||

| 18:00 | USD | Fed's Beige Book |

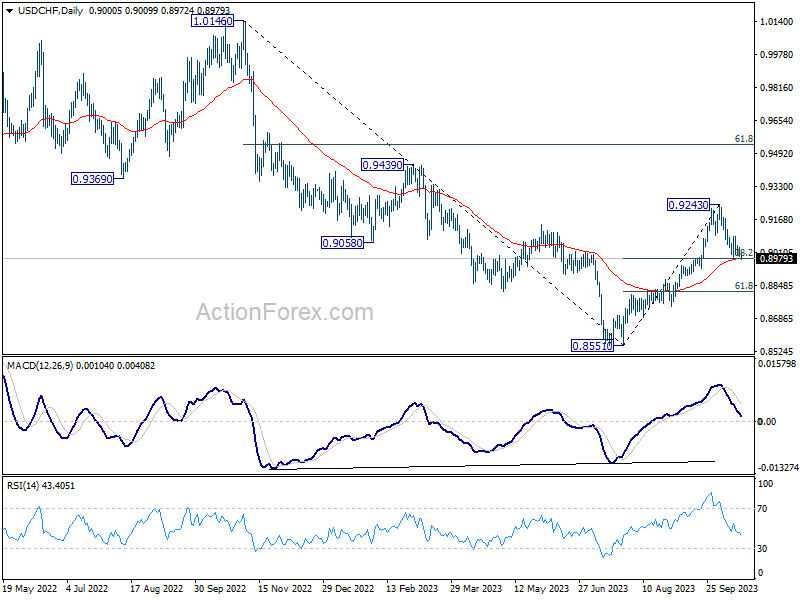

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8985; (P) 0.9008; (R1) 0.9027; More....

Immediate focus is now on 38.2% retracement of 0.8551 to 0.9243 at 0.8979. Sustained break there will extend the fall from 0.9243 to 61.8% retracement at 0.8815. That would also carry larger bearish implications. On the upside, however, , break of 0.9086 resistance will indicate that pull back from 0.9243 has completed, and turn bias to the upside for retesting this high.

In the bigger picture, as long as 55 D EMA (now at 0.8976) holds rise from 0.8551 is viewed as reversing whole down trend from 1.0146 (2022 high). On resumption, further rise should be seen to 61.8% retracement of 1.0146 to 0.8551 at 0.9537 and above. However, sustained break of 55 D EMA will revive medium term bearishness, for retesting 0.8551 low at a later stage.

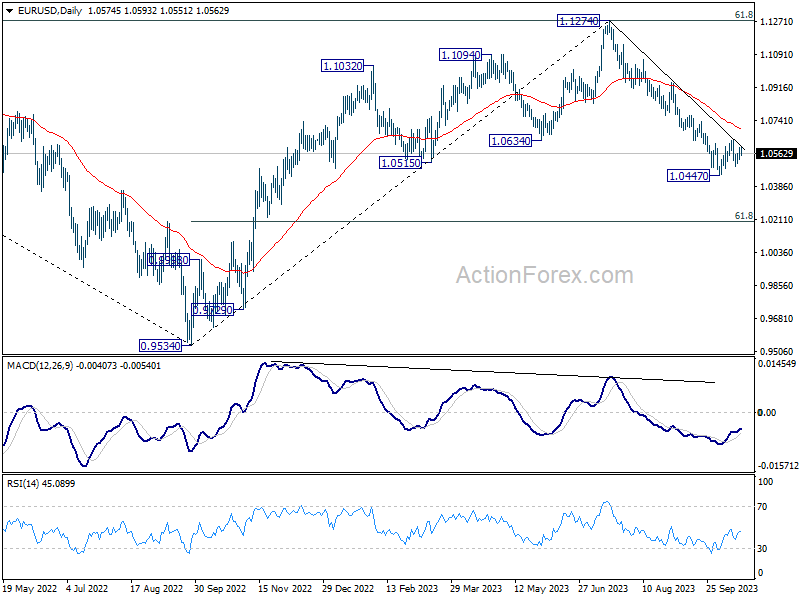

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0541; (P) 1.0568; (R1) 1.0603; More...

No change in EUR/USD's outlook as consolidation from 1.0447 is extending. Intraday bias remains neutral. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0694).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0694) holds, in case of rebound.

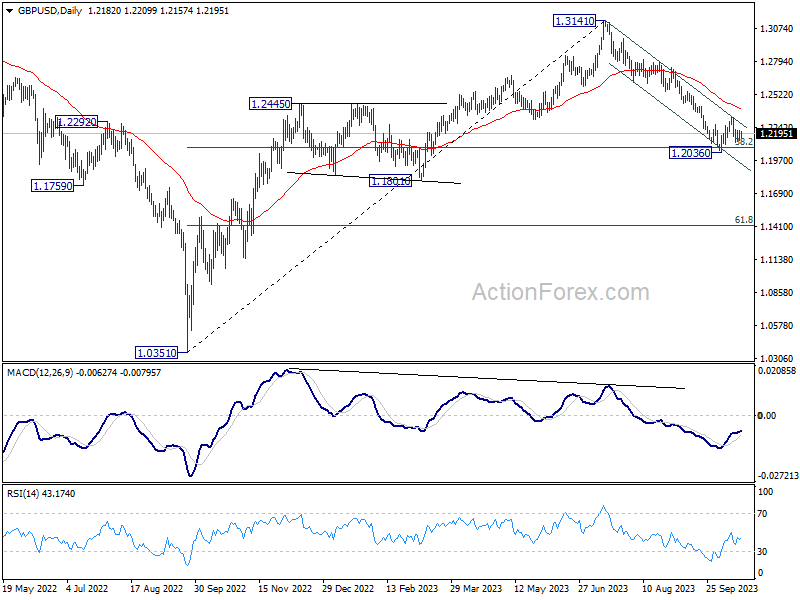

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2137; (P) 1.2178; (R1) 1.2222; More

No change in GBP/USD's outlook as consolidation from 1.2026 is still extending. Intraday bias remains neutral at this point. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will resume the rebound from 1.2036 to 55 D EMA (now at 1.2394).

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2394) holds, in case of rebound.

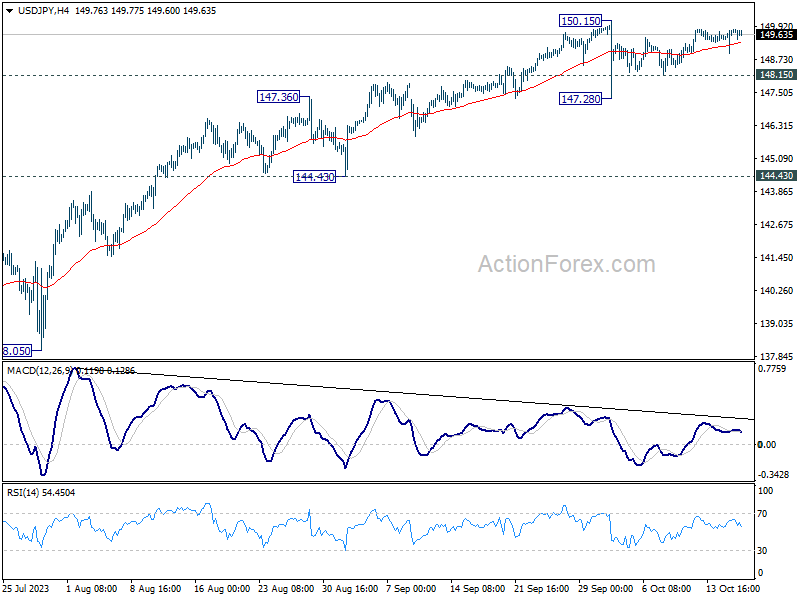

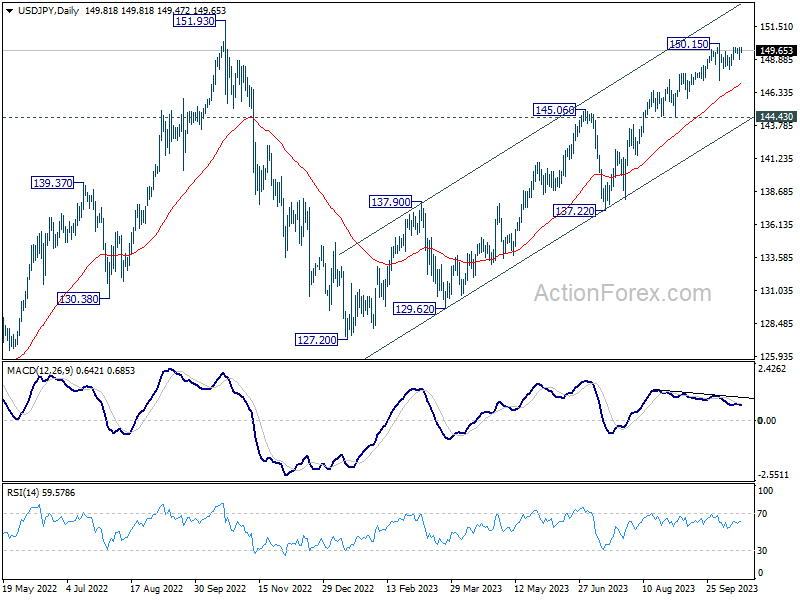

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.37; (P) 149.61; (R1) 150.05; More...

USD/JPY is still extending sideway trading and intraday bias stay neutral for the moment. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

British Pounds Shrugs as CPI Remains Steady

- UK CPI unchanged, core CPI ticks lower

- US retail sales hotter than expected

The British pound is showing limited movement on Wednesday. In the European session, GBP/USD is trading at 1.2194, down 0.09%.

UK CPI unchanged, core CPI ticks lower

Today’s UK inflation report showed little change from a month ago, a reminder that the battle to curb inflation will be a long one. Headline CPI was unchanged in September at 6.7%, remaining at its lowest level in 18 months, but above the market estimate of 6.6%. Month-to-month, headline CPI rose 0.5%, up from 0.3% in August. A sharp rise in gasoline prices was the main driver of September inflation, which was partially offset by a decline in food prices.

Core CPI, which is closely watched by the Bank of England, dropped in September from 6.2% y/y to 6.1%. However, the core rate jumped to 0.5% m/m, up sharply from 0.1% in August, matching the market estimate. The upswing points to core inflation remaining sticky, but the future markets are widely expecting the BoE to pause for a second straight month, after 14 consecutive rate hikes. Today’s inflation report is unlikely to shed much light on what the BoE will do at the November 2nd meeting, and Governor Bailey said on Monday that like the September meeting, upcoming rate decisions would be close calls.

US retail sales jump in September

US retail sales in September were hotter than expected, a sign that consumer spending remains robust despite the challenging economic picture. Retail sales are not adjusted for inflation, which means that consumers have managed to keep up with price increases. Consumer spending has been strong in the third quarter, which should translate into a solid GDP reading next week. It also provides support for the Fed to keep interest rates at elevated levels – Fed rate odds for a December hike have risen to 34%, up from 30% prior to the release.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2202. Next, there is resistance at 1.2281

- There is support at 1.2137 and 1.2066

EURJPY Attempts Breakout Above Cloud But Tough Resistance at 158.60

- EURJPY turns more bullish after rising above 50-day SMA and cloud

- But 158.60 level proving to be a more difficult obstacle

- Bigger picture remains neutral

EURJPY has gained some positive traction in recent days after clearing both the 50-day simple moving average (SMA) as well as the top of the Ichimoku cloud. However, the bulls can only claim partial victory because there is a high risk of a pullback if the pair is unable to break above the 158.60 hurdle, which is hindering a more convincing breakout above the cloud.

The momentum indicators are pointing to a continuation of the bullish bias in the near term. But whereas the fast and slow stochastics are positively aligned and rising, the RSI appears to have flatlined slightly above 50, questioning whether the current upside momentum will be strong enough to drive further gains.

Should the bulls manage to push the price above the 158.60 barrier, the next target will be the August top of 159.75, which was a 15-year high. A successful climb above the 160.00 zone would likely turn attention to the 165.00 area, which last acted as resistance all the way back in 2008. This was also when the pair came just shy of the next crucial level of 170.00.

On the other hand, if EURJPY fails to overcome the immediate resistance of 158.60, a downside reversal would probably follow, with initial support coming from the 50-day SMA at 157.90. A steeper slide would bring into scope the 100-day SMA, which is about to intersect the Kijun-sen line at 156.49, while lower down, the bottom of the cloud could halt the decline at 155.57.

In the medium term, however, the outlook remains neutral and only a sustained advance above the August peak of 159.75 would shift it to bullish. Otherwise, a drop below the cloud would not only turn the short-term picture to bearish, but it would undermine the neutral structure in the medium term as well as question the longer-term uptrend.