Sample Category Title

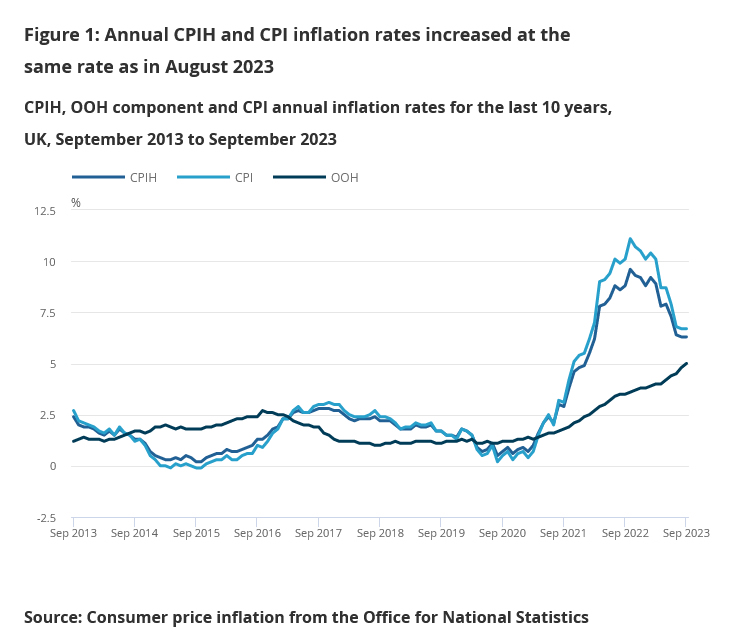

UK CPI unchanged at 6.7% yoy in Sep, services inflation back at 3-decade high

UK CPI was unchanged at 6.7% yoy in September, above expectation of slowing to 6.6% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 6.2% yoy to 6.1% yoy, above expectation of 6.0% yoy.

CPI goods annual rate fell slightly from 6.3% to 6.2%. CPI services annual rate rose from 6.8% to 6.9%, joint highest rate (with May 2023) since March 1992.

On a monthly basis, CPI rose 0.5% mom, above expectation of 0.4% mom, quickly than prior month's 0.3% mom.

Macro Data Surprises to the Upside in US and China

Market movers today

UK September CPI is due for release this morning, consensus expects core inflation to continue moderating to 6.0% in y/y terms after the downside surprise in August.

Final inflation data will also be released for euro area. We expect no major changes to the flash release, but the data will still shed some light on the details of what drove the downtick in core inflation.

A range of Fed speakers will be on the wires today, including Kashkari, Waller, Williams, Bowman and Harker.

Joe Biden will visit Israel today.

Overnight, Australian labour market data is due for release.

The 60 second overview

China: Chinese Q3 GDP beat expectations by growing 1.3% q/q (from 0.5% in Q2, consensus 1.0%). In September, the uptick in growth was driven especially by retail sales (5.5%; from 4.6%) while growth in industrial production (4.5%; from 4.5%) and fixed investments (3.1%; from 3.2%) remained more stable. Overall, it appears that the stimulus measures are finally starting to have an effect on the Chinese economy, which is now set to reach the central government's 5% growth target for 2023. That said, the uncertainty related to the real estate sector will remain a drag for now, with one of China's largest developers, Country Garden, having potentially defaulted on its USD bond coupon payment this morning (see Reuters).

US: Hard US macro data continued the streak of upside surprises yesterday, as retail sales grew by 0.7% in m/m SA in September (August revised higher to 0.8%). While gasoline prices provided a modest lift to sales, even the control group sales (which exclude volatile, car, gasoline, restaurants and building materials) grew by 0.6% m/m (August 0.2%; consensus 0.0%). As Core CPI grew by 0.3% in September, it looks like real consumption volume continued to grow, suggesting that the US economy has remained on a more solid footing than expected. Industrial production also surprised to the upside (0.3%; consensus 0.0%), although the uptick was compensated for by a downward revision to August data (0.0%; from 0.4%). In any case, US yields continued to edge higher yesterday, and while the Fed has communicated that it will most likely remain on hold at the November meeting two weeks from now, the market-implied probability of a final hike in December or January has now reached around 50%. We still stick to our long-held call that the Fed is likely already done hiking despite the recent positive data surprises.

Geopolitics: Tensions seem to be tightening on many fronts, and not least in Israel where Joe Biden is headed for a visit today. In the Nordics, Sweden reported yesterday that it is investigating damage to a telecom cable to Estonia. While the cause remains unknown for now, the timing and physical location of the damage were close to the Balticconnector gas pipeline between Finland and Estonia, which was last week reported to have been damaged likely from the outside (see Reuters). And on US-China relations, Biden administration announced a further tightening in microchip export controls yesterday, targeted at blocking China's access to the most advanced chips used especially for AI solutions (see FT).

Equities: Good news was bad news when retail sales turned out better than expected. Equities were muted as a result, with S&P 500 and Stoxx 600 closing unchanged, off worst levels. As yields moved higher, value cyclicals outperformed (energy, materials, and financials) with rotation out of real estate and tech. The latter was a headwind after confirmation of additional restrictions on US exports on advanced chips from China. US futures are unchanged this morning and Asian markets lower.

FI: Global yields continued to move higher yesterday, following the release of stronger-than-expected US retail sales data. 10Y UST yields rose 13bp to 4.84%, the highest level since 2007, driving a renewed steepening of the 10s2s curve. In line with moves seen over the past month, real rates were the main driver of yesterday's move, as long-term inflation expectations remained relatively unchanged. Markets are pricing in close to 15bp of additional policy tightening in the US until January, while the first full 25bp cut is now seen in June 2024. The sell-off was also visible in European bond markets, with the 10Y Bund yield rising nearly 10bp throughout the day.

FX: In Scandies space, EUR/DKK briefly rose above 7.4620 yesterday and thus broke the recent top from September. EUR/SEK oscillated within 11.51 and 11.56 as the Riksbank hearing provided no news for the markets and risk sentiment soured, where the latter helped push EUR/NOK closer to 11.60, the upper end of the recent range. In majors, EUR/USD moved higher but bounced at 1.059 before spending the Asian session around 1.0575. USD/JPY very briefly dropped below 149 yesterday but was not comfortable and soon tested 150. The CHF continues to trade on a strong note albeit seeing a slight correction from last week with EUR/CHF close to 0.95.

Credit: Yesterday, credit markets continued the cautious sentiment while global rates continued to move upwards across the curves, leaving CDS indices broadly unchanged with iTraxx Main (-0.4bp) at 83.5bp and iTraxx Xover (-0.6bp) at 445bp. In addition, the primary market activity was very subdued as the Q3 earning season kicks in.

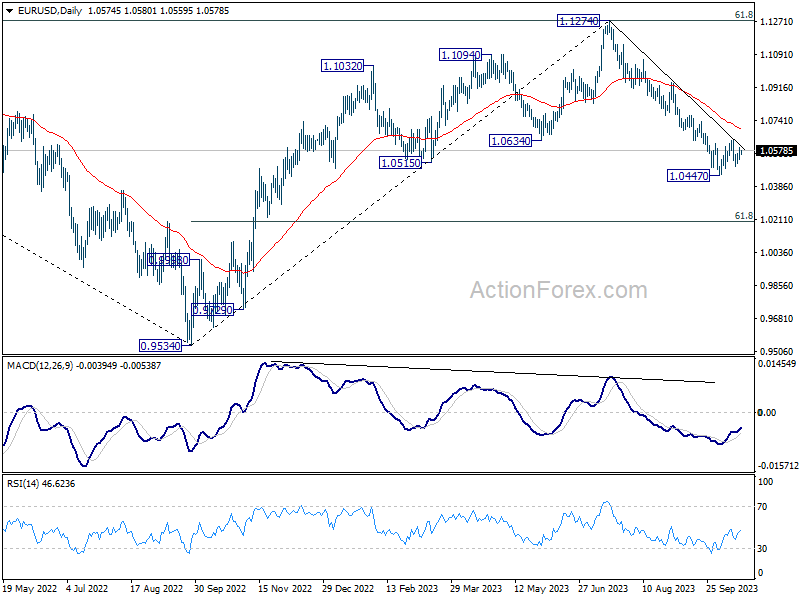

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0541; (P) 1.0568; (R1) 1.0603; More...

Intraday bias in EUR/USD remains neutral for the moment. Outlook stays bearish with 1.0639 resistance intact. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0694).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0694) holds, in case of rebound.

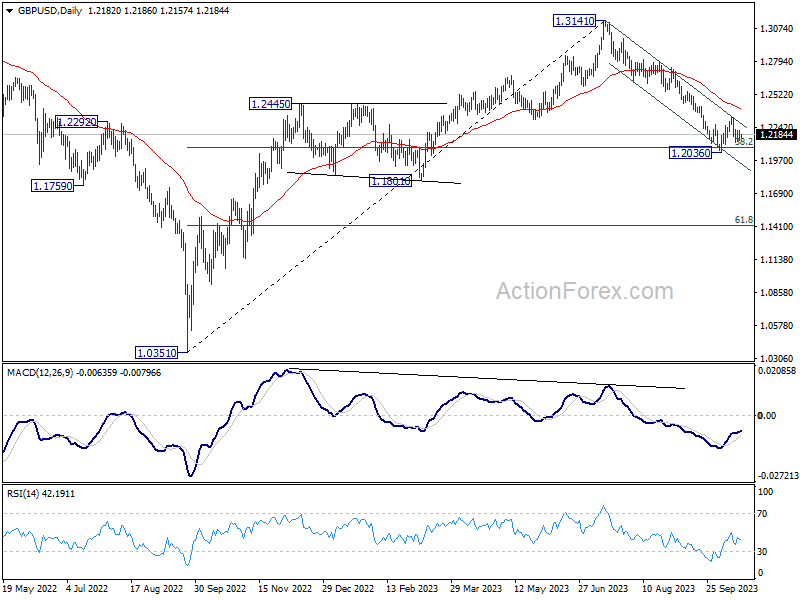

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2137; (P) 1.2178; (R1) 1.2222; More

GBP/USD is still extending the consolidation form 1.2036 and intraday bias stays neutral. On the downside, decisive break of 1.2036 will resume whole decline from 1.3141 for 1.1801 support next. However, break of 1.2336 will resume the rebound from 1.2036 to 55 D EMA (now at 1.2394).

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2394) holds, in case of rebound.

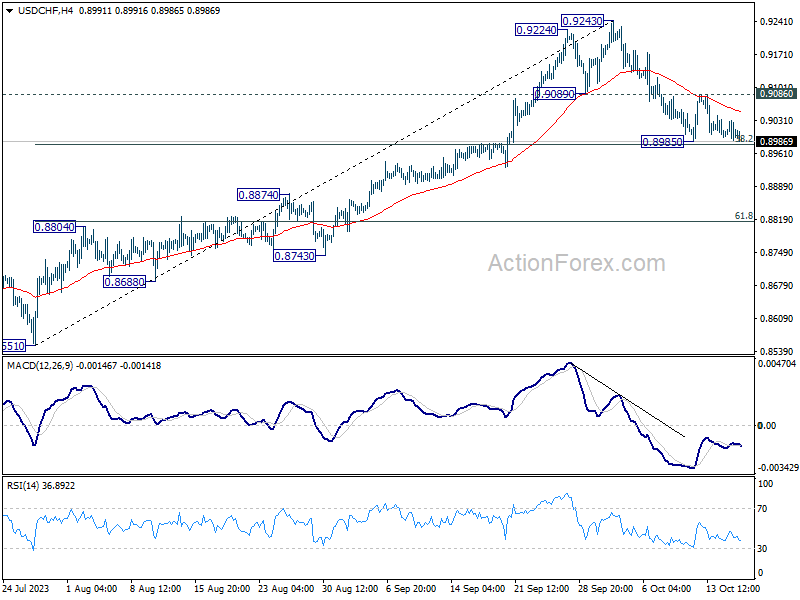

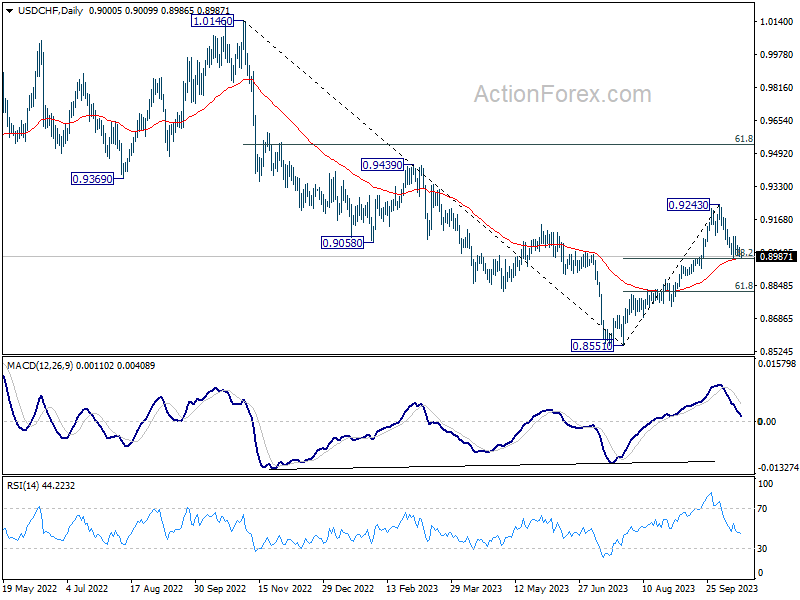

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8985; (P) 0.9008; (R1) 0.9027; More....

Intraday bias in USD/CHF stays neutral and outlook is unchanged. On the upside, break of 0.9086 resistance will indicate that pull back from 0.9243 has completed, and turn bias to the upside for retesting this high. However, sustained break of 38.2% retracement of 0.8551 to 0.9243 at 0.8979 will argue that deeper fall is under way to 61.8% retracement at 0.8815.

In the bigger picture, as long as 55 D EMA (now at 0.8976) holds rise from 0.8551 is viewed as reversing whole down trend from 1.0146 (2022 high). On resumption, further rise should be seen to 61.8% retracement of 1.0146 to 0.8551 at 0.9537 and above. However, sustained break of 55 D EMA will revive medium term bearishness, for retesting 0.8551 low at a later stage.

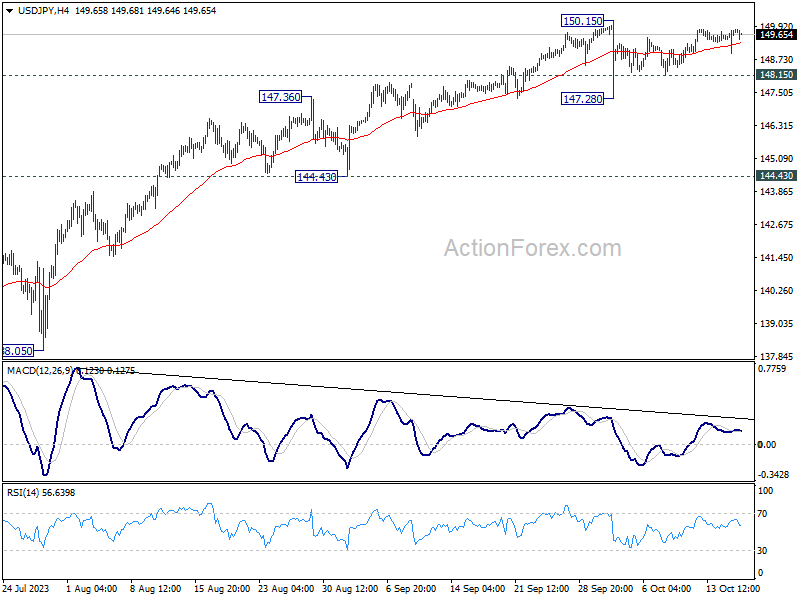

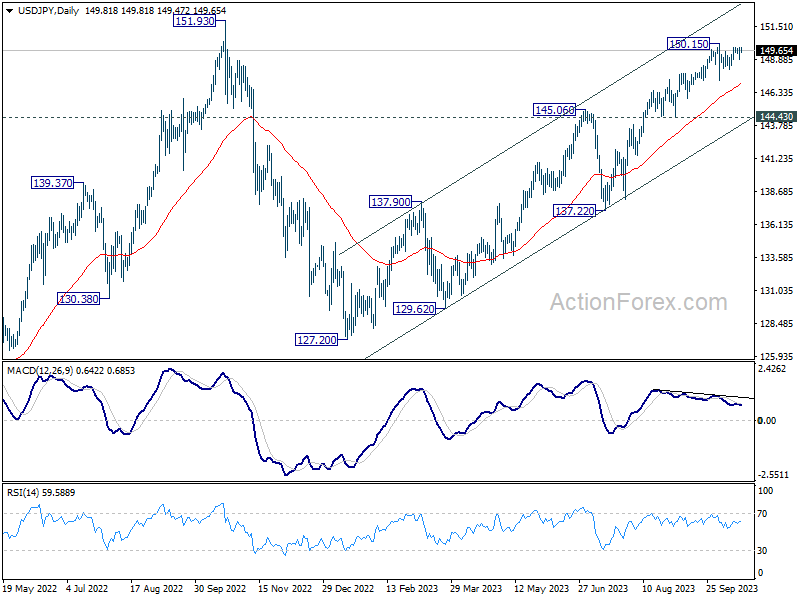

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.37; (P) 149.61; (R1) 150.05; More...

Intraday bias in USD/JPY remains neutral as range trading continues. On the downside, below 148.24 minor support will turn bias to the downside for another down leg through 147.28. On the upside, firm break of 150.15 will resume larger up trend to test 151.93 high.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by sustained break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

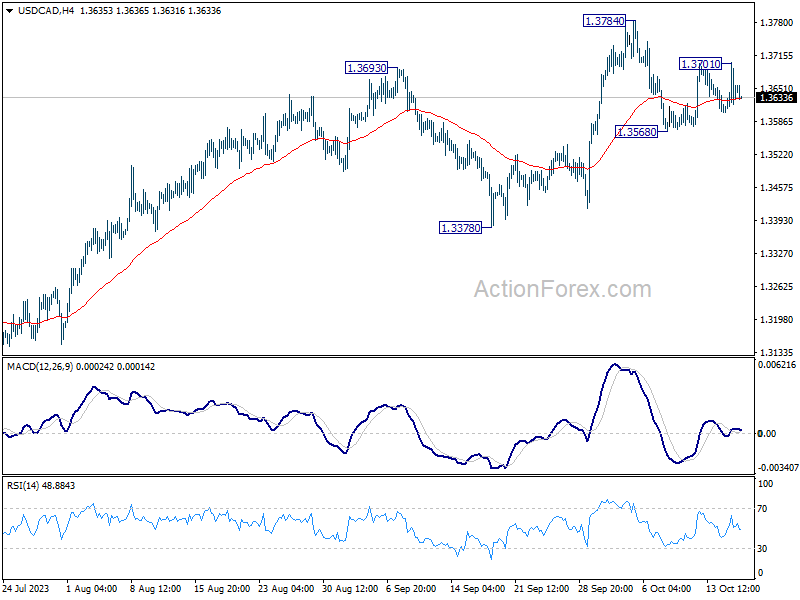

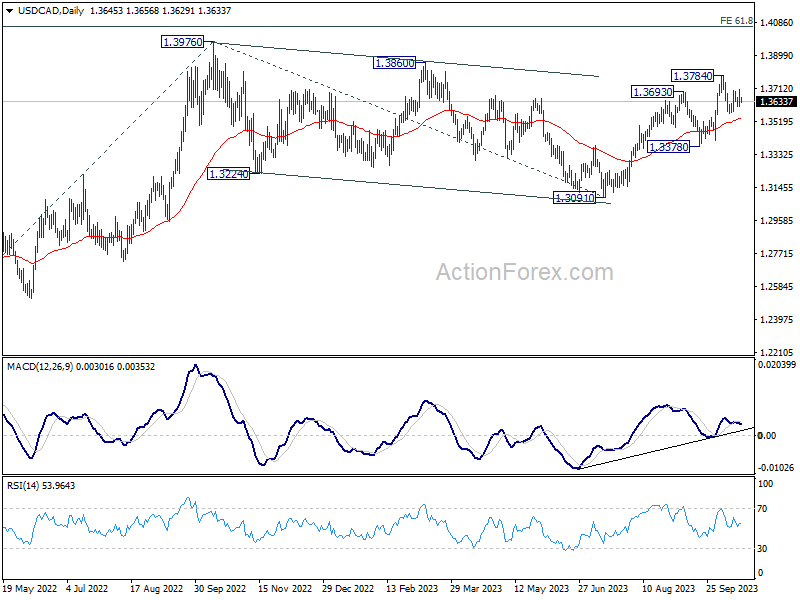

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3589; (P) 1.3627; (R1) 1.3648; More....

Intraday bias in USD/CAD remains neutral for the moment. On the downside, break of 1.3568 will bring another falling leg to extend the near term corrective pattern from 1.3784 . Meanwhile, break of 1.3701 will target 1.3784 first. Break there will resume larger rise from 1.3091 to retest 1.3976 high.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

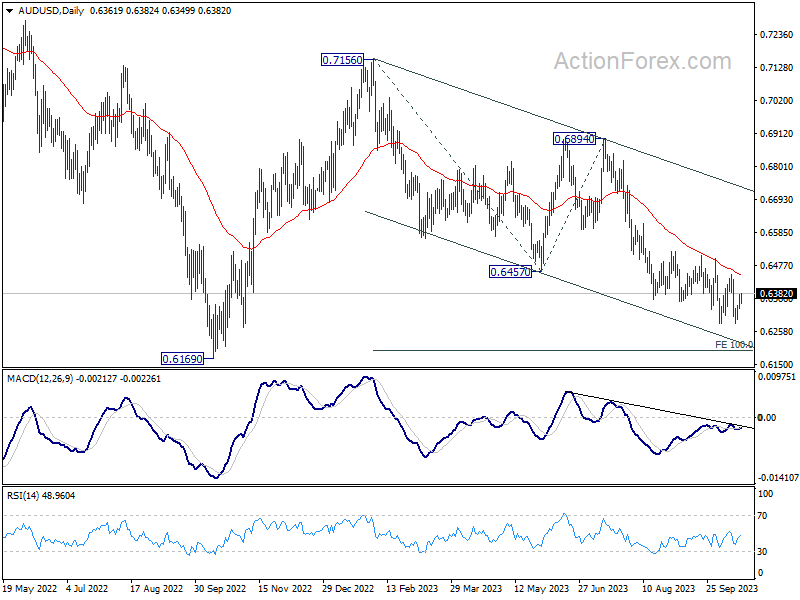

AUD/USD Daily Report

Daily Pivots: (S1) 0.6339; (P) 0.6360; (R1) 0.6386; More...

AUD/USD's recovery continues today but stays below 0.6444 resistance. Intraday bias remains neutral and outlook stays bearish. On the downside, decisive break of 0.6284 will confirm resumption of whole decline from 0.7156. Next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support. Nevertheless, firm break of 0.6444 will confirm short term bottoming, and turn bias to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

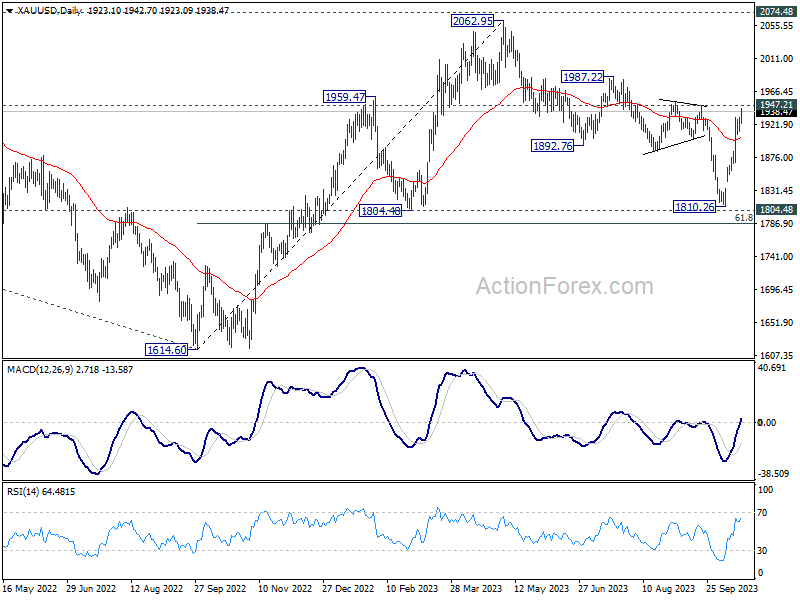

Gold and Oil Prices Rise Amidst Re-escalating Middle East Tensions

The Middle East sees a re-escalation in geopolitical tensions following a tragic strike on a Gaza hospital, leading to significant rise in both Oil and Gold prices. The effect of this development extends into Asian session. However, risk aversion is not starkly evident in other markets, as Asian indices, excluding Japan, record only marginal losses. Treasury bonds and Swiss Franc have not seen noteworthy inflows, indicating that traders are maintaining a cautious, observatory approach. All eyes are also set on the meeting between Russian President Vladimir Putin and Chinese President Xi Jinping.

China also attracts attention due to its encouraging economic data released today, lending a slight uplift to Chinese Yuan. This positivity has, in turn, given a slight uplift to Australian and New Zealand dollars. Conversely, Dollar has lost some steam as the rally following retail sales data from yesterday began to wane quickly. Euro and Sterling aren't faring much better, with both currencies ranking among the day's laggards. Japanese Yen is similarly on the softer side, eclipsed by Swiss Franc and Canadian Dollar. As it stands, the majority of major currency pairs and their crosses remain confined within the trading range set the previous day. However, the forthcoming UK inflation data could provide the catalyst for more significant market movements.

Technically, Gold's rise from 1810.26 resumes today and it's now targeting 1942.71 resistance. Decisive break there will further strengthen the case that correction from 2062.95 has completed with three waves down to 1810.26, just ahead of 1804.40. Further rally could then be seen through 1987.22 to retest 2062.95 high. In any case, near term outlook will stay bullish as long as 55 D EMA (now at 1902.96) holds.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is down -0.10%. China Shanghai SSE is down -0.61%. Singapore Strait Times is down -0.54%. Japan 10-year JGB yield is up 0.028 at 0.813. Overnight, DOW rose 0.04%. S&P 500 dropped -0.01%. NASDAQ dropped -0.25%. 10-year yield rose 0.135 to 4.847.

RBA's Bullock highlights sticky services inflation, housing and job market

RBA Governor Michele Bullock voiced concerns over stickiness in services inflation, rising house prices and tight labor market at an Australian Financial Security Authority event.

"We're seeing a slowdown in consumption," Bullock said, pointing out a decline in per capita consumption. This can be attributed to the central bank's policy measures, as indicated by her remark, "monetary policy is starting to bite." She elaborated that businesses were starting to find it hard to pass on cost increases as demand begins to taper.

However, the stickiness of inflation remains a significant concern. Bullock highlighted a stubborn rise in services inflation, which encompasses various sectors, from restaurants to hairdressers. "That inflation is running at a bit over 4 per cent," she noted, acknowledging it exceeds RBA's target and mirrors inflationary trends observed globally.

Additionally, housing prices are on the rise again, coupled with a tight employment market, contributing to inflationary pressures. These economic elements, combined with external factors such as the Israel-Gaza conflict escalating fuel costs, suggest that inflation might remain a persistent issue.

Australia's Westpac Index reports fourteenth month in red, despite marginal improvement.

Australia's economic outlook remains subdued as indicated by the Westpac Leading Index, which, though it rose slightly from -0.48% to -0.34% in September, continues to signal prolonged weak conditions. Fourteen successive months of subzero readings on the headline index growth rate project that the anaemic sub-trend growth momentum is anticipated to linger into 2024.

Westpac anticipates the nation's GDP growth to decelerate to 1.2% in 2023, maintaining this tepid pace into the initial half of 2024, with an annualized growth rate pegged at 1.1%. This projection is notably beneath the expected population growth, which is projected to hover around 2.3%.

The recent minutes from RBA's October meeting shed light on the central bank's discomfort with the current inflationary environment, revealing its "low tolerance" towards unexpected inflationary spikes.

As the market casts its gaze towards the upcoming RBA meeting slated for November 7, Westpac anticipates revisions in the near-term forecasts for headline inflation. However, adjustments to the central bank's medium-term view, a critical determinant for any further rate hike, are not expected.

However, this anticipation hinges significantly on the unveiling of the September quarter CPI, scheduled for release on October 25. Any significant surprises in this data could recalibrate expectations and potentially prompt the RBA to rethink its stance.

China's Q3 GDP growth beats expectations; IMF cautions on future prospects

China's economy exhibited resilience in Q3, with GDP growing at 4.9% yoy, outpacing anticipated 4.5% yoy increase. However, this growth rate reflects deceleration from 6.3% yoy expansion observed in Q2. On quarterly basis, the economy grew 1.3% qoq, marking an improvement from revised 0.5% qoq in the preceding quarter and outpacing anticipated 1.0% qoq expansion.

Industrial output in September echoed the positive trend, registering a 4.5% yoy uptick, marginally above 4.3% yoy forecast. Retail sales also followed suit, with 5.5% yoy increase, surpassing expected 4.9% yoy rise. However, fixed asset investments underperformed expectations, with year-to-date growth of 3.1% yoy, slightly below anticipated 3.2%.

Despite these seemingly positive indicators, China's National Bureau of Statistics sounded a note of caution. The NBS underscored the challenges posed by a complicated external environment and lackluster domestic demand, calling for enhanced efforts to fortify the economic recovery's foundation.

Separately, International Monetary Fund adjusted its growth outlook for China downward, citing a "losing steam" recovery impacted significantly by the property sector's frailty. IMF now projects China's economy to grow by 5% in 2023 and 4.2% in 2024, a downward revision from its earlier forecast of 5.2% and 4.5% respectively.

The IMF's report highlighted contraction in manufacturing purchasing managers' indexes from April to August, coupled with additional weaknesses in real estate sector, as pivotal factors behind the revised forecast.

Looking ahead

UK CPI and PPI are the main focuses in European session while Eurozone will publish CPI final. Later in the day, US will release building permits and housing starts, as well as Fed' Beige Book economic report.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6339; (P) 0.6360; (R1) 0.6386; More...

AUD/USD's recovery continues today but stays below 0.6444 resistance. Intraday bias remains neutral and outlook stays bearish. On the downside, decisive break of 0.6284 will confirm resumption of whole decline from 0.7156. Next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195, which is close to 0.6169 medium term support. Nevertheless, firm break of 0.6444 will confirm short term bottoming, and turn bias to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Sep | 0.10% | -0.04% | ||

| 02:00 | CNY | GDP Y/Y Q3 | 4.90% | 4.50% | 6.30% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 5.50% | 4.90% | 4.60% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 4.50% | 4.30% | 4.50% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Sep | 3.10% | 3.20% | 3.20% | |

| 06:00 | GBP | CPI M/M Sep | 0.40% | 0.30% | ||

| 06:00 | GBP | CPI Y/Y Sep | 6.60% | 6.70% | ||

| 06:00 | GBP | Core CPI Y/Y Sep | 6.00% | 6.20% | ||

| 06:00 | GBP | RPI M/M Sep | 0.50% | 0.60% | ||

| 06:00 | GBP | RPI Y/Y Sep | 8.90% | 9.10% | ||

| 06:00 | GBP | PPI Input M/M Sep | 0.20% | 0.40% | ||

| 06:00 | GBP | PPI Input Y/Y Sep | -2.30% | |||

| 06:00 | GBP | PPI Output M/M Sep | 0.30% | 0.20% | ||

| 06:00 | GBP | PPI Output Y/Y Sep | -0.40% | |||

| 06:00 | GBP | PPI Core Output M/M Sep | -0.10% | |||

| 06:00 | GBP | PPI Core Output Y/Y Sep | 1.60% | |||

| 09:00 | EUR | Eurozone CPI Y/Y Sep F | 4.30% | 4.30% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep F | 4.50% | 4.50% | ||

| 12:30 | USD | Building Permits M/M Sep | 1.45M | 1.54M | ||

| 12:30 | USD | Housing Starts M/M Sep | 1.39M | 1.28M | ||

| 14:30 | USD | Crude Oil Inventories | -0.5M | 10.2M | ||

| 18:00 | USD | Fed's Beige Book |

Gold Price Rally Seems Far From Over, US President To Visit Israel

Key Highlights

- Gold prices rallied significantly after the Israeli–Hamas war intensified.

- A connecting bullish trend line is forming with support near $1,895 on the 4-hour chart.

- Today, US President Joe Biden is scheduled to visit Israel and Jordan.

- Growing border concerns amid the Israeli–Hamas war is keeping investors on the edge.

Gold Price Technical Analysis

Gold prices started a strong increase after the Israeli–Hamas war intensified. The price rallied above the $1,890 and $1,900 resistance levels to move into a positive zone. Today, US President Joe Biden is scheduled to visit Israel and Jordan, where he will address the ongoing conflict with both Israeli and Arab leaders.

The 4-hour chart of XAU/USD indicates that the price gained pace above the $1,900 resistance. It settled above the $1,900 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

It even surpassed the 76.4% Fib retracement level of the downward move from the $1,947 swing high to the $1,810 low. The current price action suggests there are high chances of more upsides above $1,930.

Immediate resistance is near the $1,935 level. The first major resistance is $1,950. An upside break above the $1,950 level could send the price soaring toward the $1,965 resistance. The next major resistance is near the $1,980 level, above which Gold could revisit the key $2,000 resistance zone.

On the downside, the price might find support near the $1,900 level. There is also a connecting bullish trend line forming with support near $1,895 on the 4-hour chart.

The next key support is near the gap area at $1,880. If the bulls fail to protect the $1,880 support, there is a risk of a major decline. In the stated case, the price could decline toward the $1,840 level.

Looking at crude oil prices, there was a decent increase toward the $88 resistance and the bulls might now aim a move toward $92.

Economic Releases to Watch Today

- UK Consumer Price Index for Sep 2023 (YoY) – Forecast +6.5%, versus +6.7% previous.

- UK Core Consumer Price Index for Sep 2023 (YoY) – Forecast +6.0%, versus +6.2% previous.