Sample Category Title

Cautious Risk Environment Prevents Dollar from Stacking Up Losses

Markets

Core bonds slid for a second day straight yesterday. US Treasuries underperformed Bunds following (very) strong September retail sales and industrial production figures. NAHB housing market confidence slipped more than expected in October to the lowest since February (from 44 to 40) but its impact was either non‐existent (at the short end of the curve) or only temporary (long end). US yields rallied between 7.4 bps and 15.3 bps. The 2‐y yield (+11.1 bps) hit the highest level since 2006 (>5.20%). The 10‐y tenor closed above 4.8% for the first time since 2007. German yields added between 5.3 and 10.1 bps, bringing the short and long end of the curve about 15 bps away from their respective cycle highs. Word about Biden’s “de‐escalation” summit with Arab leaders being cancelled reached the market only after closing hours. The reason was a deadly strike on a hospital in Gaza City, which Israeli and Hamas blame each other for. Core bond yields contain their disappointment in a first reaction during Asian dealings. US cash yields ease less than 2.5 bps. Stock markets yesterday ended a volatile day little changed. The dollar forfeited its initial, early gains against the euro (EUR/USD 1.0577). The US currency did close higher against several other global peers, limiting the losses for DXY (stable at 106.25). Sterling traded on the backfoot amid huge gilt outperformance following a weaker‐than‐expected but incomplete labour market report. EUR/GBP rose from 0.864 to 0.868. China’s yuan is doing slightly better this morning after slightly better‐than‐expected Q3 growth figures (see below). With the property being an obvious drag still, it’s not a huge reason to cheer. USD/CNY eases to 7.30. The Japanese yen sits around USD/JPY 150. Yields in the country are on the rise. The 10‐y yield adds 3 bps to a new fresh decade high (>0.8%), prompting an unscheduled bond buying operation by the BoJ. Sentiment turned more sour again in Asia with equity indices losing 1% and more in China & Taiwan. Several non‐bank companies are reporting earnings today. The season is gaining traction and could become important for general market sentiment in the upcoming days. Geopolitics are too but it’s anyone’s guess how the conflict will evolve. ECB’s Stournaras in an interview with the Financial Times and Holzmann both noted that the situation in the Middle East could be stagflationary but differ on the potential implications for monetary policy. After the recent sharp moves and with the long end nearing cycle highs, we wouldn’t be surprised to see yields taking a breather today. A cautious risk environment prevents the dollar from stacking up losses. EUR/USD 1.064 serves as a first resistance. After yesterday’s wage data UK (core) inflation this morning tops estimates, offering conflicting signals what to expect from the Bank of England in November. Sterling ekes out a tiny gain to EUR/GBP 0.8675.

News and views

China Q3 GDP growth came out stronger than expected. Growth amounted to 1.3% Q/Q and 4.9% Y/Y (vs 0.9% Q/Q consensus and 0.5% Q/Q in Q2). YTD growth printed at 5.2% Y/Y (from 5.5%). The Q3 release suggests that the government might be on track to reach its full year growth target of about 5%. The data suggest that stimulus efforts are finally delivering. September data also surprised on the upside. Retail sales jumped from 4.6% Y/Y to 5.5% Y/Y. Industrial production at 4.5% Y/Y also was marginally stronger than expected. The jobless rate declined from 5.2% to 5.0%. The property sector continues to struggle with YTD property investments drifting further into negative territory (‐9.1% YTD Y/Y). There was no market euphoria after the data. The CSI 300 equity index is holding negative territory (‐0.7%). The yuan gains but at USD/CNY 7.3065 already reversed part of the initial gains.

In a speech yesterday, the governor of the Czech National Bank (CNB) Michl indicated that the internal debate on easing policy has started and that the CNB internally agreed on a strategy. However, in line with comments from other board members recently, he stressed that any easing will be gradual. The CNB governor didn’t make any commitments on concrete steps at the two remaining meetings this year. Decisions will be taken on the basis of new data and staff forecasts. Whatever they will be, Michl said that the CNB will remain hawkish and continue to protect the country from future inflation. We expect a 25 bps policy rate cut (currently 7%) after better than expected September inflation data (6.9% Y/Y) published last week. However, in a gradual approach the December meeting might also still only result in a next 25 bps step to 6.5%.

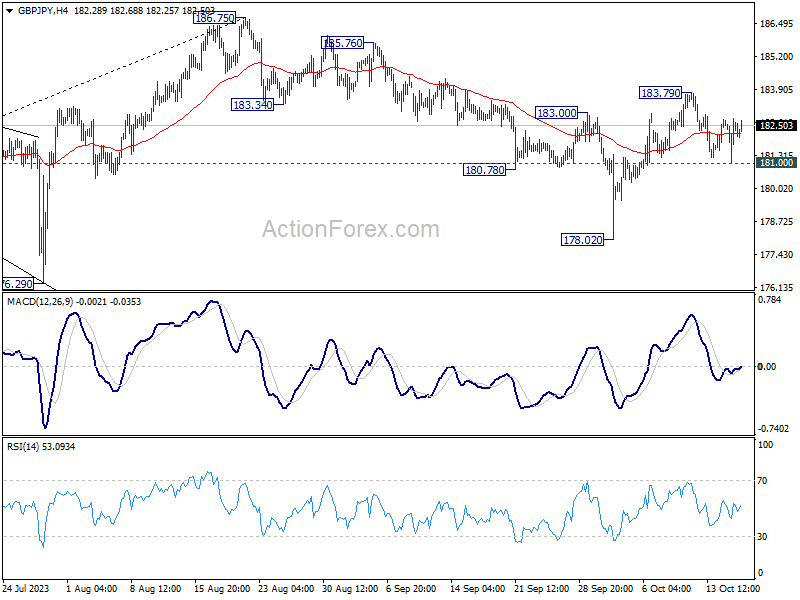

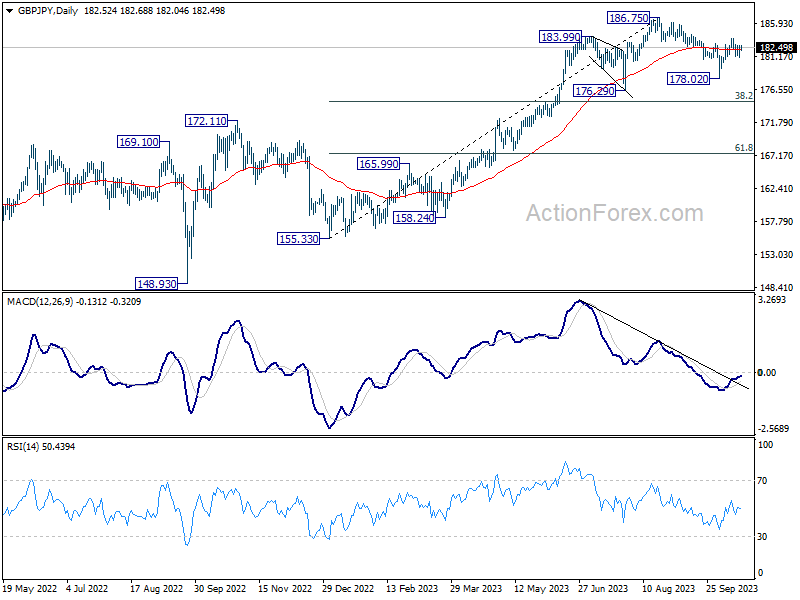

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.76; (P) 182.29; (R1) 183.02; More...

GBP/JPY recovered quickly after dipping to 181.00 and intraday bias stays neutral. The favored case is still that correction from 186.75 has completed at 178.02. Above 183.79 will resume the rise from 178.02 to retest 186.75 high. However, break of 181.00 will dampen this view, and turn bias back to the downside for 178.02 instead.

In the bigger picture, fall from 186.75 is seen as a corrective move only. As long as 176.29 support holds, larger up trend from 123.94 (202 low) should still be in progress. Break of 186.75 will target 195.86 (2015 high). Nevertheless, firm break of 176.29 will confirm medium term topping, and bring lengthier and deeper consolidations.

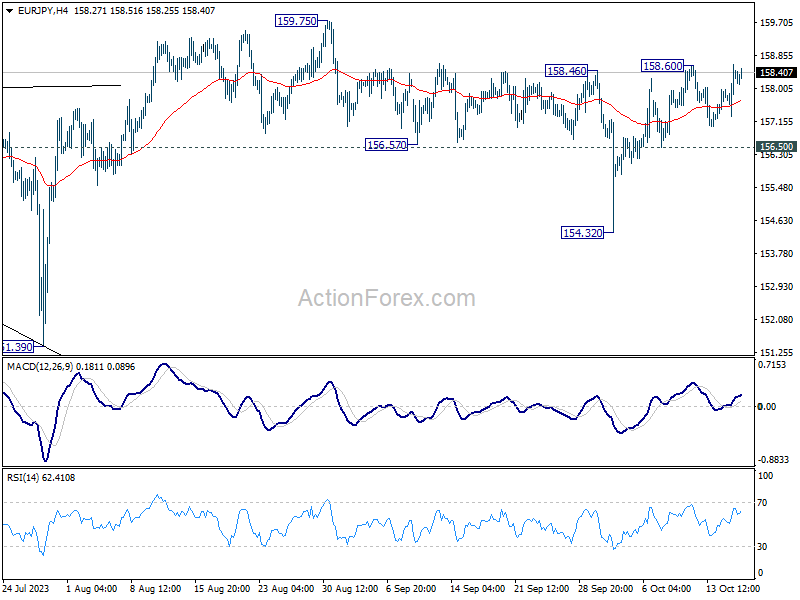

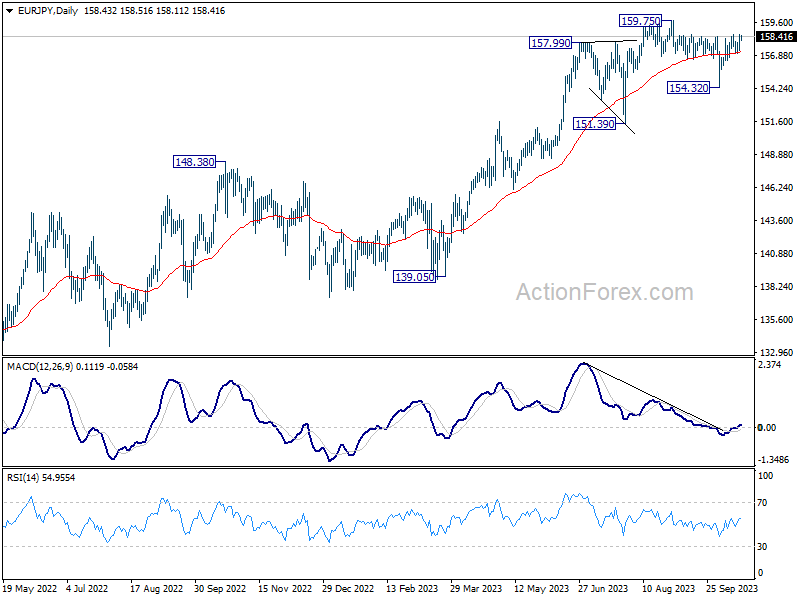

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.73; (P) 158.18; (R1) 158.89; More....

Intraday bias in EUR/JPY remains neutral at this point. Outlook is also unchanged that correction from 159.75 should have completed at 154.32. Above 158.60 will resume the rise from 154.32 and target 159.75 high. However, break of 156.50 will dampen this view, and bring another fall to extend the corrective pattern from 159.75.

In the bigger picture, price actions from 159.75 are views as a corrective pattern. As long as 151.39 support holds, rise from 114.42 (2020 low) is expected to continue through 159.75 at a later stage. Nevertheless, firm break of 151.39 will confirm medium term topping, and bring lengthier and deeper correction.

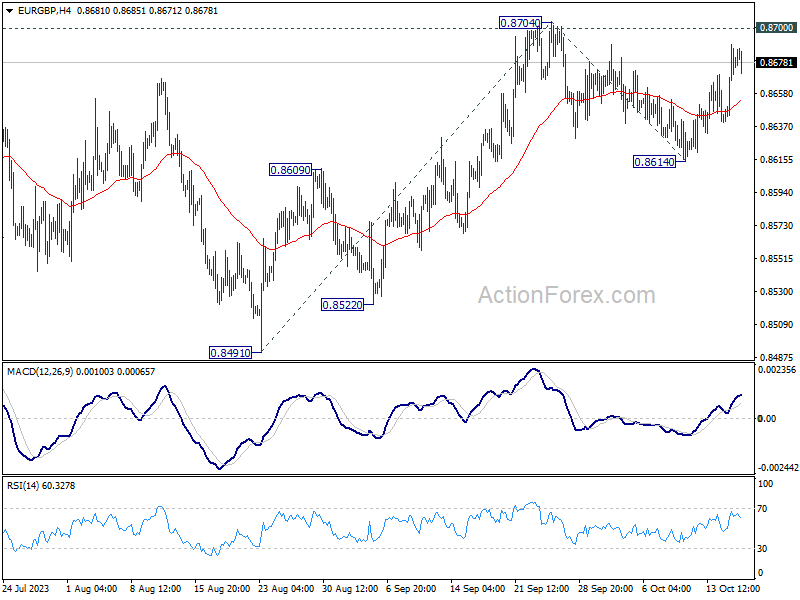

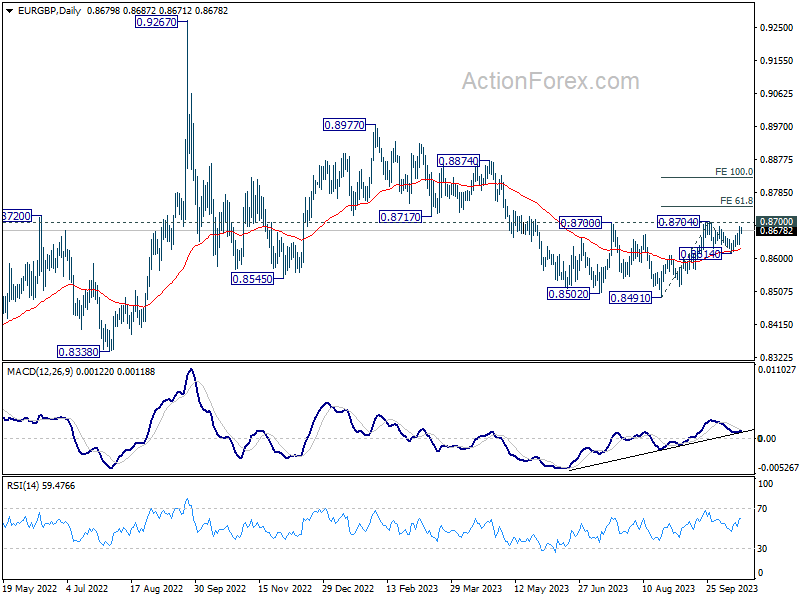

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8651; (P) 0.8671; (R1) 0.8701; More....

Intraday bias in EUR/GBP stays neutral first. On the upside, decisive break of 0.8700/4 resistance will resume the rebound from 0.8491, and carry larger bullish implications. Nevertheless, break of 0.8614 will turn bias to the downside to resume the fall from 0.8704 instead.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Decisive break of 0.8700 resistance will argue that this decline has completed with three waves down to 0.8491. Rise from 0.8491 could then be another leg inside the pattern and targets 0.8977 and above. However, rejection by 0.8700 will keep the down trend alive for another fall through 0.8491 at a later stage.

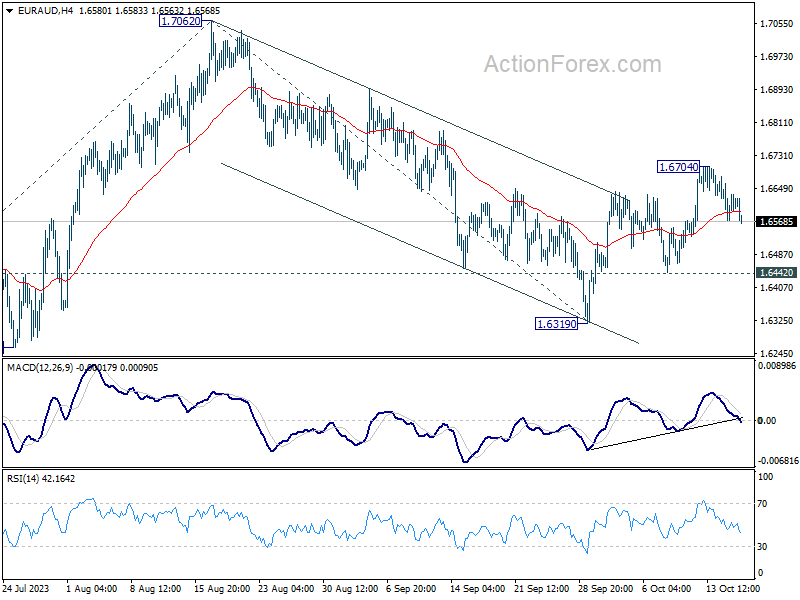

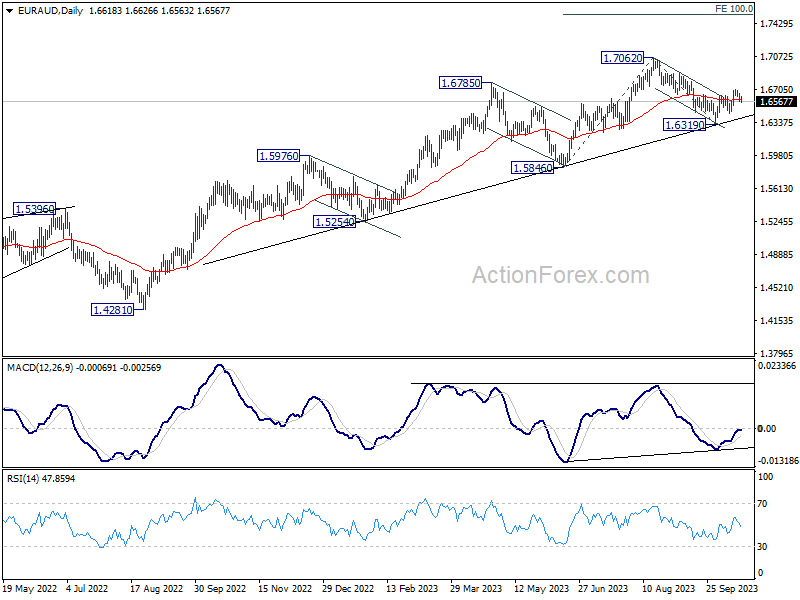

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6568; (P) 1.6620; (R1) 1.6666; More...

Intraday bias in EUR/AUD stays neutral and outlook is unchanged. Correction from 1.7062 should have completed at 1.6319. Above 1.6704 will resume the rise from 1.6319 to retest 1.7062 high. However, firm break of 1.6442 support will dampen this view and turn bias back to the downside for 1.6319 support instead.

In the bigger picture, the strong support from medium term rising trend line indicates that rise from 1.4281 (2022 low) is still in progress. On resumption, next target is 100% projection of 1.5846 to 1.7062 from 1.6319 at 1.7353. In any case, outlook will stay bullish as long as 1.6319 support holds.

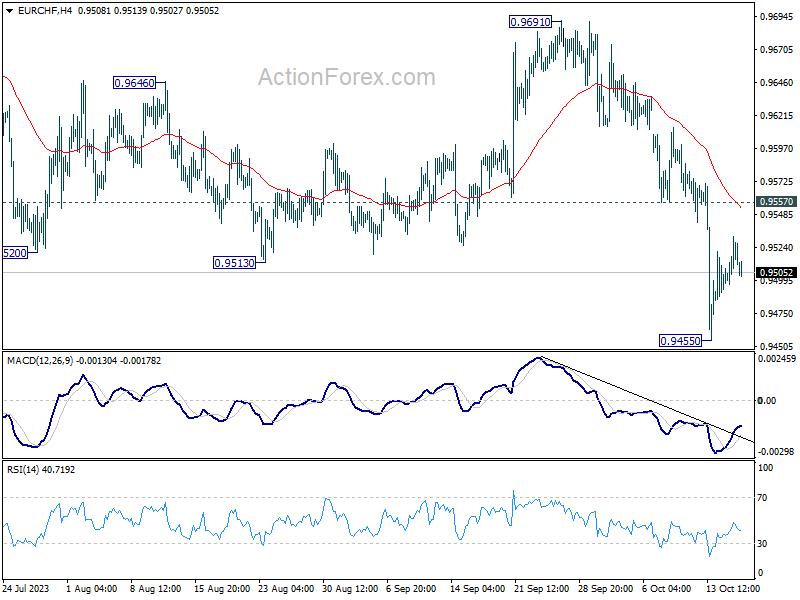

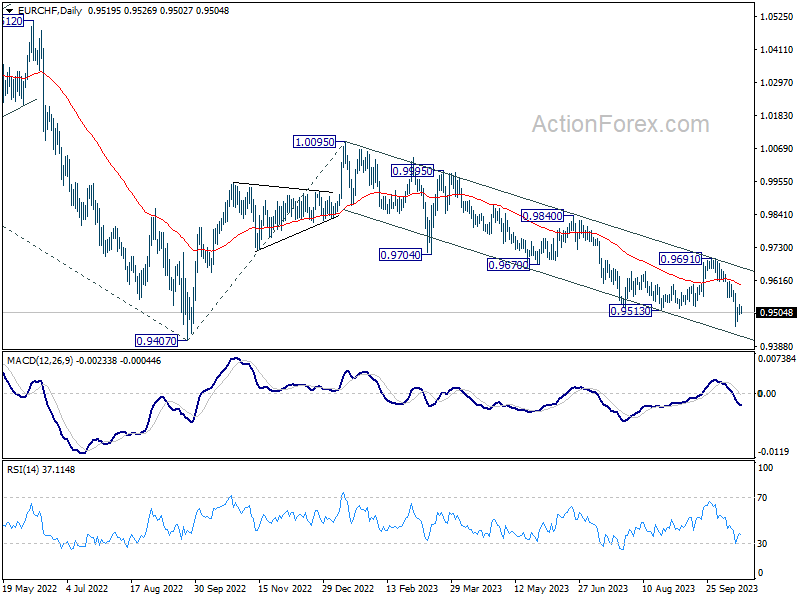

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9503; (P) 0.9518; (R1) 0.9538; More...

EUR/CHF is extending the consolidation form 0.9455 and intraday bias remains neutral. Further decline is expected with 0.9557 resistance intact. Below 0.9455 will resume larger decline from 1.0095 to 0.9407 medium term bottom. Nevertheless, break of 0.9557 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, medium term outlook remains bearish with the cross capped well below falling 55 W EMA (now at 0.9782). Firm break of 0.9407 (2022 low) will confirm resumption of larger down trend from 1.2004 (2018 high). Next target will be 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. On the upside, break of 0.9691 resistance is needed to indicate medium term bottoming. Otherwise, outlook will stay bearish.

EUR/AUD Potential Short-Term Downside Pressure after Upbeat China Data

- China’s Q3 GDP, Retail Sales, and Industrial Production for September beat expectations.

- China’s Country Garden is still at risk of an imminent default as its grace period of overdue bond coupon payments of US$15.4 million expires today.

- The FX market is ignoring the default risk of Country Garden as the offshore yuan (CHN) has continued to trade sideways against the US dollar since 28 September.

- The resilience of CNH against the US dollar has triggered a dissipating US dollar strength movement against CHH’s proxies (AUD & SGD).

China’s trio of key economic data has managed to surpass expectations to the upside where Q3 GDP came in at 4.9% y/y, above consensus estimates of 4/4% but below Q2 print of 6.3% y/y. Growth in retail sales for September rose at the fastest pace in four months; 5.5% y/y accelerated from 4.6% y/y in August and beat expectations of 4.9% y/y.

Industrial production also managed to beat expectations marginally as it grew 4.5% y/y in September, above consensus estimates of 4.3% y/y but unchanged from 4.5% y/y in August.

Overall, the current targeted approach of expansionary fiscal and monetary policies adopted by China’s top policymakers seems to be working at this juncture and has negated the risk of a deflationary spiral triggered by a prolonged property market crisis and weak external demand. Also, a growing hope that China will be able to meet its 2023 official annual GDP growth target of around 5%.

Liquidity crunch is still lingering in China’s property market

However, the coast is not all clear yet to bring out the champagnes for an early celebration as severe liquidity crunch conditions are still lingering in China’s property market where the canary in the coal mine now is Country Garden, the largest private property developer.

Time is running out for Country Garden to restructure its overdue coupon payments of US$15.4 million of a public dollar bond as its grace period expires today, 18 October where a no payment will trigger a default clause. Even if Country Garden manages to doge the “default bullet” today, it still has a slew of overdue coupon payments of dollar bonds where their respective grace periods are expiring soon with the next one on 27 October for overdue coupon payments that amount to US$40 million.

FX market is ignoring the heightened default risk of Country Garden

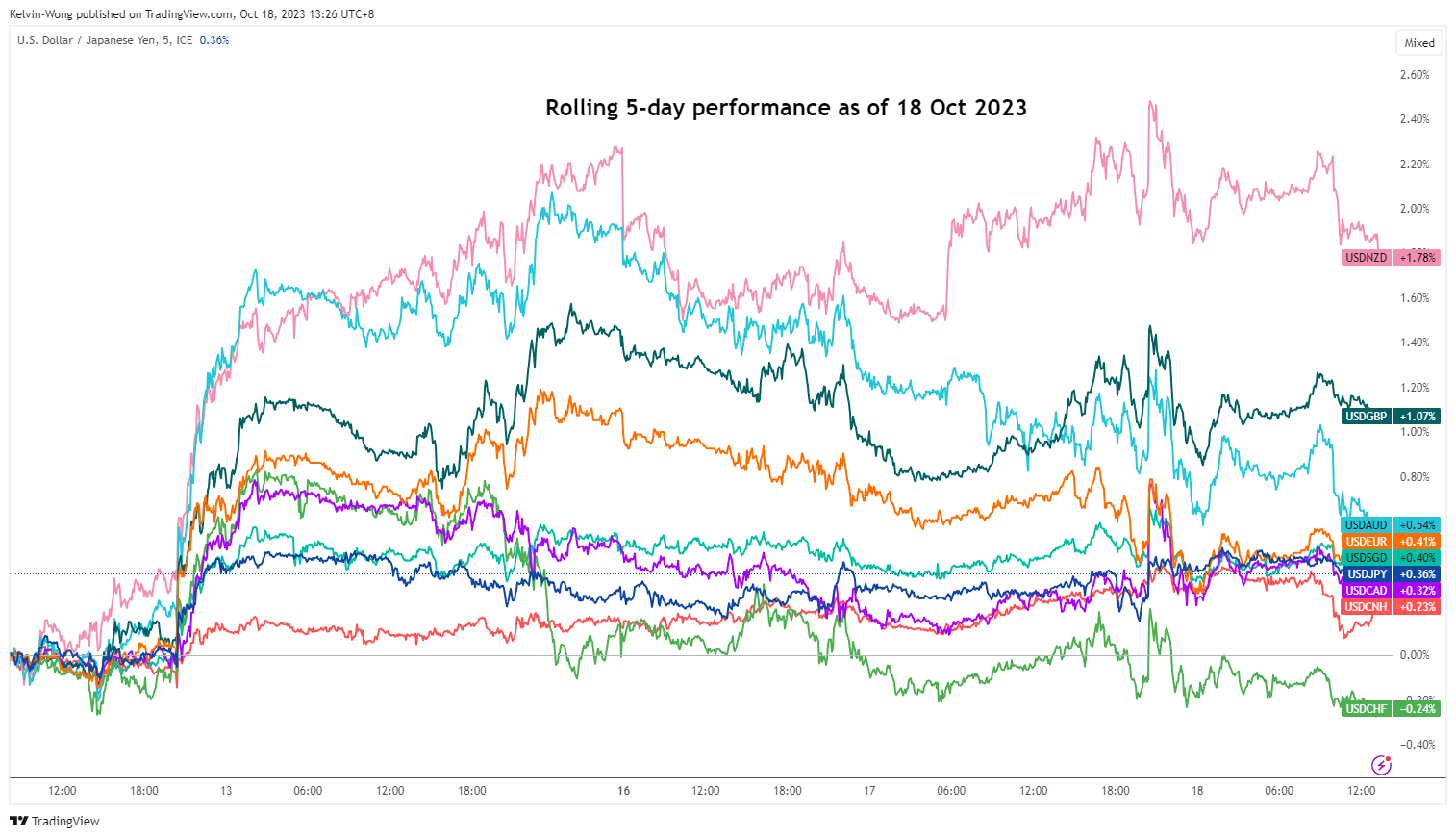

Fig 1: USD major pairs rolling 5-day performance as of 18 Oct 2023 (Source: TradingView, click to enlarge chart)

Interestingly, current short-term price action movements depicted in the foreign exchange market are not pricing in the potential imminent default of Country Garden that can trigger a systemic risk in China and even globally. The offshore yuan (CNH) has been resilient against the recent US strength seen against the European currencies (EUR & GBP). The USD/CNH rate has managed to hold steady below a minor range resistance of 7.3280 since 28 September.

The current bout of sideways movement seen in the USD/CNH has managed to trigger a minor US dollar underperformance against the yuan’s proxies such as the AUD, and SGD. Based on a five-day rolling performance basis as of 18 October 2023, the USD strength against the AUD has dissipated since Tuesday, 17 October, and the USD/AUD has now recorded a gain of just +0.54% at this time of the writing from around +1.25% earlier.

EUR/AUD bearish reaction from 50-day moving average

One of the AUD cross pairs that is being impacted by the current set of rosy China’s key economic data is the EUR/AUD.

In the lens of technical analysis, the current price action movements of EUR/AUD indicate a further potential corrective decline at least in the short term.

Several bearish elements have emerged; the recent +170 pips rebound from its minor swing low of 12 October 2023 has stalled right at the 50-day moving average where the EUR/AUD has been trading below it in the last four weeks.

The 4-hour RSI momentum indicator has staged a momentum bearish breakdown below a parallel ascending support at around the 50 level and has not reached the oversold condition (below 30).

These observations suggest that short-term downside momentum has resurfaced which in turn supports a further potential down move in EUR/AUD.

Watch the near-term support at 1.6550 (also the 20-day moving average) and a break below it may see a further slide to retest the 29 September 2023 swing low area of 1.6360/6320 in the first step.

However, a clearance above the 1.6710 key short-term pivotal resistance invalidates the bearish tone for a squeeze up towards the next intermediate resistance at 1.6890 (minor range top from 25 August/5 September 2023 and the 76.4% Fibonacci retracement of the prior minor short-term downtrend phase from 17 August 2023 high to 29 September 2023 low).

The News Jungle

US retail sales beat expectations, fueled Federal Reserve (Fed) hawks and bets of another rate hike in December – or January – yesterday. The US 2-year yield spiked to a fresh high since 2007, and the 10-year yield spiked above the 4.80% mark regardless of mounting tensions in Gaza – reminding those who seek protection against geopolitical tensions that the US sovereigns’ safety is limited by potentially sharp reaction to economic data, a crowded issuance calendar, the possibility of a further belt-tightening from the Fed and concerns about US deficit in an environment where the US is not only expected to help Ukrainians, but finance the Israeli war in Gaza, as well.

Gold spike above its 200-DMA defying mountains, and the rising US yields. The yellow metal is a solid hedge against risky assets that get smashed by a severe fall in appetite.

Higher yields are also bad news for stock valuations, but what triggered yesterday’s stock selloff was not only a rebound in yields, but also – and mostly - a major slump in US chip stocks. The AI investors’ darling Nvidia took an almost 5% hit yesterday after the US announced that they will bring more sanctions to advanced chip exports to China, to prevent the Chinese from using to improve their military equipment. Intel fell 1.37%, and AMD shed 1.24%.

US President Joe Biden went to Israel to show his support to Israel, which in the meantime bombed a hospital in Gaza and killed at least 500 people. The rising tensions pushed oil to a fresh high since tensions in Gaza started, the barrel of American crude flirted with the $89pb level. I am afraid we will see tensions further escalate in Gaza, and that could send oil prices higher by a big chunk, especially if Iran gets involved in the carnage of the Middle East. The fact that the US oil inventories fell by 4.4mio barrels last week, and the agreement between US and Venezuela to relieve a part of sanctions against the Venezuelan oil are rapidly swept under the rug when things get ugly in the Middle East.

- Last week’s draw in US oil inventories is just a correction of the huge 12-mio barrel fall of the week before.

- Venezuela has the potential to replace the Iranian oil, as it has the world’s largest proven oil reserves and it used to pump around 3-4-mio barrels a day. BUT production fell by 75% since the 1990s peak, as the Venezuelan state oil giant has been severely debilitated due to years of defaults, mismanagement, insufficient investment, sanctions, corruption, and a massive outflow of skilled workers from the nation. As such, Venezuelan oil won’t submerge global market overnight.

And that’s ‘tant mieux’ for oil companies which see their stock prices surge on all this brilliant set of news. Shell hit a record high yesterday in Amsterdam, even though its CEO had to give his speech via a video link, instead of in person at London’s Park Lane Energy Intelligence Forum because a younf lady called Greta Thunberg and her followers came to protest climate damages in front of the venue. Charming Greta got arrested, as big boys of oil cheered the juicy profits. Climate will pay the bill.

Oh, I almost forgot

Bank earnings released yesterday were mixed. Goldman’s profit fell for the 8th straight quarter, by a decent 33%. The stock price fell near the $300 mark. BoFA, on the other hand, topped profit estimates on trading and net interest income. Its shares rebounded 2% from an almost 2-year low. Morgan Stanley will report today, along with Tesla and Netflix.

Some good news

On the economic data front, Chinese growth beat expectations as it came this close to the 5% mark in Q3, retail sales rose more than expected as unemployment fell. On the flip side of the world, inflation in Canada eased, wages in the UK grew slower than expected and but inflation didn’t fall as much as expected. Now, note that the deviation from expectations is minor and the latest update won’t matter for the Bank of England (BoE) expectations, which will certainly keep the interest rates steady at its next meeting. But that will hardly prevent Cable from falling toward 1.20 if Fed doves give in to strong economic data.

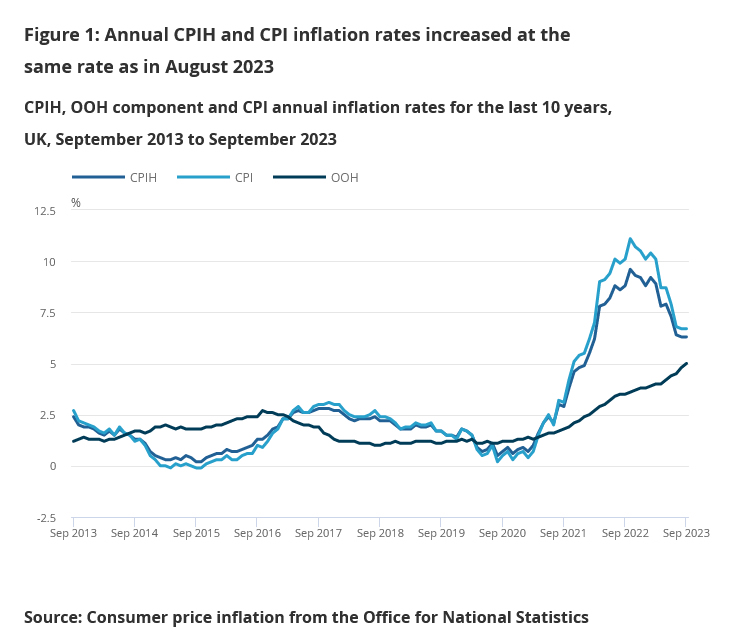

UK CPI unchanged at 6.7% yoy in Sep, services inflation back at 3-decade high

UK CPI was unchanged at 6.7% yoy in September, above expectation of slowing to 6.6% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 6.2% yoy to 6.1% yoy, above expectation of 6.0% yoy.

CPI goods annual rate fell slightly from 6.3% to 6.2%. CPI services annual rate rose from 6.8% to 6.9%, joint highest rate (with May 2023) since March 1992.

On a monthly basis, CPI rose 0.5% mom, above expectation of 0.4% mom, quickly than prior month's 0.3% mom.

Macro Data Surprises to the Upside in US and China

Market movers today

UK September CPI is due for release this morning, consensus expects core inflation to continue moderating to 6.0% in y/y terms after the downside surprise in August.

Final inflation data will also be released for euro area. We expect no major changes to the flash release, but the data will still shed some light on the details of what drove the downtick in core inflation.

A range of Fed speakers will be on the wires today, including Kashkari, Waller, Williams, Bowman and Harker.

Joe Biden will visit Israel today.

Overnight, Australian labour market data is due for release.

The 60 second overview

China: Chinese Q3 GDP beat expectations by growing 1.3% q/q (from 0.5% in Q2, consensus 1.0%). In September, the uptick in growth was driven especially by retail sales (5.5%; from 4.6%) while growth in industrial production (4.5%; from 4.5%) and fixed investments (3.1%; from 3.2%) remained more stable. Overall, it appears that the stimulus measures are finally starting to have an effect on the Chinese economy, which is now set to reach the central government's 5% growth target for 2023. That said, the uncertainty related to the real estate sector will remain a drag for now, with one of China's largest developers, Country Garden, having potentially defaulted on its USD bond coupon payment this morning (see Reuters).

US: Hard US macro data continued the streak of upside surprises yesterday, as retail sales grew by 0.7% in m/m SA in September (August revised higher to 0.8%). While gasoline prices provided a modest lift to sales, even the control group sales (which exclude volatile, car, gasoline, restaurants and building materials) grew by 0.6% m/m (August 0.2%; consensus 0.0%). As Core CPI grew by 0.3% in September, it looks like real consumption volume continued to grow, suggesting that the US economy has remained on a more solid footing than expected. Industrial production also surprised to the upside (0.3%; consensus 0.0%), although the uptick was compensated for by a downward revision to August data (0.0%; from 0.4%). In any case, US yields continued to edge higher yesterday, and while the Fed has communicated that it will most likely remain on hold at the November meeting two weeks from now, the market-implied probability of a final hike in December or January has now reached around 50%. We still stick to our long-held call that the Fed is likely already done hiking despite the recent positive data surprises.

Geopolitics: Tensions seem to be tightening on many fronts, and not least in Israel where Joe Biden is headed for a visit today. In the Nordics, Sweden reported yesterday that it is investigating damage to a telecom cable to Estonia. While the cause remains unknown for now, the timing and physical location of the damage were close to the Balticconnector gas pipeline between Finland and Estonia, which was last week reported to have been damaged likely from the outside (see Reuters). And on US-China relations, Biden administration announced a further tightening in microchip export controls yesterday, targeted at blocking China's access to the most advanced chips used especially for AI solutions (see FT).

Equities: Good news was bad news when retail sales turned out better than expected. Equities were muted as a result, with S&P 500 and Stoxx 600 closing unchanged, off worst levels. As yields moved higher, value cyclicals outperformed (energy, materials, and financials) with rotation out of real estate and tech. The latter was a headwind after confirmation of additional restrictions on US exports on advanced chips from China. US futures are unchanged this morning and Asian markets lower.

FI: Global yields continued to move higher yesterday, following the release of stronger-than-expected US retail sales data. 10Y UST yields rose 13bp to 4.84%, the highest level since 2007, driving a renewed steepening of the 10s2s curve. In line with moves seen over the past month, real rates were the main driver of yesterday's move, as long-term inflation expectations remained relatively unchanged. Markets are pricing in close to 15bp of additional policy tightening in the US until January, while the first full 25bp cut is now seen in June 2024. The sell-off was also visible in European bond markets, with the 10Y Bund yield rising nearly 10bp throughout the day.

FX: In Scandies space, EUR/DKK briefly rose above 7.4620 yesterday and thus broke the recent top from September. EUR/SEK oscillated within 11.51 and 11.56 as the Riksbank hearing provided no news for the markets and risk sentiment soured, where the latter helped push EUR/NOK closer to 11.60, the upper end of the recent range. In majors, EUR/USD moved higher but bounced at 1.059 before spending the Asian session around 1.0575. USD/JPY very briefly dropped below 149 yesterday but was not comfortable and soon tested 150. The CHF continues to trade on a strong note albeit seeing a slight correction from last week with EUR/CHF close to 0.95.

Credit: Yesterday, credit markets continued the cautious sentiment while global rates continued to move upwards across the curves, leaving CDS indices broadly unchanged with iTraxx Main (-0.4bp) at 83.5bp and iTraxx Xover (-0.6bp) at 445bp. In addition, the primary market activity was very subdued as the Q3 earning season kicks in.