Sample Category Title

(FED) Minutes of the Federal Open Market Committee

June 13–14, 2023

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on Tuesday, June 13, 2023, at 10:30 a.m. and continued on Wednesday, June 14, 2023, at 9:00 a.m.1

Attendance

Jerome H. Powell, Chair

John C. Williams, Vice Chair

Michael S. Barr

Michelle W. Bowman

Lisa D. Cook

Austan D. Goolsbee

Patrick Harker

Philip N. Jefferson

Neel Kashkari

Lorie K. Logan

Christopher J. Waller

Thomas I. Barkin, Raphael W. Bostic, Mary C. Daly, and Loretta J. Mester, Alternate Members of the Committee

James Bullard and Susan M. Collins, Presidents of the Federal Reserve Banks of St. Louis and Boston, respectively

Kelly J. Dubbert, Interim President of the Federal Reserve Bank of Kansas City

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Brian J. Bonis, Assistant Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson, Economist

Roc Armenter, James A. Clouse, Brian M. Doyle, Beverly J. Hirtle, Andrea Raffo, Chiara Scotti, and William Wascher, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Jose Acosta, Senior Communications Analyst, Division of Information Technology, Board

Gianni Amisano, Assistant Director, Division of Research and Statistics, Board

Philippe Andrade, Senior Economist and Policy Advisor, Federal Reserve Bank of Boston

Alyssa Arute,2 Manager, Division of Reserve Bank Operations and Payment Systems, Board

Penelope A. Beattie,3 Section Chief, Office of the Secretary, Board

Carol C. Bertaut, Senior Adviser, Division of International Finance, Board

Jennifer J. Burns, Deputy Director, Division of Supervision and Regulation, Board

Marco Cagetti, Assistant Director, Division of Research and Statistics, Board

Mark A. Carlson, Adviser, Division of Monetary Affairs, Board

Juan C. Climent, Special Adviser to the Board, Division of Board Members, Board

Daniel M. Covitz, Deputy Director, Division of Research and Statistics, Board

Stephanie E. Curcuru, Deputy Director, Division of International Finance, Board

Ahmet Degerli, Economist, Division of Monetary Affairs, Board

Cynthia L. Doniger, Principal Economist, Division of Monetary Affairs, Board

Rochelle M. Edge, Deputy Director, Division of Monetary Affairs, Board

Jon Faust, Senior Special Adviser to the Chair, Division of Board Members, Board

Erin E. Ferris, Principal Economist, Division of Monetary Affairs, Board

Jonas Fisher, Senior Vice President, Federal Reserve Bank of Chicago

Glenn Follette, Associate Director, Division of Research and Statistics, Board

Jennifer Gallagher, Assistant to the Board, Division of Board Members, Board

Carlos Garriga, Senior Vice President, Federal Reserve Bank of St. Louis

David Glancy,4 Principal Economist, Division of Monetary Affairs, Board

Christopher J. Gust, Associate Director, Division of Monetary Affairs, Board

Valerie S. Hinojosa, Section Chief, Division of Monetary Affairs, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Michael T. Kiley, Deputy Director, Division of Financial Stability, Board

Don H. Kim,2 Senior Adviser, Division of Monetary Affairs, Board

Edward S. Knotek II, Senior Vice President, Federal Reserve Bank of Cleveland

Andreas Lehnert, Director, Division of Financial Stability, Board

Paul Lengermann, Assistant Director, Division of Research and Statistics, Board

Kurt F. Lewis, Special Adviser to the Board, Division of Board Members, Board

Geng Li, Assistant Director, Division of Research and Statistics, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

Brent Meyer, Assistant Vice President, Federal Reserve Bank of Atlanta

Bernardo C. Morais, Principal Economist, Division of International Finance, Board

Michelle M. Neal, Head of Markets, Federal Reserve Bank of New York

Edward Nelson, Senior Adviser, Division of Monetary Affairs, Board

Nicolas Petrosky-Nadeau, Vice President, Federal Reserve Bank of San Francisco

Achilles Sangster II, Senior Information Manager, Division of Monetary Affairs, Board

Zeynep Senyuz, Deputy Associate Director, Division of Monetary Affairs, Board

Margie Shanks, Deputy Secretary, Office of the Secretary, Board

Nitish Ranjan Sinha, Special Adviser to the Board, Division of Board Members, Board

A. Lee Smith, Senior Vice President, Federal Reserve Bank of Kansas City

Hiroatsu Tanaka,5 Senior Economist, Division of Monetary Affairs, Board

Mary H. Tian, Group Manager, Division of Monetary Affairs, Board

Robert L. Triplett III, First Vice President, Federal Reserve Bank of Dallas

Clara Vega, Special Adviser to the Board, Division of Board Members, Board

Daniel J. Vine, Principal Economist, Division of Research and Statistics, Board

Jeffrey D. Walker,2 Associate Director, Division of Reserve Bank Operations and Payment Systems, Board

Fabian Winkler, Principal Economist, Division of Monetary Affairs, Board

Alexander L. Wolman, Vice President, Federal Reserve Bank of Richmond

Paul R. Wood, Special Adviser to the Board, Division of Board Members, Board

Rebecca Zarutskie, Special Adviser to the Board, Division of Board Members, Board

Developments in Financial Markets and Open Market Operations

The manager turned first to a review of developments in financial markets. Policy-sensitive rates increased over the intermeeting period, reflecting indications of continued resilience in the economy, persistently elevated core inflation, and reduced downside tail risks following the resolution of the debt limit. The shift in policy expectations contributed significantly to higher Treasury yields. The increase in nominal yields primarily reflected higher real rates rather than inflation compensation. Broad equity prices rose, although the outperformance was concentrated in a handful of companies with a large market capitalization. Cyclical sectors fared better than sectors that tend to appreciate in a downturn, suggesting some reduced investor concern about downside risks to growth. Investor sentiment about the banking sector improved as perceived tail risks regarding regional banks appeared to have receded. Equity prices for regional banks rose over the intermeeting period but were still well below early March levels. Financial conditions indexes were roughly unchanged, as higher rates and a stronger dollar were offset by higher equity prices and narrower credit spreads.

The vast majority of respondents to the Open Market Desk's Surveys of Primary Dealers and Market Participants expected no rate change at this meeting. While the median path from the surveys pointed to no rate changes through early 2024, there was significant dispersion across respondents, and respondents saw a clear probability of additional tightening at coming meetings. Respondents' average probability distribution for the level of the peak policy rate shifted higher since the May meeting and respondents on average assigned about 60 percent probability to the peak being above the current target range. The market-implied path for the policy rate continued to show some decline this year but less so than it had in recent months. Measures of uncertainty about the path of the policy rate derived from options remained very elevated, though they came down some over the intermeeting period.

Desk survey respondents still saw a recession occurring in the near term as quite likely, but the expected timing was again pushed later, as economic data pointed to the continued resilience of economic activity. Overall, respondents generally continued to expect that any downturn would be neither deep nor prolonged. With regard to inflation expectations, respondents marked up their projections for quarterly core personal consumption expenditures (PCE) inflation in the second and third quarters of this year, while projections for later quarters were little changed.

The manager then turned to money market developments and policy implementation. The median respondent to the Desk surveys expected the three-month bill yield to increase slightly relative to the similar-maturity overnight index swap (OIS) rate and to remain above it into the fourth quarter. This expectation likely reflected a combination of rising net supply of bills as part of the Treasury Department's plan to rebuild the Treasury General Account (TGA) following the resolution of the debt limit and expectations for healthy investor demand for bills. The overnight reverse repurchase agreement (ON RRP) facility, which continued to support effective policy implementation and control over the federal funds rate, saw somewhat lower participation since the resolution of the debt limit, consistent with the historical experience that ON RRP participation is typically responsive to changes in money market conditions. The median respondent to the Desk's Survey of Primary Dealers expected ON RRP participation to trend lower over the rest of this year. The staff assessed that the replenishment of the TGA and the ongoing balance sheet runoff, among other factors, were likely to subtract from reserves more than the decline in ON RRP participation would add to them. On net, the staff judged that reserves at the end of the year were likely to remain abundant. Uncertainty surrounding the outlooks for both reserves and ON RRP participation was substantial.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information available at the time of the June 13–14 meeting suggested that real gross domestic product (GDP) was expanding at a modest pace in the second quarter. Labor market conditions remained tight in recent months, as job gains were robust and the unemployment rate was low. Consumer price inflation—as measured by the 12-month percent change in the price index for PCE—continued to be elevated in April.

Labor market conditions remained tight in April and May. Total nonfarm payroll employment increased at a robust pace during those two months. The unemployment rate edged up, on net, but was still at a low level of 3.7 percent in May. On balance, the unemployment rate for African Americans moved up to 5.6 percent, while the jobless rate for Hispanics moved down to 4.0 percent. In aggregate, the labor force participation rate held steady in April and May, and the employment-to-population ratio ticked down. The private-sector job openings rate in April—as measured by the Job Openings and Labor Turnover Survey—was unchanged from its relatively high first-quarter average, though it was lower than a year earlier.

Recent measures of nominal wage growth continued to be elevated, although lower than their highs last year. Over the 12 months ending in May, average hourly earnings for all employees increased 4.3 percent, below its peak of 5.9 percent early last year. Over the year ending in the first quarter, compensation per hour in the business sector increased 3.2 percent, down from 5.5 percent a year earlier.

Consumer price inflation remained elevated. Total PCE price inflation had eased since the middle of last year, reflecting declines in consumer energy prices and softening consumer food price inflation, but recent readings for core PCE price inflation—which excludes changes in consumer energy prices and most consumer food prices and usually provides a better signal about future inflation than the more volatile total inflation measure—were little changed. Total PCE price inflation was 4.4 percent over the 12 months ending in April, and core PCE price inflation was 4.7 percent—the same as the 12-month percent change recorded in January. In May, the 12-month change in the consumer price index (CPI) was 4.0 percent, and core CPI inflation was 5.3 percent—only slightly below its January reading. The trimmed mean measure of 12‑month PCE price inflation constructed by the Federal Reserve Bank of Dallas was 4.8 percent in April. Survey-based measures of longer-term inflation expectations in May from the University of Michigan Surveys of Consumers and the Federal Reserve Bank of New York's Survey of Consumer Expectations remained within the range of their values reported in the decade before the pandemic; near-term measures of inflation expectations from these surveys moved down in May and continued to be below their peaks seen last year.

Real GDP appeared to be increasing modestly in the second quarter following its stronger first-quarter gain. Private domestic final purchases (PDFP)—which includes PCE, residential investment, and business fixed investment and often provides a better signal of underlying economic momentum than GDP—looked to be expanding more slowly in the second quarter than its robust first-quarter pace. For the first half as a whole, PDFP growth seemed to be more resilient than in the second half of last year.

The annual revisions to international trade statistics suggested that net exports contributed positively to U.S. real GDP growth in the first quarter, with real exports rebounding more strongly than real imports following their fourth-quarter declines. In April, however, the nominal trade deficit widened notably, as nominal exports decreased and nominal imports rose further.

Foreign economic growth rebounded in the first quarter, reflecting in part the reopening of China's economy from its COVID-19-related shutdowns and strong services-sector activity in other Asian countries, Canada, and Mexico. In the euro area, however, real GDP contracted modestly for a second consecutive quarter amid a pullback in consumer spending. Indicators pointed to a step-down in the pace of foreign economic growth in the second quarter, with the impetus from China's reopening dissipating and global manufacturing activity remaining weak.

Global prices for energy and agricultural commodities were little changed, on net, over the intermeeting period, while prices for metals fell further. Declines in retail energy prices since the beginning of the year contributed to a notable easing in headline consumer price inflation in the foreign economies. By contrast, core inflation had yet to materially decline from its recent highs in many economies. In this context, and with tight labor market conditions, foreign central banks underscored the need to raise policy rates further or hold them at sufficiently restrictive levels to bring inflation back to their respective targets and be well positioned in case inflation failed to decline as expected.

Staff Review of the Financial Situation

Over the intermeeting period, market participants appeared to interpret incoming data as signaling, on balance, more resilience in economic activity than previously assumed and viewed communications from FOMC participants overall as pointing to a tighter path for policy than expected. As a result, Treasury yields and the expected future path for the federal funds rate shifted upward significantly. Meanwhile, broad equity prices also increased notably. Financing conditions remained moderately restrictive, but credit availability generally remained solid.

The expected path of the policy rate implied by market quotes moved up notably over the intermeeting period. A straight read of federal funds futures rates suggested that market participants expected that the federal funds rate would be roughly flat over the course of the rest of this year. The year-end expected rate was about 70 basis points higher than the year-end expectation before the May FOMC meeting. Beyond this year, the policy rate path implied by OIS quotes also moved up, to about 3.7 percent by the end of 2024. Similarly, nominal Treasury yields rose significantly. The rise in nominal yields mostly reflected an increase in real yields, as measures of inflation compensation were little changed, on net, amid somewhat mixed news on inflation. Measures of uncertainty about the path of interest rates remained very elevated by historical standards.

The S&P 500 stock price index increased sizably, on net, over the intermeeting period, led by technology-related stocks. The VIX—the one-month option-implied volatility on the S&P 500 index—edged down, on balance, and ended the period near the 30th percentile of its historical distribution. Bank equity price indexes moved up notably, on net, over the intermeeting period. Stock prices for large banks were only somewhat below their levels before the failure of Silicon Valley Bank (SVB), while those for regional banks remained below their levels in early March.

Market-based policy rate expectations rose notably in most advanced foreign economies, as core inflation data surprised to the upside in some countries and central bank communications were perceived as pointing to more restrictive policy than expected. Notwithstanding the rise in global yields, foreign equity prices, credit spreads, and risk sentiment in foreign markets were little changed over the intermeeting period. The staff's trade-weighted broad dollar index was also little changed, on net, but the exchange value of the dollar appreciated significantly against the Chinese renminbi amid increased investor concerns over China's economic growth prospects.

Conditions in overnight bank funding and repurchase agreement markets remained generally stable over the intermeeting period. The 25 basis point increase in administered rates at the May FOMC meeting fully passed through to overnight money market rates. Spreads and issuance volumes in unsecured short-term funding markets stayed within their typical ranges. In May, yields of Treasury bills maturing in June and thus potentially affected by the federal debt limit rose sharply before largely retracing those increases after an agreement was reached to suspend the debt limit.

In domestic credit markets, borrowing costs for businesses, households, and municipalities increased notably over the intermeeting period. Interest rates on newly originated bank loans to businesses and households in the first quarter rose further above their peaks from the previous tightening cycle, and yields on leveraged loans also rose, reaching levels close to their peak at the onset of the pandemic. Rates also moved up on a broad array of fixed-income securities, including investment- and speculative-grade corporate bonds, municipal bonds, both agency and non-agency commercial mortgage-backed securities (CMBS), and agency residential mortgage-backed securities. The increases in yields on these instruments over the intermeeting period were generally in line with, or less than, the changes in their Treasury benchmarks. Small businesses and households saw continued increases in their borrowing costs. Rates on 30-year conforming residential mortgages stepped up, broadly in line with increases in comparable-duration Treasury yields. Interest rates on credit card offers continued to rise through April, and auto loan interest rates moved sideways during the intermeeting period. Both credit card and auto loan interest rates stood at, or near, their highest levels since the Global Financial Crisis.

Banks' ability to fund loans to businesses and consumers appeared to have stabilized in recent weeks but remained somewhat strained relative to before the closure of SVB in March. Although banks continued to experience outflows of core deposits, the pace of those outflows moderated substantially relative to March, suggesting some easing of bank funding pressures. Banks also continued to attract inflows of large time deposits, reflecting higher interest rates on new certificates of deposit. Total bank assets were little changed, on net, over the intermeeting period.

In capital markets, funding had generally been resilient. Issuance of nonfinancial investment-grade corporate bonds rose at a robust pace in May after slowing in April, partly due to the "earnings blackout" period. Speculative-grade issuance increased in late April and in May but remained subdued by historical standards. Gross issuance of municipal bonds was solid in April and May.

Conditions in the leveraged loan and CMBS markets were somewhat more strained. Leveraged loan issuance remained subdued, reflecting weak investor demand amid concerns over the credit worthiness of borrowers. Both agency and non-agency CMBS issuance volumes were low in May relative to pre-pandemic levels. In addition, for small businesses, credit availability continued to show signs of tightening.

Credit remained easily available in the residential mortgage market for high credit score borrowers who met standard conforming loan criteria. For borrowers with lower scores, credit availability tightened slightly in April but remained close to pre-pandemic levels. In consumer credit markets, conditions stayed generally accommodative, with credit available for most borrowers.

The credit quality of most businesses and households remained solid, although market participants appeared to expect some deterioration in the coming quarters, which could weaken lender balance sheets and possibly weigh on credit availability. A measure of the May CMBS delinquency rate showed about a 50 basis point increase, driven by a sharp rise in the delinquency rate for office buildings.

Staff Economic Outlook

The economic forecast prepared by the staff for the June FOMC meeting continued to assume that the effects of the expected further tightening in bank credit conditions, amid already tight financial conditions, would lead to a mild recession starting later this year, followed by a moderately paced recovery. Real GDP was projected to decelerate in the current quarter and the next one before declining modestly in both the fourth quarter of this year and first quarter of next year. Real GDP growth over 2024 and 2025 was projected to be below the staff's estimate of potential output growth. The unemployment rate was forecast to increase this year, peak next year, and remain near that level through 2025. Current tight resource utilization in both product and labor markets was forecast to ease, with the level of real output moving below the staff's estimate of potential output in 2025 and the unemployment rate rising above the staff's estimate of its natural rate at that time.

The staff's inflation forecast was little revised relative to the previous projection, and supply–demand imbalances in both goods markets and labor markets were still judged to be easing only slowly. On a four-quarter change basis, total PCE price inflation was projected to be 3.0 percent this year, with core inflation at 3.7 percent. Core goods inflation was forecast to move down further this year and then remain subdued. Housing services inflation was considered to have about peaked and was expected to move down over the rest of the year. Core nonhousing services inflation was projected to slow gradually as nominal wage growth eased further. Reflecting the effects of the easing in resource utilization over the projection, core inflation was forecast to slow through next year but remain moderately above 2 percent. With expected declines in consumer energy prices and further moderation in food price inflation, total inflation was projected to run below core inflation this year and the next. In 2025, both total and core PCE price inflation were expected to be close to 2 percent.

The staff continued to judge that uncertainty around the baseline projection was considerable and still viewed the risks as being influenced importantly by the potential macroeconomic implications of banking-sector developments, which could end up being more, or less, negative than assumed in the baseline. Given the continued strength in labor market conditions and the resilience of consumer spending, however, the staff saw the possibility of the economy continuing to grow slowly and avoiding a downturn as almost as likely as the mild‑recession baseline. On balance, the staff saw the risks around the baseline inflation forecast as tilted to the upside, as economic scenarios with higher inflation appeared more likely than scenarios with lower inflation and because inflation could continue to be more persistent than expected and inflation expectations could become unanchored after a long period of elevated inflation.

Participants' Views on Current Conditions and the Economic Outlook

In conjunction with this FOMC meeting, participants submitted their projections of the most likely outcomes for real GDP growth, the unemployment rate, and inflation for each year from 2023 through 2025 and over the longer run. The projections were based on their individual assessments of appropriate monetary policy, including the path of the federal funds rate. The longer-run projections represented each participant's assessment of the rate to which each variable would be expected to converge, over time, under appropriate monetary policy and in the absence of further shocks to the economy. A Summary of Economic Projections (SEP) was released to the public following the conclusion of the meeting.

In their discussion of current economic conditions, participants noted that economic activity had continued to expand at a modest pace. Nonetheless, job gains had been robust in recent months, and the unemployment rate had remained low. Inflation remained elevated. Participants agreed that the U.S. banking system was sound and resilient. They commented that tighter credit conditions for households and businesses were likely to weigh on economic activity, hiring, and inflation. However, participants agreed that the extent of these effects remained uncertain. Against this background, participants concurred that they remained highly attentive to inflation risks.

In assessing the economic outlook, most participants noted that real GDP growth had been resilient in recent quarters. Participants generally judged that growth would be subdued over the remainder of this year. They assessed that the cumulative tightening of monetary policy over the past year had contributed significantly to more restrictive financial conditions and lower demand in the most interest rate sensitive sectors of the economy, especially housing and business investment. Participants also acknowledged uncertainty about the lags with which monetary policy affects the economy and discussed the extent to which the full effects of monetary tightening on the economy had been realized. While total inflation had moderated over the past year, core inflation had not shown a sustained easing since the beginning of the year. With inflation well above the Committee's longer-run 2 percent objective, participants expected that a period of below-trend growth in real GDP and some softening in labor market conditions would be needed to bring aggregate supply and aggregate demand into better balance and reduce inflationary pressures sufficiently to return inflation to 2 percent over time.

Participants generally noted that banking stresses had receded and conditions in the banking sector were much improved since early March. Participants generally continued to judge that a tightening in credit conditions spurred by banking-sector stress earlier in the year would likely weigh further on economic activity, but the extent remained uncertain. Several participants mentioned that credit conditions had not appeared to have tightened significantly beyond what would be expected in response to the monetary policy actions taken since early last year. Some participants judged that it was still too early to assess with confidence the eventual effects of tighter bank credit conditions on economic activity and noted that it would be important to monitor closely the potential effects of banking-sector developments on credit conditions and economic activity.

In their discussion of the household sector, participants generally noted that consumer spending so far this year had been stronger than expected. Several participants noted that aggregate household wealth remained high, as equity and home prices had not declined much from their recent highs. A few participants mentioned that while, overall, the household sector still retained much of the excess savings it had accumulated during the pandemic, there were signs that consumers were facing increasingly tighter budget constraints, given high inflation and, especially for low-income households, depleted savings.

Regarding the business sector, various participants said that reports from their contacts were mixed, with some pointing to softening economic conditions and others indicating greater-than-expected strength. Many participants noted that developments in the banking sector appeared to have had only a modest effect so far on credit availability for firms. Some participants remarked that the effect of high interest rates on the housing sector appeared to be bottoming out, with home sales, builder sentiment, and new construction all having improved a little since the start of the year.

In their discussion of economic activity, several participants pointed out that recent GDP readings had been stronger than expected earlier in the year, while gross domestic income (GDI) readings had been weak. Of those who noted the discrepancy between GDP and GDI, most suggested that economic momentum may not be as strong as indicated by the GDP readings. In discussing that possibility, a couple of these participants also cited the recent subdued growth in aggregate hours worked.

Participants noted that labor market conditions remained very tight, with robust payroll gains and the unemployment rate still near historically low levels. Nevertheless, they noted some signs that supply and demand in the labor market were coming into better balance, with the prime-age labor force participation rate moving up in recent months and further reductions in rates of job openings and quits, and declines in average weekly hours. A couple of participants conveyed that they heard at a recent Fed Listens event that, in various parts of the country, the lack of affordable housing in the area was preventing some lower-income workers from relocating to accept jobs. Similarly, a few participants noted that their District contacts reported less difficulty in hiring and retaining workers, lower turnover rates, and some layoffs. Some participants pointed out that payroll gains had remained robust but noted that some other measures of employment—such as those based on the Bureau of Labor Statistics' household survey, the Quarterly Census of Employment and Wages, or the Board staff's measure of private employment using data from the payroll processing firm ADP—suggested that job growth may have been weaker than indicated by payroll employment. Participants anticipated that employment growth would likely slow further, consistent with their projections of below-trend economic growth. Participants noted that nominal wage growth had shown signs of easing but observed that it was still running at a pace that, given current estimates of trend productivity growth, was above what would be consistent over the longer run with the Committee's 2 percent inflation objective. Participants expected supply and demand conditions in the labor market to come into better balance over time, easing pressures on wages and prices.

Participants agreed that inflation was unacceptably high and noted that the data, including the CPI for May, indicated that declines in inflation had been slower than they had expected. Participants observed that although core goods inflation had moderated since the middle of last year, it had slowed less rapidly than expected in recent months, despite data and reports from business contacts indicating that supply chain constraints had continued to ease. Some participants noted the recent moderation in housing services inflation and expected this trend to continue. However, a few participants pointed to upside risks to the outlook for housing services inflation associated with near-record low inventories of homes for sale, solid housing demand, and less-than-expected deceleration recently in measures of rents for leases signed by new tenants. Additionally, some participants remarked that core nonhousing services inflation had shown few signs of slowing in the past few months. Several participants noted that longer-term measures of inflation expectations from surveys of households and businesses remained well anchored. Participants emphasized that, with appropriate firming of monetary policy, well-anchored longer-term inflation expectations would support a return of inflation to the Committee's 2 percent longer-run goal over time.

Participants generally noted a high degree of uncertainty regarding the cumulative effects on the economy from both already-enacted monetary policy tightening and the potential additional tightening in credit conditions stemming from recent banking-sector developments. Participants noted that the full effects of monetary tightening had likely yet to be observed, though several highlighted the possibility that much of the effect of past monetary policy tightening may have already been realized. Regarding downside risks to economic activity, participants noted the possibility that the cumulative and rapid tightening of monetary policy would eventually affect economic activity more than expected, and that the additional effects of the tightening of bank credit conditions could prove more substantial than anticipated. Regarding risks to inflation, with inflation remaining well above the Committee's longer-run goal, some participants mentioned the possibility that longer-term inflation expectations could become unanchored, particularly in light of stronger-than-expected consumer demand and a still-tight labor market. Several participants cited the possibility of delayed effects of tighter credit conditions potentially contributing to a slowdown in economic activity that reduces inflationary pressures.

In their consideration of appropriate monetary policy actions at this meeting, participants concurred that while inflation had moderated since the middle of 2022, it remained well above the Committee's longer-run goal of 2 percent. Economic activity had continued to expand at a modest pace. The labor market remained very tight, with robust job gains in recent months and the unemployment rate still low, but there were some signs that supply and demand in the labor market were coming into better balance. The economy was facing headwinds from tighter credit conditions, including higher interest rates, for households and businesses, which would likely weigh on economic activity, hiring, and inflation, although the extent of these effect remained uncertain. Against this backdrop, and in consideration of the significant cumulative tightening in the stance of monetary policy and the lags with which policy affects economic activity and inflation, almost all participants judged it appropriate or acceptable to maintain the target range for the federal funds rate at 5 to 5-1/4 percent at this meeting. Most of these participants observed that leaving the target range unchanged at this meeting would allow them more time to assess the economy's progress toward the Committee's goals of maximum employment and price stability. Some participants indicated that they favored raising the target range for the federal funds rate 25 basis points at this meeting or that they could have supported such a proposal. The participants favoring a 25 basis point increase noted that the labor market remained very tight, momentum in economic activity had been stronger than earlier anticipated, and there were few clear signs that inflation was on a path to return to the Committee's 2 percent objective over time. All participants agreed that it was appropriate to continue the process of reducing the Federal Reserve's securities holdings, as described in its previously announced Plans for Reducing the Size of the Federal Reserve's Balance Sheet.

In discussing the policy outlook, all participants continued to anticipate that, with inflation still well above the Committee's 2 percent goal and the labor market remaining very tight, maintaining a restrictive stance for monetary policy would be appropriate to achieve the Committee's objectives. Almost all participants noted that in their economic projections that they judged that additional increases in the target federal funds rate during 2023 would be appropriate. Most participants observed that uncertainty about the outlook for the economy and inflation remained elevated and that additional information would be valuable for considering the appropriate stance of monetary policy. Many also noted that, after rapidly tightening the stance of monetary policy last year, the Committee had slowed the pace of tightening and that a further moderation in the pace of policy firming was appropriate in order to provide additional time to observe the effects of cumulative tightening and assess their implications for policy. Participants agreed that their policy decisions at every meeting would continue to be based on the totality of incoming information and its implications for the economic outlook as well as the balance of risks. They also emphasized the importance of communicating to the public their data-dependent approach. Most participants observed that postmeeting communications, including the SEP, would help clarify their assessment regarding the stance of monetary policy that is likely to be appropriate to bring inflation down to 2 percent over time.

Participants also discussed several risk-management considerations that could bear on future policy decisions. Almost all participants stated that, with inflation still well above the Committee's longer-run goal and the labor market remaining tight, upside risks to the inflation outlook or the possibility that persistently high inflation might cause inflation expectations to become unanchored remained key factors shaping the policy outlook. Even though economic activity had been resilient recently and that the labor market remained strong, some participants commented that there continued to be downside risks to economic growth and upside risks to unemployment. Despite the receding of the stresses in the banking sector, some participants commented that it would be important to monitor whether developments in the banking sector lead to further tightening of credit conditions and weigh on economic activity. Some participants noted concerns about the potential risks stemming from weakness in commercial real estate.

A number of participants observed that the resolution of the federal government debt limit had removed one source of significant uncertainty for the economic outlook. A few participants noted that there could be some upward pressure on money market rates in the near term as the Treasury issued more bills to meet expenditures and return the balance in the TGA to the Treasury's preferred level. Those participants observed that upward pressure on money market rates relative to the rate offered on the ON RRP facility could lead to a decline in usage of the facility.

Committee Policy Actions

In their discussion of monetary policy for this meeting, members agreed that economic activity had continued to expand at a modest pace. They also concurred that job gains had been robust in recent months, and the unemployment rate had remained low. Inflation had remained elevated.

Members concurred that the U.S. banking system was sound and resilient. They also agreed that tighter credit conditions for households and businesses were likely to weigh on economic activity, hiring, and inflation, but that the extent of these effects was uncertain. Members also concurred that they remained highly attentive to inflation risks.

Members agreed that the Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the members agreed to maintain the target range for the federal funds rate at 5 to 5-1/4 percent. Members agreed that holding the target range steady at this meeting allowed the Committee to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, members concurred that they will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, members agreed that the Committee will continue to reduce the Federal Reserve's holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. All members affirmed that they are strongly committed to returning inflation to their 2 percent objective.

Members agreed that, in assessing the appropriate stance of monetary policy, they would continue to monitor the implications of incoming information for the economic outlook. They would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. Members also agreed that their assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective June 15, 2023, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 5 to 5-1/4 percent.

- Conduct standing overnight repurchase agreement operations with a minimum bid rate of 5.25 percent and with an aggregate operation limit of $500 billion.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 5.05 percent and with a per-counterparty limit of $160 billion per day.

- Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $60 billion per month. Redeem Treasury coupon securities up to this monthly cap and Treasury bills to the extent that coupon principal payments are less than the monthly cap.

- Reinvest into agency mortgage-backed securities (MBS) the amount of principal payments from the Federal Reserve's holdings of agency debt and agency MBS received in each calendar month that exceeds a cap of $35 billion per month.

- Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons.

- Engage in dollar roll and coupon swap transactions as necessary to facilitate settlement of the Federal Reserve's agency MBS transactions."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"Recent indicators suggest that economic activity has continued to expand at a modest pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5 to 5-1/4 percent. Holding the target range steady at this meeting allows the Committee to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments."

Voting for this action: Jerome H. Powell, John C. Williams, Michael S. Barr, Michelle W. Bowman, Lisa D. Cook, Austan D. Goolsbee, Patrick Harker, Philip N. Jefferson, Neel Kashkari, Lorie K. Logan, and Christopher J. Waller.

Voting against this action: None.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board voted unanimously to maintain the interest rate paid on reserve balances at 5.15 percent, effective June 15, 2023. The Board also voted unanimously to approve the establishment of the primary credit rate at the existing level of 5.25 percent.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, July 25–26, 2023. The meeting adjourned at 10:20 a.m. on June 14, 2023.

Notation Vote

By notation vote completed on May 23, 2023, the Committee unanimously approved the minutes of the Committee meeting held on May 2–3, 2023.

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Attended through the discussion of developments in financial markets and open market operations. Return to text

3. Attended through the discussion of the economic and financial situation and all of Wednesday's session. Return to text

4. Attended Tuesday's session only. Return to text

5. Attended from the discussion of the economic and financial situation through the end of Tuesday's session. Return to text

Sunset Market Commentary

Markets

With markets awaiting the restart of US trading, the China Caixin services PMI confirmed recent disappointing data, pointing to a lackluster recovery in the Chinese economy. This put markets in a mild risk-off modus that deepened throughout the European session. According to the ECB monthly consumer expectations survey, consumers saw inflationary pressures easing. Perceived inflation over the previous 12 months in May decreased to 8.0% from 8.9%. Median inflation expectations for the next 12 months also eased slightly from 4.1% to 3.9%. Expected inflation 3 years ahead was unchanged at 2.5%. Consumers also turned more cautious on nominal spending in a context of a mild recession (growth for the next year expected at -0.7%). At the same time, the EMU June final composite PMI was also downwardly revised into ‘contraction’ territory (49.9 from 50.3). European bonds jumped higher after the release, with German yields initially up to 5 bps lower. However, they found a bottom in the run-up to the US trading session. German yields currently are changing between -3.0 bps (2 & 5-y) and +0.5 bps (30-y). US data (factory orders) will only be released after finishing this report, but probably are no market mover. The main dish for US markets comes later today, with the Minutes of the June 14 Fed meeting. Markets will look out for the argumentation of a Fed rate skip while at the same time the majority of Fed governors in the dots still saw a potential need for two additional rate hikes. US yields show a (mixed) steepening with the 30-y +3.0 bps. The two 2-y yield (4.91%) pauses ahead of the 5.0% barrier (-3.0 bps). Global risk sentiment remains negative with the Eurostoxx50 again drifting away from the cycle top (-0.8%). US indices open about 0.5% lower. Brent oil ($76.0 p/b) is testing first resistance near $78 p/b as talk on OPEC+ production cuts (Saudi Arabia & Russia) continues.

Again no big moves in the major FX cross rates. EUR/USD hovers near the 1.09 pivot. The USD/JPY uptrend for now is taking a pause (144.40). Sterling is taking a breather after yesterday’s rally (EUR/GBP 0.857). UK bonds continue to underperform (5-y yield +5 bps).

News & Views

Turkish inflation accelerated in June with the monthly pace picking up from 0.04% to 3.92%. The significant increase, even as it was slightly below expectations, came after household gas prices were statistically recorded as zero in May. President Erdogan back then offered families one month of free natural gas ahead of the elections. A dramatic decline in the Turkish lira since Erdogan’s reelection also fanned (imported) inflation. The currency in June fell more than 25% against the US dollar as the new finance minister in a turn towards policy orthodoxy eased the FX controls that were artificially containing the lira’s decline. Yearly price pressures eased from 39.59% to a still stunning 38.21%, which is miles above the 5% central bank target. Core inflation on the other hand quickened from 46.62% to 47.33%. These high inflation numbers mean the real policy rate is still deeply negative, despite last month’s 650 bps increase to 15%. The CBRT did say it plans to tighten policy further, be it gradual. The lira, however, is in need of a decisive, not gradual, response to inflation. USD/TRY today extends gains (TRY loses) towards 26.08. Finishing above 26.05 would mean a new closing record high for USD/TRY.

Sweden’s Swedbank/Silf services PMI plunged from a downwardly revised 49.2 in May to 46.1 in June. Barring an only marginally lower reading in February this year (46), it’s the lowest outcome since the pandemic in 2020. Details were horrible with business volume dropping to 46.5 from 50.6, new orders venturing deeper in contraction territory (45..4 from 48.9) and employment also hitting a sub 50 figure (49 from 53.9). Combined with Monday’s 44.8 manufacturing PMI (a bit less worse than the 41.5 expected), the composite PMI hit a post-pandemic low of 45.8, signaling economic contraction across the private sector. The Swedish krone picked up the weak data points today. At current levels of 11.83, EUR/SEK is set for the highest close on record. The pair end last and earlier this week intraday hit even higher levels of 11.85. The currency is trading in the defensive for several months now on a combination of high inflation, a too slow Riksbank response, general economic uncertainty and concerns about real estate turbulence potentially sparking financial instability.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0863; (P) 1.0893; (R1) 1.0908; More...

Range trading continues in EUR/USD and intraday bias stays neutral at this point. Further rally is still in favor. On the upside, break of 1.1011 will resume the rise from 1.0634 and target 1.1094 resistance. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. However, firm break of 1.0834 will turn bias to the downside for 1.0634 support instead.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

GBP/USD Mid-Day Outlook

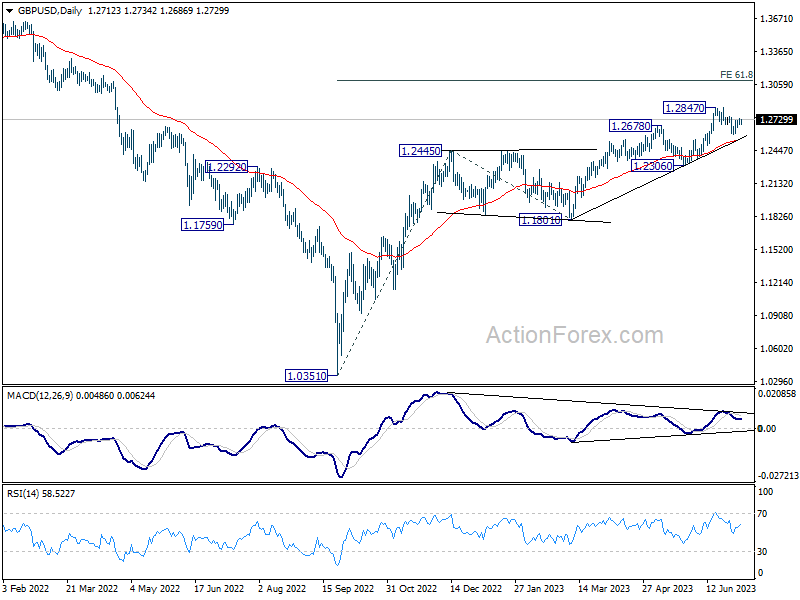

Daily Pivots: (S1) 1.2685; (P) 1.2712; (R1) 1.2740; More...

Intraday bias in GBP/USD remains mildly on the upside at this point. Further rise would be seen to retest 1.2847 high. Firm break there will resume larger up trend from 1.0351, to 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. On the downside, though, break of 1.2589 will extend the fall to 55 D EMA (now at 1.2547).

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

USD/CHF Mid-Day Outlook

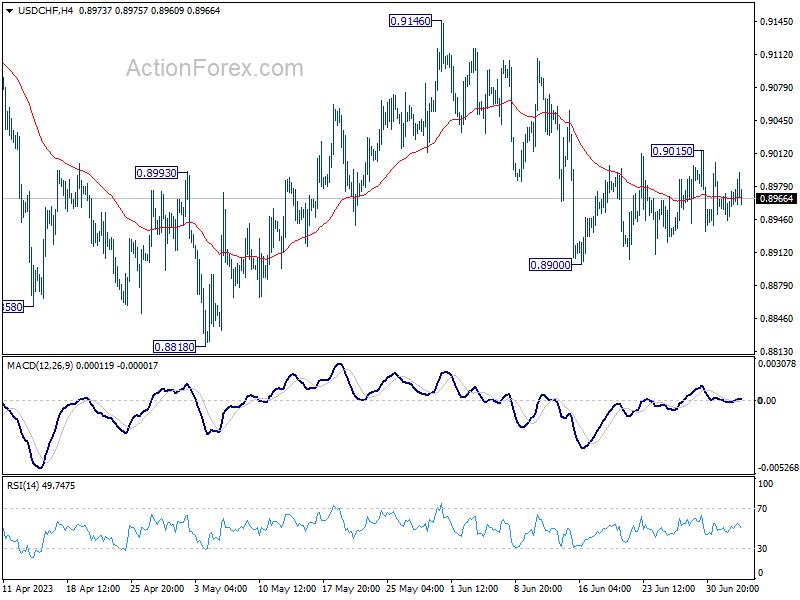

Daily Pivots: (S1) 0.8953; (P) 0.8965; (R1) 0.8984; More...

Intraday bias in USD/CHF remains neutral and outlook stays bearish. On the downside, break of 0.8900 will resume the fall from 0.9146 to 0.8818 low or below. On the upside, above 0.9015 will bring stronger rise towards 0.9146 resistance instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high). While further decline cannot be ruled out, strong support is expected from 0.8756 long term support to bring reversal. Firm break of 0.9146 resistance should confirm medium term bottoming.

USD/JPY Mid-Day Outlook

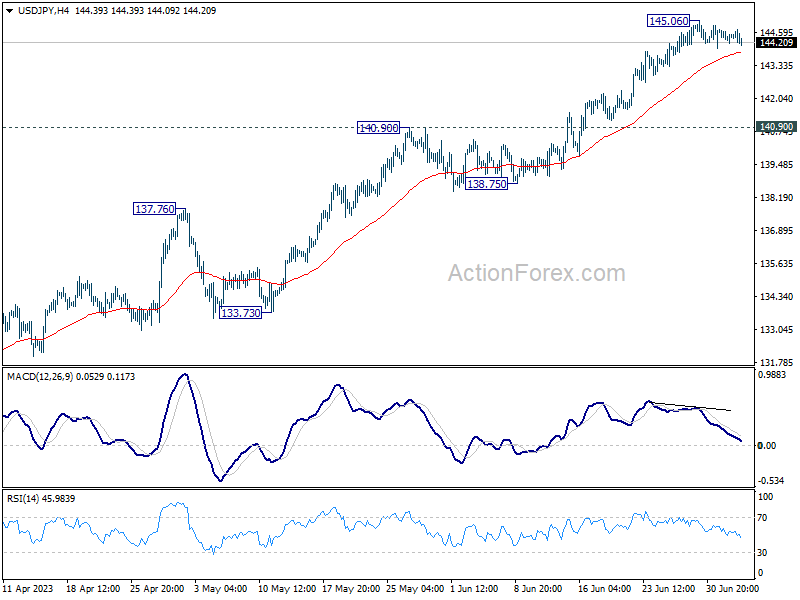

Daily Pivots: (S1) 144.22; (P) 144.47; (R1) 144.72; More...

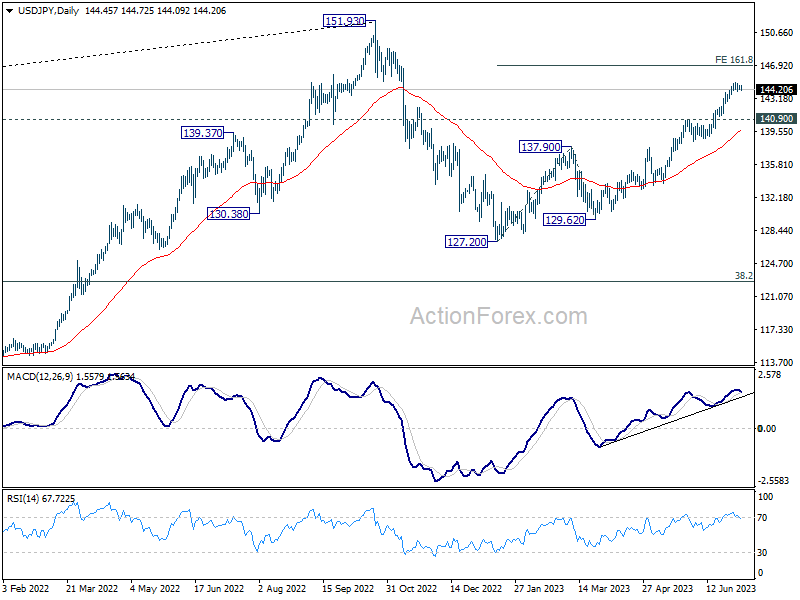

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, break of 55 4H EMA (now at 143.85) could trigger deeper correction. But further rally will remain in favor as long as 140.90 resistance turned support holds. On the upside, break of 145.06 will resume larger rise to 161.8% projection of 127.20 to 137.90 from 129.62 at 146.93.

In the bigger picture, rise from 127.20 is currently seen as the second leg of the corrective pattern from 151.93 high. Further rally is expected as long as 138.75 support holds, to retest 151.93. But strong resistance could be seen there to limit upside. Break of 138.75 will indicate the the third leg has started back towards 127.20.

USD/CAD Mid-Day Outlook

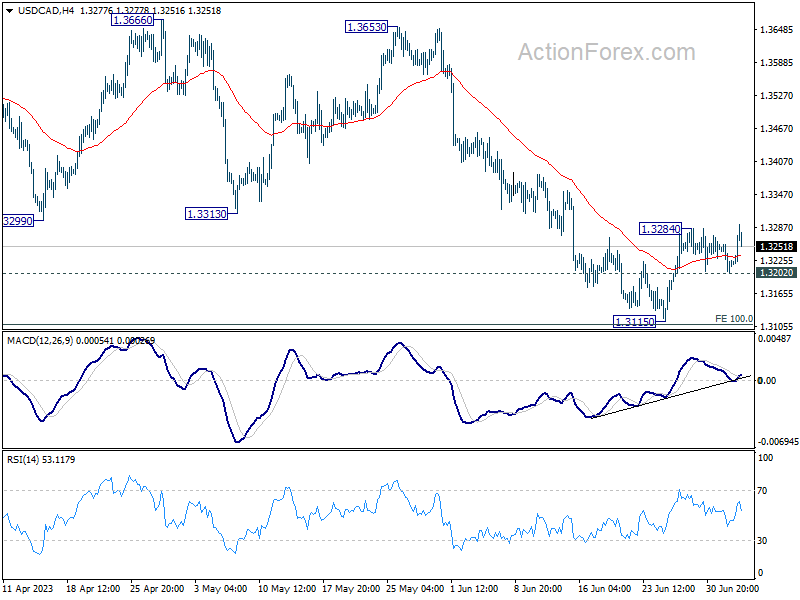

Daily Pivots: (S1) 1.3198; (P) 1.3228; (R1) 1.3252; More....

USD/CAD's rebound from 1.3115 is trying to resume by breaching 1.3284 temporary top. Intraday bias is back on the upside for 55 D EMA (now at 1.3369). On the downside, break of 1.3202 minor support will turn bias back to the downside for retesting 1.3115 low instead.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low). Risk will stay on the downside as long as 1.3299 support turned resistance holds. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. However, sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.

Markets Turning Cautious ahead of FOMC Minutes, 10-Year Yield Making Progress

Dollar and Japanese Yen are posting marginal gains as market attention shifts towards the release of June FOMC meeting minutes. Concurrently, major European indices are slightly down, reflecting a similar sentiment in US futures market. This development has put commodity currencies on the back foot. However, neither Dollar nor Yen has demonstrated enough strength to break free from their near-term trading range against their European counterparts. The restrained market movement signals traders' hesitation to take a strong position ahead of Friday's non-farm payroll data.

For the rest of the day, the primary market focus will be on minutes of June FOMC meeting. However, new revelations from the minutes are considered unlikely. The committee's overall perspective was sufficiently conveyed through the recent dot plot. Fed Chair Jerome Powell was straightforward in expressing his view that the current monetary policy might not be restrictive enough and that it hasn't been restrictive for an adequate period. A considerable majority of the committee anticipates two or more rate hikes this year. Yet, these decisions will be contingent on forthcoming economic data.

Technically, 10-year yield appears to be finally gathering enough momentum to break through 3.859 resistance decisively today. Sustained trading above this resistance will solidify the case that whole correction from 4.333 has completed at 3.253. Further rise should be seen towards 4.091 resistance next. Such development should give additional support to Dollar, especially against Yen.

In Europe, at the time of writing, FTSE is down -0.74%. DAX is down -0.74%. CAC is down -0.84%. Germany 10-year yield is down -0.0224 at 2.434. Earlier in Asia, Nikkei dropped -0.25%. Hong Kong HSI dropped -1.57%. China Shanghai SSE dropped -0.68%. Singapore Strait times dropped -0.57%. Japan 10-year JGB yield rose 0.0117 to 0.387.

ECB consumer expectation survey: 1-year inflation expectations fell further

According to May ECB Consumer Expectations Survey, consumers are indicating a slight easing in their inflation expectations for the near and medium term, while growth expectations stay largely cautious.

In detail, mean inflation expectations for one year ahead in May stood at 5.1%, dipping from 5.3% in April and significantly lower than March's 6.3%. Median inflation expectations for the same period also saw a decline, registering at 3.9% in May, compared to 4.1% in April and 5.0% in March.

Furthermore, consumers' mean inflation expectations for three years ahead were at 4.0% in May, a slight increase from April's 3.8%, yet still lower than March's 4.3%. The median inflation expectations for the same term remained steady at 2.5% for both May and April, below March's 2.9%.

On the growth front, mean expectations for economic expansion over the next 12 months saw a slight uptick, registering at -0.7% in May, compared to -0.8% in April and -1.0% in March. Meanwhile, the median economic growth expectation for the next 12 months held steady at 0% for May, unchanged from April and March.

Eurozone PPI down -1.9% mom, -1.5% yoy in May

Eurozone PPI was down -1.9% mom, -1.5% yoy in May, versus expectation of -1.8% mom, -1.3% yoy. For the month, industrial producer prices decreased by -5.0% mom in the energy sector, by -1.0% mom for intermediate goods and by -0.1% mom for non-durable consumer goods, while prices remained stable for capital goods and increased by 0.3% mom for durable consumer goods. Prices in total industry excluding energy decreased by -0.4% mom.

EU PPI was down -1.8% mom, -0.5% yoy. The largest monthly decreases in industrial producer prices were recorded in Ireland (-7.4%), Italy (-3.1%) and Finland (-3.0%), while increases were observed in Cyprus (+2.8%), and Malta (+0.4%).

Eurozone PMI composite finalized at 49.9, all major euro countries lost considerable momentum

Eurozone Services PMI was finalized at a 5-month low at 52.0 from May's 55.1, while Composite PMI was finalized at a 6-month low at 49.9, down from May's 52.8.

Exploring some member states' performance, a general slowdown was observed with Spain hitting a 5-month low at 52.6, Ireland at a 6-month low with 51.4, Germany at a 5-month low at 50.6, Italy hitting a 6-month low with 49.7, and France, with the most significant contraction, at a 28-month low of 47.2.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that "all major euro countries have again lost considerable momentum." Slowdown was accompanied by weaker rise in new business, lower price increases, and decline in business expectations." Neertheless, job creation remained roughly as solid as in the previous month

While price pressure in the services sector, a key point of focus for ECB, has somewhat eased, de la Rubia cautioned that input costs are still rising robustly by historical standards. This is forcing service firms to pass on at least some of these cost increases, partially driven by higher wages, to end customers. The resulting stubbornly high core inflation suggests that the ECB may continue hiking policy rates in response.

UK PMI services finalized at 53.7, showing renewed signs of fragility

UK's Service sector displayed signs of vulnerability in June, according to recent PMI readings. PMI Services reading was finalized at 53.7, a slight downturn from May's 55.2, while Composite PMI eased to 52.8, down from 54.0 in May.

Tim Moore, Economics Director at S&P Global Market Intelligence, said, "The service sector showed renewed signs of fragility in June as rising interest rates and concerns about the UK economic outlook took their toll on customer demand." He pointed out that business activity saw the slowest expansion in three months, and rate of new order growth slid further from the peak recorded in April.

Despite the tepid pace of activity, Moore observed that labor market conditions remained relatively buoyant. He highlighted that job creation reached a nine-month high, with an improvement in candidate availability enabling firms to fill vacancies and rebuild business capacity.

On the price front, service providers experienced deceleration in overall input price inflation. Business expenses climbed at the most modest pace since May 2021. Nonetheless, cost pressures ranked among the most substantial seen since the survey began in July 1996. Salary payments continued to surge across the board, offsetting the decline in fuel bills and energy prices. This situation underscores the ongoing challenge of inflationary pressures in the UK economy.

China Caixin PMI services fell to 53.9, recovery losing steam

China's Caixin Services PMI for June plunged to 53.9, down from 57.1 in the previous month and significantly below the expectation of 56.2. The composite PMI also tumbled from 55.6 to a discouraging 52.5, marking the lowest readings since the growth cycle kick-started in January.

Wang Zhe, a senior economist at the Caixin Insight Group, commented on the less-than-promising data: "A slew of recent economic data suggests that China's recovery has yet to find a stable footing, with prominent issues including a lack of internal growth drivers, weak demand, and dimming prospects persisting."

Zhe emphasized the disparity between the manufacturing and services sectors, noting that "In June, Caixin China PMIs showed that conditions in the manufacturing sector lagged far behind services. Employment contracted, deflationary pressure mounted, and optimism waned in the manufacturing sector."

Despite the ongoing post-Covid rebound of the services sector, Zhe expressed concerns about the sustainability of the recovery, adding that "the services sector continued a post-Covid rebound, but the recovery was losing steam."

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3198; (P) 1.3228; (R1) 1.3252; More....

USD/CAD's rebound from 1.3115 is trying to resume by breaching 1.3284 temporary top. Intraday bias is back on the upside for 55 D EMA (now at 1.3369). On the downside, break of 1.3202 minor support will turn bias back to the downside for retesting 1.3115 low instead.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low). Risk will stay on the downside as long as 1.3299 support turned resistance holds. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. However, sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Jun | 53.9 | 56.2 | 57.1 | |

| 06:45 | EUR | France Industrial Output M/M May | 1.20% | -0.20% | 0.80% | |

| 07:45 | EUR | Italy Services PMI Jun | 52.2 | 53 | 54 | |

| 07:50 | EUR | France Services PMI Jun F | 48 | 48 | 48 | |

| 07:55 | EUR | Germany Services PMI Jun F | 54.1 | 54.1 | 54.1 | |

| 08:00 | EUR | Eurozone Services PMI Jun F | 52 | 52.4 | 52.4 | |

| 08:30 | GBP | Services PMI Jun F | 53.7 | 53.7 | 53.7 | |

| 09:00 | EUR | Eurozone PPI M/M May | -1.90% | -1.80% | -3.20% | |

| 09:00 | EUR | Eurozone PPI Y/Y May | -1.50% | -1.30% | 1.00% | 0.90% |

| 14:00 | USD | Factory Orders M/M May | 0.60% | 0.40% | ||

| 18:00 | USD | FOMC Minutes |

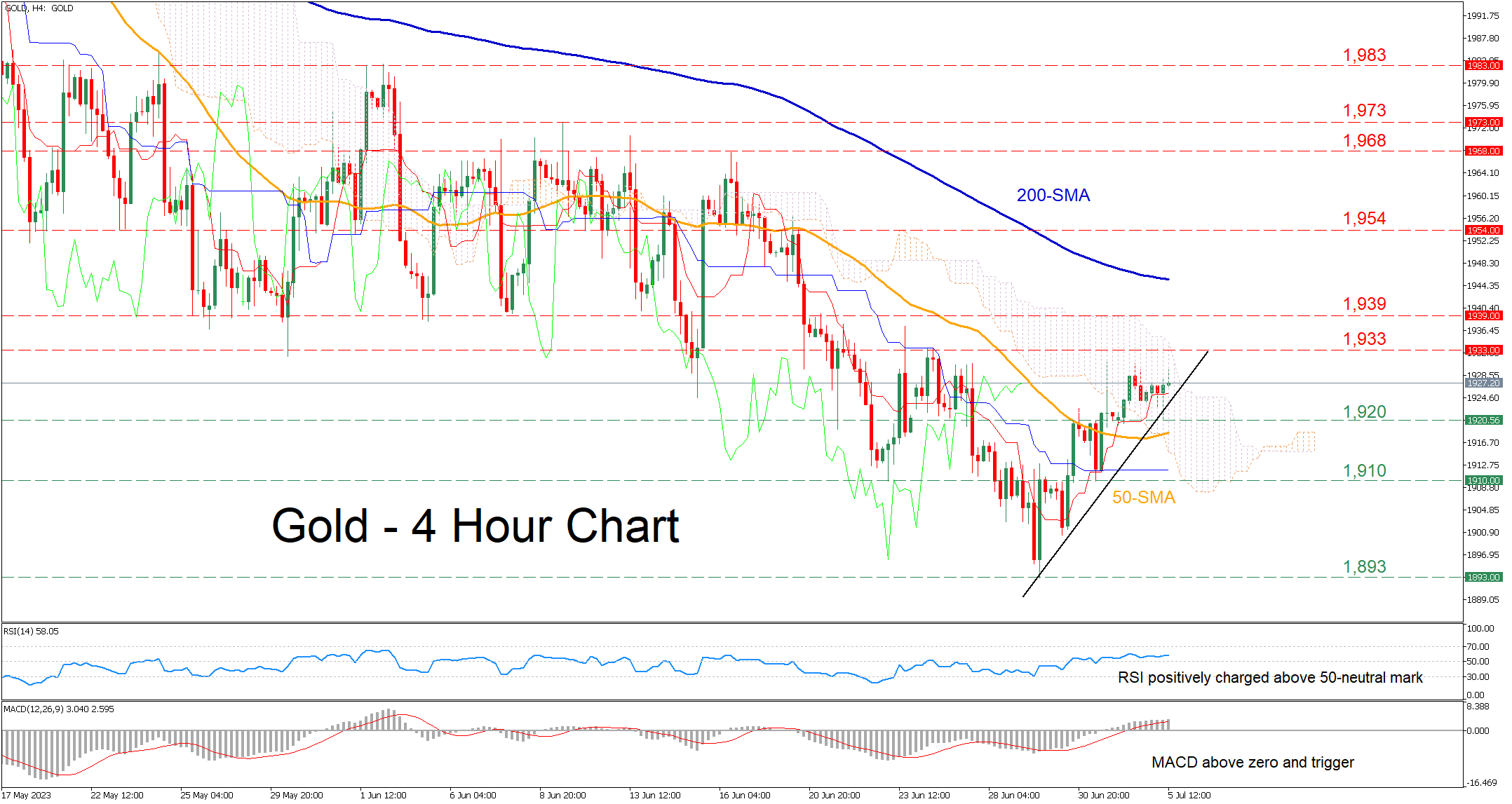

Gold in Recovery Mode But Bearish Structure Holds

Gold has been losing ground since mid-June, dropping below the 1,900 handle for the first in more than three months. However, the commodity managed to regain traction and jump above its 50-period simple moving average (SMA), while it is set to challenge the upper boundary of the Ichimoku cloud.

The momentum indicators currently suggest that bullish forces are in control. Specifically, the RSI is ascending above its 50-neutral mark, while the MACD is strengthening above its red signal line in the positive territory.

Should the price extend its advance, the 1,933 resistance zone could prove to be the first hurdle for buyers to clear. Breaking above that zone, bullion could challenge 1,939, which served as both resistance and support throughout June. Even higher, further advances could cease at the 1,954 barrier before the spotlight turns to 1,968.

On the flipside, if the recovery falters and the price reverses lower, the recent support of 1,920 might act as the first line of defence. Sliding beneath that floor, gold could dip below its 50-period SMA to test the 1,910 support region. A violation of the latter could pave the way for the three-month low of 1,893.

In brief, gold seems to be in a recovery phase, with its latest advance being on hold for now. Therefore, a break above the Ichimoku cloud could provide early indications that the recent rebound is likely to persist.