Sample Category Title

Markets Turning Cautious ahead of FOMC Minutes, 10-Year Yield Making Progress

Dollar and Japanese Yen are posting marginal gains as market attention shifts towards the release of June FOMC meeting minutes. Concurrently, major European indices are slightly down, reflecting a similar sentiment in US futures market. This development has put commodity currencies on the back foot. However, neither Dollar nor Yen has demonstrated enough strength to break free from their near-term trading range against their European counterparts. The restrained market movement signals traders' hesitation to take a strong position ahead of Friday's non-farm payroll data.

For the rest of the day, the primary market focus will be on minutes of June FOMC meeting. However, new revelations from the minutes are considered unlikely. The committee's overall perspective was sufficiently conveyed through the recent dot plot. Fed Chair Jerome Powell was straightforward in expressing his view that the current monetary policy might not be restrictive enough and that it hasn't been restrictive for an adequate period. A considerable majority of the committee anticipates two or more rate hikes this year. Yet, these decisions will be contingent on forthcoming economic data.

Technically, 10-year yield appears to be finally gathering enough momentum to break through 3.859 resistance decisively today. Sustained trading above this resistance will solidify the case that whole correction from 4.333 has completed at 3.253. Further rise should be seen towards 4.091 resistance next. Such development should give additional support to Dollar, especially against Yen.

In Europe, at the time of writing, FTSE is down -0.74%. DAX is down -0.74%. CAC is down -0.84%. Germany 10-year yield is down -0.0224 at 2.434. Earlier in Asia, Nikkei dropped -0.25%. Hong Kong HSI dropped -1.57%. China Shanghai SSE dropped -0.68%. Singapore Strait times dropped -0.57%. Japan 10-year JGB yield rose 0.0117 to 0.387.

ECB consumer expectation survey: 1-year inflation expectations fell further

According to May ECB Consumer Expectations Survey, consumers are indicating a slight easing in their inflation expectations for the near and medium term, while growth expectations stay largely cautious.

In detail, mean inflation expectations for one year ahead in May stood at 5.1%, dipping from 5.3% in April and significantly lower than March's 6.3%. Median inflation expectations for the same period also saw a decline, registering at 3.9% in May, compared to 4.1% in April and 5.0% in March.

Furthermore, consumers' mean inflation expectations for three years ahead were at 4.0% in May, a slight increase from April's 3.8%, yet still lower than March's 4.3%. The median inflation expectations for the same term remained steady at 2.5% for both May and April, below March's 2.9%.

On the growth front, mean expectations for economic expansion over the next 12 months saw a slight uptick, registering at -0.7% in May, compared to -0.8% in April and -1.0% in March. Meanwhile, the median economic growth expectation for the next 12 months held steady at 0% for May, unchanged from April and March.

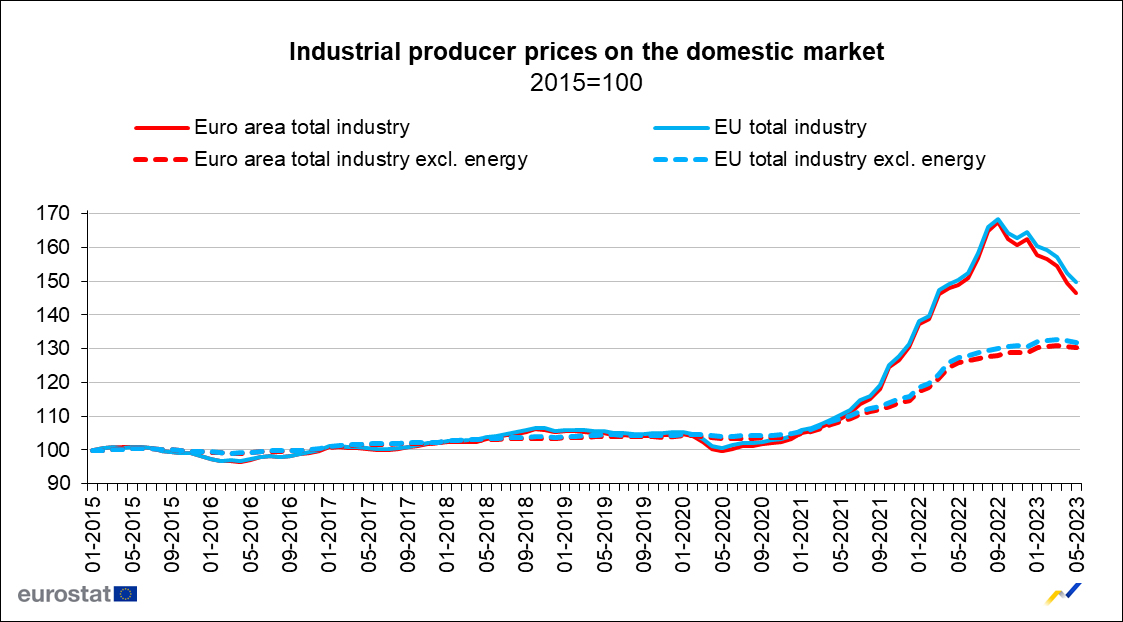

Eurozone PPI down -1.9% mom, -1.5% yoy in May

Eurozone PPI was down -1.9% mom, -1.5% yoy in May, versus expectation of -1.8% mom, -1.3% yoy. For the month, industrial producer prices decreased by -5.0% mom in the energy sector, by -1.0% mom for intermediate goods and by -0.1% mom for non-durable consumer goods, while prices remained stable for capital goods and increased by 0.3% mom for durable consumer goods. Prices in total industry excluding energy decreased by -0.4% mom.

EU PPI was down -1.8% mom, -0.5% yoy. The largest monthly decreases in industrial producer prices were recorded in Ireland (-7.4%), Italy (-3.1%) and Finland (-3.0%), while increases were observed in Cyprus (+2.8%), and Malta (+0.4%).

Eurozone PMI composite finalized at 49.9, all major euro countries lost considerable momentum

Eurozone Services PMI was finalized at a 5-month low at 52.0 from May's 55.1, while Composite PMI was finalized at a 6-month low at 49.9, down from May's 52.8.

Exploring some member states' performance, a general slowdown was observed with Spain hitting a 5-month low at 52.6, Ireland at a 6-month low with 51.4, Germany at a 5-month low at 50.6, Italy hitting a 6-month low with 49.7, and France, with the most significant contraction, at a 28-month low of 47.2.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that "all major euro countries have again lost considerable momentum." Slowdown was accompanied by weaker rise in new business, lower price increases, and decline in business expectations." Neertheless, job creation remained roughly as solid as in the previous month

While price pressure in the services sector, a key point of focus for ECB, has somewhat eased, de la Rubia cautioned that input costs are still rising robustly by historical standards. This is forcing service firms to pass on at least some of these cost increases, partially driven by higher wages, to end customers. The resulting stubbornly high core inflation suggests that the ECB may continue hiking policy rates in response.

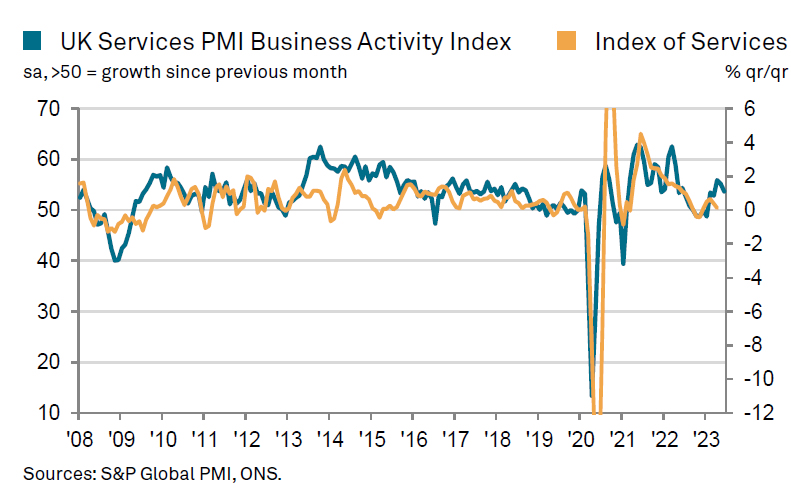

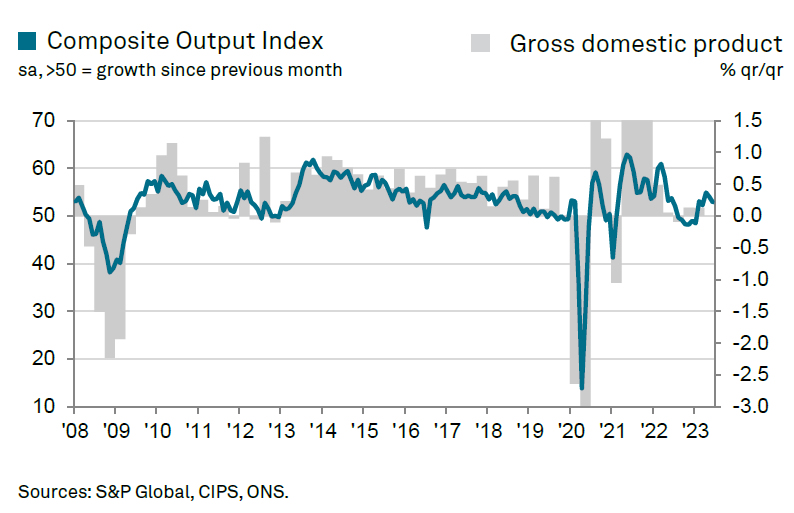

UK PMI services finalized at 53.7, showing renewed signs of fragility

UK's Service sector displayed signs of vulnerability in June, according to recent PMI readings. PMI Services reading was finalized at 53.7, a slight downturn from May's 55.2, while Composite PMI eased to 52.8, down from 54.0 in May.

Tim Moore, Economics Director at S&P Global Market Intelligence, said, "The service sector showed renewed signs of fragility in June as rising interest rates and concerns about the UK economic outlook took their toll on customer demand." He pointed out that business activity saw the slowest expansion in three months, and rate of new order growth slid further from the peak recorded in April.

Despite the tepid pace of activity, Moore observed that labor market conditions remained relatively buoyant. He highlighted that job creation reached a nine-month high, with an improvement in candidate availability enabling firms to fill vacancies and rebuild business capacity.

On the price front, service providers experienced deceleration in overall input price inflation. Business expenses climbed at the most modest pace since May 2021. Nonetheless, cost pressures ranked among the most substantial seen since the survey began in July 1996. Salary payments continued to surge across the board, offsetting the decline in fuel bills and energy prices. This situation underscores the ongoing challenge of inflationary pressures in the UK economy.

China Caixin PMI services fell to 53.9, recovery losing steam

China's Caixin Services PMI for June plunged to 53.9, down from 57.1 in the previous month and significantly below the expectation of 56.2. The composite PMI also tumbled from 55.6 to a discouraging 52.5, marking the lowest readings since the growth cycle kick-started in January.

Wang Zhe, a senior economist at the Caixin Insight Group, commented on the less-than-promising data: "A slew of recent economic data suggests that China's recovery has yet to find a stable footing, with prominent issues including a lack of internal growth drivers, weak demand, and dimming prospects persisting."

Zhe emphasized the disparity between the manufacturing and services sectors, noting that "In June, Caixin China PMIs showed that conditions in the manufacturing sector lagged far behind services. Employment contracted, deflationary pressure mounted, and optimism waned in the manufacturing sector."

Despite the ongoing post-Covid rebound of the services sector, Zhe expressed concerns about the sustainability of the recovery, adding that "the services sector continued a post-Covid rebound, but the recovery was losing steam."

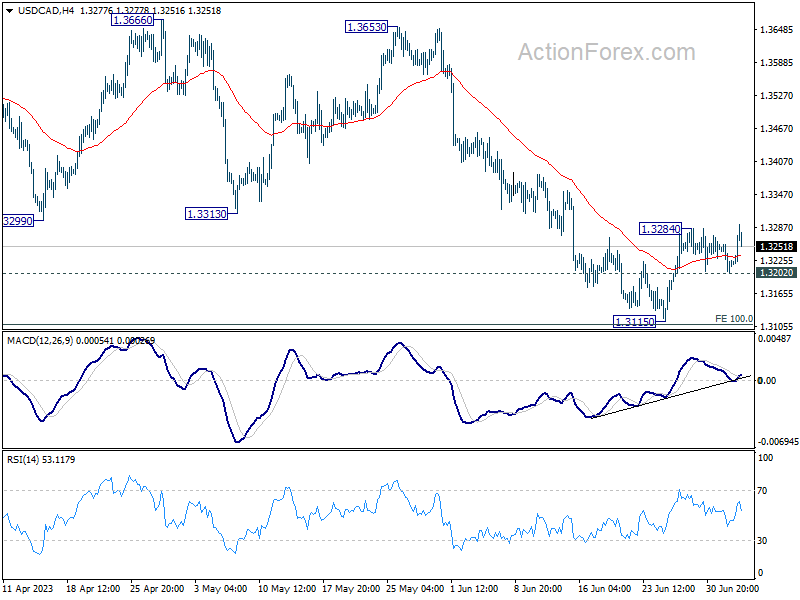

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3198; (P) 1.3228; (R1) 1.3252; More....

USD/CAD's rebound from 1.3115 is trying to resume by breaching 1.3284 temporary top. Intraday bias is back on the upside for 55 D EMA (now at 1.3369). On the downside, break of 1.3202 minor support will turn bias back to the downside for retesting 1.3115 low instead.

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low). Risk will stay on the downside as long as 1.3299 support turned resistance holds. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. However, sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Jun | 53.9 | 56.2 | 57.1 | |

| 06:45 | EUR | France Industrial Output M/M May | 1.20% | -0.20% | 0.80% | |

| 07:45 | EUR | Italy Services PMI Jun | 52.2 | 53 | 54 | |

| 07:50 | EUR | France Services PMI Jun F | 48 | 48 | 48 | |

| 07:55 | EUR | Germany Services PMI Jun F | 54.1 | 54.1 | 54.1 | |

| 08:00 | EUR | Eurozone Services PMI Jun F | 52 | 52.4 | 52.4 | |

| 08:30 | GBP | Services PMI Jun F | 53.7 | 53.7 | 53.7 | |

| 09:00 | EUR | Eurozone PPI M/M May | -1.90% | -1.80% | -3.20% | |

| 09:00 | EUR | Eurozone PPI Y/Y May | -1.50% | -1.30% | 1.00% | 0.90% |

| 14:00 | USD | Factory Orders M/M May | 0.60% | 0.40% | ||

| 18:00 | USD | FOMC Minutes |

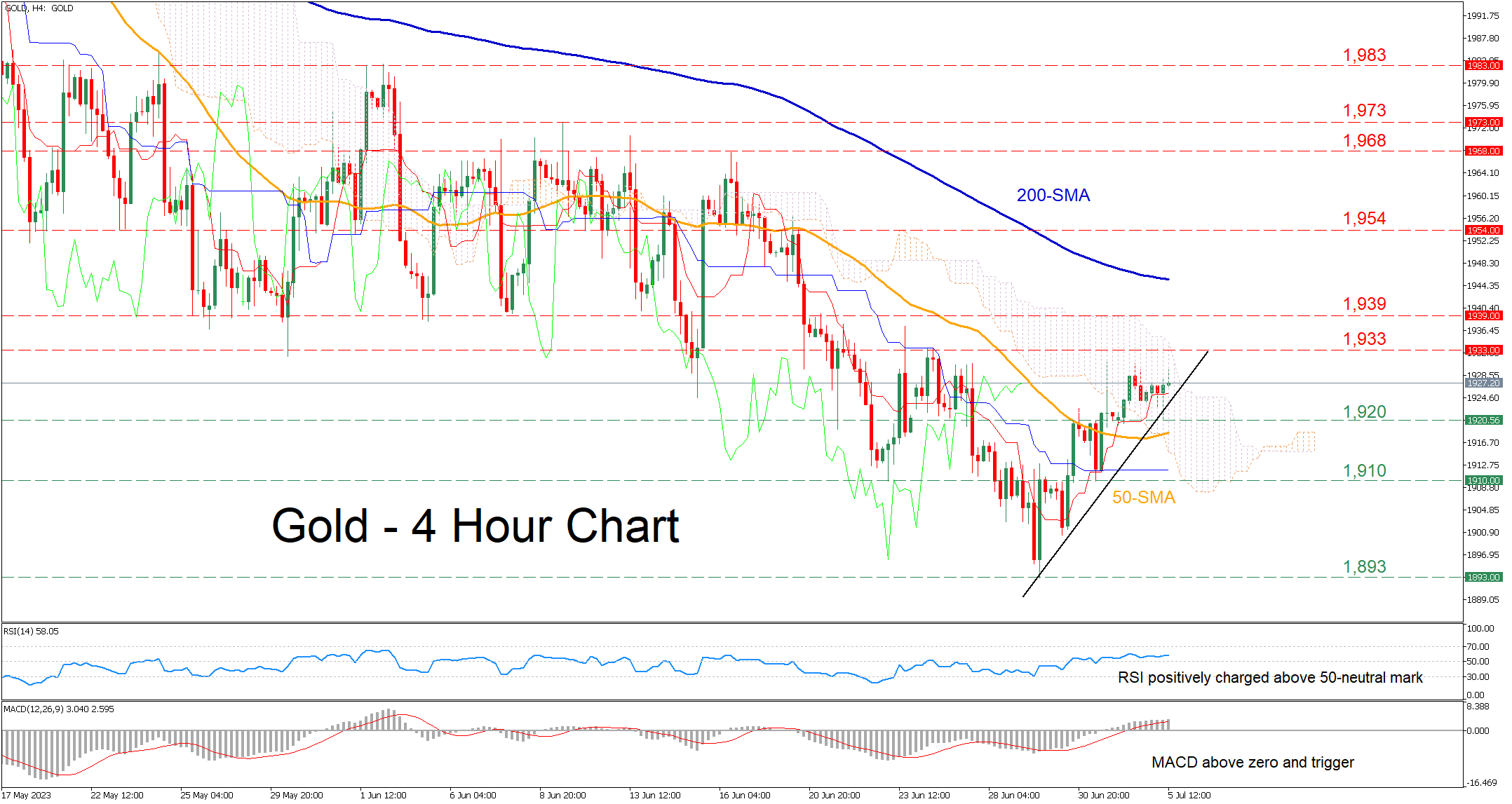

Gold in Recovery Mode But Bearish Structure Holds

Gold has been losing ground since mid-June, dropping below the 1,900 handle for the first in more than three months. However, the commodity managed to regain traction and jump above its 50-period simple moving average (SMA), while it is set to challenge the upper boundary of the Ichimoku cloud.

The momentum indicators currently suggest that bullish forces are in control. Specifically, the RSI is ascending above its 50-neutral mark, while the MACD is strengthening above its red signal line in the positive territory.

Should the price extend its advance, the 1,933 resistance zone could prove to be the first hurdle for buyers to clear. Breaking above that zone, bullion could challenge 1,939, which served as both resistance and support throughout June. Even higher, further advances could cease at the 1,954 barrier before the spotlight turns to 1,968.

On the flipside, if the recovery falters and the price reverses lower, the recent support of 1,920 might act as the first line of defence. Sliding beneath that floor, gold could dip below its 50-period SMA to test the 1,910 support region. A violation of the latter could pave the way for the three-month low of 1,893.

In brief, gold seems to be in a recovery phase, with its latest advance being on hold for now. Therefore, a break above the Ichimoku cloud could provide early indications that the recent rebound is likely to persist.

Euro Trading Quietly Around 1.09, FOMC Minutes Next

- Eurozone and German Services PMIs weaken in June

- Markets looking for clues as Fed releases minutes on Wednesday

EUR/USD is showing limited movement on Wednesday. In the European session, the euro is almost unchanged at 1.0882.

German and eurozone Services PMIs ease

The eurozone services sector continues to show growth, but the June numbers showed a deceleration. Eurozone PMI slowed to 52.0, shy of the consensus of 52.4 and down from 55.1 in May. This marked a five-month low. Germany’s services sector stalled, dropping from 53.9 to 50.6 and missing the consensus of 50.8 points. The 50.0 level separates contraction from expansion.

The eurozone economy has been recovering slowly, with services driving economic activity as manufacturing continues to decline. The ECB, which showed up late to the rate-hiking party but has been quite hawkish, will need to tread carefully in order to guide the economy to a soft landing. The central bank meets next on July 27th and is expected to raise rates. Inflation has been falling but core CPI remains persistently high.

The ECB has signalled more rate hikes are coming and Joachim Nagel, head of the German central bank, reiterated the ECB’s stance, saying this week that inflation risks are tilted to the upside and the ECB’s rate-hike cycle has “some way to go”.

Wednesday’s highlight is the FOMC minutes of the June meeting, when the Fed raised rates by 0.25%, bringing the benchmark cash rate to a range of 5.00%-5.25%. The markets are widely expecting the Fed to hike at the July meeting but aren’t sure about another rate hike this year. Fed Chair Powell has signalled that the Fed plans two hikes in the second half of the year and the minutes could change the market’s tune if the Fed’s tone is hawkish.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0908. The next resistance line is 110.50

- 1.0838 and 1.0766 are providing support

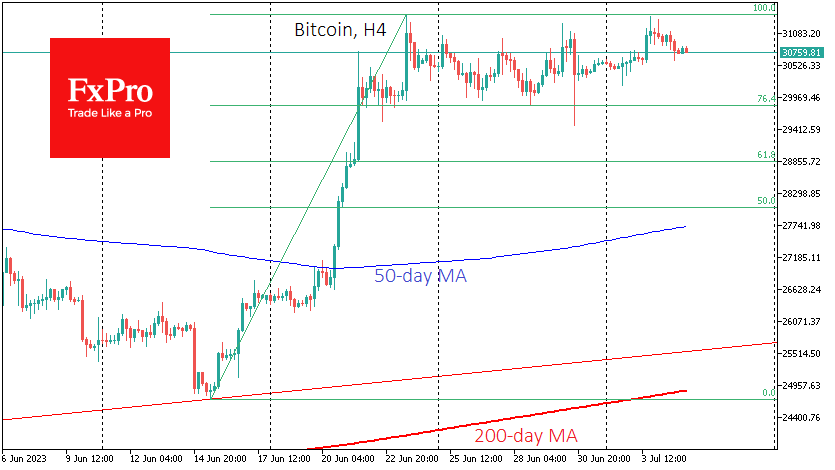

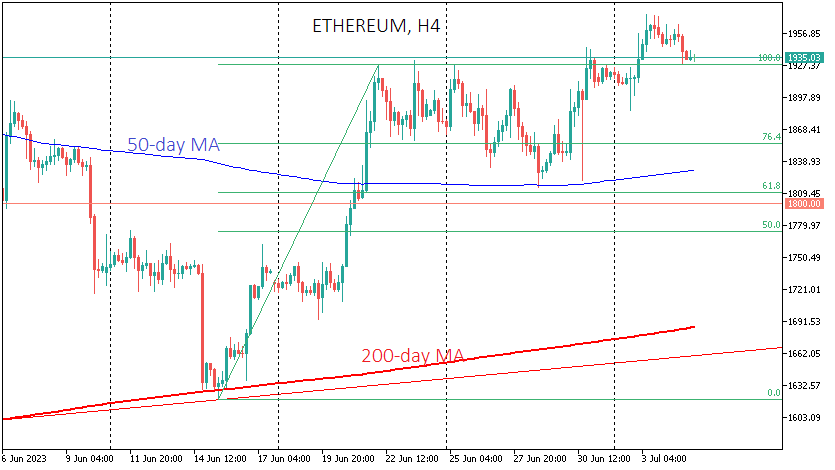

Bitcoin Retreats, But Ethereum Poised for a Bullish Breakout

Market picture

Cryptocurrency market capitalisation fell 0.7% over the past 24 hours to $1.21 trillion, remaining near its peak since late April. The Cryptocurrency Fear and Greed Index retreated from 64 to 61 by early Wednesday afternoon, staying in “greed” territory.

Bitcoin has pulled back from the top of its recent trading range above $31.3K and is trading back near $30.8K. An upside breakout has not been confirmed, and the logical development is a pullback to the lower end of the range at $29.8K. Only a sustained exit outside the $29.8-31.3K corridor will signal the end of the consolidation and further movement towards the breakout.

Ethereum is also undergoing a local correction, but its stronger momentum is bullish for Bitcoin. ETHUSD broke through local resistance on Monday and completed a corrective pullback. The local retreat brought the price back to the former resistance in place since late April.

News background

Shares of the world’s largest cryptocurrency operator Bitcoin Depot rose nearly 12% on its first day of trading on the NASDAQ. Cryptocurrency companies also saw significant gains. Shares in Coinbase jumped 12%, while MicroStrategy gained 10%.

According to Kaiko, cryptocurrency spot trading volumes fell sharply in the second quarter of 2023, hitting lows seen in late 2020. Binance saw the most significant decline, with trading volumes falling nearly 70%.

The alliance of South Korean cryptocurrency exchanges introduced a system to track market volatility. The alert system was designed to protect users by eliminating asymmetries and inconsistencies in incoming exchange information.

The Luminex team behind the Ordinaries platform unveiled the BRC-69 standard, making issuing NFT collections of recursive inscriptions in the Bitcoin blockchain easier and cheaper. According to the developers, BRC-69 reduces the cost of giving collections by more than 90%.

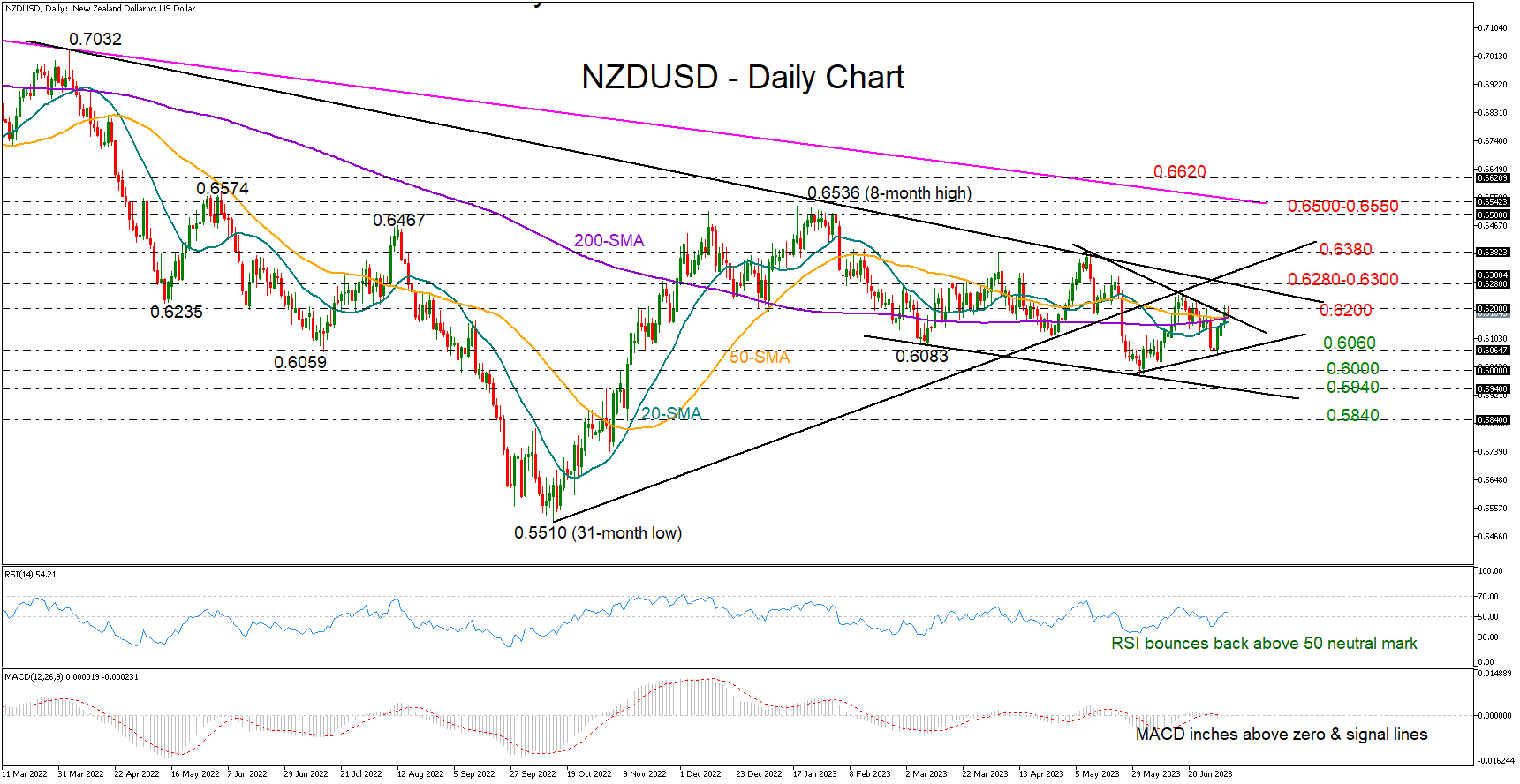

NZDUSD’s Next Battle at 0.6300

NZDUSD turned green after printing a doji candlestick around 0.6050 last Thursday, currently aiming to extend its winning strike above the 0.6200 round level.

The latest rebound in the price has confirmed a higher low in the short-term picture, increasing hopes for a bullish trend reversal. The RSI has bounced back above its 50 neutral mark and the MACD has ticked above its signal and zero lines, both revealing improving market sentiment. Yet, whether the pair has enough fuel in the tank to pierce through the nearby trendline territory of 0.6280-0.6300 remains to be seen.

Specifically, an extension above the simple moving averages and the 0.6200 level could bring the key trendline from April 2022 at 0.6280 and the support trendline from October’s 31-month low at 0.6300 under examination. Breaking that constraining zone, the price could immediately get squeezed around the February-May wall of 0.6380. If not, then the bullish wave might expand towards the 0.6500-0.6550 constraining zone. Notably, the price could re-challenge the long-term descending trendline from March 2021 within the same region.

Alternatively, a pullback below the 20-day simple moving average (SMA) could initially pause near last week’s floor of 0.6060. Moving lower, the pair might retest the 0.6000 psychological level before tumbling towards the tentative support line at 0.5940. The 0.5840 territory could be the next destination.

In brief, although the short-term risk seems to be leaning on the positive side, NZDUSD will need to climb above the trendline zone of 0.6280-0.6300 to boost buying confidence.

USD/JPY – Is Japan Mulling an Intervention?

- Japanese Services PMI continues to expand

- Federal Reserve to release June meeting minutes on Wednesday

USD/JPY continues to have a very quiet week and is trading at 144.36, down 0.07%, in the European session.

Japanese Services PMI points to growth

Japanese business activity continues to expand. The Services PMI, released on Wednesday, was revised lower to 54.0 in June from 54.2. This was lower than the record-high 55.9 in May but indicated that the services economy remains strong. The 50.0 level separates expansion from contraction.

The solid services data was a welcome contrast from Monday’s soft manufacturing numbers. The Manufacturing PMI was unrevised at 49.8 in June, down from 50.6 in May. Manufacturing has sputtered, posting five contractions in factory activity this year. The discrepancy between the services and manufacturing sectors is not unique to Japan, as we’re seeing a similar trend in most of the major economies.

Weak yen could trigger intervention

The Bank of Japan is showing little appetite for tightening its ultra-loose monetary policy. Governor Ueda has said that he would consider a tighter policy if wage growth rises and high inflation remains sustainable. In the meantime, Ueda hasn’t veered from the BoJ’s stance that inflation, which remains above the BoJ’s target of 2%, is temporary.

The Japanese yen has been paying the price of the BoJ’s policy. The US/Japan rate differential continues to widen, as the Fed keeps hiking and the BoJ stands pat. The yen has fallen close to 9% since April 1st, which has triggered verbal intervention from the Ministry of Finance (MoF). In September 2022, the MoF stunned the markets when it intervened after the yen fell to 145. With the yen just shy of that level, there is concern that the MoF could intervene in the currency markets in order to prop up the listless yen. Japanese officials aren’t giving away any clues, saying only that all options remain on the table. If the yen breaks below 145 and moves closer to 150, the possibility of another intervention will increase.

The Fed will release the minutes of the June meeting later today. The markets are widely expecting a 0.25% hike at next week’s meeting and investors will be looking for some clues in the minutes as to the Fed’s rate path. The markets are more in sync with the Fed’s aggressive stance than they were a few months ago, when rate cuts were expected before the end of the year. Now, the markets are not expecting the Fed to trim rates before early 2024.

USD/JPY Technical

- There is resistance at 145.28 and 146.23

- 144.11 is a weak support level. The next support line is 143.16

ECB consumer expectation survey: 1-year inflation expectations fell further

According to May ECB Consumer Expectations Survey, consumers are indicating a slight easing in their inflation expectations for the near and medium term, while growth expectations stay largely cautious.

In detail, mean inflation expectations for one year ahead in May stood at 5.1%, dipping from 5.3% in April and significantly lower than March's 6.3%. Median inflation expectations for the same period also saw a decline, registering at 3.9% in May, compared to 4.1% in April and 5.0% in March.

Furthermore, consumers' mean inflation expectations for three years ahead were at 4.0% in May, a slight increase from April's 3.8%, yet still lower than March's 4.3%. The median inflation expectations for the same term remained steady at 2.5% for both May and April, below March's 2.9%.

On the growth front, mean expectations for economic expansion over the next 12 months saw a slight uptick, registering at -0.7% in May, compared to -0.8% in April and -1.0% in March. Meanwhile, the median economic growth expectation for the next 12 months held steady at 0% for May, unchanged from April and March.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh increase from the 143.30 support zone. The US Dollar climbed higher above the 144.20 resistance zone against the Japanese Yen.

A high is formed near 145.00 and the pair is now correcting gains near the 50-hour simple moving average. Immediate resistance on the upside is near a connecting bearish trend line at 144.65. The first major resistance is near the 144.90 level, above which the pair might gain bullish momentum.

The next major resistance is near the 145.20 zone. A clear break above the 145.20 resistance could push the pair further higher toward 145.80.

If there is a fresh decline, the pair might find bids near the 144.20 level. The next support sits near the 143.80 zone, below which there is a risk of a drop toward the 143.30 level.

Eurozone PPI down -1.9% mom, -1.5% yoy in May

Eurozone PPI was down -1.9% mom, -1.5% yoy in May, versus expectation of -1.8% mom, -1.3% yoy. For the month, industrial producer prices decreased by -5.0% mom in the energy sector, by -1.0% mom for intermediate goods and by -0.1% mom for non-durable consumer goods, while prices remained stable for capital goods and increased by 0.3% mom for durable consumer goods. Prices in total industry excluding energy decreased by -0.4% mom.

EU PPI was down -1.8% mom, -0.5% yoy. The largest monthly decreases in industrial producer prices were recorded in Ireland (-7.4%), Italy (-3.1%) and Finland (-3.0%), while increases were observed in Cyprus (+2.8%), and Malta (+0.4%).

UK PMI services finalized at 53.7, showing renewed signs of fragility

UK's Service sector displayed signs of vulnerability in June, according to recent PMI readings. PMI Services reading was finalized at 53.7, a slight downturn from May's 55.2, while Composite PMI eased to 52.8, down from 54.0 in May.

Tim Moore, Economics Director at S&P Global Market Intelligence, said, "The service sector showed renewed signs of fragility in June as rising interest rates and concerns about the UK economic outlook took their toll on customer demand." He pointed out that business activity saw the slowest expansion in three months, and rate of new order growth slid further from the peak recorded in April.

Despite the tepid pace of activity, Moore observed that labor market conditions remained relatively buoyant. He highlighted that job creation reached a nine-month high, with an improvement in candidate availability enabling firms to fill vacancies and rebuild business capacity.

On the price front, service providers experienced deceleration in overall input price inflation. Business expenses climbed at the most modest pace since May 2021. Nonetheless, cost pressures ranked among the most substantial seen since the survey began in July 1996. Salary payments continued to surge across the board, offsetting the decline in fuel bills and energy prices. This situation underscores the ongoing challenge of inflationary pressures in the UK economy.