Sample Category Title

US-China Tensions Weigh on Market Mood, Strengthen Yen and Dollar

Yen and Dollar are gaining momentum in today's trading as market sentiment appears to have soured in Asia. The development could be interpreted more as a response to escalating US-China tensions rather than hawkish tone of FOMC minutes released overnight. After all, the minutes just reinforced expectations of further monetary tightening, despite a pause in June. Meanwhile, major US indexes closed only slightly lower, even as treasury yields saw a notable surge.

Australian Dollar is emerging as the day's worst performer so far, trailed by Euro and Canadian Dollar. On the flip side, Swiss Franc is strengthening on risk aversion, while Sterling displays mixed performance, buoyed by buying against Euro. Market participants are keenly awaiting tomorrow's US non-farm payroll report, the key event for the week. However, today's ADP employment and ISM services data may trigger some traders to make early moves.

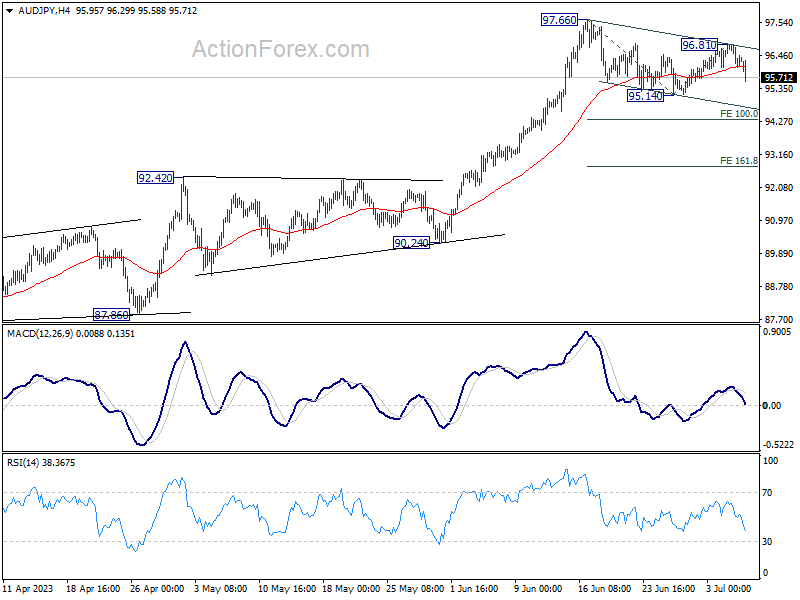

Technically, AUD/JPY's decline today argues that correction from 97.66 might be ready to resume through 95.14 support. For now, strong support is likely at around 100% projection of 97.66 to 95.14 from 96.81 at 94.29 to complete the correction. But strong break there and downside acceleration below the projection level would raise the chance of larger bearish reversal.

In Asia, at the time of writing, Nikkei is down -1.70%. Hong Kong HSI is down -3.08%. China Shanghai SSE is down -0.53%. Singapore Strait Times is down -0.79%. Japan 10-year JGB yield is up 0.0072 at 0.394. Overnight, DOW dropped -0.38%. S&P 500 dropped -0.20%. NASDAQ dropped -0.18%. 10-year yield rose 0.087 to 3.945.

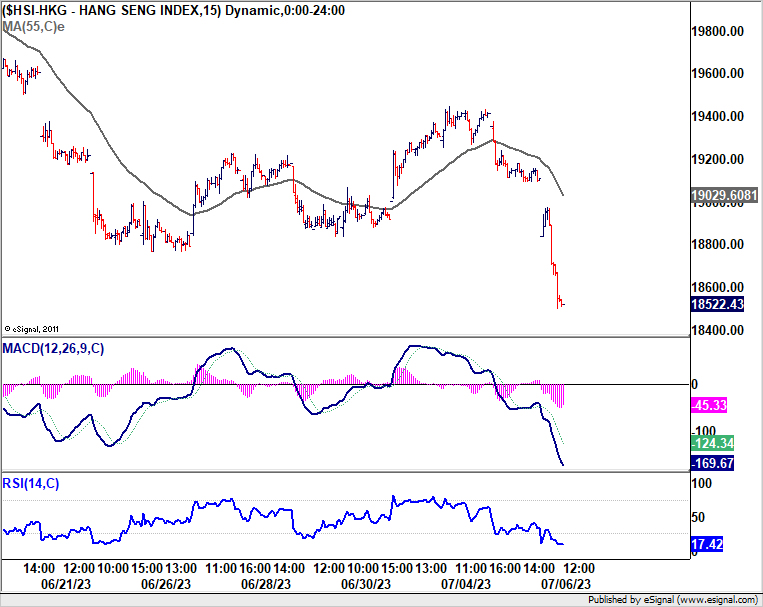

HK HSI dives as Yellen visit China amid rising US-China tensions

Hong Kong HSI is taking a hit today as it gapped down at open and further sell-offs materialized during the initial part of Asian trading session. This market movement mirrors intensifying investor concerns as US Treasury Secretary Janet Yellen starts a four-day visit to China. While the intention behind Yellen's visit is to de-escalate potential conflicts between these two economic behemoths, atmosphere has notably soured this week.

Earlier in the week, China struck a discordant note by announcing fresh restrictions on export of several critical minerals used in manufacture of semiconductors and solar panels. This move appears to be a tit-for-tat response to the tech export limitations that the US has imposed on China, limiting the sale of advanced computer chips. Further adding to the apprehension, US government is reported to be contemplating additional measures to restrict China's access to US-based cloud computing services.

On a separate front, China delivered another blow to international diplomatic relations when it abruptly canceled a visit by European Union foreign policy chief Josep Borrell, scheduled for next week, according to an EU spokesperson. The Chinese authorities have not yet disclosed the reasons behind this unexpected cancellation.

From a technical perspective, today's market turbulence in Hong Kong, marked by a gap down followed by a sharp drop, appears to validate rejection by 55 D EMA (now at 19428.57). Fall from 20155.92 is likely to be another chapter in the overall descent from 22700.85. As decline progresses, a drop below 18044.85 low is expected. However, substantial support is still expected from 61.8% retracement of 14597.31 to 22700.85 at 17692.86, and this could potentially spur a reversal. Let's see how it goes.

Fed minutes signal disagreement over rate pause

In a display of internal discord, Fed's June 13-14 meeting minutes indicate that while most officials deemed it "appropriate or acceptable" to maintain rates at 5% to 5.25% target range, a few would have backed a quarter-point increase.

"The participants favoring a 25 basis point increase noted that the labor market remained very tight, momentum in economic activity had been stronger than earlier anticipated, and there were few clear signs that inflation was on a path to return to the Committee's 2 percent objective over time," the minutes said.

Yet, many officials expressed concerns about an accelerated tightening pace. "Many also noted that, after rapidly tightening the stance of monetary policy last year, the Committee had slowed the pace of tightening and that a further moderation in the pace of policy firming was appropriate in order to provide additional time to observe the effects of cumulative tightening and assess their implications for policy," read the minutes.

Overall, these June minutes portray a Federal Reserve grappling with the delicate balancing act of controlling inflation while not excessively tightening monetary policy. The diverging views underscore the precarious position the central bank finds itself in as it navigates the complexities of the evolving economic landscape.

Fed Williams: Data support more rate hikes at some point

New York Fed President John Williams voiced his support for the decision to hold rates steady in June, stating yesterday that it was the right move to allow for further data collection and assessment.

"We can take some time and assess and collect more information and then be able to act, knowing that we also communicated through our projections that we don't think we're done, based on what we know," he said.

However, Williams hinted at further rate hikes while he reaffirmed his commitment to be "data dependent" in his decision-making. But he added that recent data "support the idea the Fed may need to raise rates further at some point."

Williams' statements were grounded in ongoing concerns about high core inflation, although he acknowledged the progress made in curtailing inflation so far. He highlighted a slowdown in the inflation of non-housing services prices, a key indicator closely watched by Fed officials. "Even in the category of core services excluding shelter, we're seeing some slowing of inflation," he added.

Looking ahead

Germany factory orders, UK construction PMI and Eurozone retail sales will be released in European session. Later in the day, focuses will be on US ADP employment, jobless claims and ISM services. US and Canada will also release trade balance.

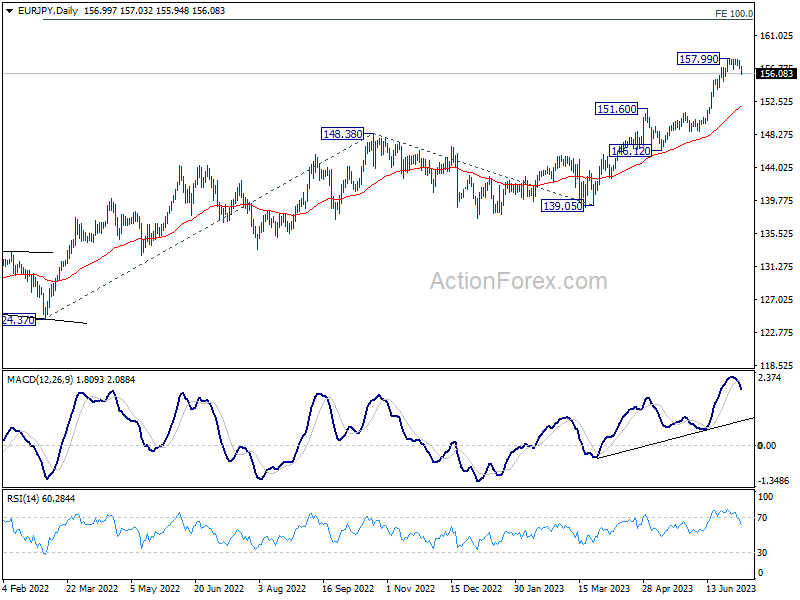

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.63; (P) 157.18; (R1) 157.56; More....

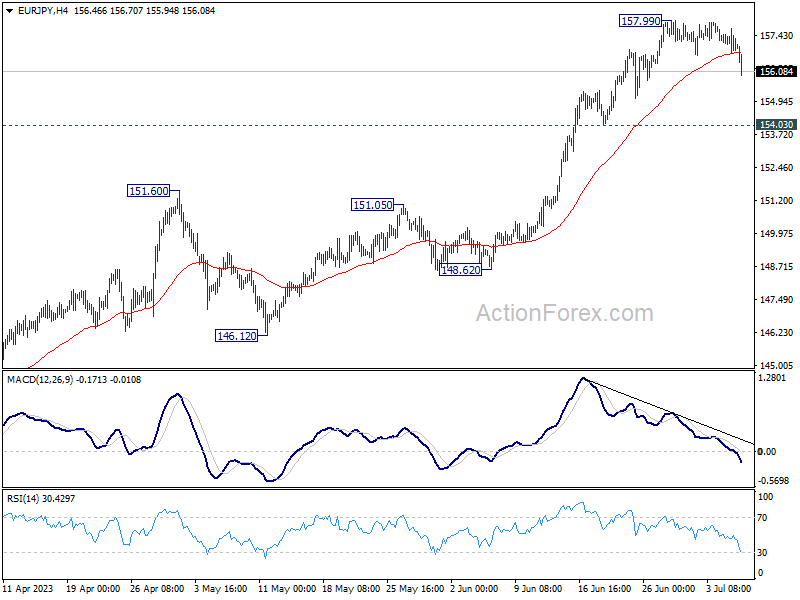

EUR/JPY's fall from 157.99 is extending lower today and intraday bias is now on the downside with strong break of 55 4H EMA. Deeper correction could be seen to 154.03 support or below. But overall outlook will stay bullish as long as 151.60 resistance turned support holds. Larger rally is still expected to resume through 157.99 after the correction completes.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 151.60 resistance turned support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) May | 11.79B | 10.70B | 11.16B | |

| 06:00 | EUR | Germany Factory Orders M/M May | 1.50% | -0.40% | ||

| 08:30 | GBP | Construction PMI Jun | 50.9 | 51.6 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M May | 0.20% | 0.00% | ||

| 11:30 | USD | Challenger Job Cuts Jun | 286.70% | |||

| 12:15 | USD | ADP Employment Change Jun | 250K | 278K | ||

| 12:30 | USD | Initial Jobless Claims (Jun 30) | 249K | 239K | ||

| 12:30 | USD | Trade Balance (USD) May | -68.2B | -74.6B | ||

| 12:30 | CAD | Trade Balance (CAD) May | 1.5B | 1.9B | ||

| 13:45 | USD | Services PMI Jun F | 54.1 | 54.1 | ||

| 14:00 | USD | ISM Services PMI Jun | 51.3 | 50.3 | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | -9.6M |

HK HSI dives as Yellen visit China amid rising US-China tensions

Hong Kong HSI is taking a hit today as it gapped down at open and further sell-offs materialized during the initial part of Asian trading session. This market movement mirrors intensifying investor concerns as US Treasury Secretary Janet Yellen starts a four-day visit to China. While the intention behind Yellen's visit is to de-escalate potential conflicts between these two economic behemoths, atmosphere has notably soured this week.

Earlier in the week, China struck a discordant note by announcing fresh restrictions on export of several critical minerals used in manufacture of semiconductors and solar panels. This move appears to be a tit-for-tat response to the tech export limitations that the US has imposed on China, limiting the sale of advanced computer chips. Further adding to the apprehension, US government is reported to be contemplating additional measures to restrict China's access to US-based cloud computing services.

On a separate front, China delivered another blow to international diplomatic relations when it abruptly canceled a visit by European Union foreign policy chief Josep Borrell, scheduled for next week, according to an EU spokesperson. The Chinese authorities have not yet disclosed the reasons behind this unexpected cancellation.

From a technical perspective, today's market turbulence in Hong Kong, marked by a gap down followed by a sharp drop, appears to validate rejection by 55 D EMA (now at 19428.57). Fall from 20155.92 is likely to be another chapter in the overall descent from 22700.85. As decline progresses, a drop below 18044.85 low is expected. However, substantial support is still expected from 61.8% retracement of 14597.31 to 22700.85 at 17692.86, and this could potentially spur a reversal. Let's see how it goes.

Fed Williams: Data support more rate hikes at some point

New York Fed President John Williams voiced his support for the decision to hold rates steady in June, stating yesterday that it was the right move to allow for further data collection and assessment.

"We can take some time and assess and collect more information and then be able to act, knowing that we also communicated through our projections that we don't think we're done, based on what we know," he said.

However, Williams hinted at further rate hikes while he reaffirmed his commitment to be "data dependent" in his decision-making. But he added that recent data "support the idea the Fed may need to raise rates further at some point."

Williams' statements were grounded in ongoing concerns about high core inflation, although he acknowledged the progress made in curtailing inflation so far. He highlighted a slowdown in the inflation of non-housing services prices, a key indicator closely watched by Fed officials. "Even in the category of core services excluding shelter, we're seeing some slowing of inflation," he added.

Fed minutes signal disagreement over rate pause

In a display of internal discord, Fed's June 13-14 meeting minutes indicate that while most officials deemed it "appropriate or acceptable" to maintain rates at 5% to 5.25% target range, a few would have backed a quarter-point increase.

"The participants favoring a 25 basis point increase noted that the labor market remained very tight, momentum in economic activity had been stronger than earlier anticipated, and there were few clear signs that inflation was on a path to return to the Committee's 2 percent objective over time," the minutes said.

Yet, many officials expressed concerns about an accelerated tightening pace. "Many also noted that, after rapidly tightening the stance of monetary policy last year, the Committee had slowed the pace of tightening and that a further moderation in the pace of policy firming was appropriate in order to provide additional time to observe the effects of cumulative tightening and assess their implications for policy," read the minutes.

Overall, these June minutes portray a Federal Reserve grappling with the delicate balancing act of controlling inflation while not excessively tightening monetary policy. The diverging views underscore the precarious position the central bank finds itself in as it navigates the complexities of the evolving economic landscape.

U.S. Dollar Strength to Continue Until Inflation Beast is Quelled

Highlights

- The U.S. dollar had an incredible run throughout much of 2022 as the Federal Reserve embarked on its historic rate hiking cycle to curtail the worst bout of inflation in forty years.

- With inflation pressures proving more persistent than anticipated, global central banks are poised to continue their rate hiking campaigns and keep policy rates higher for longer.

- The cumulative tightening of central banks will slow global economic activity, with the most deleterious effects in Europe, where central banks will remain in tightening mode for longer. Heightened uncertainty and relative U.S. economic outperformance is likely to push the trade-weighted dollar higher over the remainder of this year.

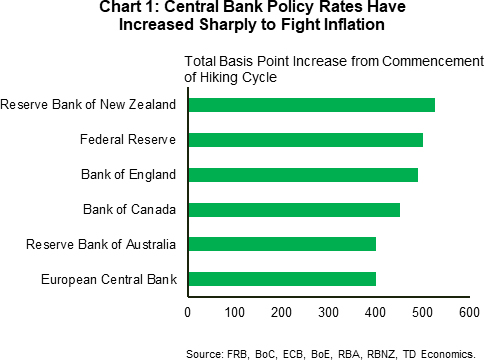

After a slow response to accelerating inflation, central banks have spent the last two years playing catch up with rapid increases in policy rates. The Federal Reserve has been one of the most aggressive, raising the federal funds rate from the zero lower bound to a range of 5.0%-5.25%, before pausing in June (Chart 1).

The Fed’s front-loaded rate increase led to hefty gains in the U.S. dollar against most major currencies over the course of last year. However, as other central banks caught up, the trade-weighted dollar retreated and has spent most of this year moving sideways.

This may be about to change. The swift actions of global central banks have started to show progress in bringing down inflation, but the job is not yet done. Wringing the remaining inflation out is likely to require a meaningful weakening in economic growth, with countries facing the stickiest price growth paying the highest costs. As recession fears mount, American economic outperformance in combination with the dollar’s safe-haven status is likely to lead to newfound U.S. dollar strength over the second half of this year.

Central Banks’ Job is Not Quite Done

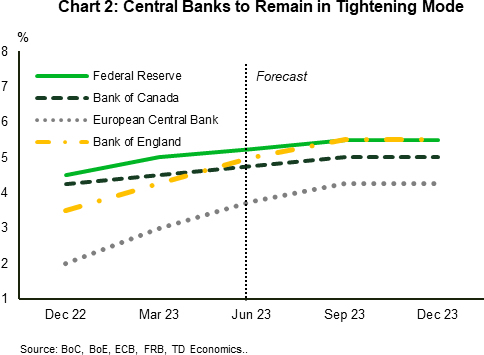

Central banks are poised to remain in tightening mode for the remainder of the year, with relatively more hikes in store from central banks in Europe and the UK, which have made slower progress on curtailing price pressures (Chart 2).

The Fed’s aggressive rate hikes to date mean it is close to the end of its journey. After pausing in June, the Federal Reserve is likely to raise the federal funds rate just one more time. This is as much a testimony to the resilience of economic activity in the face of higher interest rates as it is to stubborn inflation. Activity in several interest-rate sensitive sectors, most notably the U.S. housing sector, has accelerated in recent months.

Elsewhere, after pausing its rate hiking campaign in March, the Bank of Canada (BoC) surprised financial markets with a 25-basis point (bps) hike in June, responding to higher-than-anticipated inflation. The BoC is likely to administer one additional rate hike, though a pullback in inflation in May makes this a close call.

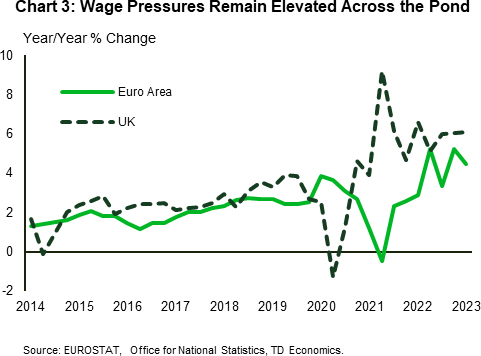

Across the pond, inflation in both the UK and euro area has proven to be more persistent than in North America with much of the retreat in the headline number coming from falling energy prices. Policy makers face an additional obstacle in curtailing price pressures with wage growth remaining elevated (Chart 3).

All this points to the European Central Bank (ECB) and the Bank of England (BoE) continuing their tightening campaigns longer than either the Fed or the BoC. We expect three additional rate hikes from the ECB, while the BoE will continue to be the most aggressive central bank even after surprising markets with a 50-bps hike at its June meeting.

Cloudy Economic Outlook Will Benefit the Greenback

With central banks at different points in their fight against inflation, the impact of additional tightening is likely to vary across countries. Economies that have been more resilient to the cumulative effects of central bank tightening and made the most progress in reducing inflation, are better positioned to withstand additional rate hikes.

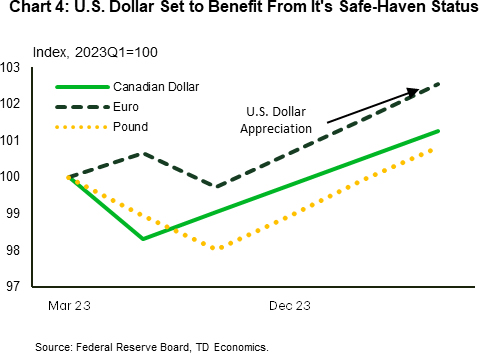

The euro area is starting from a position of weakness, with real GDP having contracted in the final quarter of 2022 and the first quarter of 2023. While higher energy costs strained consumers wallets earlier this year, higher borrowing costs will exert further drag on economic growth. The euro area faces additional headwinds through trade channels as concerns over the economic recovery in China – one of its main trading partners, continue to mount. The uncertainty surrounding the euro area is likely to be reflected in a period of near-term weakness in the euro against the U.S. dollar (Chart 4).

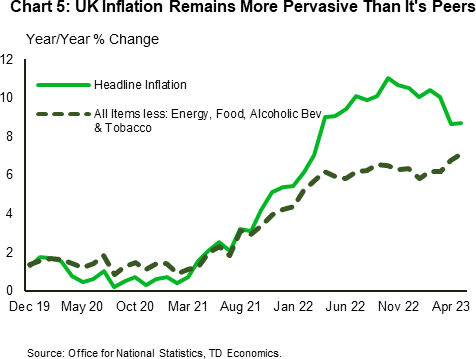

The story in the UK is also dour, with inflation remaining more pervasive than its peers and underlying price pressures reaching their highest levels since 1992 (Chart 5). Economic growth has slowed markedly and is expected to remain muted as the BoE pushes forward with additional rate hikes. The economy could face additional headwinds from rising mortgage costs that could put further stain on consumers. All told, softening economic growth in the UK will likely spell near-term downside risk for the pound against the dollar.

The Canadian dollar (CAD), meanwhile, looks set to extend the trend of near-term weakness against the dollar. While the aggressive actions of the BoC cushioned the CAD’s slide against the greenback, heightened global uncertainty and flight-to-safety flows are likely to benefit the U.S. dollar against the loonie over the next year.

Bottom Line

The performance of the dollar over much of 2022 was a classic case of textbook economics where relatively higher U.S. interest rates bolstered the dollar. While the dollar retreated from its 2022 highs as other central banks joined the fight against inflation, the higher interest rate environment has created headwinds for the global economy that are unlikely to abate any time soon. In this environment of heightened global uncertainty, flight-to-safety inflows are likely to push the dollar higher. Only once economic uncertainty abates is the dollar likely to see some reversal.

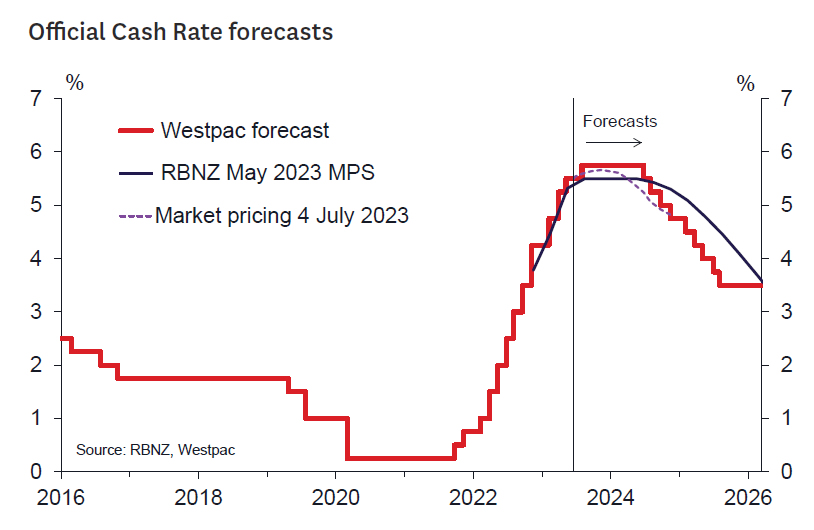

From “Fast and Furious” to “Frozen” – RBNZ to keep the OCR on hold

- The Reserve Bank will leave the OCR at 5.50% at its July policy review.

- The RBNZ likely sees recent data as in line with their projected peak in the OCR.

- The accompanying statement should be concise to avoid misinterpretation.

- The RBNZ might take the opportunity to communicate a more data-driven future approach than communicated in the May Monetary Policy Statement.

We expect the Reserve Bank to leave the OCR unchanged at 5.50% at next Wednesday's monetary policy review. In the May Monetary Policy Statement the RBNZ gave markets a strong steer that it expected that no further increases in the OCR would be required and that now is the time to "watch, worry and wait". In signalling this 'end of cycle' stance, the RBNZ was at pains to emphasize that there was no case to expect any cuts to the OCR for a good while yet. The RBNZ's forecasts indicated that the first easing in policy would need to wait until late next year.

The data flow since May will likely have given comfort to the RBNZ that its on-hold stance is appropriate – at least for now. The key piece of information was the release of March quarter GDP which came in close to Westpac's own forecasts but was weaker than the RBNZ's. Hence from their perspective, the economy started the year in a slightly less overheated position than might have been feared when they produced their May

Statement. Given the RBNZ's strident on-hold stance this data alone will probably be enough to keep rates unchanged this time around.

Other recent developments paint a mixed picture of the risks for inflation and future interest rates. Some downside risks for domestic inflation and interest rates are accumulating in the form of the weaker than expected bounce back of the Chinese economy, with implications for export demand (reflecting this, in June Westpac revised down its forecast of the farmgate milk price). Many indicators of domestic demand seem consistent with a cooling economy – for example the retail and construction sectors seem to be evolving as one should expect given the interest rate increases that we have already seen. The corporate tax take is also weakening.

On the other side of the ledger, global central banks are generally finding inflation to be more resilient than anticipated and have upgraded their view of the likely peak in policy rates. The RBNZ will be aware of the risks of repeating the mistake of drawing the tightening cycle to an end too early and having to change tack should the economy and inflation prove more resilient. Some domestic indicators are consistent with lingering economic resilience. In particular, the labour market has not cracked yet – while migration has surged, jobs growth is still outstripping increases in the population. Consumer and business confidence looks to have found a base with the latter seeming quite strong if the top of the tightening cycle is really in place. The housing market has also found a bottom probably somewhat sooner than the RBNZ probably had factored in. Market pricing still reflects a risk of a further increase in the OCR this year (and Westpac retains its call for a 25-point increase in August).

It's likely the RBNZ's commentary accompanying the onhold stance will be brief. Saying too much raises the risk of misinterpretation and might lead markets to price in rate cuts or increases that the RBNZ won't want to endorse right now. The main message we might expect to see is that the future direction of interest rates is data-dependent, so as to to leave room for the RBNZ to shift tack should upside (or downside) risks to the inflation profile accumulate. We think that this "data-dependent" message may have gotten a bit lost in the on-hold messaging at the May Statement.

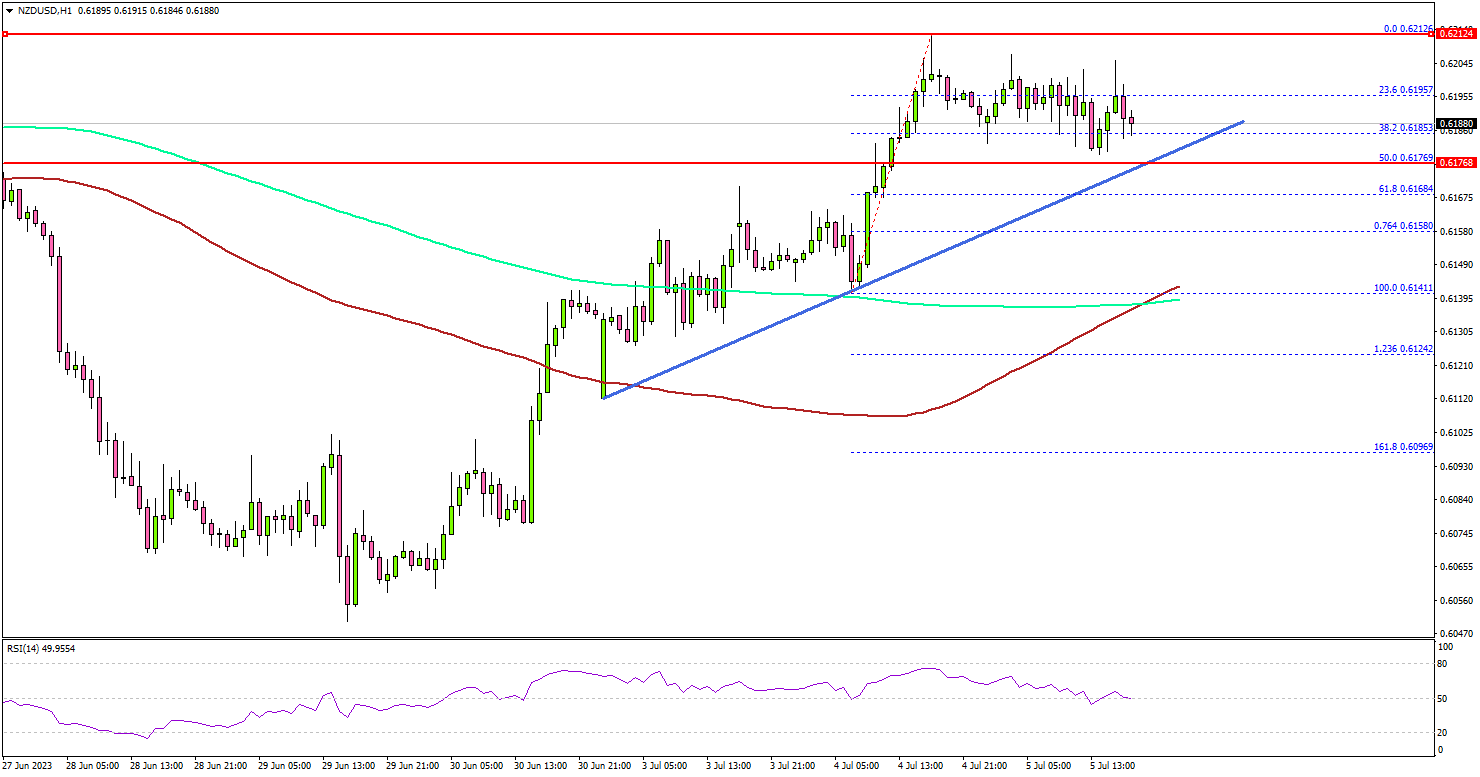

NZD/USD Consolidates Gains, US Jobs Report Next

Key Highlights

- NZD/USD climbed higher above the 0.6150 resistance.

- A major bullish trend line is forming with support near 0.6175 on the 4-hour chart.

- AUD/USD is facing a major hurdle near 0.6710 and 0.6745.

- The US ADP employment could change by 228K in June 2023, down from 278K.

NZD/USD Technical Analysis

The New Zealand Dollar found support near 0.6050 and started a fresh increase against the US Dollar. NZD/USD climbed above the 0.6100 and 0.6120 resistance levels.

Looking at the 4-hour chart, the pair climbed above the 0.6150 resistance zone, the 200 simple moving average (green, 4 hours), and the 100 simple moving average (red, 4 hours).

The pair even spiked above the 0.6200 level. A high is formed near 0.6212 and the pair is now consolidating gains. There was a minor decline below 0.6200. The pair dipped below the 23.6% Fib retracement level of the upward move from the 0.6141 swing low to the 0.6212 high.

Immediate support is near the 0.6175 level. There is also a major bullish trend line forming with support near 0.6175 on the same chart.

The next major support is near the 0.6160 level or the 76.4% Fib retracement level of the upward move from the 0.6141 swing low to the 0.6212 high. If there is a downside break below the 0.6160 support, the pair could decline toward the 100 simple moving average (red, 4 hours).

On the upside, the first major resistance is near 0.6210. The next major resistance is near 0.6240. If there is a move above the 0.6240 resistance, the pair could rise toward 0.6300. Any more gains might send NZD/USD toward the 0.6350 level.

Looking at AUD/USD, the pair started an upside correction but it is still well below the key resistance at 0.6745.

Economic Releases

- US ADP Employment Change for June 2023 - Forecast 228K, versus 278K previous.

- US Initial Jobless Claims - Forecast 245K, versus 239K previous.

- US ISM Services Index for June 2023 – Forecast 51.0, versus 50.3 previous.

Fed Minutes Send Bond Yields Higher

The Fed minutes showed that policymakers were divided and that the hawks will still want to deliver more tightening. Fed Officials are concerned a tight labor market will make inflation tight throughout the rest of the year. If inflation remains persistent, that could be a gamechanger for inflation expectations. Wall Street was getting comfortable with higher for a little bit longer, but they are not ready to price in more than a half-point in rate hikes. In order to conquer inflation the Fed seems set on forecasting a mild recession, which is very much different than Powell’s slower growth call.

In the end, the fate of these Fed policy decisions will depend on the data and right now both the labor market and inflation readings are expected to soften over the next week. Friday’s NFP report is expected to show job growth cooled from 339,000 to 225,000, while the unemployment rate ticks lower to 3.6%. The June inflation report is going to show the base effects help the disinflation process as the headline year over year reading falls from 4.0% to 3.0%. Some analysts are making the case for a 2.8% reading, which seems relatively close to the Fed’s target. The problem for the Fed is that inflation will likely rise over the coming months.

The dollar will play tug-of-war with the majors as the risk of more Fed tightening is debated, while the Europeans struggle to bring inflation down.

Fed’s Williams spoke after the close and his comments support the case for more rate hikes. Williams noted that the data supports more action and that the Fed’s work is not done.

Fed rate hike expectations have edged a little higher for the July 26th meeting, but the peak rate remains steady. The yield on the 10-year Treasury yield rose 7.7 bps to 3.932%.

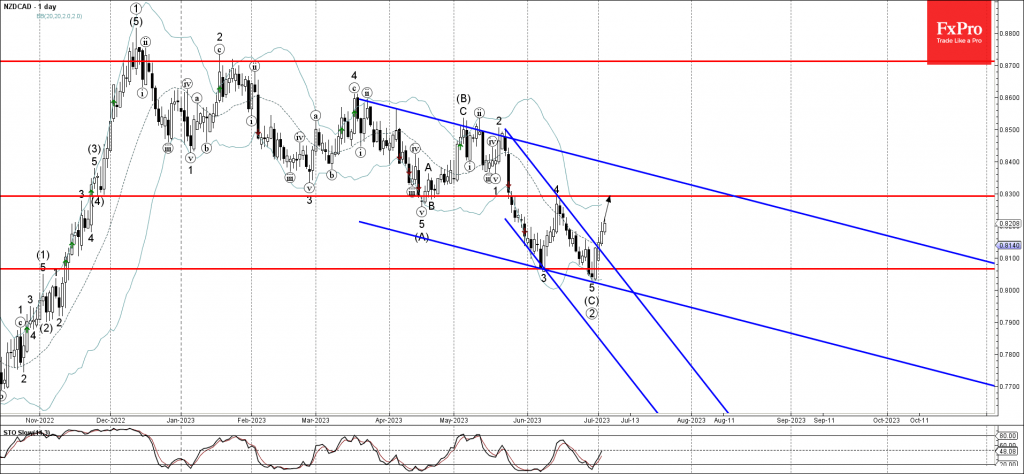

NZDCAD Wave Analysis

- NZDCAD broke accelerated down channel

- Likely to rise to resistance level 0.8300

NZDCAD currency pair continues to rise inside the minor impulse wave 1,which started earlier with the daily Morning Star from the key support level 0.8066.

The active impulse wave 1 belongs to the primary upward impulse sequence (3) from the end of June.

Having recently broken the accelerated down channel from May, NZDCAD currency pair can be expected to rise further toward the next resistance level 0.8300 (top of the earlier minor correction 4 from last month).

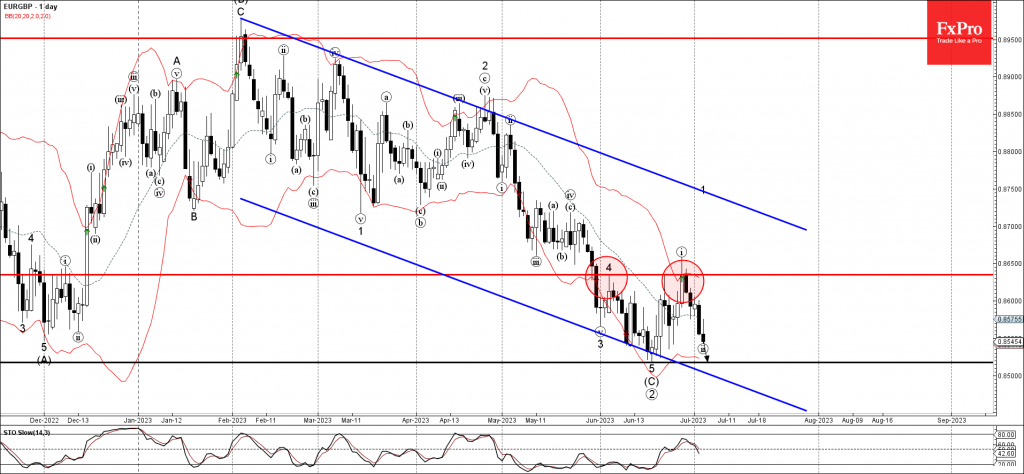

EURGBP Wave Analysis

- EURGBP falling inside wave (ii)

- Likely to reach support level 0.8515

EURGBP currency pair continues to fall inside the minor corrective wave (ii), which started earlier from the key resistance level 0.8635 .

The active corrective wave (ii) belongs to the higher order upward impulse wave 1 from last month.

Given the multi-month downtrend and the continued euro sales across the FX markets, EURGBP currency pair can be expected to fall further toward the next support level 0.8515 (previous monthly low from June).