Sample Category Title

EUR/JPY Daily Outlook

Daily Pivots: (S1) 154.84; (P) 155.38; (R1) 156.45; More....

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Current up trend should target 100% projection of 139.05 to 151.60 from 146.12 at 158.67. On the downside, break of 154.03 minor support will turn intraday bias neutral again and bring consolidations.

In the bigger picture, rise from 114.42 (2020 low) is in progress. Next target is 100% projection of 124.37 to 148.38 from 138.81 at 162.82. For now, medium term outlook will remain bullish as long as 148.38 resistance turned support holds, even in case of deep pull back.

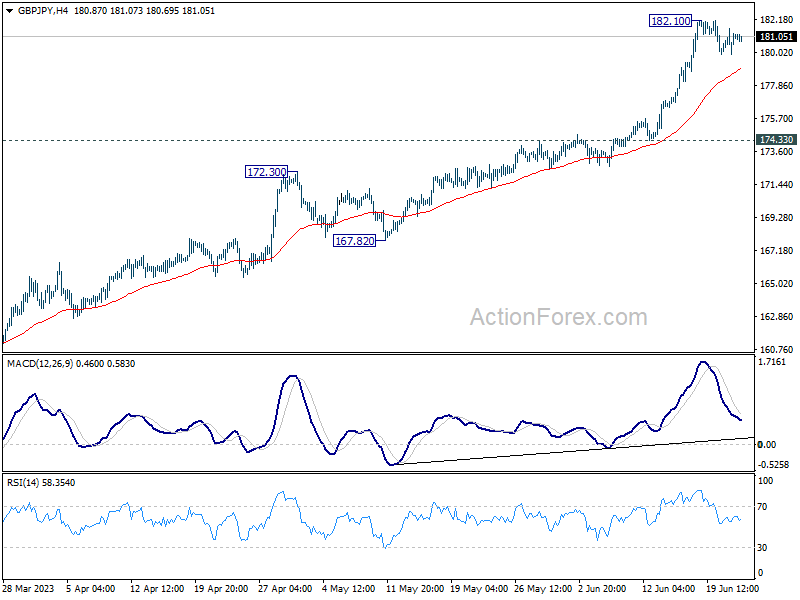

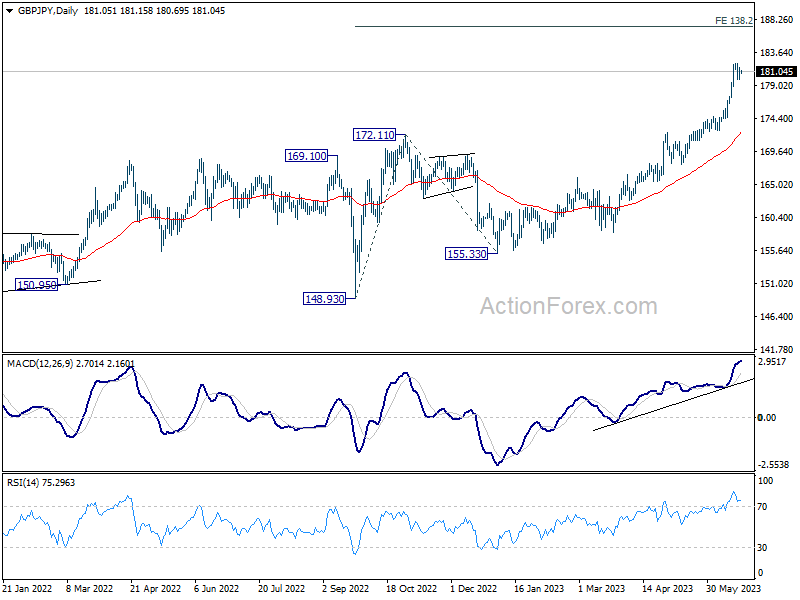

GBP/JPY Daily Outlook

Daily Pivots: (S1) 180.19; (P) 180.90; (R1) 181.86; More...

Intraday bias in GBP/JPY remains neutral as consolidation from 182.10 extends. Downside of retreat should be contained above 174.33 to bring another rally. Break of 182.10 will resume larger up trend to 138.2% projection of 148.93 to 172.11 from 155.33 at 187.36.

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target is 195.86 (2015 high). For now, medium term outlook will remain bullish as long as 172.11 resistance turned support holds, even in case of deep pull back.

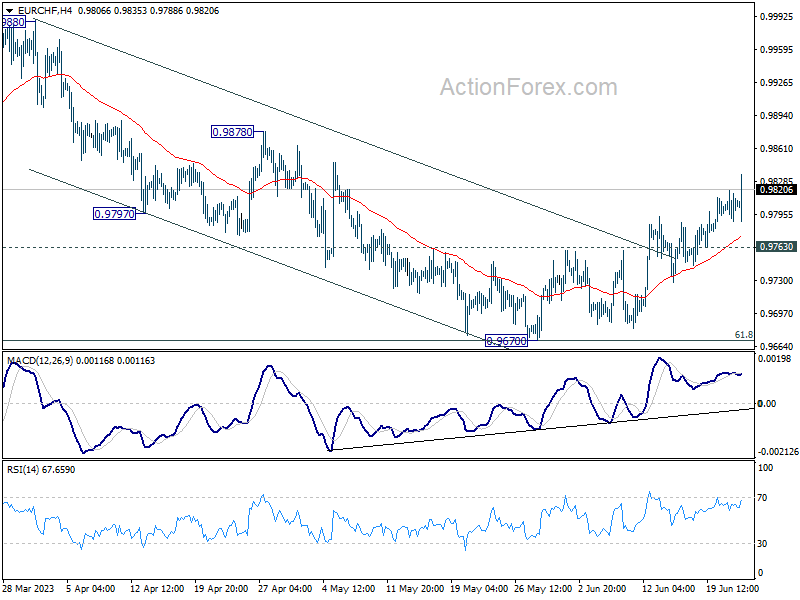

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9796; (P) 0.9808; (R1) 0.9826; More...

Intraday bias in EUR/CHF remains on the upside as rise from 0.9670 short term bottom continues today. As noted before, whole correction from 1.0995 could have completed at 0.9670 already. Further rally should be seen to 0.9878 resistance first. Firm break there should confirm this bullish case. On the downside, however, break of 0.9763 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, prior rejection by 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. The pair is also capped below 55 W EMA (now at 0.9924). Down trend from 1.2004 (2018 high) is not complete yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

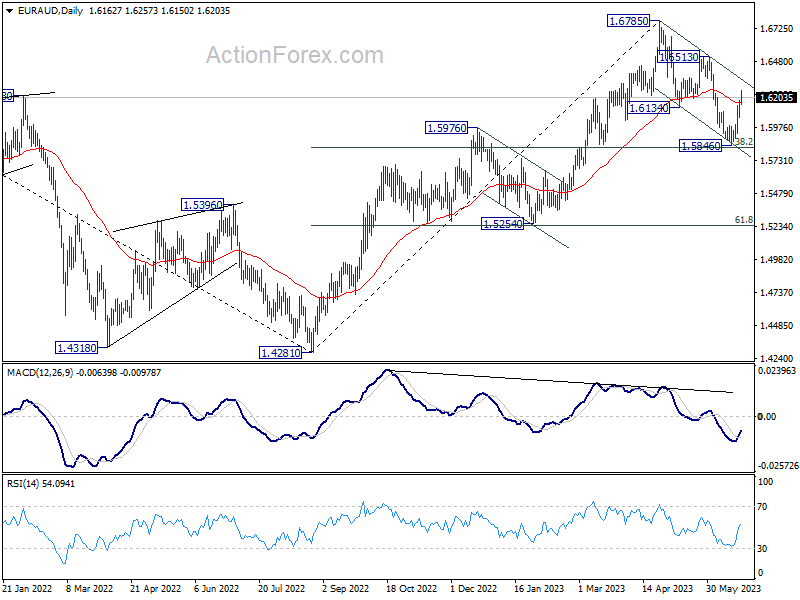

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6088; (P) 1.6137; (R1) 1.6215; More...

Intraday bias in EUR/AUD stays on the upside at this point. Corrective fall from 1.6785 should have completed with three waves down to 1.5846. Further rise should be seen to 1.6513 resistance next. On the downside, though, break of 1.6057 minor support will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, price actions from 1.6785 are seen as a correction to up trend from 1.4281 (2022 low) only. Strong support should be seen around 38.2% retracement of 1.4281 to 1.6785 at 1.5828 to complete the first leg and bring rebound. However, sustained trading below 1.5828 will raise the chance of trend reversal and target 61.8% retracement at 1.5238.

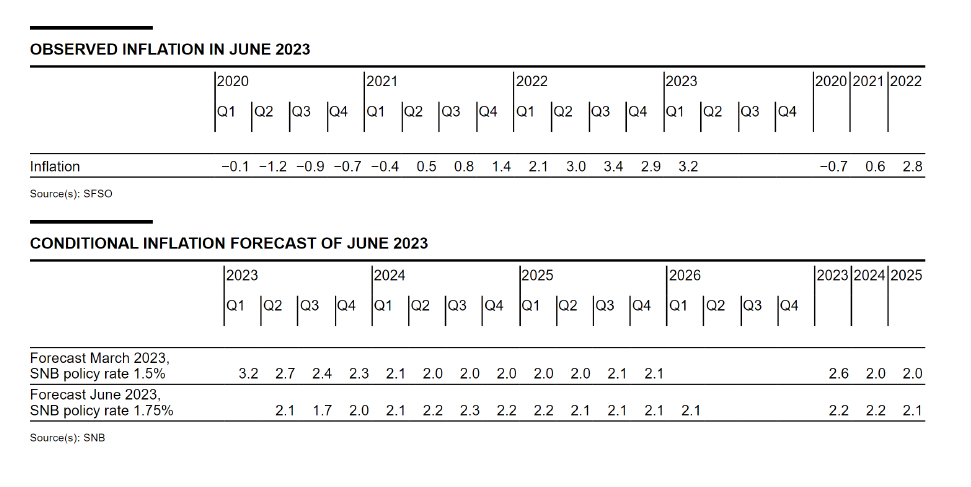

SNB hikes 25bps, inflation to fall to 1.7% in Q3 then bounce

SNB raises policy rate by 25bps to 1.75%, for "countering inflationary pressure, which has increased again over the medium term". The central bank also leaves the door open for more tightening, as "it cannot be ruled out that additional rises in the SNB policy rate will be necessary". SNB also maintains the willingness to intervene in the currency markets, with focus on "selling foreign currency".

In the new conditional forecast, 2023 inflation projection is lowered from 2.6% to 2.2%, down in from Q2 through Q4, with trough at 1.7% in Q3. However, 2024 and 2025 inflation projections are raised from 2.0% (both) to 2.2% and 2.1% respectively. Inflation is estimated to stay above 2% target from the tart of 2024 through Q1 2026, with a peak at 2.3% in Q3 2023.

Regarding the economy, SNB expects "modest growth" for the rest of the year. Overall GDP is to growth by 1.0% in 2023 and unemployment rise will "probably rise slightly". "Subdued demand from abroad, the loss of purchasing power due to inflation, and more restrictive financial conditions are having a dampening effect."

(SNB) Swiss National Bank tightens monetary policy further and raises SNB policy rate to 1.75%

The SNB is tightening its monetary policy further and is raising the SNB policy rate by 0.25 percentage points to 1.75%. In doing so, it is countering inflationary pressure, which has increased again over the medium term. It cannot be ruled out that additional rises in the SNB policy rate will be necessary to ensure price stability over the medium term. To provide appropriate monetary conditions, the SNB also remains willing to be active in the foreign exchange market as necessary. In the current environment, the focus is on selling foreign currency.

The SNB policy rate change applies from tomorrow, 23 June 2023. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate of 1.75% up to a certain threshold. Sight deposits above this threshold will be remunerated at an interest rate of 1.25%, and thus still at a discount of 0.5 percentage points relative to the SNB policy rate.

Inflation has declined significantly in recent months, and stood at 2.2% in May. This decrease was above all attributable to lower inflation on imported goods, in particular lower prices for oil products and natural gas.

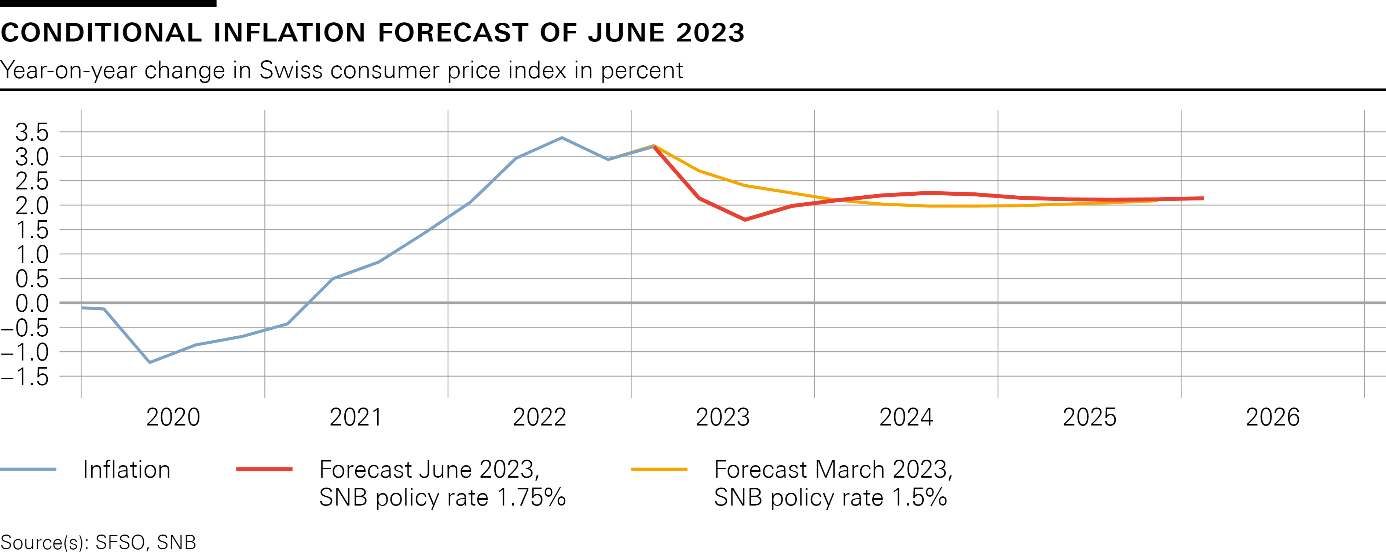

The new conditional inflation forecast is based on the assumption that the SNB policy rate is 1.75% over the entire forecast horizon (cf. chart 1). Through to the end of 2023, the new forecast is below that of March. The lower oil and gas prices and the stronger Swiss franc are having a dampening effect over the short term. From 2024 onwards, the new forecast is higher than in March, despite today's increase in the SNB policy rate. The reasons for this are ongoing second-round effects, higher electricity prices and rents, and more persistent inflationary pressure from abroad. The new forecast puts average annual inflation at 2.2% for 2023 and 2024, and 2.1% for 2025 (cf. table 1). Without today's policy rate increase, the inflation forecast would be even higher over the medium term.

Economic growth was modest in the advanced economies in the first quarter of 2023. Although inflation declined again in many countries, it remains clearly above central banks' targets. Core inflation in particular is still stubbornly elevated. Against this background, numerous central banks have tightened their monetary policy further, albeit at a somewhat slower pace than in the previous quarters.

The growth outlook for the global economy in the coming quarters remains subdued. At the same time, inflation is likely to remain elevated worldwide for the time being. Over the medium term, however, it should return to more moderate levels, not least thanks to the more restrictive monetary policy and due to the economic slowdown.

This scenario for the global economy remains subject to large risks. In particular, the high level of inflation in some countries could be more persistent than expected. Equally, the energy situation in Europe could deteriorate again in Q4 2023 and Q1 2024.

Swiss GDP growth was solid in the first quarter of 2023. The services sector gained momentum, and there was also a slight increase in value added in manufacturing. The labour market remained robust, and overall production capacity has been well utilised.

However, the SNB expects modest growth for the remainder of the year. Subdued demand from abroad, the loss of purchasing power due to inflation, and more restrictive financial conditions are having a dampening effect. Overall, GDP is likely to grow by around 1% this year. In this environment, unemployment will probably rise slightly, and the utilisation of production capacity is likely to decline somewhat.

The forecast for Switzerland, as for the global economy, is subject to high uncertainty. The main risk is a more pronounced economic slowdown abroad.

As regards the real estate market, price growth for single-family houses and privately owned apartments has slowed in recent quarters, while prices for apartment buildings have declined. Mortgage growth has remained largely unchanged. The vulnerabilities on the mortgage and real estate markets persist.

GBP Consolidates Gains

GBP/USD seeks support

Cable struggles as a flare up inflation last month sows doubt in the UK economy. A bearish RSI divergence showed a deceleration in the rally and a drop below 1.2770 prompted short-term buyers to bail out. May’s high of 1.2670 has turned into a fresh support to see if buyers would make their way back. Failing that, 1.2530 next to the bullish MA cross on the daily chart would be a major floor to maintain Sterling’s edge. The newly formed supply zone 1.2800-1.2850 is the obstacle to clear before the uptrend could resume.

USD/CAD breaks lower

The Canadian dollar advanced as April’s retail sales came out above expectations. The pair remains under pressure after it broke below November’s low of 1.3250. A bearish MA cross is likely to attract more selling interests in the near-term as previous buyers look to switch sides. 1.3270 is the first resistance to expect the bears to sell into strength and the support-turned-resistance of 1.3350 from the daily chart is a major level to lift to initiate a meaningful rebound. A fall below 1.3180 would extend the sell-off towards 1.3100.

US OIL awaits breakout

WTI crude bounces as traders expect the Fed to be near the end of the tightening after Powell’s testimony. As a show of resilience, the price has managed to stay above the critical floor of 66.00. A close above the first resistance of 71.60 has eased the downward pressure but the bulls will need to lift the recent peak of 73.50 before they could end the lengthy consolidation and push for a broader recovery above 76.00. On the downside, the psychological level of 70.00 is the first support to keep the current momentum intact.

US 30 Cash Index Edges Lower as Bearish Pressure Intensifies

The US 30 cash index has completed five red candles after again failing to decisively rally above 34,280. This level has morphed into a key sentiment area as over the past 10 months the bulls have registered six false breakouts. The US 30 index is currently hovering a tad above the 33,754 level but below the December 2, 2022 downward sloping trendline.

The momentum indicators appear to mostly favour the bears at this juncture. While the Average Directional Movement Index (ADX) is hovering below its 25-threshold and signaling a range-trading market, the RSI is edging lower, well below its recent peak. More importantly, the stochastic has broken below its overbought territory and it is moving lower in an almost vertical fashion.

Should the bears continue to push the index lower and manage to overcome the 61.8% Fibonacci retracement of the January 5, 2022 – October 3, 2022 downtrend at 33,754, they would then target the arguably more important 33,353-33,606 area. The combination of the 50- and 100-day simple moving averages (SMAs) and the October 1, 2021 low means that the bears’ determination would really be put to the test there.

On the flip side, the bulls would love a retest of the August 16, 2022 high at 34,280 but they firstly have to break the December 2, 2022 downward trendline. The December 13, 2022 high at 34,930 would be the next aim, a tad below the busier 35,091-35,496 range defined by the April 21, 2022 and May 10, 2021 highs respectively.

To sum up, the US 30 cash index bulls’ inability to break the 34,280 level has given the bears the opportunity to take control of the market.

Hawkish Powell Weighs on Stocks, 50 Basis Points on the Table for BoE

European stocks are poised to open a little lower on Thursday, tracking moves we saw in the US on Wednesday following Jerome Powell's appearance in Congress.

The Fed Chair appeared before the House Financial Services Committee and very much stuck to last week's script, which should come as a surprise to no one. Inflation is not under control and the vast majority at the Fed believe more rate hikes will be warranted was the message, although we got that from the dot plot.

For once, markets are buying what the Fed is selling and have priced in a 70% chance of a hike in July. But that's where they believe it ends with the easing cycle then starting around the turn of the year so the Fed and the markets aren't entirely on the same page. The data will likely determine whether markets remain in agreement on July as I imagine it will take less to convince investors that another hike isn't warranted than the Fed.

Will the BoE be tempted to hike by 50 basis points?

What the Bank of England would do to be in a position to be debating whether another rate hike or two is even necessary. Instead today, the debate will be whether 25 basis points is even enough or if it should revert back to 50. The central bank has made almost no progress in getting inflation back to 2%, in fact, core inflation is still rising which should be causing some alarm on the MPC.

Aside from the decision itself, the vote will be very interesting today. At each of the last three meetings, two policymakers have voted for a pause. Will they stand firm today or accept that more is needed and what will that hawkish pivot do to interest rate expectations? They're already pretty hawkish, with the terminal rate seen at around 6% early next year but that could cement the view that much more is needed.

Oil remains choppy but edging towards the upper end of its range

Oil prices remain very volatile as we've seen over the last week. Trading has been very choppy as traders have tried to reconcile weaker Chinese growth, slightly more modest support from the PBOC, more hawkish central banks, and resilient economies. We appear to be in a position where we're either waiting for the economy to break or for central banks to achieve their soft landing aims.

Brent remains in its lower trading range for this year between $70-$80 but we are getting closer to the upper end of that and there's still plenty of momentum in the move. A break above $80 could be a very bullish development and suggest traders are feeling less pessimistic about the economy.

Gold sell-off losing momentum ahead of the BoE

Gold has been seriously testing its recent range lows over the last 48 hours but so far it's struggling to generate enough momentum for a significant move lower. Despite Powell's hawkish delivery in Congress, the yellow metal recovered earlier losses to close only marginally lower on the day, albeit below the lower end of the $1,940-$1,980 range it previously largely traded within.

Ahead of day two of his testimony, this time in front of the Senate, gold is trading relatively flat and potentially in need of another bearish catalyst. The sell-off is losing momentum although it could get an extra nudge from the BoE if we see a more hawkish shift.

Multiple Central Banks Decide on Monetary Policy

Markets

(Much) higher than expected May UK inflation temporarily sent trembles through global bond markets yesterday morning, but in the end spill-overs outside the UK remained limited. With headline inflation holding at 8.7% Y/Y (0.7% M/M) and core inflation accelerating from 6.8% to 7.1%, pressure on the Bank of England is mounting the reaccelerate the pace of rate hikes starting at today’s meeting. The 2-y initially jumped more than 15 bps (new top near 5.1175%), but yields closed off the intraday highs (2-y +9.3 bps; 30-y +5.9 bps). Even so, uncertainty on today’s BoE action prevented sterling to profit from higher yields. Investors scaled back sterling longs. EUR/GBP jumped from the 0.8530 area after the release to even close just north of the 0.86 big figure. Fed’s Powell in its testimony before the House held close to last week’s post FOMC assessment. Explaining last week’s ‘pauze’, the Fed chair indicated that at current point in the hiking process, it makes sense to move rates higher but at more moderate pace. However, the Fed still has quite a way to go inflation. In this respect, he sees two additional rate hikes as guided in the new dots as a good guess. Powell’s ‘hawkish’ rhetoric only had a limited impact on US interest rates. The US curve also turned further inverse (2-y +3 bps; 30-y -0.4 bps). On this side of the Atlantic, German yields added between 3.7 bps (5-y) and 2.6 bps (2-y), the very long end outperforming (-0.6 bps). Powell’s anti-inflationary commitment at least didn’t help the dollar. DXY dropped from the 102.7 area pre Powell to close near 102.10. The euro again outperformed. EUR/USD even clear the June top to close at 1.097. The yen again underperformed. USD/JPY finished near 141.88. EUR/JPY even closed at a new multi-year top (155.89). Equities on both side of the Atlantic fell prey to further profit taking (EuroStoxx 50 -0.47%, S&P -0.52%, Nasdaq -1.21%).

Today, multiple central banks including the Norges Bank (NB), the Swiss National Bank (SNB), the national bank of Turkey and of course the Bank of England will decide on monetary policy. The SNB and the Norges Bank are expected to raise rates by 25 bps, but for the NB it might be a close call (25 bps step or 50 bps). For the CBRT, markets look out for a U-turn in policy after the post-election change at the helm of the CBRT (hike expected from 8.5% to 20.0%). Markets evidently will be keen the see the BoE reaction after several months of higher than expected inflation. Money markets are uncertain whether this will immediately translate into a 50 bps step. Whatever the decision, the BoE will have to strengthen its guidance/anti-inflationary commitment. The potential negative impact of tighter policy on growth and on other UK assets yesterday was a negative for sterling. Even in case of more decisive BoE action, we stay cautious on sterling.

News and views

The Bank of Canada at the June meeting deliberated a hike or hold and flag an increase for July meeting. It opted for the former (to 4.75%) after holding rates constant since January. "Members were of the view that with the resurgence in household spending growth, the pickup in consumer confidence, and the slowing in disinflationary momentum, monetary policy did not look to be sufficiently restrictive," the minutes read. It sticks to a data-dependent approach. Since the June gathering, Canada unexpectedly lost jobs in a possible sign of a softening labour market, but April retail sales were much stronger than expected. In this respect, the "Governing Council agreed that the economy remained clearly in excess demand and that the rebalancing of supply and demand was likely to take longer than previously expected". The Canadian dollar appreciated against the dollar yesterday with an intraday 2% oil rise supporting the move. It was nevertheless mainly a USD move though, following fainting US yields during Fed chair Powell’s testimony. USD/CAD dipped to 1.3164, the lowest level since September 2022.

The Brazilian central bank kept the Selic rate steady at 13.75% yesterday for a seventh meeting straight. It dropped language pledging rate hikes could resume if inflation doesn’t follow the projected path but stuck to the idea that rates should be high for a long enough period to ensure inflation, 3.94% in May, reverses back to target (3.25% this year and 3% in 2024 and 2025). Interestingly, the statement steers clear from hinting at rate cuts, ignoring increasingly louder calls from president Lula and his government. The central bank lowered its inflation forecast for this year to 5% from 5.8% and cut the one for next year to 3.4% from 3.6%. Brazil’s real finished near intraday highs vs the USD yesterday. The close at 4.764 was the weakest since June last year.