Sample Category Title

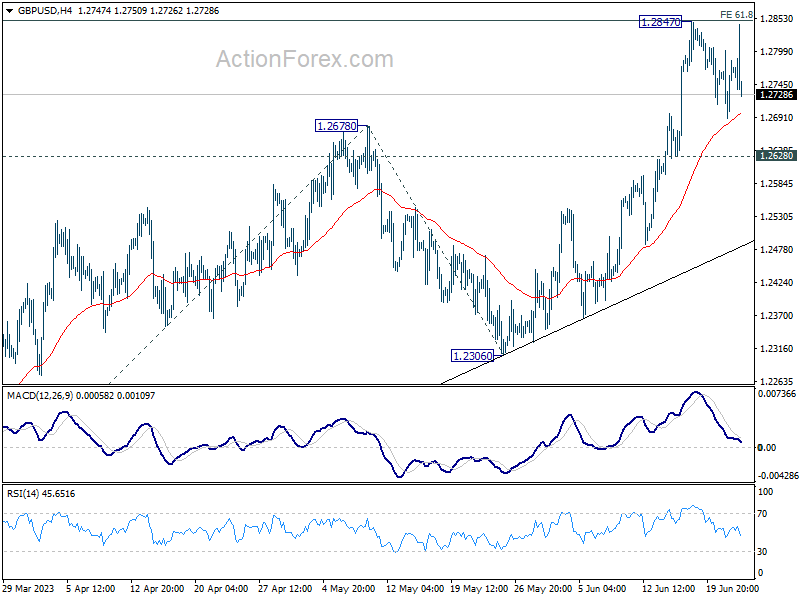

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2754; (R1) 1.2815; More...

GBP/USD failed to break through 1.2847 resistance today, and stays in consolidations. Intraday bias remains neutral for the moment. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next. However, firm break of 1.2628 will turn bias to the downside, for deeper fall to 1.2306 support instead.

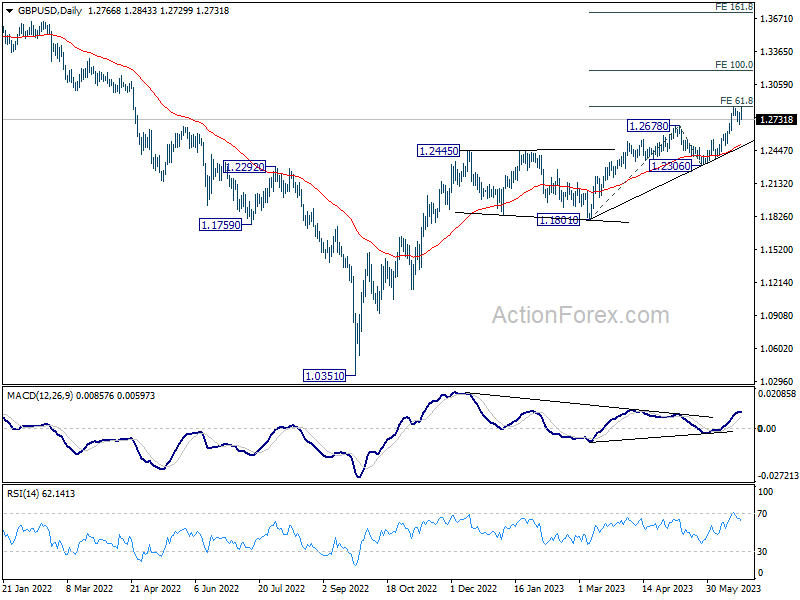

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

BoE and SNB Rate Hikes Add Spice, But Lack Impact

The market witnessed some ups and downs today with BoE and SNB rate decisions stirring the waters. However, these movements failed to usher in a sustainable trend, as both currencies remain shackled within yesterday's range against most major counterparts. BoE's larger than expected rate hike sparked initial momentum but the impact quickly faded quickly. The impact of offset by repeated emphasis that inflation is going to fall significantly in the coming months. On the other hand, SNB's new economic projection has left market players scratching their heads. The projection sees CPI dipping below target this year before a bounce-back, adding to the uncertainty.

Taking a broader view of the week, Euro emerges as the star performer, the Canadian Dollar and Swiss Franc following behind. Australian Dollar, on the other hand, finds itself at the tail end of the performance spectrum, with New Zealand Dollar and Sterling keeping it company. Dollar and Japanese Yen are holding their ground for now, standing on the sidelines waiting for clearer signals from the risk markets. Hopefully, tomorrow's release of PMI data from various countries and regions might just be the catalyst needed to trigger decisive market movements.

Technically, EUR/CHF's rally from 0.9670 continues today. With SNB risk now cleared, the rise remains on track to 0.9878 resistance. Decisive break there will add to the case that whole correction form 1.0095 has completed, and target a test on this resistance. Strength in EUR/CHF should help cushion any pull back attempts in Euro.

In Europe, at the time of writing, FTSE is down -0.96%. DAX is down -0.45%. CAC is down -0.88%. Germany 10-year yield is up 0.0461 at 2.486. Earlier in Asia, Nikkei dropped -0.92%. Japan 10-year JGB yield rose 0.0051 to 0.379. Singapore Strait Times dropped -0.04%.

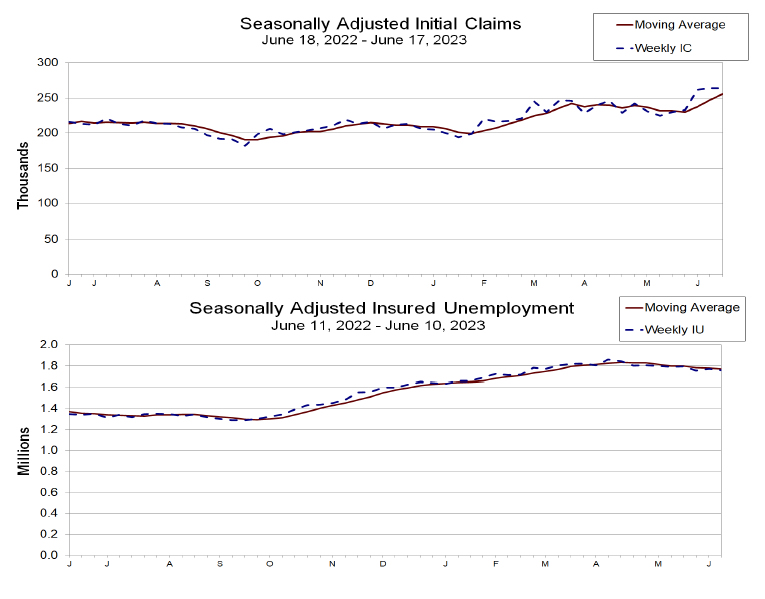

US initial jobless claims unchanged at 264k

US initial jobless claims was unchanged at 264k in the week ending June 17, above expectation of 256k. Four-week moving average of initial claims rose 8.5k to 256k highest since November 13, 2021.

Continuing claims dropped -13k to 1759k in the week ending June 10. Four-week moving average of continuing claims dropped -7.5k to 1770.

BoE hikes 50bps by 7-2 vote, further tightening could be required

BoE raises Bank Rate by 50bps to 5.00%, larger than consensus of 25bps. The decision was made by 7-2 vote, with only known dove Swati Dhingra and Silvana Tenreyro voted for no change again.

Tightening bias is maintained as the central bank noted, "if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required."

BoE continues to expect CPI to "fall significantly further during the course of the year". Services CPI is projected to "remain broadly unchanged in the near term". Meanwhile, core goods CPI is expected to "decline later this year".

Second-round effects in domestic price and wage developments are "likely to take longer to unwind than they did to emerge". There has been "significant upside news in recent data that indicates more persistence in the inflation process."

SNB hikes 25bps, inflation to fall to 1.7% in Q3 then bounce

SNB raises policy rate by 25bps to 1.75%, for "countering inflationary pressure, which has increased again over the medium term". The central bank also leaves the door open for more tightening, as "it cannot be ruled out that additional rises in the SNB policy rate will be necessary". SNB also maintains the willingness to intervene in the currency markets, with focus on "selling foreign currency".

In the new conditional forecast, 2023 inflation projection is lowered from 2.6% to 2.2%, down in from Q2 through Q4, with trough at 1.7% in Q3. However, 2024 and 2025 inflation projections are raised from 2.0% (both) to 2.2% and 2.1% respectively. Inflation is estimated to stay above 2% target from the tart of 2024 through Q1 2026, with a peak at 2.3% in Q3 2023.

Regarding the economy, SNB expects "modest growth" for the rest of the year. Overall GDP is to growth by 1.0% in 2023 and unemployment rise will "probably rise slightly". "Subdued demand from abroad, the loss of purchasing power due to inflation, and more restrictive financial conditions are having a dampening effect."

SNB Jordan: We cannot rule out further tightening

In the post-meeting press conference, SNB Chair Thomas Jordan affirmed that "We cannot rule out further monetary policy tightening".

"Without a more restrictive monetary policy, there would be a danger of inflation becoming entrenched and much stronger rate increases would be needed in the future," Jordan warned.

Jordan acknowledged the recent marked decline in inflation as a welcome result of SNB's more restrictive monetary policy in place for the past year. However, he cautioned that underlying inflationary pressure continued to intensify. "We are therefore observing persistent second-round effects in many domestic goods and services," Jordan said.

Despite today's rate increase, SNB's new forecasts for inflation from 2024 onwards are higher than their March predictions. Jordan attributed this upward revision to ongoing second-round effects, increased electricity prices and rents, and sustained inflationary pressure from overseas.

BoJ Noguchi: Important to maintain monetary easing

BoJ board member Asahi Noguchi underlined the necessity of maintaining monetary easing as Japan navigates signs of wage growth.

"What's most important now is for the BOJ to maintain monetary easing and ensure budding signs of wage growth become a sustained, strong trend," he said.

Noguchi predicts that core consumer inflation, which has been running above the bank's 2% target, will likely drop below this level around September or October. He attributed this anticipated decrease to the fading effects of past increases in raw material costs.

However, he noted that the possibility of inflation bouncing back above 2% later on and maintaining that level hinges largely on future wage trends and service prices.

New Zealand goods exports up 2.8% yoy in may, imports rose 4.4% yoy

New Zealand's monthly trade balance in May registered smaller surplus than anticipated, clocking in at NZD 46m against expected NZD 350m. This outcome followed rise in goods exports by NZD 189m (2.8% yoy) to NZD 7.0B, while goods imports saw an increase of NZD 292m (4.4% yoy), totalling NZD 6.9B.

China led the growth in monthly exports, with total exports increasing by NZD 308m (18% yoy). USA also reported a significant rise in exports, up by NZD 68m (9.7% yoy), while Japan experienced a modest increment of NZD 18m (4.2% yoy). On the other hand, total exports to Australia and the European Union fell by NZD -122m (-14% yoy) and NZD -60m (-11% yoy) respectively.

When it comes to imports, USA claimed the top spot with a massive jump of NZD 435m (87% yoy). South Korea followed with an increase of NZD 152m (41% yoy), while Australia and the European Union saw increases of NZD 81m (11% yoy) and NZD 31m (3.2% yoy) respectively. However, China's imports into New Zealand declined by NZD 52m (-3.6% yoy).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2754; (R1) 1.2815; More...

GBP/USD failed to break through 1.2847 resistance today, and stays in consolidations. Intraday bias remains neutral for the moment. On the upside, firm break of 1.2847 will resume larger up trend and target 100% projection of 1.1801 to 1.2678 from 1.2306 at 1.3183 next. However, firm break of 1.2628 will turn bias to the downside, for deeper fall to 1.2306 support instead.

In the bigger picture, the strong support from 55 W EMA (now at 1.2345) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 46M | 350M | 427M | 236M |

| 07:30 | CHF | SNB Rate Decision | 1.75% | 1.75% | 1.50% | |

| 08:00 | CHF | SNB Press Conference | ||||

| 11:00 | GBP | BoE Rate Decision | 5.00% | 4.75% | 4.50% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 7--0--2 | 7--0--2 | 7--0--2 | |

| 12:30 | USD | Initial Jobless Claims (Jun 16) | 264K | 256K | 262K | 264K |

| 12:30 | USD | Current Account (USD) Q1 | -219B | -217B | -207B | -216B |

| 14:00 | USD | Existing Home Sales May | 4.25M | 4.28M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -17 | -17.4 | ||

| 14:30 | USD | Natural Gas Storage | 89B | 84B | ||

| 15:00 | USD | Crude Oil Inventories | 0.3M | 7.9M |

US initial jobless claims unchanged at 264k

US initial jobless claims was unchanged at 264k in the week ending June 17, above expectation of 256k. Four-week moving average of initial claims rose 8.5k to 256k highest since November 13, 2021.

Continuing claims dropped -13k to 1759k in the week ending June 10. Four-week moving average of continuing claims dropped -7.5k to 1770.

BoE Slams on the Brakes Again, CBRT a Step in the Right Direction

The Bank of England accelerated its tightening efforts after meeting this week, hiking rates by 0.5% in response to another raft of worrying inflation data.

And it's not just yesterday's CPI data that will have caused considerable discomfort for the MPC, the April figures were also far too high and wage numbers we've had in the interim suggest its becoming increasingly embedded. That had to have caused serious alarm within the BoE, within seven members of the committee anyway.

Two policymakers voted to hold rates steady for the fourth meeting highlighting the widening gulf between the views on the MPC which may make finding a consensus going forward that much more challenging.

There's every chance that those backing 50 basis points did so in the hope that doing more now may necessitate the need to do less later on and for a shorter period of time. That's not how markets are initially perceiving it though, with the odds of Bank Rate rising above 6% increasing. It could get rather painful in inflation doesn't improve soon.

The pound appears to be weighing up both of these considerations, as is evident in the very volatile response we've seen in the currency. Rate hikes are generally good for a currency but when they're rising to levels that could seriously threaten the economy, there's certainly an argument for the opposite to happen.

Turkish interest rates finally heading in the right direction

Another interest rate decision was announced alongside the BoE, with the CBRT reverting back to hiking interest rates aggressively in order to put a lid on inflation and steady the currency which has fallen another 15% in recent weeks.

President Erdogan won the election promising to defend lower interest rates having led a campaign of aggressive rate cuts under Governor Şahap Kavcıoğlu, before immediately replacing him and the finance minister after the vote. A rate hike today was widely expected but the range of forecasts was vast and if anything, the 6.5% hike was at the lower end of the range.

Turkey faces many problems going forward as a result of the misguided policies over the last couple of years and that will likely warrant more aggressive tightening in the future. For now, investors may be mildly relieved that rates are heading in the right direction, if not fast enough. The risk is that Erdogan hasn't really hesitated to sack Governors that raise rates in the past so investors will never feel fully at ease as long as he's President.

SNB Opts for Smaller Hike But Signals It Isn’t Done Yet

The Swiss National Bank slowed the pace of its tightening cycle on Thursday, in line with market expectations but signaled there is more to come.

While most central banks would dream of 2.2% inflation right now, the SNB has made clear that there will be no complacency. Today’s hike likely doesn’t mark the end of its cycle, with another 25 basis points expected in September.

Having previously indicated that he believes the neutral rate is around 2%, Chair Thomas Jordan has effectively signaled to the markets that they won’t be done until at least this level is reached and today’s comments support that.

As did the forecasts, which assuming steady rates, had inflation remaining above 2% in two years’ time. In other words, more tightening will be necessary, alongside currency interventions, in order to get inflation back below 2%.

Despite some initial volatility, the Swiss franc is only a little lower on the day and not far from its pre-release levels. Against the dollar, it has been trending sideways for more than a month and today’s decision has so far failed to sway it one way or another.

A move below 0.8850 could make things interesting, as could a move above 0.91, but with the price sitting almost in the middle of these two levels currently, we may have to wait a little longer yet.

Markets are pricing in a strong chance of another hike in the cycle while indicating a small chance that the central bank is done. There is still a long way to go in the global inflation fight and, if the last couple of years are anything to go by, there may be some more twists and turns to come.

USD/CHF Technical

Gold Tests Nearby Support; Outlook Discouraging

Gold is repeating yesterday’s test of the descending line at 1,926, which helped the price stay afloat above the three-month low of 1,934.

Sentiment remains poor in the four-hour chart. The RSI is hovering around its 30 oversold mark, increasing speculation that the price could change direction to the upside soon, but the downturn in the stochastic oscillator and the falling MACD are reducing the odds for a proper rebound as the price deviates below its simple moving averages (SMAs).

If the precious metal closes below the trendline and stretches beneath the 1,918 low, the decline could initially stall around the 1,907 handle before picking up pace towards the 1,887-1,880 zone, where the price bottomed out on March 15. Interestingly, the extension of the March-April descending line happens to be in the neighborhood. Hence, a move lower could gain an extra leg to 1,860.

In the positive scenario, where the price secures a strong foothold around 1,927, the 20- and 50-period SMAs could come first into view at 1,938 and 1,947 respectively. Should upside forces stretch above the 1,955 border too, the recovery could continue towards the 200-period SMA at 1,970. Another bounce higher could meet the tough ceiling around 1,985.

Summing up, the yellow metal could stay under pressure in the coming sessions. Failure to bounce on the 1,927 base could lead to additional bearish episodes.

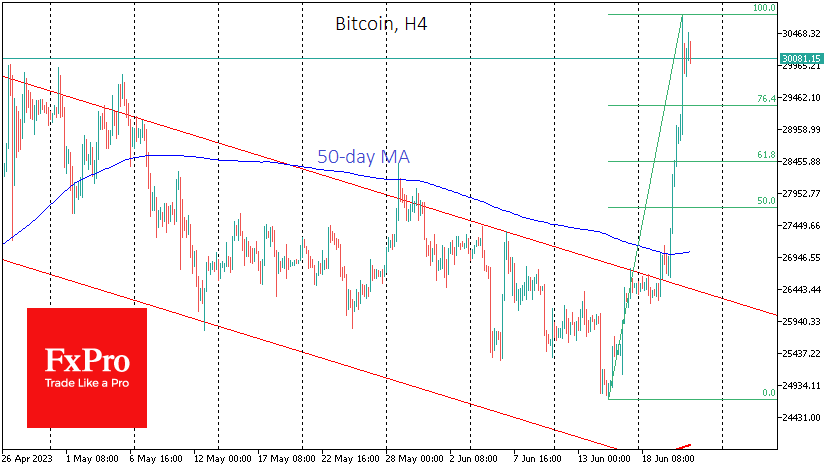

Crypto Needs a Breather

Market picture

The crypto market has gained another 3.9% in the past 24 hours, reaching a capitalisation of $1.18 trillion. It has diverged from the stock indices, which have fallen sharply in the previous days due to expectations of a rate hike.

Bitcoin has surged more than 15% in two days, revisiting the area of April highs just above 30K. However, this is where the recovery has paused. Bitcoin needs to consolidate a bit before it can resume its ascent. Moreover, there are doubts that the cryptocurrency rally will continue soon, as the stock indices create a challenging environment for risk-sensitive assets across the board.

The technical targets for the BTCUSD correction are the 29.3 and 28.5 levels, 76.4% and 61.8% of the latest rally, respectively. If the decline is halted at either of these levels, we could expect new multi-month highs soon.

News background

The official launch of the new crypto exchange EDX Markets boosted Bitcoin’s rise. The project is backed by financial giants Citadel Securities, Fidelity Investments and Charles Schwab. The market also reacted positively to BlackRock’s application to the SEC for a spot bitcoin ETF, filed last week.

Grayscale Investments’ GBTC bitcoin fund saw its trading volume increase five-fold to $80 million after BlackRock’s filing with the SEC. Following BlackRock, three other major investment firms – WisdomTree, Invesco and Bitwise – also applied for a spot bitcoin ETF.

Fed chief Jerome Powell said the regulator considers payment stablecoins as money and therefore has to regulate their issuance. He said it would be a “grave error” to allow large amounts of private funds to be created without oversight.

Stablecoins and DeFi projects could be the following targets of the SEC’s crackdown, according to investment bank Berenberg. After suing major exchanges, the SEC may now go after the issuers of the two largest stablecoins, Tether (USDT) and USD Coin (USDC).

BoE hikes 50bps by 7-2 vote, further tightening could be required

BoE raises Bank Rate by 50bps to 5.00%, larger than consensus of 25bps. The decision was made by 7-2 vote, with only known dove Swati Dhingra and Silvana Tenreyro voted for no change again.

Tightening bias is maintained as the central bank noted, "if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required."

BoE continues to expect CPI to "fall significantly further during the course of the year". Services CPI is projected to "remain broadly unchanged in the near term". Meanwhile, core goods CPI is expected to "decline later this year".

Second-round effects in domestic price and wage developments are "likely to take longer to unwind than they did to emerge". There has been "significant upside news in recent data that indicates more persistence in the inflation process."

(BOE) Bank Rate increased to 5%

Monetary Policy Summary, June 2023

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 21 June 2023, the MPC voted by a majority of 7–2 to increase Bank Rate by 0.5 percentage points, to 5%. Two members preferred to maintain Bank Rate at 4.5%.

At the time of the previous MPC meeting and May Monetary Policy Report, the market-implied path for Bank Rate averaged just over 4% over the next three years. Since then, gilt yields have risen materially, particularly at shorter maturities, now suggesting a path for Bank Rate that averages around 5½%. Mortgage rates have also risen notably. The sterling effective exchange rate has appreciated further.

The Committee is continuing to monitor closely the impact of the significant increases in Bank Rate so far. As set out in the May Report, the greater share of fixed-rate mortgages means that the full impact of the increase in Bank Rate to date will not be felt for some time.

Business surveys continue to suggest underlying quarterly GDP growth of around ¼% during the middle of this year. Indicators of household spending have tended to strengthen a little. LFS employment increased by 0.8% in the three months to April, higher than expected at the time of the May Report. The counterpart to this strong employment growth has been a further fall in the inactivity rate. The unemployment rate has been flat at 3.8%, in line with the May Report. The vacancies-to-unemployment ratio has fallen further but remains significantly elevated.

Annual growth in private sector regular Average Weekly Earnings (AWE) increased to 7.6% in the three months to April, 0.5 percentage points above the expectation at the time of the May Report. Three-month on three-month growth in this measure of pay has also picked up. Indications of future pay growth from the KPMG/REC survey and the Bank's Agents suggest that AWE growth will ease over the rest of this year, however.

Twelve-month CPI inflation fell from 10.1% in March to 8.7% in April and remained at that rate in May. This is 0.3 percentage points higher than expected in the May Report. Services CPI inflation rose to 7.4% in May, 0.5 percentage points stronger than expected at the time of the May Report, while core goods price inflation has also been much stronger than projected. In general, news in the latter component is less likely to imply persistent inflationary pressures.

CPI inflation is expected to fall significantly further during the course of the year, in the main reflecting developments in energy prices. Services CPI inflation is projected to remain broadly unchanged in the near term. Core goods CPI inflation is expected to decline later this year, supported by developments in cost and price indicators earlier in the supply chain. In particular, annual producer output price inflation has fallen very sharply in recent months. Food price inflation is projected to fall further in coming months.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

The MPC recognises that the second-round effects in domestic price and wage developments generated by external cost shocks are likely to take longer to unwind than they did to emerge. There has been significant upside news in recent data that indicates more persistence in the inflation process, against the background of a tight labour market and continued resilience in demand. At this meeting, the Committee voted to increase Bank Rate by 0.5 percentage points, to 5%.

The MPC will continue to monitor closely indications of persistent inflationary pressures in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.

The MPC will adjust Bank Rate as necessary to return inflation to the 2% target sustainably in the medium term, in line with its remit.

Minutes of the Monetary Policy Committee meeting ending on 21 June 2023

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP growth in 2023 Q2 was expected to be marginally stronger than anticipated at the time of the May Monetary Policy Report, following a slightly weaker-than-expected outturn for Q1. The most acute risks from recent global banking sector stresses appeared to have faded. Following the end of its zero-Covid policy in December 2022, growth momentum in China appeared to have slowed in Q2, in line with expectations at the time of the May Report. Recent weakness in Chinese tradable goods prices could start to put downward pressure on world export price inflation.

3: Labour markets had remained tight in both the euro area and the United States, with unemployment rates remaining close to their historically low levels alongside flat or rising labour participation rates, elevated but declining vacancies-to-unemployment ratios and strong wage pressure. This continued labour market tightness could have contributed to elevated services price inflation in both regions.

4: European wholesale spot and futures gas prices had been relatively volatile given changes in long-range weather forecasts and disruptions in supplies from Norway, but had ended the period since the MPC's previous meeting little changed. The Brent crude oil spot price had declined by around 3% since the MPC's previous meeting to around $75 per barrel. Agricultural commodity prices had been broadly unchanged.

5: Headline consumer price inflation had continued to decline in the euro area and the United States. Annual euro-area HICP inflation had decreased to 6.1% in May from 7.0% in April, accounted for mainly by continued falls in energy price inflation. The decline in annual core HICP inflation had been less pronounced as services price inflation had remained high while core goods price inflation had continued to decline gradually. In the United States, headline CPI inflation had fallen by 0.9 percentage points in May, to 4.0%, which was consistent with annual PCE inflation having declined to 3.8%. Within CPI inflation, while both core goods and services inflation had remained broadly at their April levels, core goods inflation was significantly below its 2022 peak.

Monetary and financial conditions

6: At its meeting ending on 14 June, the Federal Open Market Committee had left the federal funds rate unchanged and, at its meeting ending on 15 June, the ECB Governing Council had raised its key policy rates by 25 basis points, both in line with market expectations. In the United Kingdom, the market path implied that Bank Rate would be around 4.8% following this meeting, and would now average around 5½% over the next three years, compared to just over 4% in the conditioning assumption underpinning the May Monetary Policy Report.

7: There had been a material increase in both shorter and longer-term government bond yields globally, which had been particularly pronounced in the United Kingdom. Since the MPC's previous meeting, the one-year overnight index swap (OIS) rate, one year forward had increased by around 40, 80 and 140 basis points respectively in the euro area, United States and United Kingdom, and the 10-year government bond yield had increased by around 5, 25 and 55 basis points respectively in Germany, the United States and United Kingdom.

8: The Committee discussed the possible drivers of the increases in interest rates. There had been some positive news from data in the United States, and from the resolution of US debt ceiling negotiations, while downside risks related to the banking sector stress seen in March 2023 were perceived to have receded somewhat. These factors had had an impact globally.

9: The movements in UK rates had been much larger than in other major advanced economies, leaving the UK OIS curve both higher and flatter than its US and euro-area counterparts. In part, this had reflected some news about the continued resilience of UK demand. To a greater degree, it had appeared to reflect an increase in market participants' expectations of UK inflation persistence. The median respondent to the Bank's latest Market Participants Survey (MaPS), which had been conducted before the latest UK labour market and CPI releases, now expected CPI inflation one and three years ahead to be 3.1% and 2.2% respectively, compared with 2.7% and 2.0% in the previous survey in May.

10: There was some evidence that market pricing had been more sensitive to economic data outturns than had been usual over the past decade. Recent data releases had been accompanied by larger movements in the OIS curve than surprises of a similar magnitude had generated previously, notably in response to the material upside surprises in recent UK data releases on CPI inflation and the labour market. MaPS respondents had cited the evolution of wage growth, labour market tightness and services price inflation as the most important indicators when forming their expectations for the evolution of UK monetary policy, in line with the MPC's recent communications.

11: Medium-term inflation compensation measures in the United Kingdom, United States and euro area had increased a little further since the MPC's previous meeting. Although interpreting the movements in UK medium-term inflation compensation measures continued to be challenging, these measures were materially lower than their peak in March 2022, while remaining above their average levels of the previous decade. MaPS respondents' expectations of CPI inflation five years ahead had remained unchanged since the May survey, at 2.0%.

12: The sterling effective exchange rate had appreciated further, and had ended the period around 2% higher than at the time of the MPC's previous meeting and around 6% higher than at the beginning of 2023. UK-focused equity prices had fallen by around 3% since the MPC's previous meeting, in contrast to an increase in major equity indices in the United States and euro area.

13: UK owner-occupied fixed-term mortgage rates had picked up materially since the MPC's previous meeting, following a period of decline in recent months. This had largely reflected the pass-through of increases in risk-free reference rates. The market-share weighted average quoted rate on a two-year fixed-rate 75% loan-to-value mortgage had increased by around 90 basis points since the May MPC meeting, to 5.6%, and the five-year equivalent had increased by around 80 basis points, to 5.1%. There had been a net decline in the number of owner-occupied mortgage products available to borrowers since the MPC's previous meeting.

14: Net secured lending to households had decreased somewhat further in April, with, unusually, net outflows of £1.4 billion, compared to roughly zero in March. Mortgage approvals for house purchase had also fallen in April, to 48,700, but had remained above the average level of the previous six months.

15: Deposit rates had increased broadly in line with previous trends seen in this cycle. Time deposit rates had moved up materially since the MPC's previous meeting, in response to higher reference rates, while sight deposit rates had risen by much less. Reflecting these relative movements in remuneration, there had been a shift in deposit volumes from instant access accounts towards time deposits over the previous six months. Such substitution was internalised within the flow of overall sterling broad money, which had grown at an annual rate of 1.6% in April, up slightly from 1.4% in March.

Demand and output

16: According to the ONS's first quarterly estimate, real GDP had increased by 0.1% in 2023 Q1, marginally stronger than had been expected in the May Monetary Policy Report. Household consumption had also risen by 0.1%, while business investment had been estimated to have increased by 0.7%. Housing investment had fallen by 2.5% in Q1, leaving the level 5.5% lower than in 2022 Q3.

17: Monthly GDP had increased by 0.2% in April, following a 0.3% fall in March, and leaving it close to its pre-pandemic level. Market sector output had also risen by 0.2% in April and had been on a rising trend over recent months, in contrast to the flatter profile of overall GDP. That divergence was in part likely to reflect the impact of strike activity on the volume of public sector output.

18: Business surveys continued to suggest an underlying pace of quarterly GDP growth of around ¼% in 2023 Q2. After taking account of the impact of idiosyncratic factors, including the additional bank holiday in May, Bank staff expected headline GDP to be flat in the second quarter, in line with the projection in the May Report.

19: The outlook for 2023 Q3 was more uncertain, but Bank staff continued to judge that an underlying quarterly growth rate of around ¼% was a reasonable central projection. This would be consistent with stronger headline GDP growth than in Q2 as the impact of idiosyncratic factors unwound. The Bank's Agents had noted a slight pickup in the outlook for underlying activity in 2023 H2, while the S&P Global/CIPS UK composite PMI output expectations index also pointed to some further increase in underlying growth momentum.

20: Most indicators of household spending had tended to strengthen a little over recent months, albeit from very weak levels in some cases. Quarterly retail sales volumes had grown for the first time in 18 months, while consumer confidence had continued to pick up. Contacts of the Bank's Agents had reported that consumer demand had been more resilient than they had expected across both goods and services. The increase in mortgage rates so far during this cycle had, however, already led to higher aggregate interest payments by households, and this metric was likely to rise further.

Supply, costs and prices

21: Labour Force Survey (LFS) employment had increased by 0.8% in the three months to April, 0.2 percentage points higher than had been expected at the time of the May Monetary Policy Report. Rather than a decline in unemployment, the counterpart to this strong employment growth had been a further fall in the 16+ population's inactivity rate, particularly amongst students, which had reached its lowest level since spring 2020. HMRC PAYE employee payrolls and the S&P Global/CIPS UK PMI composite employment index had continued to point to employment growth being somewhat softer than LFS-based estimates.

22: Some measures of labour market tightness had continued to ease, but overall the labour market had remained tight by historical standards. The LFS unemployment rate had been broadly flat, at 3.8%, in the three months to April, consistent with the expectation at the time of the May Report. The vacancies-to-unemployment ratio had fallen further in the three months to April, to its lowest level since October 2021, but was still significantly elevated compared to pre-Covid levels. The number of job-to-job flows had declined again in 2023 Q1, to just above the level observed pre-Covid. Recruitment and employment consultancies responding to the KPMG/REC survey had indicated that overall staff availability had continued to improve in May. The Bank's Agents' contacts had reported that recruitment difficulties had continued to ease, but overall recruitment had still been more difficult than normal.

23: Annual private sector regular Average Weekly Earnings (AWE) growth had increased by 0.5 percentage points to 7.6% in the three months to April, 0.5 percentage points above the expectation at the time of the May Report. The pick-up in annual pay growth since the time of the May Report had been concentrated in higher-paying sectors such as financial and business services. Pay growth in lower-paid sectors like wholesaling, retailing, hotels and restaurants had been broadly flat. Three-month on three-month growth in private sector regular pay had been strong, rising to an annualised rate of around 8% in April, from 6.3% in March, contrasting notably with the falling growth rates between July 2022 and February 2023.

24: There had nevertheless been some countervailing signs of softening pay growth. The KPMG/REC survey measure of pay for new permanent hires, which had historically led AWE pay growth by around a year, had declined in May, having been broadly stable at a lower level since October 2022. This indicator pointed to a risk of private sector regular pay growth easing by more than had been expected in the May Report over the rest of this year. Some of the Bank's Agents' contacts had reported that pay settlements in the second half of this year could be somewhat lower than in the first half, largely due to lower near-term inflation expectations, with a looser labour market also expected to play a role.

25: At 8.7%, twelve-month CPI inflation in May had been unchanged from April. This release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes. The May figure was 0.3 percentage points higher than the expectation at the time of the May Report.

26: The upside CPI news since the May Report had been concentrated in core components, with core goods accounting for the majority of this news. Within core goods, for which the inflation rate had risen to 6.8% in May, the purchase of vehicles and recreational goods had accounted for the majority of this news. The surprise strength in vehicle prices had appeared to be related to a temporary supply shortage of 2-3 year old used cars, reflecting the lack of car production owing to the earlier semi-conductor shortage and coinciding with the age range of used cars for which the ONS collected prices. Non-energy goods import prices had risen further, suggesting that core goods manufacturers and retailers still faced high costs. Bank staff analysis suggested that world export prices could account for a significant share of elevated core goods CPI inflation.

27: Services CPI inflation had risen from 6.9% in April to 7.4% in May, 0.5 percentage points stronger than had been expected in the May Report, and partly reflecting a sharp rise in measured Vehicle Excise Duty rates. Airfares and package holidays had also accounted for some of the upside news. Airfares were a volatile component of the basket and the news in May had appeared to reflect the timing of Easter in April.

28: Food CPI inflation had edged down to 18.3% in May. The softening of annual food price inflation in the United Kingdom appeared to have followed developments in euro-area countries, albeit with somewhat of a lag, consistent with the global nature of recent shocks to food prices.

29: CPI inflation was expected to fall significantly further during the course of the year, in the main reflecting developments in energy prices. Energy prices were expected to drag on CPI inflation even further in October, due largely to the resetting of the Ofgem price cap faced by households at that time. There was still considerable uncertainty around the outlook for household energy prices, however, as only around a third of the relevant observation window for the October price cap had passed so far.

30: Core goods inflation was expected to remain elevated in the near term. Indicators of manufacturing cost pressures had nevertheless continued to ease. Producer price index (PPI) input and output price inflation had moderated to 0.5% and 2.9% respectively in May, broadly consistent with developments in the United States and euro area. Core goods CPI inflation had diverged from manufacturing PPI inflation recently, whereas historically these series had shown strong co-movement. The possibility of a reassertion of this historical association in the near term posed a downside risk to the outlook for core goods CPI inflation.

31: The continued pass-through of service providers' costs, including labour costs, was expected to keep services price inflation elevated in the near term. The Bank's Agents' consumer services contacts had reported that, while they had absorbed some, a fair proportion of cost increases had been passed on to consumer prices.

32: Food CPI inflation was expected to ease in the near term, reflecting the waning of pass-through from previous shocks and the recent fall-back in cost inflation further up the food supply chain.

33: Households and businesses' short-term inflation expectations had eased further but had remained somewhat above their historical averages. Households' median one-year inflation expectations, as measured by both the Bank/Ipsos and Citi/YouGov surveys, had fallen. The Decision Maker Panel survey suggested that businesses' expectations for their own prices a year ahead had also declined, to around 5% in May.

34: Households' median medium-term inflation expectations had been close to their historical averages in the latest releases of the major surveys. The Bank/Ipsos 5-year ahead measure had been below its pre-Covid average for a second successive quarter. The Citi/YouGov 5-10 year ahead measure had fallen to 3.5%, less than one standard deviation above its pre-Covid average.

The immediate policy decision

35: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

36: The Committee's latest projections for activity and inflation had been set out in the May Monetary Policy Report and had been conditioned on a market-implied path for Bank Rate that had averaged just over 4% over the next three years. In the modal case, CPI inflation had been expected to decline to a little above 1% at the two and three-year horizons, materially below the 2% target. This had reflected the projected emergence of an increasing degree of economic slack and declining external pressures that had been expected to reduce CPI inflation. However, the Committee had continued to judge that the risks around this inflation projection were skewed significantly to the upside, reflecting the potential for more persistent strength in domestic price and wage setting.

37: Since the previous MPC meeting, there had been material news in a number of UK economic data outturns, including those that the Committee had noted it would be monitoring closely as indicators of persistent inflationary pressures.

38: LFS employment had increased by 0.8% in the three months to April, higher than had been expected at the time of the May Report. The counterpart to this strong employment growth had been a further fall in the inactivity rate. The unemployment rate had been flat at 3.8%, in line with the May Report. The vacancies-to-unemployment ratio had fallen further but remained significantly elevated.

39: Annual growth in private sector regular Average Weekly Earnings (AWE) had increased to 7.6% in the three months to April, 0.5 percentage points above the expectation at the time of the May Report. Indications of future pay growth from the KPMG/REC survey and the Bank's Agents suggested that AWE growth would ease over the rest of this year, however.

40: Twelve-month CPI inflation had fallen from 10.1% in March to 8.7% in April and had remained at that rate in May. This was 0.3 percentage points higher than had been expected in the May Report. Services CPI inflation had risen to 7.4% in May, 0.5 percentage points stronger than had been expected at the time of the May Report.

41: CPI inflation was expected to fall significantly further during the course of the year, in the main reflecting developments in energy prices. Services CPI inflation was projected to remain broadly unchanged in the near term. Core goods CPI inflation was expected to decline later this year, supported by developments in cost and price indicators earlier in the supply chain. In particular, annual producer output price inflation had fallen very sharply in recent months. Food price inflation was projected to fall further in coming months.

42: The Committee was continuing to monitor closely the impact of the significant increases in Bank Rate so far. As set out in the May Report, the greater share of fixed-rate mortgages meant that the full impact of the increase in Bank Rate to date would not be felt for some time. The Committee also recognised that it had become more important to consider developments in the rental market.

43: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation departed from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term.

44: Monetary policy was also acting to ensure that longer-term inflation expectations were anchored at the 2% target. Households and businesses' short-term inflation expectations had eased further but had remained somewhat above their historical averages. Households' median medium-term inflation expectations had been close to their historical averages in the latest releases of the major surveys. UK medium-term inflation compensation measures in financial markets had increased a little further since the MPC's previous meeting and were above their average levels of the previous decade.

45: Seven members judged that a 0.5 percentage point increase in Bank Rate, to 5%, was warranted at this meeting. The second-round effects in domestic price and wage developments generated by external cost shocks were likely to take longer to unwind than they had done to emerge. There had been significant upside news in recent data that indicated more persistence in the inflation process, against the background of a tight labour market and continued resilience in demand. Some indicators of future pay growth and goods inflation had weakened, but their properties as leading indicators had not been tested in a similar period of high inflation. The scale of the recent upside surprises in official estimates of wage growth and services CPI inflation suggested a 0.5 percentage point increase in interest rates was required at this particular meeting.

46: Two members preferred to leave Bank Rate unchanged at 4.5% at this meeting. There were two main factors underlying their votes. First, as the energy price shock and other global cost-push shocks continued to reverse over the course of 2023, goods price inflation should fall sharply, which, with some lag, would reduce associated persistence in domestic wage and price setting. In contrast with the strength in recent outturns, forward-looking indicators were pointing to material falls in future wage and price inflation. Second, the lags in the effects of monetary policy meant that sizable impacts from past rate increases were still to come through. This included additional rate increases carried out in recent months, which would more than offset any additional persistence implied by the latest data. The current setting of Bank Rate would therefore be likely to reduce inflation below target in the medium term. Recent substantial increases in market yields would accentuate this, as they would mainly affect inflation in late 2024 and beyond, by which point energy price falls from their peaks and past rate rises would have lowered inflation significantly.

47: The MPC would continue to monitor closely indications of persistent inflationary pressures in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.

48: The MPC would adjust Bank Rate as necessary to return inflation to the 2% target sustainably in the medium term, in line with its remit.

49: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be increased by 0.5 percentage points, to 5%.

50: Seven members (Andrew Bailey, Ben Broadbent, Jon Cunliffe, Jonathan Haskel, Catherine L Mann, Huw Pill and Dave Ramsden) voted in favour of the proposition. Two members (Swati Dhingra and Silvana Tenreyro) voted against the proposition, preferring to maintain Bank Rate at 4.5%.

Operational considerations

51: On 21 June 2023, the total stock of assets held for monetary policy purposes was £806 billion, comprising £805 billion of UK government bond purchases and £0.8 billion of sterling non‐financial investment‐grade corporate bond purchases.

52: The following members of the Committee were present:

- Andrew Bailey, Chair

- Ben Broadbent

- Jon Cunliffe

- Swati Dhingra

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Silvana Tenreyro

Sam Beckett was present as the Treasury representative.

53: On behalf of the Committee, the Chair expressed his appreciation to Silvana Tenreyro for her contributions to the work of the MPC since becoming a member in 2017.

SNB Jordan: We cannot rule out further tightening

In the post-meeting press conference, SNB Chair Thomas Jordan affirmed that "We cannot rule out further monetary policy tightening," following a decision to increase interest rates by 25bos to 1.75% today.

"Without a more restrictive monetary policy, there would be a danger of inflation becoming entrenched and much stronger rate increases would be needed in the future," Jordan warned.

Jordan acknowledged the recent marked decline in inflation as a welcome result of SNB's more restrictive monetary policy in place for the past year. However, he cautioned that underlying inflationary pressure continued to intensify. "We are therefore observing persistent second-round effects in many domestic goods and services," Jordan said.

Despite today's rate increase, SNB's new forecasts for inflation from 2024 onwards are higher than their March predictions. Jordan attributed this upward revision to ongoing second-round effects, increased electricity prices and rents, and sustained inflationary pressure from overseas.

SNB's updated inflation projections show 2.2% in 2023 and 2024, and 2.1% in 2025, compared to previous forecasts of 2.6% for this year and 2% for the next two years.