Sample Category Title

As Yen Collapses, How Likely is FX Intervention?

With the yen breaking down lately, Japanese authorities have stepped up their warnings about FX intervention. However, the conditions for intervention are not fully present yet, as the moves in USDJPY in particular have not been sharp enough. For the yen to stage a lasting recovery, it might require some policy tightening from the BoJ or an episode of panic in global markets instead.

Yen meltdown

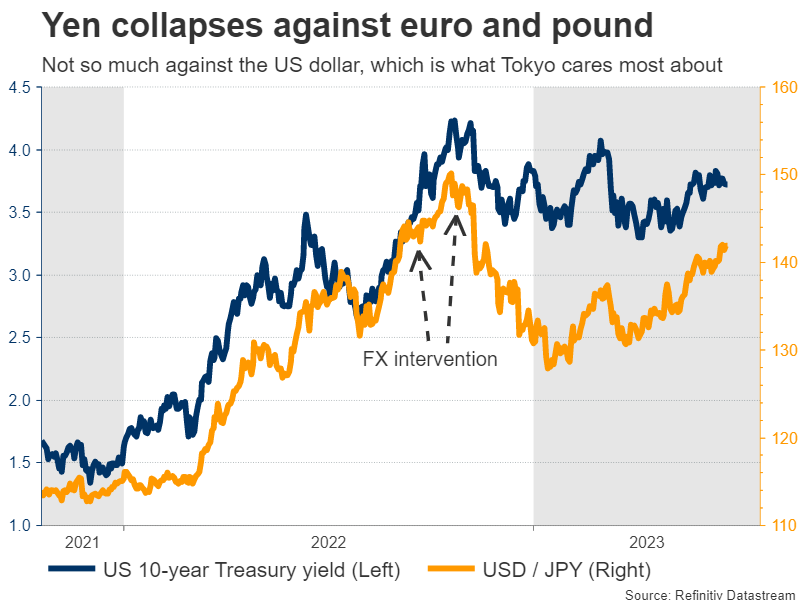

It’s been a dreadful year for the Japanese yen, which has been ravaged by the Bank of Japan’s refusal to tighten monetary policy. With most other major central banks raising interest rates in a hurry, the rate gap has widened, making the yen less attractive to hold compared to other currencies.

Naturally, the yen’s losses have been more devastating against currencies that are backed up by central banks who are expected to continue raising rates. So far this year, the yen has lost almost 14% of its value against the British pound and more than 10% against the euro, plunging to multi-year lows against both.

With the currency in freefall, Japanese officials have returned to their old playbook of threatening to intervene in the FX market. They did it twice last year to stop the yen’s downfall, so their warnings are more credible this time, since investors know they are not afraid to pull the trigger.

Intervention or mere rhetoric?

For now, the risk of FX intervention seems fairly low. Tokyo cares most about how the yen moves against the US dollar, and since that pair has not gone out of control, there isn’t much urgency to step in.

Supporting this notion is the language that Japanese authorities have used until now. The finance minister has refrained from using phrases that would suggest intervention is imminent, such as describing the FX moves as “disorderly” or “excessive”. Instead, he has been more measured with his comments.

The strategy might be to simply threaten intervention in order to discourage speculators from jumping on the bandwagon and amplifying the downside momentum in the yen. In essence, it’s a psychological tactic against speculation.

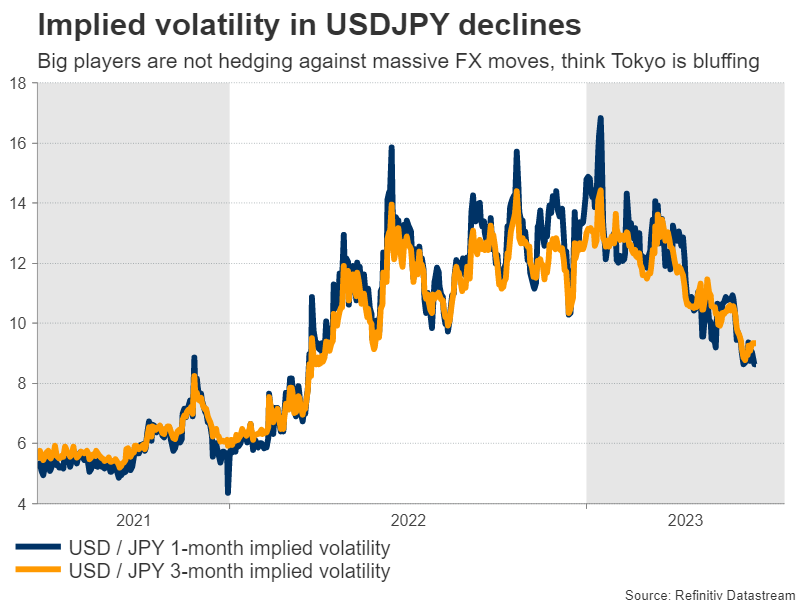

Reflecting the low risk of intervention is the implied volatility in USDJPY, which has fallen dramatically in recent weeks. This suggests that bank dealers and large asset managers are not really hedging against any massive moves in USDJPY, viewing this risk as relatively low.

Some strategists suggest that if USDJPY climbs to 145.00, it would be the ‘line in the sand’ that triggers intervention. But speed matters in this calculation - such a move could prompt intervention if it happens in a week, not over several months. Hence, it’s difficult to say exactly where the intervention ‘line’ is, mainly because it’s a moving target.

Ingredients for recovery

With the likelihood of intervention appearing low for the time being, any sustainable recovery in the yen would need to rely on other factors, such as a policy shift from the Bank of Japan.

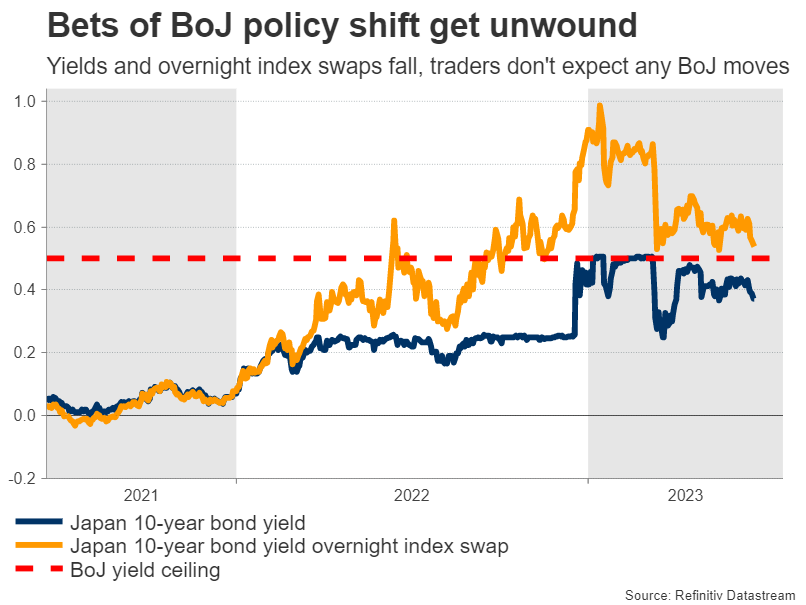

So far, the BoJ has been reluctant to raise the ceiling it has imposed on Japanese yields, even though core inflation is at its hottest level in three decades. Most officials believe this spell won’t last, as the central bank’s forecasts expect inflation to cool later this year.

Haunted by decades of deflation, the BoJ wants to make sure it won’t tighten until inflation is sustainably above its 2% target. That means their forecasts for the next 2-3 years need to show inflation remaining above 2% before they feel comfortable raising the yield ceiling that has ruined the yen.

The plot twist is that this shift could happen as early as next month. If the BoJ upgrades its inflation forecasts for 2025 at the July meeting, which seems likely considering the resilience of the economy, then inflation would be projected to remain above 2% through the entire forecast horizon. This would be a signal that tighter policy is coming, helping to stop the yen’s bleeding.

It’s important to note, however, that market participants are skeptical such a move will occur. Bets that the BoJ will adjust its policy settings have been lowered lately, something visible both in 10-year Japanese yields and in overnight index swaps tracking this instrument. Therefore, any move by the BoJ this year could come as a surprise for investors.

Another variable that will be crucial in enabling a sustainable recovery in the yen will be global risk sentiment. After all, the yen is a defensive currency that tends to shine during periods of panic in global markets. As such, if the euphoria in riskier assets calms down and there’s a correction later this year, that could also help revive the yen through safe-haven flows.

All told, currency intervention seems unlikely at this stage. Instead, the yen’s best chance for a lasting recovery is through the BoJ joining the global tightening race. Traders are saying such a shift is unlikely, yet the economic conditions seem to be falling into place. So while the yen’s crash is not over, it might be entering its final phase.

Bank of England Review – Stay Negative on GBP Ddespite 50bp Surprise

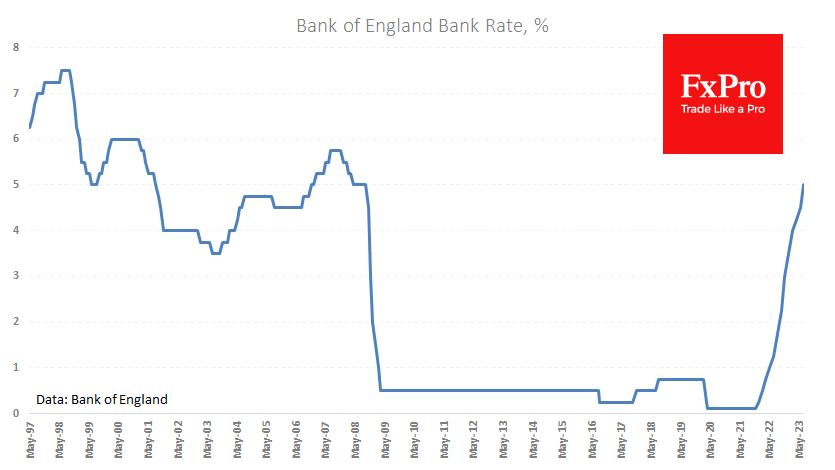

- The Bank of England (BoE) surprised markets and analysts by hiking policy rates by 50bp, bringing the Bank Rate to 5.00%.

- We view the 50bp hike as front-loaded in nature with wage growth and inflation having surprised to the topside. We pencil in 25bp rate hikes in August and September. This would mark a peak in the Bank Rate of 5.50%

- We increasingly see relative rates as a positive for EUR/GBP from here, which is one of several reasons behind our fundamental predisposition of buying EUR/GBP dips.

The Bank of England (BoE) hiked the Bank Rate (key policy rate) by 50bp to 5.00% with 7 members voting for a 50bp hike and two members voting for unchanged.

The majority of the Monetary Policy Committee (MPC) voted for an increase of 50bp as recent data releases have indicated more inflation persistence amid still elevated inflation expectations. Consequently, the MPC judges risks to inflation to be "skewed significantly to the upside". The BoE repeated that "if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required" but refrained from including "forceful tightening" which previously has been used as a phrase in BoE's forward guidance.

We largely see the 50bp hike today as frontloading of further tightening and note the phrase: "0.5 percentage point increase in interest rates was required at this particular meeting." We think that the BoE will return to a smaller 25bp hike at the August meeting if data does not surprise significantly to the upside. However, we stress that risks are skewed to the topside.

With both the global backdrop, inflation and wage growth having surprised to the topside, we do not believe that data will have weakened enough for the BoE to pause its hiking cycle at the September meeting. We thus revise our forecast to include a 25bp hike in September, marking a peak in the Bank Rate at 5.50%. Before the next meeting on 3 August, we get both another job market report (11 July) and inflation data (19 July) for June. As the key concern for the BoE remains developments in wage data as well as service inflation this is the key data releases to follow.

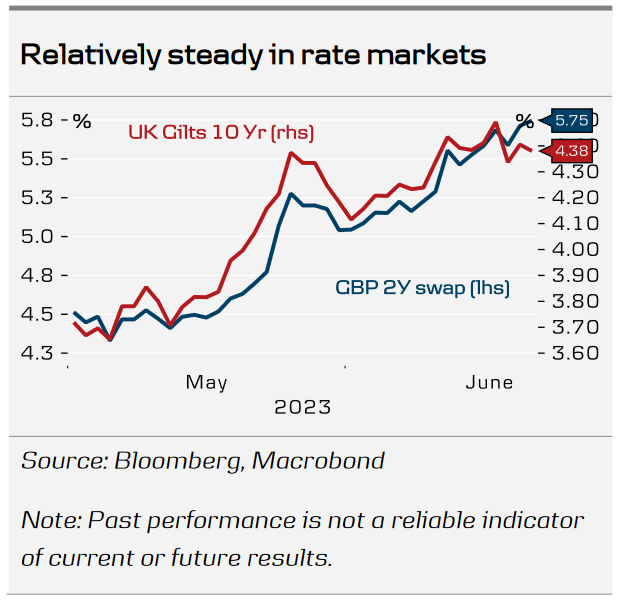

Rates. Despite the 50bp surprise, 2Y gilts yields have remain relatively steady as pricing in White and Red FRAs have adjusted to the front-loaded hike today. 10Y gilts yields on the other hand have dropped c. 10bp. Markets are pricing in 42bp for the August meeting.

FX. EUR/GBP initially moved lower but fully retraced the move within the hour. On balance, we continue to see relative rates as a positive for EUR/GBP from here, which is one of several reasons behind our fundamental predisposition of buying EUR/GBP dips. We highlight that whether the aggressive BoE market pricing will subside or inflation continues to surprise, we see it as headwinds for GBP. We still like our short GBP/CHF trade recommendation.

Our call. We continue to expect a 25bp at the August meeting although it is a close call between 25bp and 50bp. In order for BoE to opt for 50bp instead of 25bp we believe that we would have to see data releases prove considerably stronger than what we currently pencil in. Our call is considerably less than current market pricing 100bp until February 2024). We still believe that the first rate cuts will not be delivered before Q2 2024.

Bank of England Revs Up Rate Hikes

- In the wake of disappointing inflation news in recent months, the Bank of England (BoE) today decided to deliver a large 50 bps policy rate hike to 5.00%.

- In raising interest rates, the BoE said “the second-round effects in domestic price and wage developments generated by external cost shocks are likely to take longer to unwind than they did to emerge” and that if “there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required.”

- We doubt wage or price inflation will cool substantially by the time of the Bank of England's August announcement. With the BoE's economic projections in August likely to show much higher inflation forecasts, we expect the U.K. central bank to deliver another 50 bps rate increase, to 5.50%. Beyond that, we also see a 25 bps hike to 5.75% in September, which we expect to be the peak for the current cycle.

- The Norges Bank also raised its policy rate 50 bps to 3.75% and the Swiss National Bank raised its policy rate 25 bps to 1.75%. We expect both central banks to raise rates further through September, while we also think the risk of more extended ECB monetary tightening is rising.

U.K. Delivers A Large June Rate Increase

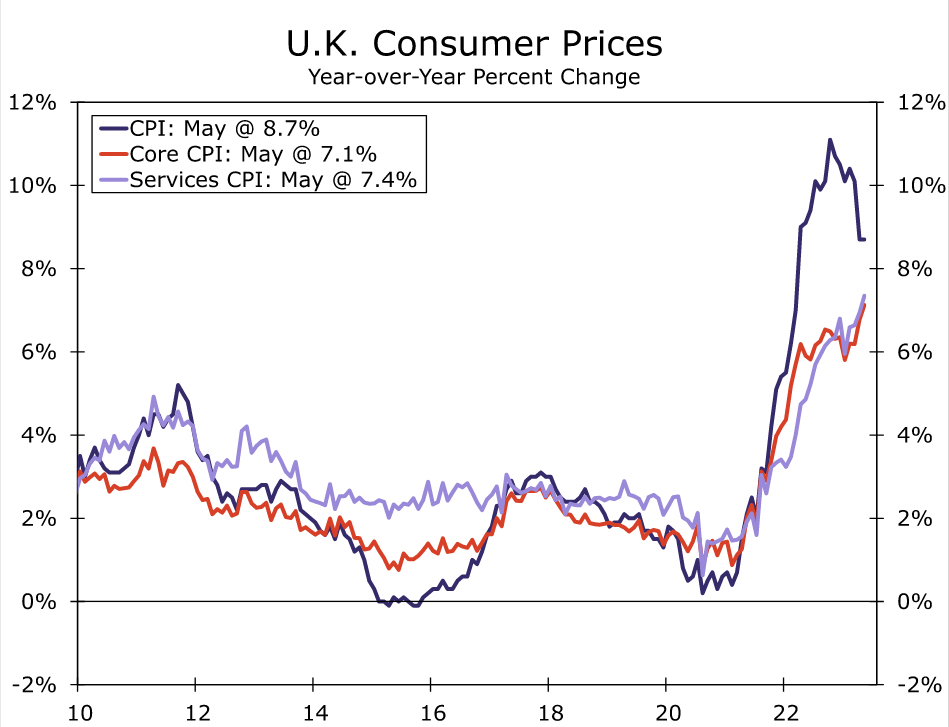

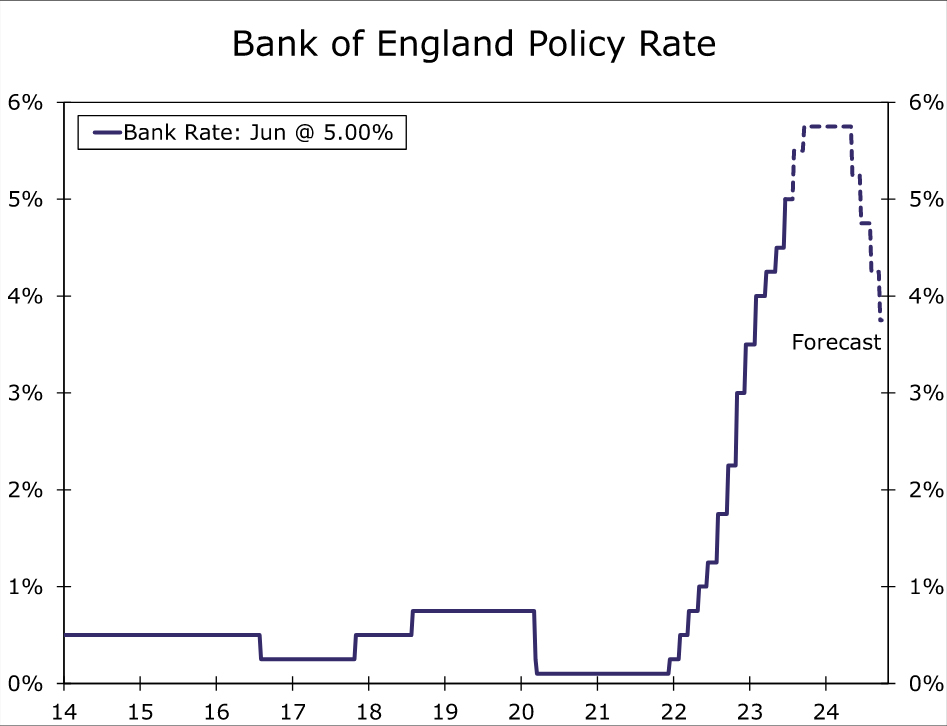

In the wake of disappointing inflation news in recent months, the Bank of England (BoE) today decided to deliver a large 50 bps policy rate hike to 5.00%. The rate hike was large relative to the past couple of meetings, which had seen 25 bps increases delivered, and also relative to the consensus forecast which had called for a 25 bps hike. The BoE's hand was essentially forced by especially rapid inflation in recent months, which saw the May headline CPI hold steady at 8.7% year-over-year, and core CPI inflation accelerate further to 7.1%.

In raising interest rates today by a 7-2 vote (with the two dissenters voting for no rate change), BoE policymakers said "the second-round effects in domestic price and wage developments generated by external cost shocks are likely to take longer to unwind than they did to emerge. There has been significant upside news in recent data that indicates more persistence in the inflation process, against the background of a tight labor market and continued resilience in demand."

In addition, policymakers said they would "continue to monitor closely indications of persistent inflationary pressures in the economy as a whole, including the tightness of labor market conditions and the behavior of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required."

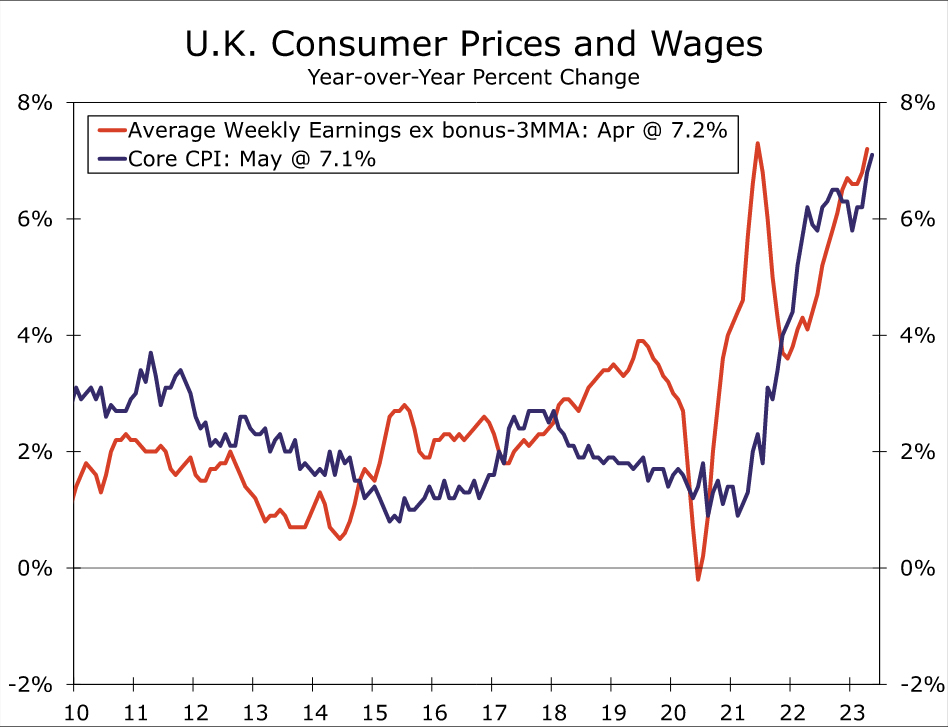

For now, wages continue to grow at a particularly rapid pace, with average weekly earnings ex bonuses for the three months to April rising 7.2% year-over-year. That is a pace of wage growth that does not augur well for a significant near-term slowing in underlying inflation trends. Employment also remains solid for now, and the unemployment rate remains quite low. Against this backdrop, we suspect the BoE will receive further indications of persistent inflation pressures that will require further monetary tightening. Between now and the BoE's August meeting we will receive one more CPI report and one more labor market report, which we doubt will show a sharp cooling in wage or price pressures. With the BoE's economic projections in August likely to show much higher inflation forecasts, we expect the U.K. central bank to deliver another 50 bps rate increase, to 5.50%. Beyond that, we also see a 25 bps hike to 5.75% in September, which we expect to be the peak for the current cycle.

With the Bank of England set to raise rates substantially further, we expect the U.K. economy to come under renewed pressure by late 2023, and look for growth to either stagnate or even for the economy to contract. Indeed, given still high inflation and rising interest rates, we now expect a mild recession, forecasting U.K. GDP to contract in Q4-2023 and Q1-2024. In terms of our full year GDP growth outlook, we forecast modest U.K. GDP growth of 0.2% for 2023 and 0.4% for 2024. But only once there are clearer signs of a growth slowdown and a deceleration of inflation, do we believe those factors will convince the Bank of England to bring its tightening cycle to an end. While we do not expect Bank of England rate cuts until Q2-2024, against a backdrop of mild recession and a more quickly declining inflation, we forecast a cumulative 250 bps of rate cuts next year, an aggressive pace of monetary easing that would broadly match that of the Federal Reserve. For the U.K., a low growth/high inflation mix, combined with an outlook for aggressive Bank of England easing next year, are reasons we remain cautious on the pound's prospects versus the greenback over the medium-term.

Europe's Other Central Banks Also Active

The Bank of England was not the only central bank in the spotlight today. The Norges Bank raised its policy rate a larger-than-forecast 50 bps to 3.75%, saying inflation and wage growth remain high, and that a higher policy rate than previously signaled is need to bring inflation down to target. The central bank also said another rate increase is likely in August, and signaled a peak policy rate of 4.25%. In keeping with that guidance, for the Norges Bank we now expect 25 bps rate increases in August and September, for a peak policy rate of 4.25%.

The Swiss National Bank (SNB) also raised its policy rate by 25 bps, as expected, to 1.75%. Even as the SNB lowered its near-term inflation forecasts, it projected medium-term inflation at or slightly above its 2% inflation target over the medium term. Specifically, the SNB forecast CPI inflation of 2.2% for 2024 and 2.1% for 2025. Against this backdrop the SNB said it "cannot be ruled out that additional rises in the SNB policy rate will be necessary to ensure price stability over the medium term." We expect the Swiss National Bank will raise its policy rate another 25 bps to 2.00% in September.

Finally, although the European Central Bank (ECB) was not active this week, we do believe the risk of more extended monetary tightening is rising. Currently, we forecast a final 25 bps rate hike to 3.75% in July—a move that has already been clearly signaled by ECB President Lagarde. However, it may be that additional favorable CPI readings (such as the downside surprise for the May CPI) will be required to dissuade the ECB from further tightening. In contrast, if underlying pressures were to remain persistent in coming months, and we do not see a perceptible shift to a less hawkish ECB outlook at the July announcement, we would be inclined to adjust our ECB monetary policy outlook to also include a 25 bps rate increase in September, to 4.00%.

Bank of England’s Expected Surprise

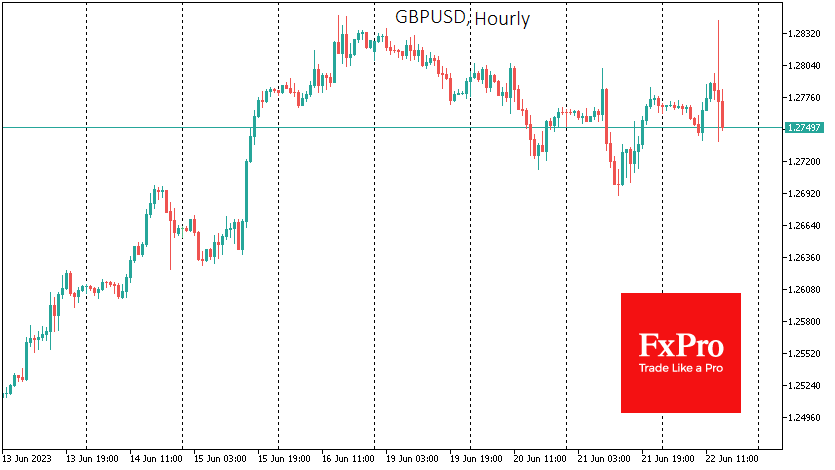

The Bank of England raised its key rate by 50bp to 5.00% – a sharper move than analysts who had made their forecasts earlier in the week had expected. However, it’s a logical move, given that the latest inflation data from the previous day exceeded both market expectations and the Bank’s forecasts. Given the persistently high inflation in the UK, we should have expected a tougher stance from the central bank.

In a companion commentary, the Bank of England acknowledged the secondary inflationary effects, from external shocks to rising service prices, solid consumer demand and a tight labour market. The forced cooling of the economy is a classic monetary policy response to the last two problems: developed country central banks are tightening policy to fight inflation until they get enough evidence of cooling final demand.

The market reaction to the rate surprise deserves a separate mention. GBPUSD jumped 60 pips up to 1.2840 and fell 100 pips down to 1.2740 within 10 minutes of the decision being published. This was obviously due to the trading robots working off the news headlines but ran into resistance from the sellers near the highs at last week’s close. However, the pound soon stabilised near the day’s opening levels, as markets saw the latest decision consistent with the available economic data.

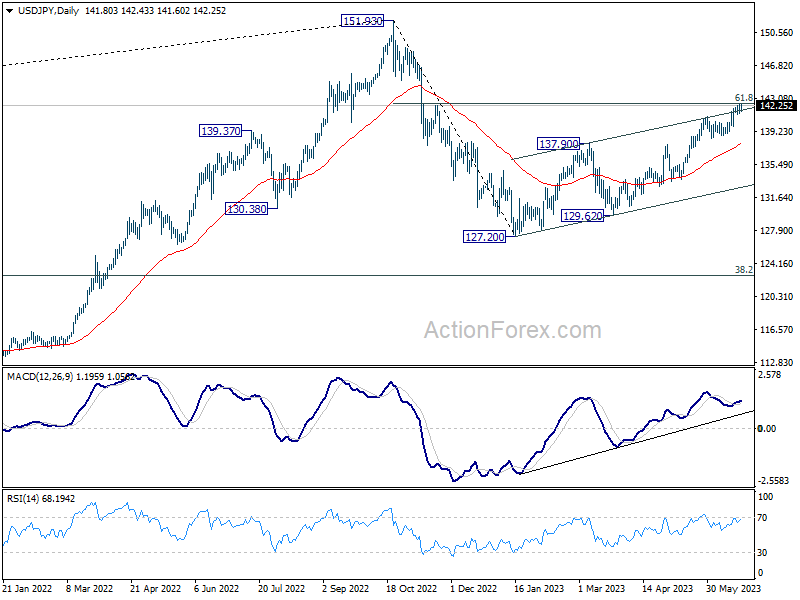

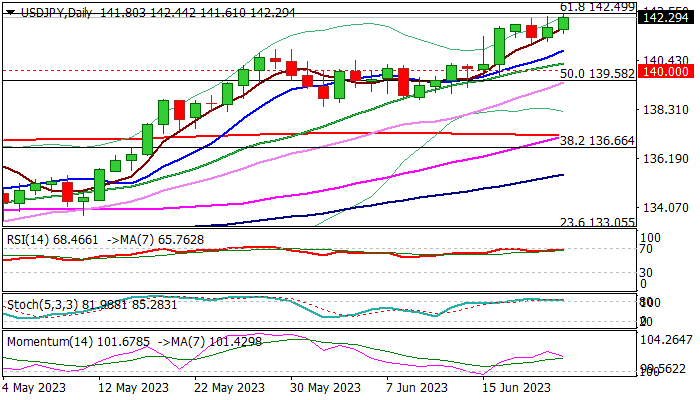

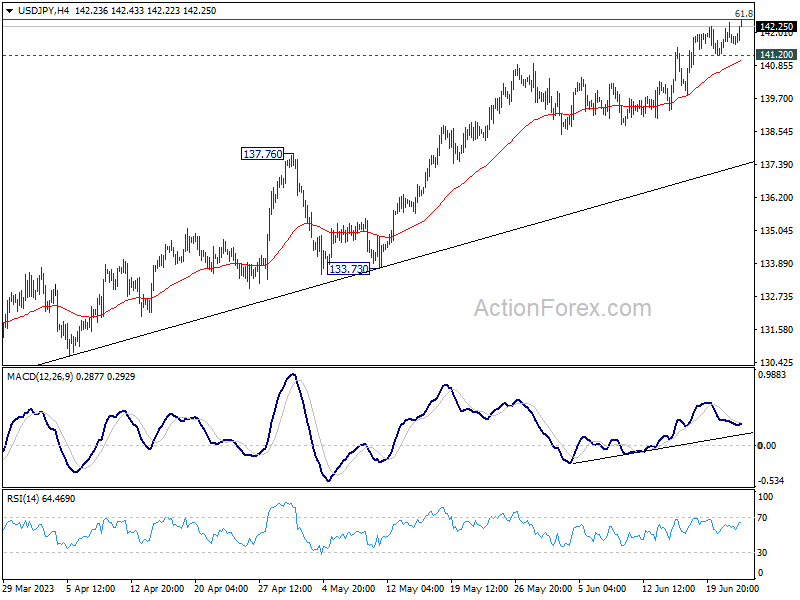

USD/JPY Needs Break of Key Fibo Barrier

USD/JPY remains supported by favorable fundamentals but needs break of key Fibo barrier to resume larger rally

The USDJPY edged higher on Thursday, pressuring pivotal Fibo resistance at 142.50 (61.8% of 151.94/127.22), underpinned by predominantly hawkish Fed’s narrative and US weekly jobless claims within expected limits.

Larger bulls continue to face headwinds from key Fibo level, along with overbought conditions and fading bullish momentum on daily chart, which may keep the pair in extend consolidation below this level.

However, near-term action is expected to remain biased higher while holding above supports at 141 zone (former top of May 30 / rising 10DMA).

Eventual break of Fibo barrier at 142.50 would generate bullish signal for fresh acceleration higher and expose targets at 145.10 (Oct 27 low) and 146.10 (Fibo 76.4%).

Res: 142.50; 143.00; 144.56; 145.10.

Sup: 141.61; 140.93; 140.30; 140.00.

Sunset Market Commentary

Markets

Today’s central bank decisions confirmed that the ‘high(er) for longer’ paradigm is stronger than it has ever been in this cycle. Banks that held some kind of benign neglect approach (Norges Bank, Bank of England) were forced to surrender, forced by unacceptably stubborn (core) inflation. Even the Turkish central bank made a U-turn in its unconventional approach, admittedly less pronounced than markets hoped for. The ones that were already convinced on the need for a longer period of restrictive policy (Swiss National bank) for now see no need to change tactics, even as their approach is gradually yielding results. In fact that was also the conclusion from the Czech national bank yesterday, as it kept ‘leaning against rate cuts’. An illustrative summary.

The Bank of England in a 7-2 vote reaccelerated the pace of rate hikes to 0.5 ppt bringing the policy rate to 5.0%. The market was still leaning toward a 25 bps hike. The BoE still expects inflation to decline significantly during the course of the year, but had to recognize that second round effects in domestic prices and wages are likely to take longer to unwind as ‘upside news in recent data indicates more persistence in the inflation process, against the background of a tight labour market and continued resilience in demand.’ Despite those big upside surprises it didn’t change its ‘guidance’ in a profound way. The statement still reads ‘The MPC will continue to monitor closely indications of persistent inflationary pressures … including the tightness of labour market conditions and the behaviour of wage growth and services price inflation. If there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required’. So no ‘unconditional commitment’ on further policy tightening. The BoE decision was a mixed bag for markets. The 2-y yield gains 3.5 bps, but long term yields are easing (about -3.0 bps for 5-30-y spectrum). Of course, today’s reaction is ‘conditioned’ by recent sharp rise, especially in short-term yields. Sterling whipsawed upon the BoE announcement, but finally returned to near unchanged levels in the 0.86 area.

The Norges Bank unexpectedly reaccelerated the tightening pace from 25 to 50 bps to 3.75% and raised the expected terminal rate from the 3.5% projected in March to 4.25%. Inflation came in much quicker than expected in May, remaining way above target while wages are set to grow faster this year than in 2022. Meanwhile the economy is holding up well, not least because of a tight labour market. All this led the Norges Bank to again revise inflation estimates across the policy horizon. Even at the very end, in 2026, inflation is seen above target still. Today’s bigger-than-expected hike also came as the Norwegian krone traded weaker than thought, fueling (imported) inflation. If inflation keeps surprising to the upside or the NOK to the downside (or both), the Norges Bank does not rule out an even higher peak policy rate. The krone in any case isn’t that impressed. EUR/NOK eases from 11.71 to 11.60. As a rough measure, EUR/NOK should stabilize around 11.50 to meet the Norges Bank 2023 target.

The Swiss National Bank (SNB) as expected raised its policy rate by 25 bps to 1.75%. Swiss May headline inflation eased to 2.2%. Core inflation even dropped to 1.9%. The decline was mainly due to lower prices of imported goods (especially oil and gas) and the strong franc. However, despite a higher policy rate path than envisaged in March, SNB raised its 2024 and 2025 inflation forecast to respectively 2.2% and 2.1% (from 2.0%) on second round effects, higher electricity prices and rents and inflationary pressures from abroad. With inflation holding above target over the policy horizon, SNB’s Jordan indicated that further tightening is mostly likely necessary. SNB also is prepared to support appropriate monetary conditions by taking action in the FX market as necessary (selling FX vs CHF). Still the franc today lost modestly against the euro (EUR/CHF 0.9830). However, this level probably is no concern for the SNB.

What a difference a governor makes. The new president of the Turkish central bank, Hafize Gaye Erkan, not only drastically shortened the monetary policy statement, she also made a U-turn in its content. The CBRT said it began the tightening process in order to establish the disinflation course. It raised the policy rate from 8.5% to 15% for starters, with as much tightening as needed to come until the inflation outlook improves significantly. The statement no longer mentions the liraization strategy, a set of unconventional policy measures (fiscal and monetary) through which Turkey tried to support its sliding currency. It’s another sign of authorities seeking a clean break with the previous administration. But markets want money on the table. The Turkish currency slid after the decision with the rate hike coming in below a 20% consensus. USD/TRY and EUR/TRY both hit a new all-time high near 24.50 and 26.90 respectively.

BoE Bailey: Raising interest rate is the best way to get inflation down

In a video release after today's 50bps rate hike, BoE Governor Andrew Bailey said, "inflation is still too high", and "recent data has shown us that further decisive action is needed".

"If we don't raise rates now, high inflation could stay with us for longer and inflation hits all of us, particularly those who can least afford it," he warned."

"Raising interest rates is the best way we have of getting inflation back down to the 2% target."

https://twitter.com/bankofengland/status/1671862096831627264

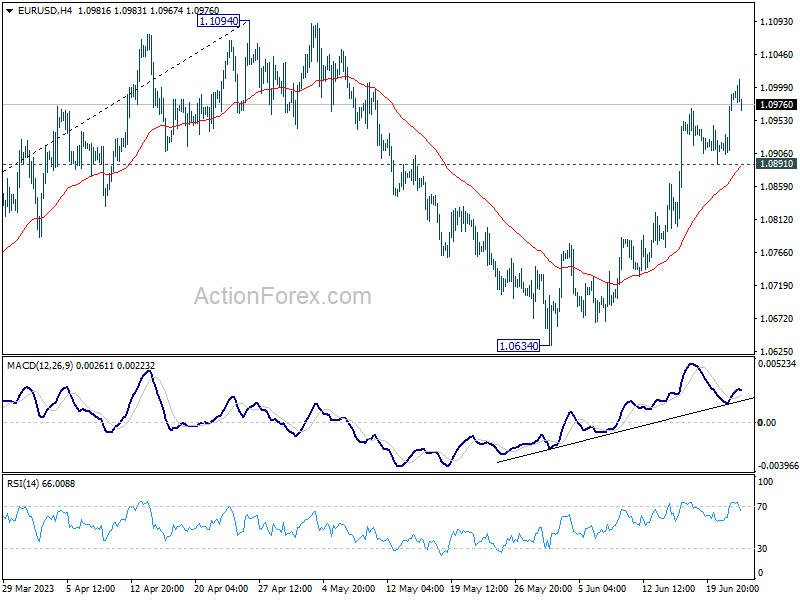

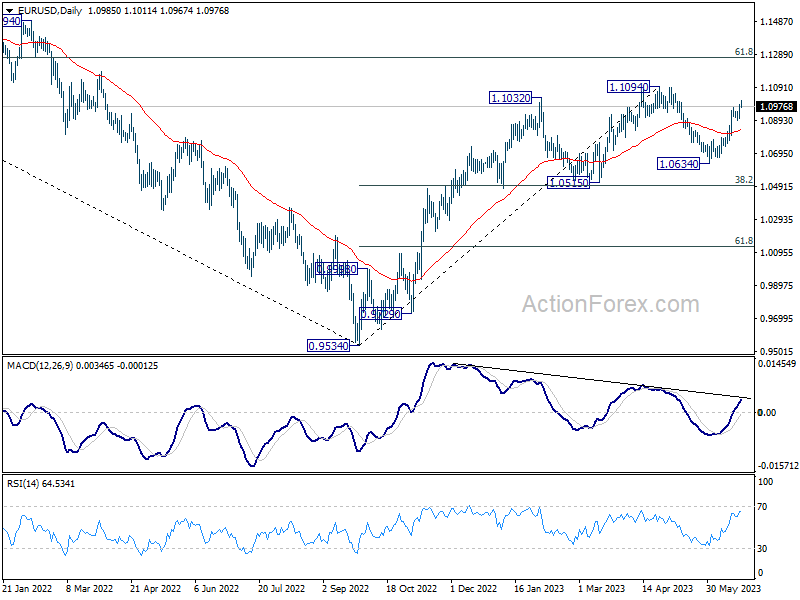

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0932; (P) 1.0961; (R1) 1.1017; More...

Intraday bias in EUR/USD remains on the upside at this point. Current rise from 1.0634 should target a test on 1.1094 high. Decisive break there will confirm resumption of whole up trend from 0.9534. However, firm break of 1.0891 will extend the corrective pattern from 1.1094 with another falling leg, targeting 1.0634 and below.

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

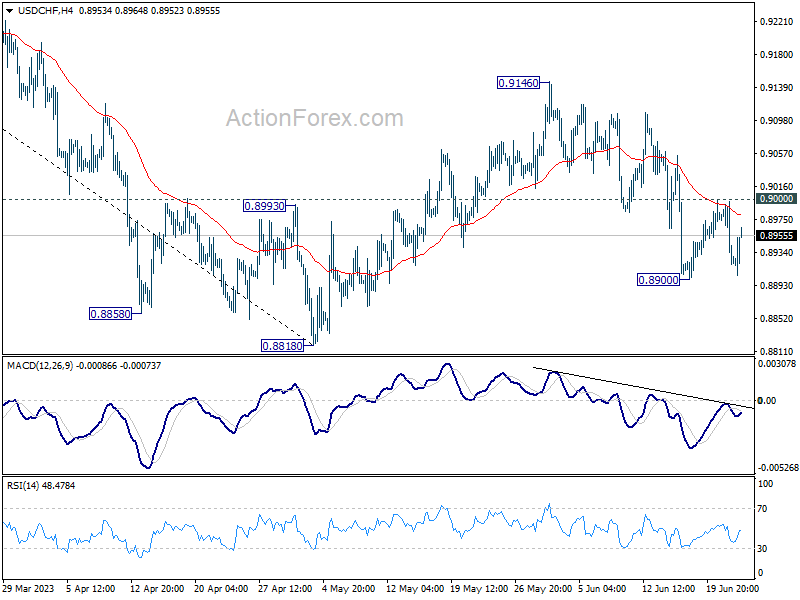

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8901; (P) 0.8950; (R1) 0.8979; More...

USD/CHF recovered ahead of 0.8900 temporary low and intraday bias remains neutral for the moment. Further decline is expected as long as 0.9000 resistance holds. Break of 0.8900 will target 0.8818 and possibly below. But strong support is still expected from 0.8756 to bring reversal. Meanwhile, above 0.9000 will turn bias back to the upside for 0.9146 resistance instead.

In the bigger picture, fall from 1.1046 (2022 high) is seen as a leg in the long term range pattern from 1.0342 (2016 high), which might have completed at 0.8818 already, just ahead of 0.8756 long term support. Sustained trading above 0.9058 support turned resistance should confirm medium term bottoming.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.34; (P) 141.85; (R1) 142.41; More...

No change in USD/JPY's outlook as further rally is expected with 141.20 minor support intact. Sustained trading above 61.8% retracement of 151.93 to 127.20 at 142.48 would extend the rise from 127.20 towards 151.93 high. However, break of 141.20 minor support will be the first sign of rejection by 142.48, and turn bias back to the downside for 55 D EMA (now at 137.77).

In the bigger picture, rise from 151.93 are seen as a corrective pattern to up trend from 102.58. The first leg has completed at 127.20. Rebound from there is seen as the second leg, and should be limited below 151.93. Sustained trading below 55 D EMA (now at 137.47) will argue that the third leg has started back to 127.20 and possibly below.