Sample Category Title

(SNB) Swiss National Bank leaves SNB policy rate unchanged at 0%

The Swiss National Bank is leaving the SNB policy rate unchanged at 0%. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold. The discount for sight deposits above this threshold still stands at 0.25 percentage points. Given the conflict in the Middle East, the SNB's willingness to intervene in the foreign exchange market has increased. The SNB thereby counters a rapid and excessive appreciation of the Swiss franc, which would jeopardise price stability in Switzerland.

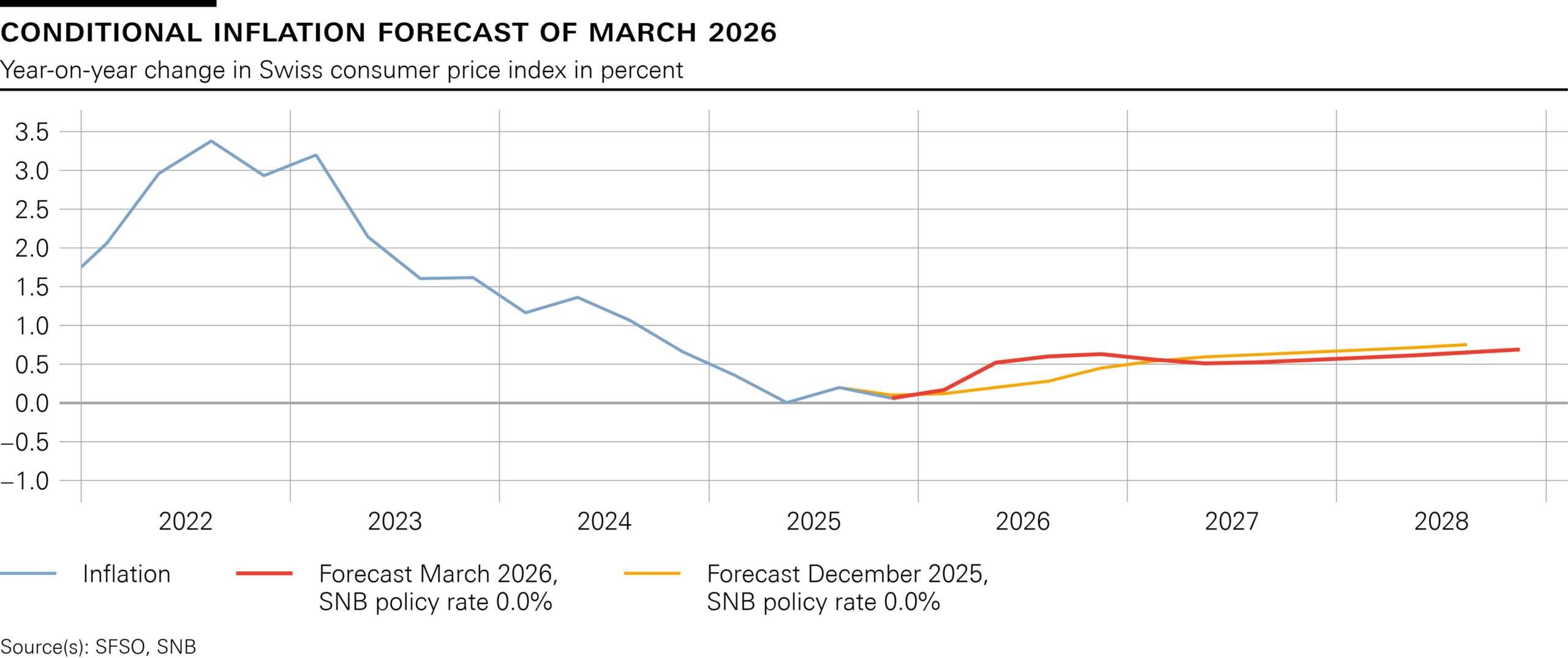

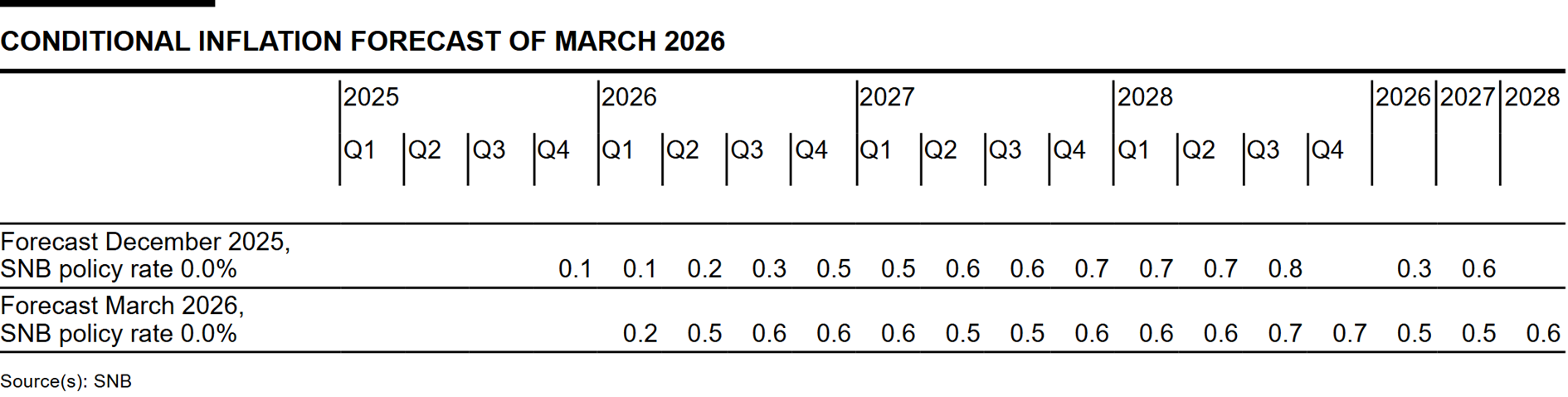

The conditional inflation forecast for the coming quarters is higher than in December due to the rise in energy prices. Medium-term inflationary pressure, however, has remained virtually unchanged since the last monetary policy assessment. The monetary policy helps to keep inflation within the range consistent with price stability and supports economic development. The SNB will continue to monitor the situation closely and adjust its monetary policy if necessary, in order to ensure price stability over the medium term.

As expected, inflation has risen slightly since the last monetary policy assessment, from 0.0% in November to 0.1% in February. This increase was driven in particular by higher goods inflation.

With the rise in energy prices due to the escalation in the Middle East, inflation is likely to increase more strongly in the coming quarters. As a result, the conditional inflation forecast in the short term is higher than in December. In the medium term, it is slightly lower due to the stronger Swiss franc. The forecast is within the range of price stability over the entire forecast horizon (cf. chart). It puts average annual inflation at 0.5% for 2026, 0.5% for 2027 and 0.6% for 2028 (cf. table). The forecast is based on the assumption that the SNB policy rate is 0% over the entire forecast horizon.

Global economic growth was solid in the fourth quarter. While inflation remained elevated in the US, in the euro area it stayed close to the central bank's target. Key rates were left unchanged in both currency areas.

With the conflict in the Middle East, the economic outlook has become considerably more uncertain. In its baseline scenario, the SNB anticipates that the increase in energy prices will raise inflation in many countries in the short term. Furthermore, global economic growth is likely to temporarily slow somewhat.

The global economic outlook is subject to significant risks, in particular owing to the situation in the Middle East. For instance, energy prices could rise more strongly than expected in the baseline scenario, which would considerably increase inflation and substantially constrain economic growth. Potential supply chain disruptions and heightened uncertainty could also weigh on growth. In addition to the situation in the Middle East, the trade policy outlook also remains uncertain.

Swiss GDP grew again in the fourth quarter, having contracted in the previous quarter. Unemployment in February was at the same level as at the time of the last monetary policy assessment.

The economic outlook for Switzerland for the coming months is uncertain. In the shorter term, growth could be rather subdued, with a certain upturn to be expected in the medium term. The SNB currently expects growth of around 1% for 2026 as a whole, followed by around 1.5% in 2027.

The main risk to the economic outlook for Switzerland is the development in the global economy. In particular, the situation in the Middle East could curb global economic activity.

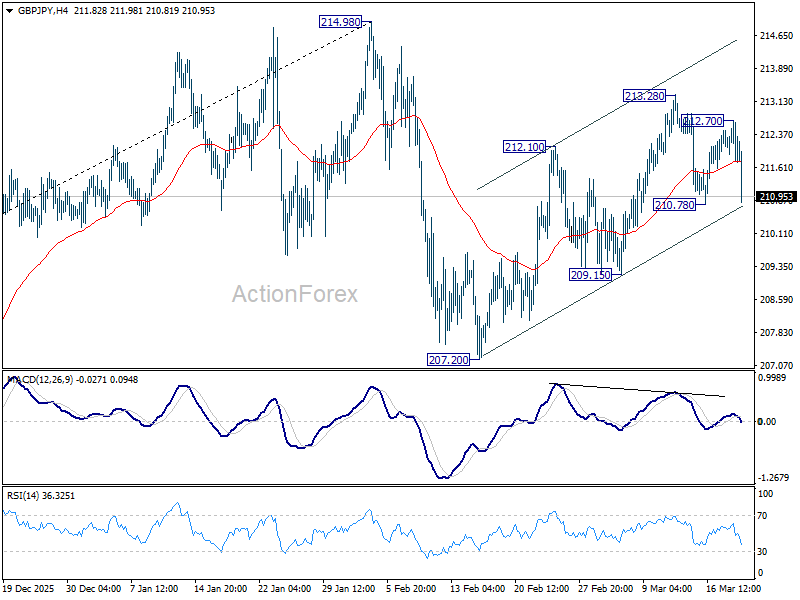

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.66; (P) 212.19; (R1) 212.49; More...

GBP/JPY's outlook is unchanged that rebound from 207.20 could have completed with three waves up to 213.28. Below 210.78 will target 209.15 support first. Firm break there will solidify this case and target 207.20 next. On the upside, however, above 213.28 will target a retest on 214.98 high instead.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.08) holds, even in case of another deep pullback.

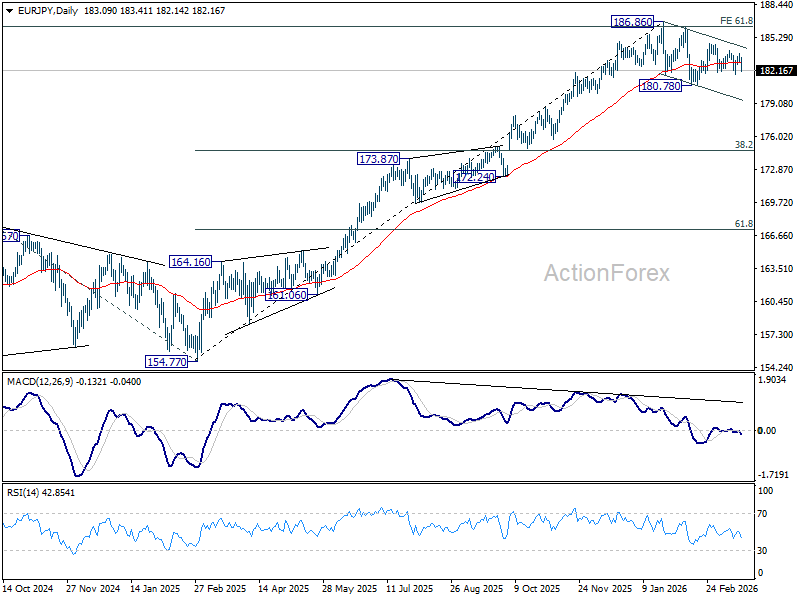

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.78; (P) 183.30; (R1) 183.65; More...

EUR/JPY weakens sharply today but stays in established range. Intraday bias remains neutral at this point. On the downside, below 181.85 will target 180.78 support. Decisive break there will indicate that fall from 186.86 is already correcting whole up rise from 154.77, and solidify the near term bearish outlook. On the upside, above 183.38 will resume the rebound from 180.78 through 185.74 resistance.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 175.29) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

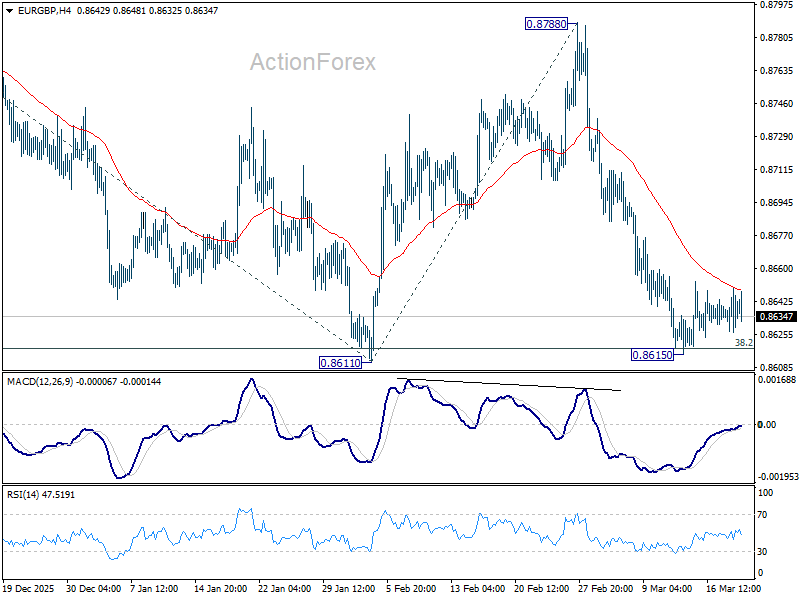

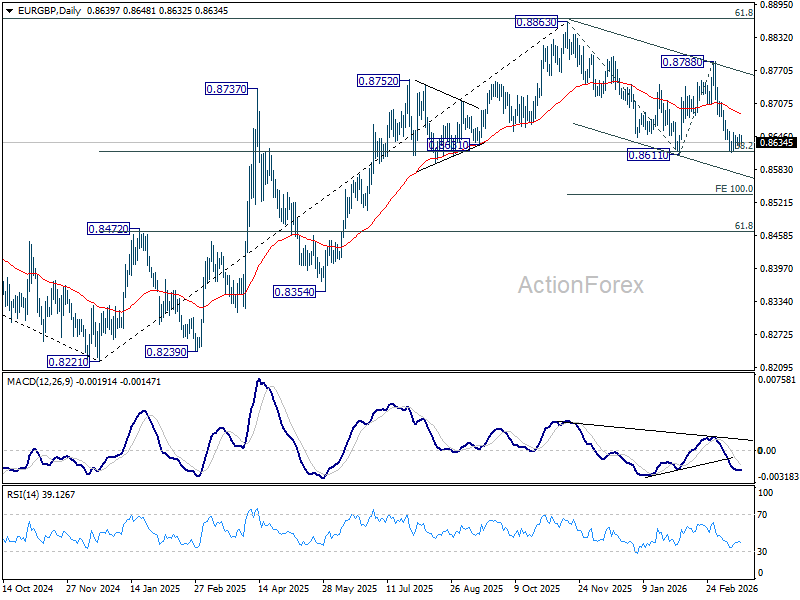

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8627; (P) 0.8640; (R1) 0.8652; More…

EUR/GBP is still bounded in sideway trading and intraday bias stays neutral. Further decline is expected as long as 55 D EMA (now at 0.8686) holds. Firm break of 0.8611 will resume the whole fall from 0.8863 to 100% projection of 0.8863 to 0.8611 from 0.8788 at 0.8536.

In the bigger picture, current development revived the case that whole rise from 0.8221 (2024 low) has completed at 0.8863, after rejection by 61.8% retracement of 0.9267 (2022 high) to 0.8221 at 0.8867. Sustained trading below 38.2% retracement of 0.8821 to 0.8863 at 0.8618 will confirm this case, and bring deeper fall to 61.8% retracement at 0.8466 at least. For now, medium term outlook is neutral at best as long as 0.8863 resistance holds.

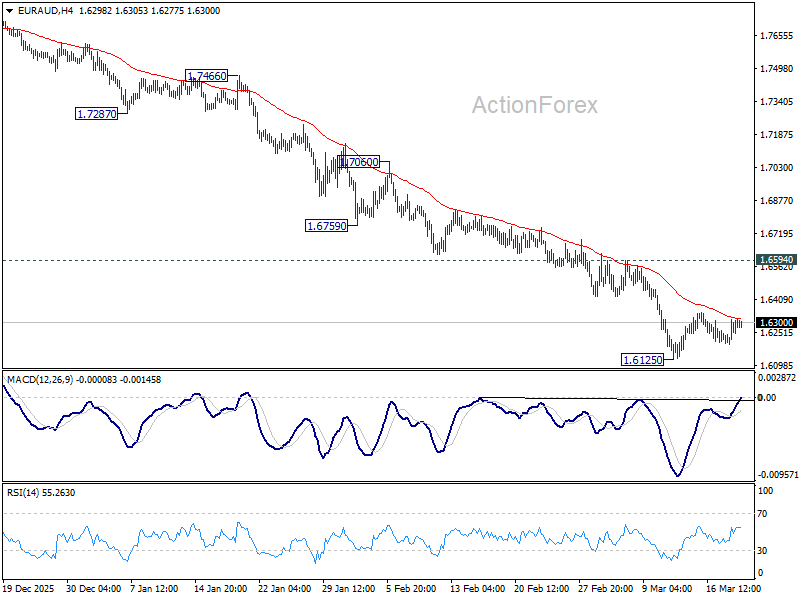

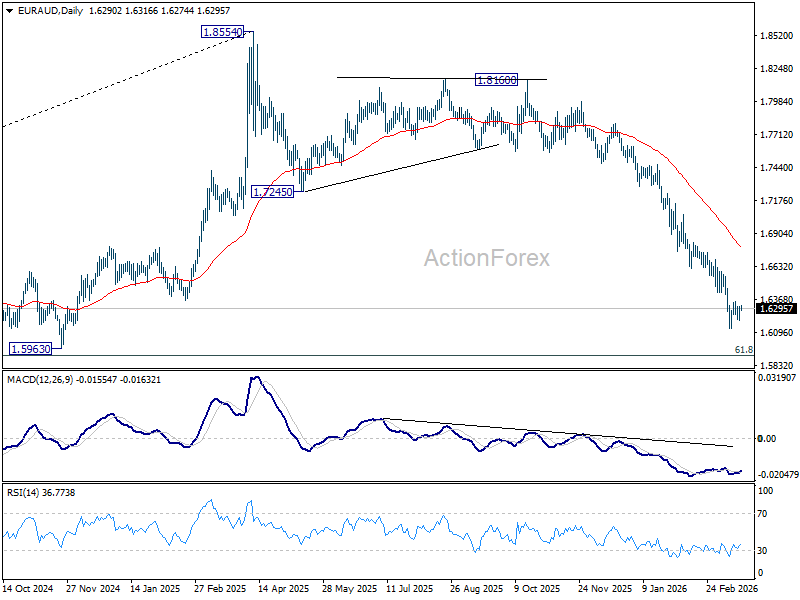

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6230; (P) 1.6275; (R1) 1.6351; More...

EUR/AUD is still bounded in established range above 1.6125 and intraday bias stays neutral. Further decline is expected with 1.6594 resistance intact. Firm break of 1.6125 will resume the fall from 1.8554 to 1.5913 fibonacci level next. Nevertheless, break of 1.6594 will indicate short term bottoming, and bring stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7238) holds, even in case of strong rebound.

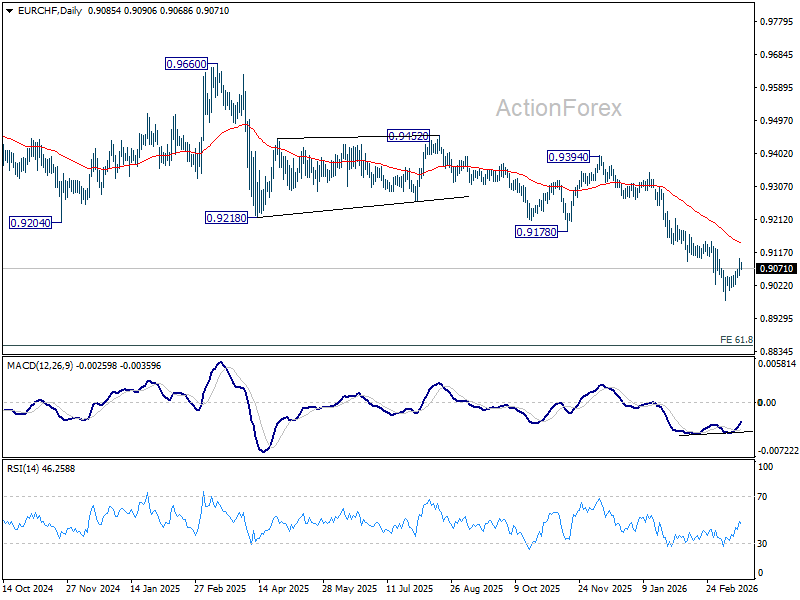

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9055; (P) 0.9080; (R1) 0.9108; More....

EUR/CHF breached 0.9092 support turned resistance but failed to sustain above it. Intraday bias stays neutral first and further decline is still mildly in favor. On the downside, firm break of 0.8979 will resume larger down trend. However, sustained break of 0.9092 will bring stronger rebound to 0.9149 resistance instead.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

Powell Kept an Agnostic View on the (Persistence, Duration of) Current Developments.

Markets

Yesterday saw a new escalation in attacks on oil infrastructure in the Middle East with a sharp rise in energy prices that dominated global markets. Iran attacked Qatar’s Ras Laffan gas infrastructure after Israël attacked Iran’s main South Pars gas field. Natural gas and oil prices (Brent $110+ levels) already jumped sharply higher before the Fed policy decision. The Fed as expected left its policy rate unchanged at 3.5-3.75%. Fed chair Powell at the press conference gave little guidance on the impact of the Middle East conflict on activity and inflation. Forward guidance is dead, at least for now. The Fed still published a new dot plot summarizing assessments from the individual Fed governors. The median dots were raised both for economic growth (2026 2.4% from 2.3%; 2027 2.3% from 2%, 2028 2.1% from 1.9%) and PCE inflation (2026 2.7% from 2.4%, 20272.2% from 2.1%; 2028 2% unchanged), but Powell stressed that these view have far less relevance than is otherwise in current environment. The median path for the Fed rate path still sees 1 additional 25 bps rate cut this and next year. Powell kept an agnostic view on the (persistence, duration of) current developments. An oil price shock might be a one-off, but the Fed will closely monitor the impact on inflation expectations. With respect to (current) inflation developments, Powell extensively elaborated on the pass-through of higher tariffs on goods inflation. Powell also indicated he intends to stay at the central bank until the DOJ investigation is completed. He wants to continue to serve as Fed chair temporarily if his successor is not confirmed by the end of this term. He hasn’t decided anything on whether he will continue to term as governor. Markets didn’t join the neutral, ‘agnostic’ attitude from the chair and mainly reacted to sharply higher energy prices causing further bear flattening (US 2-y +9.9 bps , 30-y + 4 bps). Despite Powell’s balanced assessment markets reduced the chance of a 2026 rate cut to <50%. US equities tumbled (S&P -1.36%). The dollar regained the upper hand (EUR/USD close 1.1452; USD/JPY 159.86). German yields, (closed before a late session upleg in the oil price) added between +6.1 bp (2-y) and +0.2 bps.

The energy-stagflation trade (Brent oil $113 p/b, European gas price opens 27% higher) still dominates global trading this morning with a further rise in (ST) yields, a new sharp downleg in Asian equities (Nikkei -3.38%) and a stronger dollar (DXY 100.21, EUR/USD 1.1455). We’re now going into the policy decisions of the ECB, the Bank of England the Riksbank, the Swiss National bank and the Czech national bank. Markets will especially look out for the ECB reaction function to current energy price shock. They currently fully discount a June rate hike and more than a second additional 25 bps step EoY. The 2-y swap yield jumps another 8.5 bps this morning (2.72%). Lagarde already indicated that the ECB considered some scenario analyses aside from the regular forecast update. Markets at least price that the new energy shock will warrant decisive action in the near future and are keen to see any concrete commitment from the ECB to prevent a 2022/23 pass through to second round effects. Whatever the ECB assessment, the market reaction function to higher oil prices/stagflation risk is clear.

News & Views

The Bank of Japan kept its policy rate unchanged at 0.75%. Board member Takata dissented like he did in January, in favour of a 25 bps rate hike, in a 8-1 majority vote. Hawkish tweaks to the policy statement included the need to monitor how higher oil prices could affect underlying inflation. The bank probably means upside inflation risks as the statement makes no explicit mention of downside growth risks stemming from elevated energy prices. The BoJ also expects medium and long term inflation expectations to rise, with the effects of a positive wage-price spiral adding to this view. It reiterates that if the outlook for economic activity and prices presented in the January Outlook is realized, the bank will continue raising the policy rate. We believe these conditions will be met in April, when the BoJ meets next. BoJ governor Ueda at the press conference did nothing to push back against market expectations.

February Australian employment data showed a consensus-beating 48.9 net job gain (vs 20k). Details were less encouraging with full time occupations falling by 30.5 k and the increase being due to higher levels of part-time employment (+79.4k). The unemployment rate unexpectedly moved from 4.1% to 4.3% but was backed by a higher participation rate (66.9% from 66.7%). Stats New Zealand reported 0.2% Q/Q growth in the December 2025 quarter (down from 0.9% Q/Q and below 0.4% consensus). Details showed especially government consumption contributing positively (+2.5%) with gross fixed capital formation declining (2.2%) and household consumption stabilizing at best.

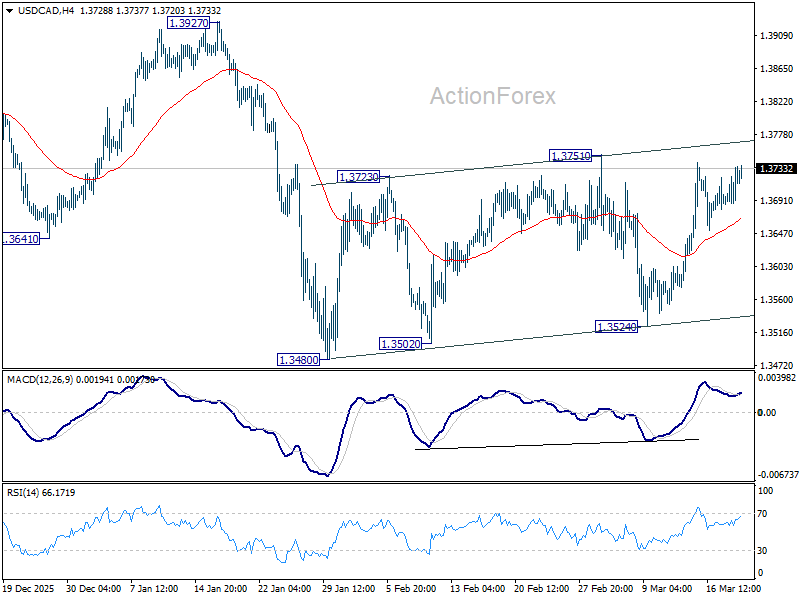

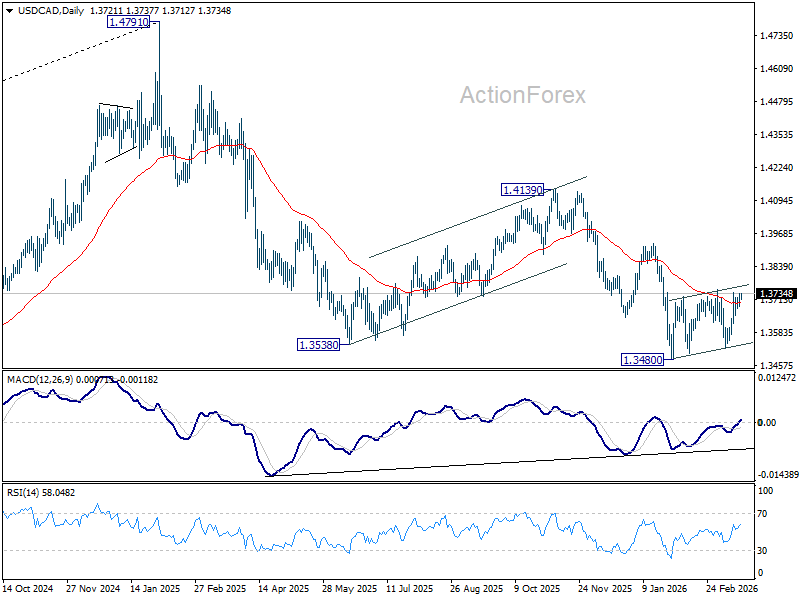

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3699; (P) 1.3719; (R1) 1.3752; More...

No change in USD/CAD's outlook and intraday bias remains neutral. On the upside, firm break of 1.3751 resistance will suggest that stronger rebound is underway, and target 1.3927 resistance first. Meanwhile, break of 1.3524 support will bring resumption of whole down trend from 1.4791.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, break of 1.3927 resistance will argue that the correction has completed with three waves down to 1.3480 already.

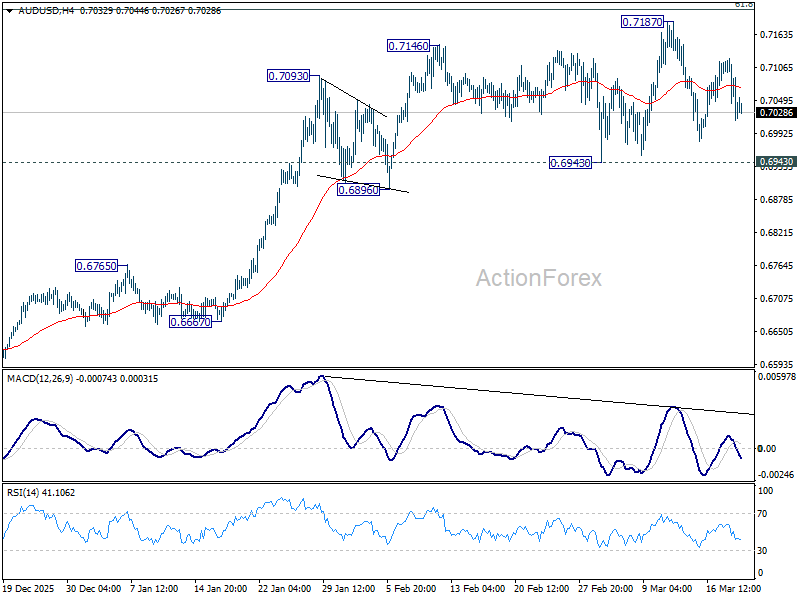

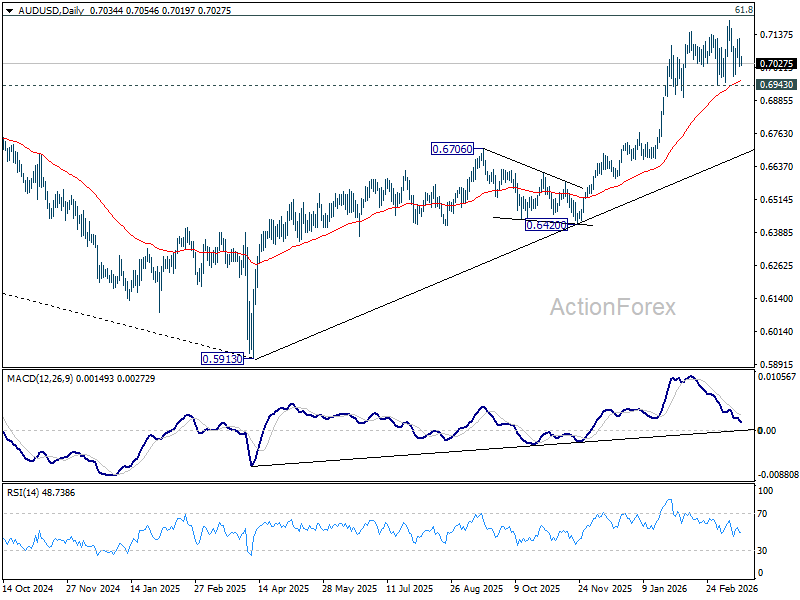

AUD/USD Daily Report

Daily Pivots: (S1) 0.6986; (P) 0.7055; (R1) 0.7093; More...

Sideway trading continues in AUD/USD and intraday bias remains neutral at this point. With 0.6943 support intact, further rally is still expected. On the upside, firm break of 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 could prompt upside acceleration to 161.8% projection at 0.7703. However, firm break of 0.6943 will indicate that a larger scale correction is already underway.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will pave the way back to 0.8006. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

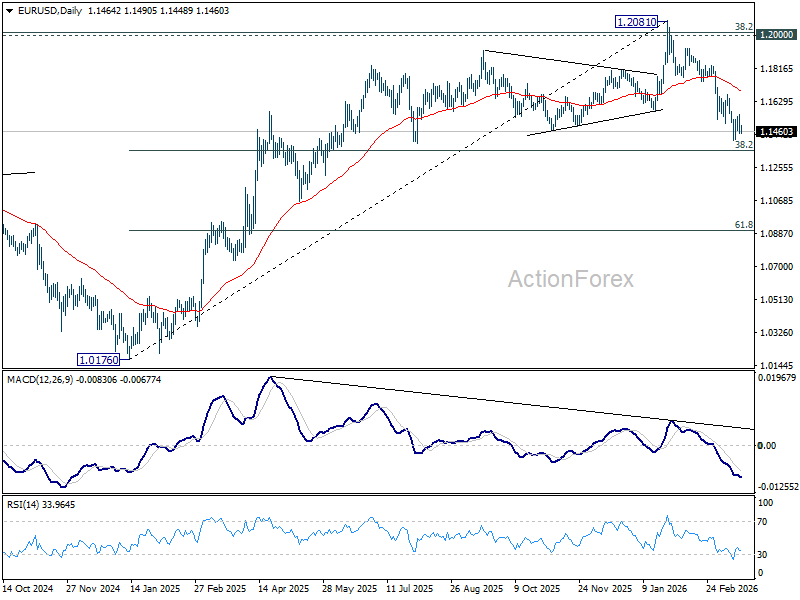

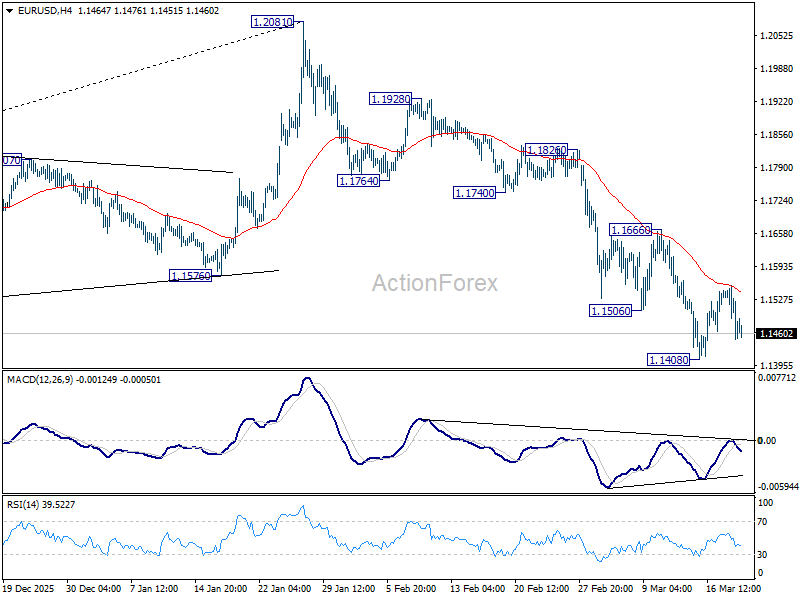

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1518; (R1) 1.1570; More….

Intraday bias in EUR/USD stays neutral and more consolidations could be seen. Further decline is expected as long as 1.1666 resistance holds. Below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Firm break there will target 61.8% projection at 1.0904 next.

In the bigger picture, the break of 55 W EMA (now at 1.1495) confirms rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. In either case, deeper fall is now expected to long term channel support (now at 1.0528. Risk will stay on the downside as long as 1.2081 holds, in case of recovery.