Sample Category Title

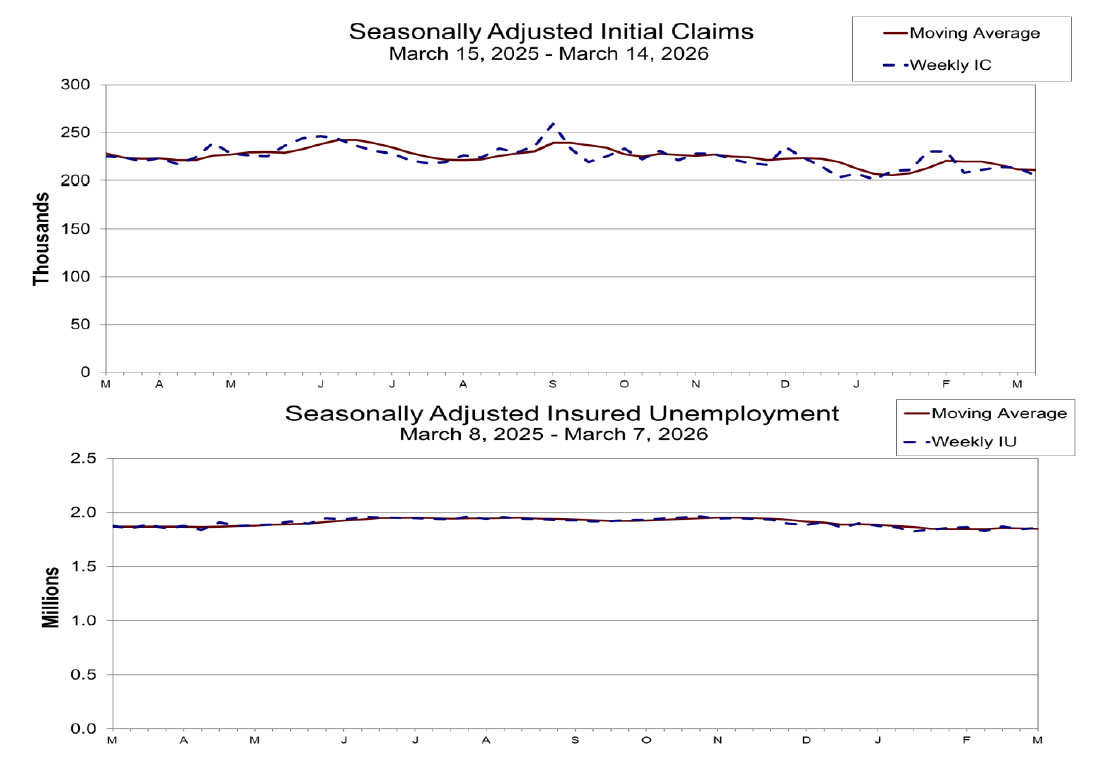

US initial jobless claims fall to 205k vs exp 215k

US initial jobless claims fell -8k to 205k in the week ending March 14, below expectation of 215k. Four-week moving average of initial claims fell -750 to 211k.

Continuing claims rose 10k to 1,857m in the week ending March 7. Four-week moving average of continuing claims fell -2k to 1.851m.

BoE unanimous rate hold surprises as doves abandon cut calls amid energy shock

Bank of England left Bank Rate unchanged at 3.75%, but the unanimous vote came as a clear surprise. Markets had expected a 6–3 or 7–2 split, with several known doves continuing to push for rate cuts. Instead, even the most dovish members backed a hold, signaling a sharp shift in near-term policy thinking as the energy shock reshapes the inflation outlook.

The statement highlighted that the escalation in the Middle East has led to a “significant increase” in global energy prices, which will feed through to both household bills and business costs. While domestic inflation had been easing prior to the shock, CPI is now expected to rise again in the near term. The Committee stressed the growing risk of second-round effects, particularly in wage and price-setting behavior.

Crucially, the unanimous decision masks a divergence in underlying views. Dovish members such as Dave Ramsden and Sarah Breeden made clear they would have voted for a cut absent the energy shock, while Swati Dhingra and Alan Taylor also maintained that easing could still be appropriate under a benign scenario. Their shift to holding reflects a pause rather than a change in medium-term bias.

On the other side, more hawkish members including Catherine Mann, Huw Pill, and Megan Greene emphasized the risk that higher energy prices could re-embed inflation. They pointed to heightened sensitivity among households and firms after years of elevated inflation, increasing the likelihood of second-round effects. This group appears more concerned that inflation persistence could return if policy is eased prematurely.

Governor Andrew Bailey and Clare Lombardelli struck a balanced tone, acknowledging both the inflationary impact of the energy shock and the drag on growth. However, the emphasis remained on ensuring inflation returns sustainably to target, reinforcing that inflation risks have regained priority despite weaker activity.

Overall, the BoE has shifted from an easing bias to a cautious pause. Rate cuts are likely delayed as policymakers wait for greater clarity on the scale and duration of the energy shock. While hiking remains a low-probability outcome, it has re-entered the discussion at the margin, marking a clear change in the policy outlook.

(BOE) Bank Rate maintained at 3.75%

Monetary Policy Summary, March 2026

At its meeting ending on 18 March 2026, the Monetary Policy Committee (MPC) voted unanimously to maintain Bank Rate at 3.75%.

Conflict in the Middle East has caused a significant increase in global energy and other commodity prices, which will affect households’ fuel and utility prices and have indirect effects via businesses’ costs. Prior to this, there had been continued disinflation in domestic prices and wages. CPI inflation will be higher in the near term as a result of the new shock to the economy.

Monetary policy cannot influence global energy prices but aims to ensure that the economic adjustment to them occurs in a way that achieves the 2% target sustainably. The MPC is alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist. The MPC is also assessing the implications for inflation of the weakening in economic activity that is likely to result from higher energy costs.

The Committee will continue to monitor closely the situation in the Middle East and its impact on global energy supply and energy prices. It stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term.

Minutes of the Monetary Policy Committee meeting ending on 18 March 2026

1: Before turning to its immediate policy decision, the Monetary Policy Committee (MPC) discussed recent developments in global economic and financial conditions, the immediate implications for the UK economy, and how these developments could affect the medium-term outlook and the MPC’s strategy.

Global economic and financial conditions

1: Since the Committee’s February meeting, the main development had been the outbreak of conflict between Israel and the United States, and Iran. The conflict had spread to other parts of the Middle East, with energy infrastructure targeted. Prior to the conflict, there had otherwise been limited news in the global economy since the February Monetary Policy Report.

2: Shipping through the Strait of Hormuz, through which around one-fifth of global oil and liquefied natural gas supply flowed, had almost ground to a halt following some Iranian attacks on vessels attempting transit. The most significant economic impact of developments in the Strait had been a sharp rise in both the level and volatility of energy prices, alongside upward pressure on a range of other commodity prices, such as fertiliser and neon gas.

3: Oil prices had increased significantly since the previous MPC meeting. The Brent crude spot price in the run-up to the MPC meeting on 18 March had been over $100 per barrel. This was around 60% higher than at the time of the February Report and the highest level since 2022, when oil prices had last increased by a comparable magnitude.

4: The Dutch Title Transfer Facility spot price, a measure of European wholesale gas prices, in the run-up to the MPC meeting on 18 March had been over €50 per MWh. This was around 60% higher than its pre-conflict level earlier in the year. Prices of futures contracts for UK natural gas, which would feed into the next Ofgem price cap for July to September, had increased on average by 35 to 40%. While the recent increase in wholesale gas prices had been substantial, prices had remained well below the peaks they had eventually reached in the period following Russia’s invasion of Ukraine in 2022.

5: The negative impact of the closure of the Strait of Hormuz on global oil supply would only be partially offset by the announcement of a coordinated release of strategic oil reserves by the member countries of the International Energy Agency. These reserves would likely be made available to the market over a period of several weeks and would take time to be transported to refineries.

6: It remained to be seen how long the conflict would last. The duration of the reduced supply of energy from the Middle East was therefore uncertain. Notwithstanding that uncertainty, intelligence from market participants suggested that their central expectation was for a relatively short-lived conflict. In that context, members noted upside risks to oil and gas prices looking ahead. Energy supply would take time to recover even if the conflict abated. Efforts to rebuild stocks, as well as greater awareness of vulnerabilities in the global energy network, could sustain higher oil and gas prices. Distributions implied by financial market options also suggested that upside risks to oil and gas prices had increased significantly, at least over the next few months.

7: The conflict had generally led to increased volatility and a deterioration in risk sentiment in financial markets relative to the Committee’s previous meeting. Equity prices across advanced economies had fallen back since the conflict began. UK equity prices were overall little changed since the February Report, having increased ahead of the outbreak of hostilities before declining thereafter. Spreads on investment-grade and high-yield corporate bonds had widened since the conflict began. The sterling effective exchange rate index was little changed since the February Report, while the US dollar had strengthened somewhat.

8: The market-implied path for Bank Rate had increased significantly since the February Report. Alongside developments in other asset prices, this meant that overall financial conditions had tightened. A large majority of responses to the Bank’s latest Market Participants Survey, which had been submitted between 4 and 6 March, expected no change in Bank Rate at this meeting, similar to market pricing. Beyond the near term, the latest market-implied path for Bank Rate sloped slightly upwards over 2026. Market intelligence gathered by Bank staff emphasised that market participants were recalibrating the balance of risks to the path for Bank Rate in light of the rise in energy prices. In the run-up to this MPC meeting, the market-implied path for ECB policy rates had suggested some tightening this year. The path for US policy rates had suggested some loosening, albeit less so than prior to the outbreak of the conflict.

9: The US Supreme Court ruling in relation to the International Emergency Economic Powers Act (IEEPA) had led the US administration to replace previously imposed IEEPA tariffs with a new temporary, uniform 10% tariff on all trade partners under alternative authority. While the direct macroeconomic implications for the UK of the lower US effective tariff rate appeared small, uncertainty around the medium-term outlook for US trade policy had increased somewhat, though remaining well below levels seen in 2025.

UK current economic conditions

10: There had been only limited news in the near-term domestic outlook prior to the Middle East conflict. Twelve-month UK CPI inflation had fallen to 3.0% in January from 3.4% in December. This was 0.1 percentage points above the short-term forecast published in the February Report, largely due to a smaller-than-expected fall in services inflation. Services consumer price inflation had been 4.4% in January, 0.2 percentage points above the February Report forecast. Higher frequency measures of underlying services inflation had picked up a little. In light of this data news, CPI inflation was now expected to be a little over 3% in February.

11: Volatility in oil and gas prices had made the short-term outlook for inflation particularly uncertain, but recent increases in energy prices would delay the return of CPI inflation to the 2% target that had been expected at the time of the February Report. The immediate effect would be through higher fuel prices. Based on energy prices as of close of business on 16 March, CPI inflation was now expected to be close to 3½% in March, almost ½ percentage point higher than expected in the February Report.

12: CPI inflation had previously been projected to fall in 2026 Q2, as previous one-off price increases in April 2025 dropped out of the year-on-year comparison alongside the disinflationary effect of the 2025 Budget. Given higher fuel prices, the decline between Q1 and Q2 was now projected to be modest. CPI inflation was expected to be around 3% in Q2 rather than 2.1% in the February Report.

13: Higher wholesale gas prices would have minimal impact on household utility bills in the near term because the Ofgem price cap for April to June had already been determined. However, if current wholesale conditions persisted, they were likely to feed through mechanically into a higher price cap from July. Based on the oil and gas futures curves as of 16 March, Bank staff projections suggested that the direct contribution of energy prices to CPI inflation in 2026 Q3 would be around ¾ percentage points.

14: If they were to occur quickly, indirect effects from firms passing on higher energy costs to consumer prices could further push up CPI inflation by around ¼ percentage point in 2026 Q3. The eventual scale and timing of such indirect effects was uncertain. Taken together with the expected direct effects, and conditioned on energy prices in the run-up to this meeting, CPI inflation could increase to up to 3½% in Q3.

15: It was too early to judge how large any second-round effects from the new energy price shock would be through wage and price-setting. Prior to recent developments in energy prices, annual growth in private sector regular Average Weekly Earnings in the three months to January had been 3.3%, below the forecast in the February Report. An updated estimate by the Bank’s Agents suggested that basic private sector pay settlements were now expected to average 3.6% over 2026, 0.2 percentage points higher than the estimate that had been available at the time of the February Report.

16: There had been some declines in inflation expectations ahead of the Middle East conflict. The latest Bank/Ipsos and Citi measures of year-ahead expected inflation had both fallen. The Decision Maker Panel survey had reported that firms’ year-ahead own-price inflation expectations in the three months to February had edged down slightly. Timelier financial market-based measures of inflation compensation had increased since the conflict started, with near-term measures having increased markedly and by much more so than medium-term measures.

17: UK GDP had expanded by 0.1% in 2025 Q4, slightly below the 0.2% rate expected in the February Report. Notwithstanding some divergence in the signal from different business surveys, activity had remained subdued in 2026 Q1 with monthly GDP flat in January. Bank staff continued to estimate that underlying quarterly GDP growth for Q1 would be around 0.1 to 0.2%.

18: Labour demand had remained weak. The Labour Force Survey unemployment rate had been 5.2% in the three months to January, unchanged from December and close to the expectation in the February Report. Employment growth had remained subdued, while the vacancies-to-unemployment ratio had remained below the Bank staff estimate of its equilibrium rate.

19: It was too early to assess the full impact of recent developments in the Middle East on bank lending conditions in the United Kingdom. Term Overnight Indexed Swap rates had increased to levels previously seen in early 2025. Some mortgage lenders had increased the interest rates quoted on new mortgage products as a result. Despite a slowing in January, annual growth in the M4ex measure of broad money had remained robust at 3.6%.

Overview and the Committee’s discussions

20: The recent conflict in the Middle East, and the consequent disruption to oil and gas supply, had led to a significant increase in wholesale energy prices since the MPC’s previous meeting. Monetary policy could not influence global energy prices but aimed to ensure that the economic adjustment to these prices occurred in a way that achieved the 2% inflation target sustainably.

21: Prior to these events, there had been continued disinflation in the UK. This partly reflected the restrictive stance of monetary policy, and was consistent with subdued economic growth and building slack in the labour market.

22: In light of the new, and potentially large, external supply shock, the Committee’s discussions at this meeting focused on: what was known at this stage and what was likely to be known in the near future; its approach to considering the risks around a new medium-term outlook; and the potential implications for monetary policy.

23: The near-term outlook for CPI inflation had risen relative to the February Report projection. Increased energy prices would impact near-term inflation directly via increased household fuel and utilities prices, and indirectly as business’ energy-related costs would also be affected. Preliminary staff estimates, based on energy price developments in the run-up to this meeting, indicated that CPI inflation was now likely to be between 3 and 3½% over the next couple of quarters. In the February Report, CPI had previously been expected to fall back to around the 2% target from April, partly owing to measures in Budget 2025.

24: The first-round impact on inflation from global factors would depend on the scale and duration of the conflict, and its impact on energy and other commodities markets. The Committee noted that even a short-lived conflict was likely to lead to a delay in restoring energy production back to normal levels, as well as the possibility of lingering instability, that could leave energy prices elevated for a period of time. A more protracted conflict could result in broader supply chain disruptions that could push up inflation further, for example owing to disrupted air and sea transport logistics, impacts on fertiliser supply, and trade disruption.

25: Taking into account the lags with which changes in Bank Rate were transmitted, the most important factor in setting policy would be how medium-term inflation was affected by this supply shock. The MPC was assessing a range of risks to medium-term inflation in both directions, although upside risks appeared to have increased most notably since February.

26: The MPC was alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which would be greater the longer higher energy prices persisted. Energy and food prices, which were expected to rise, were particularly salient for households’ formation of inflation expectations. And households and businesses could have a heightened sensitivity to any new inflationary shock, following successive negative supply shocks in recent times. This could lead to self-perpetuating behaviour in wage and price dynamics, which could embed domestic inflationary pressures.

27: The MPC was also assessing the implications for inflation from the weakening in economic activity that was likely to result from higher energy costs. In contrast to the energy price shock in 2022, this shock was occurring at a point when growth was below potential and the economy was operating with a margin of spare capacity. Increases in household fuel and utility costs, and other prices, would squeeze real incomes. Household and business confidence could deteriorate and precautionary saving could rise, further weighing on demand. This could result in a more rapid or larger rise in unemployment. These factors could widen the output gap somewhat, potentially constraining second-round effects.

28: Monetary policy had been judged to have been somewhat restrictive prior to the shock. The market-implied path for Bank Rate had shifted up significantly since the MPC’s previous meeting, and financial conditions had tightened. Against that backdrop, the Committee would continue to monitor and assess developments closely.

29: Members agreed that developments over the next six weeks could shed light on the likely scale and duration of the conflict, as well as providing some early evidence on the likely propagation of the shock. There was a range of possibilities for how monetary policy might need to respond to different developments and risks. A larger or more protracted shock, which risked greater second-round effects in wage and price setting, would require a more restrictive policy stance. Conversely, policy would need to be less restrictive if the shock was very short-lived, or if there were to be a larger opening up of slack in the economy that was expected to reduce medium-term inflationary pressures. The MPC would act as necessary to ensure the 2% target was met sustainably.

The immediate policy decision

30: The Committee turned to its policy decision at this meeting.

31: All members preferred to maintain Bank Rate at 3.75% at this meeting. The Committee would have more information and analysis ahead of its next meeting on the evolution and impact of the conflict. The Committee would continue to monitor closely the situation in the Middle East and its impact on global energy supply and energy prices, and the UK inflation outlook. All members stood ready to act as necessary to ensure that CPI inflation remained on track to meet the 2% target in the medium term.

32: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 3.75%.

33: The Committee voted unanimously in favour of the proposition.

MPC members’ views

34: Members set out the rationale underpinning their individual votes on Bank Rate.

Members are listed alphabetically.

Votes to maintain Bank Rate at 3.75%

Andrew Bailey: Large movements in energy prices have resulted from events in the Middle East and uncertainty over the duration of supply disruptions. Monetary policy cannot reverse this shock to supply. Its resolution depends on action taken at its source to restore the safe passage of shipping through the Strait of Hormuz. Monetary policy must, however, respond to the risk of a more persistent effect on UK CPI inflation. A prolonged disruption to the supply of oil, natural gas and other commodities such as fertiliser and neon gas increases the upside risk to inflation. The recent experience of high inflation may also make households and businesses more sensitive to a new inflationary shock. At the same time, the starting point for this shock is a real economy with limited pricing power. Holding Bank Rate at this meeting is appropriate. I will be monitoring developments extremely closely and stand ready to act as necessary to ensure that inflation remains on track to meet the 2% target in the medium term.

Sarah Breeden: Conflict in the Middle East has significantly shifted the outlook for inflation. Absent this shock, the underlying disinflation process had continued broadly as I expected and, consistent with my vote in February, I would have expected to vote for a cut again in March. But the conflict will have a significant, though at this point highly uncertain, impact on inflation. I associate myself strongly with the MPC’s collective assessment and communications at this meeting. Monetary policy cannot influence global energy and commodity prices, but it can and it must aim to ensure that the economic adjustment to them occurs in a way that achieves the 2% target sustainably. How that adjustment occurs is hugely uncertain, with risks to both sides, and I vote to hold at this meeting. The Committee will learn more by its April meeting about the scale and duration of the shock, as well as its possible second-round effects, and so the implications for monetary policy.

Swati Dhingra: The economic outlook is at a crossroads following hostilities in the Middle East. The UK economy will face higher energy prices, though how much higher and for how long makes all the difference. In one scenario, we could see a more modest increase in energy prices which probably slows rather than derails disinflation as limited scope exists for significant pass-through and second-round effects, given the state of the labour market and broader domestic demand environment. In another scenario, severe and longer-lasting constraints on oil and gas supply, alongside broader trade disruptions, could overwhelm orderly market adjustment. This could warrant a hold or increase in Bank Rate to stabilise price-setting dynamics albeit creating a difficult trade-off with activity following a prolonged period of weakness. If we see something resembling the lower-inflation scenario, I would expect to reduce Bank Rate, possibly quickly, over the rest of the year. For now, there is value in pausing to reassess the balance of risks to inflation from the terms-of-trade deterioration.

Megan Greene: The risk of inflation persistence has risen, perhaps significantly, in light of the negative supply shock from the war in the Middle East. Pre-conflict data showed a mixed picture for the underlying disinflationary process: the Agents revised expected average pay settlements up to 3.6% in 2026; but households’ inflation expectations, while still elevated, had dropped significantly. With this new energy shock, preliminary Bank staff estimates suggest CPI inflation will rise above 3% for much of this year, above the threshold at which households are more sensitive to inflation outturns in their expectation setting. There could also be increases in fertiliser and food prices, and both energy and food prices are particularly salient for households’ inflation expectations. Inflation has been above target for the best part of five years, and households and businesses are likely to be more sensitive to upside surprises in inflation given successive negative supply shocks. I believe there may be a larger trade-off now than in 2022, but that the impact of this energy shock on inflation is paramount. It is appropriate to hold Bank Rate to learn more about the size and duration of the shock, and the extent of potential second-round effects.

Clare Lombardelli: The conflict in the Middle East will be damaging for the UK economy, increasing inflation and reducing output. We are early in the process of assessment. The shock will have direct effects such as higher fuel and utility prices; indirect effects on business energy and transport costs; and broader second-round effects as the shock transmits through the economy impacting demand, supply, expectations of inflation, wage-setting and pricing behaviour. Policy coming into this shock may have been broadly neutral or mildly restrictive and there has since been some tightening of financial conditions. We will learn more in coming weeks about the shock itself and its effects. I am prepared to act as needed to address any persistent inflationary effects that may emerge.

Catherine L Mann: Due to the conflict, the tension between rising inflation and softening activity – a configuration of data that had been relevant for my decisions earlier last year, but which had lessened sufficiently for me to consider monetary easing – has re-emerged and could easily worsen. Sustained pressure on energy prices could re-embed the inflation persistence of the last few years, through households’ salience to energy prices, firms’ state-dependent pricing, staggered wage contracts, and attentiveness thresholds. Significant volatility in oil and gas prices will increase volatility in other prices, putting systematic upward pressure on inflation. On the activity side, while the Ofgem price cap limits household exposure now, a further weakening in consumer sentiment and demand could result from an increase in their precautionary saving buffers. Financial conditions have tightened considerably in nominal terms, but relatively less so in real terms, complicating assessment of restrictiveness. The new forecast and high-frequency data arriving over the coming weeks will help inform my next decision. Since the conflict may yield a sustained inflation shock, I see the balance between inflation and activity to have shifted away from considering a cut towards considering a longer hold, or even a hike at some point to lean against inflation persistence.

Huw Pill: Events in the Middle East have imparted an inflationary impulse to the UK economy via their impact on global energy prices. In the first instance, this impulse transmits through higher fuel and utilities prices (direct effects) and the pass-through of higher input costs into other consumer prices (indirect effects). Owing to lags in transmission, monetary policy can do little to dampen the resulting short-term volatility in inflation. But monetary policy must contain potential second-round effects that would otherwise exert a more lasting impact on CPI inflation. I continue to believe structural change in price and wage-setting behaviour over the past decade has made the propagation of inflationary impulses more persistent than in the past. This assessment has been reinforced by upward revisions to the Agents’ pay survey, with settlements in 2026 now expected at 3.6%. As such, the potential for second-round effects following recent events in the Middle East remains substantial, justifying caution in monetary policy setting. While financial conditions have tightened in recent weeks, whether this proves sufficient to contain potential upside risks to price stability stemming from energy prices is an open question. I remain alert to those risks and stand ready to act if they intensify.

Dave Ramsden: The damaging economic shock resulting from the Middle East conflict has caused me to revisit my policy position. Data releases since the February Report have broadly been in line with my expectations, and suggested continuing disinflation, so I would have otherwise voted for a 25 basis point cut in Bank Rate at this meeting. The conflict has now led me to vote for a hold in Bank Rate. There is a high degree of uncertainty around the scale and duration of the conflict, as well as its economic impact and any subsequent second-round effects. However, I agree with our current collective assessment of the economic outlook, including the risks to inflation and to activity, as set out in the Monetary Policy Summary and minutes. I stand ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term.

Alan Taylor: I think it appropriate to see us pausing to take stock, but inappropriate to infer a directional shift from this meeting. Before events in the Middle East, the disinflation process was nearly complete. Slack was worsening, with inflation set to reach target, making the case for a cut. However, the energy shock perturbs the near-term environment, with uncertain consequences contingent on its magnitude and duration. In a benign scenario, we might look through a milder shock, as in 2011 when the MPC faced an energy shock against the backdrop of a weak labour market. In this scenario, inflation would be higher and then lower in the near term, but largely unchanged in the medium term (when monetary policy has traction) with activity weakening. This could imply faster and potentially deeper rate cuts, once inflation risks subside, to avoid being behind the curve. In a less benign scenario, where supply disruptions persist, the MPC faces a tougher policy trade-off between elevated inflation and even weaker activity. Given massive uncertainty around future energy prices, I currently see a high bar to hiking. I prefer to hold while we better gauge the shock. Policy can then be calibrated to deliver our 2% target, and we can take activist steps whenever needed.

Operational considerations

35: On 18 March, the stock of UK government bonds held for monetary policy purposes was £528 billion.

36: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Brian Bell was present as the Treasury representative.

David Roberts was present as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

37: Megan Greene declared to the Committee that she would be taking up a non-executive director role at Trastor Real Estate Investment Company, a Greek real estate investment company listed on the Athens stock exchange, focused on acquiring and managing commercial real estate assets in Greece. It was confirmed that Trastor has zero exposure to UK real estate. It was agreed that Megan Greene would recuse herself from any MPC papers or discussions concerning EU commercial real estate in the event that the topic was discussed by the Committee.

XAG/USD Analysis: Silver Drops to March Low

As seen on the XAG/USD chart, the price of silver fell to the $70 level and briefly pierced it, marking the lowest level since early February.

Although geopolitical tensions typically support demand for safe-haven assets, silver is under pressure from expectations of a fresh inflationary surge driven by rising energy prices (as noted earlier, Brent crude has risen above $110).

Yesterday’s “hawkish” comments from Federal Reserve Chair Jerome Powell also played a role. The Fed maintained interest rates, signalling that any future cuts would only occur if inflation stabilises.

Technical Analysis of XAG/USD

On 4 March, analysing the XAG/USD chart, we:

- → drew a blue ascending channel;

- → suggested that price action around the channel’s median could provide key signals.

Over time, the median proved to be a strong resistance. By 10 March, point C had formed, after which:

- → on 13 March, the blue channel was breached;

- → on 17 March, price showed an intraday bearish reversal from the breakout level.

Trading volume analysis indicates that the market remains under considerable pressure.

Although the long lower shadow on the candle near the psychological $70 mark indicates some buyer activity, the overall picture remains bearish. A red descending channel can be drawn on the silver price chart, with its median potentially acting as resistance in the near term, thereby confirming the validity of the constructed channel.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

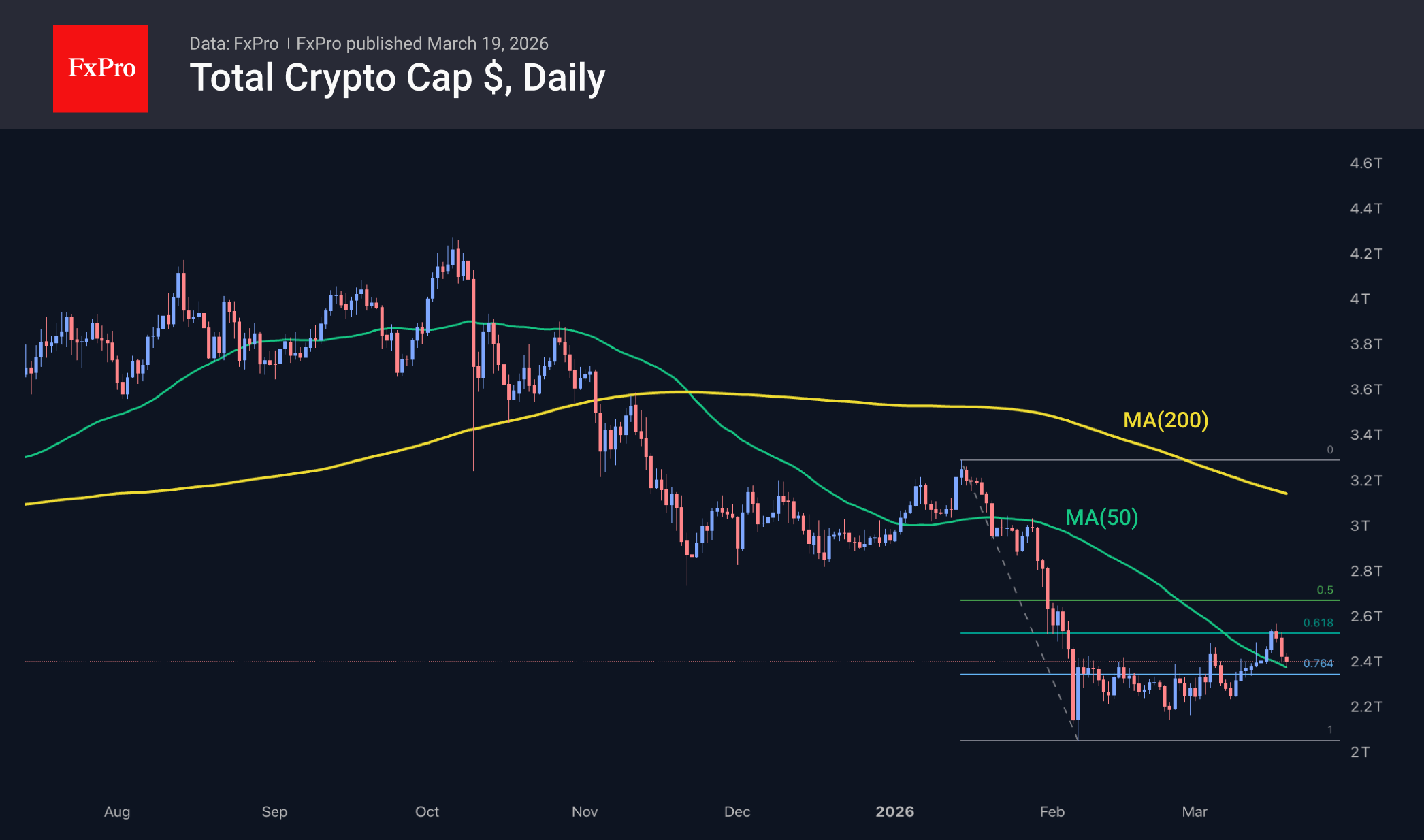

Crypto: Bulls May Have Their Horns Broken

Market Overview

The crypto market cap has fallen to $2.42 trillion, under pressure from sellers alongside risk assets, as the Fed pushes the next rate cut further into the future, boosting the dollar’s appeal. The decline also coincided with the upper boundary of the corrective rebound being touched. It is possible that cryptocurrencies were simply unable to ignore the significant deterioration in external sentiment, but they may soon return to outperforming other assets. Overall, however, we maintain a more pessimistic view, anticipating the bear market will continue, with bulls likely to be beaten soon, not least due to macro factors.

Bitcoin has fallen by 8.4% from its latest peak on Tuesday morning and briefly dipped below $70K at the start of the day on Thursday. At these levels, BTC is testing the 50-day moving average from above. As we have repeatedly warned previously, the upward momentum will face significant resistance at the boundary of a typical correction from the latest downward impulse. The leading cryptocurrency has more room to move within the $65K–$75K range. Breaking out of this range may require more momentum to determine the market’s direction for the coming days or weeks.

News Background

Investment bank Citigroup has lowered its 12-month price targets for Bitcoin and Ethereum amid delays in the adoption of US cryptocurrency legislation. The forecast for Bitcoin has been lowered from $143,000 to $112,000, and for Ethereum from $4,304 to $3,175. In a negative scenario, BTC risks falling to $58,000 and ETH to $1,198.

Bitcoin still has two-thirds of its bear cycle ahead, said Willy Wu, co-founder of the Bitcoin Vector project, urging investors to remain cautious. In his view, it is premature to expect sustained growth without an improvement in market liquidity.

Ethereum developers are testing the Fast Confirmation Rule (FCR), which will speed up transfers between the mainnet and the second layer from 13 minutes to 13 seconds.

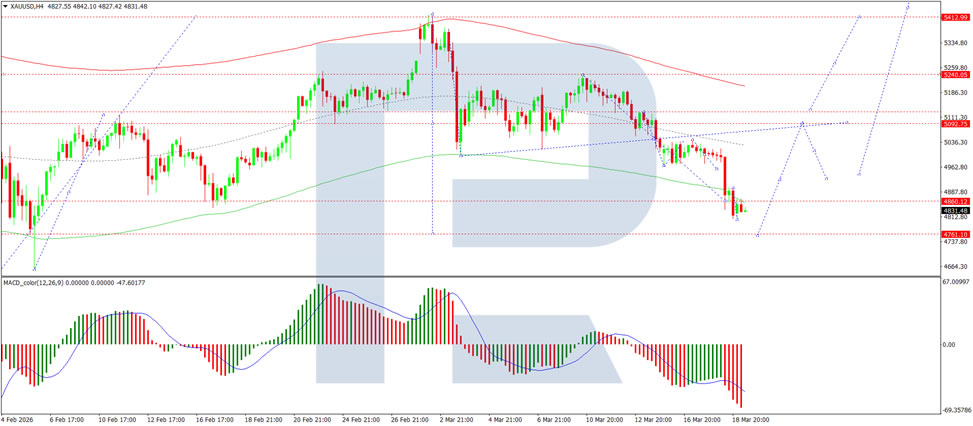

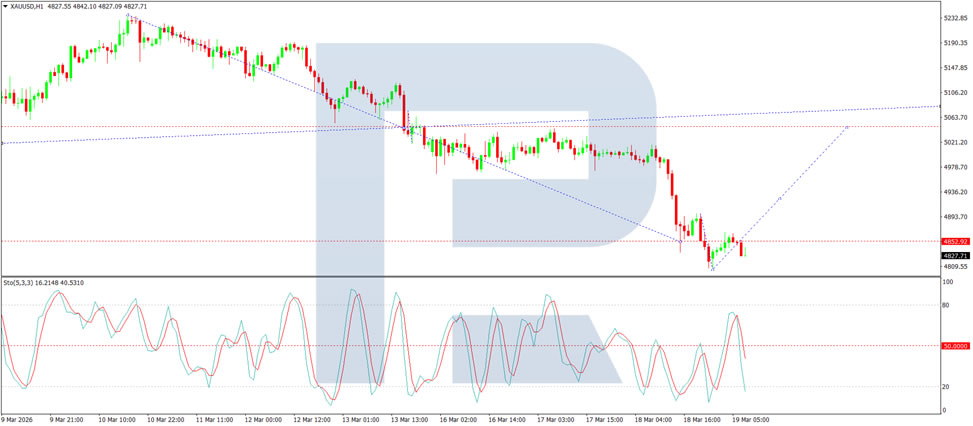

Gold Sold for Six Consecutive Days: What’s Happening

Gold prices stabilised around 4,830 USD per ounce on Thursday following a sixth consecutive decline, marking the longest losing streak since late 2024. The market remains under pressure from the Federal Reserve's hawkish stance, which currently outweighs geopolitical risks.

The Fed held rates unchanged and signalled only one cut this year. Jerome Powell emphasised that policy easing would only be possible with a more confident slowdown in inflation. The central bank also noted increased uncertainty amid the Middle East conflict, indicating that rising energy prices could add to inflationary pressure.

Tensions escalated further following Iranian missile strikes on a facility in Qatar housing the world's largest LNG infrastructure. The action was reportedly in retaliation for Israel's recent attack on the South Pars gas field.

While geopolitics typically supports safe-haven demand, it simultaneously drives oil prices higher. This dynamic intensifies pressure on gold through elevated inflation expectations and interest rate implications.

Since the start of the year, gold has remained in positive territory by approximately 12%. However, momentum has diminished as expectations for substantial rate cuts have receded, prompting some investors to lock in profits to meet margin requirements on other assets.

Technical Analysis

On the H4 XAU/USD chart, the market is forming a consolidation range around 4,858 USD. An upside breakout could pave the way for a correction towards 5,090 USD, while a downside breakout could extend the wave downward to 4,761 USD. The MACD indicator confirms the current momentum, with its signal line below the centre line and pointing strictly downwards.

On the H1 chart, the market broke below the 5,035 USD level and completed a wave down to 4,852 USD. Looking ahead, a corrective growth wave towards 5,044 USD is possible, followed by further downside to 4,761 USD. The Stochastic oscillator supports this scenario, with its signal line remaining above 50 and showing potential to rise towards 80 before turning lower.

Conclusion

Gold's six-day losing streak reflects the market's recalibration to a more hawkish Federal Reserve, with only one rate cut now priced for 2026. While escalating Middle East tensions, including strikes on Qatari LNG infrastructure, typically boost safe-haven demand, the simultaneous impact on oil prices and inflation expectations is proving the stronger force, keeping pressure on the non-yielding asset. Technical indicators suggest further downside potential towards 4,761 USD, though oversold conditions could trigger temporary bounces. The metal's year-to-date gains have been trimmed as investors adjust positions ahead of what now appears to be a prolonged period of higher rates.

Disclaimer

Any forecasts contained herein are based on the author's particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.

Chart Alert: Gold Medium-Term Downtrend Triggered as $4,960 Support Broke

Key takeaways

- Medium-term downtrend confirmed: Gold (XAU/USD) broke below the $4,960 key support (50-day MA) with a sharp sell-off, invalidating the prior rally as a “dead cat bounce” and signalling the start of a multi-week bearish phase.

- Hawkish Fed driving downside pressure: A less dovish Federal Reserve, reduced rate cut expectations, and rising 10-year US Treasury real yield have increased the opportunity cost of holding gold, weakening demand.

- Further downside risks ahead: With price action in a descending channel, gold remains bearish below $4,960 resistance, exposing next supports at $4,703–$4,554, unless a recovery above resistance negates the downtrend.

The price actions of Gold (XAU/USD) have triggered a pivotal movement yesterday, staging a bearish breakdown below with a daily close below its 50-day moving average that is acting as a key medium-term support at $4,960 (-3.7% on Wednesday, 18 March 2026 with a daily close of $4,818).

In terms of price structure, yesterday’s plunge suggests that the 23% rally from the 2 February 2026 low of $4,402 to the 2 March 2026 high of $5,420 is considered a corrective rebound, aka “dead cat bounce,” and the next movement is now skewed towards a potential multi-week bearish impulsive down move sequence.

Let’s now discuss some key macro factors that are driving this current multi-week medium-term downtrend phase of Gold (XAU/USD).

Less dovish Fed dot plot erases rate cut bets in 2026, stagflation risk reigns

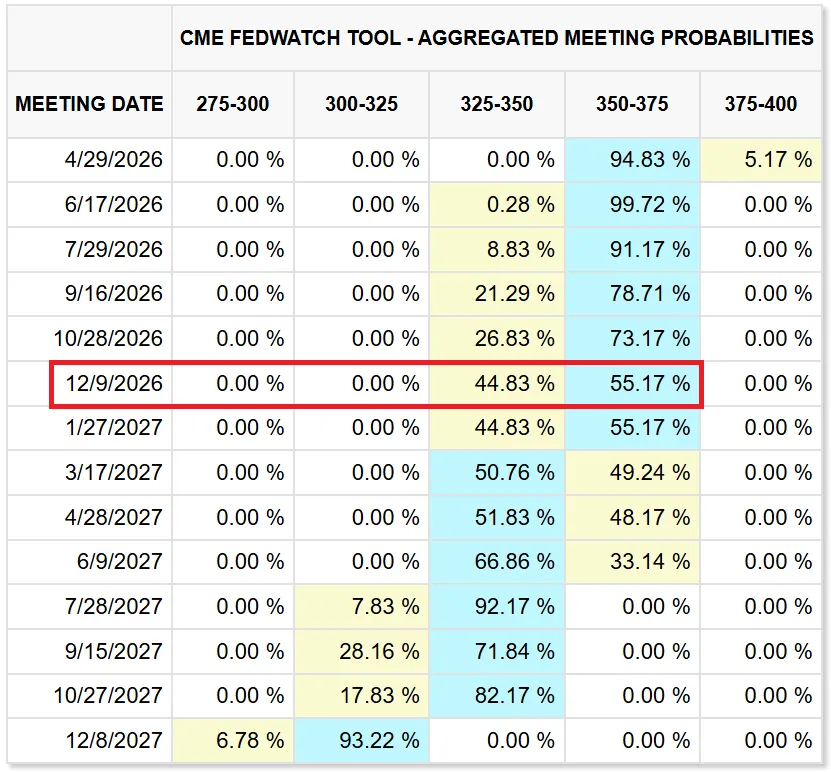

Fig. 1: Probabilities of Fed funds rate cuts, hikes, and pauses as of 19 Mar 2026 (Source: CME FedWatch tool)

Fig. 2: US 10-YR Treasury real yield medium-term trend as of 19 Mar 2026 (Source: TradingView)

Yesterday, the Fed left its Fed funds rate on hold as expected at 3.50%-3.75%. and maintained its forecast of one interest rate cut in 2026, with an upgraded median core PCE inflation trend forecast to 2.7% for 2026 from the previous projection of 2.5% made in December 2025.

Also, the most notable median projection shift was the long-run fed funds rate, up to 3.1% from 3.0%. In addition, the new 'dot plot' highlights a notable shift toward fewer projected rate cuts, and one policymaker is suggesting a rate hike next year in 2027; meanwhile, Governor Waller withdrew his dovish dissent for a cut yesterday. Hawkish vibes are brewing inside the Fed.

Overall, the data compiled by the CME FedWatch tool has indicated that the Fed funds futures market has started to price in zero-interest rate cuts in 2026, down from as many as three cuts at the start of the year. The aggregated probability for the Fed funds rate to be at 3.25%-3.50% (a 25-bps cut from the current rate of 3.50%-3.75%) now stands at 44.8% for the last FOMC meeting in 2026 on 9 December (see Fig. 1).

The 10-year US Treasury real yield jumped by 4 bps yesterday and closed above its 50-day moving average at 1.87%, now en route to potentially retest its medium-term range resistance of 1.98% (see Fig. 2).

Gold (XAU/USD) has a significant direct correlation with the longer-term US Treasury yields, as the precious yellow metal is a non-interest income-bearing asset.

A higher 10-year US Treasury real yield will imply a higher opportunity cost for owning and holding Gold (XAU/USD), in turn, creating a “lesser demand” sentiment that drives down prices of Gold (XAU/USD).

Let us now dissect the short-term trajectory (1 to 3 days) of Gold (XAU/USD) from a technical analysis perspective.

Gold (XAU/USD) – Another downleg in progress below $4,960

Fig. 3: Gold (XAU/USD) minor trend as of 19 Mar 2026 (Source: TradingView)

Fig. 4: Gold (XAU/USD) medium-term trend as of 19 Mar 2026 (Source: TradingView)

Watch the $4,960 key short-term pivotal resistance (also the 50-day moving average) to maintain the current bearish impulsive down move sequence for the next intermediate supports to come in at $4,703/4,655 and $4,587/4,554 (Fibonacci extension and lower boundary of minor descending channel from 2 March 2026 high) (see Fig. 3).

On the other hand, a clearance and an hourly close above $4,960 invalidates the bearish tone for a squeeze up to retest the next intermediate resistances at $5,040 and $5,125 (also the 20-day moving average).

Key elements to support the bearish bias on Gold (XAU/USD)

- The price actions of Gold (XAU/USD) have started to oscillate within a minor descending channel since the 2 March 2026 high of $5,420 (see Fig. 3).

- Before Gold (XAU/USD)’s bearish breakdown of its 50-day moving average yesterday, its daily RSI momentum indicator flashed on a bearish breakdown condition below its key ascending trendline support at the 50 level earlier on Monday, 16 March 2026 (see Fig. 4).

SPX Elliott Wave Chart: Larger Decline Resumes

The S&P 500 (SPX) continues to correct the cycle that began from the April 7, 2025 low. The internal subdivision of this correction is unfolding as a double three Elliott Wave structure, which reflects a complex corrective pattern rather than a simple decline. From the January 28, 2026 peak, wave (W) concluded at 6636.04, as illustrated in the 45‑minute chart. Within wave (W), the internal subdivision itself developed as another double three of lesser degree. In this sequence, wave W ended at 6775.5, wave X at 6952.51, and wave Y at 6636.04. This completed wave (W) at the higher degree.

Following this, wave (X) produced a corrective rally that terminated at 6884.9. The index has since resumed its downward trajectory in wave (Y). From the peak of wave (X), wave ((a)) ended at 6623.92, while wave ((b)) rallied to 6754.3. The near‑term outlook suggests that as long as the pivot at 6844.92 remains intact, rallies are expected to fail in either three or seven swings, leading to further downside pressure. This aligns with the broader corrective structure and reinforces the bearish bias.

The potential target for the decline is measured using the 100% to 161.8% Fibonacci extension of wave (W). This extension projects a zone between 6247 and 6475. Within this area, buyers may emerge, offering the possibility of renewed upside momentum. Thus, while the short‑term path favors weakness, the medium‑term view anticipates that the correction could eventually provide a base for another rally once the projected support zone is tested.

S&P 500 (SPX) 45-Minute Elliott Wave Chart

SPX Elliott Wave Video:

https://www.youtube.com/watch?v=IIcF5MCaGUE

XBR/USD Analysis: Brent Crude Rises Above $110

Yesterday, Brent crude prices moved sharply higher, with the XBR/USD chart showing breakouts above local resistance levels. Today, the price has climbed above the $110 mark, bringing it close to the multi-year high recorded on 9 March.

The bullish sentiment in the oil market is being driven by ongoing military tensions in the Middle East. According to recent media reports:

- → US President Donald Trump stated that Israel was responsible for the attack on Iran’s South Pars gas field;

- → Iranian missile strikes on Qatar’s key liquefied natural gas facilities caused significant damage.

Technical Analysis of XBR/USD

Recent price action allows for the construction of an ascending channel on the XBR/USD chart, reflecting heightened concerns over further escalation.

From a bullish perspective (as indicated by the arrows):

- → yesterday’s V-shaped rebound near the line dividing the lower half of the channel suggests strong buying pressure;

- → bulls showed confidence by breaking above the $106.40 level;

- → price remains in the upper half of the channel, with the median line potentially acting as support.

From a bearish perspective:

- → the RSI indicator is hovering near overbought territory;

- → long upper wicks around the $110 level point to selling pressure;

- → the upper boundary of the channel may act as resistance.

Taking the above into account, Brent prices remain under the control of buyers. As such, any pullbacks are likely to be limited in depth. A meaningful reversal would require significant changes in the geopolitical landscape.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

SNB holds rates, signals stronger FX intervention to cap Franc strength

SNB holds rates but strengthens intervention stance, aiming to cap CHF gains as energy-driven inflation rises only temporarily. The central bank kept its policy rate unchanged at 0.00%, as widely expected, but sharpened its language on foreign exchange intervention amid heightened global uncertainty.

The key shift lies in the SNB’s explicit acknowledgment that its “willingness to intervene… has increased,” in the context of escalating tensions in the Middle East. With safe haven demand likely to support the Swiss Franc, the SNB is signaling a readiness to act more forcefully to prevent excessive appreciation that could tighten financial conditions and undermine price stability.

Inflation projections reflect the temporary nature of the current energy shock. While short-term inflation is now expected to rise more strongly due to higher oil prices, medium-term pressures remain largely unchanged. The SNB continues to see inflation well within its price stability range, with forecasts at just 0.5% for both 2026 and 2027, and 0.6% for 2028.

On the growth side, the outlook remains subdued in the near term, with GDP expected to expand around 1% in 2026 before improving to 1.5% in 2027. Risks are tilted to the downside, particularly from global developments and the ongoing Middle East conflict. Taken together, the policy stance reinforces that the SNB’s primary focus remains on managing currency strength rather than responding to short-lived inflation pressures.