Sample Category Title

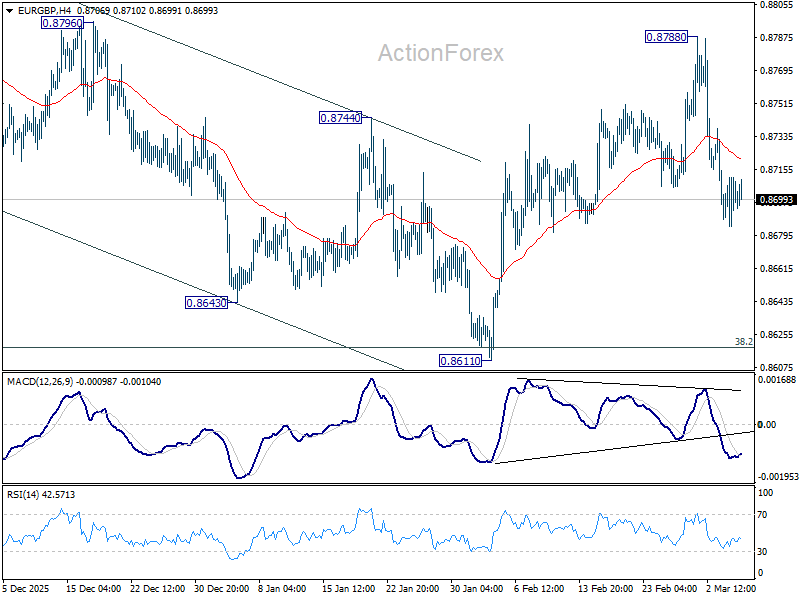

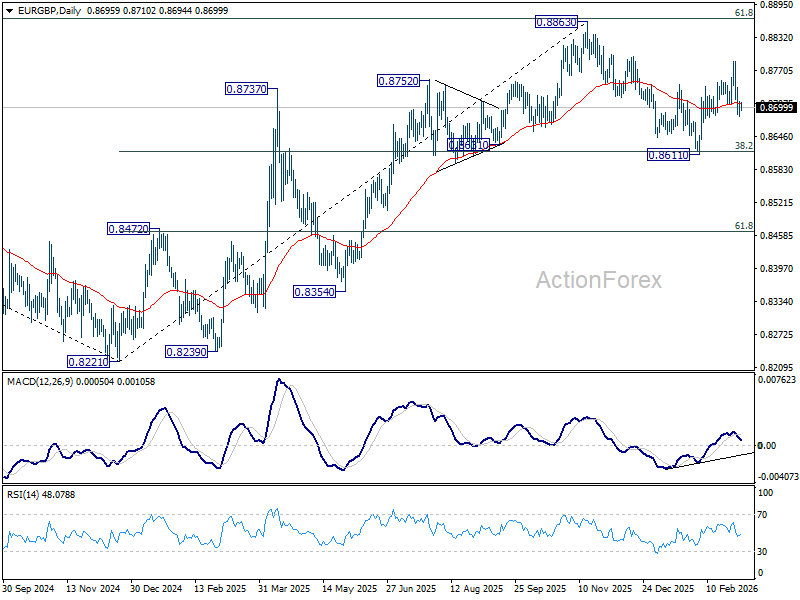

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8687; (P) 0.8700; (R1) 0.8715; More…

Intraday bias in EUR/GBP remains mildly on the downside for the moment. Rebound from 0.8611 could have completed at 0.8788. 8. The pattern from 0.8863 could already be in the third leg. Deeper fall would be seen back to 0.8611 support. For now, risk will stay mildly on the downside as long as 0.8788 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rise from 0.8221 medium term bottom is still in progress. Decisive break of 61.8% retracement of 0.9267 to 0.8221 at 0.8867 should confirm that it's reversing whole down trend from 0.9267. That should pave the way back to 0.9267. However, sustained break of 0.8611 support will indicate rejection by 0.8867 and indicate bearish reversal.

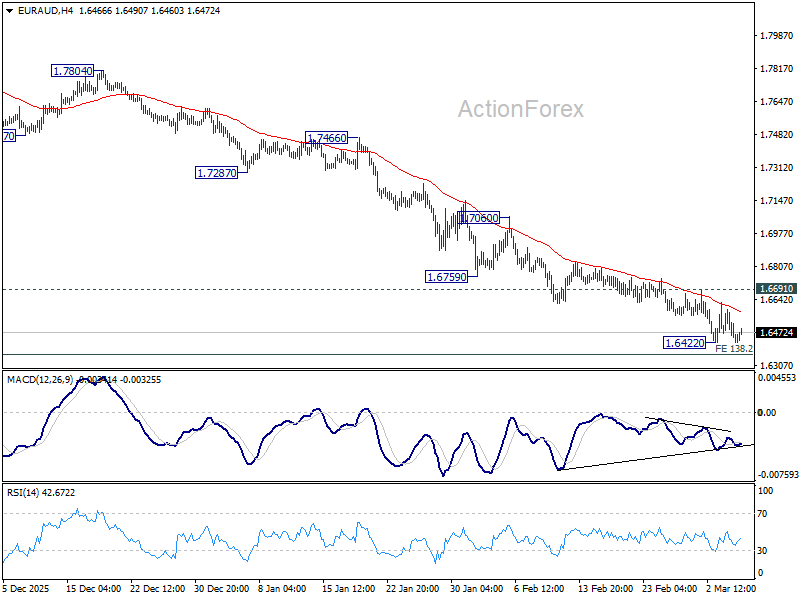

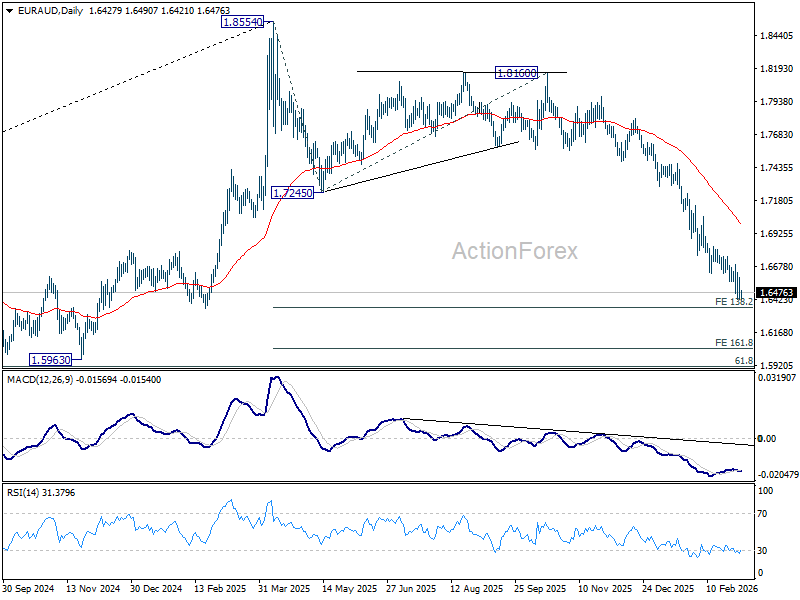

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6374; (P) 1.6487; (R1) 1.6556; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, decisive break of 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351 will resume the larger fall from 1.8554 to 161.8% projection at 1.6042 next. However, considering bullish convergence condition in 4H MACD, firm break of 1.6691 resistance will indicate short term bottoming. Intraday bias will be back on the upside fro stronger rebound towards 55 D EMA (now at 1.6994).

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

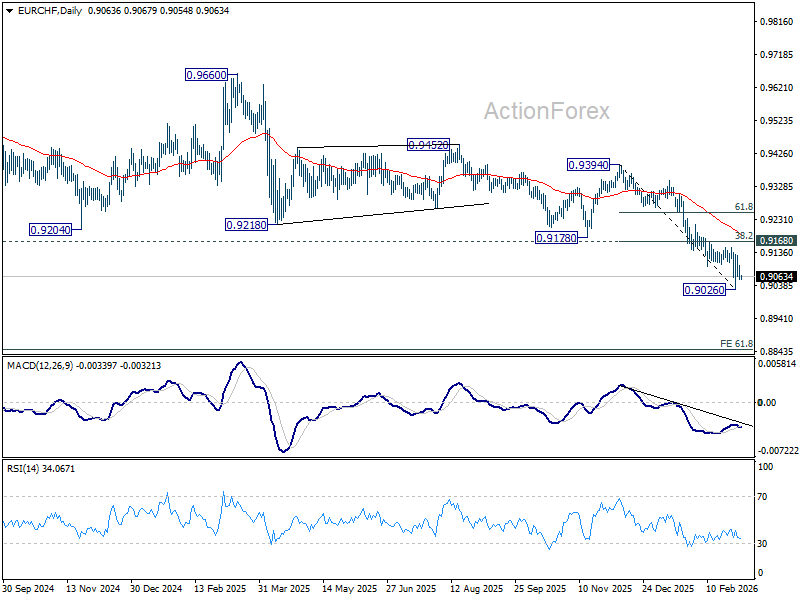

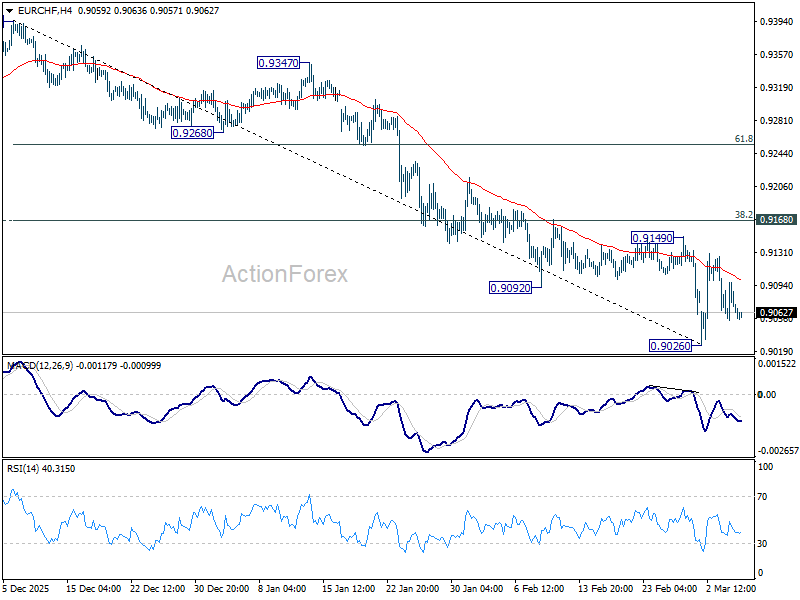

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9045; (P) 0.9076; (R1) 0.9097; More....

EUR/CHF is staying in range trading and intraday bias remains neutral. Price actions from 0.9026 short term bottom are viewed as a consolidations pattern only. While stronger recovery cannot be ruled out, upside should be limited by 0.9168 cluster resistance (38.2% retracement of 0.9394 to 0.9026 at 0.9167). Another fall below 0.9026 to resume the larger down trend is expected at a later stage. However, decisive break of 0.9167/8 will bring stronger rebound to 55 D EMA (now at 0.9186) and above.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

Senate Rejects Limits on Trump’s Iran Actions

In focus today

February flash inflation. Our forecast shows CPIF excluding energy at 1.41%, CPIF at 1.75%, and CPI at 0.52% y/y. See inflation preview here. Electricity prices were high in February, and we expect them to be nearly unchanged compared to January, before decreasing now in March. The recent developments in gas and oil are likely to contribute to slightly higher CPIF and CPI going forward, but so far, the impact on Swedish inflation appears to be moderate.

In the US, weekly jobless claims and flash Q4 productivity data are up for release. The latter will likely show cooling growth in line with the weaker-than-expected flash GDP release earlier and following Q3's sharp productivity acceleration (+4.9% q/q AR), which slowed unit labour cost growth to -1.9% q/q AR (+1.2% y/y).

Economic and market news

What happened over night

In the US, the Senate rejected a resolution seeking to limit President Donald Trump's authority to conduct military operations against Iran. The measure failed 47-53, with only limited Republican support. The outcome indicates that congressional Republicans are not ready to challenge the administration's military actions, suggesting minimal political constraints on US operations in the near term. The legislation is set to be voted on in the House today, where it is expected to face significant challenges.

China's National People's Congress opened with a 4.5-5% growth target for 2026 and plans to boost spending on defence and research, signalling a sustained strategic shift towards technology-driven growth. Premier Li Qiang highlighted the importance of innovation and industrial upgrading to address US trade pressures and subdued domestic demand, reinforcing Beijing's commitment to long-term technological self-reliance.

What happened yesterday

In energy markets, energy prices stabilised despite escalating Middle East tensions, as the conflict widened beyond the Gulf after a US submarine sank an Iranian warship off Sri Lanka and NATO intercepted a missile headed for Turkey. Weekly US oil inventory data showed no purchases for strategic reserves last week, though the US may consider selling reserves if oil price pressures persist. During a press conference, the White House stated it could not provide a timeline for securing shipping routes through the Strait of Hormuz, though naval escorts remain under consideration. Brent crude settled at 81.40 USD/bbl while European natural gas prices declined despite heightened Middle East tensions, closing at 47.3 EUR/MWh, down 13.15% d/d.

US and tech, President Donald Trump and major tech companies, including Amazon, Google, Microsoft and Meta Platforms, signed the "Ratepayer Protection" pledge. The initiative aims to prevent surging power demand from AI infrastructure from driving up household electricity prices, which have already risen by about 6% in 2025 With energy costs becoming a key campaign issue ahead of the midterm elections, the pledge seeks to address growing political pressure. However, implementation remains uncertain due to the decentralised and state-regulated nature of the US power market.

In the euro area, unemployment fell to a record-low 6.1% in January from 6.3% in December, with a decline of 184k unemployed, primarily in Italy, Spain, and France. While this signals a hawkish tilt for the ECB, frequent revisions to the data suggest caution in interpreting the sharp drop. We anticipate a more gradual decline in unemployment in 2026 as labour demand has cooled, though employment growth is likely to continue in Southern Europe, particularly Spain. Meanwhile, the final euro area PMI for February confirmed 51.9, with services slightly revised up to 51.9 and manufacturing steady at 50.8, signalling moderate growth.

In the US, the ADP national employment report showed a gain of 63k private sector jobs in February, aligning closely with consensus estimates and ADP's weekly projection (+50k). January's figures were revised down by -11k. Education and health care led job growth (+58k), continuing trends seen throughout 2025. The report is unlikely to move markets significantly. Meanwhile, the ISM non-manufacturing new orders index rose sharply to 58.6 in February from 53.1 in January, indicating robust service sector activity. Notably, the prices index declined (63.0; prev. 66.6), suggesting manufacturing cost pressures stem mainly from tariffs rather than broader inflationary factors.

In Switzerland, February inflation slightly exceeded expectations at 0.1% y/y (cons: 0.0%), with core inflation at 0.4% (prior: 0.5%), aligning with the SNB's Q1 forecast. Inflationary pressures remain subdued and should keep the SNB on its toes for the time being. This is only further amplified by the recent strengthening of CHF.

In Norway house prices fell 0.3% m/m s.a., significantly below Norges Bank's forecast of a 0.6% increase. This is not the determining short-term driver of monetary policy, but it does suggest some more caution amid reduced outlook for rate cut.

In Sweden, the services PMI unexpectedly fell to 48.3 in February from 53.8 in January, driven by a notable drop in business volume and new orders. It is too early to determine whether this decline is temporary or signals a more sustained trend. The weakness in services also pulled the composite PMI down to 50.5 from 54.4 in January.

Equities: Global equities rebounded through yesterday's session as the news flow from Iran evolved during the day. Despite mixed and at times contradictory headlines, particularly regarding Iran's willingness to negotiate, Western markets ultimately closed higher across both North America and Europe. This stood in sharp contrast to the heavy losses seen earlier in Asia and Japan yesterday.

Looking at the broader picture, however, the recent volatility has not translated into dramatic moves on a global aggregate level. Over the past five sessions global equities are down roughly 2.5%, while cyclicals have underperformed defensives by around 1pp.

Given the magnitude of the geopolitical shock originating from Iran, the relatively contained reaction across risk assets reflects that markets continue to frame the conflict primarily through the lens of energy supply risk, specifically the potential disruption of oil and gas flows through the Strait of Hormuz. So far, the broader macro-financial transmission channels remain limited.

This morning, Asian equities are trading higher, led by an extraordinary rebound of more than 10% in South Korea. As we highlighted yesterday, these markets currently display significant exuberance, and in such an environment even relatively small pieces of news can trigger outsized moves. This is why we wrote about getting caught wrong-footed yesterday and why we see many investors moving very close to benchmark.

This morning we have both European and US futures are modestly lower.

FI and FX: There was stabilisation in the market yesterday with European bond yields declining and corporate bond spread stabilising even though US bond yields rose in the afternoon after better than expected US economic data supported the equity market but also send US Treasury yields modestly higher. This morning, we have seen a rise in government bond yield across the Asian markets.

Energy prices stabilized yesterday amid a still tense situation in the Middle East. The weekly US oil inventory data showed that the US again did not buy for its strategic reserves last week ahead of the start of the military campaign. If pressure on oil prices does not start to ease, the US would likely consider selling strategic reserves. That will not be able to replace the oil shut in behind the Strait of Hormuz though but can help contain prices.

Chart Alert: WTI Crude Oil Bullish Breakout Above $78.10/Barrel in Play

Key takeaways

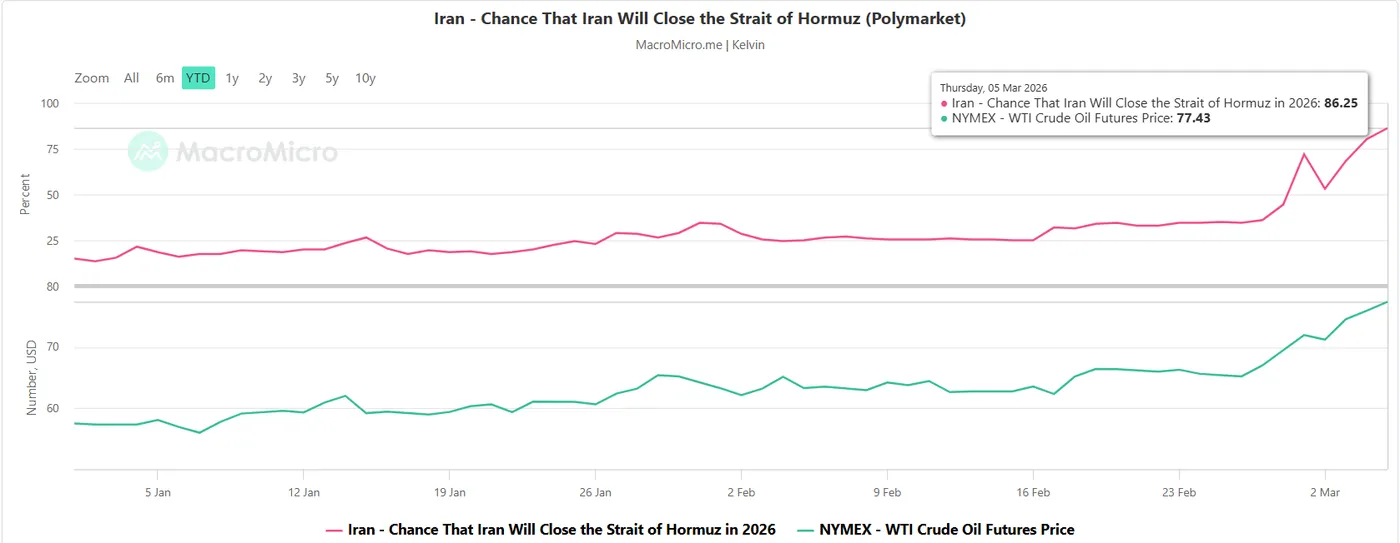

- WTI crude extends bullish breakout: Prices surged about 19% since 26 Feb, reaching a 14-month high near $78, after breaking a 28-month descending resistance, with geopolitical tensions from the United States–Israel strikes on Iran acting as the key catalyst.

- Geopolitical risk underpinning the rally: Rising fears that Strait of Hormuz—which handles roughly 25% of global seaborne oil trade—could be disrupted have pushed prediction-market odds of a closure to above 86%, reinforcing the bullish outlook for oil.

- Technical momentum still positive: WTI maintains a bullish structure above $73.38 support, and a break above $78.10 could extend the rally toward $80.30 and $83.60–$84.55, while a drop below support risks a pullback toward $69–$67.80 before the next potential upside leg.

The price actions of the West Texas (WTI) crude oil have staged the expected upside breakout from the minor bullish flag, as highlighted in our previous report.

In addition, WTI crude broke above a 28-month major descending resistance from 28 September 2023 swing high, gapped up above $71.33 on Monday, 2 March 2026, triggered by joint attacks by the US and Israel on Iran.

So far, WTI crude has rallied by around 19% since the publication of our last report on 26 February to print a 14-month intraday high of $78.06 on Tuesday, 3 March 2026.

Below are several key support factors that oil prices can continue to see further potential upside despite US President Trump’s assurance to provide naval escorts for oil tankers through the Strait of Hormuz, a key global oil flow chokepoint, to prevent any significant oil supply shock triggered by potential Iranian sabotage on oil tankers.

Rising odds on the closure of the Strait of Hormuz by Iran

Fig. 1: Probability that Iran will close the Strait of Hormuz in 2026 as of 1 February 2026 (Source: Polymarket, MacroMicro)

The Strait of Hormuz, situated between Oman and Iran, is a crucial maritime energy chokepoint, as it handles a quarter of the world's maritime oil trade and a fifth of the LNG trade, making it one of the most critical globally.

Based on the latest data from the prediction market platform Polymarket as of today (Thursday), 5 March 2026, as compiled by MacroMicro the probability of Iran closing the Strait of Hormuz in 2026 has increased to a current all-time high of 86.25%, surpassing the previous probability peak of 71.95% printed on 1 March 2026, during the onset of the latest US-Iran war (see Fig. 1).

Since the start of the probability trend of Iran closing the Strait of Hormuz in 2026, there has been a significant direct correlation with the movement of the WTI crude oil futures.

Hence, a fresh all-time high in terms of the probability of the closure of the Strait of Hormuz from Polymarket suggests that the ongoing short to medium-term bullish trend phases of WTI crude oil can persist.

Let’s now decipher the short-term (1 to 3 days) trajectory of WTI crude oil from a technical analysis perspective.

WTI Oil – Bullish acceleration intact, looking to break above $78.10/barrel

Fig. 2: West Texas Oil CFD minor trend as of 5 Mar 2026 (Source: TradingView)

Watch the tightened $73.38 key short-term pivotal support to maintain a bullish bias on the West Texas Oil CFD (a proxy of the WTI crude oil futures). A clearance above $78.10 increases the odds of the continuation of the bullish impulsive up move sequence for the next intermediate resistances to come in at $80.30 and $83.60/84.55 (also a Fibonacci extension) (see Fig. 2).

On the other hand, failure to hold with an hourly close below $73.38 support negates the bullish tone for a potential minor corrective decline to retest the next intermediate support zone of $69.26/67.80 (also close to the rising 20-day moving average) before the next potential bullish leg materializes for the West Texas Oil CFD.

Key elements to support the bullish bias on WTI Oil

- Price actions have continued to oscillate within a minor ascending channel since the 26 February 2026 low, with its lower boundary at around $73.38.

- The hourly RSI momentum indicator has staged a bullish breakout above its former descending resistance and continued to trend higher above the 50 level. These observations suggest short-term bullish momentum remains intact.

Don’t Jump to the Final Chapter Yet

Market volatility is turning investors’ heads as the Middle East conflict intensifies and enters a sixth day. Earlier reports from the New York Times that Iran was ready to negotiate were later dashed by Iranian authorities. Chinese financial institutions are scaling back their exposure to Middle Eastern debt – including Aramco – and despite US escort and insurance plans, traffic through the Strait of Hormuz reportedly came to a complete halt yesterday, with no ships transiting.

Donald Trump says that the US is doing very well in Iran, and investors are willing to believe him, hoping the conflict could move toward a resolution. But the news tell another story.

US and European markets were bid yesterday on the back of strong economic data. PMI data in Europe mostly hinted at faster expansion in economic activity in February, while ISM numbers in the US also looked solid – stronger activity combined with softening price pressures. The ADP report showed 63K new private jobs, higher than expected, though last month’s figure was revised down from 22K to 11K.

On the trade front, the US said it will raise the global tariff from 10% to 15%, but Europeans would keep their 10% tariff rate – whoop whoop – except perhaps for Spain. Trump said he does not want to trade with Spain anymore as the country is unwilling to get involved in the US/Israel conflict with Iran. But that apparently wasn’t an issue for markets – the IBEX rebounded 2.5% yesterday, while the Stoxx 600 recovered 1.37% on hopes that the Iran conflict could come to an end.

Frankly, I’m not sure why investors think so. There is no clear plan, missiles and bombs continue to fall, and oil and gas prices are trading higher this morning.

US crude is trading above $78 per barrel at the time of writing – near the highest levels since the Iran tensions began. European natural gas futures retreated 10%, but remain about 60% higher than last week’s levels. US natural gas futures remain steady – the US has been the world’s largest gas producer since the shale boom and benefits from relative energy independence. It is also the largest LNG exporter. The EIA had estimated – before the Iran conflict – that US gas prices would rise this year due to growing exports, but the US could decide to curb LNG exports to keep domestic prices in check. That would be terrible news for Europe. China, on the other hand, reportedly told its biggest refiners to halt diesel and gasoline exports.

So when I look at the news, I see one thing: escalating tensions.

Most US and European futures are down this morning – though losses are modest compared to earlier this week – while the FTSE is up, likely helped by rising energy prices. The Dubai Financial Market index, heavy in financial services and real estate, tumbled 5% after reopening for the first time since the conflict began – the exchange’s daily limit-down level.

Elsewhere, price action is mixed. The Nikkei is down 1.5%, the Hang Seng is up about 1% but struggles near its 200-day moving average, while the Kospi rebounds 11% today after yesterday’s 12% drop. Korean market moves are mind-blowing, and the amplitude alone signals that things are not going well. And I am not even talking about rising oil prices, which are outright negative for Korea, a country that imports about 97% of its energy, much of it passing through the Strait of Hormuz, where traffic reportedly halted yesterday. Price action therefore remains extremely jittery, and large gains – 11-12% intraday at the index level!! – are themselves signs of extreme volatility. And high volatility simply means high risk, including the possibility of significant losses ahead.

Globally, the rise in oil prices remains concerning. Higher energy prices could weigh on central bank expectations and push global yields higher. Rising rates would in turn pressure equity indices. The US 10-year yield continues to trend higher in Asia trading, along with Japanese and Australian yields. The US dollar is pushing higher after yesterday’s retreat. The EURUSD has slipped back below 1.16, while Cable is drifting toward 1.33.

The US dollar will likely remain in demand as long as Middle East uncertainty persists. The fact that gold hasn’t attracted stronger safe-haven flows suggests investors do not have many obvious places to hide.

So what’s next? It depends. Headlines do not point to a near resolution of the Middle East conflict, meaning the risk of further stress remains very much in play. Uncertainty will likely prevent global indices from recovering sustainably. If the conflict escalates, the dollar will appreciate further. Higher energy prices, priced in a stronger dollar, would weigh on global growth, with emerging markets likely among the hardest hit.

China today set its growth target at 4.5-5%, the lowest since 1991.

Oil exporters could diverge positively from importers in the short run. Mainland Europe, China, Japan, Korea and Taiwan are major oil importers, while the US, Canada and Brazil are among exporters. Of course, a prolonged conflict would eventually weigh on all indices – as slower global growth is bad news even for exporters – but in the short run, the pain could be heavier for economies dependent on imported energy.

There is one hope: the end of the conflict. Some investors appear willing to jump to the final chapter ahead of time – which is why we see strong gains on the smallest hints of good news. But there may still be more pain on the menu before a convincing rebound.

Elliott Wave Analysis: EURUSD Rebounding from Inflection Area

The short-term Elliott Wave outlook for EURUSD indicates that the rally to 1.2083 on January 27 marked the completion of wave (1). Following this peak, the pair entered a corrective phase in wave (2), which unfolded as a double three structure. From the high of wave (1), wave W concluded at 1.1776, while wave X ended at 1.1928. Subsequently, wave Y developed into a zigzag formation. Within this sequence, wave ((a)) finished at 1.1742, and wave ((b)) reached 1.1834, as illustrated clearly in the one-hour chart.

Wave ((c)) then extended lower, reaching the critical inflection zone between 1.142 and 1.161. This area corresponds to the 100%–161.8% Fibonacci extension of wave ((a)), a level often watched closely by traders for potential reversals. The pair has already begun to turn higher after completing the pullback at 1.153, where we identified the termination of wave ((c)) of Y of (2).

For confirmation of a sustained bullish trend, EURUSD must break above the prior wave (1) peak at 1.2083. Such a move would eliminate the risk of a double correction and reinforce the upward bias. In the near term, as long as the pivot at 1.153 remains intact, expectations favor further extension to the upside. This scenario highlights the importance of the recent inflection area as a foundation for renewed strength in the pair.

EURUSD 60-Minute Elliott Wave Chart

EURUSD Elliott Wave Video:

https://www.youtube.com/watch?v=0PPOuIUQD6w

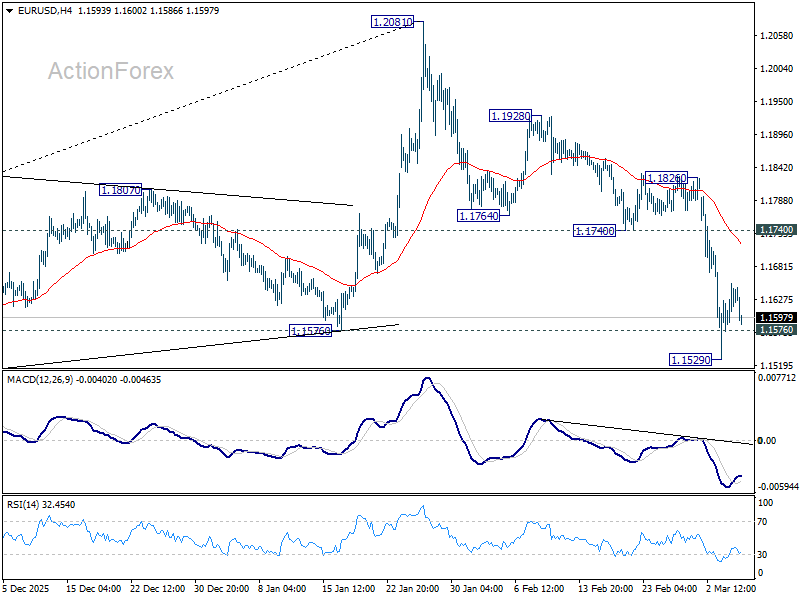

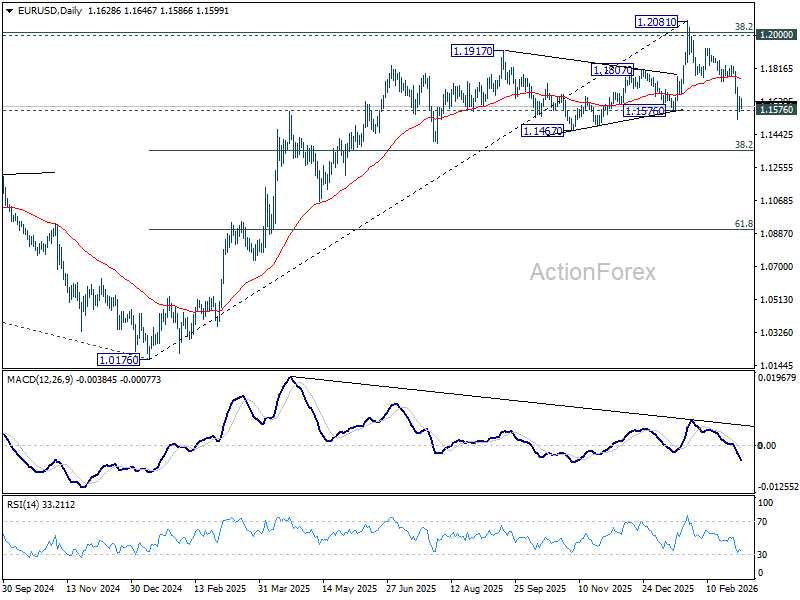

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1590; (P) 1.1622; (R1) 1.1670; More….

Intraday bias in EUR/USD remains neutral for consolidations above 1.1529 temporary low. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. However, firm break of 1.1740 support turned resistance will revive near term bullishness, and bring stronger rebound back to retest 1.2081 high.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

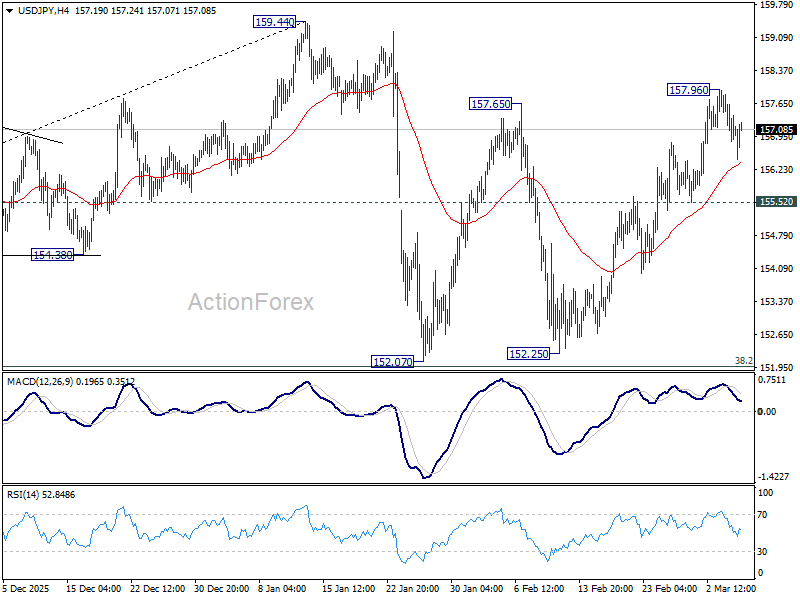

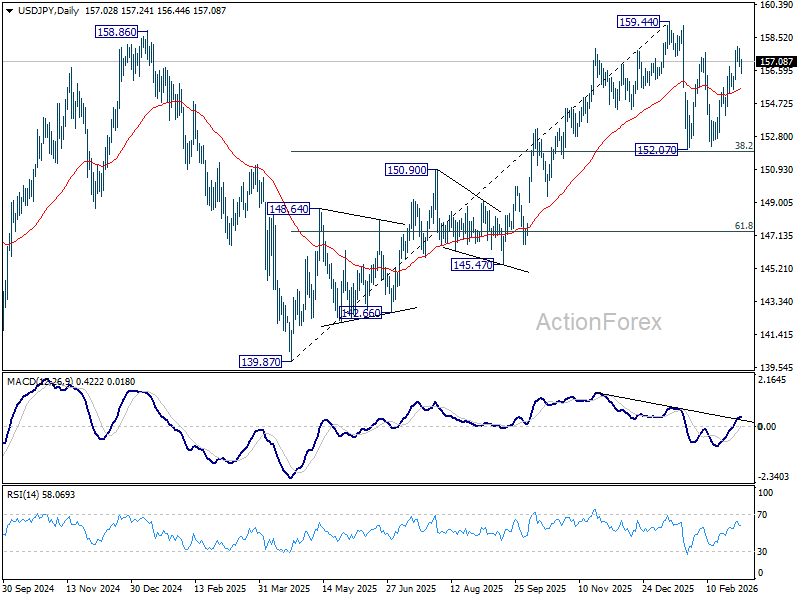

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.64; (P) 157.26; (R1) 157.65; More...

Intraday bias in USD/JPY stays neutral and more consolidations could be seen below 157.97 temporary top. On the upside, above 157.96 will extend the rebound from 152.25 to retest 159.44 high. On the downside, though, break of 155.52 will bring deeper fall back to 152.07/152.25 support zone. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

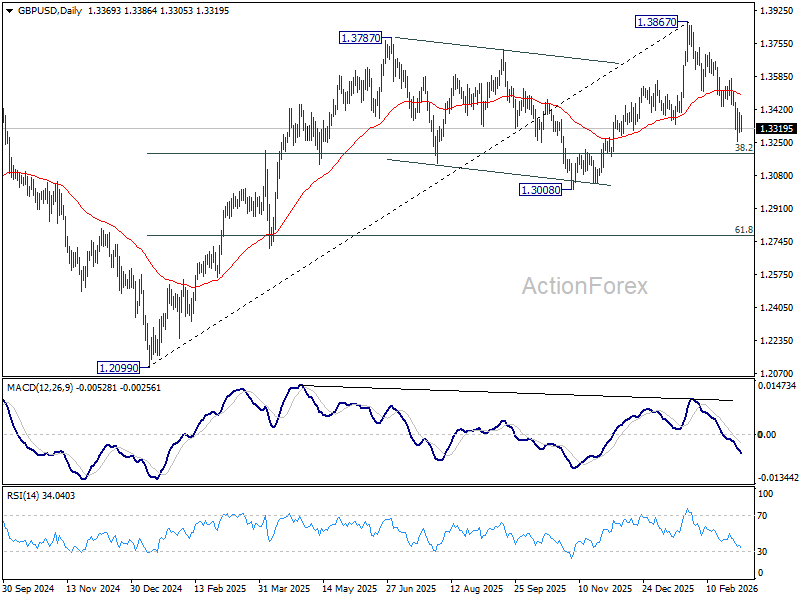

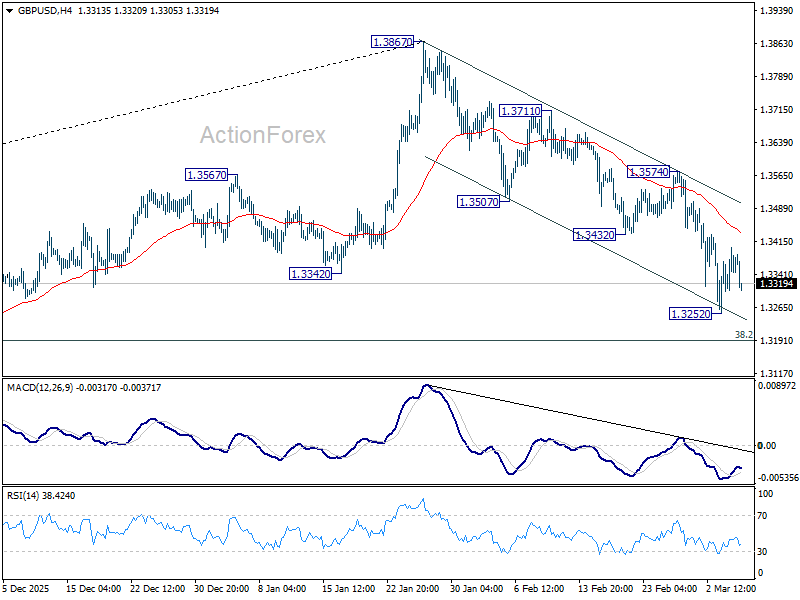

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3318; (P) 1.3361; (R1) 1.3417; More...

Intraday bias in GBP/USD remains neutral for consolidations above 1.3252 temporary low. Fall from 1.3867 should at least be correcting the rise from 1.2009. Below 1.3252 will target 38.2% retracement of 1.2099 to 1.3867 at 1.3192. Sustained break there will pave the way to 1.3008 support. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.