Sample Category Title

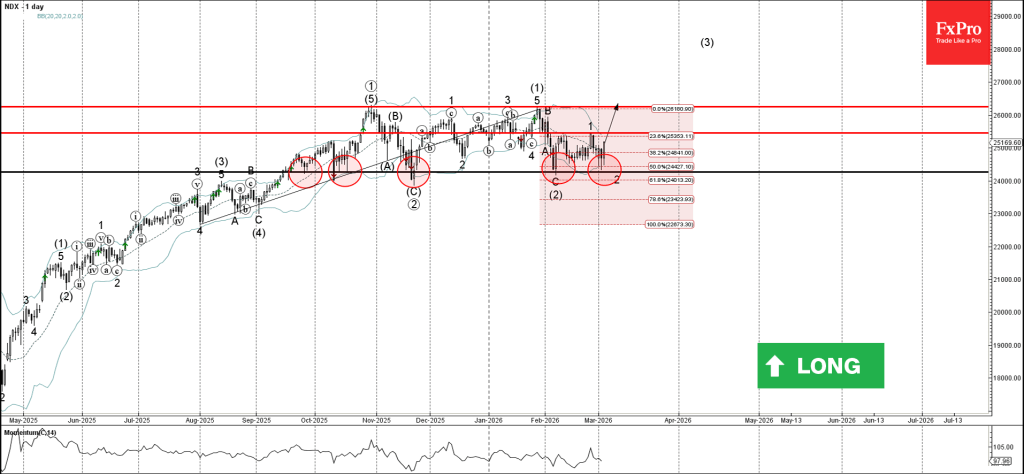

Nasdaq-100 Wave Analysis

Nasdaq-100: ⬆️ Buy

- Nasdaq-100 reversed from support zone

- Likely to rise to resistance level 25455.00

Nasdaq-100 index recently reversed from the support zone between the multi-month support level 24270.00 (which has been reversing the price from September), lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from August.

The upward reversal from this support zone stopped the earlier short-term correction 2 of the higher order impulse wave (3) from February.

Given the clear daily downtrend, Nasdaq-100 index can be expected to rise to the next resistance level 25455.00 (top of the earlier wave 1).

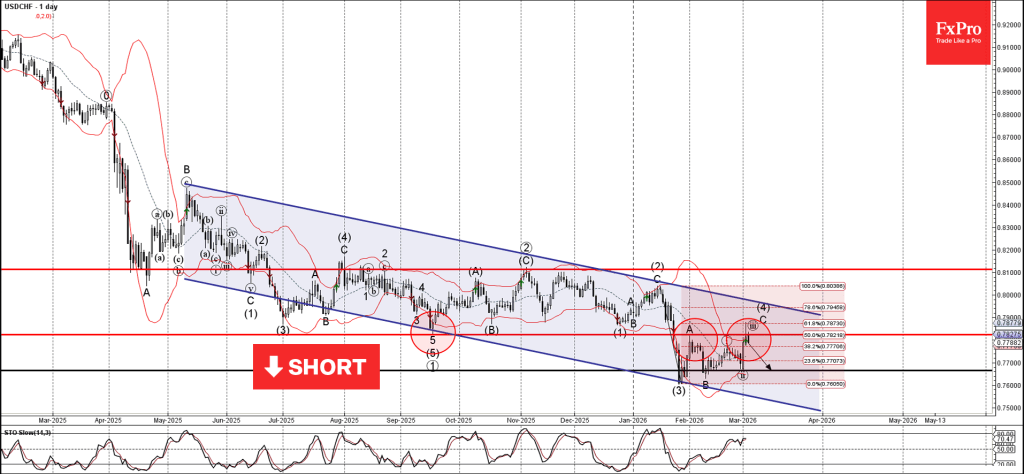

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF reversed from resistance zone

- Likely to fall to support level 1.5765

USDCHF currency pair recently reversed down from the resistance zone between the key resistance level 0.7830 (former multi-month support from September), upper daily Bollinger Band and the 50% Fibonacci correction of the downward impulse from January.

The downward reversal from this resistance zone stopped the impulse waves C of the intermediate ABC correction (4) from January.

Given the strong daily downtrend, USDCHF currency pair can be expected to fall to the next support level 1.5765 (former support from July).

Eco Data 3/5/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Jan | 2.63B | 3.95B | 3.37B | |

| 07:45 | EUR | France Industrial Output M/M Jan | 0.30% | 0.40% | -0.70% | -0.50% |

| 08:00 | CHF | Unemployment Rate M/M Feb | 3.00% | 3.00% | 2.90% | |

| 09:30 | GBP | Construction PMI Feb | 44.5 | 47.9 | 46.4 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -0.10% | 0.20% | -0.50% | 0.10% |

| 12:30 | EUR | ECB Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (Feb 27) | 213K | 215K | 212K | 213K |

| 13:30 | USD | Import Price Index M/M Jan | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | Nonfarm Productivity Q4 P | 2.80% | 1.70% | 4.90% | |

| 13:30 | USD | Unit Labor Costs Q4 P | 2.80% | 2.20% | -1.90% | |

| 15:30 | USD | Natural Gas Storage (Feb 27) | -132B | -122B | -52B |

| 00:30 | AUD |

| Trade Balance (AUD) Jan | |

| Actual | 2.63B |

| Consensus | 3.95B |

| Previous | 3.37B |

| 07:45 | EUR |

| France Industrial Output M/M Jan | |

| Actual | 0.30% |

| Consensus | 0.40% |

| Previous | -0.70% |

| Revised | -0.50% |

| 08:00 | CHF |

| Unemployment Rate M/M Feb | |

| Actual | 3.00% |

| Consensus | 3.00% |

| Previous | 2.90% |

| 09:30 | GBP |

| Construction PMI Feb | |

| Actual | 44.5 |

| Consensus | 47.9 |

| Previous | 46.4 |

| 10:00 | EUR |

| Eurozone Retail Sales M/M Jan | |

| Actual | -0.10% |

| Consensus | 0.20% |

| Previous | -0.50% |

| Revised | 0.10% |

| 12:30 | EUR |

| ECB Meeting Accounts | |

| Actual | |

| Consensus | |

| Previous | |

| 13:30 | USD |

| Initial Jobless Claims (Feb 27) | |

| Actual | 213K |

| Consensus | 215K |

| Previous | 212K |

| Revised | 213K |

| 13:30 | USD |

| Import Price Index M/M Jan | |

| Actual | 0.20% |

| Consensus | 0.20% |

| Previous | 0.10% |

| 13:30 | USD |

| Nonfarm Productivity Q4 P | |

| Actual | 2.80% |

| Consensus | 1.70% |

| Previous | 4.90% |

| 13:30 | USD |

| Unit Labor Costs Q4 P | |

| Actual | 2.80% |

| Consensus | 2.20% |

| Previous | -1.90% |

| 15:30 | USD |

| Natural Gas Storage (Feb 27) | |

| Actual | -132B |

| Consensus | -122B |

| Previous | -52B |

DAX Eyes Bullish Recovery After 6% Slide and Retest of Psychological 24000 Handle

- DAX is attempting a recovery following a 6% drop.

- The global energy shock is fueling stagflation anxiety, notably causing a record 12% plummet in the South Korean KOSPI index.

- Market performance is mixed: Technology and defense stocks are providing upward momentum, while disappointing earnings from Adidas and Bayer are weighing on the index.

- The technical outlook is bullish, with buyers returning to test the 24000 psychological level, hinting at a potential move to the upside.

The DAX index is attempting a recovery today following two sessions of aggressive selling driven by escalating conflict in the Middle East.

Market sentiment saw a slight boost after President Trump suggested the US Navy might escort oil tankers through the Strait of Hormuz. This strategic chokepoint currently remains at a standstill, causing significant disruptions to global energy flows.

Despite the diplomatic overtures, oil prices have continued their ascent climbing 14.5% so far this week, while European natural gas prices have surged a staggering 60% over the last two days following the shutdown of Qatari LNG facilities and the closure of the Strait.The economic impact of these spikes is being felt acutely across energy-dependent regions.

While the DAX shed 6% over the last two sessions, the South Korean Kospi plummeted 12% overnight, reflecting a growing global anxiety over potential stagflation. This is the KOSPI benchmarks largest drop on record as South Korea is heavily reliant on Middle Eastern oil.

Over two days the tech-heavy index has lost more than 18% of its value while the currency KRW has slumped to a 17-year low.

The trajectory of the market now hinges on the duration of the conflict and whether energy prices ease. A prolonged standoff increases the risk of a sustained energy shock, which could cement the stagflationary pressures currently being priced in by traders.

According to sources, Qatar would need 2 weeks to restart gas liquefaction after a full shutdown. Once restarted, Qatar would need at least another 2 weeks to reach full capacity, which could lead to a temporary shock in prices if the conflict was to reach a swift conclusion.

Performance within the DAX remains a mixed bag of sector-specific reactions and corporate earnings.

Technology stocks are providing some upward momentum, with Infineon Technologies rising 3.7%, while defense stocks are seeing a modest recovery.

However, individual earnings reports are weighing on the index; Adidas shares dropped 7% on disappointing results (now down 5%), and Bayer fell 4.76% after providing a weak 2026 profit outlook that overshadowed a fourth-quarter earnings beat.

Source: LSEG

Trade Idea - Potential DAX Buy Opportunity

The DAX selloff saw the index drop below the psychological 24000 handle for the first time since December 2025.

The foray has proved short-lived thus far with buyers returning as the index tested the descending channel it broke out of in December 2025.

On the daily chart, the current daily candle is eyeing a close back above 24000 while at the same time printing an inside bar hammer candle.

This would hint at a move to the upside in the days ahead.

DAX Index Daily Chart, March 4, 2026

Source: TradingView

For those looking to get involved, we drop down to a one-hour chart.

Price is caught between the 20 and 50-day MAs with a retest of the 24000 handle presenting the best risk to reward opportunity for would be bulls.

If such a pullback does not materialize, traders may wait for a break of the 50-Day MA at 24210 and look for an opportunity to get involved with targets resting at the 100-day MA around 24700 and potentially 25000 as well.

DAX Index, One-Hour Chart, March 4, 2026

Source: TradingView

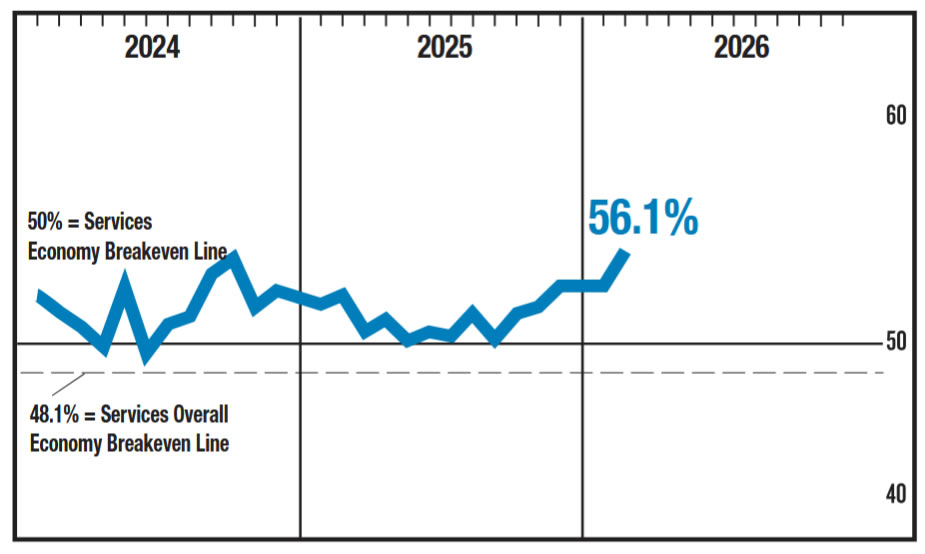

US: ISM Services Jump Up in February on Strong Demand

The ISM Services index rose sharply in February, climbing 2.3 points to 56.1. This marks the highest reading since mid-2022 and extends the expansion streak to 20 consecutive months. Growth also broadened across industries, with 14 reported expansions, up from 11 in January.

The supplier deliveries index remained in expansionary territory for a 15th straight month, edging down slightly to 53.9. Readings above 50 continue to signal slower deliveries, consistent with firmer demand conditions and ongoing capacity constraints in parts of the services economy.

New Orders rebounded forcefully in February, jumping 5.5 points to 58.6. This follows January’s pullback and suggests that demand momentum has recovered. Business activity also strengthened further, rising to 59.9, its highest level since late 2022.

New export orders staged a notable turnaround, surging back into expansionary territory to 57.2 after January’s sharp contraction. This rebound suggests that the earlier weakness tied to trade frictions and travel disruptions may have been temporary, though volatility remains elevated.

Price pressures moderated, but remain intense. The prices index fell 3.6 points to 63.0, its lowest level in nearly a year, but continues to signal widespread cost increases. Employment improved modestly, rising to 51.8, pointing to continued, albeit measured, job growth in the services sector.

Key Implications

February’s report points to a clear reacceleration in service sector demand, with new orders, business activity, and exports all strengthening meaningfully. Respondents highlighted firm underlying momentum, noting that “stronger consumer demands, interest rate stabilization, improved supply chain and stronger services activity” are driving new business, while others cited demand being pulled forward due to cost pressures from data center and infrastructure investment. The extent of strength in demand in this release likely weakens the case for imminent rate cuts from the Federal Reserve.

While price pressures eased modestly in February, they remain elevated and widespread, reinforcing concerns about sticky services inflation. One respondent noted that “costs remain high for technology, facilities, utilities, and contracted services" and that "labor expenses are also increasing due to competitive hiring” while another emphasized that supply chains have adapted but not normalized from a pricing perspective. Combined with slower supplier deliveries, these dynamics suggest inflation risks remain skewed to the upside, supporting a more cautious Federal Reserve stance on near term policy easing.

Sunset Market Commentary

Markets

Since the start of the conflict in the Middle East, markets this week already discounted a first bunch of risks related to energy supply, inflation and other sources of potential damage for the overall economy. A measured assessment simply remains illusive. However, for this kind of integrated risk-off move to reverse, markets need a clear perspective on an end game or an educated guess on how long this uncertainty might last. However this kind of visibility apparently won’t be available anytime soon. In the mean time, all kind of noise and rumors from “well-informed sources” are swirling, pushing markets back and forth. We pick out some. US president Trump ‘engaging’ the US to escort tankers in the Strait of Hormuz and/or providing financial insurance. The NYT reporting Iran indirectly reached out to the CIA to look for terms end the war (later denied by Iran). In the meantime war headlines continuously flashing on the screens, including on Turkey intercepting a projectile fired from Iran. Later, also US Secretary of Defense, Pete Hegseth repeated that they haven’t reached a mission accomplished situation. Of course, the conflict in the Middle East isn’t the only source of uncertainty investors have to cope with. At the start of US dealings, US Treasury Secretary Bessent indicated that the US might move to a global trade tariff of 15% still this week. Just to be followed by another headline suggesting the EU might be exempt from that US universal tariff, evidently again referring to people familiar with the matter. This chaotic news complex left investors at different markets drawing mixed conclusions. European equities (EuroStoxx 50), after losing abound 6% this week, are rebounding 1.5%. US indices also open with minor gains. Energy markets, a key source of uncertainty and inflation fears, show a mixed picture, with the Dutch gas reference contract easing from €60+/MWh levels to currently trade near €50/Mwh. At the same time, Brent oil holds well north of $80/b. After the recent bear steeping, mirroring the Fed’s and ECB’s inflation concerns, EMU and US interest rate markets apparently reached a first reflation point. German yields are changing between -1 bp (2-y) and +2 bps (30-y). (Much) too early to draw any conclusions. US yields are changing less than 2 bps across the curve. February ADP US private job growth printed at a solid 63k, but was understandably largely ignored. The US Services ISM might face a similar fate later today. On FX markets, the ‘USD safe haven run’ is taking a breather. DXY eases back below 99 (98.8). EUR/USD shows tentative signs of bottoming after touching an new YTD low yesterday (currently 1.1635). The yen also gained modestly (USD/JPY 157.3 from 157.75). Japanese Fin Min Katayama reiterated that the government might act to address excessive currency moves.

News & Views

Czech inflation fell by 0.1% M/M in February with the headline number slowing further below the 2% inflation target: from 1.6% Y/Y to 1.4% Y/Y. Details showed food and non-alcoholic beverage prices falling by 1.5% M/M with annual price growth in that category slowing from 1.3% to 0.4%. Energy prices were flat on the month to be 7.8% lower compared to last year. Underlying core inflation measures remain sticky above the CNB-target, ranging between 2.7% Y/Y and 3.1% Y/Y. Czech goods prices fell 0.5% in February (-0.7% Y/Y) but services inflation remains extremely sticky at 0.5% M/M and 4.5% Y/Y. In the global turmoil, the Czech market didn’t respond to the more benign numbers. Czech National Bank deputy governor Frait today said that recent global developments may limit room for a potential slight easing of Czech monetary policy if major central banks refrain from lowering their interest rates. EUR/CZK holds below first resistance at 24.40 today.

Swiss prices increased for the first time since June, rising by 0.6% M/M in February. On an annual level, price growth remained the same at 0.1%. The monthly increase is due to several factors including rising prices for housing rentals and for air transport. Hotels and other accommodation providers also recorded a price increase, as did international package holidays. Prices for food and vegetable juices fell. Swiss core inflation, excluding fresh and seasonal products, energy and fuel rose by 0.2% M/M and 0.4% Y/Y. Goods prices rose by 0.2% M/M (-1.4% Y/Y) while services prices increased by 0.9% M/M (1% Y/Y). It’s the final print before the March SNB meeting. With the policy stuck at the 0% border, focus went to the CHF-rate recently, prompting strong verbal interventions by the central bank. SNB vice-president Martin today repeated that willingness and readiness which is higher given the recent political events. The Swiss franc nevertheless holds below EUR/CHF 0.91 at historically strong levels.

US ISM services PMI jumps to 56.1, sector “heating up”

US service sector activity strengthened sharply in February, with the ISM Services PMI rising from 53.8 to 56.1, well above market expectations of 53.8, marking the highest level since July 2022. The data point to a broad-based acceleration in the services economy, which continues to be a key driver of overall US growth.

Underlying components showed strong momentum across demand and activity indicators. The Business Activity index climbed from 57.4 to 59.9, while New Orders surged from 53.1 to 58.6. Employment index also improved, rising from 50.3 to 51.8. Price pressures, however, eased slightly. Prices index declined from 66.6 to 63.0.

According to the ISM, the latest reading indicates the services sector is "heating up", with key activity and order components reaching their strongest levels since 2024. Historically, a Services PMI of 56.1 corresponds to roughly a 2.5% annualized increase in US real GDP.

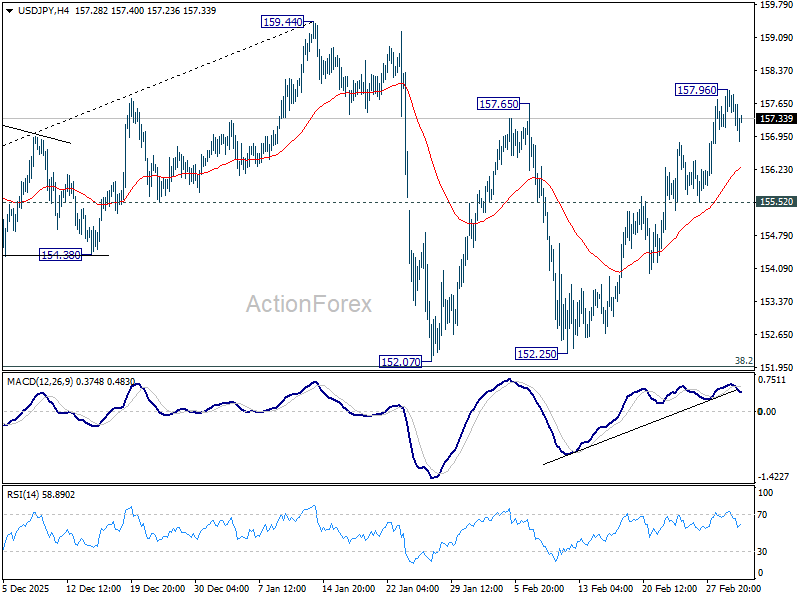

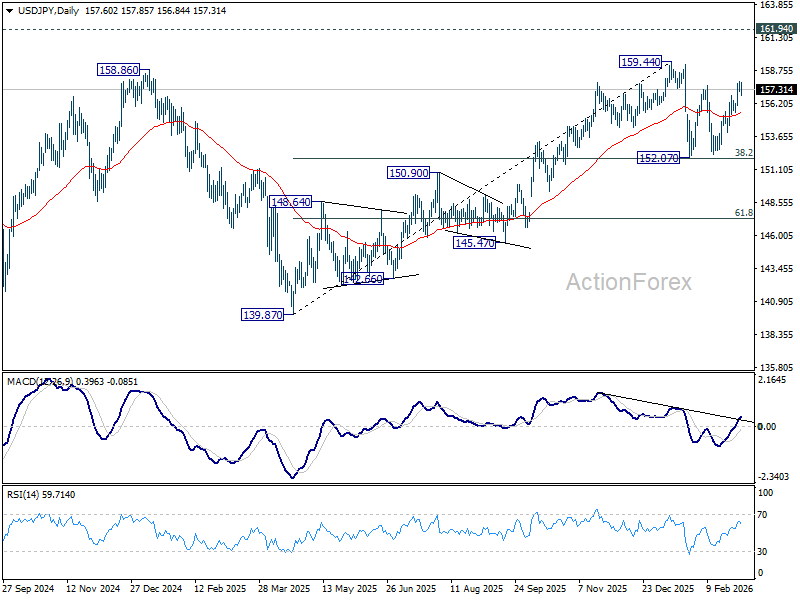

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.24; (P) 157.60; (R1) 158.06; More...

Intraday bias in USD/JPY is turned neutral with current recovery. On the upside, above 157.96 will extend the rebound from 152.25 to retest 159.44 high. On the downside, though, break of 155.52 will bring deeper fall back to 152.07/152.25 support zone. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

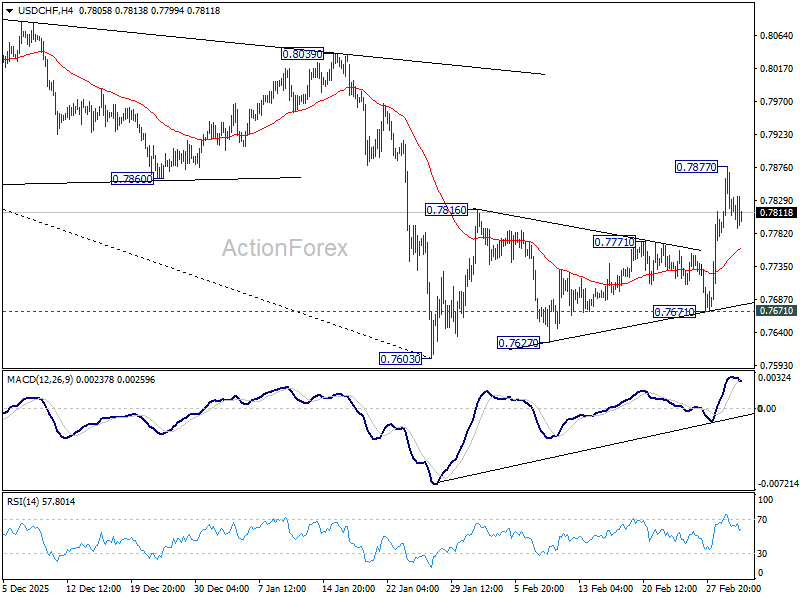

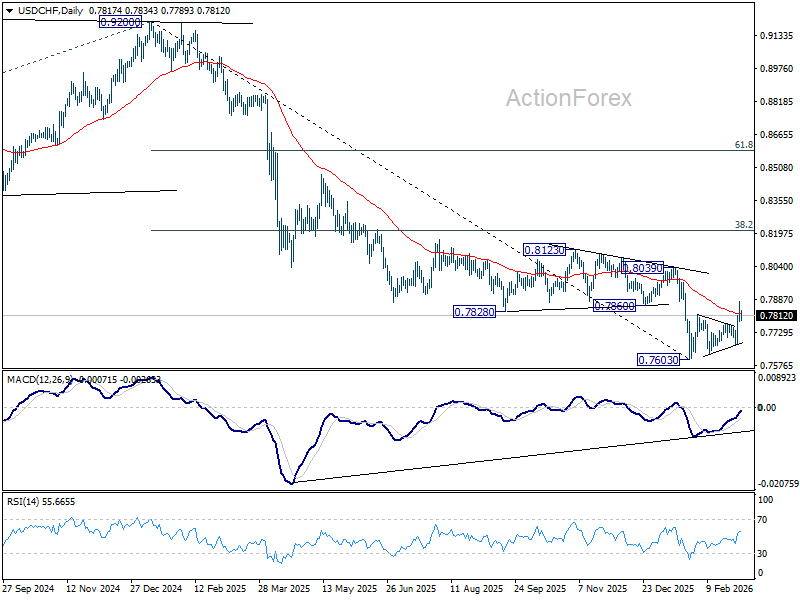

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7775; (P) 0.7827; (R1) 0.7870; More….

A temporary top is formed at 0.7877 with current retreat. Intraday bias in USD/CHF is turned neutral first. Further rise is expected as long as 0.7671 support holds. Rebound from 0.7603 is seen as correcting the whole fall from 0.9022. Above 0.76877 will target 0.8039 resistance next.

In the bigger picture, a medium term bottom could be in place at 0.7603 on bullish convergence condition in D MACD, Firm break of 0.8039 resistance will argue that it's at least correcting the down trend from 0.9002. Stronger rebound would then be seen to 38.2% retracement of 0.9200 to 0.7603 at 0.8213.

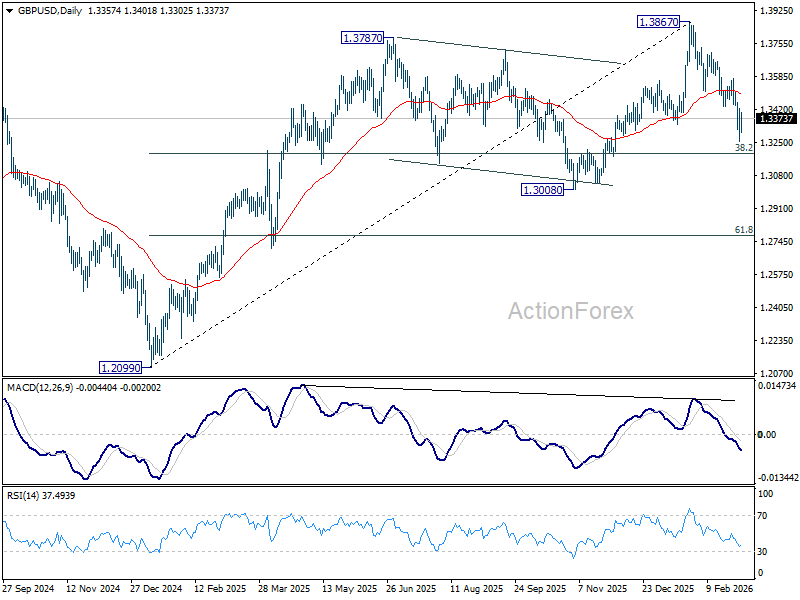

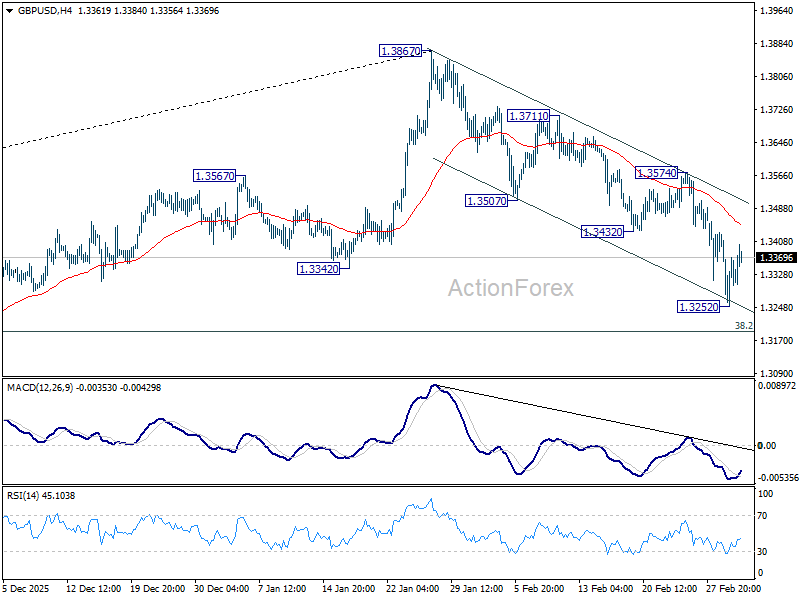

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3266; (P) 1.3345; (R1) 1.3438; More...

A temporary low is in place at 1.3252 with current recovery. Intraday bias in GBP/USD is turned neutral first. Fall from 1.3867 should at least be correcting the rise from 1.2009. Below 1.3252 will target 38.2% retracement of 1.2099 to 1.3867 at 1.3192. Sustained break there will pave the way to 1.3008 support. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.