Sample Category Title

Equities, Cryptos and Metals Under Pressure as Risk-Off Builds, Dollar Finds Uneven Support

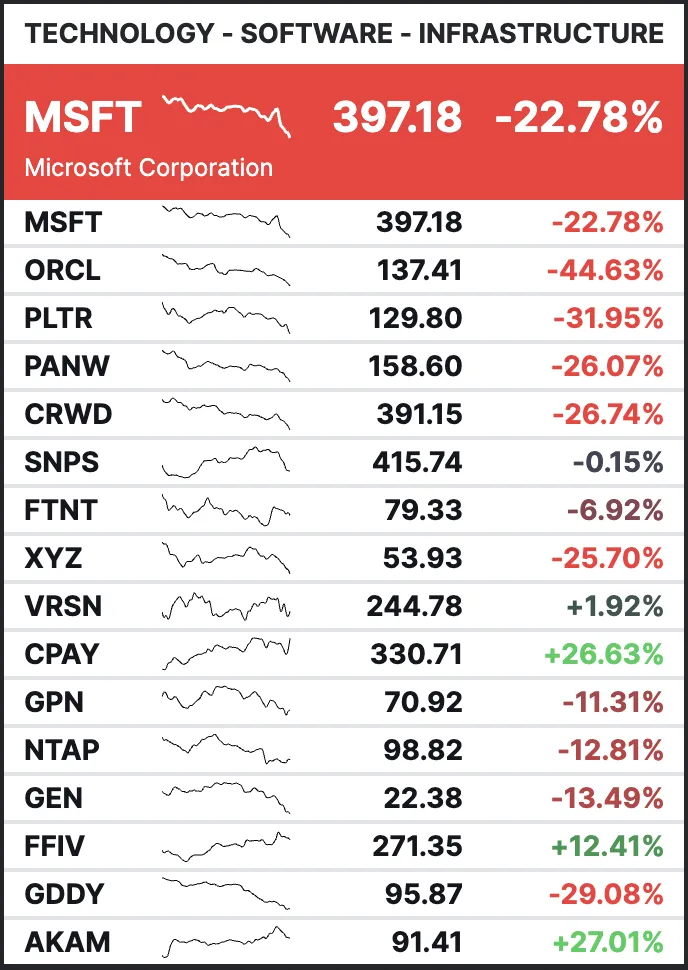

Risk aversion intensified overnight, with US equities posting broad-based losses. DOW and S&P 500 both closed more than 1.2% lower, while NASDAQ underperformed again, sliding nearly 1.6%. Notably, S&P 500’s break below near-term support zone around 6800 is technically significant. It suggests the tech-led selloff may be spilling over into more traditional sectors, raising the risk of broader equity de-risking.

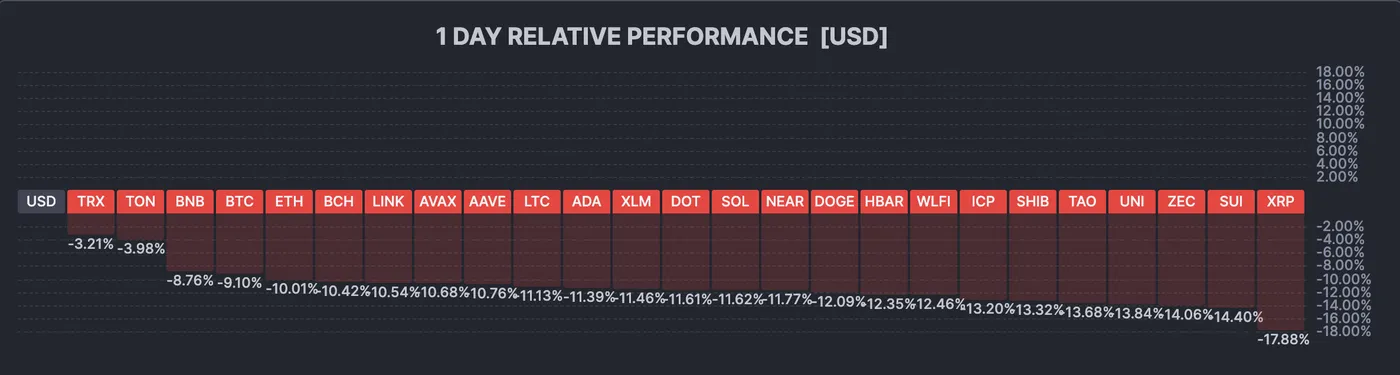

Risk-off dynamics were also evident in cryptocurrencies. Bitcoin briefly plunged through 60k level before stabilizing, marking a 50% loss from its October peak near 126k and reinforcing the sense of fragile sentiment in speculative assets. Precious metals told a similar story. Silver breached the 64 level before recovering modestly, a sharp contrast to last week’s record near 121. Gold proved more resilient but continued to struggle below 5,000 and remained well under its recent peak around 5,600.

In FX markets, Dollar is the strongest performer for the week so far, though gains against Euro remain unconvincing. The greenback is being pulled by opposing forces, with risk aversion offering support while shifting rate expectations cap upside. Fed funds futures are now pricing more than 20% chance of a March rate cut. While a hold remains the base case, a deeper and more persistent equity selloff could prompt some Fed officials to reassess the balance of risks.

Australian Dollar continues to defy the risk-off tone and ranks as the second-strongest currency this week. Support comes from the RBA’s hawkish rate hike this week, with some economists already flagging the possibility of another increase as early as May to contain resurging inflation pressures.

At the other end of the spectrum, Yen remains the weakest major, failing to benefit from risk aversion as traders position for a strong election win by Prime Minister Sanae Takaichi and the LDP this weekend. Sterling follows closely after the BoE’s dovish hold revived March cut expectations.

In Asia, at the time of writing, Nikkie is up 0.24%. Hong Kong HSI is down -1.30%. China Shanghai SSE is up 0.19%. Singapore Strait Times is down -0.90%. Japan 10-year JGB yield is up 0.002 at 2.231. Overnight, DOW fell -1.20%. S&P 500 fell -1.23%. NASDAQ fell -1.59%. 10-year yield fell -0.065 to 4.210.

BoJ’s Masu backs further hikes, flags weak Yen risks but urges caution

BoJ board member Kazuyuki Masu said further interest rate hikes will be needed to complete Japan’s monetary policy normalization. He noted that underlying inflation remains below 2% but is “drawing very close” to that level as firms and households gradually shed entrenched deflationary behavior.

He cautioned, however, that the Yen’s recent weakness could amplify price pressures by lifting inflation expectations, with potential spillovers into underlying inflation. Also, He highlighted processed food prices as a key area to watch, noting that surging rice prices may have made consumers more receptive to broader food price increases.

At the same time, Masu stressed the need for caution. "it is critical to ensure excessive rate hikes do not disrupt the virtuous cycle of a moderate rise in prices and wages that has finally begun to gain momentum in Japan," he said.

RBA's Bullock defends rate hike, cites excess demand and capacity strain

RBA Governor Michele Bullock told the House of Representatives economics committee today that the decision to raise the cash rate by 25bps to 3.85% was driven by a clear resurgence in inflation pressures during the second half of 2025.

Bullock said the Board concluded that demand in the economy had proven stronger than expected, running ahead of the supply side’s capacity to respond. As a result, inflation outcomes indicated a larger degree of "excess demand" than previously assumed.

She emphasized that this imbalance means demand growth must be dampened unless productivity and supply expand at a faster pace. With the economy now judged to be "more capacity constrained", leaving policy unchanged would risk inflation remaining elevated for longer. On that basis, the RBA determined that tighter monetary policy was required.

BoC’s Macklem sees modest growth as economy adjusts to structural shifts

In a speech overnight, BoC Governor Tiff Macklem said Canada is undergoing profound structural change, driven by the end of open trade with the US, rapid advances in artificial intelligence, and slower population growth due to aging and lower immigration. These forces, he said, are reshaping the economy in ways that will have lasting implications.

Macklem cautioned that when structural change accelerates, disruption is inevitable. While such transitions can strengthen the economy over time, they also heighten uncertainty for businesses and households, as the full effects are difficult to predict and unevenly distributed.

Against that backdrop, the BoC expects modest economic growth over the next couple of years, with inflation staying close to the 2% target. Part of the softness reflects temporary weakness from the trade conflict, but the outlook also incorporates the adjustment costs associated with deeper structural shifts.

Monetary policy, Macklem emphasized, "will not be at the centre" of managing this transition. Instead, the BoC will play a supporting role by anchoring inflation and helping the economy navigate a period of elevated uncertainty, while remaining alert to risks and prepared to adjust policy if the outlook changes.

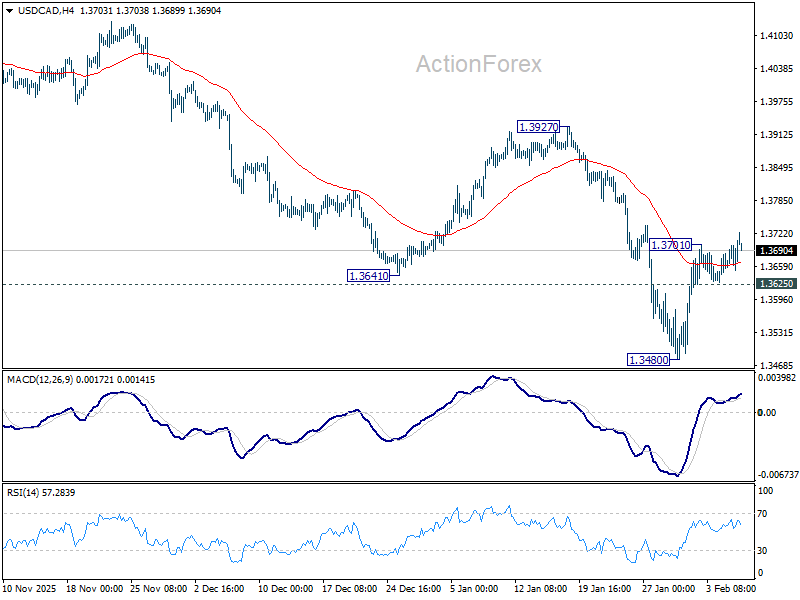

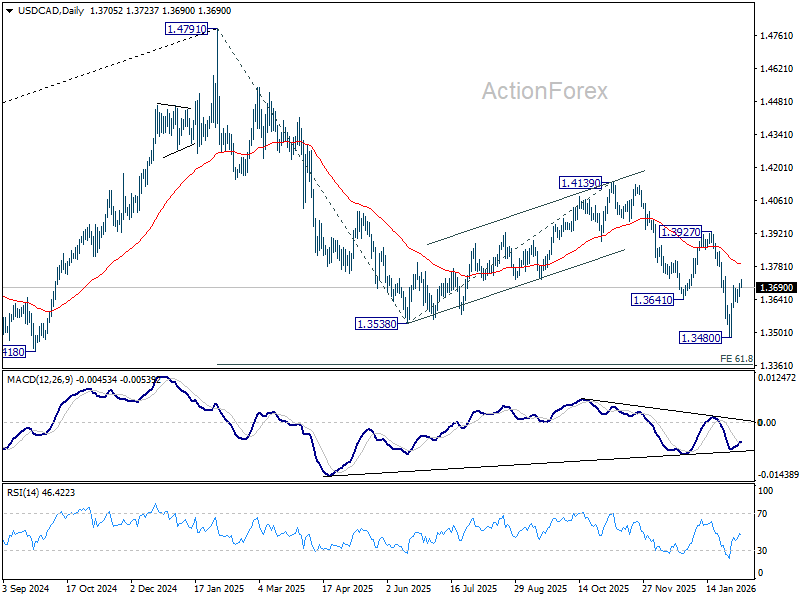

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3673; (P) 1.3693; (R1) 1.3733; More...

Intraday bias in USD/CAD is back on the upside as rebound from 1.3480 is resuming for 55 D EMA (now at 1.3788). Strong resistance could be seen there to complete the corrective bounce. On the downside, below 1.3625 support will bring retest of 1.3480 low. Firm break there will resume larger fall to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, sustained trading above 55 D EMA will raise the chance of near term bullish reversal, and target 1.3927 resistance for confirmation.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

RBA’s Bullock defends rate hike, cites excess demand and capacity strain

RBA Governor Michele Bullock told the House of Representatives economics committee today that the decision to raise the cash rate by 25bps to 3.85% was driven by a clear resurgence in inflation pressures during the second half of 2025.

Bullock said the Board concluded that demand in the economy had proven stronger than expected, running ahead of the supply side’s capacity to respond. As a result, inflation outcomes indicated a larger degree of "excess demand" than previously assumed.

She emphasized that this imbalance means demand growth must be dampened unless productivity and supply expand at a faster pace. With the economy now judged to be "more capacity constrained", leaving policy unchanged would risk inflation remaining elevated for longer. On that basis, the RBA determined that tighter monetary policy was required.

BoJ’s Masu backs further hikes, flags weak Yen risks but urges caution

BoJ board member Kazuyuki Masu said further interest rate hikes will be needed to complete Japan’s monetary policy normalization. He noted that underlying inflation remains below 2% but is “drawing very close” to that level as firms and households gradually shed entrenched deflationary behavior.

He cautioned, however, that the Yen’s recent weakness could amplify price pressures by lifting inflation expectations, with potential spillovers into underlying inflation. Also, He highlighted processed food prices as a key area to watch, noting that surging rice prices may have made consumers more receptive to broader food price increases.

At the same time, Masu stressed the need for caution. "it is critical to ensure excessive rate hikes do not disrupt the virtuous cycle of a moderate rise in prices and wages that has finally begun to gain momentum in Japan," he said.

BoC’s Macklem sees modest growth as economy adjusts to structural shifts

In a speech overnight, BoC Governor Tiff Macklem said Canada is undergoing profound structural change, driven by the end of open trade with the US, rapid advances in artificial intelligence, and slower population growth due to aging and lower immigration. These forces, he said, are reshaping the economy in ways that will have lasting implications.

Macklem cautioned that when structural change accelerates, disruption is inevitable. While such transitions can strengthen the economy over time, they also heighten uncertainty for businesses and households, as the full effects are difficult to predict and unevenly distributed.

Against that backdrop, the BoC expects modest economic growth over the next couple of years, with inflation staying close to the 2% target. Part of the softness reflects temporary weakness from the trade conflict, but the outlook also incorporates the adjustment costs associated with deeper structural shifts.

Monetary policy, Macklem emphasized, "will not be at the centre" of managing this transition. Instead, the BoC will play a supporting role by anchoring inflation and helping the economy navigate a period of elevated uncertainty, while remaining alert to risks and prepared to adjust policy if the outlook changes.

Play in May, Don’t Go Away

The higher outlook for the cash rate is quite the turnaround. We expect another rate hike in May. Other pathways are possible as risk scenarios.

- With inflation now higher (and overall demand growth stronger) than previously expected, the RBA raised the cash rate in February. The question then becomes, how much more is coming and when? We believe that another cash rate increase will occur, in May.

- There are pathways that result in the next rate hike occurring at the March meeting, but this is less likely. The RBA believes (as we do) that much of the recent increase in inflation is temporary, which reduces the urgency of follow-up hikes.

- If things turn out as we expect, the RBA will be able to point to some turnaround in inflation, as temporary factors wash out by the time the August meeting comes around. This will enable the Board to take a ‘wait-and-see’ approach with policy already restrictive. There are scenarios where it will want to raise rates even further then, but they are not our baseline expectation.

The shift in the interest rate outlook in Australia since six months ago is quite the turnaround. Inflation has kicked up in ways that were not apparent or expected in mid 2025. One reason was that, while a slowdown in public demand growth and pick-up in private demand growth were both expected – as can often be an issue – the net of the two has been more positive than anticipated. Prices tend to respond sooner than volumes when demand surprises. Above-average inflation in many administered prices didn’t help. The RBA has responded to this, first by preparing the ground for a rate hike and ruling out the previously expected cuts, and then by delivering that rate increase at its February meeting. The question then becomes, how much more should we expect the cash rate to rise, and when?

We currently expect one more rate rise, in May. Other paths are possible if the data flow turns out differently than our expectations.

The main plank supporting this view is that the RBA Monetary Policy Board appears to be dissatisfied with the inflation trajectory implied by its staff forecasts. It therefore thinks it needs to do more than the roughly one extra hike that was priced in at the time those forecasts were finalised. It is unlikely that the data flow will turn softer soon enough to prevent it from moving in May. Even if the labour market does unravel unexpectedly, that will not happen soon enough to affect a May decision. Similarly, we think there is enough near-term momentum to inflation that the narrative that “it is showing some persistence” cannot be walked back by May. Our expectation for the March quarter inflation print is only marginally lower than what we believe the RBA’s to be. Near-term inflation outcomes would have to surprise noticeably to the downside to stay the RBA’s hand at its May meeting.

Recall that RBA’s forecasts are based on the technical assumption that the cash rate follows market pricing at the time the forecasts are finalised. As the Governor repeatedly emphasises in post-meeting media conferences, this is not a forecast or promise from the RBA. Rather, it is necessary to ensure that the forecasts are coherent across financial market variables. The market path for the cash rate is the one consistent with the exchange rate being where it is, another technical assumption in the RBA’s forecasting framework.

You can, however, glean something about what the RBA thinks regarding the rates outlook from the inflation forecast that the market path delivers. If it is uncomfortably high for too long, this is a sign that the Board thinks it might need to do more than was priced in. Again, an alternative path is not baked in, but it does give a guide to the balance of probabilities. And if the tone of the post-meeting press conference is any guide, at least some Board members think they will have to do even more than the 60bp increase over 2026 that was priced in at the time.

Could the rate increase come as soon as March, as a back-to-back hike? We cannot rule this out, but it is not our base-case expectation. While the staff forecasts are consistent with the RBA believing it might have to do more, the divergence from a more desirable inflation path was not large. And it is clear both from the post-meeting communication and today’s testimony before the House of Representatives that the RBA thinks that “[m]uch of the increase in inflation is judged to be temporary” and only some of it is persistent. It is plausible that there are members of the Board and/or the staff that see the need for tightening as more urgent, and therefore possible that some votes for a hike will be recorded in March. Given the RBA’s published assessment of the nature of the increase in inflation, though, we do not think the majority will vote for a March hike.

Beyond May, we think it is possible that the RBA will want to keep raising rates, but that this scenario is less likely than an extended period on hold in a restrictive stance, one that is not far off the earlier peak. Our assessment of the outlook is that a downward trajectory in underlying inflation will emerge and will start to be evident in the Q2 data. Part of this will be the start of the unwinding of the temporary component of the recent increase. Those who are more familiar with the ‘long and variable lags’ of monetary policy will note that this would be a very quick turnaround for monetary policy to have done the deed. Watch also for the labour market slowing more and sooner than the RBA is forecasting as a signal supporting on-hold policy beyond May.

A factor that received less attention in the RBA’s post-meeting communication and testimony is the role of the exchange rate in shaping the inflation outlook. Some of the recent pick-up in inflation came from consumer goods. Most of these are imported, and the weakness earlier in 2025 in the AUD, especially relative to the USD, would have played a role in this. (Recall that China’s currency is managed closely to the USD, so the AUD/USD rate effectively comprises around 40% of Australia’s trade-weighted index.) With the AUD now noticeably higher since the previous forecast round, the contribution to overall inflation from this source will go into reverse. Our own models as well as a commercially available whole-economy model suggest that pass-through of lower prices of imported goods through to retail prices could slow overall inflation noticeably sooner than the RBA’s forecasts imply. Our own forecasts make some allowance for this, but the model-implied effect implies that this could be stronger than we assume. (There are, of course, also upside risks to inflation, notably from home-building costs.)

Bottom line: we expect another hike in the cash rate in May, and while the risks are that they move sooner or do more, the likely data flow supports a one-hike-in-May scenario.

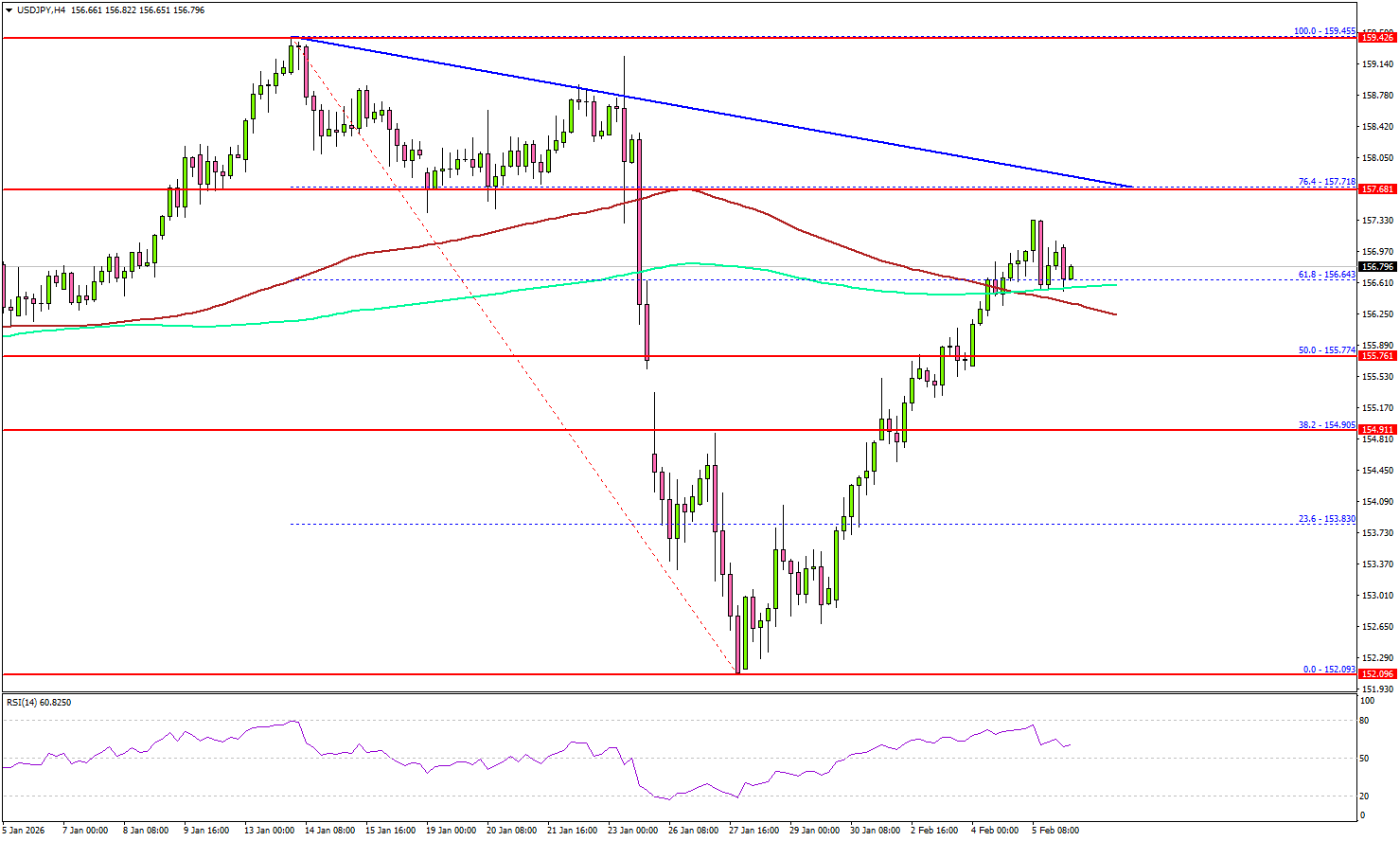

USD/JPY Presses Higher, But A Major Barrier Stands In The Way

Key Highlights

- USD/JPY recovered sharply and rallied above 155.50.

- A major bearish trend line is forming with resistance at 157.80 on the 4-hour chart.

- GBP/USD declined further and traded below 1.3620.

- Bitcoin extended losses and dived below $65,000.

USD/JPY Technical Analysis

The US Dollar started a steady increase above 154.20 against the Japanese Yen. USD/JPY cleared the 155.00 resistance to enter a positive zone.

Looking at the 4-hour chart, the pair broke the 50% Fib retracement level of the downward move from the 159.45 swing high to the 152.09 low. The pair even surpassed the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the upside, the pair could face hurdles near 157.70 or the 76.4% Fib retracement level of the downward move from the 159.45 swing high to the 152.09 low.

There is also a major bearish trend line forming with resistance at 157.80. The next stop for the bulls might be 158.00. A close above 158.00 could open the doors for more gains. In the stated case, the bulls could aim for a move toward 159.50.

Immediate support could be 156.50. The first major area for the bulls might be near 156.20. The main support sits at 154.90, below which the pair might gain bearish momentum. In the stated case, it could even revisit 152.50.

Looking at GBP/USD, the pair corrected some gains and traded below the 1.3620 support. The next key support might be 1.3500.

Upcoming Key Economic Events:

- Michigan Consumer Sentiment Index for Feb 2026 (Prelim) – Forecast 55.0, versus 56.4 previous.

- Canada’s Net Change In Employment for Jan 2026 – Forecast 7K, versus 8.2K previous.

- Canada’s Unemployment Rate for Jan 2026 - Forecast 6.8%, versus 6.8% previous.

Cliff Notes: Facing Uncertainty

Key insights from the week that was.

The RBA Monetary Policy Board decided to raise the cash rate by 25bps to 3.85% this week, in line with economist and market expectations. Justifying the decision, the Board stated that inflation had “picked up materially” against a backdrop of “greater momentum in demand”. Capacity pressures were seen as “unlikely to explain the majority of the recent increase [in inflation]”, with “sector-specific demand and price pressures” which “may not persist” also evident. Together, these dynamics are contributing to elevated near-term inflation and a slower projected return to target, a clear source of discomfort for the Board.

In a video update midweek, Chief Economist Luci Ellis discussed the RBA’s forecasts and the implications. A technical assumption of at least one more rate hike in 2026 together with a trimmed mean inflation forecast slightly above the mid-point at horizon’s end (2.6%yr in Jun-28) suggests another rate hike is most probable. We have consequently incorporated a follow-up 25bp hike in May into our baseline view. Note though, this adjustment reinforces our view that rate cuts are likely to prove necessary down the track, most likely in November 2027 and February 2028, leaving the cash rate at 3.60%.

Higher actual and expected interest rates have softened house price growth at the margin. Stripping out the effect of ‘thin’ trading over summer, Cotality reports that national house price gains on a seasonally adjusted basis have moderated from 1.1% in Oct-Nov to 0.9% over Dec-Jan. Choppy monthly reads for dwelling approvals have meanwhile made assessing the strength of ‘front-end’ housing supply a challenge. 2025 was a more positive year for new supply, but it was still well below the Government’s Housing Accord target. And headwinds are now stronger.

Before moving offshore, a final note on trade. The latest read on goods trade saw the surplus edge slightly higher to $3.4bn in December, supported by a modest gain in export earnings and a small decline in the import bill. The underlying dynamics point to a continued trend narrowing in the surplus, as global demand for commodity exports remains subdued and domestic recovery buoys consumer imports.

Offshore, there was plenty of central bank communications to parse.

The Bank of England kept rates steady at 3.75% in a 5-4 vote. Forward guidance points to a slower pace of easing in 2026 than 2025, with future decisions characterised as “a closer call”. According to the minutes, there are presently three camps in the MPC. The most hawkish advocated to keep rates on hold, concerned inflation may hold above target. The middle camp, which contained Governor Bailey and Catherine Mann, noted that there is room for additional easing, but wanted further evidence that weaker activity will feed through to inflation. While the four doves that voted for a cut are already confident inflation will normalise.

The updated BoE forecasts certainly make the case for additional easing in 2026. Most notably, the inflation profile has been revised down significantly, now foreseeing a return to 2.0%yr by Q3 this year and a pace at year end 0.5ppts lower than expected three months ago. GDP growth is forecast to be 0.3ppt lower in Q4 2026 at 1.1%yr, and the unemployment rate 0.3ppts higher at 5.3%. We continue to anticipate a further Bank Rate cut in March followed by a final cut in Q2.

The European Central Bank meanwhile decided to hold rates steady in February. No new forecasts were released, and the central bank’s forward guidance was largely unchanged, with the Governing Council set to “follow a data-dependant and meeting-by-meeting approach”. In the press conference, President Lagarde highlighted external risks stemming from “a volatile global policy environment” and weaker sentiment in financial markets. On inflation, she stated that underlying inflationary pressures remain consistent with the 2% target, but also acknowledged that euro appreciation could push inflation below the desired level.

The stable outlook for inflation allowed President Lagarde to reiterate that the ECB is in a “good place”, signalling that she, and likely most Governing Council members, currently see no reason to alter the existing policy stance. We hold a similar view, expecting policy to be unchanged through 2026, though we are mindful of the potential disinflationary impact of euro appreciation.

Finally to the US, the ISM PMIs for January pointed to improved conditions in the manufacturing sector and little change for services. The manufacturing PMI rose 4.7pts overall as the new orders component gained 9.7pts and employment was up 3.3pts. Note though that employment remains 4.8pts below the pre-COVID average, consistent with other labour market indicators which point to limited marginal labour demand. For services, conditions were unchanged overall despite a large decline in inventories and export orders. Employment also fell 1.4pts to be 6.3pts below its pre-COVID average.

Upstream prices pressures remain evident across the economy, the manufacturing prices component up 0.5pts in the month to be 3.2pts higher than its historic average and the services measure up 1.5pts, 10.4pts above the pre-COVID average. Tariffs, energy costs and capacity constraints across the economy are likely fuelling these pressures.

Bitcoin Tumbles to $63,000 Amid Global Tech Selloff – BTC/USD Outlook

Looking at the crypto market today, the outlook is grim. Bitcoin has lost nearly 50% of its value since that peak, total market capitalization has fallen back to Trump re-election levels, and major altcoins such as Solana have corrected by as much as 70% or more.

What goes up — especially when it goes up too fast — must eventually come down.

Current flows are eerily reminiscent of the November 2021 tech and crypto meltdown, making that period worth revisiting.

Tech Sector 3-month performance – Courtesy of Finviz. February 5, 2026

At the time, Bitcoin had surged from its $3,800 COVID lows to $69,000 in roughly a year and a half, topping in November 2021 before collapsing nearly 80% to around $15,800 — a move that felt like the end of the world.

Total crypto market cap fell from just over $3 trillion to roughly $736 billion during that drawdown.

That decline was accompanied by a series of brutal headlines, including the Terra/Luna collapse and the eventual FTX blow-up in 2022.

Total Crypto Market Cap, February 2026 – Source: TradingView

Since then, Bitcoin staged an impressive sixfold rally from its November 2022 lows.

Aside from the brief Liberation Day sweep toward $75,000, the market barely retraced — and it is now paying the hefty price.

A 70% decline from the $126,400 record high would bring Bitcoin back toward the $30,000 area – That may sound extreme from today’s levels, but in crypto, nothing is impossible. Extreme volatility is part of the asset class’s DNA, on both the upside and the downside.

Before diving into a deeper analysis of the father of cryptocurrencies, it’s worth remembering that these drawdowns are exactly what markets do best.

They create stories, hope, and spectacular trends — but also nightmares, grief, and collapses. Bubbles are nothing new, and while markets evolve from them, they rarely learn. They simply reflect humanity’s purest forms of exuberance and despair.

The key risk now is whether these declines spill over into other asset classes and trigger cascading effects. But it isn’t only about fear. Historically, assets that lose more than 50% of their value can become attractive accumulation candidates — often more so than buying at full price. Still, catching falling knives is dangerous, and many fortunes have been lost trying.

Plan carefully, scale in progressively, and always spread your risk.

Let's explore some key levels of interest from Weekly to Daily charts and trading levels for Bitcoin (BTC) to spot where the current drop could hold (and potentially reverse, even if the mood doesn't corroborate much with this idea).

Bloodshed in the Crypto Market

Daily overview of the Crypto Market, February 5, 2026 – Source: Finviz

The daily drops are staggering.

The selloffs have been accelerating in the past few minutes with Ethereum reaching $1,860 and XRP at $1.18 which could prompt short-term buyings of dip.

Still, be careful with falling knives!

Bitcoin multi-timeframe technical analysis

Weekly Chart

Bitcoin Weekly Chart, February 5, 2026 – Source: TradingView

With the fast-paced acceleration, Bitcoin is now dropping back to the $63,000 Major Support (which extends to $60,000), key level which served as the basis of the 2024 breakout.

The weekly candle is an ugly one.

If this extends further, it will be interesting to see how traders react to the 200-Week Moving average at $58,000. Let's take a closer look to see where we stand and spot for potential troughs.

Daily Chart and Technical Levels

Bitcoin Daily Chart, February 5, 2026 – Source: TradingView

With the daily run, it would be surprising to see the action continue much further in a straight line – However, the fragile market conditions wouldn't warrant an immediate bottom.

Keep a close look to immediate reactions between $60,000 to $63,000 as the session closes back to pre-breakout levels.

A striking Measured Move pattern could also be developing and seems like a decent target for such a drop.

Taking the October to November 2025 drop gives the base, which extends to $52,000, an interesting level for dip-buying if we get there.

Of course, investors will want to be extremely careful with themes around Markets as we keep correcting.

What starts with liquidations could easily turn into a larger disaster and contribute to even more extreme moves around Markets.

Levels of interest for BTC trading:

Support Levels:

- $60,000 to $63,000 Main 2024 support (immediate test)

- $52,000 to $58,000 Next support and 200-Week MA

- $2023 Breakout base $25,000 to $34,000

Resistance Levels:

- $75,000 Key long-term Pivot

- $80,000 to $83,000 mini-resistance

- $90,000 to $95,000 Pivotal Resistance

- Current all-time high $126,250

Safe Trades!

Bitcoin Wave Analysis

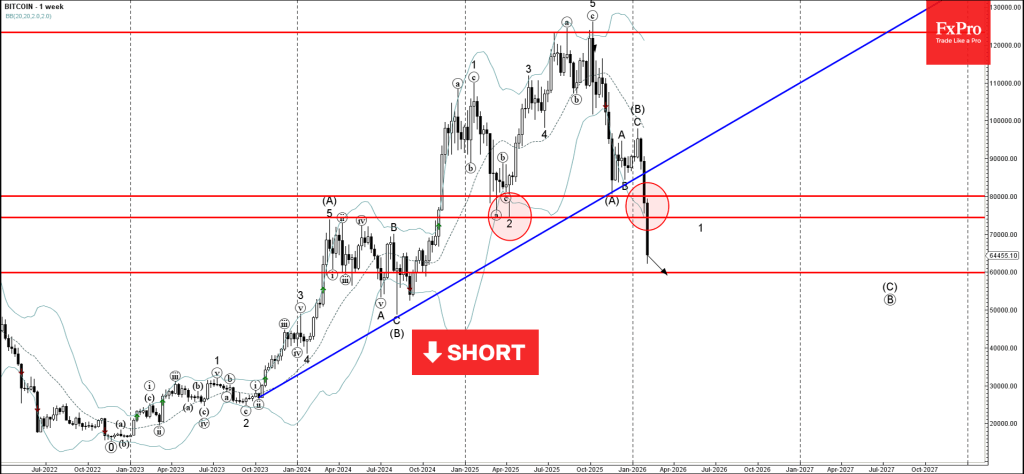

Bitcoin: ⬇️ Sell

- Bitcoin broke round support level 80000.00

- Likely to fall to support level 60000.00

Bitcoin cryptocurrency falling sharply after the price broke the round support level 80000.00, the support level 74342.00 (yearly low from 2025) and the weekly support trendline from 2023.

Each of these breakouts accelerated the active impulse waves 1 and (C).

Given the strongly bearish sentiment seen across cryptocurrency markets today, Bitcoin cryptocurrency can be expected to fall toward the next support level 60000.00.

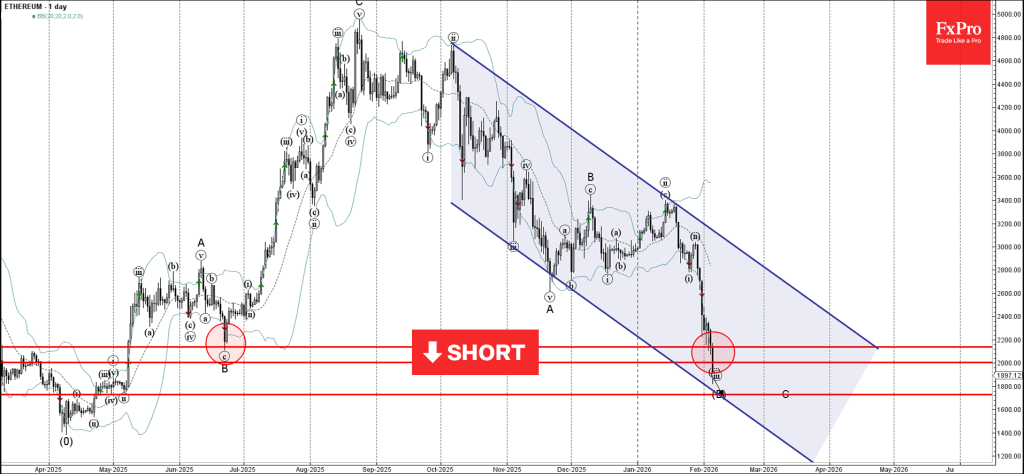

Ethereum Wave Analysis

Ethereum: ⬇️ Sell

- Ethereum broke round support level 2000.00

- Likely to fall to support level 1725.00

Ethereum cryptocurrency recently broke the support zone between the support level 2120.00 (former multi-month low from June) and the round support level 2000.00.

The breakout of this support zone accelerated the active impulse wave C of the multi-month downward ABC correction (B) from August.

Ethereum can be expected to fall toward the next support level 1725.00 (former low from May and the target for the completion of the active impulse wave C).