Sample Category Title

Eco Data 2/6/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Dec | -2.60% | -0.30% | 2.90% | |

| 05:00 | JPY | Leading Economic Index Dec P | 110.2 | 109.8 | 109.9 | |

| 07:00 | EUR | Germany Industrial Production M/M Dec | -1.90% | -0.30% | 0.80% | 0.20% |

| 07:00 | EUR | Germany Trade Balance (EUR)Dec | 17.1B | 14.5B | 13.1B | |

| 08:00 | CHF | Unemployment Rate M/M Jan | 2.90% | 3.00% | 3.00% | |

| 08:00 | CHF | Foreign Currency Reserves Jan | 712B | 725B | ||

| 13:30 | CAD | Net Change in Employment Jan | -24.8K | 7.3K | 8.2K | |

| 13:30 | CAD | Unemployment Rate Jan | 6.50% | 6.80% | 6.80% | |

| 15:00 | CAD | Ivey PMI Jan | 50.9 | 49.7 | 51.9 | |

| 15:00 | USD | UoM Consumer Sentiment Feb P | 57.3 | 55.8 | 56.4 | |

| 15:00 | USD | UoM 1-Yr Inflation Expectations Feb P | 3.50% | 4% |

| 23:30 | JPY |

| Overall Household Spending Y/Y Dec | |

| Actual | -2.60% |

| Consensus | -0.30% |

| Previous | 2.90% |

| 05:00 | JPY |

| Leading Economic Index Dec P | |

| Actual | 110.2 |

| Consensus | 109.8 |

| Previous | 109.9 |

| 07:00 | EUR |

| Germany Industrial Production M/M Dec | |

| Actual | -1.90% |

| Consensus | -0.30% |

| Previous | 0.80% |

| Revised | 0.20% |

| 07:00 | EUR |

| Germany Trade Balance (EUR)Dec | |

| Actual | 17.1B |

| Consensus | 14.5B |

| Previous | 13.1B |

| 08:00 | CHF |

| Unemployment Rate M/M Jan | |

| Actual | 2.90% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 08:00 | CHF |

| Foreign Currency Reserves Jan | |

| Actual | 712B |

| Consensus | |

| Previous | 725B |

| 13:30 | CAD |

| Net Change in Employment Jan | |

| Actual | -24.8K |

| Consensus | 7.3K |

| Previous | 8.2K |

| 13:30 | CAD |

| Unemployment Rate Jan | |

| Actual | 6.50% |

| Consensus | 6.80% |

| Previous | 6.80% |

| 15:00 | CAD |

| Ivey PMI Jan | |

| Actual | 50.9 |

| Consensus | 49.7 |

| Previous | 51.9 |

| 15:00 | USD |

| UoM Consumer Sentiment Feb P | |

| Actual | 57.3 |

| Consensus | 55.8 |

| Previous | 56.4 |

| 15:00 | USD |

| UoM 1-Yr Inflation Expectations Feb P | |

| Actual | 3.50% |

| Consensus | |

| Previous | 4% |

ECB Review: Accentuate the Positive

- ECB decided to leave its key policy rates unchanged with the deposit facility rate at 2.00% as widely expected by markets and consensus.

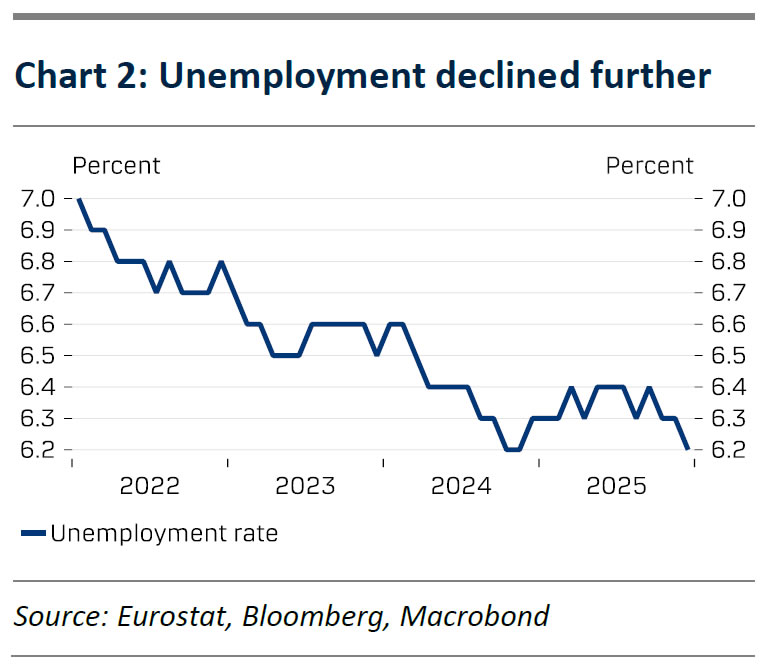

- Lagarde accentuated the positive factors of the economy such as low unemployment while downplaying the role of the inflation undershooting and strengthened euro.

- We maintain our call that the ECB will leave the deposit rate unchanged at 2.00% throughout both 2026 and 2027.

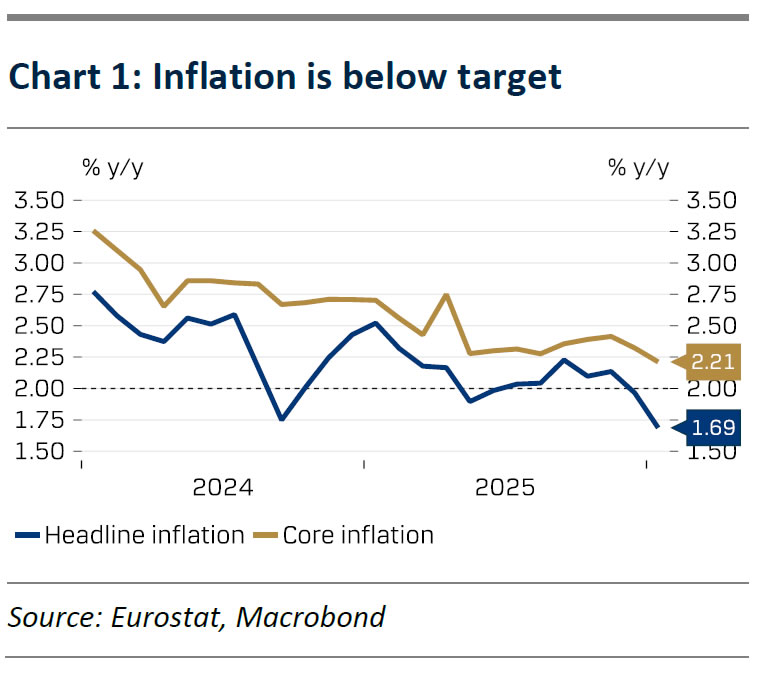

The ECB left the deposit rate unchanged at 2.00% as expected by both markets and analysts. The press release was short with the guidance paragraph similar to December. Interestingly, it was the positive aspects of the economy like low unemployment, solid private balance sheets and increased public spending that was accentuated despite inflation declining to 1.7% in January.

During the press conference Lagarde further emphasised the positive aspects, with limited reference to negative factors like tariffs. On inflation she focused on energy base effects and one-offs as the reason for lower inflation in January while stressing stable underlying indicators and most medium-term inflation expectations at 2%. She noted that the ECB has projected inflation below 2% in 2026 for a long time and that the 1.7% observed in January was consistent with the September staff projections despite coming in lower than the December projections. Hence, there still seems to be a clear bias towards holding the deposit rate steady despite inflation being below the 2% target.

Regarding the exchange rate, Lagarde stated that the ECB does not target specific rates but acknowledges its significance for inflation. The governing council discussed the exchange rate moves particularly against the USD and observed that the appreciation has occurred since March, and that no recent developments have raised concerns. The impact of the higher EUR/USD is already factored into the baseline projections. Hence, Lagarde clearly downplayed the euro strengthening and gave a very neutral answer as we had expected.

Lagarde also mentioned that the ECB is taking steps on reframing repo lines with the hopes of an announcement within the next few days. More specifically, she mentioned that the ECB is in the progress on reframing repo lines. Specifically opening up access and making them more attractive to other national central banks outside the euro area and Europe.

We maintain our call that the ECB will leave the deposit rate unchanged at 2.00% throughout both 2026 and 2027. Higher than expected growth and lower unemployment reduces the need for cuts in 2026 despite inflation falling below target. With inflation also projected below target in 2027 we do not expect ECB to hike rates. On the strategy side, we maintain our long-held payer bias in the short end of the EUR swap curve given the positive growth outlook, tight labour markets and the outlook of an increase in public spending in e.g. Germany.

Bank of England Review – Dovish Outlook Suggests More Cuts

- The Bank of England kept the Bank Rate unchanged at 3.75%.

- The vote split was 5-4, which was a dovish surprise.

- The new economic outlook for the UK entails less growth and inflation.

- We continue to aim for the next rate cut in April and pencil in another cut in November.

The Bank of England (BoE) kept the Bank Rate unchanged at 3.75% as expected. The decision was taken with a 5-4 vote, which was a closer call than expected and as such the probability of a rate cut in March and of several cuts has increased in our opinion. With two labour market reports and two inflation prints ahead of the March meeting, much can still happen by then.

Dissenting to the decision to hold rates were Dhingra, Taylor, Ramsden and Breeden, with the latter two as surprise moves, considering how data, if anything, has come in on the hawkish side since the December meeting. In the MPC member views, they both highlighted new analysis in the monetary policy report as a key reason why upside risks to inflation have diminished. Here BoE staff find that "structural changes in wage-setting will not keep adding to inflationary pressures".

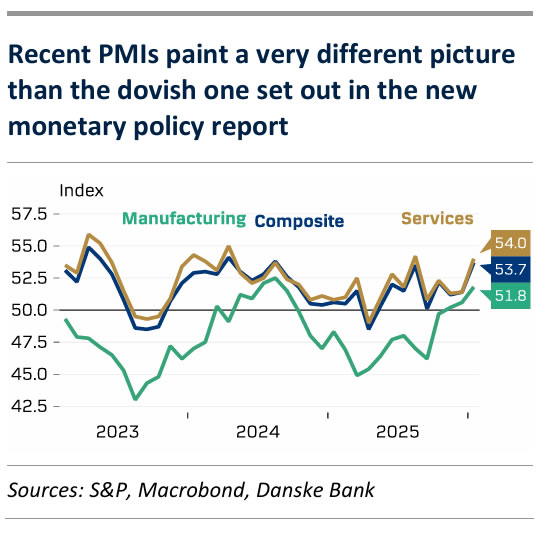

In its monetary policy report, the new BoE outlook has a more dovish tone with both GDP and inflation forecasts lower and unemployment higher compared to November. CPI Inflation is now expected at 1.7% in 2027Q1 vs. 2.2% in the November report, while annual GDP growth has been revised 0.3pp lower to 1.2%. We highlight that recent PMI data had a particularly more hawkish flavour, with composite PMI at its highest level in three years and price indices suggesting more sustained inflation pressures. Upcoming data will judge what to make of this.

BoE call. Once again, the timing of the next rate cut is coming down to Governor Bailey. He clearly looks ready to cut rates further and said he finds the two cuts currently priced by markets as fair. The timing will hinge on incoming data, and we expect the bar for cutting further has been raised as the Bank Rate has closed in on neutral levels. We continue to aim for the next rate cut in April and pencil in another one in November.

Market reaction. EUR/GBP traded a bit higher on announcement, supporting our expectation for a further weakening of GBP. We aim for EUR/GBP at 0.89 levels on a 12M horizon on decreasing rate differentials, relatively weaker growth outlook in the UK and positive correlation to a USD negative environment.

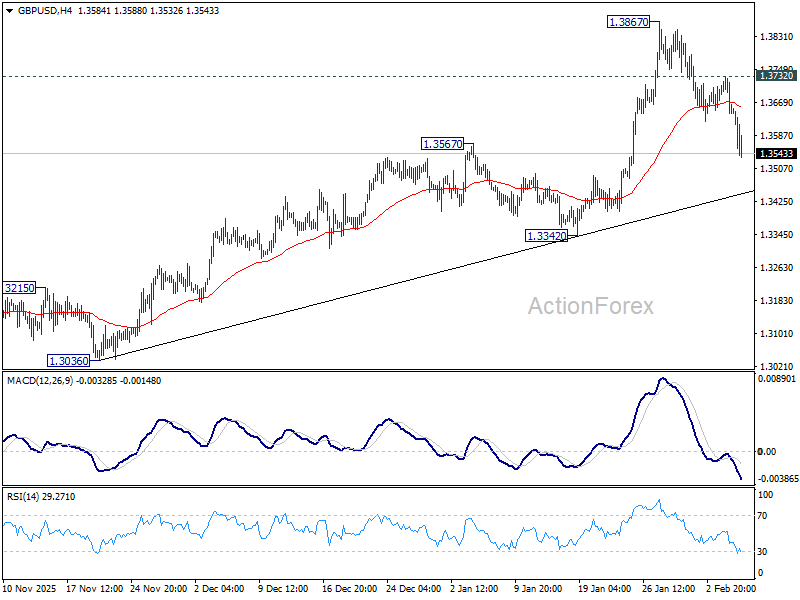

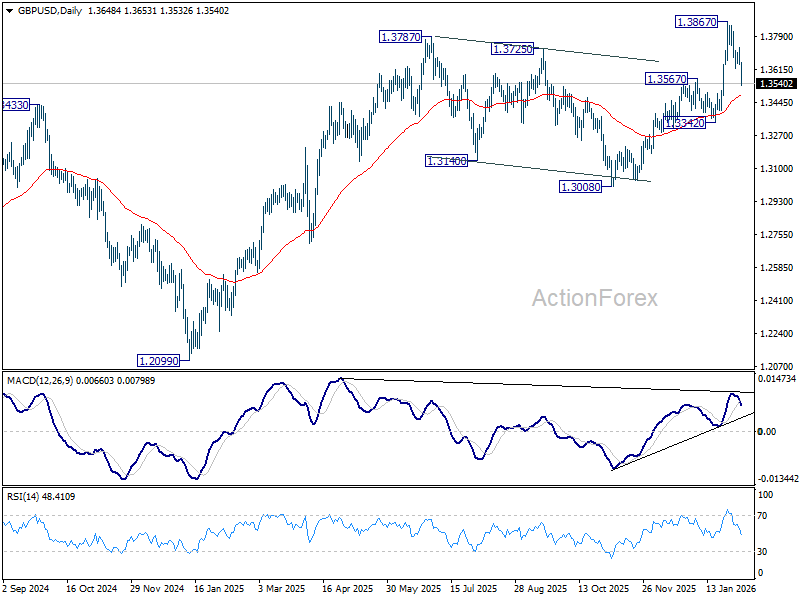

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3622; (P) 1.3677; (R1) 1.3712; More...

GBP/USD's fall from 1.3867 short term top is in progress. Intraday bias stays on the downside for 55 D EMA (now at 1.3482). Sustained break there will raise the chance of larger scale correction, and target 1.3342 support for confirmation. On the upside, above 1.3732 minor resistance will bring retest of 1.3867. Firm break there will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

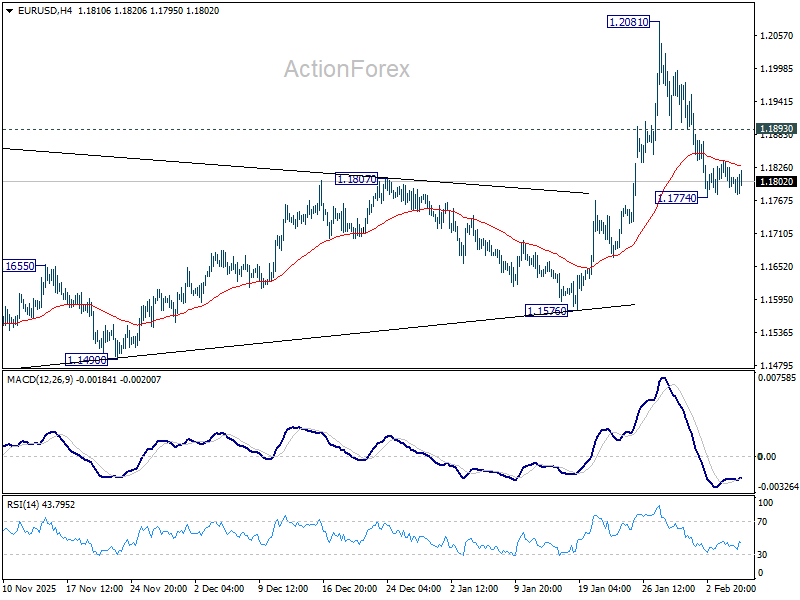

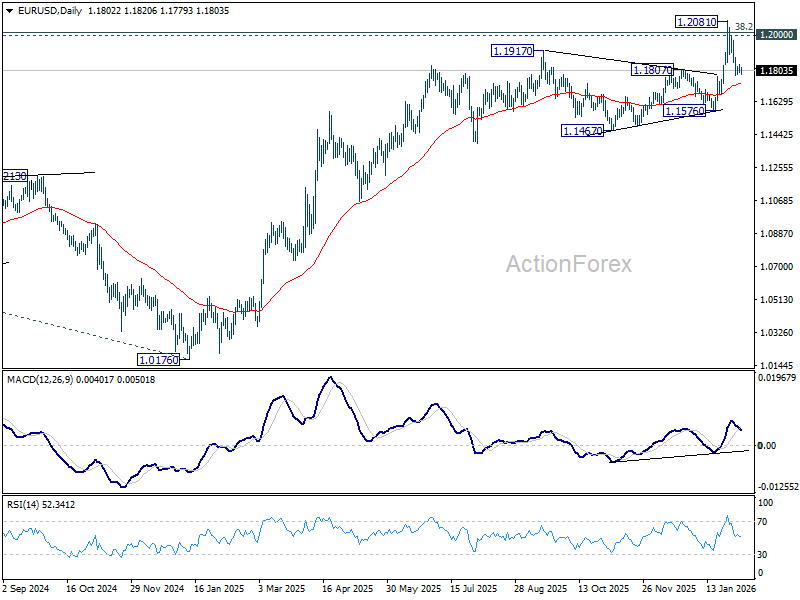

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1786; (P) 1.1812; (R1) 1.1833; More….

EUR/USD is still gyrating in tight range and intraday bias remains neutral. On the downside, below 1.1774 will extend the fall from 1.2081 short term top to 55 D EMA (now at 1.1724). Firm break there will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support. On the upside, above 1.1893 minor resistance will bring stronger rebound to retest 1.2081. Decisive break above 1.2 will carry larger bullish implications.

In the bigger picture, as long as 55 W EMA (now at 1.1458) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

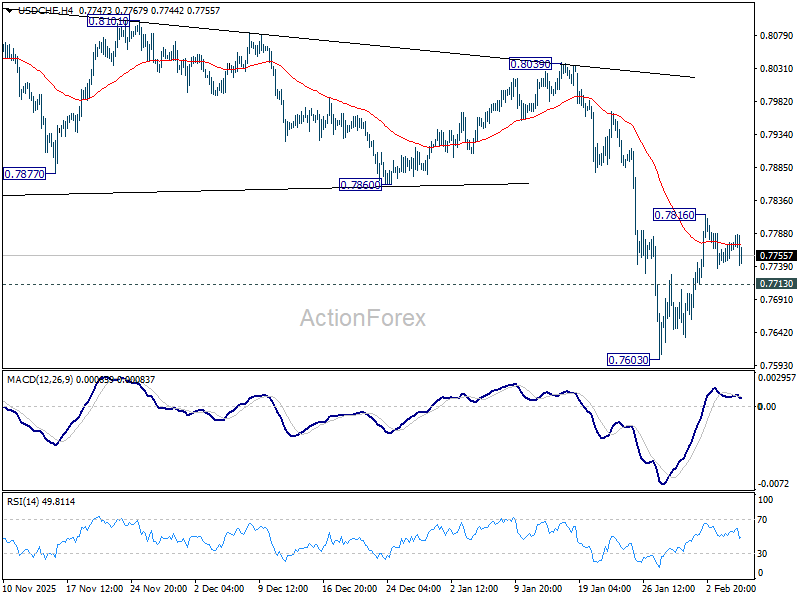

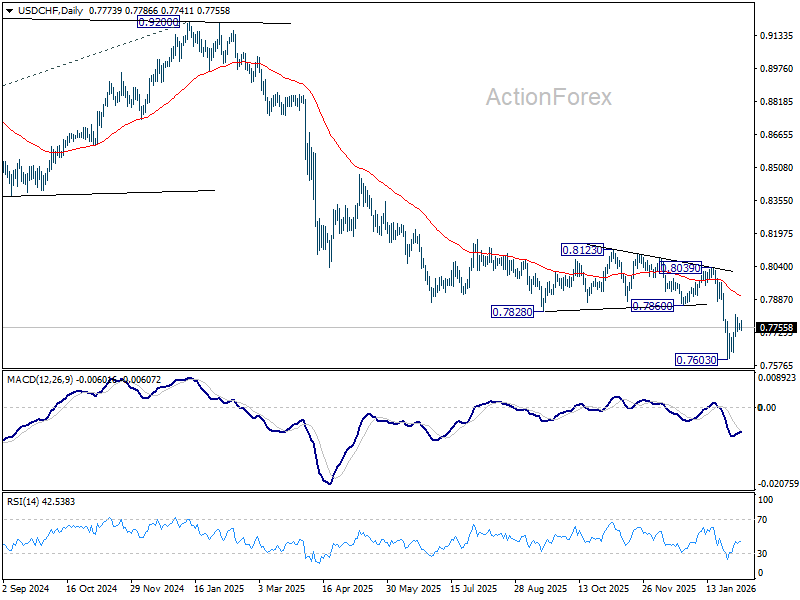

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7754; (P) 0.7765; (R1) 0.7785; More….

Intraday bias in USD/CHF stays neutral and outlook is unchanged. On the upside, above 0.7816 will resume the rebound from 0.7603 short term bottom to 55 D EMA (now at 0.7905). On the downside, below 0.7713 minor support will bring retest of 0.7603. Firm break there will resume larger down trend to 0.7382 projection level next.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8166) holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.03; (P) 156.49; (R1) 157.34; More...

No change in USD/JPY's outlook and intraday bias stays on the upside for the moment. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Further rebound should be seen to retest 159.44 next. On the downside, below 155.51 minor support will turn intraday bias neutral first. But overall outlook will stay bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96, in case of another dip.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.59) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

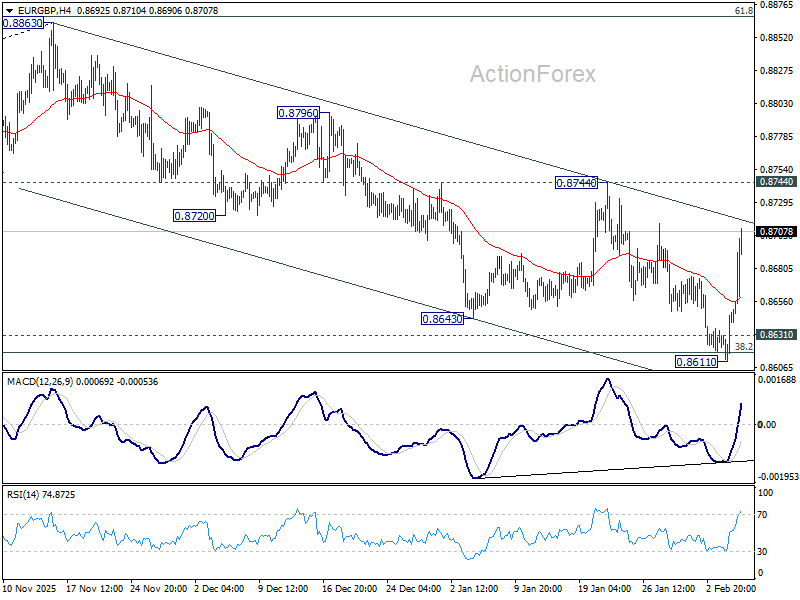

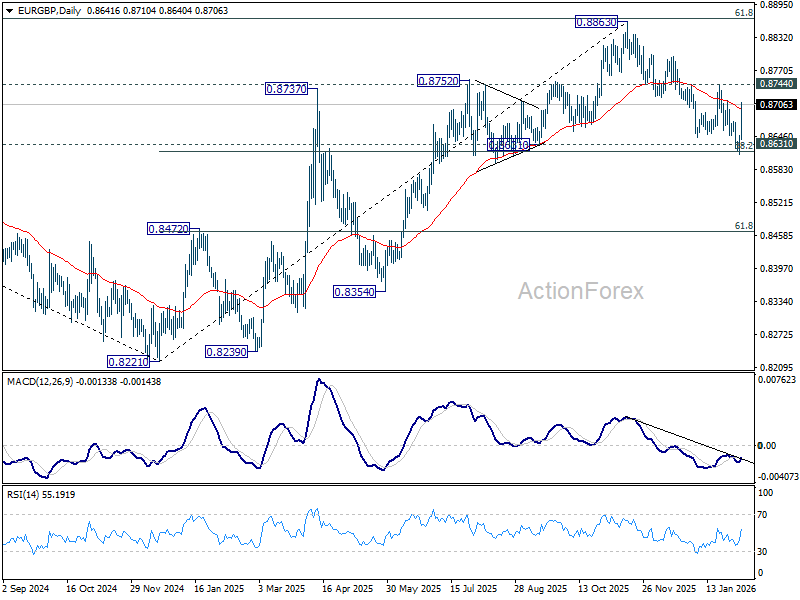

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8623; (P) 0.8636; (R1) 0.8660; More…

EUR/GBP's rebound from 0.8611 extended higher today but stays below 0.8744 resistance. Intraday bias stays neutral first. On the upside, firm break of 0.8744 will argue that fall from 0.8863 has completed as a correction. Intraday bias will be back to the upside for retesting 0.8863, with prospect of resuming larger up trend. Nevertheless, on the downside, decisive break of 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618) will carry larger bearish implications.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

BoE Dovish Tilt Knocks Sterling; Tech Rout Continues

Sterling weakened sharply after the dovish read-through from the BoE’s rate hold. Although Bank Rate remained at 3.75%, the narrow 5–4 vote surprised markets and brought forward expectations for another cut. The close split highlighted a policy committee on a knife edge. With nearly half the MPC already favoring easing, investors quickly began to price a higher probability of a March move.

That perception was reinforced by Governor Andrew Bailey’s press conference. Bailey framed the outlook as “one of good news,” emphasizing that the disinflation process is firmly on track and progressing faster than the Bank anticipated late last year. Bailey said inflation is expected to average around 3% through the first quarter before dropping close to the 2% target in April and staying there. He stressed that this timeline is roughly a year earlier than the Bank expected in November.

Those comments strengthened the view that, barring negative surprises, doves could hold the upper hand at the March meeting. Markets interpreted the message as lowering the bar for additional easing rather than reaffirming caution.

The broader market backdrop also turned less supportive for risk assets. Risk sentiment soured as US equities opened lower, led by renewed losses in the NASDAQ, extending the ongoing tech rout. Adding to the unease, the Challenger, Gray & Christmas report showed job cuts surged by 108k in January—the highest January total since 2009 and the largest monthly reading since October 2025.

Whether this tech-led weakness bleeds into traditional sectors is now the key watchpoint. For now, markets are cautious rather than panicked, but the labor signal has raised eyebrows. Risk-off sentient is giving Yen and Swiss Franc a lift as markets enter into the US session.

Euro also held modest gains following the ECB’s hold. With policy seen as appropriately set and Euro appreciation already factored into the baseline, the ECB signaled no urgency to move.

On the other hand, sterling is the weakest performer after the BoE’s dovish tilt. Aussie and Kiwi also lag on risk-off sentiment. Yen and Swiss Franc outperform with Euro. Dollar and Loonie trade in the middle.

In Europe, at the time of writing, FTSE is down -0.93%. DAX is down -0.92%. CAC is down -0.55%. UK 10-year yield is up 0.007 at 4.564. Germany 10-year yield is up 0.006 at 2.870. Earlier in Asia, Nikkei fell -0.88%. Hong Kong HSI rose 0.14%. China Shanghai SSE fell -0.64%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield fell -0.023 to 2.228.

BoE holds at 3.75%, 5-4 vote highlights uneasy balance

The BoE left Bank Rate unchanged at 3.75%, in line with expectations, but the decision masked a much tighter internal debate than markets had anticipated. The 5–4 vote highlighted how finely balanced was the policy considerations as inflation cools but uncertainties persist.

Five members, including Governor Andrew Bailey, backed holding rates steady. Within this group, Megan Greene, Clare Lombardelli and Huw Pill argued that a "more prolonged period of restriction" may still be needed to prevent inflation from settling above target. Bailey and Catherine Mann were more confident that easing inflation would mitigate that risk, but judged that the "evidence was yet sufficient" enough to justify a cut.

On the other side, four members—Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor—voted for an immediate 25bp reduction. They judged that risks of inflation persistence had "receded materially" and placed greater weight on weaker demand, arguing that policy remains overly restrictive.

Despite the hold, the overall message retained a clear easing bias. The statement reiterated that Bank Rate is "likely to be reduced further", but emphasized that future decisions will be finely judged and data-dependent, leaving the timing and pace of cuts firmly open.

ECB holds at 2.00%, Euro strength already factored in

The ECB left the deposit rate unchanged at 2.00%, in line with expectations. The accompanying statement reaffirmed confidence that inflation should stabilize at the 2% target over the medium term and reiterated a data-dependent, meeting-by-meeting approach to policy decisions.

At the press conference, President Christine Lagarde emphasized that risks are “broadly balanced.” She acknowledged that some risks have increased while others have eased, leaving the Governing Council comfortable with current settings rather than inclined toward near-term action.

Lagarde outlined upside and downside inflation scenarios. On the upside, persistent energy price increases, more fragmented global supply chains, slower moderation in wage growth, and planned boosts in defence and infrastructure spending could lift inflation over the medium term.

On the downside, weaker external demand from tariffs, excess global capacity spilling into euro area imports, tighter financial conditions, and a stronger Euro could all dampen price pressures.

On the exchange rate, Lagarde noted that Euro appreciation could bring inflation down beyond current expectations. However, she added that the Euro’s gains against the dollar since March 2025 are already incorporated into the ECB’s baseline, while stressing that the Bank will continue to monitor pass-through effects closely.

Eurozone retail sales fall -0.5% mom in December as consumer weakness persists

Retail sales across the Eurozone fell -0.5% mom in December, a steeper decline than the expected -0.2% drop.

Detail shows a clear split between essentials and discretionary items. Food-related sales rose slightly by 0.1% mom, but non-food purchases excluding fuel slumped 1.2%, pointing to continued restraint on big-ticket and discretionary spending. Fuel sales were flat, offering little offset to the broader weakness.

The weakness was broad-based across the European Union, where retail sales also fell 0.5% on the month. Among reporting countries, Portugal (-3.1%), Sweden (-1.9%) and Denmark (-1.6%) recorded the largest declines, while Luxembourg (+7.0%), Slovakia (+3.1%) and Croatia (+1.8%) posted solid gains.

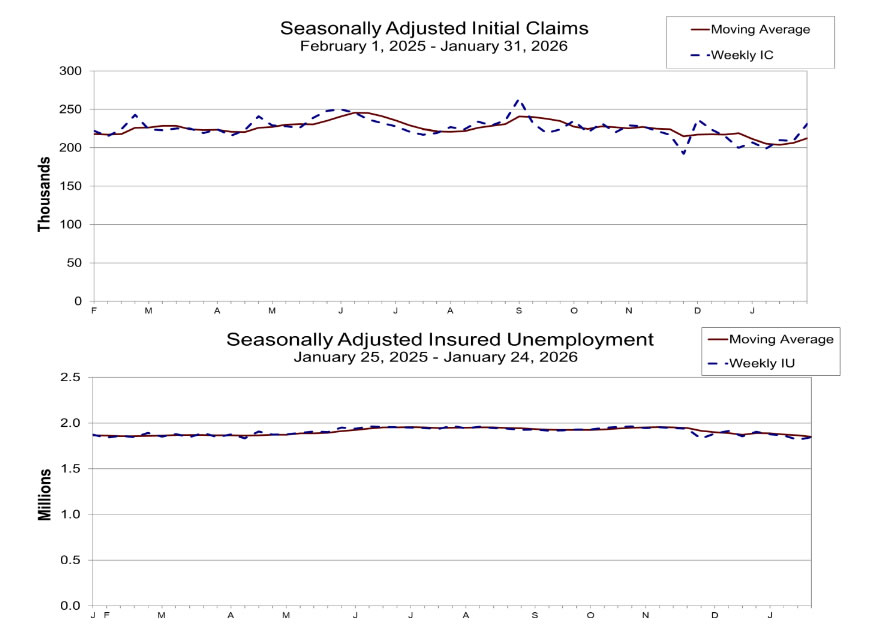

US initial jobless claims surge to 231k vs exp 210k

US initial jobless claims jumped 22k to 231k in the week ending January 31, well above expectation of 210k. Four-week moving average of initial claims rose 6k to 212k.

Continuing claims rose 25k to 1,844k in the week ending January 24. Four-week moving average of continuing claims fell -15k to 1851k, lowest since October 5, 2024.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8623; (P) 0.8636; (R1) 0.8660; More…

EUR/GBP's rebound from 0.8611 extended higher today but stays below 0.8744 resistance. Intraday bias stays neutral first. On the upside, firm break of 0.8744 will argue that fall from 0.8863 has completed as a correction. Intraday bias will be back to the upside for retesting 0.8863, with prospect of resuming larger up trend. Nevertheless, on the downside, decisive break of 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618) will carry larger bearish implications.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

US initial jobless claims surge to 231k vs exp 210k

US initial jobless claims jumped 22k to 231k in the week ending January 31, well above expectation of 210k. Four-week moving average of initial claims rose 6k to 212k.

Continuing claims rose 25k to 1,844k in the week ending January 24. Four-week moving average of continuing claims fell -15k to 1851k, lowest since October 5, 2024.