Sample Category Title

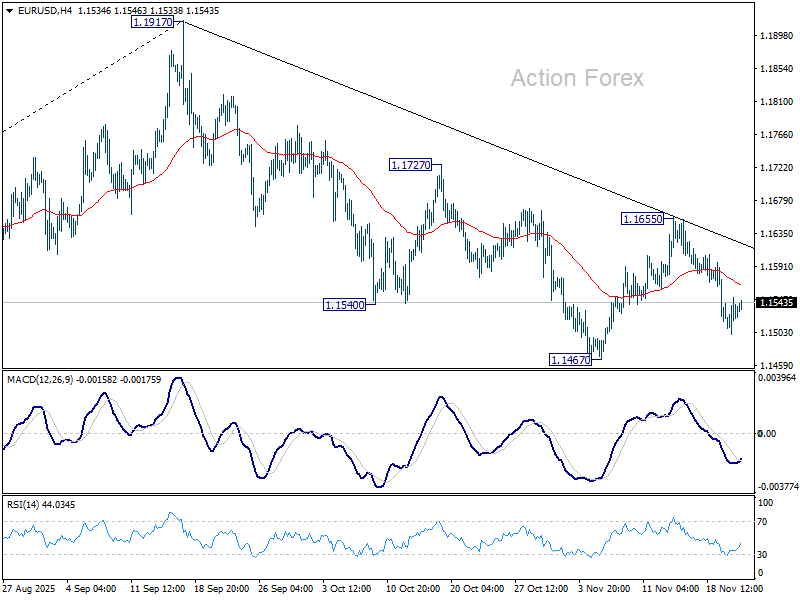

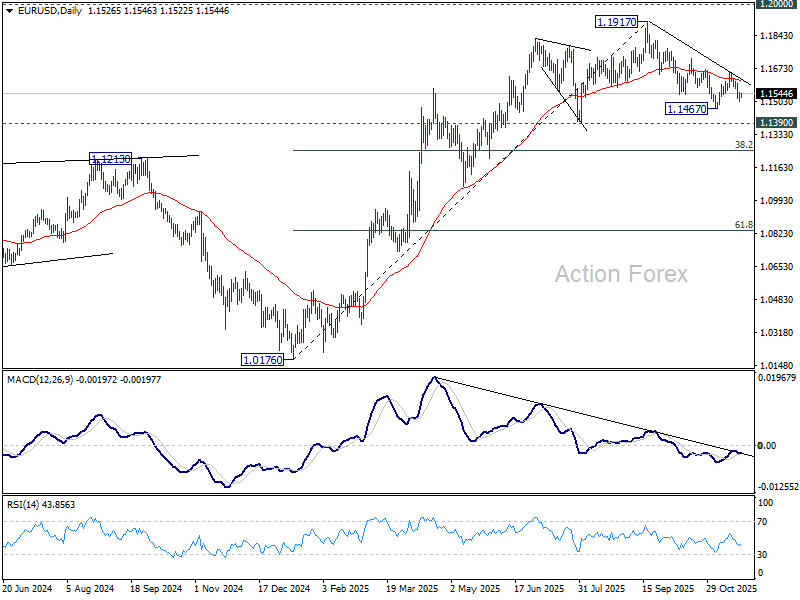

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1504; (P) 1.1527; (R1) 1.1551; More…

Intraday bias in EUR/USD stays mildly on the downside for retesting 1.1467 first. Firm break there will target 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. For now, risk will stay on the downside as long as 1.1655 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

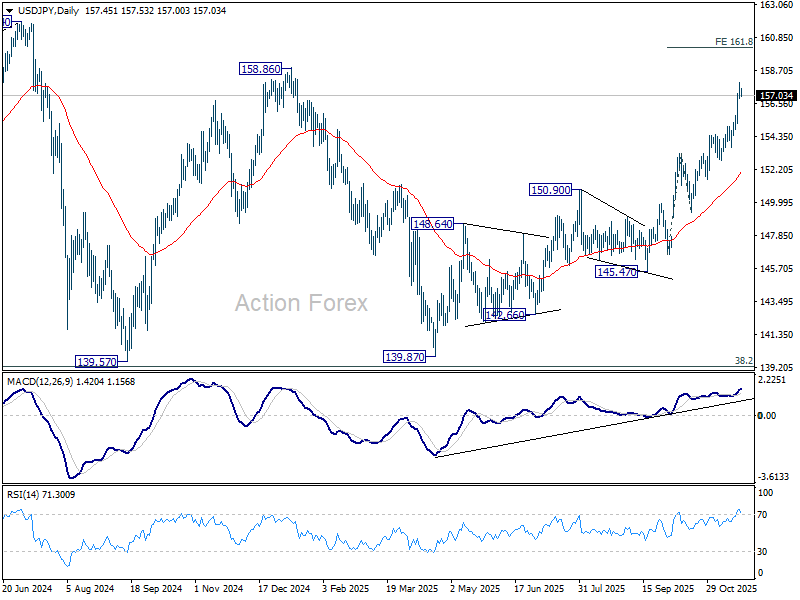

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.93; (P) 157.41; (R1) 157.94; More...

Intraday bias in USD/JPY is turned neutral with current retreat and some consolidations would be seen. Downside should be contained above 154.47 resistance turned support to bring another rally. Above 157.88 temporary top will resume larger rise to 161.8% projection of 146.58 to 153.26 from 149.37 at 160.17.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 restiveness turned support will dampen this bullish view and extend the corrective pattern with another falling leg.

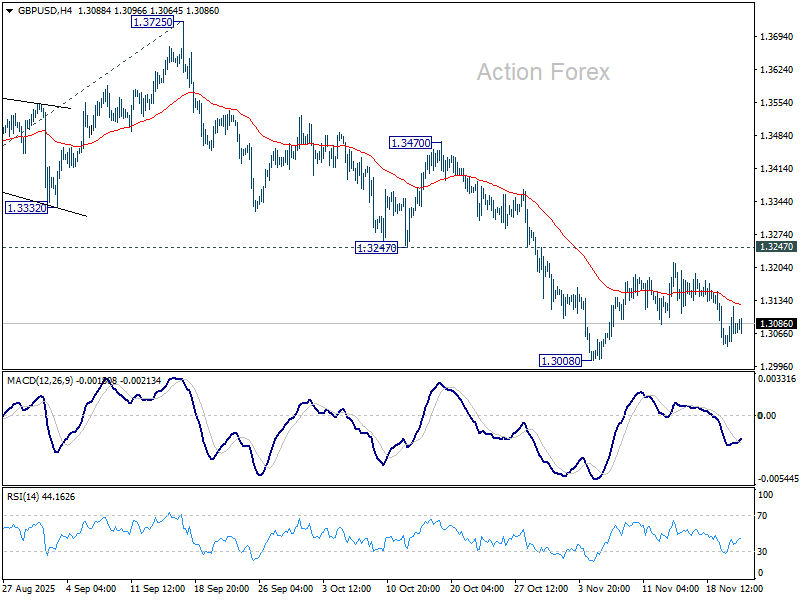

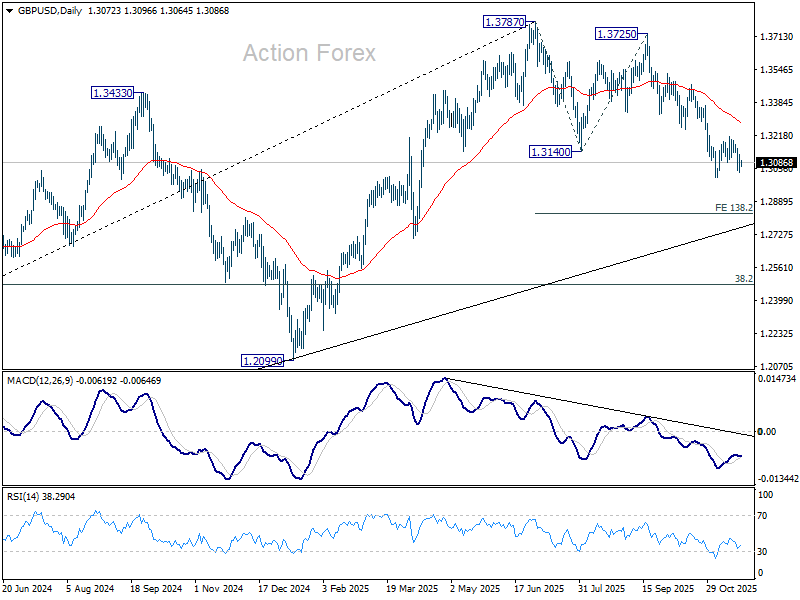

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3033; (P) 1.3078; (R1) 1.3119; More...

Range trading continues in GBP/USD and intraday bias stays neutral. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

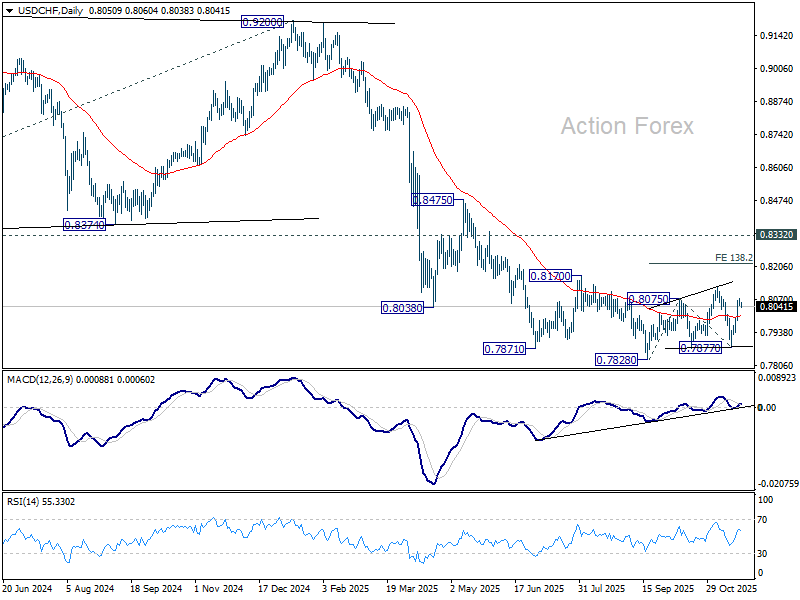

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8047; (P) 0.8062; (R1) 0.8076; More…

Intraday bias in USD/CHF is turned neutral first with current retreat. Overall, corrective pattern from 0.7828 is still extending. Above 0.8076 will target 0.8123 resistance next. On the downside, though, break of 0.7984 support will bring deeper fall back to 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

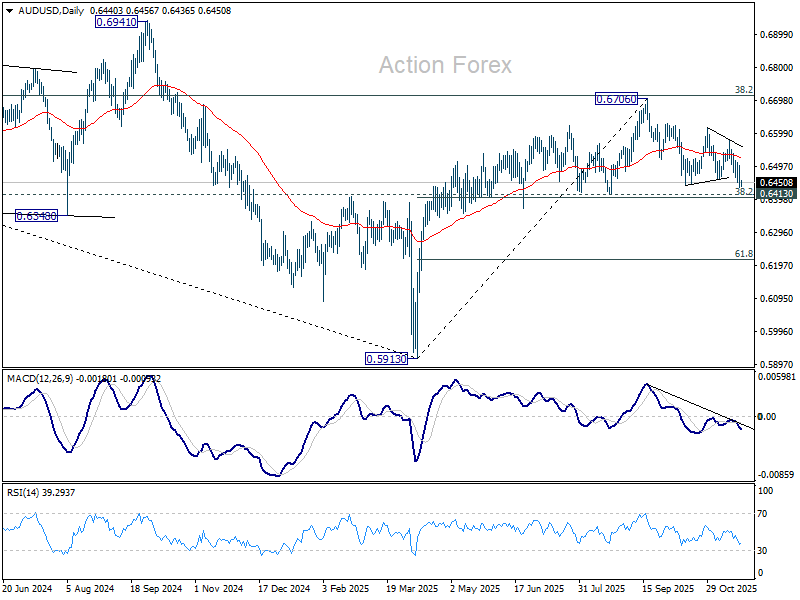

AUD/USD Daily Report

Daily Pivots: (S1) 0.6418; (P) 0.6460; (R1) 0.6485; More...

Intraday bias in AUD/USD stays on the downside as fall from 0.6706 resumed. Decisive break of 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403) will carry larger bearish implications. On the upside, above 0.6501 minor resistance will turn intraday bias neutral again first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

USDJPY Rally Stays Firm – Dips Continue to Draw Aggressive Buyers

The short-term Elliott Wave outlook for USDJPY indicates that the cycle from the October 17 low remains in progress as a five-wave impulsive structure. From that low, wave 1 concluded at 155.04, followed by a corrective pullback in wave 2, which ended at 153.60, as illustrated in the accompanying one-hour chart. Subsequently, the pair resumed its upward trajectory in wave 3, unfolding with internal subdivisions that reflect a lower-degree five-wave impulse.

Within this advance, wave ((i)) completed at 155.44, while the corrective dip in wave ((ii)) found support at 155.04. The pair has since extended higher in wave ((iii)), which is progressing toward the 157.89 level. Currently, a pullback in wave ((iv)) is underway, serving to correct the cycle that began from the November 18 low. Once this retracement concludes, the pair is expected to resume its upward movement in wave ((v)).

In the near term, as long as the pivot at 153.60 remains intact, any dips should find support in either a 3-, 7-, or 11-swing corrective structure, paving the way for further gains. The next potential upside target lies within the 100% to 161.8% Fibonacci extension range measured from the October 17 low. This zone spans from 159.26 to 162.75.

USDJPY 60-Minute Elliott Wave Chart From 11.21.2025

USDJPY Elliott Wave Video

https://www.youtube.com/watch?v=Qpqyd9i5oxI

Lunatic

Yesterday was something. We were happily sitting and watching Nvidia save the market after announcing another round of impressive results the night before. And all of a sudden – shortly after the US open – the mood started souring, and things went downhill from there. The Nasdaq, which jump-started 2% higher at the open, finished the day nearly 2.5% lower. That was really something.

Most of the news will say that AI spending and credit worries resurfaced – which is true. Oracle – the latest VIP member of OpenAI’s mega-deal circle – has now become the bellwether of AI credit risk, partly because it's spending billions financed by debt, and partly because it has weaker credit grades compared with Microsoft or Google. And Oracle saw its 5-year CDS spike past 110 bps – the highest in three years. CDS stands for credit default swaps, an instrument investors buy to hedge against the risk of default by a company or government. The higher the perceived risk of default, the higher the demand from investors, and the higher the price. I don’t want to bring this back, but Credit Suisse’s fall began in the CDS market.

Coming back to why market sentiment turned from euphoria to drama: a few reports and analyst comments on Nvidia’s own books started circulating yesterday, suggesting unease around two pressure points: swelling inventories and unusual patterns in deferred revenue. People started pointing out that Nvidia has built up large stockpiles of chips – partly because demand is shifting toward its next-generation Blackwell platform, and partly because US export controls have left billions’ worth of H20 chips potentially unsellable, forcing a multi-billion-dollar write-down.

At the same time, it’s been flagged that Nvidia has been taking in hefty pre-payments from customers and then recognising those payments as revenue too quickly, before chips are delivered. This is not illegal. It is a practice that can flatter near-term results but could leave a gap if future orders slow. And Nvidia may have done it to smooth out the avalanche of revenue it expects from Blackwell chip sales this year and next – Huang was talking about roughly $500bn in sales over that period. But together, the inventory overhang and the fast-cycling deferred revenue fuelled concerns that some of Nvidia’s blockbuster growth may be front-loaded, with future quarters more exposed than the headlines suggest.

When you dig deep enough, you’re sure to find dirt. And people only start digging when they begin to feel uncomfortable — and that level of discomfort is rising. Market opinion is becoming increasingly polarised between those who scream that this is a bubble and those who are willing to keep running. I believe this dynamic will lead to heightened volatility and big moves. It will be fun.

Also, the delayed data out of the US looks mixed and confusing. The September jobs data – released yesterday – was not only old and dusty, but also somewhat mixed. The report suggested that the US economy added nearly 120k new jobs in September, far above the 53k expected by analysts. The separate weekly report showed jobless claims falling to 220,000 – unexpectedly strong. That was the glass-half-full part. But the uptick in the unemployment rate to 4.4% and slowing wages were the glass-half-empty part – half-empty depending on whom, of course, since soft data fuels the Federal Reserve (Fed) doves and is often supportive for risk appetite.

But it didn’t yesterday. The data helped the Fed doves gain field, but the AI worries and Nvidia rumours kept the upper hand. The sharp decline in US 2-year yields and the improved chance of a December cut couldn’t talk the bulls in.

The good news is that Japanese yields are down from peak levels this morning – maybe inflation climbing to a 3-month high cooled the Bank of Japan (BoJ) doves. But it was hard to crack a smile out of SoftBank this morning: the shares tanked more than 10% and are down almost 40% since the October peak.

The crash in cryptocurrencies may be forcing investors to liquidate other positions – likely their tech bets. Bitcoin is testing the $86k level at the time of writing, and to be fair, there’s nothing to stop the fall given that we have no idea what a coin is worth – other than the value we collectively give it.

So the week will end in a worse dilemma than where it started. Nvidia couldn’t save the market. The Fed is still expected not to cut rates in December. Japanese yields kept pushing higher this week, and the 10-year JGB surpassed a critical level thought to trigger Japanese repatriation back home. That’s roughly $3.4 trillion in overseas assets held by Japanese investors – from US Treasuries to tech and EM – that could, in theory, be pulled back home if domestic yields climb further. So the bubble talk is bubbling everywhere. The valuations are high, the problem diggers are out digging.

No one can tell if or when the balloon will burst or who will take the hit. And there is no guarantee that history will repeat itself. Yet comparing today’s prices to past cycles is always interesting. Nasdaq, gold and Japanese assets show similar trends compared with the dot-com bubble, the gold boom of 1976–1982, and the Japanese bubble between 1986 and 1992. But today’s prices are not even halfway to the past peaks. Again, I can’t – and no one can – tell you whether this is going to be dot-com bubble 2.0 or Japanese asset bubble 2.0, but if history is any guide, bubbles tend to inflate well beyond what reason would suggest.

Ukrainian Concessions Key in US Peace Proposal as Pressure Builds

In focus today

In the euro area, November flash PMIs are due. In October, the services PMI rose to 53.0 while manufacturing reached 50.0, moving out of contraction territory. The developments suggest positive momentum for the euro area heading into Q4, and we expect the November PMIs to remain unchanged from October's.

We also receive the ECB's indicator of negotiated wages for Q3, which is heavily influenced by last year's one-off inflation bonuses. Q2 negotiated wages rose 4.0% y/y (up from 2.5% in Q1) due to base effects, but we expect a sharp decline to 2.2% y/y in Q3, as signalled by the ECB's wage tracker. Wage growth is trending lower, supporting reduced services inflation.

In Sweden, data for capacity utilisation, gross investments, inventories, and the inventory-adjusted production value index for Q3 are being released. The production value index has shown strong performance, supporting the notion that the recovery is progressing slightly better than anticipated. The inventory adjustment is unlikely to change this outlook.

Economic and market news

What happened overnight

Ukraine-Russia, the 28-point peace plan proposed by the US to Ukraine seems to heavily favour Russia, requiring significant Ukrainian concessions and capping its military at 600,000 troops. Although NATO membership is ruled out, the possibility of EU accession remains open. While the plan's security guarantees are vague, additional documents reportedly include NATO-like assurances. With Ukraine facing mounting pressure on the battlefield, the likelihood of a ceasefire this year has increased, potentially further supported by robust guarantees.

In Japan, new PM Takaichi has approved a supplementary budget worth JPY21.3 trillion, representing the largest stimulus package since the pandemic. The runup to this has weighed heavy on the yen recently and pushed longer-dated JGB yields higher. Also overnight, nationwide CPI inflation excluding fresh food increased a bit to 3.0%, confirming the uptick from the Tokyo data. The weak yen will continue to push for high import prices, which adds to speculation that the Bank of Japan will soon hike rates again. We are also closing in on a situation where FX intervention to support the yen is once again on the table. This is a government decision, though, not the central bank's.

What happened yesterday

In the US, September NFP rose by 119k (cons: +50k), while August was revised down to a 4k decline from +22k. Despite stronger-than-expected NFP, the unemployment rate increased to 4.4% from 4.3%, driven by a rise in the native US-born labour force (+636k) and a decline in immigrant workers (-166k). This supply-driven increase in unemployment eased labour market tightness, triggering a dovish market reaction with UST yields slightly lower and EUR/USD rising. However, we do not view this as a strong dovish signal for the Fed or expect the trend to persist. We still expect the Fed to stay on hold in December, with markets currently pricing around 32% probability of a cut.

In Denmark, GDP grew 2.3% q/q in Q3, driven by Novo Nordisk's pharmaceutical export, excluding pharma, growth was a modest 0.7% q/q. Domestic consumption remains weak despite rising real incomes, we expect consumption to pick up eventually, driven by rising real wages, but the timing remains uncertain. Future GDP growth will depend on Novo Nordisk, while broader conditions remain stable with low unemployment and solid demand.

Consumer confidence dropped to -20.1 in November, a 2.5-year low, reflecting economic concerns and inflation fears. Despite easing food prices, Danes perceive inflation as much higher than 2%. Record household savings could drive spending if optimism improves, though current data suggests this is unlikely soon.

In the euro area, November's flash consumer confidence held steady at -14.2, slightly below expectations of -14.0. Weak confidence continues to weigh on consumption growth, despite supportive fundamentals such as rising employment, lower rates, and increasing real incomes.

In Norway, Norges Bank's Q4 expectations survey showed slightly higher inflation expectations on 12M and 2Y, which is not ideal but unlikely to shift policy given recent inflation volatility. Labour organisations raised wage expectations for this and next year, though average wage growth forecasts for 2025 (4.4%) and 2026 (3.9%) remain below Norges Bank's September MPR projections.

Equities: Global equity markets experienced a pronounced rollercoaster yesterday. After rising roughly 1.6% heading into the early afternoon, supported by the latest US data releases, sentiment abruptly reversed, sending major indices sharply lower. MSCI world ultimately closed down around 1.1%, marking an almost 3% peak-to-trough swing on the day. S&P500 ended -1.6% lower, Nasdaq -2.2% and Russell2000 -1.8%. The only sector offering resilience was consumer staples, buoyed by Walmart's strong Q3 earnings beat. Despite already elevated expectations and a PE higher than the Mag7, Walmart outperformed and offered a rare pocket of stability (Walmart +6.5%).

Overnight, Asian equity indices are down this morning except Japan due to its announced fiscal stimuli, see below.

Volatility surged as defensive sectors outperformed cyclicals in the sea of red. The VIX briefly spiked above 28 on an intraday level before settling at 26.4, which is the highest level since April. Few need to be reminded of market developments then, yet it is important to recognize the significant uncertainty from the equity markets this week. Importantly, this episode is concentrated within equity markets; in contrast, bond-market volatility actually declined yesterday, and the VIX/MOVE-dynamics have decoupled. Overall, the market dynamic was not a classic flight to safety albeit there was not a clear catalyst for the abrupt intraday reversal. Speculation continues whether this is the ongoing AI capex story or profit taking, yet this lacks hard economic fundamental justification at this stage.

FI and FX: The US September jobs report was a mixed read, but with US yields declining 4-5 bp across the curve, the interpretation was mainly to the dovish side. EUR/USD drifted slightly higher but is still lower on the week. Nvidia's earnings report supported risk sentiment initially, but roughly halfway through the US session we saw a huge intraday reversal with the Nasdaq falling 5% from its intraday highs and the S&P500 closing at a weekly low. The sudden risk-off impacted FX markets, where especially commodity-currencies felt the strain, with EUR/NOK rising sharply towards 11.80. EUR/SEK, on the other hand, saw only limited moves yesterday and remains firmly anchored at 11.00.

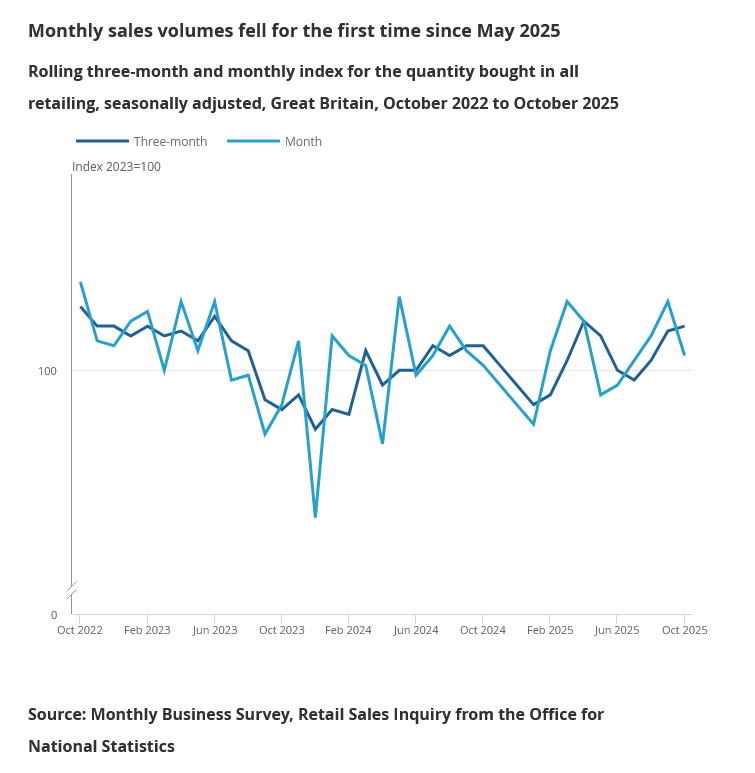

UK retail sales slump -1.1% mom in October as shoppers hold off for Black Friday

UK retail sales delivered a sharp downside shock in October, falling –1.1% mom, well below expectations of a modest 0.1% increase. It was the first monthly decline since May and reflected broad weakness across supermarkets, clothing, and online retailers.

Some retailers suggested that consumers deliberately postponed purchases in anticipation of Black Friday promotions, magnifying the pullback at a time when household budgets remain stretched by high interest rates and inflation.

Despite the poor monthly reading, retail sales in the three months to October were still up 1.1% compared with the prior three-month period.

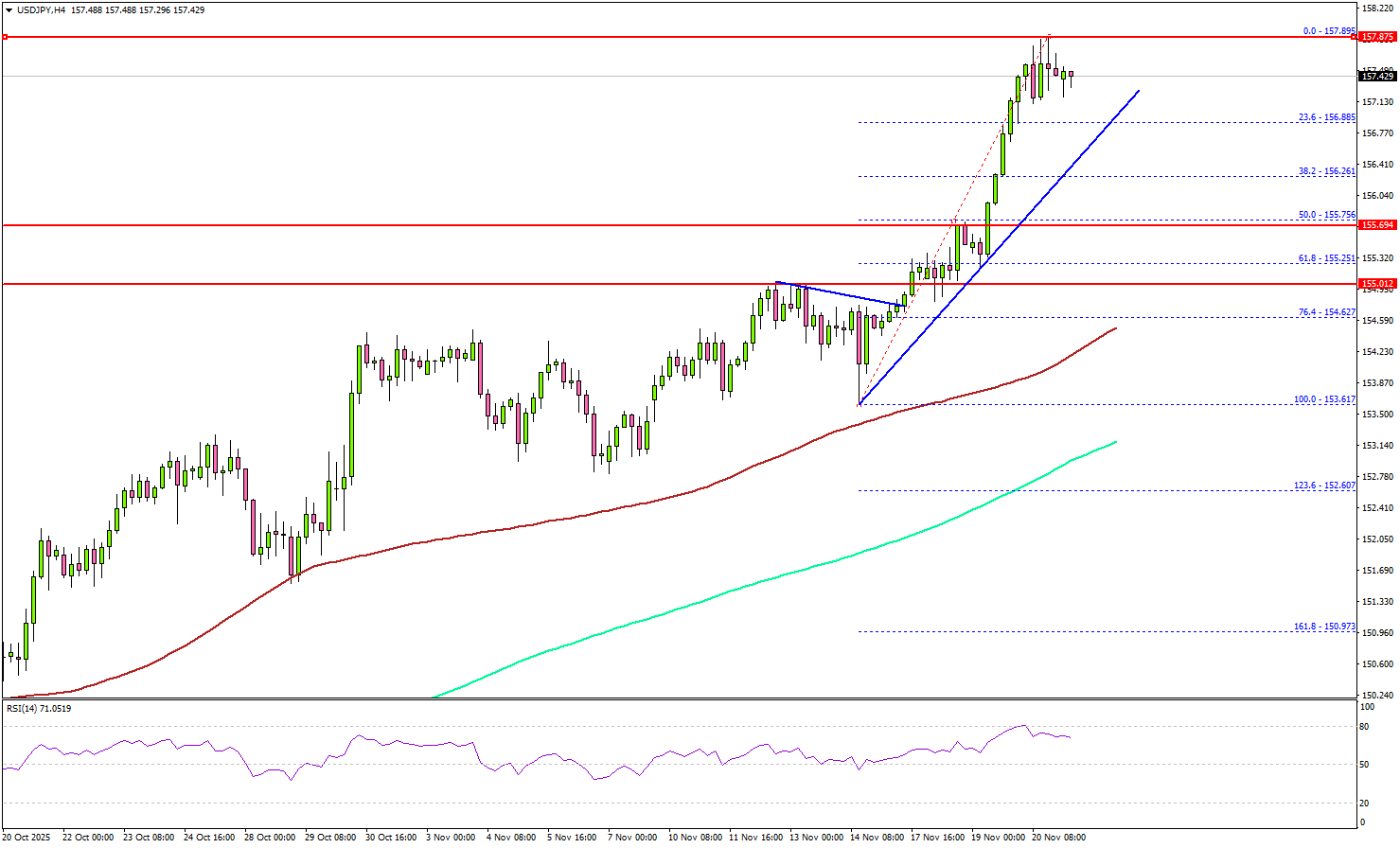

USD/JPY Jumps Again as Buyers Tighten Grip on Near-Term Trend

Key Highlights

- USD/JPY started a fresh surge above 155.00 and 156.00.

- A bullish trend line is forming with support at 156.60 on the 4-hour chart.

- EUR/USD is again declining and might revisit 1.1450.

- GBP/USD could struggle to recover above 1.3150 and 1.3200.

USD/JPY Technical Analysis

The US Dollar remained well-bid above 152.50 against the Japanese Yen. USD/JPY started a fresh surge and cleared many hurdles near 155.00.

Looking at the 4-hour chart, the pair settled above 156.00, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even spiked above 157.50 and might continue to rise.

On the upside, the pair faces resistance near the 158.00 zone. The first key hurdle sits at 158.40. A close above 158.40 might send the pair higher toward 159.20.

The next resistance could be 160.00. Any more gains could set the pace for a steady increase toward 162.00. On the downside, there is a key support at 156.70. There is also a bullish trend line forming with support at 156.60.

The next support is 156.20, below which the pair could start a steady decline to 155.70. A close below 155.70 could start a pullback toward 155.00. Any more losses might open the doors for a test of 154.50 and the 100 simple moving average (red, 4-hour).

Looking at GBP/USD, the pair failed to recover steadily and is now at risk of another decline, possibly below the 1.3000 support.

Upcoming Key Economic Events:

- US S&P Global Manufacturing PMI for Nov 2025 (Preliminary) – Forecast 52.0, versus 52.5 previous.

- US S&P Global Services PMI for Nov 2025 (Preliminary) – Forecast 54.8, versus 54.8 previous.

- Michigan Consumer Sentiment Index for Nov 2025 – Forecast 50.5, versus 50.3 previous.