Sample Category Title

Dollar Eases as Markets Shift to Risk-On Despite Strong NFP

Dollar strength faded mildly after the stronger-than-expected U.S. non-farm payroll report, as traders showed little appetite to extend the post-data rally. The muted reaction reflects a market that had already repriced aggressively after yesterday’s hawkish FOMC minutes, which pushed expectations for a December rate cut sharply lower. In that sense, much of the adjustment had already been done before today’s data even hit.

The jobs report merely reinforces the prevailing view: the Fed may not need to cut again in December, and policymakers can comfortably adopt a wait-and-see approach. Rather than reset expectations, the numbers simply validated what markets had already shifted toward following the minutes. With the pricing for a December cut already pared back, there was limited room for the Dollar to gain further on the headline beat alone.

At the same time, risk sentiment has flipped decisively into positive territory, driven by renewed AI enthusiasm after Nvidia’s earnings report. The resurgence in tech optimism has spilled across global equities and FX markets, providing fresh support to risk-sensitive currencies, even Sterling, and curbing defensive flows into Dollar.

Still, one feature of the FX markets that hasn’t changed this week is the extended and persistent weakness in Yen. Expectations that BoJ will delay its next rate hike — combined with rising global yields and Japan’s pro-stimulus policy backdrop — continue to leave the currency pinned at the bottom of the performance table.

For the week so far, Dollar remains the strongest performer, followed by Loonie and then Aussie. Yen sits firmly at the bottom, trailed by Swiss Franc and Kiwi. Euro and Sterling are positioned in the middle, with the Pound maintaining a slight edge thanks to improved risk appetite.

In Europe, at the time of writing, FTSE is up 0.62%. DAX is up 1.11%. CAC is up 0.90%. UK 10-year yield is down -0.015 at 4.584. Germany 10-year yield is up 0.014 at 2.731. Earlier in Asia, Nikkei rose 2.65%. Hong Kong HSI rose 0.02%. China Shanghai SSE fell -0.40%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield jumped 0.049 to 1.820.

US NFP beats expectation with 119k growth, but unemployment rate ticks up to 4.4%

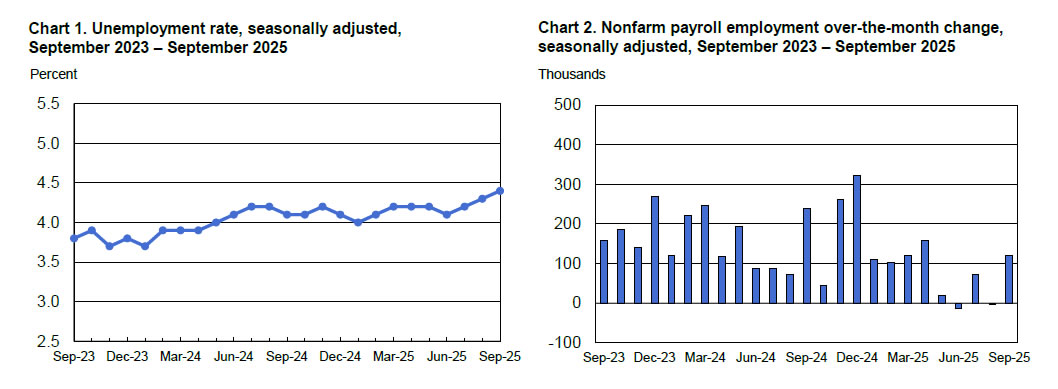

U.S. non-farm payrolls surprised strongly to the upside in September, rising 119k versus expectations of 53k, more than making up for August’s downward revision from 22k to -4k. The stronger headline signals that hiring momentum hasn’t stalled as much as feared.

However, the details of the report were more mixed. The unemployment rate edged up from 4.3% to 4.4%, slightly above expectations. Though the increase came alongside a modest rise in participation from 62.3% to 62.4%, suggesting more workers entered the labor force.

Wage growth cooled, with average hourly earnings up only 0.2% mom, below the 0.3% consensus, bringing annual growth to 3.8% yoy. The average workweek held steady at 34.2 hours, pointing to no deterioration in hours worked.

Taken together, the data portray an economy that is still generating jobs but with softer wage pressures—likely welcomed by the Fed as it evaluates the necessity of another rate cut before year-end.

BoJ hawkish voice emerges as Koeda presses for further tightening

BoJ board member Junko Koeda delivered one of the clearest hawkish signals from the Bank in recent months, arguing that real interest rates remain “significantly low” and must be moved back toward "a state of equilibrium" to avoid “unintended distortions” later.

With Japan’s output gap hovering around zero and labor market tightness intensifying amid widespread staff shortages, she said in a speech that current economic backdrop justifies continued normalization. In her view, the BoJ should “continue to raise” the policy rate as economic conditions improve, adjusting monetary support in line with the broader recovery in activity and prices.

Koeda stressed that underlying inflation is running near 2%, but achieving the target sustainably requires the Bank to test how firmly "underlying inflation has remained stable or been anchored". That means looking beyond headline data to evaluate whether price momentum can hold as temporary factors fade.

Her message contrasted with recent political pressure urging caution on tightening, reinforcing the divide between policymakers seeking gradual normalization and government voices favoring prolonged accommodation.

PBoC stays on hold, but markets still see easing ahead

China kept its benchmark lending rates unchanged for the sixth straight month today, leaving the one-year Loan Prime Rate at 3.0% and the five-year rate at 3.5%. The decision was widely expected, as policymakers continue to balance the need to support the economy with the desire to avoid fuelling financial instability.

Despite the steady stance, markets remain convinced that monetary easing has merely been delayed, not abandoned. Expectations are building for a “dual cut” — both policy rates and banks’ reserve requirement ratio — in the first quarter of 2026.

A run of softer October activity data has strengthened that view. Exports contracted, retail sales slowed further, and the property-related drag has shown little sign of easing. Combined, these have heightened concerns that Q4 will bring more headwinds rather than signs of stabilization.

Adding to the pressure, new bank lending fell sharply in October as both households and businesses remained reluctant to take on fresh debt amid weak confidence and ongoing US-China trade tensions. Without a meaningful pickup in credit demand, Beijing may soon have little choice but to act more decisively to shore up activity in early 2026.

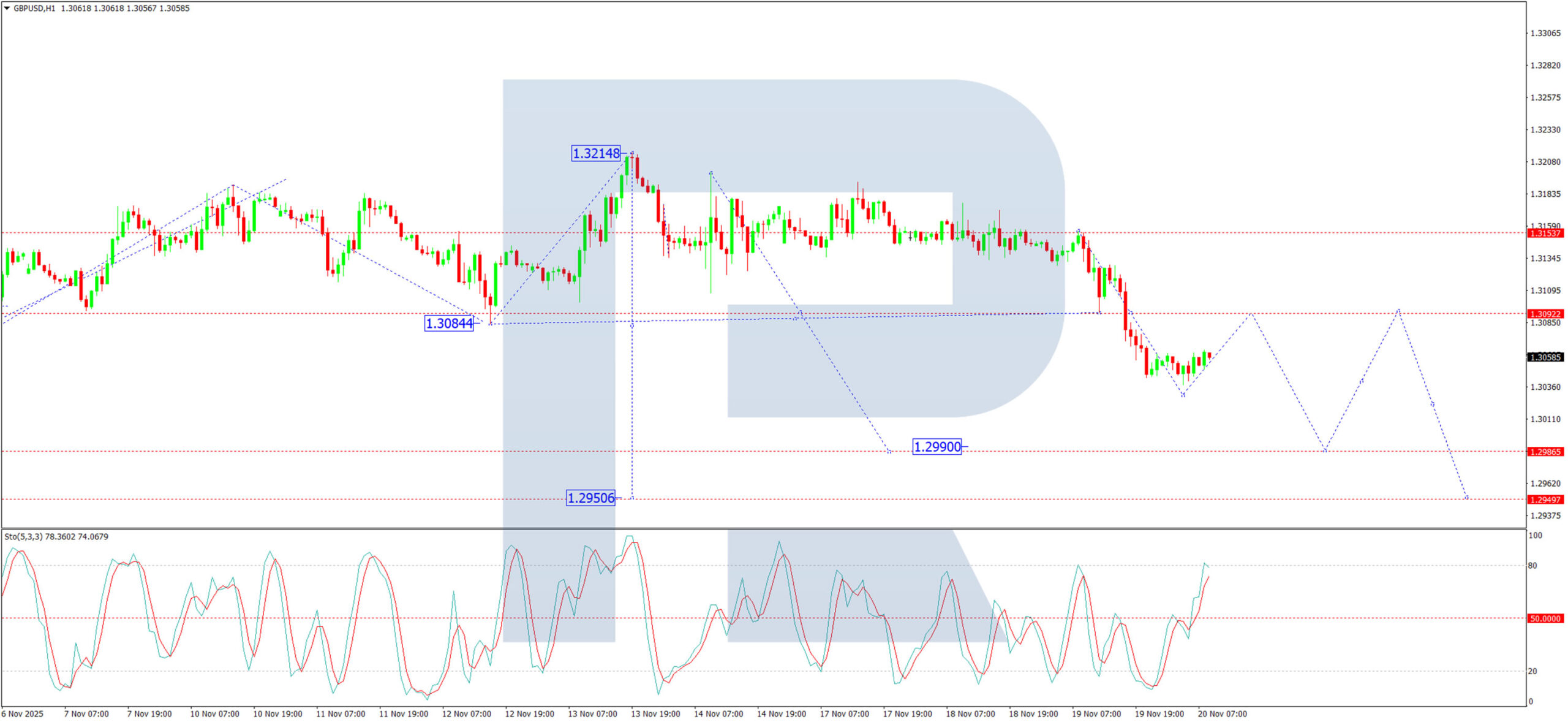

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3018; (P) 1.3087; (R1) 1.3129; More...

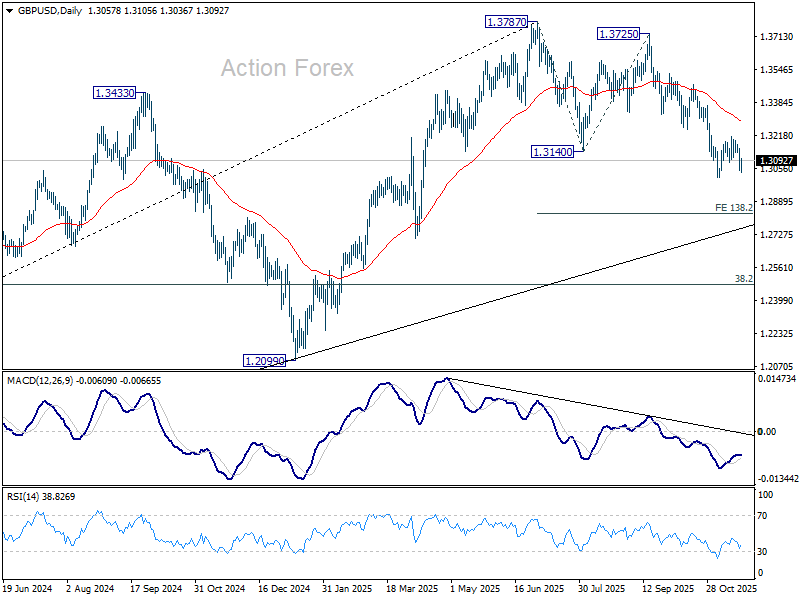

GBP/USD recovers mildly today as range trading continues. Intraday bias remains neutral and outlook is unchanged. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

US NFP beats expectation with 119k growth, but unemployment rate ticks up to 4.4%

U.S. non-farm payrolls surprised strongly to the upside in September, rising 119k versus expectations of 53k, more than making up for August’s downward revision from 22k to -4k. The stronger headline signals that hiring momentum hasn’t stalled as much as feared.

However, the details of the report were more mixed. The unemployment rate edged up from 4.3% to 4.4%, slightly above expectations. Though the increase came alongside a modest rise in participation from 62.3% to 62.4%, suggesting more workers entered the labor force.

Wage growth cooled, with average hourly earnings up only 0.2% mom, below the 0.3% consensus, bringing annual growth to 3.8% yoy. The average workweek held steady at 34.2 hours, pointing to no deterioration in hours worked.

Taken together, the data portray an economy that is still generating jobs but with softer wage pressures—likely welcomed by the Fed as it evaluates the necessity of another rate cut before year-end.

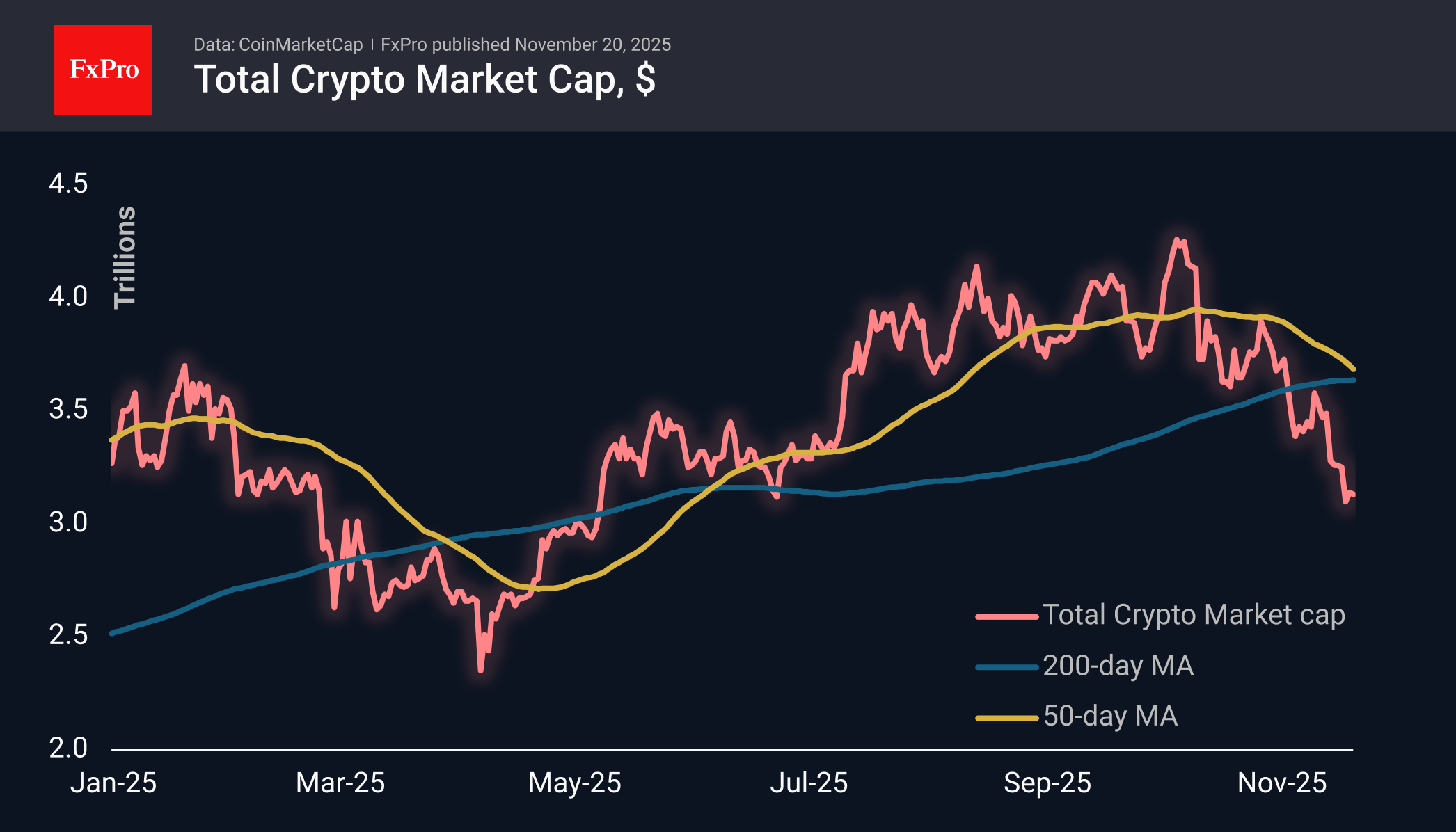

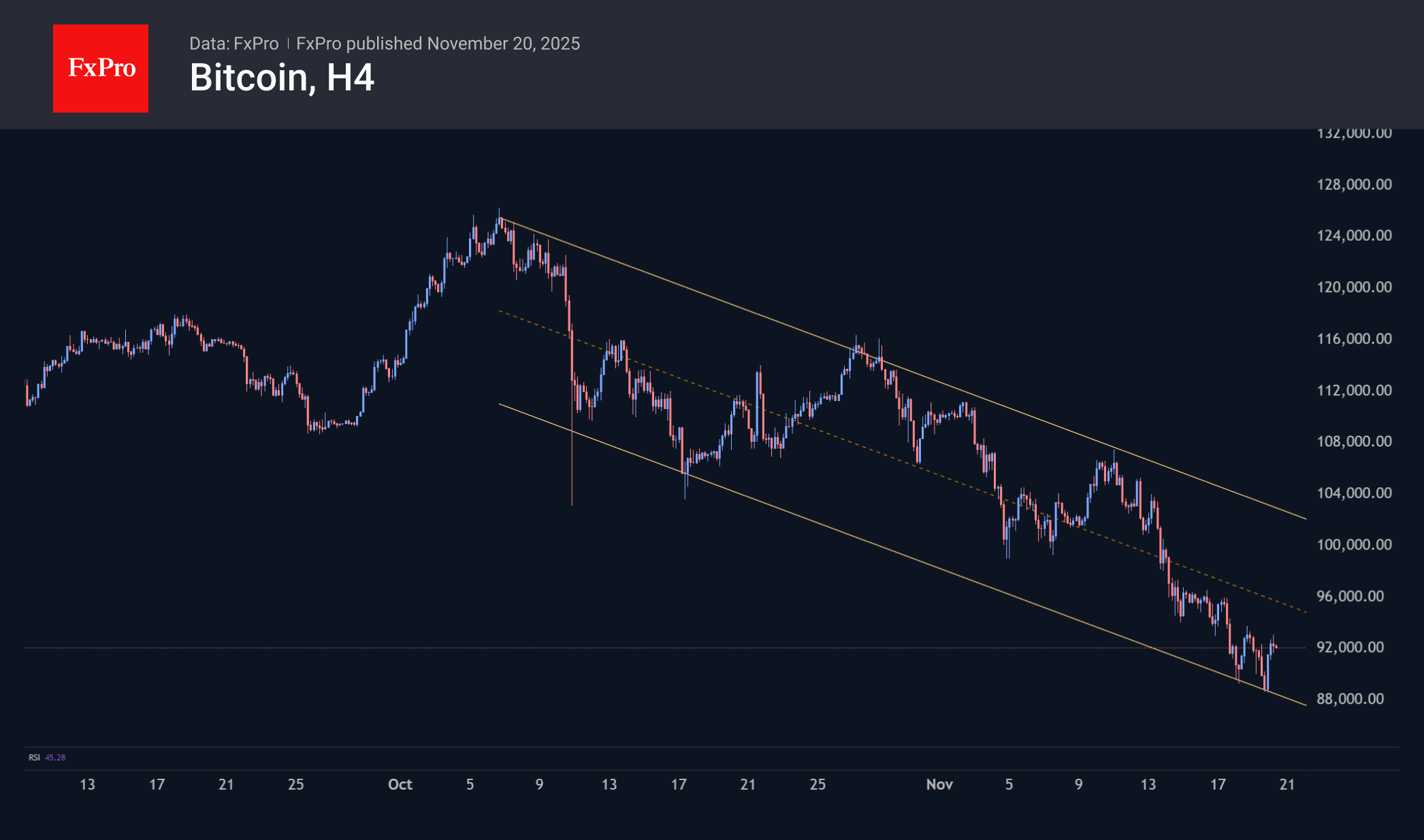

Crypto: Still Got the Blues

Market Overview

The crypto market fluctuated slightly over the past day, ranging from a low of $3.02 trillion before the publication of the FOMC minutes and Nvidia’s earnings, to a peak of $3.16 trillion in the middle of the Asian session. However, it has now fallen back to $3.13 trillion, remaining almost unchanged for the day. The cryptocurrency market remains pessimistic, reacting eagerly to negative news and quickly deflating on positive news.

Bitcoin is trading just above $92K at the start of the day on Thursday. It has been hovering around this level for the last four days, but the last ten days have seen lower local lows (falling to $88.5K at the end of the day on Wednesday) and local highs, indicating a very aggressive sell-off. In such conditions, it is only a matter of days before the bears find stop-out levels, triggering a self-sustaining avalanche of selloffs.

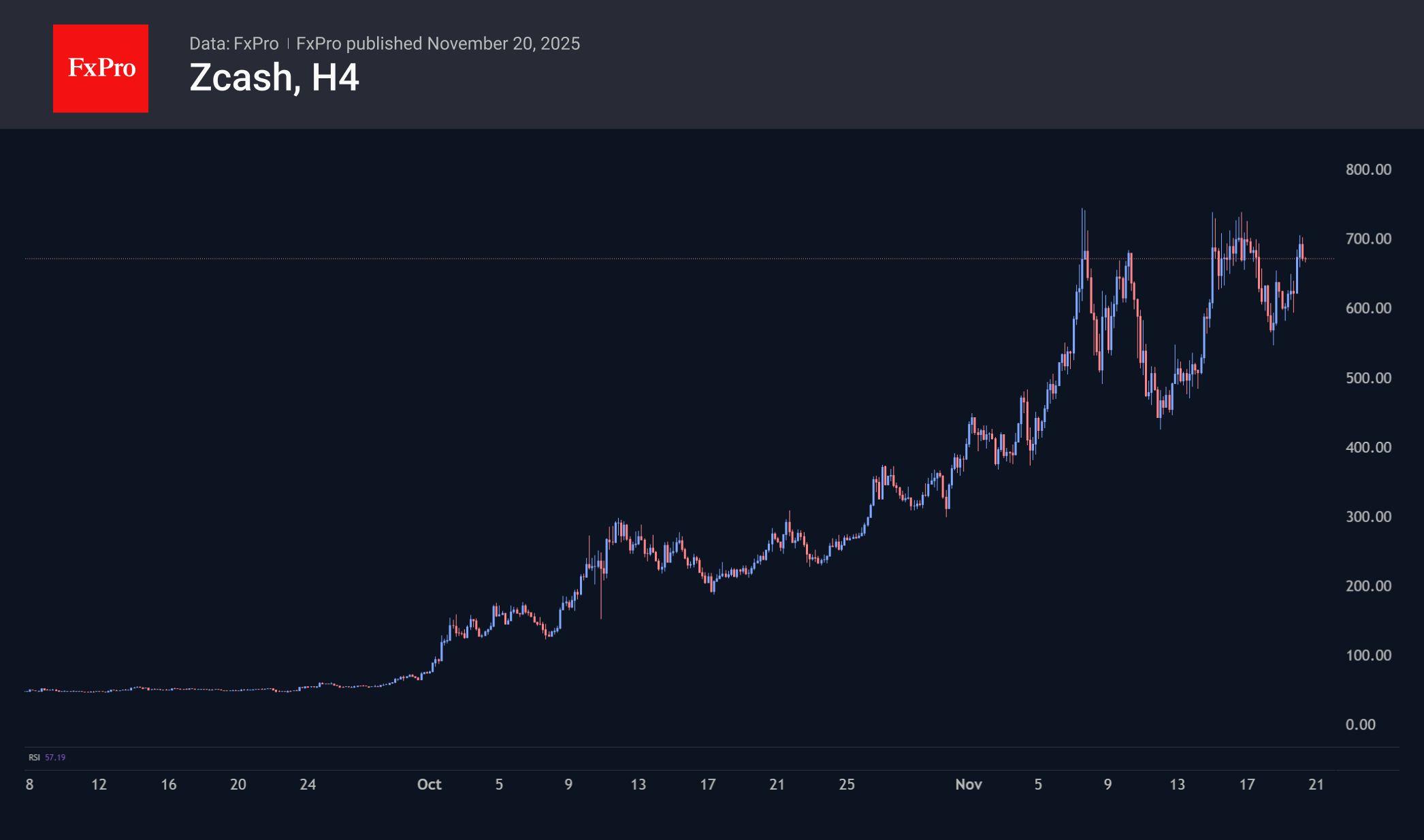

ZEC remains a standout in the crypto market. The coin quickly recovered to the multi-year highs of $700 set earlier this month. This is quite impressive, considering the retreat of Bitcoin, which affects the entire crypto market. At the same time, we are wary of this growth, given its difficult legacy, as in previous bull markets, the rise of Zcash was a harbinger of the end.

News Background

The inflow into spot Solana ETFs in the US has continued for 16 consecutive trading sessions. During this time, $420.4 million has been invested in the funds. Canary’s recently launched XRP ETF in the US is also performing well, with an inflow of $276.8 million over three trading sessions; however, the bulk of the investment occurred on the first day of trading.

On November 18th, trading commenced on Solana-based spot exchange-traded funds from Fidelity (FSOL) and Canary Capital (SOLC) on the NYSE Arca and Nasdaq exchanges, respectively. Thus, five Solana spot ETFs are now trading in the US.

Aggressive bullish bets on the Bitcoin options market have been replaced by ‘clearly bearish’ positions, reflecting investors’ concerns about the market correction continuing, notes CoinDesk analyst Omkar Godbole. Short-term put options with strikes of $84,000-80,000 prevail.

Some experts attribute the current decline in the crypto market to a liquidity shortage amid the US government shutdown, rather than fundamental factors such as outflows from ETFs or a decrease in DAT company activity.

GBP/USD Weakens Rapidly Amid Dovish Data and External Pressures

The GBP/USD pair fell sharply to 1.3048 on Thursday, pressured by a combination of soft domestic inflation data and a broadly stronger US dollar.

The pound's decline was triggered by the latest UK Consumer Price Index (CPI) report, which showed inflation slowed to 3.6% year-on-year in October, matching forecasts. This bolstered market expectations that the Bank of England (BoE) could initiate interest rate cuts as early as December. The data fits a broader narrative of weakening domestic demand: the labour market is cooling, GDP growth is undershooting the central bank's projections, and core inflation is tracking slightly below the BoE's anticipated path. In light of this, institutions, including Deutsche Bank, suggest the Monetary Policy Committee (MPC) will gain the confidence needed to lower the Bank Rate from its current 4.00% level.

Additional headwinds for sterling stemmed from a resurgent US dollar, which found support ahead of key US macroeconomic data and the highly anticipated earnings report from the AI-chip giant, Nvidia.

Globally, investor attention is also captivated by the Japanese yen, which slumped to a 10-month low after the Ministry of Finance issued a statement expressing a "high degree of caution" over the currency's movements. This phrase stopped short of threatening direct intervention.

Overall, market uncertainty is elevated. US statistical agencies are only just beginning to release the backlog of data delayed by the recent government shutdown, leaving traders to piece together the true state of the world's largest economy.

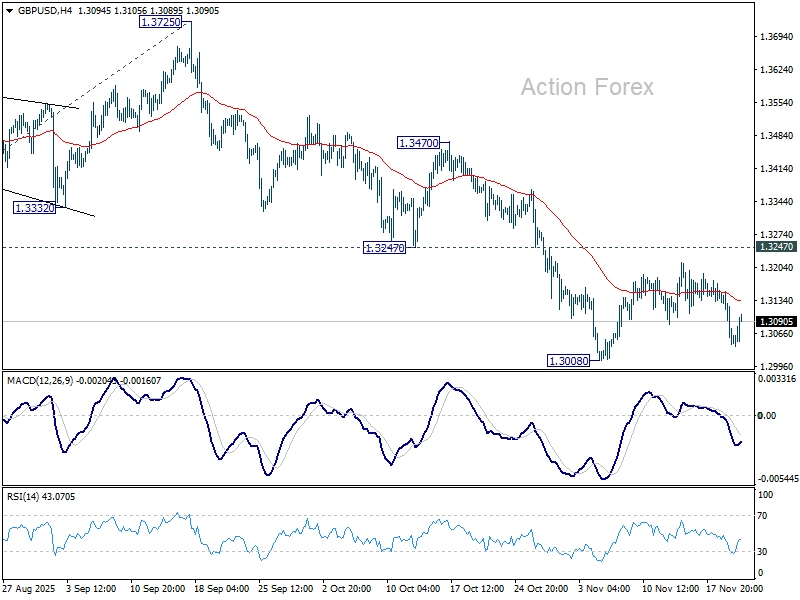

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD has completed a downward wave to 1.3037. We now anticipate a technical correction towards at least 1.3080. Following this pullback, the primary downtrend is expected to resume, driving the pair towards 1.2990, with a longer-term prospect of extending losses to 1.2915. This bearish scenario is confirmed by the MACD indicator. Its signal line is located below zero and pointing decisively downward, indicating that selling momentum remains firmly intact.

H1 Chart:

On the H1 chart, the pair broke downwards from a consolidation range around 1.3090, confirming the continuation of the bearish impulse. The immediate target for this leg is 1.3030. A corrective bounce to retest the 1.3090 level from below is likely before the next wave of selling takes the pair down to 1.2990 and potentially towards 1.2950. The Stochastic oscillator aligns with this view. Its signal line is above 50, indicating that a short-lived corrective bounce is underway before the dominant downtrend reasserts itself.

Conclusion

The GBP/USD is facing a perfect storm of domestic dovish shifts and external dollar strength. The softer inflation print has significantly increased the odds of a December BoE rate cut, eroding sterling's yield appeal. Technically, the path of least resistance remains firmly to the downside. While a short-term correction towards 1.3080 is likely, this should be viewed as a potential selling opportunity within the broader bearish trend, which has clear targets at 1.2990 and 1.2915.

USD/JPY Rises Above 157.00 for the First Time Since January

According to media reports, the Japanese government is in the final stages of preparing an economic stimulus package worth 21.3 trillion yen (USD 135.38 billion) to help households cope with persistent inflation. This could become the largest stimulus since the COVID pandemic.

The Cabinet plans to approve the package on Friday, and the supplementary budget to fund it on 28 November, aiming to secure parliamentary approval before the end of the year.

This decision has led to a significant weakening of the national currency.

Technical Analysis of the USD/JPY Chart

Fluctuations in the Japanese yen against the US dollar are forming an upward channel (shown in blue), and the fundamental backdrop this week has caused the price to:

→ break the QL line from below (and after the breakout, the rise accelerated, indicating imbalance — forming a Fair Value Gap pattern);

→ reach the median.

It is reasonable to assume that around the median, supply and demand may balance each other, stabilising the market. It is also possible that the FVG area will act as support in the event of a correction.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Tech Stocks Rally After Nvidia’s Earnings Report

As the chart shows, the Nasdaq 100 index (US Tech 100 mini on FXOpen) is displaying positive momentum today. A strong catalyst for growth arrived with the release of Nvidia’s quarterly report, which exceeded Wall Street’s optimistic expectations.

Nvidia reported quarterly revenue of $57bn (vs. the expected $54.9bn), and earnings per share of $1.30 (forecast: $1.26). Meanwhile, CEO Jensen Huang stated that demand for the new Blackwell chips is “off the charts”.

Nvidia’s strong report revived “risk appetite” in the tech sector and eased concerns about a potential AI bubble.

Technical Analysis of the Nasdaq 100 Chart

Analysing the hourly chart of the Nasdaq 100 (US Tech 100 mini on FXOpen) two days earlier, we:

→ noted that the previously active upward channel had broadened downwards;

→ suggested a scenario in which the bulls might attempt to return the index to an upward trajectory if Nvidia’s quarterly results were strong.

Yesterday’s report from the equity market leader confirmed that demand for artificial intelligence infrastructure remains enormous, paving the way for the tech-sector rally to continue.

From the standpoint of supply pressure, resistance may come from:

→ the upper red line drawn through the lower November highs;

→ the 25,400 level, which had acted as local support but was decisively broken by a large bearish candle.

On the other hand:

→ the decline towards 24,400 once again activated buying interest;

→ the November drop may prove to be only an intermediate correction, after which the upward trend could resume.

Whether the bulls can maintain positive momentum in the Nasdaq 100 (US Tech 100 mini on FXOpen) following Nvidia’s strong quarterly figures will depend largely on the outcome of the delayed September US employment report, postponed due to the shutdown.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US Eco Data Will Again Take Center Stage

Markets

The Minutes of the end October Fed meeting and Nvidia results were the main features for global trading yesterday. The latter were poised to address market concerns on a developing tech bubble causing hiccups of market volatility of late. Both sales for the previous quarter and the outlook were materially stronger than expected and CEO Jensen Huang indicated that at least his company did see ‘something very different’ from an AI bubble. US equity indices already slowed recent correction in the run-up to the (post-market) Nvidia results and US futures are firmly in positive territory this morning. (Nasdaq Future + 1.8%) setting the stage for a risk-rebound today. Of late, the (US) interest rate markets showed an indecisive trading pattern as investors grew ever more uncertainty whether the Fed would already execute a next follow-up insurance rate cut at the December 10 meeting. The minutes at least showed highly different views on policy going forward. ‘Most participants judged that further downward adjustments to the target range for the federal funds rate would likely be appropriate as the Committee moved to a more neutral policy stance over time, although several of these participants indicated that they did not necessarily view another 25 basis point reduction as likely to be appropriate at the December meeting’, the report reads. US yields moved again towards the upper part of recent short-term rage adding about 2 bps across the curve. The odds on a December rate cut declined to < 30%. German yields in technical trading mostly gained up to 1.0 bps. Even as equity sentiment improved, the dollar remained well bid, with USD/JPY taking the lead as uncertainty on sustainability of Japan fiscal policy hammered the yen. USD/JPY jumped to close north of 157. DXY (100.25) is again testing the 100.25/36resistance area. EUR/USD drifted further south in the 1.15 big figure (close 1.154). UK gilts underperformed (30-y +6.2 bps) despite a further easing of inflation in October (3.6%). Sterling slightly underperformed (close 0.8835.

This morning, Asian indices (ex-China) mostly join the Nvidia-driven rebound. Headlines (Reuters) on the Japanese government preparing a JPY 21.3 trillion fiscal stimulus package (to be released tomorrow), continue to both pressure Japanese bonds (10-y + 4.5 bps) and the yen (USD/JPY 157.7). Still, the dollar remains well bid overall (EUR/USD 1.152). Later today, for once, US eco data will again take center stage with the delayed release of the US September payrolls, which will be the only new labour market report available for the December Fed meeting. Consensus expected a 51k month job growth. It remains a bit strange for the FOMC to give a heavy weight at one outdated data release to decide on the (timing) of further easing. Even so, a softer figure (September ADP was -32k) might ease recent ‘rise’ in US yields and rebalance expectations on a December fed rate cut. In this process the dollar also nears important resistance levels (DXY 100.25/50 area, EUR/USD 1.1469 November low ) which might also have a role to play in case of a soft report.

News & Views

The Chinese government mulls additional measures to get the ailing housing sector back on its feet, Bloomberg reported citing people familiar with the matter. Options include mortgage subsidies for new homebuyers but on a nationwide level for the first time, raising income tax rebates for mortgage borrowers and lowering home transaction costs. The real estate downswing has been around for four years and shows little signs of improving. Completed investment in the sector has been declining sharply but after having appeared to find a bottom through 2024, things took another turn for the worse from Q2. Y/Y investment measures (-14.7%) are nearing the 2020 crash (and alltime) low of -16.3%. With many consumers heavily indebted, the malaise weighs on sentiment and consumption. It also raises the question whether measures aimed at stimulating even more borrowing are actually worth doing.

The French 2026 budget will probably be rejected when parliament votes on it this Sunday. PM Lecornu unlike his predecessor said he won’t circumvent parliament in pushing through the budget and insisted on having lawmaker’s backing. But that resulted in thousands of amendments of the original draft which turned it into a document policymakers now say no one can recognize themselves in. Voting it down means the government is running ever shorter on time to have it agreed on time. While France can resort to measures that roll over 2025 spending levels into 2026, it would kill off ambitions to narrow down the gaping deficit...

Nikkei 225: Bulls Back in Vogue With 4% “Takaichi Trade” Rally

Key takeaways

Nikkei 225 remains supported by macro tailwinds, including aggressive fiscal stimulus under PM Takaichi and a renewed steepening in Japan’s government bond yield curves, both historically correlated with upside in the index.

A weakening Japanese yen is attracting stronger foreign inflows, with USD/JPY at a 10-month high and foreign net purchases of Japanese equities trending higher, reinforcing bullish pressure on the Nikkei 225.

Short-term technicals lean positive, with the Japan 225 CFD Index holding above key moving averages and momentum indicators strengthening; a break above 50,730 could unlock the next leg higher towards 51,530 and 52,775/52,830.

The Japan 225 CFD Index (a proxy of the Nikkei 225 futures) has staged the expected minor bullish reversal right at the 49,370/48,450 key inflection support zone as it dropped to an intraday low of 49,099 on 5 November before it rallied by 4.9% to hit an intraday high of 51,514 on 13 November.

Thereafter, it wobbled, erased its earlier gains, and declined by 4.8% to retest the lower limit of the key inflection support at 48,450 on Tuesday, 18 November, on the backdrop of a weaker footing from the US stock market due to fears of overvaluation in Artificial Intelligence (AI)- related stocks.

Interestingly, several localized macro factors remain supportive of the ongoing short- to medium-term bullish trend of the Nikkei 225. Let’s examine them in greater detail.

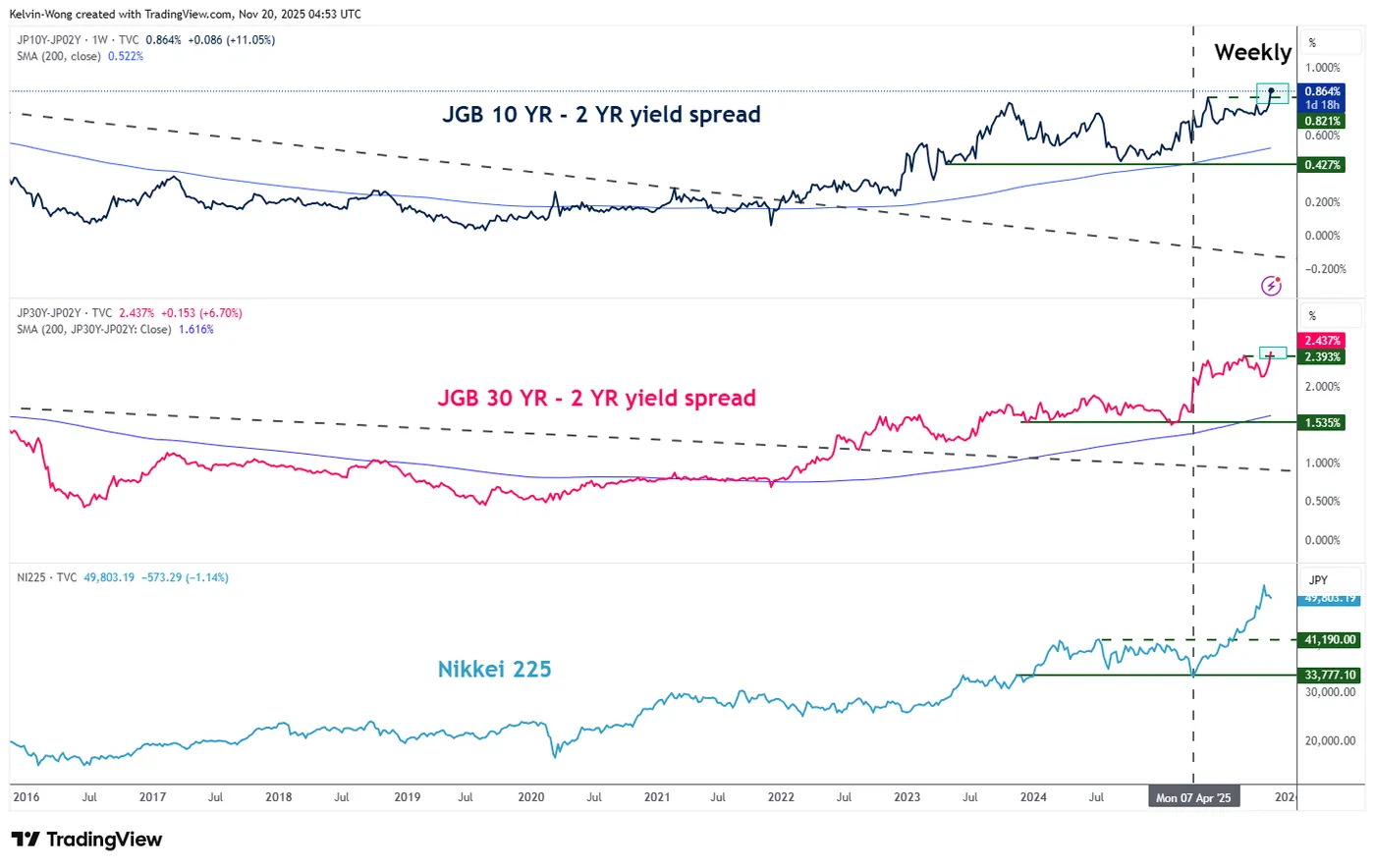

Further steepening of the JGB yield curve as it broke new highs

Fig. 1: JGGs yield curve with Nikkei 225 major trends as of 20 Nov 2025 (Source: TradingView)

The “Takaichi Trade” is backed in the front seat as market participants turn their attention to focus on the new Japanese Prime Minister Takaichi’s push on the implementation of an aggressive fiscal policy and a tilt towards lower interest rates to drive economic growth in Japan.

Takaichi’s administration is expected to unveil a new economic package in parliament this week, where the additional supplementary budget for this fiscal year is expected to be at around 20 trillion yen, far bigger than the 13.9 trillion-yen package compiled a year ago by Takaichi’s predecessor.

The higher fiscal stimulus is likely to trigger a boost to domestic consumption in Japan as early as the first quarter of 2026, in turn, causing the Japanese Government (JGB) yield curves (both the 10-year and 30-year against 2-year) to steepen further (see Fig. 1).

The 10-year/2-year JGB yield curve has broken above its prior May 2025 high of 0.82% and currently trades at 0.86%, a 13-year high.

In addition, the 30-year/2-year JGB yield curve jumped to a new record high of 2.44% at the time of writing, surpassing the September 2025 peak of 2.39%.

The major bullish breakout (steepening conditions) of the JGB yield curves (both 10-year and 30-year against the 2-year) since June 2022 has a direct correlation with the movements of the Nikkei 225.

Hence, the continuation of a further steepening of the JGB yield curves is likely to trigger another round of a positive feedback loop in the Nikkei 225.

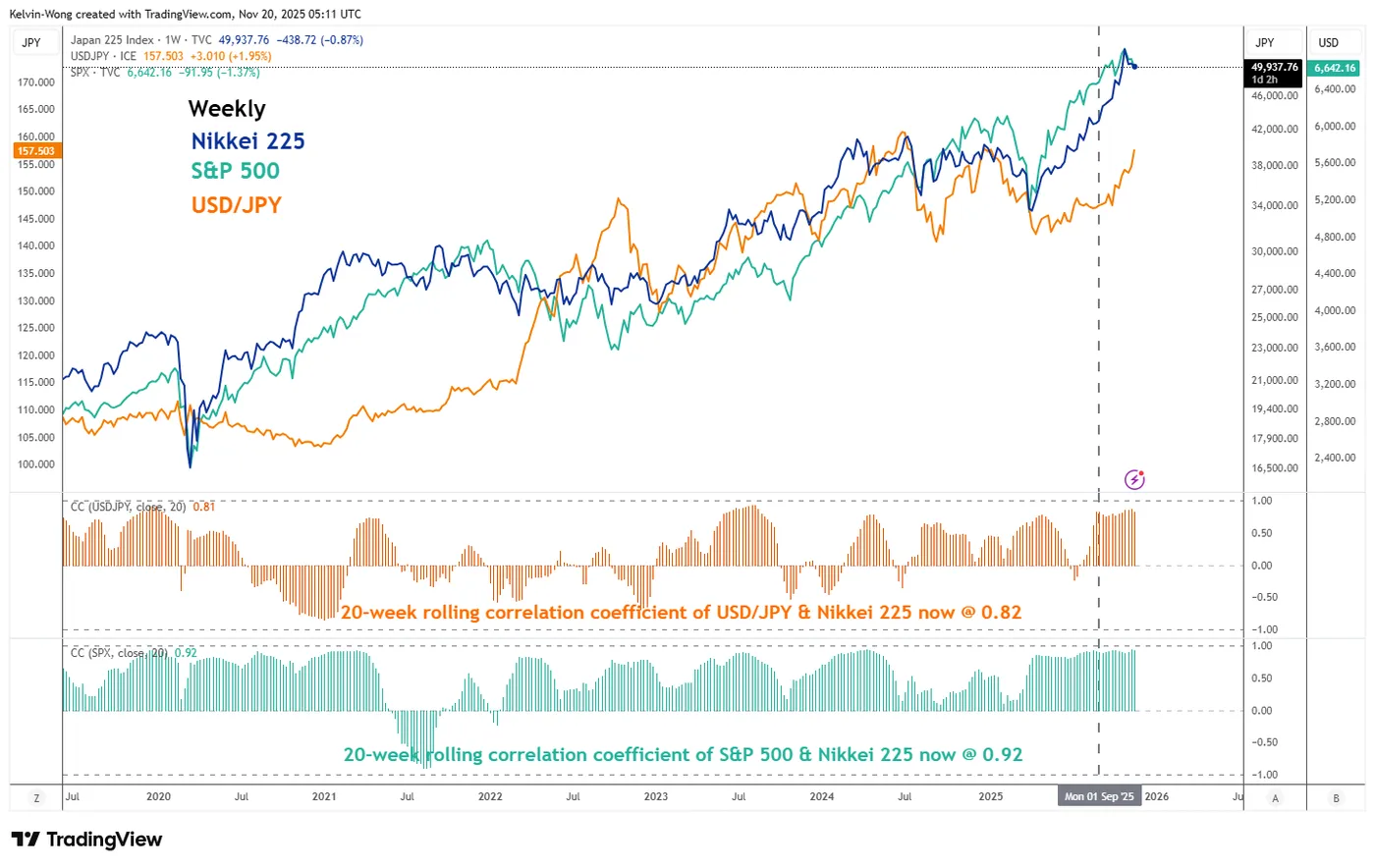

A weak JPY may attract higher foreign net inflows into Japanese equities

Fig. 2: Correlation trends of USD/JPY & S&P 500 with Nikkei 225 as of 20 Nov 2025 (Source: TradingView)

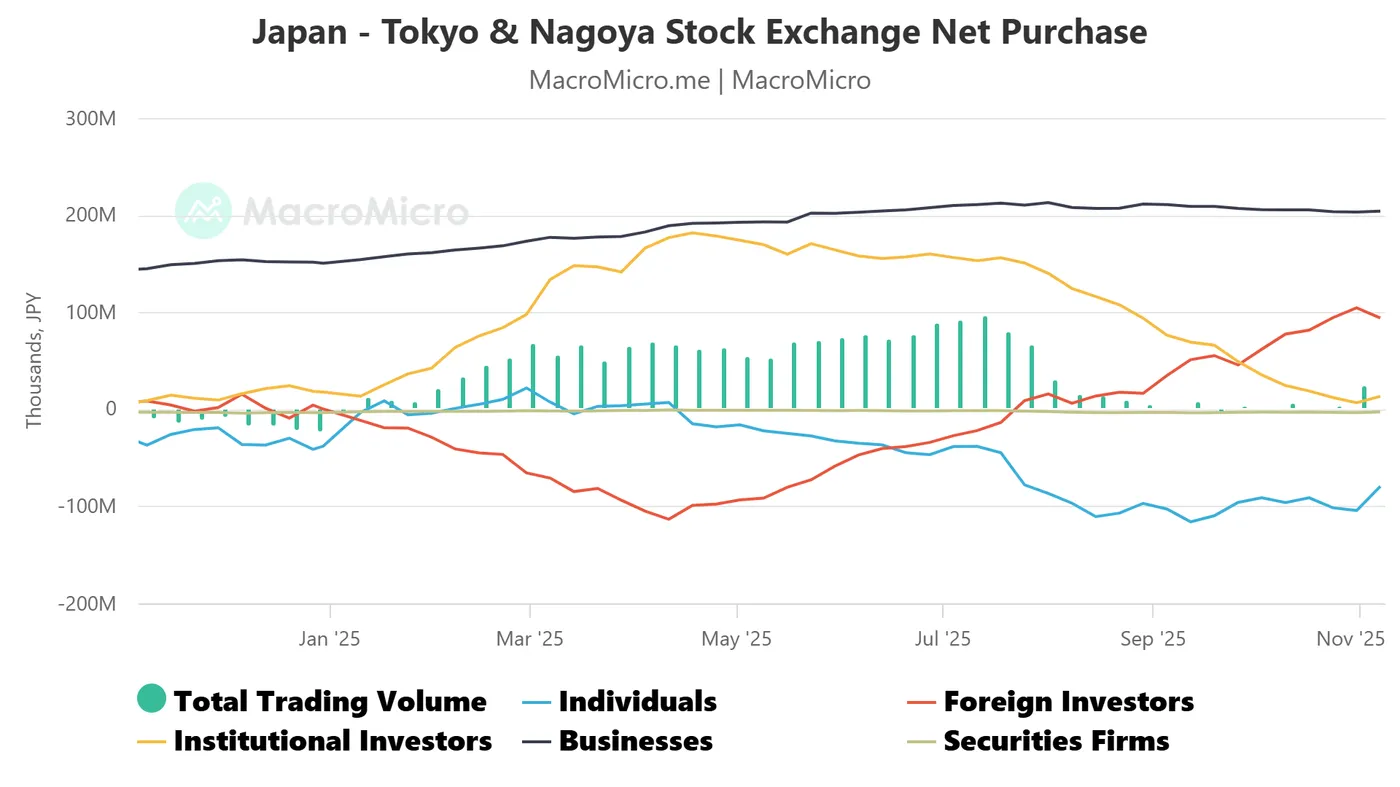

Fig. 3: Net purchases of Tokyo & Nagoya stock exchanges as of 7 Nov 2025 (Source: MacroMicro)

Another “cause and effect” from the “Takaichi Trade” is a weaker JPY, as the Bank of Japan (BoJ) is likely to face an increased risk of jawboning from the new administration in pushing back the gradual interest rate hikes advocated by BoJ’s latest monetary policy stance.

The Japanese yen has weakened significantly against the US dollar in the past month, where it shot past 154.00 “easily” to trade at a 10-month low of 157.50 per US dollar at the time of writing.

The USD/JPY has been moving in direct union with the Nikkei 225 since September 2025, where the 20-week rolling correlation coefficient of the USD/JPY with the Nikkei 225 stands at a high value of 0.82 as of 20 November 2025 (see Fig. 2).

In conjunction, the 52-week average of foreign investors’ net purchases of Japanese equities listed on the Tokyo and Nagoya stock exchanges has continued to increase from 77.44 billion in the week of 10 October 2025 to 93.98 billion for the week of 7 November 2025 (see Fig. 3).

Hence, a further weakening of the JPY may see a continuation of more foreign inflows to support the bullish trend of the Nikkei 225.

Let’s now shift to Nikkei 225’s potential share price trajectory from a short-term technical perspective, focusing on the next one to three days.

Preferred trend bias (1-3 days) – Potential bullish break above 20-day moving average

Fig. 4: Japan 225 CFD Index minor trend as of 20 Nov 2025 (Source: TradingView)

Bullish bias with 49,085 as key short-term pivotal support for the Japan 225 CFD Index (a proxy of the Nikkei 225 futures).

A clearance above 50,730 (also the 20-day moving average) reinforces the potential bullish impulsive up move sequence to see the next intermediate resistances coming in at 51,530 and 52,775/52,830 next (see Fig. 4).

Key elements

- The price action of the Japan 225 CFD Index has continued to oscillate above its 50-day moving average and a medium-term ascending channel support that has been in place since the 7 April 2025 low.

- The hourly RSI momentum indicator has continued to shape a series of “higher lows” without any bearish divergence condition at its overbought zone (above the 70 level).

- These observations suggest the medium-term uptrend phase of the Japan 225 CFD Index remains intact with a build-up in short-term bullish momentum.

Alternative trend bias (1 to 3 days)

Failure to hold at the 49,085 key short-term support negates the bullish tone on the Japan 225 CFD Index for a slide to retest the 48,450 key medium-term pivotal support.

How Long Can Nvidia’s Fuel Keep Market Engine Running?

I had no doubt that Nvidia was about to dump another set of impressive – and record-breaking – results. There was also very little doubt about its capacity to beat expectations. Indeed, Nvidia respected the fairly odd trend of beating the average revenue consensus by around $2bn by announcing $57bn in revenue – a 62% growth from the same time last year. Data-centre revenue surpassed the $50bn mark, and earnings per share came in higher than expected, as well.

But more impressively – yet perfectly consistent with his earlier comments – Jensen Huang said that “Blackwell sales are off the charts”. The company now expects revenue to grow to $65bn this quarter. That was higher than analysts expected, but still in line with Huang’s earlier claim that they have already sold around $500bn worth of Rubin and Blackwell chips for this year and next. In short, there was nothing in yesterday’s quarterly report that sounded off. Nvidia did what it has done best since 2023: it surprised to the upside.

And the bulls couldn’t resist. The share price jumped 5%. What might have made a difference in the market’s reaction is Huang saying that “we’ve entered the virtuous cycle of AI. The AI ecosystem is scaling fast – with more new foundation model makers, more AI startups, across more industries and in more countries. AI is going everywhere, doing everything, all at once.”

Translated into simpler terms: don’t worry about circularity; just look at the horizon.

So I believe it’s safe to say that Huang saved the day. Nasdaq futures are up nearly 2% as I write this morning, while Asian tech buddies are raving with joy: the Kospi is up around 2.5%, and the Japanese Topix is up around 2%. But SoftBank is having a hard time holding on to its gains: a reminder that not all clouds have dissipated. Anxiety about overinvestment in AI and concerns about AI-related debt keep ballooning – and for good reason. Bond issuance from Google, Amazon, Meta, Microsoft and Oracle has risen above the $100bn mark this year, at least 2.5 to 5 times previous years.

And while Nvidia sees revenues flowing in from big spenders, investors will still want to see the hyperscalers generate revenue from outside the AI circle. Let’s see how long Nvidia’s fuel keeps this market engine running.

Outside Nvidia, the news and expectations around the Federal Reserve (Fed) are not heading in the right direction – to say the least. One of yesterday’s biggest headlines was the BLS announcement that the October jobs report will not be released before the Fed’s December meeting – it will instead be published together with the November numbers, one week after the Fed’s verdict. The BLS says it wasn’t able to collect enough data due to the government shutdown – which is likely true – but if the delay also reflects numbers that look bad (a possibility, given the Trump-led drama around the BLS), then this certainly doesn’t serve the White House’s wish for lower rates.

The news that the BLS won’t publish the October jobs data – combined with uncertainty around when the October CPI will land – further smashed expectations of a 25bp cut from the Fed. Activity on Fed funds futures now suggests less than a 30% chance of a December cut. Ultimately, that’s not good for risk appetite as higher yields pull valuations down. And yields are rising. The US 2-year yield – which best captures Fed expectations – is consolidating above 3.60% this morning, while the 10-year sits near 4.14%.

The US dollar surged past its 200-DMA on the back of waning dovish Fed expectations and is extending gains in Asia today. And – though it will feel like a weather forecast from last month – September jobs data from the US will be worth watching. A Bloomberg consensus suggests the economy may have added 53k jobs in September, before the shutdown.

But a softer or stronger number is unlikely to reverse the “no-cut” expectation, as the FOMC minutes yesterday confirmed that “many” Fed members think it would be better to keep rates where they are in December. So expect further upside in US yields.

Speaking of yields, the sell-off in Japanese bonds continues at full speed. The 30-year JGB yield is testing 3.40% this morning, while the 10-year has hit 1.84%. Rising yields in Japan – which could encourage Japanese pension funds to repatriate funds – also pull the rug from under US Treasuries at a time when confidence and appetite for US government debt are already waning due to ballooning deficits and deteriorating US relations with the rest of the world. As Japanese yields rise, so does the risk of reverse carry trades. And I don’t need to tell you how bad a reverse carry is for global equities. It could trigger a 10–15% sell-off in the S&P 500 in a matter of weeks. This is one of the biggest risks to the year-end market rally.

Because we always want to go one step further: the vanishing yen carry trade, and the end of Japan’s era of free liquidity, could eventually be replaced by a newcomer. And that newcomer could be China.

What allowed Japan to print endless free money was its long battle against deflation. Now it’s China fighting deflation – along with an ageing population and a property crisis. And guess what: the Chinese 10-year yield has just dipped below the Japanese 10-year yield.

In other words, the world’s favourite funding currency may be quietly changing hands.

If China keeps easing while the rest of the world tightens or normalises, markets may soon discover a new source of “free liquidity”, rerouting capital flows and rewriting familiar carry-trade dynamics.

It’s early days, but the seeds of a China-funded carry era are clearly being planted — and investors are already watching for the first shoots.

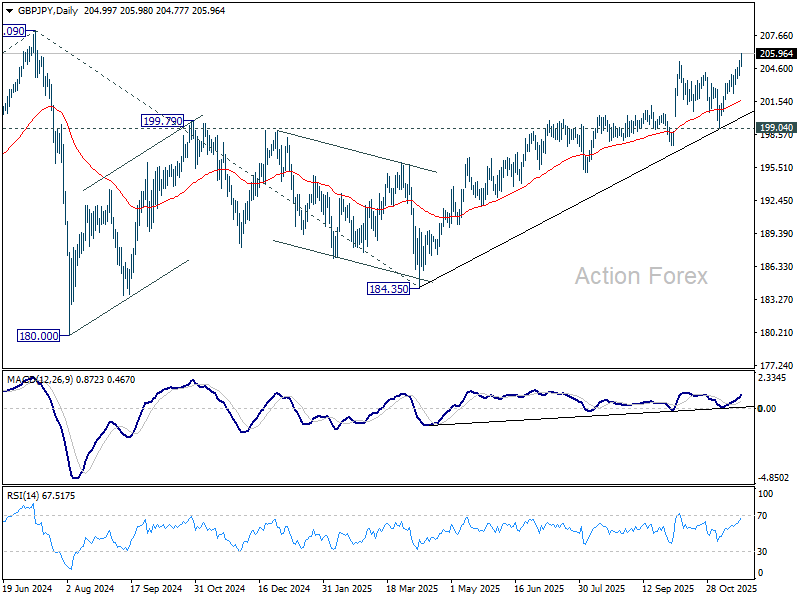

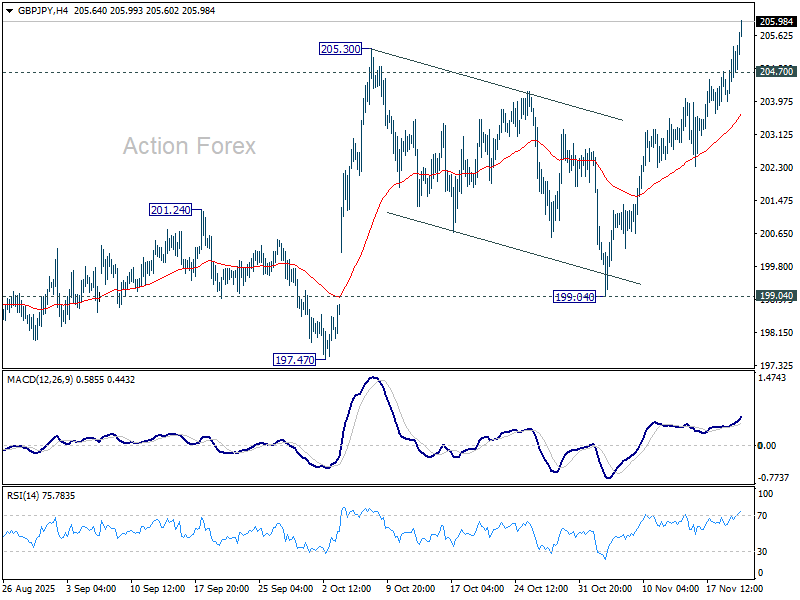

GBP/JPY Daily Outlook

Daily Pivots: (S1) 204.36; (P) 204.86; (R1) 205.75; More...

GBP/JPY's rise from 184.35 resumed by breaking through 205.30 and intraday bias stays on the upside for 208.09 high. Decisive break there will confirm long term up trend resumption. On the downside, below 204.70 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.