Sample Category Title

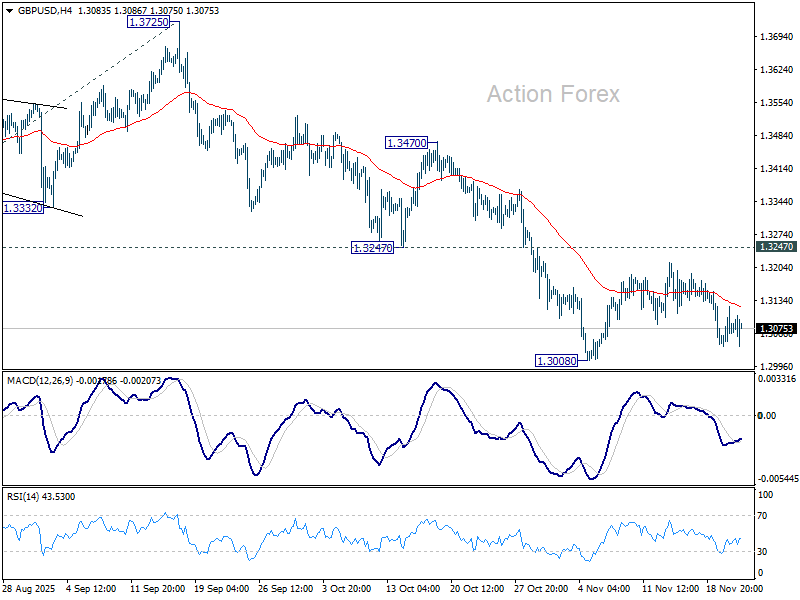

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3033; (P) 1.3078; (R1) 1.3119; More...

No change in GBP/USD's outlook and intraday bias remains neutral. With 1.3247 support turned resistance intact, further decline is expected. On the downside, firm break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, decisive break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

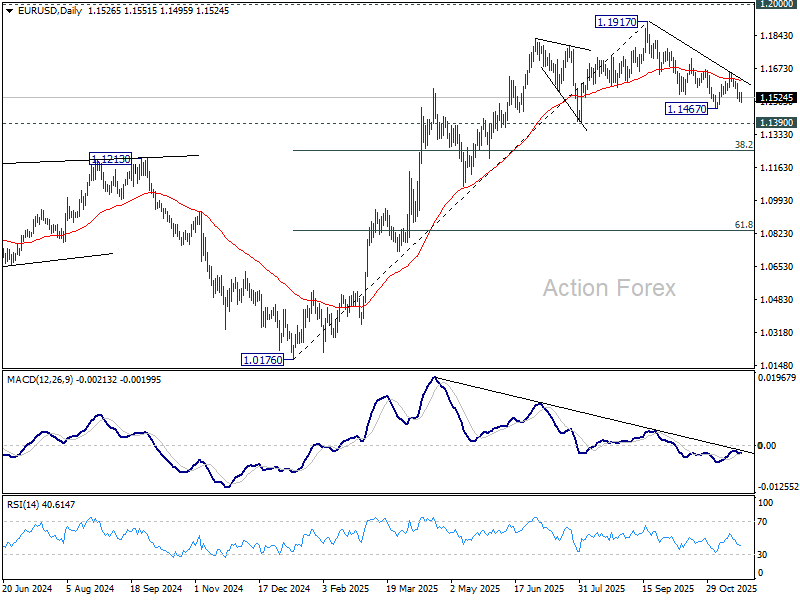

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1504; (P) 1.1527; (R1) 1.1551; More…

Intraday bias in EUR/USD remains mildly on the downside for 1.1467 first. Firm break there will target 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1551 minor resistance will turn intraday bias neutral. But risk will stay on the downside as long as 1.1655 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Williams Rekindles December Fed Cut Bets, Markets Scramble to Reprice

New York Fed President John Williams delivered the day’s biggest surprise, signaling that he sees scope for another rate cut in the near term. As head of the New York Fed — a permanent FOMC voter and a traditional bellwether for committee consensus — his comments dramatically shifted the policy conversation. Only yesterday markets were digesting a message of caution from the October FOMC minutes; today, traders are again contemplating the possibility of an imminent easing step.

Pricing in the futures market flipped almost instantly. Expectations for a December rate cut surged from 35% to about 70%, marking one of the most abrupt single-session repricings in weeks. The rapid repricing underscored not only the influence of Williams’s stance but also the market’s latent readiness to pivot back toward an easing narrative after a week of mixed signals from policymakers.

The shift in expectations also helped snap Wall Street out of its AI-driven selloff. U.S. equity futures jumped meaningfully, pointing to a strong rebound at the open. Still, whether the optimism can carry through the rest of the day is unclear. Investors may be more inclined to treat Williams’s comments as a tactical boost rather than a structural re-anchoring of the outlook.

Currency markets, however, displayed a more tempered reaction. Dollar slipped briefly after the headlines but quickly recovered. The greenback remains firmly the best performer of the week. Loonie and Sterling are currently the next strongest.

Swiss Franc has now fallen to the bottom of the performance board as the Yen — which had been hammered for days — finally showed signs of stabilization and clawed its way off the floor. Still, the fact that Aussie holds the third-weakest position signals that risk undertones remain soft, even as stock futures point higher. Kiwi and Euro continue to hover mid-table.

In Europe, at the time of writing, FSTE is down -0.09%. DAX is down -0.47%. CAC is down -0.08%. UK 10-year yield is down -0.042 at 4.547. Germany 10-year yield is down -0.026 at 2.698. Earlier in Asia, Nikkei fell -2.40%. Hong Kong HSI fell -2.38%. China Shanghai SSE fell -2.45%. Singapore Strait Times fell -0.95%. Japan 10-year JGB yield fell -0.033 to 1.788.

Fed's Williams sees room for another rate cut in the near term

New York Fed President John Williams maintained a cautiously dovish tone today, saying he continues to view U.S. monetary policy as “modestly restrictive.” With that in mind, he sees room for “a further adjustment in the near term” to bring the federal funds rate closer to neutral.

Williams reiterated his confidence that inflation will moderate as tariff effects filter through the economy without generating lasting price pressures. At the same time, he emphasized that the labor market appears to be cooling in a controlled manner.

The unemployment rate reached 4.4% in September, a level he noted was comparable to pre-pandemic norms—when the job market was healthy but “not overheated.”

Canada's retail sales fall -0.7% mom in September, flat in October

Canada’s retail sector weakened in September, with headline sales falling -0.7% mom to CAD 69.8B, in line with expectations. The decline was broad-based, with six of nine subsectors posting decreases, led primarily by motor vehicle and parts dealers. When excluding autos and gasoline, core retail sales were essentially flat. In volume terms, retail sales slid 0.8% mom, marking a clear step down in real consumption.

On a quarterly basis, nominal retail sales eked out a 0.2% gain in Q3, but volumes declined -0.3%, showing that inflation-adjusted spending continues to stagnate.

The advance estimate for October suggests no meaningful improvement, with retail sales expected to be broadly unchanged.

Eurozone PMI composite climbs to 53.1, but manufacturing still far from a turnaround

Eurozone business activity lost a little momentum in November as PMI Composite edged down from 52.5 to 52.4. Manufacturing slipped back into contraction at 49.7, down from 50.0, a five-month low. Services inched up from 53.0 to an 18-month high of 53.1.

Hamburg Commercial Bank’s Chief Economist Cyrus de la Rubia noted that manufacturing remains “marooned in a no-man’s land of directionlessness,” with soft demand showing up in yet another decline in new orders. He warned the sector is still “months, possibly even several quarters” away from a sustained turnaround, pointing to deteriorating conditions in both Germany and France. Indeed, Germany’s PMI Manufacturing fell from 49.6 to 48.4 and France dropped from 48.8 to 47.8.

By contrast, services continue to provide a much-needed buffer. Germany’s service-sector growth slowed (down from 54.6 to 62.7) but stayed comfortably positive. France returned to expansion (up from 48.0 to 50.8). With the services sector carrying far more weight in the Eurozone economy, the currency bloc is still on track for faster growth in Q4 compared with Q3.

UK PMI drops to 50.5; Sluggish growth and softer prices bolster December BoE cuts

UK flash PMIs for November delivered a broadly downbeat signal on the economic outlook. Manufacturing managed to edge back into expansion territory, rising from 49.7 to 50.2 — its highest level in 14 months. But that improvement was overshadowed by a sharp drop in services activity, with PMI Services sliding from 52.3 to 50.5, a seven-month low. As a result, Composite PMI fell notably from 52.2 to 50.5.

According to Chris Williamson of S&P Global Market Intelligence, the latest readings point to an economy that has “stalled,” with job losses accelerating and business confidence deteriorating sharply. The PMI readings are broadly consistent with zero GDP growth for November and only around 0.1% growth so far in Q4.

While part of the slowdown is being blamed on paused spending decisions ahead of the Autumn Budget, weakening confidence suggests the hesitation may “turn into a downturn” if households and firms brace for new "demand-dampening measures" .

The inflation outlook also softened meaningfully. Selling price inflation dropped to its lowest in almost five years, with goods prices falling at the fastest rate since 2016 and service-sector pricing power weakening.

Taken together, the PMI data reinforce expectations that the BoE would cut rates in December, especially if next week's Budget reinforces the pessimistic tone.

UK retail sales slump -1.1% mom in October as shoppers hold off for Black Friday

UK retail sales delivered a sharp downside shock in October, falling –1.1% mom, well below expectations of a modest 0.1% increase. It was the first monthly decline since May and reflected broad weakness across supermarkets, clothing, and online retailers.

Some retailers suggested that consumers deliberately postponed purchases in anticipation of Black Friday promotions, magnifying the pullback at a time when household budgets remain stretched by high interest rates and inflation.

Despite the poor monthly reading, retail sales in the three months to October were still up 1.1% compared with the prior three-month period.

BoJ's Ueda flags bigger FX pass-through to underlying inflation

BoJ Governor Kazuo Ueda told parliament today that Yen weakness is increasingly feeding into domestic inflation. He noted that as companies have become "more active in raising prices and wages," the pass-through from higher import costs to consumer inflation has intensified. That dynamic raises the risk that currency-driven price gains could influence inflation expectations and “underlying inflation,” he warned.

Ueda added that the central bank will assess a rate hike at upcoming meetings, with the focus firmly on data that sheds light on next year’s wage momentum. He emphasized said policymakers want to "spend a bit more time to confirm whether firms' active wage-setting behavior won't be disrupted,"

He added that the Bank is still gathering information from its nationwide branches and intends to incorporate both official data and its own surveys into the next policy discussions.

Japan CPI core accelerates again to 3% in October

Japan’s October CPI data showed inflation firming again, with core CPI (ex-fresh food) rising to 3.0% yoy from 2.9%, matching expectations and marking the second month of renewed acceleration. The measure has now stayed above the BoJ’s 2% target for more than three and a half years, highlighting how persistent the price backdrop has become.

Core-core CPI, which excludes both fresh food and energy, edged up from 3.0% to 3.1% yoy, while headline CPI rose from 2.9% to 3.0%.

Food excluding fresh items surged 7.2%, and utilities rose 2.2%, confirming that household-facing inflation pressures remain elevated. Rice inflation, however, continues to ease sharply, slipping to 40.2% from September’s 49.2% and offering slight relief after months of extreme gains.

Japan PMI composite rises to 52.0 as services lead and manufacturing stabilizes

Japan’s November flash PMIs offered a cautiously constructive signal for the economy, with the Composite Index rising from 51.5 to 52.0 — the best reading in three months and joint-highest since August 2024. Manufacturing activity remained in contraction but improved to 48.8 from 48.2. Services held steady at a solid 53.1.

S&P Global’s Annabel Fiddes noted that the decline in manufacturing output eased to its slowest pace since August, hinting at a gradual move toward stabilization. Business confidence also strengthened, reaching its highest level since January. That pickup in sentiment helped drive the strongest rise in employment since June, as firms look to expand capacity in anticipation of firmer activity ahead.

Inflation pressures remain a lingering concern. Input costs rose at the fastest rate in six months amid higher labor expenses and supplier price increases. In response, firms lifted selling prices at a solid pace to protect margins.

Australia's PMI composite rises to 52.6, firmer growth with manufacturing rebounds

Australia’s November flash PMIs delivered a surprisingly upbeat signal, with manufacturing jumping back into expansion at 51.6 after October’s soft 49.7. Services PMI also nudged higher from 52.5 to 52.7, lifting Composite Index from 52.1 to 52.6. The rebound in manufacturing is particularly encouraging given the sector’s recent weakness.

S&P Global’s Jingyi Pan noted that new orders in goods returned to expansion for the first time since August, helping lift overall momentum. Rising business optimism—now at a five-month high—also points to firmer activity ahead.

Price pressures, while slightly firmer than at the start of the quarter, remain "broadly muted". Employment growth slowed, but survey responses indicate this was driven partly by "hiring challenges" rather than a sharp loss in demand, particularly in the services sector.

NZ sees strong EU export growth, yet trade balance hit by China import surge

New Zealand’s October trade report showed exports and imports both rising solidly from a year earlier, yet leaving the country with a monthly deficit of NZD -1.5B. Goods exports climbed 16% yoy to NZD 6.5B, driven by broad-based strength across key markets. However, imports grew nearly as fast—up 11% to NZD 8.0B—as demand for overseas goods remained firm, particularly from China.

Export performance was strong across most major destinations. Shipments to China rose 18% yoy, while exports to Australia increased 14%. Notably, exports to the EU surged 40%—a standout gain that helped offset softer growth in other regions. The U.S. and Japan also saw moderate increases of 5.4% and 7.5% respectively.

On the import side, the story was more uneven. Imports from China surged 29% yoy and those from Australia rose 6.8%, pushing the total higher even as purchases from several other partners fell. The U.S. and South Korea both saw sizeable declines in imports, down -15% and -19% respectively, while the EU recorded a small drop of -2.6%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1504; (P) 1.1527; (R1) 1.1551; More…

Intraday bias in EUR/USD remains mildly on the downside for 1.1467 first. Firm break there will target 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1551 minor resistance will turn intraday bias neutral. But risk will stay on the downside as long as 1.1655 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Canada’s retail sales fall -0.7% mom in September, flat in October

Canada’s retail sector weakened in September, with headline sales falling -0.7% mom to CAD 69.8B, in line with expectations. The decline was broad-based, with six of nine subsectors posting decreases, led primarily by motor vehicle and parts dealers. When excluding autos and gasoline, core retail sales were essentially flat. In volume terms, retail sales slid 0.8% mom, marking a clear step down in real consumption.

On a quarterly basis, nominal retail sales eked out a 0.2% gain in Q3, but volumes declined -0.3%, showing that inflation-adjusted spending continues to stagnate.

The advance estimate for October suggests no meaningful improvement, with retail sales expected to be broadly unchanged.

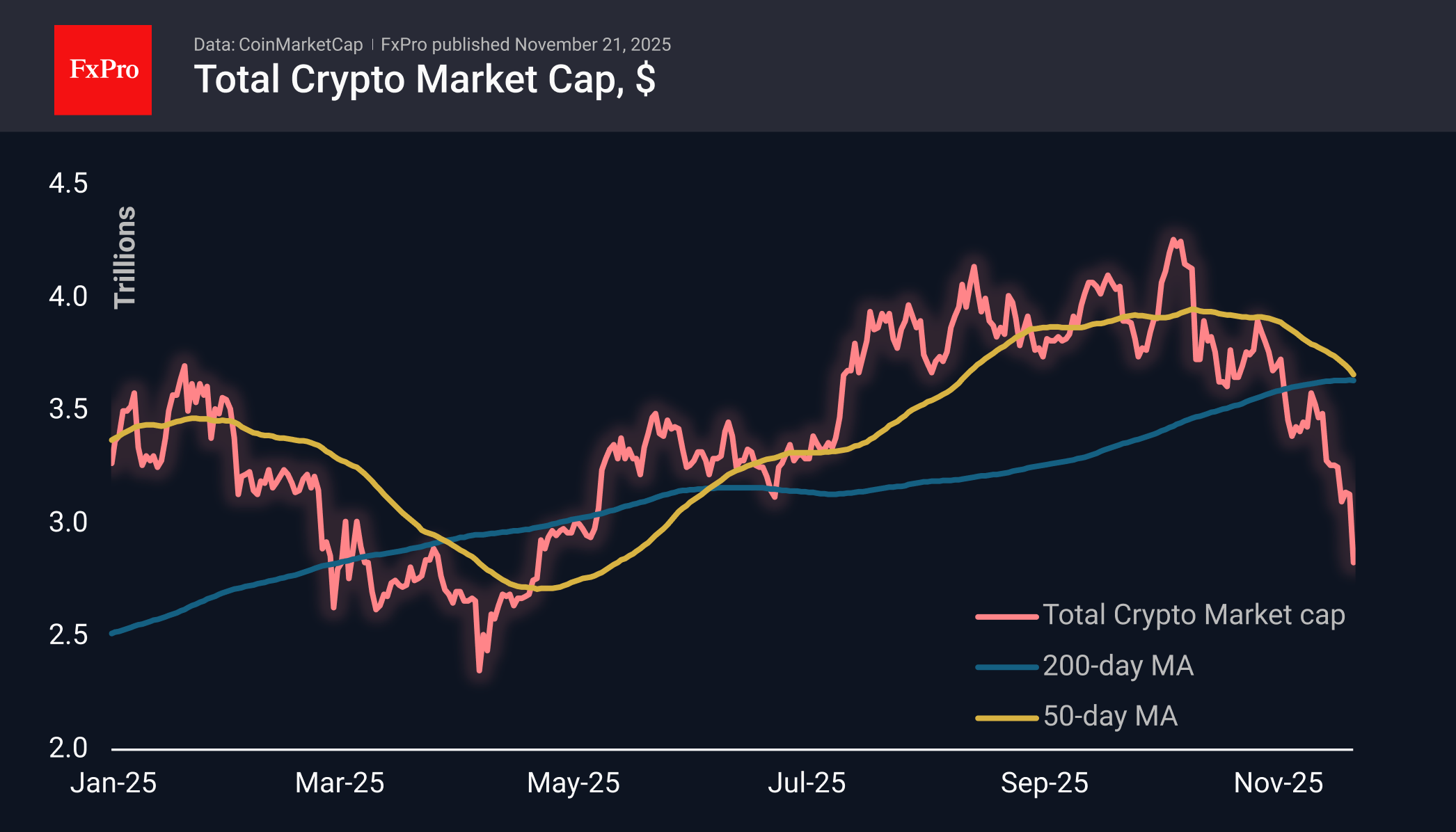

Margin Calls in Crypto, But This is Unlikely to be the Bottom

Market Overview

The crypto market capitalisation plummeted by more than 9% to $2.82 trillion, reaching its lowest level since the end of April. This already appears to be a real liquidation of margin positions. The following technically necessary support line seems to be the $2.4 trillion area. The market found support here in early April 2025 and consolidated around it throughout April 2024.

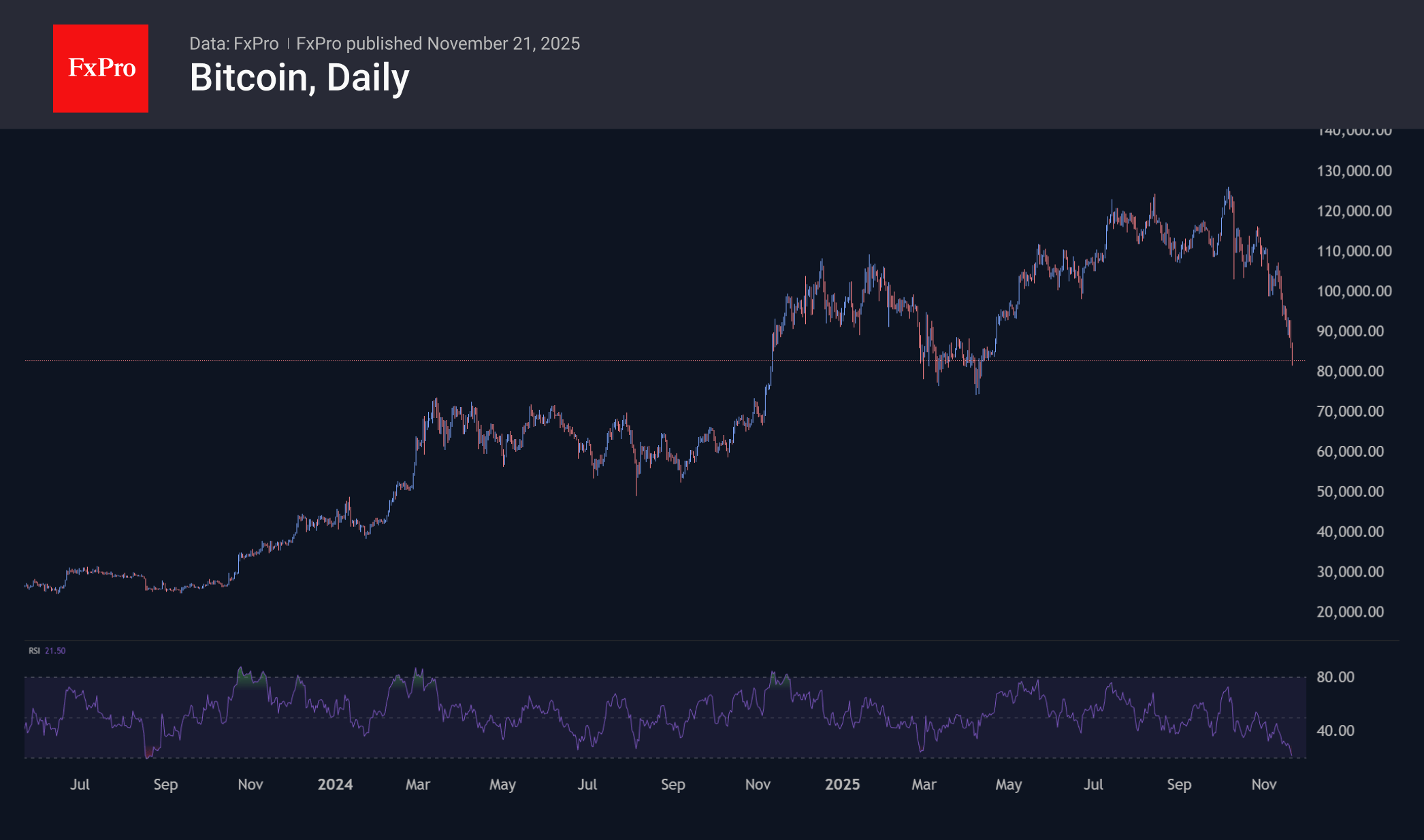

Bitcoin is trading below $83K, and at its lowest point fell to $81K, starting the day at $88K. The timing and scale of the dynamics suggest a wave of margin calls in the early hours of Friday, with an attempt at stabilisation during the European session. The price of Bitcoin has returned to the stabilisation levels seen from late February to mid-April. The RSI index on the daily charts has fallen to 20, where it last stood before the massive rally in August 2023. Touching this level in mid-2022 was not far from the price’s bottom (10% higher), but the reversal then took 6 months to materialise.

News Background

CryptoQuant indicates that market conditions for BTC have become the most bearish since the start of the bull cycle in January 2023. A break below the average investor entry price of $82,000 would be the first serious confirmation of a bearish trend since May 2022.

Bitcoin could fall to the $60,000-80,000 range and remain there until the end of the year if the Fed refuses to cut its key rate on 10 December, XWIN Research warns. Currently, the market estimates the probability of it remaining at its current level at 58%. On the other hand, crypto exchanges have accumulated record reserves of stablecoins worth $72 billion.

The unprecedented pace of Ethereum accumulation by institutional investors poses fundamental threats to Ethereum, said ETH co-founder Vitalik Buterin. Currently, nine Wall Street giants, including BlackRock, as well as several dozen DAT companies, have accumulated 10.4% of the total supply of the leading altcoin.

The launch of BlackRock’s staking-enabled Ethereum ETF poses a threat to the business model of DAT companies, such as BitMine, which accumulate cryptocurrency, according to 10x Research. Investors cannot exit such structures without significant losses.

Cryptocurrency-backed lending reached $73.6 billion at the end of the third quarter, surpassing the previous record set in 2021, according to Galaxy Research.

USD/JPY: Eases on Verbal Intervention

USD/JPY eased from new ten-month high on Friday after the latest comments from top Japanese officials boosted expectations for intervention, as yen weakened significantly in past couple of weeks and came closer to the levels where the central bank last intervened.

Overbought daily studies also contributed to profit-taking, though pullback is unlikely to be deep (as long as prevailing market expectations that direct intervention will not occur while the pair stay below 160, remain in play).

The dollar remains firm in post-NFP time, on growing hopes that the Fed will keep interest rates on hold in the next meeting that supports the notion.

The price still holds well above first Fibo support at 155.88 (23.6% of 149.37/157.89) with deeper drop to face rising 10DMA (155.42) and expected to find firm ground above broken upper boundary of bull-channel (154.76) and Fibo 38.2% (154.63).

The pair is on track for strong weekly gain, although developing upper shadow on weekly candle warns that bulls might be losing steam, but larger bulls still hold grip and favor scenario of fresh push higher after limited correction, as there is still space until 160 level (possible trigger for intervention).

Res: 157.53; 157.89; 158.20; 158.87.

Sup: 156.44; 155.88; 154.76; 154.63.

Fed’s Williams sees room for another rate cut in the near term

New York Fed President John Williams maintained a cautiously dovish tone today, saying he continues to view U.S. monetary policy as “modestly restrictive.” With that in mind, he sees room for “a further adjustment in the near term” to bring the federal funds rate closer to neutral.

Williams reiterated his confidence that inflation will moderate as tariff effects filter through the economy without generating lasting price pressures. At the same time, he emphasized that the labor market appears to be cooling in a controlled manner.

The unemployment rate reached 4.4% in September, a level he noted was comparable to pre-pandemic norms—when the job market was healthy but “not overheated.”

XBR/USD Chart Analysis: Brent Crude Falls to Monthly Low

As the XBR/USD chart shows, today (Friday) Brent crude has dropped below $62, after rising above $64.50 as recently as Tuesday. This represents a decline of over 4% from the week’s high.

This sharp bearish movement is driven by an easing of geopolitical risks and hopes for an end to the conflict in Ukraine.

Media outlets are circulating insider reports and rumours of secret coordination between the Trump administration and Moscow on a ceasefire plan. The fall in oil prices suggests that the risk premium, which reflected fears of escalation and supply disruptions, is now being replaced by a scenario of conflict resolution, potentially including a relaxation of sanctions on Russia.

Bearish pressure is also supported by news of:

→ weakness in China’s economy, the world’s largest oil consumer;

→ rising oil inventories in US storage facilities.

Technical Analysis of XBR/USD

Since late October, oil prices have been forming a downward channel. Signs of aggressive selling include (as indicated by the arrows):

1→ a sharp drop without retracements during yesterday’s trading session;

2→ a breach of the $62.60 support level with a bearish gap.

In this context, it is reasonable to suggest that:

→ Brent crude could move towards the lower half of the channel;

→ the channel’s median may act as resistance.

Furthermore, if fundamental indicators confirm progress towards ending the war in Ukraine, the downward trend may continue. This does not rule out a scenario in which Brent tests the lower boundary of the channel, around the psychological $60 per barrel mark.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Nasdaq 100: 8% Sell-Off Damages Medium-Term Uptrend, Potential Multi-Week Corrective Decline Ahead

Key takeaways

- US equities suffered a sharp reversal, with major indices wiping out strong intraday gains and closing deeply in the red, marking the sharpest swing since April’s tariff shock.

- Nvidia’s failed post-earnings rally was the main catalyst, reversing from a 5% intraday surge to a 3.2% loss and erasing nearly $400 billion in market cap, triggering negative reflexivity across the Nasdaq 100.

- Technical conditions point to growing downside risk, with Nasdaq 100 market breadth deteriorating and Nvidia’s bearish setup threatening to drag the index into a deeper medium-term downtrend.

The US stock market delivered a dramatic reversal on Thursday, 20 November 2025, its sharpest swing since April’s “Liberation Day” reciprocal tariffs shock.

Bearish movements were observed in the S&P 500 and Nasdaq 100, where both initially rose by 2% and 2.4%, respectively, before all gains were wiped out, ending the US session with losses of 1.6% and 2.4%, respectively. The Dow Jones Industrial Average (-0.8%) and small-cap Russell 2000 (-1.8%) were not spared from the rout.

The main bearish trigger was the evaporation of the Artificial Intelligence (AI) bellwether, Nvidia’s ex-post earnings share price gains, where it rallied by 5% intraday before a wave of relentless selling took place at mid-US session yesterday. Nvidia ended Thursday’s US session with a loss of 3.2%, wiping out almost $400 billion in market capitalization from its intraday high.

Let’s now focus on the latest technical elements to decipher the medium-term trend (1 to 3 weeks) trajectory of the Nasdaq 100.

Nvidia’s bearish reversal may trigger further negative reflexivity feedback loop

Fig. 1: Nvidia medium-term trend as of 20 Nov 2025 (Source: TradingView)

Fig. 2: Nvidia’s ex-post Q4 2024 earnings results price actions on 26 February 2025 (Source: TradingView)

Nvidia, being the AI juggernaut and the world’s most valuable company in terms of market capitalization, will have a significant impact on the movement of the Nasdaq 100 and the entire global equities universe via the sentiment feedback loop effect.

Even though the current price actions of Nvidia are still holding at the 177.70 key medium-term pivotal support, the ex-post earnings price reaction has shaped a daily “Bearish Engulfing” candlestick (a long body that has a wide trading range and closed near its session low), which suggests that the 177.70 key medium-term support is vulnerable to a bearish breakdown (see Fig.1)

Also, based on the prior Q4 2024 earnings release on 26 February 2025, Nvidia has shaped a similar daily “Bearish Engulfing” candlestick pattern that led to a price decline of 31% in the next 26 days (see Fig. 2).

Hence, Nvidia now faces a technical deterioration that is likely to trigger further weakness in the Nasdaq 100.

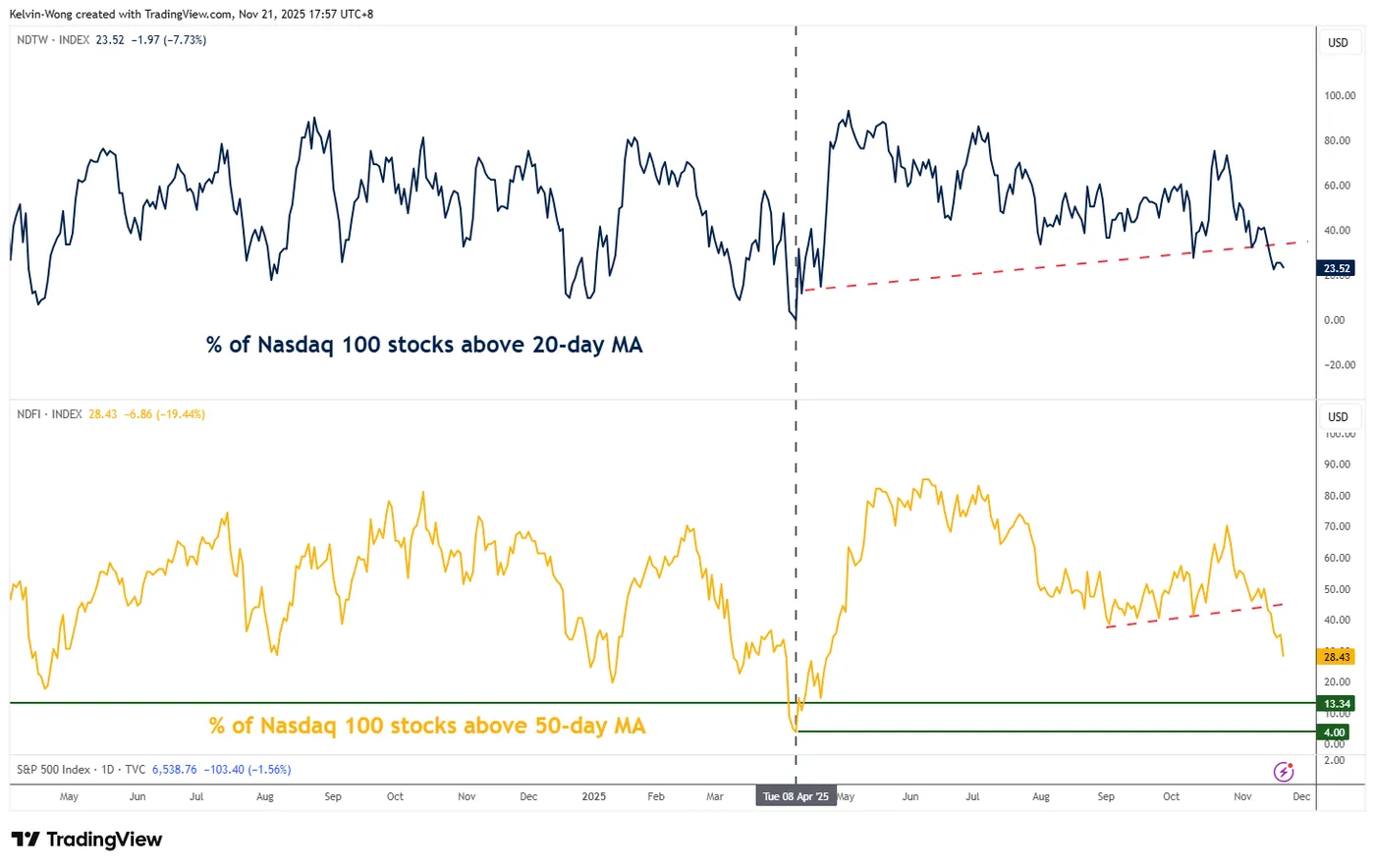

Bearish market breadth in the Nasdaq 100

Fig. 3: Percentage of Nasdaq 100 component stocks trading above 50-day & 200-day moving averages as of 20 Nov 2025 (Source: TradingView)

The Nasdaq 100 remains above its 200-day moving average, which continues to serve as a key long-term pivotal support at 22,250.

However, market breadth has weakened sharply. The share of Nasdaq 100 constituents trading above their 200-day moving averages plunged from 50% on 12 November 2025 to just 28% by Thursday, 20 November 2025 (see Fig. 3).

It has not reached the “bullish capitulation” zone of 13%/4% which suggests the Nasdaq 100 may have further room to decline at this juncture.

Preferred trend bias (1-3 weeks) – Start of medium-term downtrend

Fig. 4: US Nasdaq 100 CFD Index medium-term trend as of 21 Nov 2025 (Source: TradingView)

The price actions of the Nasdaq 100 CFD Index (a proxy of the Nasdaq 100 futures) have dropped by around 8% from its current all-time high of 26,288 printed on 30 October 2025.

Failure to hold above the 50-day moving average after a reintegration above it on Thursday, 20 November 2025, on an intraday basis invalidates a bullish reversal scenario.

In addition, the 4-hour MACD trend indicator has continued to trend downwards steadily below its centreline, which reinforces a medium-term downtrend phase.

Watch the 25,290 key medium-term pivotal resistance (also the 20-day moving average) for another leg of potential bearish impulsive down move sequence to expose the next medium-term supports at 23,455 and 22,990 (also 38.2% Fibonacci retracement of the up move from 22 April 2025 low to the current all-time high of 30 October 2025).

A break below 22,900 may see a further decline to test the 22,250 key long-term pivotal support (also the 200-day moving average) (see Fig. 4).

Alternative trend bias (1 to 3 weeks)

A clearance above 25,290 key resistance negates the bearish tone to see a potential push up to retest 25,745. Only a breakout with a daily close above 25,745 kickstarts a potential brand new bullish impulsive up move sequence towards the current all-time high of 26,288, followed by the next medium-term resistance at 26,480/26,545.

Euro Area Business Activity Remains Solid as EUR/USD Hovers Near Key Levels

Provisional PMI data for November shows that business activity in the eurozone is still growing strongly, and companies are feeling optimistic about the upcoming year.

However, there are some mixed signals: the growth of new orders has slowed down, and businesses stopped hiring new workers after a brief increase in October.

Financially, companies are facing higher expenses. Their operating costs rose at the fastest speed in eight months, largely due to higher prices in manufacturing. Despite these rising costs, businesses only raised their own prices slightly, the smallest increase for customers in over a year.

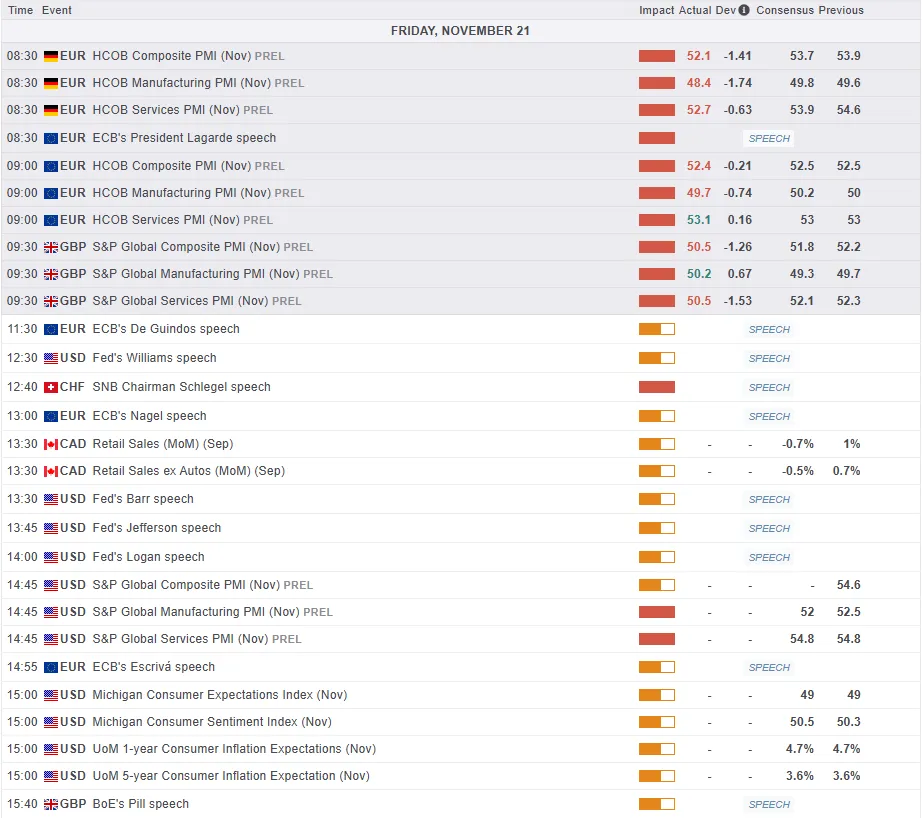

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

The eurozone economy continued to show solid growth in November, although the momentum remains uneven across sectors.

Overall Activity: The Composite PMI Output Index posted at 52.4, signaling a solid monthly rise in business activity, marking the 11th consecutive month of growth. This rate of expansion is among the sharpest seen in the last two and a half years.

Sector Divide: Growth was driven almost entirely by the service sector, which expanded at its fastest pace in a year and a half. In contrast, manufacturing production increased only slightly, tying for the slowest rate in the current nine-month growth sequence.

New Orders: While new orders rose for the fourth month in a row, the rate of growth slowed down. This was largely due to weak international demand, as export orders (including trade within the eurozone) decreased again.

On the inflation front, input costs rose at the fastest rate since March, but output price inflation eased to its lowest level in just over a year. Business sentiment edged higher in November, signaling improving confidence despite softer demand indicators.

Euro Area Q3 Negotiated Wages

The European Central Bank's survey of negotiated wages for the third quarter came in well below expectations with a print of 1.87% YoY vs estimates of 2.45%. The ECB and market participants had been hoping for a better number which would have shown that real wages are rising which would lead to solid demand in 2026.

This will now be something the ECB will monitor moving forward and lines up with some of the concerns around demand raised by the PMI data.

Technical Analysis - EUR/USD

Looking at EUR/USD from a technical standpoint, the pair appears on course to print a fresh lower low.

EUR/USD has largely been driven by US Dollar developments of late and the one concern may hinge on the price action of the US Dollar Index.

The Dollar index has peaked above the psychological 100.00 mark but has printed what looks like a double top pattern.

If the Dollar index begins to drop this could scupper the move for EUR/USD to print a fresh lower low and EUR/USD coil revisit the recent swing high at 1.1650.

EUR/USD Daily Chart, November 21, 2025

Source:TradingView.com

Support

- 1.1500

- 1.1450 (key pivot level)

- 1.1405 (200-day MA)

Resistance

- 1.1585

- 1.1650

- 1.1700

Looking Ahead

Later in the day we have several central bank officials are scheduled to speak today, most notably ECB President Christine Lagarde at a conference in Frankfurt. Since the event focuses on the benefits of investing in Europe, Lagarde may discuss the idea of strengthening the Euro's role on the world stage. Recent reports suggest the ECB is considering a plan to let central banks outside the eurozone access Euros more easily.

This strategy is designed to make countries more comfortable using the Euro for international trade, similar to a method China has used for its currency and to boost the Euro's global standing.